The Venture Debt Trap in Pharmaceutical Royalty Transactions: How Liens, Covenants and Capital Stack Order Reshape Deal Outcomes

When Geron Corporation announced its $375 million package of synthetic royalty and senior secured debt financings in November 2024, a quiet but consequential transaction sat at the centre of the structure.

Geron used a portion of the new proceeds to fully repay $86.5 million owed under its existing loan agreement with Hercules Capital and Silicon Valley Bank. The Hercules facility was terminated. The UCC-1 was released.

This was not an accident of timing. It was a deliberate sequencing decision that recognised an uncomfortable structural reality: a venture debt lender's first-priority lien and intellectual property negative pledge are largely incompatible with the structural protections that pharmaceutical royalty buyers now demand as standard.

The venture debt had to go before the royalty deal could close cleanly.

The interaction between venture debt and royalty financing has become one of the more consequential structural questions in life sciences capital markets. Both forms of financing are growing rapidly. Venture debt deal volume reached $53.3 billion globally in 2024, nearly double the 2023 figure. Pharmaceutical royalty transactions exceeded $32 billion across 2020 to 2025, according to Gibson Dunn's market analysis.

The two asset classes increasingly compete for the same collateral pool, the same intellectual property, and the same pre-revenue or early-commercial cash flows.

Where they overlap on a single company's balance sheet, the order in which they were executed and the structural choices made at inception determine what each holder recovers when stress arrives.

This article examines how venture debt operates structurally, how its lien architecture and covenant package create downstream consequences for royalty buyers, and how recent cases from 2024 to 2026 illustrate the three pathways biotech borrowers use to navigate the collision.

What Venture Debt Actually Is, Structurally

Venture debt is a senior secured credit facility extended to venture-backed companies that have completed at least one institutional equity round, typically Series B or later, but have not yet generated sufficient cash flows to qualify for traditional bank lending.

The product sits between equity and conventional corporate credit. Foley Hoag's primer and Cooley's term sheet guide describe the standard architecture.

The economics

The economic terms typically include:

- Interest at SOFR plus 600 to 900 basis points

- Three to four-year terms, with a 12 to 18-month interest-only period

- Warrant coverage of 0.5 to 1.5% of the company's equity

- An end-of-term fee of 3 to 6%

- Prepayment penalties scaled to the timing of the prepayment

For biotech borrowers, interest rates ranged from approximately 8% to 15% in 2024 and 2025, with floating-rate structures predominating.

The structural mechanics

The structural mechanics are more consequential than the economics.

Venture lenders almost universally require a first-priority lien on substantially all company assets, perfected through UCC-1 filings in each relevant state. The collateral pool typically includes accounts receivable, inventory, equipment, deposit accounts, equity in subsidiaries, and general intangibles.

Intellectual property is treated separately. Some venture lenders take an outright lien on patents, trademarks and copyrights through filings with the USPTO and Copyright Office. Others accept a negative pledge on IP, which prohibits the borrower from granting a security interest in the IP to any other lender without consent.

The negative pledge does not create a lien itself. It blocks the borrower from creating one in favour of anyone else.

For a subsequent royalty buyer that wants a backup security interest in the underlying patents, an existing IP negative pledge is a hard barrier. It requires either consent from the venture lender or refinancing of the venture debt before the royalty transaction can close.

The Covenant Package: Where Operational Control Lives

The lien structure is one half of venture debt's structural footprint. The covenant package is the other.

A typical biotech venture debt facility includes affirmative covenants requiring monthly or quarterly financial reporting, maintenance of insurance, and continued compliance with material agreements.

The negative covenants are more consequential. They typically prohibit:

- Incurrence of additional secured indebtedness without lender consent

- Granting of liens outside a defined permitted-liens basket

- Restricted payments such as dividends or share buybacks

- Fundamental transactions including mergers and asset sales above defined thresholds

- Material changes in business

Financial covenants vary by lender and stage

The most common are minimum cash balance covenants, requiring the borrower to maintain a defined floor of unrestricted cash. Burn rate ceilings and revenue floors appear in commercial-stage facilities.

According to a Q1 2026 debt advisory survey cited by Fynqo, approximately 45% of debt funds now require minimum cash-on-hand headroom of 35% of the total facility, up from 15 to 20% in earlier cycles.

The MAC clause

The "material adverse change" or MAC clause sits at the apex of the covenant package and is also its most subjective trigger.

A MAC clause permits the lender to declare an event of default if, in the lender's judgment, the borrower's financial condition or business prospects have materially worsened. Because the determination is largely discretionary, the MAC clause creates a tail risk that the borrower cannot fully model.

Investor abandonment clauses operate similarly: if existing equity sponsors decline to participate in a follow-on financing, the lender may declare default even though no payment has been missed.

Venture debt transfers a meaningful degree of operational control to the lender. The borrower retains formal management authority but operates under continuous covenant oversight.

Default consequences range from interest-rate step-ups (commonly 200 to 300 basis points) to acceleration of the entire outstanding balance and UCC foreclosure on the collateral pool.

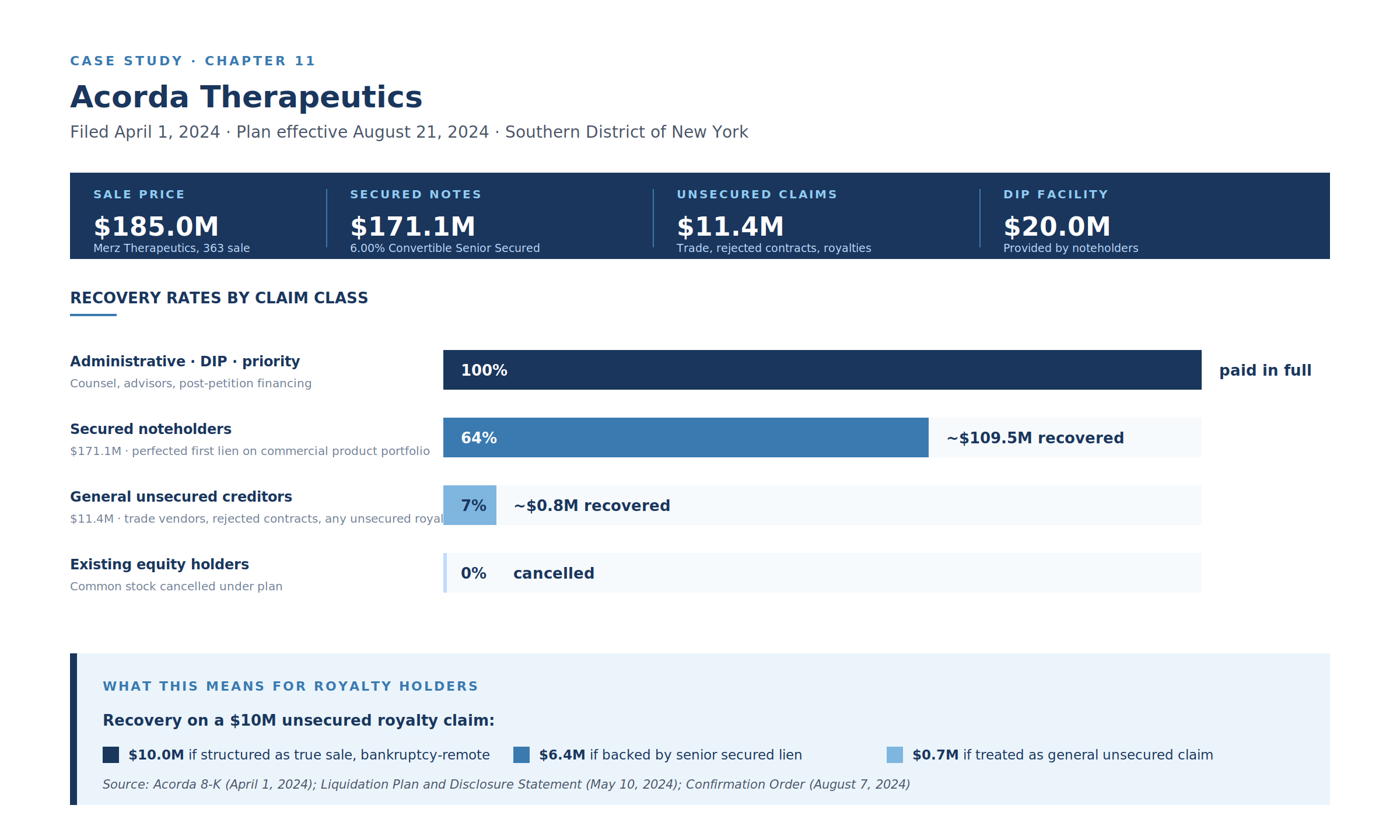

What Happens in Distress: The Acorda Recovery Data

The structural questions become concrete in bankruptcy. Acorda Therapeutics' April 2024 Chapter 11 provides the clearest recent benchmark.

Acorda did not have venture debt in the strict sense, but it did have $171.1 million in 6.00% convertible senior secured notes with a perfected first-priority lien on its commercial product portfolio. The structural position was equivalent to a senior secured venture facility.

The Section 363 sale to Merz Therapeutics produced $185 million in proceeds. The confirmed liquidation plan distributed those proceeds as follows:

- Administrative, DIP, and priority claims: 100% recovery

- Secured noteholders ($171.1M): 64% recovery, approximately $109.5M

- General unsecured creditors ($11.4M): 7% recovery, approximately $0.8M

- Equity holders: cancelled

The royalty implication is direct.

A $10 million royalty obligation structured as a true sale (bankruptcy-remote) recovers the full $10 million, because it is not part of the estate. The same $10 million obligation backed by a senior secured lien recovers $6.4 million. The same $10 million obligation treated as a general unsecured claim recovers $0.7 million.

The 14-fold gap between the best and worst outcomes is not a function of the underlying economics of the royalty. It is a function of how the transaction was structured at inception.

Where Venture Debt and Royalty Financing Collide

The structural collision arises because both venture debt and pharmaceutical royalty financing typically require some form of security interest or covenant protection in respect of the same intellectual property and revenue streams.

The modern royalty deal architecture, as documented in Gibson Dunn's 2026 market update, has converged on a standard package that includes:

- True sale documentation

- A backup security interest covering the royalty payment stream and underlying product rights

- Non-incurrence covenants restricting additional secured debt at the product level

- SPV structures that isolate the royalty interest from the operating company's estate

Each of these elements interacts directly with what a venture lender has already taken. Five points of friction recur across transactions.

1. The negative pledge collision

A venture debt negative pledge on IP prevents the borrower from granting a security interest in the underlying patents to a royalty buyer.

The royalty deal cannot close as drafted unless the venture lender consents to a carve-out, releases the negative pledge against the specific IP being monetised, or is repaid in full.

2. The non-incurrence covenant collision

Royalty buyers commonly require that the borrower not incur additional secured debt at the product level. A pre-existing venture debt facility violates this covenant on day one of the royalty transaction.

It must either be refinanced or expressly grandfathered in the royalty agreement.

3. Cross-default exposure

A covenant breach under the venture debt facility, even a technical breach with no payment default, can trigger cross-default provisions in the royalty agreement.

The royalty holder may find its capped synthetic royalty accelerates to the full hard cap precisely at the moment the venture lender is moving to enforce against the collateral pool.

4. Priority on backup security interests

When a royalty deal is structured as a true sale with a backup security interest, the priority of that backup interest depends on the order of UCC filings and any applicable subordination agreements.

If the venture lender filed first and refuses to subordinate, the royalty buyer's backup lien sits behind the venture lender. The backup is then a second-priority recovery mechanism whose value depends on whether the venture lender's claim is fully satisfied from the collateral pool.

5. Fraudulent transfer exposure on royalty payments

When a borrower in financial distress pays royalty obligations from operating cash within the look-back window before insolvency, those payments may be challenged as preferential transfers or fraudulent conveyances.

The Bankruptcy Code's 90-day preference window for ordinary creditors and one-year window for insiders means that royalty payments made shortly before a Chapter 11 filing are routinely scrutinised.

SPV structures help isolate cash flows from this risk, but the structural separation must be substantive, not nominal, to survive challenge.

Three Pathways: How Recent Transactions Have Resolved the Collision

When a biotech with existing venture debt seeks royalty financing, three structural pathways predominate. Each produces different outcomes for the royalty holder if the borrower subsequently encounters distress.

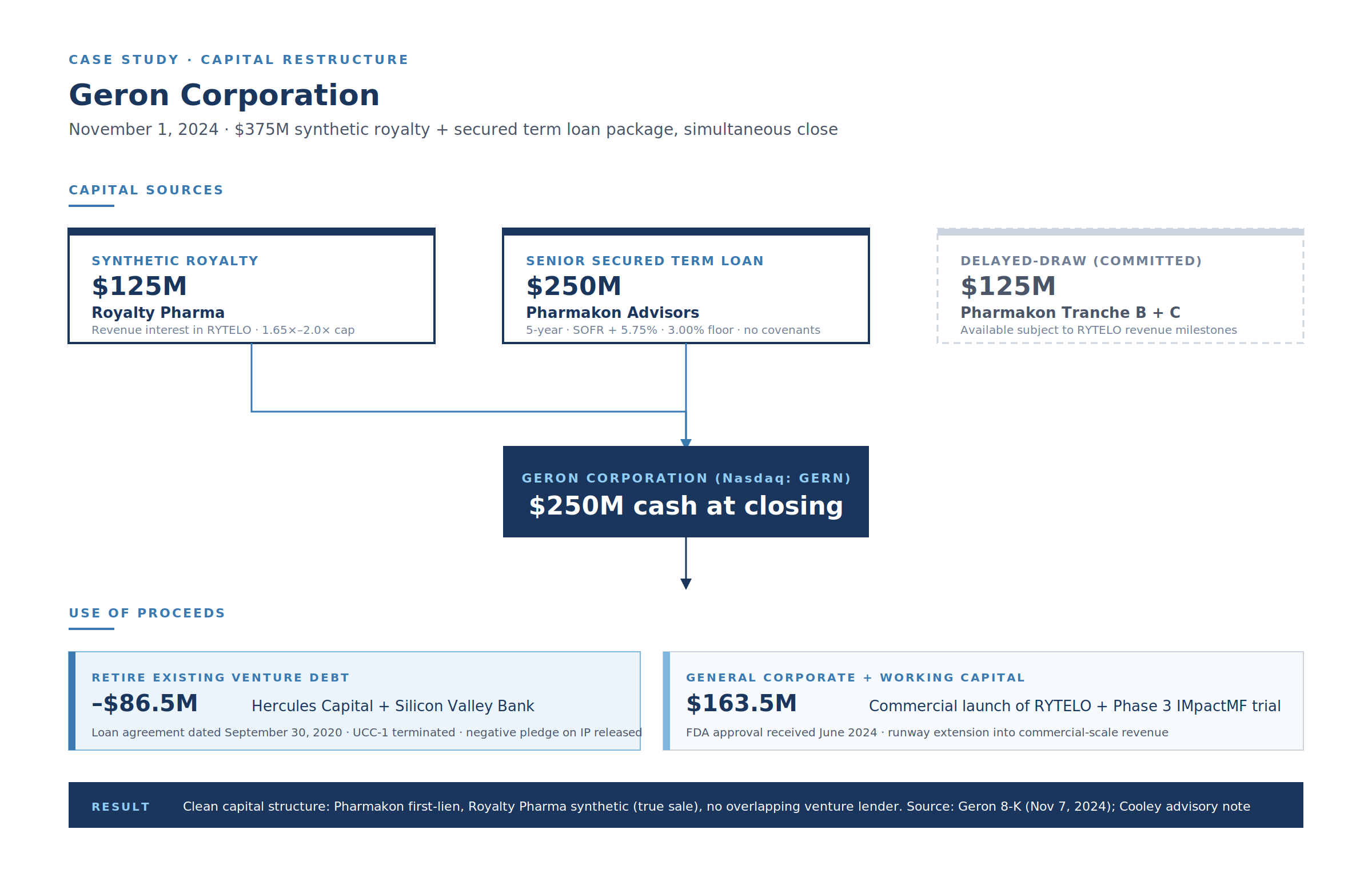

Pathway A: Full refinancing

The cleanest structural pathway is full refinancing of the venture debt as part of the royalty transaction. Geron's November 2024 transaction is the canonical example.

Geron simultaneously closed a $125 million synthetic royalty agreement with Royalty Pharma and a $250 million senior secured term loan facility from investment funds managed by Pharmakon Advisors.

A first tranche of $125 million was drawn on the Pharmakon facility at closing. Of that, $86.5 million was used to fully repay the company's existing Hercules Capital and Silicon Valley Bank loan.

The Hercules facility was terminated. The UCC-1 was released. The new lender package took clean structural priority over the company's assets.

The resulting capital structure was unambiguous:

- Pharmakon held a senior secured term loan with a first-priority lien

- Royalty Pharma held the synthetic royalty interest documented as a true sale

- No overlapping venture lender remained to negotiate with

The synthetic royalty's revenue cap sat at 1.65 to 2.0 times the $125 million invested, with no scheduled amortisation on the Pharmakon loan and no financial covenants, priced at SOFR plus 5.75% with a 3.00% SOFR floor.

Trade-offs of full refinancing are real but bounded. Prepayment fees, end-of-term charges, lost warrant relationship value. The resulting structure is the cleanest available.

Pathway B: Carve-out and subordination

The second pathway preserves the venture lender (or other senior secured creditor) but carves the relevant royalty stream out of its collateral package.

Clearside Biomedical's August 2022 royalty agreement with HealthCare Royalty Partners is illustrative. Its subsequent bankruptcy in November 2025 also reveals the limits of the structure.

Clearside created a dedicated royalty subsidiary, Clearside Royalty LLC, and transferred to it the rights to receive royalty and milestone payments related to XIPERE and the SCS Microinjector technology. The subsidiary then sold those rights to HealthCare Royalty for $32.5 million.

Clearside pledged the equity in the royalty subsidiary to the parent's creditors. But the underlying royalty stream had been moved structurally outside the operating estate.

When Clearside filed for Chapter 11 in November 2025, the SPV architecture functioned as designed. The royalty interest itself was not property of the operating debtor's estate. HealthCare Royalty's structural position was protected.

But the equity in the royalty subsidiary was an estate asset. A September 2025 amendment to the royalty agreement, which an Ad Hoc Group of Equity Holders alleged had waived a contingent $12.5 million payment, became the focus of an allocation dispute that has not yet been resolved at the time of writing.

SPV structures provide effective insolvency-remote protection for the royalty payment stream itself. They do not eliminate disputes about residual SPV value, equity pledges, or pre-petition amendments executed in the zone of insolvency.

Pathway C: Layered backup lien

The third pathway, in which a royalty buyer accepts a backup security interest that ranks behind an existing senior secured creditor, is the fastest to close but carries the most severe insolvency consequences if the structure is tested.

Acorda is the cautionary benchmark. As the recovery data above demonstrate, when a junior royalty position sits behind senior secured debt, and the senior secured creditor absorbs most of the estate value, the junior recovery collapses to single digits.

Comparing the Three Pathways

The recovery differential across the three pathways is substantial.

A $100 million royalty investment, modelled against a borrower with $80 million of senior venture debt and a $150 million enterprise sale value, produces dramatically different outcomes:

- Pathway A (full refinancing): ~$95M recovery

- Pathway B (carve-out and SPV): ~$70M recovery

- Pathway C (junior backup): ~$7M recovery

The 14× differential between the best and worst structures is not a function of the underlying credit quality of the borrower. It is a function of how the deal was structured years before distress arrived.

The Recharacterisation Question Returns

Each of the three pathways interacts with the underlying question of true sale versus secured loan characterisation, which the Mallinckrodt and PhaseBio decisions brought into sharp focus.

A royalty agreement structured as a true sale places the royalty stream outside the bankrupt estate, but only if the structure survives a fact-intensive challenge in court.

The presence of a senior secured venture lender complicates that analysis in two ways.

First, if the venture lender's collateral package includes the underlying product IP and revenue streams, a court considering whether the royalty has been "truly sold" may give weight to the fact that the same assets remained subject to the senior lien. The economic substance test asks whether the risk of loss genuinely transferred to the buyer. A royalty interest that is structurally subordinate to a venture debt lien on the same revenue stream looks more like a participation in a secured loan than an outright sale.

Second, intercreditor agreements between the venture lender and the royalty buyer often contain payment subordination provisions, standstill periods, and turnover obligations that can be cited as evidence that the royalty buyer did not, in substance, take an irrevocable transfer. DLA Piper's analysis of intercreditor terms in venture debt transactions describes the negotiation dynamics that produce these provisions, but their downstream effect on true-sale analysis is rarely discussed at the negotiation stage.

Cross-Border Complications

The structural collision intensifies in cross-border transactions.

A US-based venture lender taking UCC-perfected security under New York law does not automatically obtain enforceable rights against assets located in Switzerland, Israel, the United Kingdom, or the European Union.

The Swiss case

Switzerland does not recognise the floating charge or blanket lien concept that underlies most US venture debt structures. A Swiss biotech that has granted a "lien on substantially all assets" under a New York-law venture debt facility may find that the lien is not enforceable in Swiss bankruptcy proceedings without separate Swiss-law security documents covering each category of asset.

A royalty buyer that has taken a backup security interest under New York law faces the same enforcement gap.

The English law dimension

Under the Gibbs rule, an English-law-governed debt cannot be discharged by foreign insolvency proceedings.

A royalty agreement governed by English law preserves the buyer's right to enforce the obligation regardless of a continental European or US insolvency proceeding. The same protection is not available to a New York-law-governed venture debt facility against an English borrower.

The choice of governing law in the venture debt and in any subsequent royalty financing should be coordinated, not left as a default.

The EU harmonisation directive

The November 2025 provisional agreement on EU insolvency harmonisation introduces pre-pack procedures and avoidance rules that will affect how venture debt and royalty obligations are treated in member-state restructurings.

The directive's pre-pack provision permits the sale of a debtor's business with automatic transfer of executory contracts. A royalty obligation could be assigned to a buyer that the original royalty holder did not evaluate as a credit risk, without consent. Venture debt-related assets and obligations may move similarly.

Implications for Deal Structuring

The relative seniority and structural compatibility of venture debt and royalty financing must be analysed at the inception of either transaction, not when distress arrives.

For a biotech with existing venture debt contemplating a royalty financing

Diligence sequence:

- Detailed review of existing venture debt covenants and security package

- Identification of any IP negative pledge or non-incurrence restrictions

- Modelling of prepayment economics if Pathway A is pursued

- Assessment of the venture lender's willingness to subordinate or release if Pathway B is pursued

- Candid evaluation of recovery scenarios under Pathway C if distress materialises

For a royalty buyer evaluating a transaction with existing venture debt

Diligence sequence:

- UCC search in all relevant jurisdictions to confirm scope of the existing lien

- Assessment of the venture lender's reputation for forbearance versus aggressive enforcement

- Analysis of whether the royalty agreement fits within the venture debt's permitted-liens or restricted-payments baskets

- Stress test of the recovery position in a Section 363 sale or Chapter 11 plan

For a venture lender originating a new facility into a biotech

The lien package should be drafted with explicit treatment of any anticipated royalty stream. A blanket prohibition on royalty financing forecloses an important non-dilutive option for the borrower. A permitted-baskets approach with negotiated thresholds preserves flexibility while protecting the lender's economic interest.

What This Means

The biotech insolvency wave that has run from 2023 through 2026 is now well documented. The 2024 venture debt market reached a record $53.3 billion. The royalty market continues to grow alongside it.

The structural questions raised by the interaction of these two asset classes are not theoretical. They will be tested, repeatedly, in bankruptcy courts on both sides of the Atlantic over the coming years.

The borrowers, lenders, and royalty buyers who think carefully about the lien architecture at inception will fare better than those who do not.

All information in this article was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, court decisions, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.