The Co-Funding Royalty: Phase III Co-Investment, Synthetic Revenue Interests, and How BD Teams Position the Hybrid Proposal

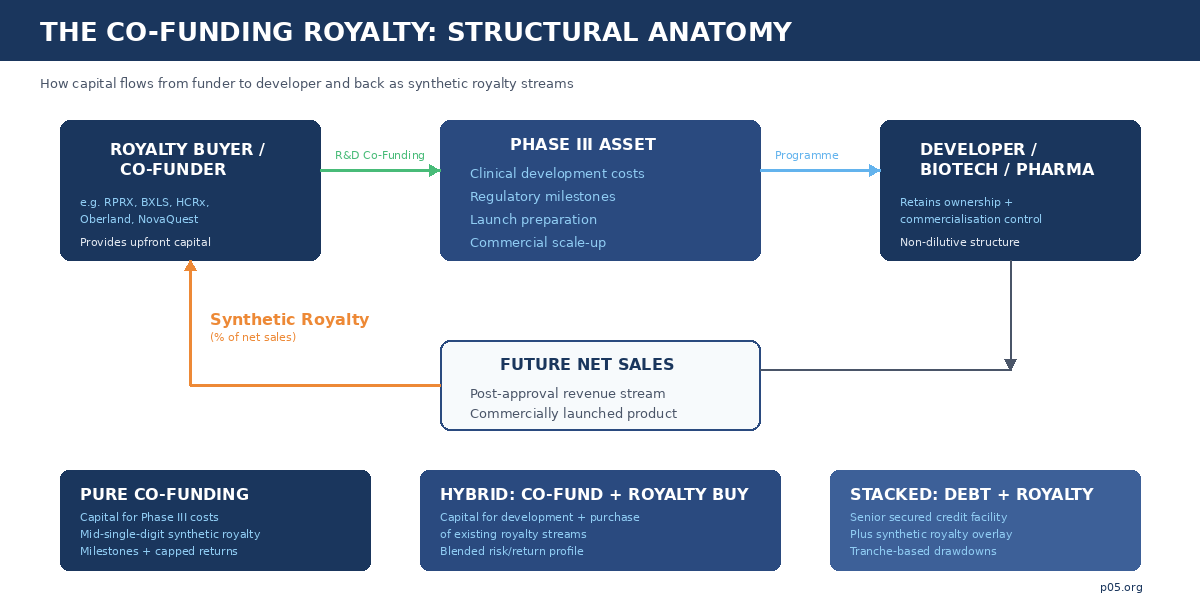

Somewhere between a licence, a loan, and an equity investment — but structurally none of these — sits a transaction type that has quietly become one of the most consequential instruments in late-stage pharmaceutical finance. No IP changes hands. No fixed coupon is owed. No shares are issued, no board seats granted. The capital provider funds Phase III clinical development and, in exchange, receives a newly created synthetic royalty on future product net sales.

The co-funding royalty, as practitioners now call it, lets the buyer manufacture the royalty stream it will later own. The seller retains full programme control, avoids equity dilution, and sidesteps the covenant architecture of venture debt. The risk profile sits between venture and annuity — clinical-stage uncertainty on the front end, duration-matched cashflow on the back end — and the contractual engineering required to make it work is dense, bespoke, and increasingly competitive.

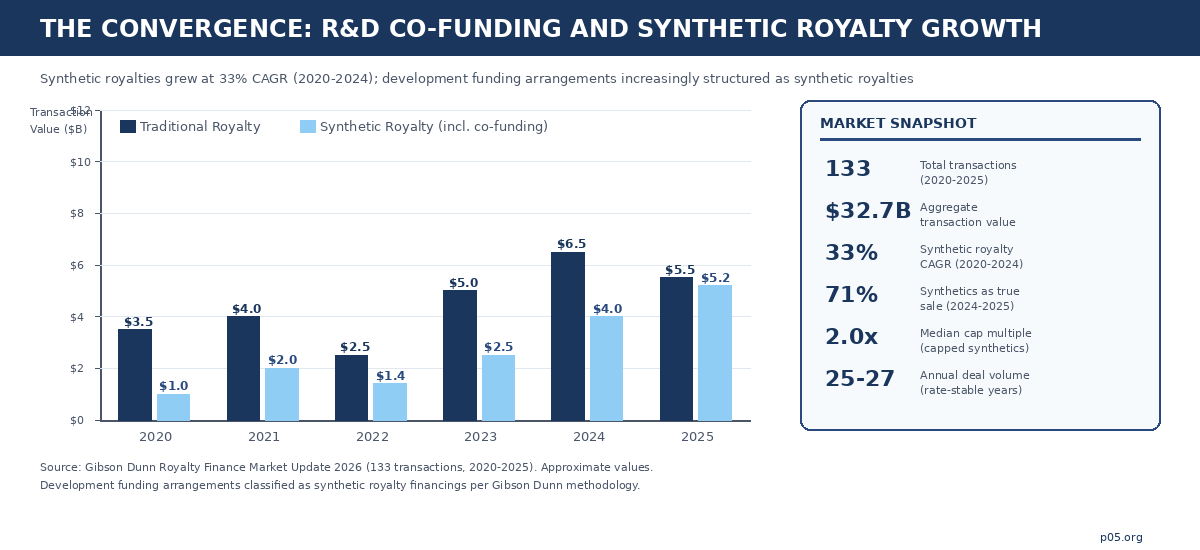

Six years of deal data now exist to study. Gibson Dunn's 2026 Royalty Finance Market Update catalogues 133 transactions totalling $32.7 billion in aggregate value across 2020-2025. Synthetic royalties — the category that captures co-funding arrangements — grew at an average annual rate of 33% over the five-year period. Annual deal volume held steady at 25-27 transactions per year even as the federal funds rate climbed above 5%, and the market reached record levels once rate volatility stabilised. A mature and expanding asset class with $32.7 billion behind it demands a correspondingly serious treatment.

What follows covers the structural mechanics, the deal landscape as of April 2026, the BD positioning considerations that determine whether a hybrid proposal succeeds or fails, and the second-order consequences for royalty stacking, M&A optionality, and capital-markets signalling.

The structural logic: why co-fund when you can just buy?

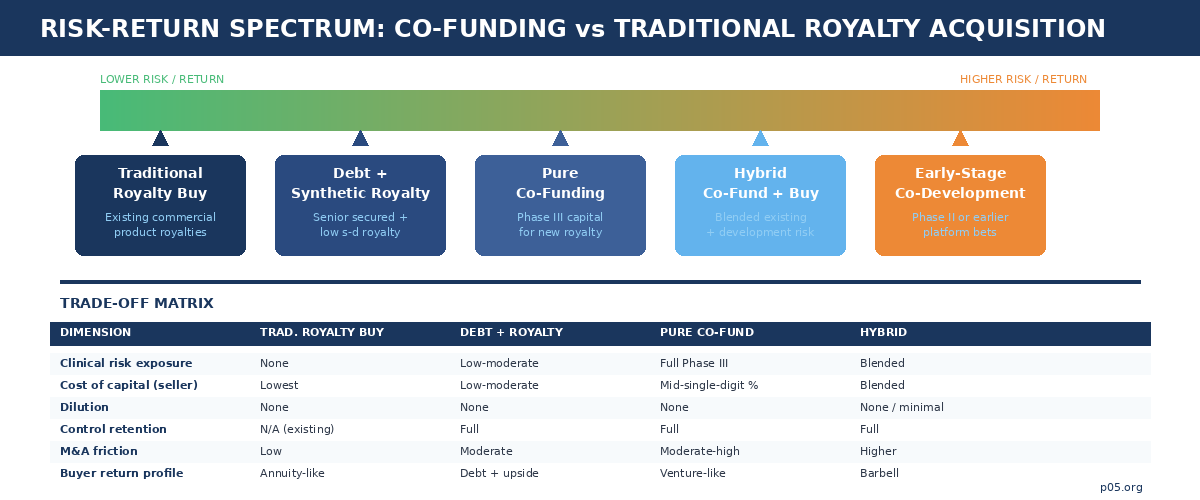

Traditional royalty acquisition is conceptually simple. A fund purchases an existing royalty interest — or a synthetic interest in future net sales — from a licensor, university, or operating company that originated the royalty through an earlier licence. The buyer underwrites a known or estimable revenue stream. The seller receives upfront capital. Risk is contained because the royalty obligation already exists, typically backed by a marketed product or a late-stage asset with substantial clinical evidence.

Co-funding abandons this comfort. The buyer provides capital directly to the developer to fund pivotal clinical trials, regulatory submissions, and launch preparation. In exchange, the developer grants a newly created royalty on future product net sales — a royalty that did not exist before the cheque was written. The buyer is creating an asset rather than purchasing one, and its value is contingent on the clinical, regulatory, and commercial success of the programme it is funding.

The economics are intuitive: by bearing development risk, the co-funder obtains a royalty at a significantly lower effective cost than it would pay to acquire the same interest post-approval. The developer receives non-dilutive capital that preserves equity ownership, maintains full programme control, and avoids the covenant structures typical of venture debt. Neither side gives up what it values most.

The structural formulation is:

NPV(Co-Fund) = Σ [p(approval) × p(commercial) × α × Net Sales(t)] / (1 + r)^t − Capital Invested

Where α is the synthetic royalty rate, p(approval) captures Phase III and regulatory risk, p(commercial) captures launch and market-share uncertainty, and the discount rate r embeds both the time value of capital and the buyer's required risk premium for bearing clinical-stage exposure.

The distinction from venture lending is in the return profile: the buyer's participation tracks a percentage of downstream commercial value rather than a fixed coupon, meaning upside is uncapped (or capped at a negotiated multiple) and duration can extend for a decade or more post-launch. The distinction from equity co-investment is in governance: no board seats, no dilution, no control transfer. The co-funder is, in economic terms, a silent participant in the product's commercial future.

The deal landscape: five funds, five structural variants

Every major royalty-focused capital provider has developed its own variant of the co-funding structure, tailored to its portfolio construction and return targets. Studying the deals in sequence reveals the mechanics and the competitive dynamics shaping the market as of April 2026.

Royalty Pharma has been the most active and most explicit proponent, describing its model as funding innovation "directly when it partners with companies to co-fund late-stage clinical trials and new product launches in exchange for future royalties." Three recent transactions illustrate the range. The Biogen/litifilimab collaboration (up to $250 million for a Phase III lupus programme, in exchange for mid-single-digit royalties and milestones) is a textbook pure co-funding structure: one asset, one funder, one synthetic royalty, clinical risk fully accepted.

The $2 billion Revolution Medicines partnership on daraxonrasib layers a synthetic royalty of up to $1.25 billion with a $750 million secured debt facility — a stacked structure where the royalty and debt instruments work in tandem, and where the first tranche is drawn only after FDA approval. And the $500 million JNJ-4804 co-funding (March 2026) takes the model into earlier-stage territory, committing capital across 2026-2027 to a dual-pathway co-antibody still in active clinical development.

That last deal is worth pausing on: it is Royalty Pharma deploying half a billion dollars into a programme that has not yet reported pivotal data, a risk posture that would have been unthinkable for a traditional royalty buyer even five years ago.

Blackstone Life Sciences pioneered the mega-scale hybrid, and its structural template has been widely imitated. The 2020 $2 billion collaboration with Alnylam combined the purchase of 50% of Alnylam's inclisiran royalties ($1 billion) with $150 million in R&D co-funding for the Phase III development of vutrisiran and ALN-AGT, plus corporate debt and an equity purchase. The architecture is a barbell: an existing commercial-stage royalty provides near-term cashflow, while the co-funded pipeline assets provide development optionality. The lifecycle of this deal is itself instructive.

Blackstone funded vutrisiran through its pivotal HELIOS-B trial, the drug was approved as Amvuttra, and Blackstone then sold the royalty interest to Royalty Pharma for $310 million in November 2025 — demonstrating that co-funded royalties, once de-risked, are fully tradable in the secondary market. More recently, Blackstone committed $400 million to co-fund J&J's bleximenib for acute myeloid leukaemia, and invested $700 million in MSD's sacituzumab tirumotecan ADC programme in exchange for a royalty stream.

The BXLS platform now reports an 86% regulatory approval rate across its Phase III assets, compared to an industry average of roughly 48%. That track record is the underwriting thesis made real.

Oberland Capital occupies a distinctive structural niche: senior secured notes combined with tiered royalty payments and milestone-based tranches. The $600 million Biohaven investment (April 2025) provided $250 million at closing for troriluzole development in spinocerebellar ataxia, with $150 million contingent on FDA approval and up to $200 million available at mutual agreement for strategic acquisitions. In exchange, Oberland receives tiered single-digit royalties on global net sales, capped at a multiple of amounts funded and limited to 10 years from closing.

The note purchase agreement provides downside protection through security; the royalty overlay captures commercial upside. This is the debt-plus-royalty variant — less clinical risk for the funder than a pure co-fund, but also a more moderate return profile.

HealthCare Royalty (HCRx), now majority-owned by KKR with $7+ billion committed across 110+ products, deploys a similar stacked approach. Its April 2026 Apnimed financing illustrates the mechanics precisely: a $150 million senior secured credit facility with milestone-triggered tranches ($50 million at closing, $50 million on FDA approval of AD109, $50 million on a sales milestone), plus a synthetic royalty at a low single-digit percentage of AD109 net sales.

The four-year interest-only period (extendable to five on hitting a sales target) is the credit instrument; the synthetic royalty is the equity-like upside layer. The Apnimed deal is notable because it funds commercial launch preparation rather than pivotal trials — the NDA submission is expected this quarter — positioning HCRx's capital at the approval-to-launch transition rather than the trial-to-readout transition.

NovaQuest Capital (originally the strategic investment arm of Quintiles, now IQVIA) brands its approach as "Product Finance": structured, non-dilutive investments in late-stage pharmaceutical products where capital funds pivotal trials and launches in exchange for royalty-like participation.

The Phathom Pharmaceuticals revenue-interest financing ($100 million upfront, $160 million on FDA approval, capped at 2.0x invested capital) shows the cap-and-tail mechanics that define NovaQuest's risk management: once the cap multiple is reached, the royalty terminates and all subsequent revenue reverts to the developer. This time-bounded, multiple-capped structure is characteristic of co-funders optimised for IRR rather than perpetual yield.

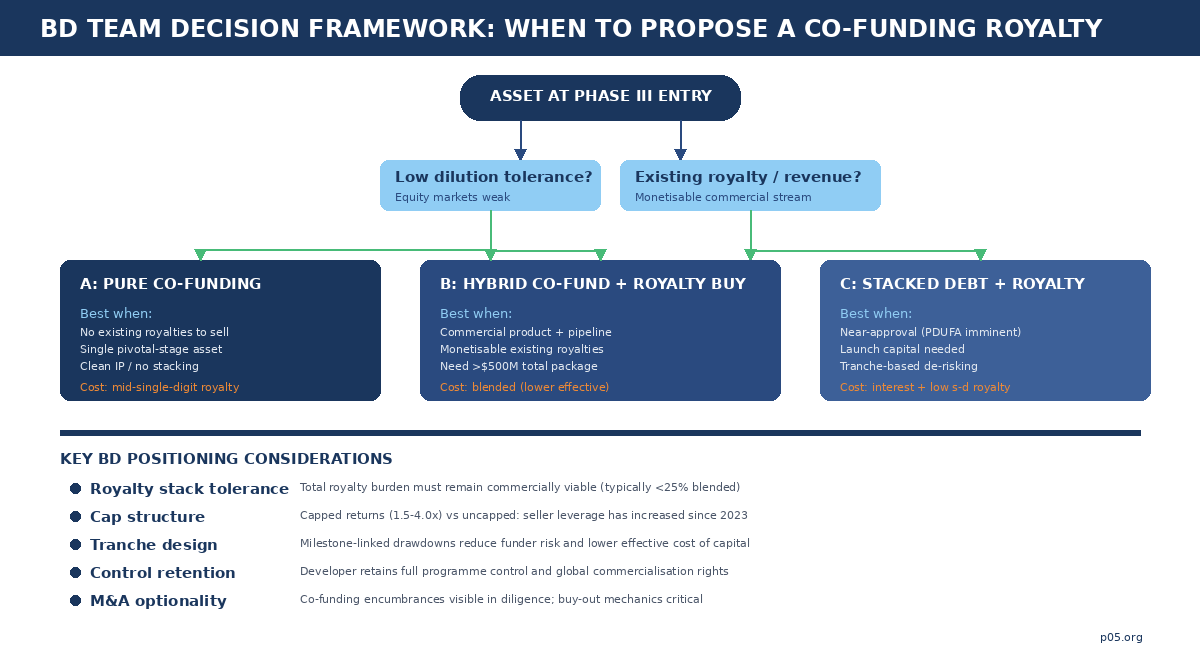

How BD teams position the hybrid proposal

For a biotech BD team approaching a Phase III financing decision, the co-funding royalty demands more than term-sheet negotiation. It is a strategic positioning exercise that requires solving simultaneously for capital needs, dilution constraints, programme control, royalty-stack management, and downstream M&A optionality. The framing determines which counterparties engage and at what terms.

Establishing the use case

The co-funding structure works best when the company's equity is trading at depressed levels or the market is unreceptive to follow-on offerings, the pipeline is concentrated around a single pivotal asset where Phase III is the primary value inflection, the existing royalty stack is thin enough to absorb a new synthetic royalty without impairing commercial economics, and the board has a strong preference for retaining programme control without ceding governance rights. These conditions tend to cluster: a biotech with a single late-stage asset in a weak equity market and a clean IP position is the canonical co-funding candidate.

Not every Phase III programme is co-fundable, however. The buyer's diligence will focus on clinical differentiation (is this a me-too or a potential best-in-class?), addressable market size (does the revenue potential justify a multi-hundred-million-dollar commitment?), intellectual property position (is there freedom-to-operate risk or patent-cliff proximity?), and competitive dynamics (how many shots on goal exist in the same indication?).

BD teams that approach co-funders with a generic "we need Phase III capital" pitch will be screened out. The pitch needs to answer the buyer's real question: "Is this the kind of asset I want to own a royalty on for the next decade?"

Calibrating the royalty: rate, tier, cap, and tail

The most consequential negotiation variable is the royalty rate itself. As of 2026 market practice, pure co-funding arrangements in Phase III typically command mid-single-digit synthetic royalties on annual worldwide net sales, though the effective cost varies significantly with tier structures, caps, and tranche mechanics.

Tiered rates — where the royalty percentage declines as product sales scale — are now common and represent a meaningful improvement for sellers of high-conviction assets. A structure might pay 5% on the first $1 billion of annual net sales and 3% above that threshold, functionally creating an annual soft cap that protects upside. Hard cap structures range from 1.55x to 4.0x of invested capital (median 2.0x for capped synthetics), and approximately half of synthetic royalty financings include some form of cap.

Once reached, the royalty terminates and all subsequent revenue reverts to the developer. The tail — the period after the cap is reached or the primary royalty term expires — remains a critical negotiation point: traditional royalty financings include tail provisions at more than three times the rate of synthetics, reflecting the distinction between perpetual-interest buyers and time-bounded co-funders.

For the BD team, the art is in matching the royalty design to the counterparty's return model. A fund that needs annuity-like cashflows may accept a lower rate in exchange for longer duration and no cap. A fund optimised for IRR may prefer higher initial rates with milestone acceleration and a defined exit. The pitch must be tailored to the counterparty's portfolio construction logic, matching the royalty design to their return model rather than defaulting to the company's funding requirement.

Tranche design: milestone-gated capital deployment

Nearly every co-funding transaction of the past three years features milestone-linked drawdowns, and the tranche structure is both a risk-management device and a signalling mechanism. A first tranche is funded at closing (providing immediate capital for trial costs), with subsequent tranches contingent on clinical readouts, regulatory filings, or FDA approval.

The Oberland/Biohaven structure is canonical: $250 million at closing, $150 million upon FDA approval, up to $200 million at mutual agreement for strategic acquisitions. The HCRx/Apnimed structure follows identical logic at a smaller scale: $50 million at closing, $50 million on approval, $50 million on a sales milestone. For the funder, milestone gating reduces capital-at-risk by staging deployment against de-risking events. For the developer, it ensures capital availability at the moments of greatest need.

BD teams should position the tranche design as a feature: the funder's capital enters only as the programme de-risks, each tranche deploying into a progressively more certain asset. This framing converts a funding limitation into an alignment mechanism — both parties share the same milestones, the same binary outcomes, the same temporal pressure.

Managing the royalty stack

The royalty-stack conversation is where many co-funding proposals fail. If the developer's asset already carries a background royalty (to a university licensor, a platform technology provider, or a previous financing), adding a synthetic royalty may push the total burden above commercially viable levels. Payer pressure, competitive dynamics, and margin requirements typically constrain the aggregate royalty stack to something in the range of 20-25% of net sales, though this varies by therapeutic area, pricing power, and reimbursement structure.

The BD team must present a transparent royalty waterfall to the prospective co-funder, showing exactly how the new synthetic royalty layers onto existing obligations. Transparency here does double work: it demonstrates credibility and it pre-empts diligence surprises that could derail negotiation. The best proposals include an illustrative scenario analysis showing the product's gross-to-net cascade, aggregate royalty burden, and remaining operating margin under base, upside, and downside commercial assumptions.

Offset mechanics — contractual provisions allowing the developer to credit third-party royalty payments against the co-funder's royalty — are increasingly common and should be proposed proactively. These provisions reduce the economic risk of stack accumulation and make the co-funder's interest more resilient to downstream licensing activity.

The hybrid advantage: blending existing royalties with development funding

The purest expression of the co-funding model is the hybrid: a single transaction in which the buyer simultaneously purchases existing royalty streams and co-funds new clinical programmes. The Blackstone/Alnylam transaction remains the structural benchmark, but the MorphoSys partnership (Royalty Pharma, December 2023) is equally instructive and arguably more complex.

In the MorphoSys deal, Royalty Pharma committed $2.025 billion across multiple instruments: it acquired MorphoSys's existing Tremfya (guselkumab) royalties as the commercial anchor, purchased royalty and milestone interests in four development-stage therapies (gantenerumab, otilimab, pelabresib, and CPI-0209), provided up to $350 million in Development Funding Bonds to finance clinical programmes, and purchased $100 million of MorphoSys equity.

The pelabresib and CPI-0209 interests were structured as synthetic royalties on future net sales (3% each) — created through the transaction rather than acquired from a pre-existing licence. The Development Funding Bonds explicitly funded clinical development.

The hybrid architecture gives the buyer a barbell portfolio within a single transaction: the existing Tremfya royalty provides near-term, de-risked cashflow, while the development-stage synthetic royalties and co-funding bonds provide optionality on pipeline assets. The blended risk-return profile is more attractive than either component alone, because the commercial-stage anchor subsidises the cost of capital for the development-stage bets.

For BD teams at companies with both a marketed product and a pivotal pipeline, the positioning insight is fundamental: offer a portfolio, not an asset. Let the buyer anchor its investment in commercial-product economics and take development-stage optionality at a marginal cost that is far below what a standalone co-funding would price.

This is one of the few structures where the seller's complexity is an advantage rather than a liability — because the buyer can construct an internal hedge that no single-asset co-fund can replicate.

Second-order consequences: what BD teams forget to negotiate

Co-funding royalties carry costs beyond the explicit royalty rate, and the ones that matter most are routinely underweighted in initial negotiations.

M&A encumbrance

Every synthetic royalty created through co-funding becomes visible in acquisition diligence. A potential acquirer will scrutinise the change-of-control provisions, assignment mechanics, acceleration triggers, and buy-out price alongside the royalty rate itself. A well-drafted co-funding agreement anticipates M&A by including a negotiated change-of-control buy-out at a defined multiple of remaining expected payments. A poorly drafted agreement can become a blocking position — or at minimum a significant price-adjustment item — in an acquisition process.

The standard approach is a buy-out right at a pre-agreed multiple (often 1.5-2.0x of remaining invested capital, declining over time), ensuring the co-funder is compensated for early termination while the developer retains strategic flexibility. BD teams should negotiate this at the outset — the co-funder will resist a cheap buy-out precisely because it reduces their hold value; the developer should insist on one precisely because it preserves optionality. The tension is real and the resolution is usually in the multiple.

Capital-markets signalling

A co-funding royalty sends a mixed signal to equity investors. The validation is real: a sophisticated royalty fund has diligenced the programme and committed capital, which is an implicit endorsement of clinical prospects. But so is the encumbrance: every dollar of net sales now has a percentage claim on it, reducing the equity holders' residual. The net signalling effect is term-dependent: a small-stake, uncapped co-funding at a low royalty rate reads as validation; a large-stake, high-rate co-funding with no cap reads as dilution-by-another-name.

Communications strategy matters as much as term-sheet strategy. The announcement should frame the co-funding as a de-risking event and a validation of the clinical thesis. "A leading capital partner has validated our programme and funded our path to approval without dilution" is a different equity narrative from "we needed money and this was the least dilutive option available."

Secondary-market tradability

Once a co-funded royalty is created, it becomes a tradable asset. The Blackstone-to-Royalty Pharma secondary sale of the Amvuttra royalty interest demonstrates the lifecycle: fund the Phase III trial, de-risk through approval, sell the resulting royalty to a longer-duration holder at a premium to the co-funder's basis. The co-funder's exit liquidity improves, reducing the discount rate demanded at origination — but the developer must accept that its capital partner may change identity over the life of the royalty.

Assignment provisions — who the royalty can be transferred to, under what conditions, with what notice — are therefore as important as the economic terms. A restriction on assignment to competitors or strategic acquirers may be appropriate. An absolute prohibition on assignment will reduce the funder's willingness to commit and increase the effective cost of capital. The right answer is usually a consent right with a reasonableness standard, plus a carve-out for transfers to affiliates and within the funder's fund family.

Where the model goes from here

The most visible shift heading into the second half of 2026 is that the model is moving earlier. The JNJ-4804 co-funding ($500 million for a programme still in active development) and Blackstone's bleximenib commitment ($400 million for a Phase III AML asset) both represent the most capitalised funds accepting greater clinical risk in exchange for larger royalty positions. If this continues, co-funding may eventually overlap with traditional pharma co-development structures — blurring the already-thin line between royalty finance and strategic partnership.

The dominance of true-sale structures reinforces this trajectory. Gibson Dunn's data showing that 71% of 2024-2025 synthetic deals and 91% of synthetic deal value were structured as true sales — not debt instruments — means co-funding royalties are increasingly treated as asset purchases. The consequences for accounting treatment (off-balance-sheet for sellers), bankruptcy remoteness (the royalty buyer's interest survives the developer's insolvency), and tax characterisation (sale of a future income stream rather than a borrowing) are material and require specialist advisory.

Meanwhile, the competitive landscape among royalty buyers is the most intense it has ever been. KKR-backed HCRx, Blackstone Life Sciences (which just closed a record $6.3 billion fund), Royalty Pharma, Oberland, NovaQuest, XOMA Royalty, OMERS, CPPIB, and DRI Capital are all actively deploying. Seller leverage has increased accordingly: tiered rates, capped returns, and seller-friendly offset provisions are direct consequences of this competitive dynamic. BD teams that run a competitive process across multiple potential co-funders will extract meaningfully better terms than those that negotiate bilaterally.

The intersection of co-funding with AI-driven drug discovery remains unexplored but structurally inevitable. As AI platforms accelerate the identification and optimisation of clinical candidates, the volume of Phase III-ready assets will increase, and the demand for non-dilutive pivotal-stage capital will grow. Co-funding structures will need to adapt to pipelines where the development timeline is compressed and the number of potential commercial products per platform is higher — creating both opportunity (more royalty-eligible assets per company) and risk (attribution complexity and royalty-stacking pressure across a broader portfolio).

The co-funding royalty has graduated from exotic to standard. Every company entering Phase III should evaluate whether a co-funding proposal — pure, hybrid, or stacked — offers a superior risk-adjusted path to launch compared to equity, venture debt, or traditional licensing. The companies that position the proposal correctly will fund their programmes on terms that preserve equity value and strategic optionality. The companies that do not will discover, usually too late, that the royalty they gave away was worth more than the dilution they avoided.

All information in this article was accurate as of the research date (April 2026) and is derived from publicly available sources including SEC filings, press releases, Gibson Dunn's Royalty Finance Market Update, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.