The Deuterium Problem: When a Hydrogen Swap Becomes a Royalty Dispute

How a royalty fund and a pharma company ended up in arbitration over whether deutivacaftor is the same compound as ivacaftor — and what it means for the pharmaceutical royalty market

{kind=link}

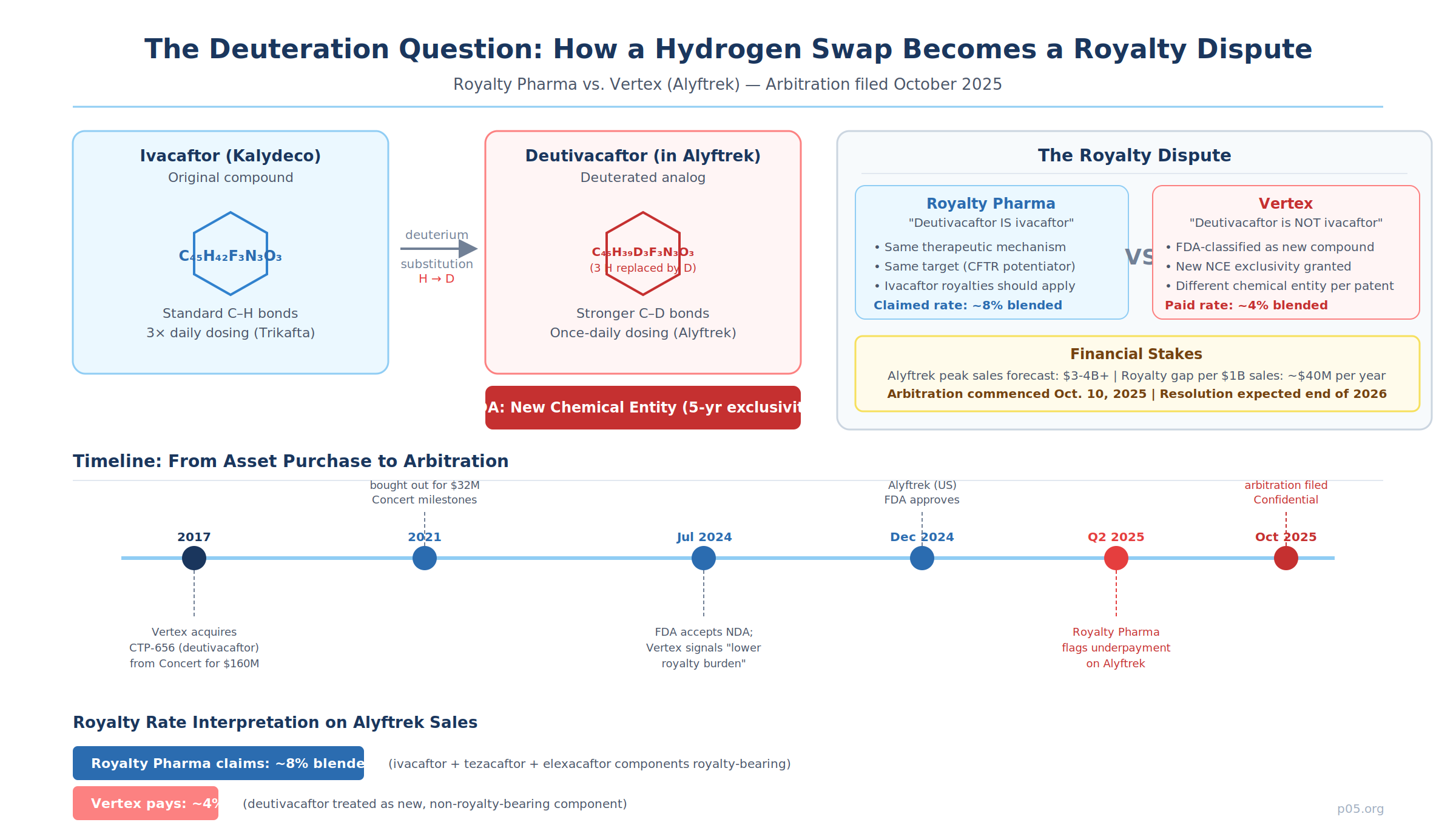

In July 2024, Vertex Pharmaceuticals disclosed something unusual in its FDA acceptance filing for the vanza triple: the investigational once-daily treatment would carry "a meaningfully lower single-digit royalty obligation, compared to the rate payable on Vertex's current CF portfolio." The company was not being modest about a minor administrative detail. It was pre-announcing a position it intended to take in what would become one of the most significant royalty scope disputes in pharmaceutical history.

That position — that deutivacaftor, the modified potentiator at the heart of Alyftrek (vanzacaftor/tezacaftor/deutivacaftor), is a new compound not covered by existing royalty agreements on ivacaftor — is now the subject of a confidential arbitration filed by Royalty Pharma on October 10, 2025.

The outcome will determine the royalty rate on a cystic fibrosis franchise that analysts expect to generate billions in annual sales. And the underlying question — whether a drug modified only by isotopic substitution is legally and contractually the same compound as its predecessor — will shape how licensees approach next-generation drug development for years to come.

What Deuteration Is, and Why It Matters for Royalties

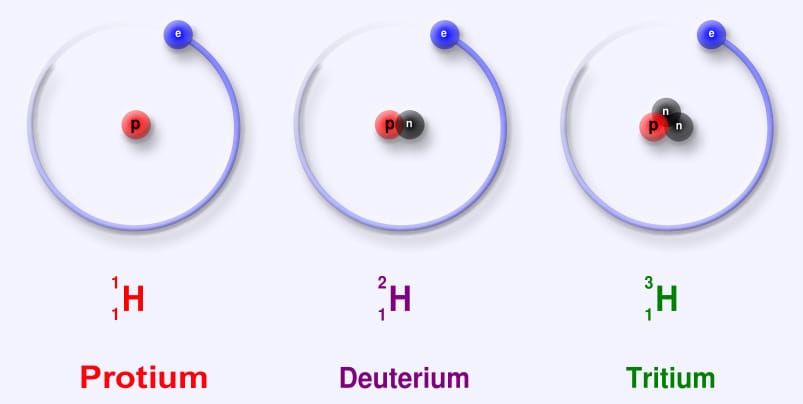

Deuterium is a naturally occurring, non-radioactive isotope of hydrogen. It contains one proton and one neutron, compared to hydrogen's single proton, making its atomic mass approximately twice that of hydrogen. When a carbon-hydrogen bond in a drug molecule is replaced with a carbon-deuterium bond, the resulting molecule is chemically very similar to the original but metabolically distinct: the stronger carbon-deuterium bond is harder for cytochrome P450 enzymes to cleave, which can slow metabolism, extend half-life, and alter the drug's pharmacokinetic profile.

From a regulatory standpoint, the FDA treats deuterated compounds as new chemical entities. Because deuterium changes the nature of a covalent bond, the agency's structure-centric interpretation of "active moiety" classifies a deuterated analog as a different compound from its parent, making it eligible for five-year new chemical entity exclusivity.

This classification is commercially powerful — it resets the exclusivity clock — but it creates a structural ambiguity when applied to legacy royalty agreements that were written with a specific compound in mind, not its isotopic variants.

The drug industry's experience with deuteration is recent. Teva's Austedo (deutetrabenazine), approved in April 2017, was the first deuterated drug to receive FDA clearance. It is a selectively deuterated version of tetrabenazine, which Lundbeck markets as Xenazine for Huntington's chorea.

The two methoxy groups in tetrabenazine that are targets of CYP2D6 oxidation were replaced with deuteromethyl groups, slowing the metabolism of the active metabolites and allowing less frequent dosing with a more consistent exposure profile. FDA classified deutetrabenazine as a new chemical entity — a determination that set the precedent Vertex would later rely upon.

Since then, four deuterated drugs have received FDA approval, with more in clinical development. The class includes deucravacitinib (Bristol-Myers Squibb's Sotyktu, approved 2022), deuruxolitinib (Sun Pharma's Leqselvi, approved 2024), and deutivacaftor in Alyftrek.

For each, the question of whether existing licensing and royalty agreements on the parent compound extend to the deuterated analog depends entirely on the language of those agreements and the intent of the original parties — which, in most cases, predates the commercial relevance of deuterium chemistry entirely.

The Vertex Situation: Two Positions, One Molecule

Ivacaftor is a CFTR potentiator discovered by Vertex and approved in 2012 as Kalydeco. It works by increasing the channel open probability of defective CFTR protein at the cell surface, allowing salt and water to flow more normally across cell membranes. It is one of the most commercially successful drugs ever developed for cystic fibrosis, and royalties on its sales are held by Royalty Pharma as part of a larger portfolio of CF franchise interests.

Deutivacaftor — originally called CTP-656 and also known as VX-561 — was developed by Concert Pharmaceuticals by applying deuterium chemistry to ivacaftor. Vertex acquired worldwide development and commercialization rights to the compound from Concert in 2017 for an initial cash payment of $160 million, with up to $90 million in additional milestones. Concert subsequently sold those milestone rights back to Vertex in 2021 for $32 million, securing non-dilutive capital to advance its own pipeline.

Deutivacaftor performs the same potentiator function as ivacaftor but, because of the stronger carbon-deuterium bonds at the two methoxy positions, it is metabolized more slowly. This pharmacokinetic difference is what enabled Vertex to incorporate it into a once-daily triple combination (vanzacaftor/tezacaftor/deutivacaftor), whereas the earlier Trikafta (elexacaftor/tezacaftor/ivacaftor) requires dosing twice daily.

Alyftrek received FDA approval in December 2024 and UK MHRA approval in March 2025, with European Commission approval following in July 2025.

Vertex's position is straightforward: deutivacaftor is not ivacaftor. The FDA has classified it as a new chemical entity. It has its own patent protection, its own new drug application, and its own NCE exclusivity period. The royalty obligations on Alyftrek, in Vertex's view, apply only to the components that are independently royalty-bearing — meaning the non-deutivacaftor ingredients — producing a blended royalty of approximately 4%.

Royalty Pharma's position is equally direct: the functional and therapeutic identity of deutivacaftor with ivacaftor means it falls within the scope of existing royalty agreements.

As stated in the company's 2024 10-K filing with the SEC, "we believe that deuterated ivacaftor (deutivacaftor) is the same as ivacaftor and is therefore royalty-bearing, which would result in a blended royalty of approximately 8% for Alyftrek." The four-percentage-point difference represents the application of ivacaftor-tier royalties (tiered from 6.5% to 10% on ivacaftor sales) to Alyftrek's sales allocation for the deutivacaftor component.

The Financial Stakes

The dispute is not theoretical. Royalty Pharma disclosed on its Q2 2025 earnings call that it had not received the royalties it believed it was contractually entitled to on Alyftrek net sales, and subsequently commenced the dispute resolution process. Formal arbitration was filed on October 10, 2025 and is confidential. Royalty Pharma has guided that resolution is expected no earlier than the end of 2026.

At current Alyftrek adoption trajectories, even modest penetration of the CF market generates hundreds of millions in annual product sales. The incremental royalty difference between 4% and 8% on, say, $2 billion in annual Alyftrek sales amounts to approximately $80 million per year, compounding over the expected royalty duration of 2039-2041 per Royalty Pharma's own estimates. The total at-stake value over the life of the product is material even against Royalty Pharma's multi-billion-dollar portfolio.

Royalty Pharma CFO Terry Coyne described patient conversion from Trikafta to Alyftrek as "gradual but steady" on the Q4 2025 earnings call, noting that switching from Trikafta is difficult given its strong efficacy. The franchise's long-term contribution remains significant for Royalty Pharma in any arbitration outcome scenario.

The table below summarises the key financial parameters of the dispute.

| Parameter | Royalty Pharma Position | Vertex Position |

|---|---|---|

| Deutivacaftor characterization | Same as ivacaftor; royalty-bearing | New chemical entity; not royalty-bearing |

| Blended Alyftrek royalty claimed/paid | ~8% | ~4% |

| Royalty on ivacaftor sales (tiered) | 6.5%–10% | Not applicable to deutivacaftor |

| Royalty on elexacaftor component | Mid-single digit | Mid-single digit (not in dispute) |

| Arbitration filed | Royalty Pharma, 10 Oct 2025 | Defending against claim |

| Expected resolution | End 2026 | End 2026 |

The Legal and Contractual Tension

The core interpretive question is whether "ivacaftor" in the royalty agreements means the specific chemical compound with the formula C₄₅H₄₂F₃N₃O₃, or whether it means any compound that performs the ivacaftor function — including structural analogs that share the same mechanism of action.

In pharmaceutical licensing, compound definitions typically fall into one of several categories: a specific chemical structure defined by CAS number or IUPAC name; a class of compounds sharing a structural feature; a therapeutic category; or a gene target. Agreements drafted before deuterium chemistry became commercially relevant would almost certainly not have anticipated the possibility of a deuterated analog that is functionally equivalent but chemically distinct under FDA classification.

The FDA's determination that deuterated compounds are new chemical entities reflects a structure-centric view of molecular identity. But royalty agreements are contractual instruments, not regulatory classifications. A court or arbitration panel interpreting a licensing agreement will generally apply the intent of the contracting parties as expressed in the agreement's language — not what the FDA says about new drug applications. If the agreement defines "ivacaftor" by reference to the compound's CFTR potentiator function, or by reference to a class of related compounds, deutivacaftor may fall within scope. If it defines "ivacaftor" by specific chemical identity, it may not.

Neither Royalty Pharma's nor Vertex's public statements have disclosed the precise contractual language at issue. Both parties have acknowledged the dispute in regulatory filings while declining to detail the specific contractual provisions. The arbitration is confidential, which means the outcome may not become public except through its financial effects on both companies' reported royalty receipts.

Analogous Patterns in Pharmaceutical Licensing

The Vertex/Royalty Pharma dispute is unusual in its scale and public visibility, but the underlying tension between drug modification and royalty scope is not unprecedented. Several comparable situations illustrate the range of outcomes.

Prodrug and active metabolite disputes arise when a licensee commercializes a compound that converts to the licensed molecule in vivo. If a royalty agreement covers drug X, and the licensee sells a prodrug of X that is metabolized to X in the body, the licensor may argue that the royalty extends to prodrug sales. Courts and arbitrators have generally examined the economic reality — does the prodrug capture the same market as the licensed compound — alongside the contractual language defining the licensed product.

The outcome depends heavily on whether the agreement's definitions were written broadly (covering therapeutic function) or narrowly (covering the specific compound).

Enantiomer switching is a structurally analogous situation. Several pharmaceutical companies have successfully commercialized the single active enantiomer of a racemic drug as a new product — a practice sometimes called "chiral switching" — and argued that royalty agreements on the original racemic mixture do not apply to the purified enantiomer. The most commercially visible example is AstraZeneca's development of esomeprazole (Nexium) as the S-enantiomer of omeprazole (Prilosec), which received new regulatory approvals with a fresh patent term.

Royalty holders on omeprazole faced questions about whether their agreements covered esomeprazole. The enantiomer dispute pattern has not generated consistent legal precedent, partly because most such disputes are resolved by private settlement rather than public litigation.

Salt and polymorph disputes occur when a drug is reformulated as a different salt form or crystalline polymorph than the compound specified in a licensing agreement. Different salts can have meaningfully different pharmacokinetic profiles, bioavailability, and patent protection — yet the therapeutic molecule and mechanism of action are identical. Royalty agreements that define the licensed compound by free base form may or may not extend to salt forms, depending on the drafting.

The Concert IP precedent itself is worth noting. Concert Pharmaceuticals built its business model around exactly the kind of value creation at issue here: taking existing licensed compounds, applying deuterium chemistry, and creating new proprietary assets. Concert's original CTP-656 program — applying deuteration to Vertex's own Kalydeco — demonstrates that Concert itself believed it was creating a new compound, not merely modifying ivacaftor. Vertex's acquisition of that program reinforced the view that deutivacaftor was a distinct asset with independent commercial value.

Implications for Royalty Investors

The dispute has several practical implications for the pharmaceutical royalty market that extend beyond the specific Vertex/Royalty Pharma situation.

Definition clauses are now commercially critical. Any royalty agreement covering a compound with ongoing development potential should now explicitly address what happens if a deuterated, enantiomeric, or other isotopically or structurally modified version of that compound is later commercialized.

The absence of such language in agreements drafted before deuterium chemistry became commercially relevant is precisely the gap that the Vertex dispute is testing. Going forward, sophisticated royalty investors and licensors will negotiate explicit provisions covering analogs, derivatives, deuterated forms, and next-generation formulations.

Regulatory classification does not determine contractual scope. Vertex's reliance on the FDA's NCE classification of deutivacaftor as a new chemical entity is a reasonable argument, but it is not determinative in a contract interpretation dispute. The FDA classifies compounds for regulatory purposes; arbitrators interpret contracts for commercial purposes.

These frameworks can diverge significantly. Royalty Pharma's position that the therapeutic identity of deutivacaftor with ivacaftor governs the royalty analysis reflects a substance-over-form approach that arbitrators in commercial disputes sometimes favor.

Lifecycle management creates systematic royalty risk for holders. Deuterium chemistry is one of several tools pharmaceutical companies use to extend the commercial life of existing compounds. Others include new salt forms, new indications, new formulations (extended-release, subcutaneous), and new delivery mechanisms. Each of these tools creates potential scope disputes for royalty holders who invested in the original compound.

The Alyftrek situation is the first prominent dispute to reach public arbitration involving deuterium specifically, but the underlying tension is pervasive across the royalty market. Royalty Pharma's Q4 2025 investor materials continue to characterize Trikafta and Alyftrek as part of a unified CF franchise, implicitly treating deutivacaftor as part of the same royalty-bearing stream.

The scale of the Vertex franchise concentrates the impact. Royalty Pharma's CF franchise is among its largest royalty streams. The company's 2024 10-K estimates royalty duration through 2039-2041 based on expected Alyftrek patent expiration, with Trikafta expected to remain on patent through approximately 2037.

An adverse outcome in the arbitration does not eliminate the CF royalty, but it materially reduces the royalty rate on what is expected to be Vertex's primary CF product through the 2030s as patients convert from Trikafta to Alyftrek. The economic exposure over the product's life is substantial.

What the Outcome Could Look Like

The arbitration is confidential and neither party has disclosed the specific contractual provisions at issue. The range of possible outcomes is correspondingly wide.

If Royalty Pharma prevails, Vertex will owe back royalties from the date of first Alyftrek sales at the higher blended rate, plus interest. The ongoing royalty on Alyftrek would increase from approximately 4% to approximately 8%. Vertex would also likely need to revisit royalty provisions on any future products incorporating deutivacaftor or other deuterated analogs of royalty-bearing compounds. The precedent would create significant caution among licensees considering deuterium switches of licensed compounds.

If Vertex prevails, the existing 4% royalty rate is confirmed. Future CF franchise royalties will decline as Trikafta patients convert to the lower-royalty Alyftrek. Royalty Pharma's CF royalty receipts, while not eliminated, would erode as the product mix shifts. The precedent would signal to the broader industry that FDA NCE classification provides a defensible basis for treating deuterated compounds as outside the scope of existing royalty agreements.

A negotiated settlement is also possible. Given the long expected duration of Alyftrek royalties and the commercial relationship between Royalty Pharma and Vertex as an ongoing counterparty, both parties have incentives to reach a negotiated resolution that provides certainty for the remainder of the royalty term. A settlement might involve a rate between 4% and 8%, a fixed payment to resolve past underpayments, or a modified royalty structure for future Alyftrek sales.

Royalty Pharma CFO Terry Coyne indicated on the Q4 2025 earnings call that the CF franchise remains an important contributor even in a downside arbitration scenario, underscoring that the company has sized its guidance and outlook to absorb a range of outcomes.

A Structural Question for the Asset Class

The Vertex/Royalty Pharma dispute is the pharmaceutical royalty market's first prominent test of whether isotopic modification creates a new compound for royalty purposes. It will not be the last.

Deuterium chemistry has produced four FDA-approved drugs as of early 2026, with additional programs in development. The technique's application is not limited to small molecules — it is being explored across therapeutic areas wherever metabolic stability improvements could benefit dosing convenience or tolerability. Each of those programs potentially involves a licensed compound that was modified through isotopic substitution, creating the same ambiguity that Vertex and Royalty Pharma are now litigating.

The broader lesson for royalty investors is that the future value of a pharmaceutical royalty depends not only on the commercial trajectory of the licensed compound but on the contractual precision with which the licensed compound was defined.

Agreements drafted in the 1990s and early 2000s — when the royalty market's primary risks were clinical failure and generic competition — were not written with deuterium chemistry, enantiomeric separation, or other sophisticated lifecycle management tools in mind. The resulting definitional gaps are systematic across the portfolio of legacy royalty interests.

The resolution of the Royalty Pharma/Vertex dispute, whenever it comes, will provide a reference point for how existing royalty agreements should interpret structural analogs of licensed compounds. In the meantime, both royalty investors and pharmaceutical companies with active deuterium programs have strong incentives to clarify the scope of their existing agreements — before the next hydrogen swap creates the next arbitration.

All information in this article was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, regulatory announcements, and financial reporting. Information may have changed since publication. This content is for informational purposes only. I am not a lawyer or financial adviser. Nothing in this article constitutes investment, legal, or financial advice.