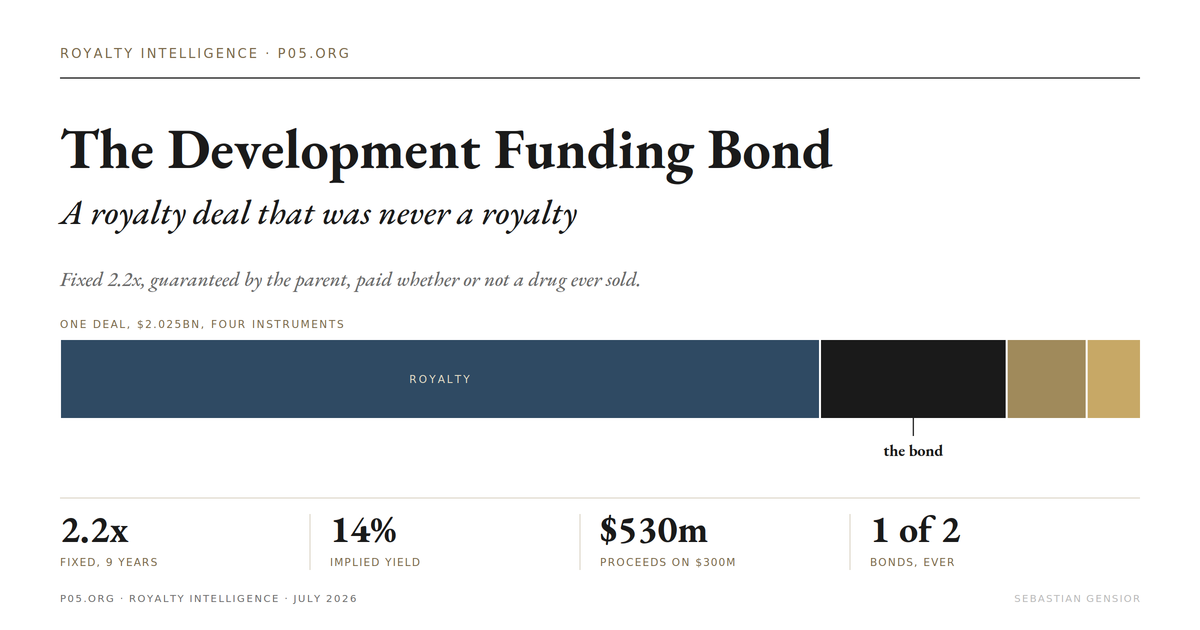

The development funding bond a royalty deal that was never a royalty

The development funding bond is a royalty deal that was never a royalty: fixed multiple, fixed schedule, guaranteed by the parent, paid regardless of sales. Why both sides chose debt over a true sale, the tax and accounting logic, and why the structure stays a category of two.

When Royalty Pharma committed up to 2.025 billion dollars to MorphoSys in June 2021, only one slice of it was a bond.

The rest was recognisable royalty finance. Royalty Pharma bought the Tremfya royalty stream, took a revenue participation right on two Constellation pipeline assets, and put in equity.

But sitting inside the package was a discrete instrument that behaved like none of those things: up to 350 million dollars of Development Funding Bonds, issued by the acquired subsidiary, guaranteed by the parent, repayable at a fixed 2.2 times whatever was drawn, on a fixed quarterly schedule, whether or not a single pill was ever sold.

That last clause is the whole point.

A synthetic royalty pays the investor only if the drug reaches the market and sells. This instrument paid on a schedule set at signing.

It was a bond wearing the language of royalty finance, and it is close to the only one of its kind. The question worth asking is not what it is, which the filings state plainly, but why anyone built it as a bond when a straight royalty was available, and why almost nobody has built one since.

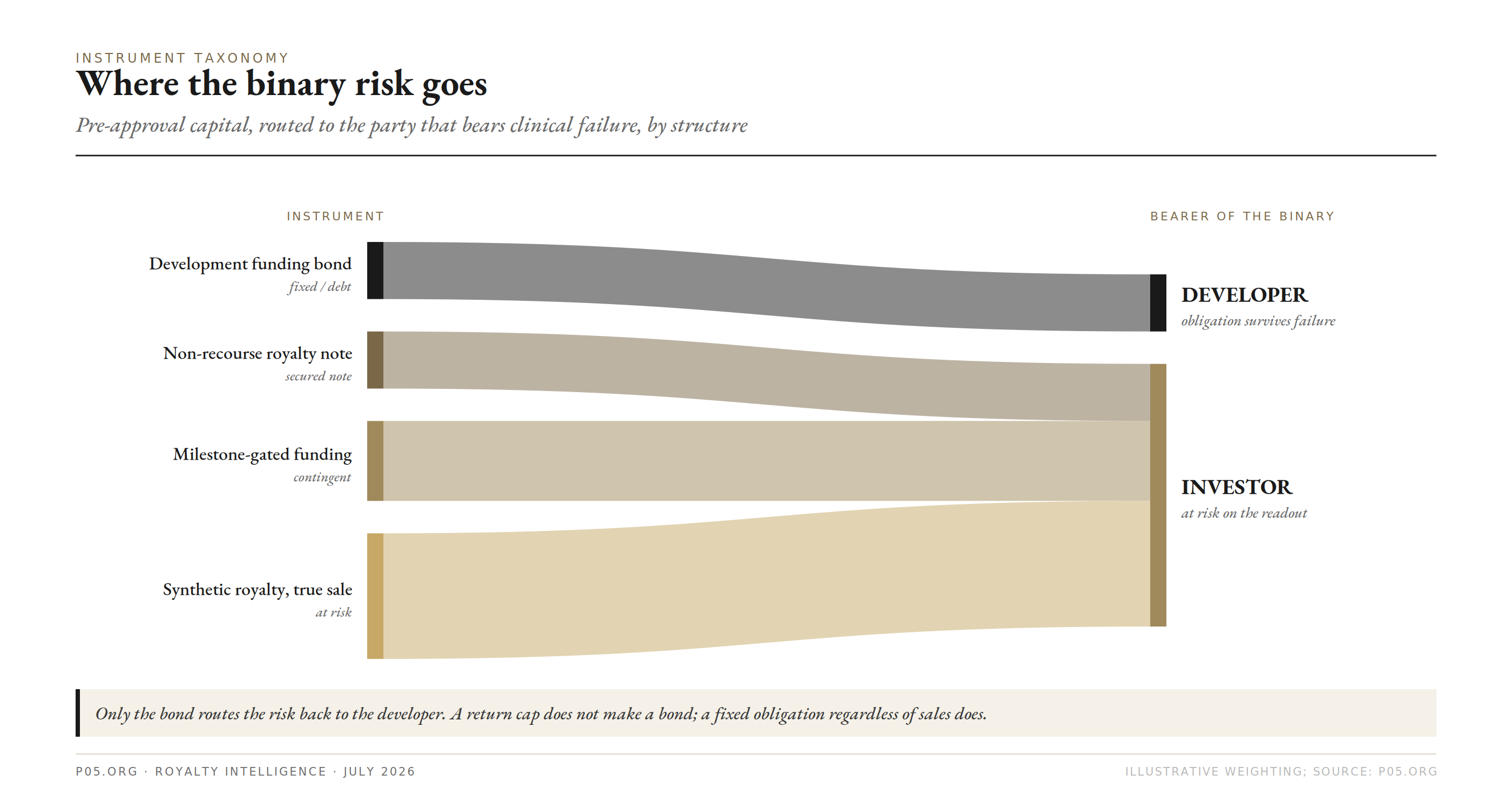

Figure 1. Pre-approval capital routed to the party that bears clinical failure. Only the development funding bond routes the binary back to the developer; the other structures leave it with the investor.

An earlier piece, Pharmaceutical Royalty Bonds, maps the four security types that share the "royalty bond" label, and places the MorphoSys instrument as one coupon archetype among the bilateral notes.

This piece does not re-run that taxonomy. It goes inside the one instrument: the purchase agreement, the reason it is debt and not a sale, and whether any other bond like it exists.

What the Purchase Agreement Says

The economics are a fixed-income instrument. The form is a bond issued under a purchase agreement, and the structure lives in the operative terms.

The provisions below come from the Development Funding Bond Purchase Agreement dated June 2, 2021, filed as an exhibit to MorphoSys's annual report.

The issuer is the acquired company, not the parent.

The agreement names Constellation Pharmaceuticals as Issuer, effective on a joinder at the merger close, with MorphoSys AG as Guarantor and Royalty Pharma USA as Buyer.

Constellation issues the bond because Constellation holds the assets the cash funds. The proceeds are covenanted to the clinical development and commercialisation of biopharmaceutical products, which is to say the pelabresib and CPI-0209 programmes that came with the acquisition.

The repayment is a fixed multiple on a fixed schedule.

Royalty Pharma was to receive 2.2 times the amount funded, quarterly over nine years, with the first payment two years after funding.

MorphoSys's interim statement frames the tenor as repayment within ten years and nine months after the first drawdown, with no repayment in the first two years.

Either way the shape is the same: a two-year holiday, then a defined annuity to a defined multiple. Nothing in it moves with Tremfya sales or with the fate of the funded pipeline.

The draw is bounded and time-limited.

MorphoSys had to draw a minimum of 150 million dollars and could draw a maximum of 350 million, over a one-year window from the July 15, 2021 merger close.

It drew 300 million dollars in September 2022.

The guarantee is of payment, not of collection.

MorphoSys AG guarantees that amounts due under the bonds will be paid in full when due, and the agreement states this is a guaranty of payment and not of collection, with the guarantor's obligations unconditional and irrespective of the enforceability of the bonds.

In plain terms, Royalty Pharma does not have to exhaust its remedies against Constellation before turning to the parent.

That single clause is what converts a claim on a clinical-stage subsidiary into a claim on the consolidated MorphoSys credit. Hold on to it; it is the reason the whole structure exists.

The granular default, security, and prepayment schedule of the bond form is redacted in the public exhibit. What is visible is enough: a guaranteed, fixed-multiple, fixed-schedule debt instrument, issued to fund an acquisition, that does not depend on any product succeeding.

Why a Bond, and Not a Straight Royalty

The natural question from anyone who does royalty finance is why either side chose this over a synthetic royalty on the same assets.

The answer is that a bond and a royalty solve different problems, and for this deal the bond solved the ones that mattered. Four reasons, and they compound.

It was acquisition financing, and acquisitions want fixed money.

The bond did not fund the development of a MorphoSys asset. It helped fund MorphoSys's 1.7 billion dollar purchase of Constellation.

Acquisition finance has a known quantum and a known closing date, and it is naturally matched by an instrument with a known repayment. A royalty, whose cash flow depends on how a pipeline performs years later, is a poor match for a purchase price due at closing.

A guarantee turns a single-asset bet into a corporate-credit bet.

This is the structural core.

A synthetic royalty is tied to a specific product's sales and is non-recourse to the parent by design. A guaranteed bond is the opposite: it is a claim on MorphoSys AG, a company with a marketed royalty base in Tremfya, which generated 1.347 billion dollars of sales in 2020.

Royalty Pharma did not have to underwrite whether pelabresib would succeed. It underwrote whether MorphoSys would be solvent, which is a different and, here, a better question.

A royalty cannot do that. The guarantee is the mechanism, and the guarantee only exists because the instrument is debt.

Fixed can be cheaper than contingent when the obligor is strong.

A synthetic royalty is priced to compensate the buyer for the chance the drug fails. When the developer has diversified, marketed cash flows and the buyer is really taking corporate credit risk, that clinical-failure premium is not warranted, and a fixed multiple is a lower implied cost of capital.

MorphoSys's own accounts imply the trade was struck at a 14 percent implied interest rate against a 6.5 percent market rate, a low-teens cost of capital that a synthetic royalty on an unapproved asset would rarely match.

Both sides wanted debt, and the accounting explains why.

The developer that wants risk transfer chooses a true-sale royalty and takes it off the balance sheet. MorphoSys wanted the opposite: it was comfortable carrying debt, and debt characterisation carried an advantage a sale did not.

MorphoSys recognised the financing as a financial liability at amortized cost using the effective interest method under IFRS 9. Because the implied 14 percent rate exceeded the 6.5 percent market rate, it carved out an off-market component of 69.0 million dollars, or 58.4 million euro, amortised to interest expense over the term.

By the end of 2023 the development funding bond alone sat on the MorphoSys balance sheet at 377.8 million euro. A liability, growing at an imputed rate: that is debt, not a disposed asset.

The true-sale-versus-secured-loan machinery, the Investment Company Act treatment, and the tax characterisation that sit behind all royalty-bond structuring are set out in the royalty bonds piece. The point specific to this instrument is narrower: MorphoSys did not attempt sale treatment. It wanted the debt.

Were There Other Bonds

The short answer is that the name is unique and the structure is nearly so.

A search of the disclosed record turns up exactly one instrument called a "Development Funding Bond," the MorphoSys one. But there is one genuine structural cousin, and drawing the line around it tells you what actually counts as a bond here.

The cousin is Cytokinetics.

In the May 2024 expansion of its collaboration with Royalty Pharma, Cytokinetics took 100 million dollars of development funding for a confirmatory Phase III trial of omecamtiv mecarbil.

The repayment terms are what make it bond-like. Per Royalty Pharma's filing, if approval is not received within the specified time frame, Royalty Pharma receives a return of 2.4 times the funding over 18 quarters; if the trial is not successful, 2.3 times over 22 quarters.

Read that again. The developer pays a fixed multiple precisely in the failure case. The obligation survives the clinical outcome.

That is the defining feature of a bond, and it is why Cytokinetics's shares fell about 20 percent on the announcement, with analysts calling the omecamtiv piece a financial burden. Investors understood they were looking at debt, not a royalty.

Now the instructive contrast, the deal that looks similar and is not a bond.

In November 2021 BioCryst took 350 million dollars from Royalty Pharma and OMERS against Orladeyo. It has the surface features people associate with these structures: a two-year holiday before the first payment, and a capped total return of 1.425 or 1.550 times.

But the payments are a royalty of 7.5 percent on annual net sales up to 350 million dollars, 6 percent above that, and nothing over 550 million. If Orladeyo does not sell, OMERS is not paid.

The cap makes it look like a bond; the sales-contingency makes it a synthetic royalty.

That is the exact line. A return cap is not what makes a bond. A fixed obligation regardless of sales is.

So the census: one named development funding bond, one close cousin with genuine fixed-payment downside, and a large field of capped, tranched, milestone-gated instruments that borrow the vocabulary of debt while staying contingent.

The bond, properly defined, is a category of essentially two.

The Bond Was One Layer of Four

The reason the bond is rare on its own is that it works best as one component of a blended deployment, which is how Royalty Pharma used it.

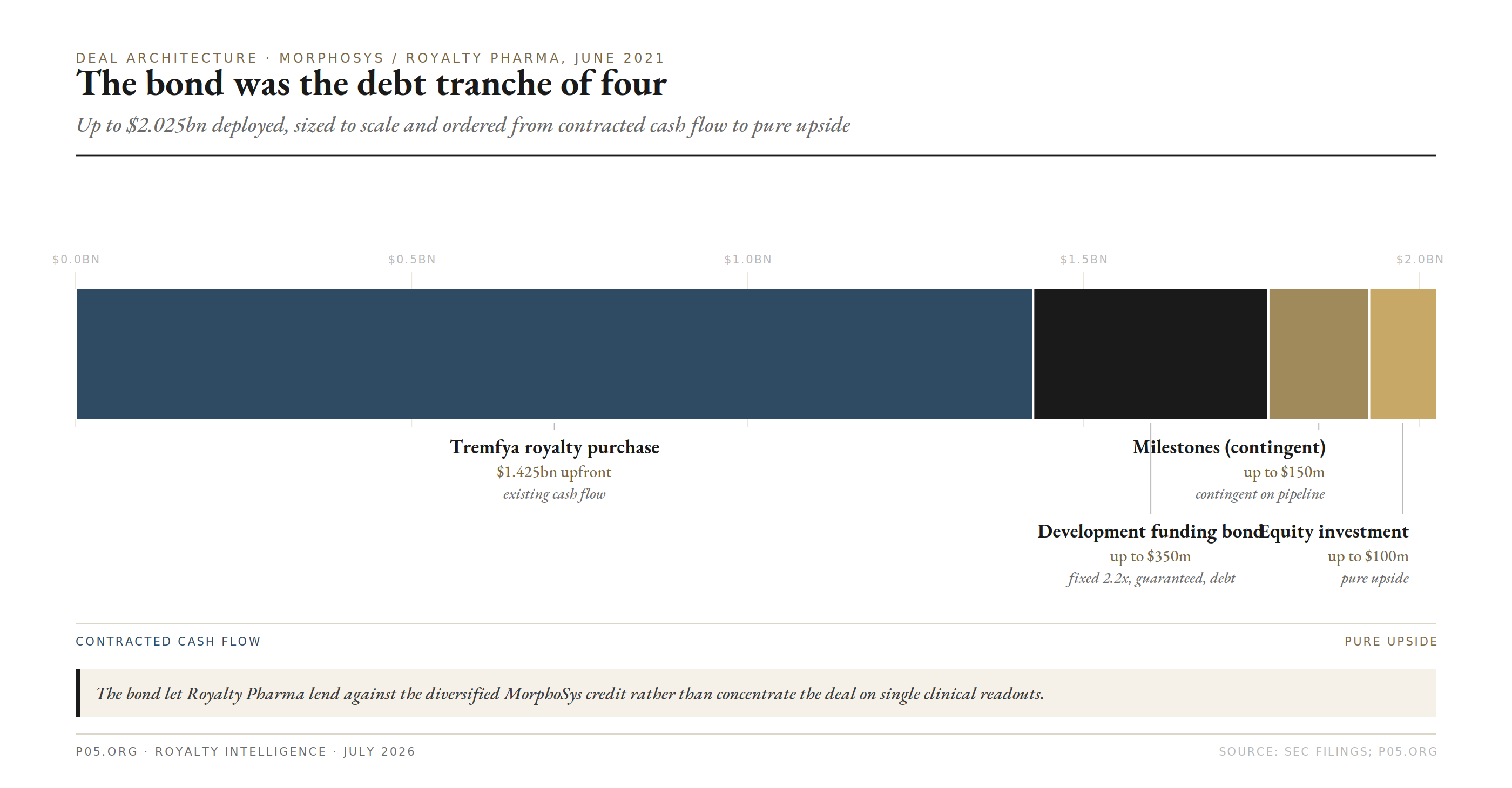

Figure 2. The four instruments in the MorphoSys package, sized by dollars and ordered from contracted cash flow to pure upside. The bond is the debt tranche, between the marketed Tremfya royalty and the contingent pipeline and equity pieces.

The package layered four instruments.

The Tremfya royalty purchase was an existing, marketed cash flow, the safest piece. The revenue participation right, 3 percent of future net sales of pelabresib and CPI-0209, was a contingent bet on the acquired pipeline. The equity was pure upside.

And the bond was the fixed, guaranteed, debt layer in the middle, the piece that let Royalty Pharma scale the total commitment to 2.025 billion dollars without making the whole deployment a wager on single clinical assets.

Seen this way, the bond is not competing with the synthetic royalty. It is doing a job the royalty cannot.

It lets a large capital provider lend against the diversified corporate credit while separately buying the specific royalty and revenue-participation exposures it actually wants. Pull the bond out and replace it with more royalty, and you have concentrated the whole deal on a handful of clinical readouts.

The bond exists because a blended deployment needs a credit-backed debt layer, and a royalty cannot be that layer.

The Payoff: When the Fixed Form Wins

The logic is clearest with the arithmetic of the two structures on the same asset base.

Take a developer with a marketed product throwing off a stable royalty and a pipeline asset in Phase III, wanting 300 million dollars.

It has two offers. A synthetic royalty priced for clinical risk asks for a share of the pipeline asset's future sales targeting, say, a 2.8 times return, paid only if the asset is approved and sells. A development funding bond asks for a fixed 2.2 times over nine years, guaranteed by the parent, paid regardless.

If the pipeline asset fails, the royalty pays nothing and the developer keeps its cash. That is the developer's insurance, and the reason the royalty is priced high.

But if the developer is confident, and the parent is strong enough that the payments are really corporate credit, the fixed bond is cheaper: 2.2 times over nine years is a lower implied cost of capital than 2.8 times contingent, and the developer is not paying a large premium to insure a risk it does not think it carries.

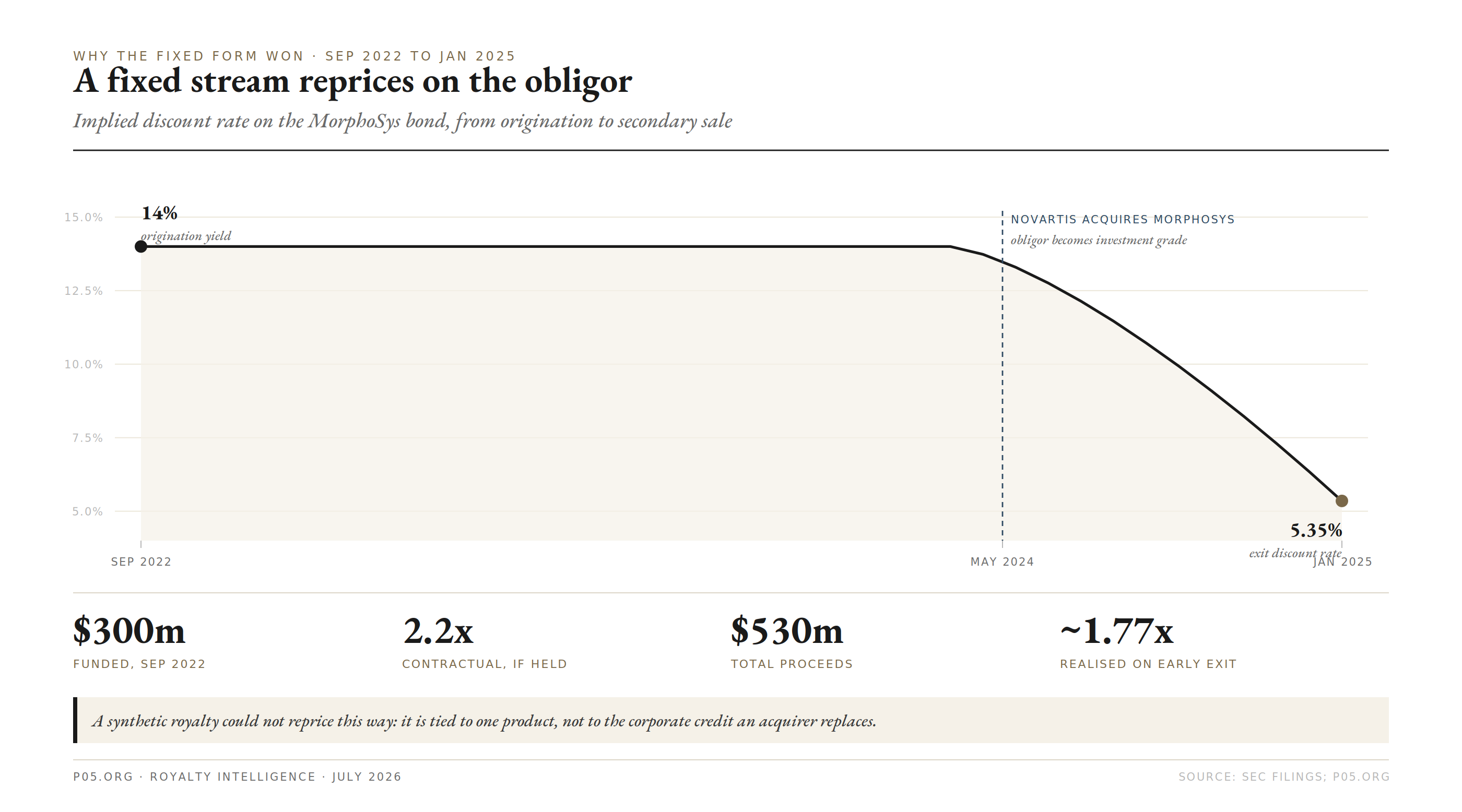

Figure 3. The implied discount rate on the MorphoSys bond, held at 14 percent from origination, then repricing to a 5.35 percent exit once Novartis converted the obligor to investment grade.

The MorphoSys outcome is the worked example in the real world.

The bond was struck at an implied 14 percent. In February 2024 Novartis agreed to acquire MorphoSys for 68.00 euro per share, about 2.7 billion euro, and the fixed obligation of a mid-cap biotech became, in substance, an obligation of an investment-grade pharma.

A fixed stream reprices entirely on the obligor's credit, and the credit had just been transformed.

In January 2025 Royalty Pharma sold the remaining payments for 511 million dollars, 530 million in total proceeds on the 300 million investment, at a 5.35 percent discount rate.

The realised multiple was about 1.77 times against the 2.2 times available on hold, the price of exiting early. But the exit was possible only because a fixed instrument reprices on credit and a royalty does not.

A synthetic royalty on pelabresib would not have converted when the parent was acquired. The bond did.

Where This Sits in Royalty Finance

The development funding bond is not a royalty instrument, and that is exactly why it is useful to people who do royalty finance. It occupies the one seat a royalty cannot fill.

For an originator, the menu is a spectrum of contingency, and the bond sits at the far, fixed end.

A synthetic royalty transfers the binary and stays contingent. A milestone-gated funding agreement releases capital as risk retires. An approval-gated senior secured loan, the debt leg of the Revolution Medicines structure, is debt that refuses to fund pre-approval risk at all.

The development funding bond is the only one that puts fixed money to work before approval on the strength of the obligor. It is therefore the only one that requires a strong obligor to make sense.

For a buyer, the bond is a specialty position rather than a repeatable strategy.

The underwriting is a corporate-credit analysis wearing royalty-deal clothing, and the return depends on holding a fixed stream to term or catching a credit-conversion event.

A development-stage book is built on contingent synthetics and approval-gated loans. The fixed-payment bond is the rare line item reserved for the case where a strong obligor will pay for certainty.

The through-line with the rest of this site is the recurring gap between an instrument's legal form and its economic substance.

A pre-funded warrant is a share that does not count as one until it does. A synthetic royalty is a sale that the accounting treats as a loan.

The development funding bond completes the set from the other direction: it is the piece of a royalty deal that was never a royalty at all.

The Risks the Structure Carries

The fixed form removes clinical risk from the investor and hands the developer a set of exposures the royalty would not have created.

The obligation survives failure.

This is the mirror image of the royalty's appeal. A developer that takes a development funding bond, or the Cytokinetics-style development funding, owes the fixed payments whether or not the funded asset works.

Cytokinetics owes up to 2.4 times its development funding in exactly the scenario, non-approval, where a royalty would have owed nothing. For a single-asset company that is a dangerous liability, prudent only where the parent can service it independent of the asset.

It is leverage, with covenants and priority.

Because the instrument is debt, it sits in the capital structure with the rights of debt: guarantees, potential acceleration, and a claim that ranks ahead of equity.

A synthetic royalty structured as a true sale does not add leverage in the same way. A developer choosing the bond is choosing to lever the balance sheet.

The value swings with credit, not with the drug.

For the investor, a fixed stream is a credit instrument, and its mark moves with the obligor's credit and with rates, not with the asset.

That cuts both ways. MorphoSys converted favourably, but a fixed stream against a deteriorating biotech credit would have repriced the other way, with no sales upside to offset it.

Liquidity depends on the obligor being wanted.

The MorphoSys stream traded because Novartis had made it an investment-grade credit. Absent such an event, a fixed-payment bond from a single-name biotech is an illiquid, credit-sensitive position with no natural secondary bid.

A buyer should underwrite it as hold-to-term and treat the credit-conversion exit as upside, not a base case.

What Each Side Should Ask

For the developer and its advisers:

Is this financing meant to transfer risk, or to raise cheap certain capital? If risk transfer, a true-sale synthetic royalty is the tool, and a bond is the wrong one.

Can the parent service the fixed payments independent of the funded asset? A guarantee converts single-asset risk into corporate credit, which is a strength only if the corporate credit is real.

Are we comfortable adding leverage with its covenants and priority, rather than a non-recourse royalty that stays off the debt stack?

For the investor:

Is the real underwriting a corporate-credit analysis rather than a clinical one? A guaranteed fixed bond is a bet on solvency, not on approval.

Where does the fixed multiple sit against a contingent royalty on the same asset? The bond wins only where the obligor is strong enough that the clinical-failure premium is not warranted.

What is the realistic exit? Assume hold-to-term, and treat a credit-conversion event as the upside case that made MorphoSys work, not the plan.

The development funding bond is the instrument a royalty-finance house reaches for when the job is not actually a royalty.

It funds an acquisition or a trial with fixed money, leans on a parent guarantee to make single-asset risk into corporate credit, and books cleanly as debt on both sides because both sides wanted debt.

That it is nearly unique is not a gap in the market waiting to be filled. It is a statement about where the fixed form clears: only where the obligor is strong enough to make certainty cheaper than contingency.

Read the purchase agreement rather than the headline, and the reason a royalty-finance deal contains a bond is in the guarantee.

All information in this article was accurate as of the research date and is derived from publicly available sources including SEC filings, issuer annual reports, accounting standards guidance, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, accounting, tax, or financial advice. The author is not a lawyer, accountant, tax adviser, or financial adviser.