The Royalty Token That Never Paid: Tokenized Pharma Cash Flows Against the Howey Wall, and the Value That Went to Equity Instead

A decade in, no token has paid a pharmaceutical royalty. When decentralized science finally produced a commercial deal, the money went to equity holders, which is exactly where securities law sends it.

Every eighteen months someone announces that pharmaceutical royalties are about to go on-chain. The pitch is stable: an approved drug throws off a contractual revenue stream, that stream is illiquid and locked inside a dozen specialist balance sheets, and a token will fractionalize it, price it in a public secondary market, and pay holders programmatically.

The observation underneath is correct. There is no functioning secondary market for royalty interests, and the asset class is gated. What the pitch omits is that none of the three hard problems in a royalty deal, which are securities characterization, payment origination, and enforcement in default, is a problem a token solves. Two of them a token makes worse.

This time the argument does not have to rest on theory, because the evidence is finally in. The decentralized-science movement has spent five years and raised hundreds of millions of dollars building exactly the tokenized-IP machine the pitch describes. As of July 2026, the count of tokens that have paid a holder a share of pharmaceutical or medical revenue is zero.

More instructive than the zero is where the money went when the science actually worked. When two decentralized-science-funded programs signed real commercial deals in 2025, the proceeds flowed to the equity holders of ordinary corporations, and the token holders who funded the research received nothing. That outcome is not a failure of execution. It is the securities laws working exactly as designed, and it is the whole answer to the tokenized-royalty question compressed into two deals.

This piece takes the on-chain royalty apart the way the minimum guarantee came apart, by refusing the marketing noun and asking what the instrument actually is, what actually shipped, and who actually got paid. It stays with pharmaceuticals, healthcare, and medtech, and it treats the decentralized-science experiments covered here last year as the prior generation whose results are now legible.

The through-line is one reframing. Tokenization changes the ledger on which ownership is recorded. It does not change what is owned, who is obligated, or how the obligation is discharged.

Two different things called the same thing

Start by separating the funding token from the cash-flow token, because they sit at opposite ends of the only axis that matters, which is proximity to an actual stream of royalty dollars.

The funding-and-governance token is what the decentralized-science world actually built, and it does not tokenize a royalty at all. Molecule pioneered the IP-NFT, a non-fungible token wrapping a research licence and its data on-chain, then the IP Token, a fungible ERC-20 minted from the IP-NFT through a Tokenizer contract.

What an IPT conveys is governance over an IP pool, meaning votes on licensing terms, data access, and research direction, not a contractual claim on drug revenue. The distinction is not pedantic. The next section shows it is the entire ballgame.

The cash-flow token is the object of the pitch: a token whose holder is entitled to a pro-rata slice of the revenue a product generates. The historical control case is music, and it is worth one paragraph because it hit the wall in the open a decade ago.

Royalty Flow, a Royalty Exchange spin-out, acquired 25 percent of the Eminem catalogue royalties paid to FBT Productions for 18.75 million dollars and tried to sell fractional interests to the public through a Regulation A+ offering, in which subscribers bought an equity interest entitling them to future dividends. The offering never closed, Nasdaq pulled its provisional listing, and it was never on a blockchain.

It is the clean control: fractionalize a royalty for the retail public and you are selling securities, and the registration path grinds you down before any token layer is reached. Everything that has happened in pharma and medtech since is a re-run of that lesson with a chain bolted on.

The funding token can, with careful drafting, be argued out of security status. The cash-flow token cannot. And the reason the funding token is safe is precisely that it does not pay you anything, which is the finding the whole ecosystem now confirms in the negative.

What actually materialized: five years, and no royalty

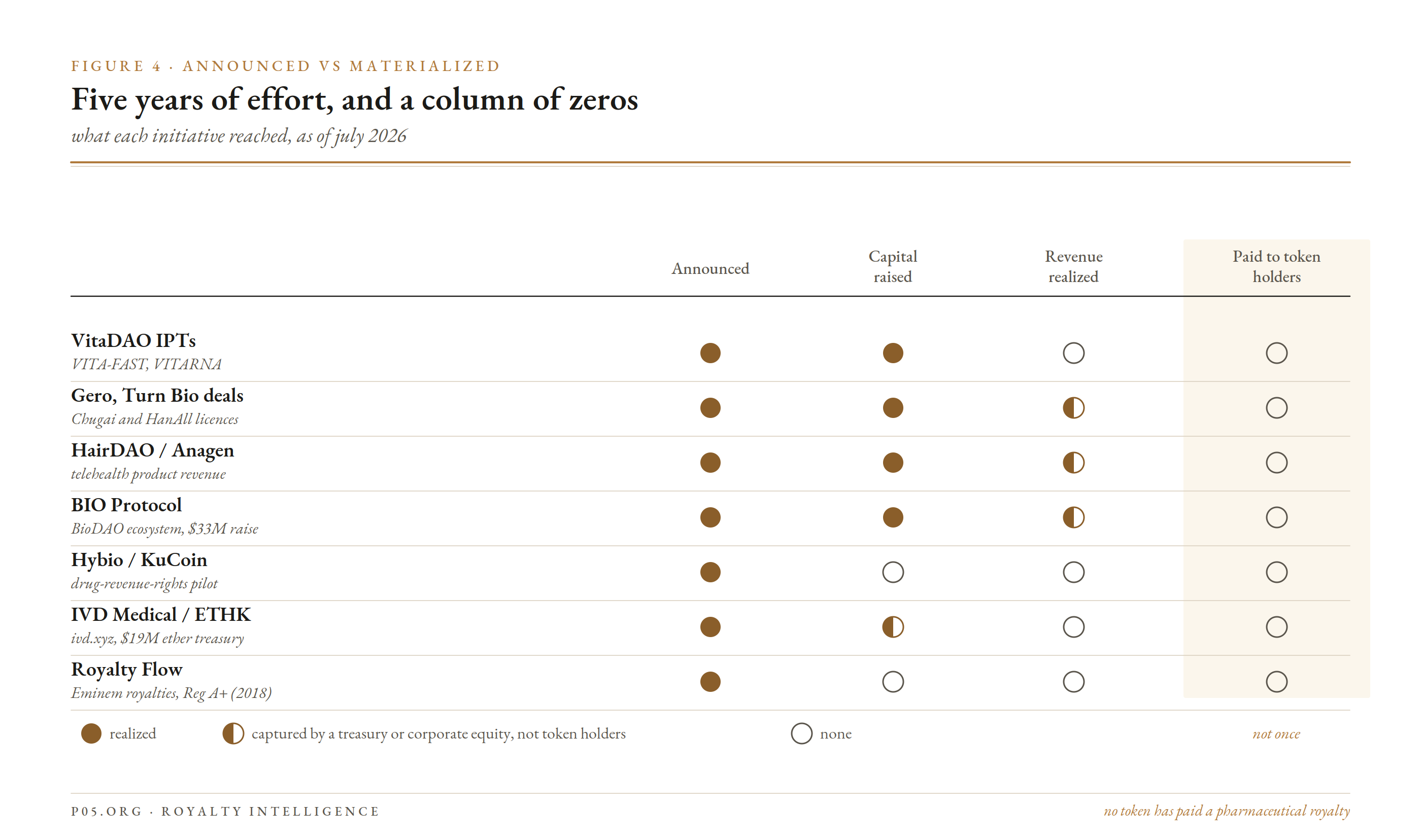

Set the press releases aside and hold every attempt to one test. As of July 2026, has any decentralized-science DAO, or any pharma or medtech issuer, distributed royalty income, licensing revenue, dividends, or any IP-derived payout to its token or IPT holders? The answer, across the entire field, is no. Not once.

Begin with the confession, because the projects say it themselves. VitaDAO, the flagship, is unambiguous that its token is not an economic instrument: its own guide states that holding VITA grants governance access and does not give holders ownership rights to any of the IPs. The independent trackers put it more bluntly still, describing VITA as a token that functions exclusively as a governance token without dividend rights or profit sharing.

BIO Protocol, the Binance-backed meta-layer that raised more than 33 million dollars in its December 2024 genesis and skims roughly seven percent of each affiliated BioDAO's tokens, routes any IP or product proceeds back to a DAO treasury, not to holders. The IPTs do the same. There is no royalty pipe in any of these instruments, by construction.

Raised, carried, distributed: three numbers, kept apart

The confusion in most coverage comes from collapsing three numbers that must be separated: money raised, treasury value carried, and revenue distributed.

VitaDAO has pooled north of ten million dollars, deployed roughly 4.7 million into 31 projects, and carries a treasury reported at 55.8 million dollars, of which 38 million is booked as IP assets.

That last figure is a carrying valuation, not cash, and none of the three numbers is a dollar of revenue reaching a token holder. A royalty underwriter knows this discipline instinctively: the upfront a fund raises, the mark it carries an asset at, and the coupon it actually pays are three different things, and only the third is a royalty.

When the science worked, the money went to equity

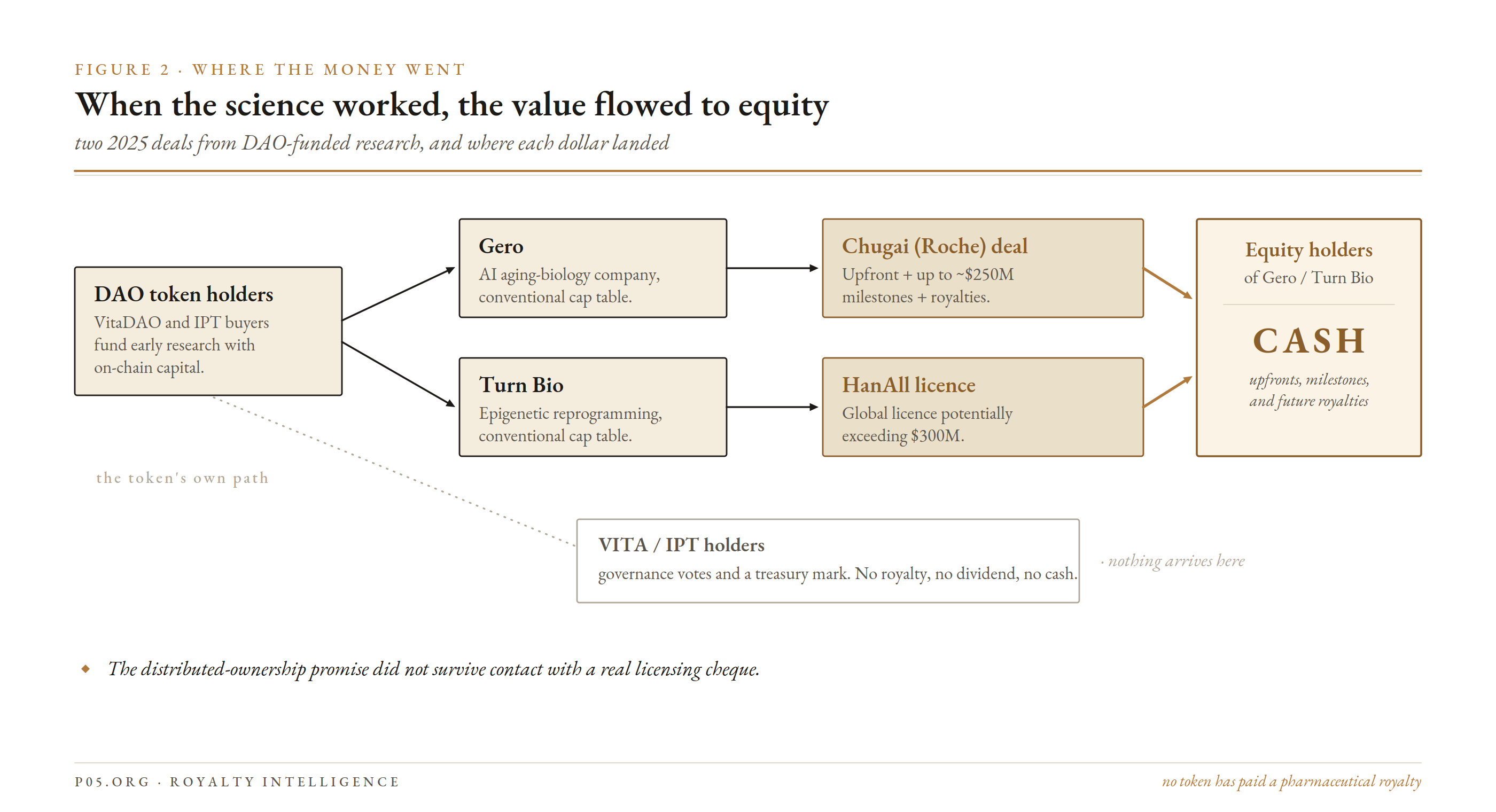

Now the finding that resolves the entire debate. In 2025 two VitaDAO-backed programs produced exactly the commercial success the model was built to generate, and in both the value flowed to corporate equity, not to the token.

Gero, an AI-driven aging-biology company VitaDAO funded early, signed a research and licensing agreement with Roche's Chugai in July 2025 carrying an upfront payment plus up to roughly 250 million dollars in milestones plus royalties on any launched product, a deal some coverage framed as potentially exceeding a billion dollars on a peak-royalty scenario.

Turn Biotechnologies, another portfolio company, signed a global licence with HanAll Biopharma potentially exceeding 300 million dollars for the first of several planned products.

Both counterparties pay Gero and Turn Bio, private companies with conventional cap tables. Not one dollar of either deal was routed to VITA holders, and VitaDAO itself has conceded that any royalty-sharing terms with the token remain undisclosed, which is the polite way of saying there are none. The science worked. The token was not standing where the money landed.

This is the empirical heart of the matter, so it is worth stating without hedging. The decentralized-science thesis was that tokenizing IP lets the crowd that funds research share in its upside. When the upside finally arrived, it went to the equity holders of Gero and Turn Bio, exactly as it would have in a standard venture deal, and the tokens captured governance minutes and a treasury mark. The distributed-ownership promise did not survive contact with a real licensing cheque.

When the science worked, the value flowed to equity. The licensing cash from Chugai and HanAll reaches the equity holders of Gero and Turn Bio. The tokens that funded the research receive governance votes and a treasury mark, and no cash.

What did ship, credited precisely

What did materialize is real and should be credited without inflation. Decentralized science is a functioning early-stage funding and commercialization engine.

VitaDAO co-funded a rapamycin-and-exercise Phase 2a trial that completed its data-collection phase and counts clinical-stage portfolio companies such as the senolytics developer Rubedo. HairDAO, the most commercial of the BioDAOs, filed the first DAO scientific patent and spun out Anagen, a US telehealth clinic whose novel hair-loss treatments have driven real, fast-growing product revenue. VitaDAO sells a spermidine supplement, VD-001, for modest treasury income.

But note what each of these is. The clinical progress belongs to portfolio companies, not to the DAO-owned IPTs. The flagship tokenized assets, VITA-FAST for autophagy and VITARNA for Artan Bio's suppressor-tRNA program, remain preclinical, years from an IND. The product revenue that does exist, Anagen's and VD-001's, flows to a corporate cap table or a DAO treasury, and never to a holder as a royalty.

Even Molecule now concedes the gap and is engineering around it in the wrong direction for the pitch. Its Protocol V2, reframing the stack as IP real-world assets with an equity bridge and a revenue-distribution phase, sends any eventual revenue to KYC-verified equity holders in a corporation, not to ordinary token holders, and as of July 2026 no project has executed a V2 revenue distribution at all. The pioneer's own roadmap ends at equity, which is the tell the closing section returns to.

What each initiative actually reached. Announcements and capital raises are common; the column that matters, cash paid to token holders, is empty in every row.

| Effort | Venue | What was announced | What materialized by July 2026 |

|---|---|---|---|

| VitaDAO / VITA and IPTs | US, global | Community shares in tokenized IP upside | Governance only; explicitly no dividends; no royalty ever paid |

| VITA-FAST, VITARNA, Matrix Bio | US, global | Fractional ownership of drug IP | Token sales funding preclinical research |

| Gero / Chugai, Turn Bio / HanAll | corporate | Proof DeSci science can reach pharma | Real deals; value to company equity, nothing to VITA |

| HairDAO / Anagen | US | Community-owned therapeutics | Real product revenue, to corporate and treasury, not holders |

| BIO Protocol and BioDAOs | global | On-chain science economy | 33M dollar raise; proceeds to treasuries, not holders |

| Hybio / KuCoin | Hong Kong | China's first drug-revenue-rights token | A letter of intent; no token, no distribution |

| IVD Medical, now ETHK Labs | Hong Kong | ivd.xyz platform tokenizing healthcare assets | A 19M dollar ether treasury buy; platform never launched |

| Royalty Flow (music, precedent) | US | Retail fractions of Eminem royalties | Offering pulled; never closed |

The offshore pilots that stayed announcements

The live attempts to tokenize an actual drug or device revenue stream, as opposed to early IP, are all offshore, and none reached a payout. That geography is not incidental, and the next section explains why.

The closest thing to a pharma royalty token is a mainland-Chinese pipeline routed through Hong Kong. In August 2025 the Shenzhen-listed peptide maker Hybio and the exchange KuCoin signed what they billed as China's first RWA pilot, with future income rights from innovative drug R&D as the underlying asset, specifically Hybio's GLP-1 peptide programs.

Read the instrument. It was only a strategic cooperation letter of intent to explore and advance a pilot, and nearly a year later Hybio's own newsroom, which runs through conventional 2026 licensing deals and an FDA approval, records no token, no issuance, and no distribution. KuCoin's intended role, providing the on-chain mapping and the revenue distribution, was itself the tell: a centralized exchange in the middle doing the valuation and the payout. And the underlying asset was future income on a pipeline, which is development funding wearing a royalty's clothes.

The medtech case is a treasury trade dressed as a platform. The Hong Kong-listed diagnostics group IVD Medical, since renamed ETHK Labs, bought roughly 19 million dollars of ether through HashKey and announced ivd.xyz, an Ethereum platform to tokenize healthcare assets, plus a planned IVDD stablecoin settlement layer.

What actually materialized was the ether purchase and a company rename. The tokenization exchange never launched, the stablecoin was never issued, and the ivd.xyz domain now hosts a corporate investor page oriented to AI-healthcare acquisitions rather than a live venue. What shipped was a crypto treasury with staking plans. The tokenized medtech royalty remained a slide.

The reckoning is stark. A decade after Royalty Flow, the count of tokens actually paying fractional holders a share of pharmaceutical or medical revenue is zero, and RWA.xyz, which tracks the on-chain real-world-asset market, does not carry a pharma-royalty category at all: the roughly 26 billion dollars of tokenized RWA is Treasuries, money funds, private credit, gold, and real estate.

Set that against the off-chain royalty market it was supposed to disrupt, where Royalty Pharma alone is worth around 26 billion dollars and closed a 250 million dollar non-recourse royalty-backed note on Zymeworks' Ziihera in March 2026 using entirely conventional structures. The commentary around the Hong Kong deals concedes the reason in passing, admitting that medical IP is highly intangible, non-standardized, tied to future clinical-trial success rather than existing cash flows, and subject to dual financial and pharmaceutical oversight. Those are the problems, stated by the people selling the solution.

Why the money went to equity: the Howey wall did not move in 2026

The empirical fact that value flows to equity and never to the token is not an accident of these particular deals. It is securities law expressing itself, and the 2026 regulatory reset that the industry read as a liberation did nothing to change it for royalties.

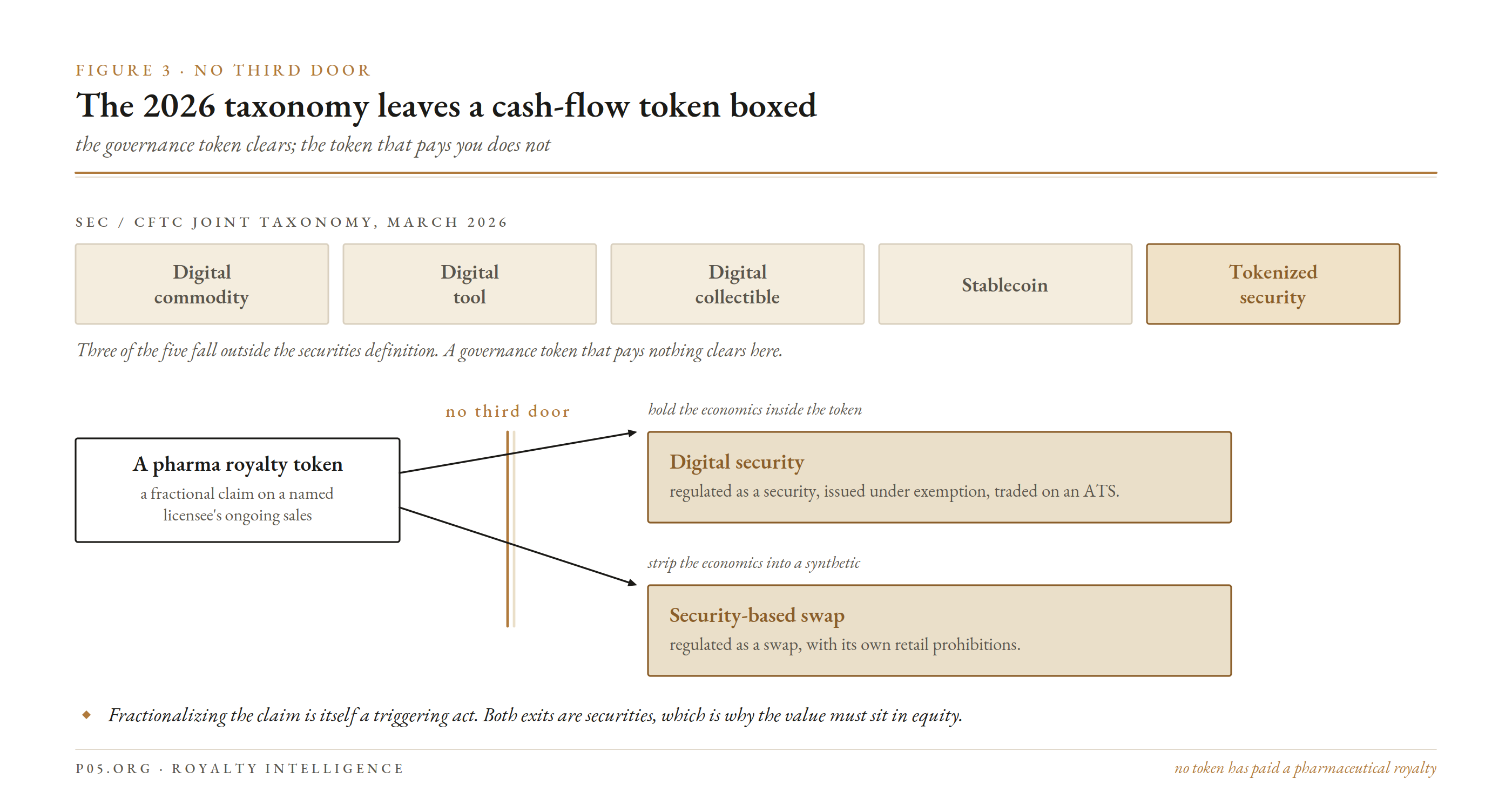

The facts first. On 17 March 2026 the SEC, joined by the CFTC, issued a joint interpretive release applying Howey to crypto assets and establishing a five-part taxonomy, superseding the 2019 staff framework and formalizing what the courts had already forced, that the transaction, not the token, is the unit of analysis. Chairman Atkins had trailed this in his November 2025 Project Crypto speech.

Three of the five categories, digital commodities, tools, and collectibles, fall outside the securities definition. For a governance token that pays nothing, this is genuine relief, and it is exactly why VITA, BIO, and the IPTs can breathe: they were engineered to carry no economic claim, so they clear the taxonomy.

For a cash-flow token it changes nothing, because the fifth category is the trap. Tokenized securities remain securities. The January 2026 staff statement that the industry keeps quoting without reading held that securities, however represented, remain securities, that the format used to record ownership does not alter the applicability of the federal securities laws, and that economic reality, not the label, governs. The practitioner shorthand, new plumbing, same rules, is exact.

Run a royalty token through Howey without the crypto distraction and it is an easy case. There is an investment of money, in a common enterprise (holders share pro-rata in one stream), with an expectation of profit derived from the efforts of others, and the others are unusually identifiable, because a pharma royalty depends continuously on a named licensee's manufacturing, marketing, and defence of the product.

There is no path to the sufficiently-decentralized argument that rescues a network token, because the value of a Zejula or a Trelegy royalty is umbilically tied to a specific company's execution. The guidance also warns from both sides: fractionalizing a claim is itself a triggering act, and stripping the economics out into a synthetic pushes toward security-based swap treatment, with its own retail prohibitions. Hold the economics inside a fractional claim and it is a digital security; strip them out and it is a swap. There is no third door.

No third door. Three of the five taxonomy categories fall outside the securities definition, and a governance token clears them. A token that pays a royalty has only two exits, digital security or security-based swap, and both are securities.

Which is precisely why the Gero and Turn Bio money went to equity. A well-advised structure has exactly one compliant place to put a claim on a company's economic success, and that place is equity or debt issued under an exemption to qualified holders, not a freely trading token.

Molecule's own lawyers wrote this down. Their March 2026 submission to the SEC Crypto Task Force, the Coin-to-Company model, engineers the token to convey no claim on income and channels all investment exposure into equity through Regulation D, S, CF, A, or Rule 701. The empirical outcome and the legal design are the same fact seen twice. The value flowed to equity because equity is where the securities laws require a claim on a firm's success to sit, and the token was built, deliberately, to stand somewhere else.

The question the whitepapers never reach: who actually pays?

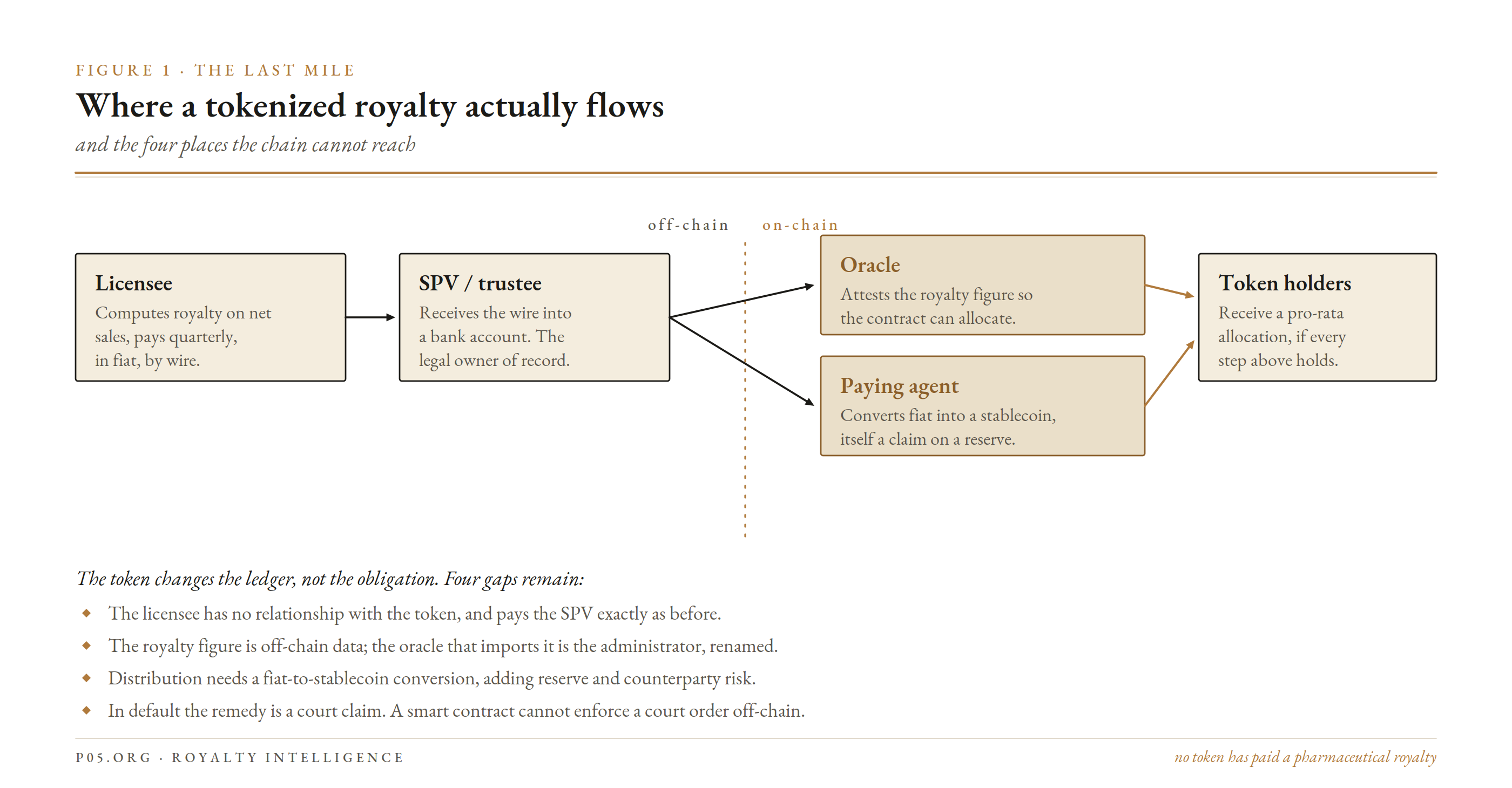

Grant, for argument, a fully compliant royalty security-token. The deeper problem is mechanical, and it is the one every on-chain royalty pitch declines to work through. A pharmaceutical royalty is a contractual claim paid by a specific counterparty through a specific process, and the token touches none of it.

Trace the dollars. A licensee sells product, computes a royalty on net sales under a contract with defined deductions and a quarterly reporting lag, and remits to whoever owns the stream, historically an SPV, into a bank account, in fiat. Tokenization inserts nothing into that chain. The licensee has no relationship with the token, does not know the holders exist, and pays the same SPV it always paid.

For the money to reach a holder, three off-chain acts must still occur, none of which a smart contract can perform: the SPV must receive the wire, someone must convert fiat to a distributable on-chain asset (a stablecoin, itself a claim on an off-chain reserve), and an oracle must report the royalty amount so the contract can allocate.

ffiThe last mile. The token changes the ledger, not the obligation. The licensee still pays the SPV off-chain, an oracle must attest the royalty figure, a paying agent must convert fiat to stablecoin, and in default the remedy is a court claim a smart contract cannot enforce.

Each is a point of trust that reintroduces the exact intermediation the token was meant to remove. The oracle problem is the load-bearing wall: smart contracts are deterministic and cannot natively access off-chain information, so they depend on oracles to import the royalty report, and a corrupted feed triggers erroneous settlement even when the chain is sound.

The royalty amount is not observable on-chain. It is a number produced by a licensee's finance function, sometimes disputed, sometimes restated, always trailing an audit right, and someone must attest to it. The Hong Kong pilots made this concrete even in the abstract: Hybio's design put KuCoin, an exchange, in charge of the mapping and distribution, and ETHK's ran settlement off the issuer's own ether treasury. Neither reached a live payout, but the architecture already tells you the token was never going to remove the intermediary. It would have renamed it.

Enforcement is worse, and Chainlink of all sources says so plainly: a smart contract can move tokens, but it cannot enforce a court order off-chain. If the licensee underpays, disputes the deduction base, or stops paying because the product is withdrawn, the remedy is a contract claim litigated in court by an entity with standing.

A dispersed set of pseudonymous token holders has neither the standing nor the coordination to run an audit or a lawsuit, which is the governance-fragmentation problem flagged in the DeSci piece wearing a financial hat. Tokenizing the interest does not perfect it, does not grant a security interest in the receivable, and does not give holders a seat at the audit. It splinters the claimant.

This is why the sharper voices concluded the whole originate-off-chain-then-tokenize model adds little. The a16z view for 2026 is that debt should be originated on-chain, not originated off-chain and tokenized, because wrapping a pre-existing off-chain claim leaves all the servicing and enforcement cost in place and adds an oracle on top.

A pharma royalty is the most off-chain claim imaginable, created by a licence negotiated years earlier, computed by a corporate finance team, and paid through the banking system. There is no version of it that originates on-chain. The token is always the wrapper a16z warns about, and the payment it promises is a promise about a wire it cannot see, made by a party it cannot compel, converted by an intermediary it cannot remove.

The market has voted with its capital: the on-chain RWA stock is overwhelmingly Treasuries, money funds, and private credit, cash flows that are sovereign-certain or already run through an administrator that can serve as the trusted attestor. Even there, the IMF notes that tokenized lending has not grown meaningfully because lenders lean on overcollateralization for want of counterparty information. Pharma royalties offer none of those comforts.

The true-sale overlay the token cannot escape

For readers who came through the sale-versus-loan analysis, a second layer survives tokenization untouched, because it turns on risk allocation and recourse, not on the ledger.

Tokenized private credit uses a twin structure precisely because real-world assets require a legal wrapper for enforceability: an SPV holds the asset and the token references a claim on the SPV. So the SPV does not disappear, it becomes mandatory, and with it every recharacterization factor from the paper world.

If the token embeds a hard minimum or a repurchase right to make it marketable, that recourse threatens sale treatment exactly as in a paper deal. If the SPV holds the licence, section 365(n) and the security package still govern recovery in bankruptcy, and a smart contract has no role in a court's treatment of an executory contract. The DAO-personhood problem compounds it: a naively tokenized royalty pool can expose its holders to general-partnership liability, the opposite of the limited, tradable exposure the pitch promised.

Net of all this, tokenizing a royalty imports the entire off-chain legal architecture, the SPV, the perfection, the true-sale opinion, the bankruptcy analysis, and then adds an oracle, a stablecoin conversion, and a transfer-agent question on top. It is additive complexity over a securitization, not a replacement for one.

What a compliant structure actually looks like

The compliant path is not a clever way around the securities laws. It is the decision to stop looking for one, and the striking thing is that the market has already been running it in plain sight.

A compliant royalty token concedes digital-security status from the first line of the offering memo and rebuilds the traditional apparatus on-chain:

- Issuance under an exemption, not a retail sale. Reg D 506(c) to accredited investors or Reg S offshore is the realistic base case; the Reg A+ retail path is what broke Royalty Flow.

- A registered transfer agent maintaining the record on distributed ledger. The January 2026 statement expressly contemplates ownership recorded in the transfer agent's file using DLT. The chain is a bookkeeping method, not a bearer instrument.

- Secondary trading confined to a registered ATS, with transfer restrictions and holding periods enforced at the token level, the opposite of free permissionless trading.

- KYC on every holder, because a security cannot trade to anonymous wallets, which forecloses the composability that was half the point.

- An SPV, an oracle, a paying agent, and an audit right, unchanged from the paper deal, because the payment still originates off-chain.

Each of those requirements strips out a feature that made the token attractive. What is left is a restricted instrument that trades on a permissioned venue to verified holders.

At which point the honest question is what the token adds over the structure a royalty originator already knows: a Luxembourg compartment issuing rated or unrated notes into a private placement with a trustee, a paying agent, and a servicer. The compartment does the tranching, the bankruptcy-remoteness, and the eligibility the token must reproduce anyway, inside a settled regime with a functioning secondary market among the institutions that actually buy royalty paper.

The token's marginal benefit is 24/7 settlement and programmable distribution once the fiat has already been converted and attested, which is real but modest, and it is bought at the cost of oracle risk, stablecoin-reserve risk, and a transfer overlay that removes the liquidity that justified the exercise. For a sub-50-million-dollar stream, the overhead is difficult to earn back.

Two footnotes close the loop.

The offshore route the Hong Kong efforts attempted is not the exception that disproves this, it is the same trade with the regulator swapped out, and it did not even get built. Hong Kong's virtual-asset framework permits a product US law would treat as an unregistered security, which is why the mainland pipelines went there, but the permission is jurisdictional, not structural: the token still needs the SPV, the valuation, the attestor, and the paying agent, and still cannot reach US investors without pulling the whole apparatus back inside Regulation S or D.

And the decentralized-science pioneers have already conceded the destination. Molecule's V2 ends at equity for KYC-verified holders, and the Gero and Turn Bio proceeds went to equity in practice, because equity issued under an exemption is the one place securities law lets a claim on a firm's success sit. The compliant structure is not a novel token. It is the structure the market already uses, which is why Royalty Pharma keeps writing conventional notes and the tokenized version keeps not shipping.

Verdict

The recurring dream of the freely traded, self-paying pharma royalty token fails on three independent grounds, and the 2025 to 2026 evidence tightened all three.

On securities law, the cash-flow token is a digital security, and the taxonomy says so twice, in the tokenized-securities statement and in the rule that fractionalizing a claim is itself a triggering act. The thaw that freed governance tokens does not touch a token whose value is a named licensee's ongoing sales. The proof is in where the money goes: when decentralized-science science finally sold, the proceeds went to equity in Gero and Turn Bio, because equity is the only compliant home for a claim on a company's success, and the tokens that funded the work received governance minutes and a treasury mark.

On payments, the question was never approached. A royalty is paid by a counterparty with no relationship to the token, through a wire the chain cannot see, converted by an intermediary the design cannot remove, and reported by an oracle that is the trusted administrator renamed. Tokenization does not originate the payment, does not perfect the claim, and cannot enforce it, which is why the on-chain market is Treasuries and money funds and the single-name pharma royalty exists only as a Hong Kong letter of intent and an ether treasury purchase.

On structure, the token imports the entire off-chain securitization and adds oracle, stablecoin, and partnership risk on top, then hands back a restricted instrument on a permissioned venue. That is a Luxembourg compartment with extra steps and a worse secondary market.

The clean way to hold all of it: after five years, hundreds of millions raised, real clinical progress, real patents, and two genuine pharma licensing deals, the number of tokens that have paid a holder a pharmaceutical or medical royalty is zero, and the number that will under current law, absent conceding they are securities and rebuilding the whole apparatus, is also zero.

The people closest to the problem have concluded that the token is for community and the security is for cash, and that the two must never be the same instrument. Their own deals proved it. Before you ask how to put a royalty on-chain, ask who pays it, in what currency, on what trigger, and who sues when they stop. Answer those and you will find you have specified a securitization, and the chain is the least interesting part of it.

The royalty was always the security. The payment was always off-chain. And when the money finally moved, it moved to equity, which is exactly where the law was always going to send it.

All information in this report was accurate as of the research date and is derived from publicly available sources including SEC and CFTC interpretive releases and staff statements, company and counterparty press releases, DAO and protocol disclosures and governance documentation, SEC filings, court opinions, regulatory and professional-services guidance, academic and multilateral-institution literature, and financial news reporting. Self-reported treasury, valuation, and deal figures have been distinguished from realized cash where possible. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, tax, or financial advice. The author is not a lawyer or financial adviser.