The Minimum Guarantee, Disaggregated: Floors, Puts, and the Sale/Loan Boundary in Healthcare Royalty Finance

A minimum guarantee is a written put. Where it sits on the sale-to-loan boundary sets the accounting, tax and bankruptcy outcome of a healthcare royalty deal.

Four different instruments hide under one phrase. Each sits at a different point on the sale/loan boundary, each triggers a different accounting, tax, and bankruptcy result, and each is really a written put whose value the market still prices unevenly.

Ask three royalty principals what a minimum guarantee is and you get three answers, because the phrase covers at least four distinct instruments that behave nothing alike. A minimum annual royalty in a university licence and a true-up that hands a revenue-interest investor a floored IRR are both called minimum guarantees, and they sit at opposite ends of the only axis that matters here: the distance from a true sale to a secured loan.

Where a given floor sits on that axis determines whether the seller books an upfront gain or a liability with imputed interest, whether the upfront is a capital receipt or borrowed money for tax, and whether the buyer owns an asset or holds an unsecured promise when the seller files.

This piece takes the phrase apart. It separates the four instruments, prices the floor as the written put it actually is, walks the recharacterization boundary that decides accounting and bankruptcy outcome, and then asks the question the sell side too often skips: whether a floor improves the buyer's position at all, or merely swaps asset risk for counterparty risk. Everything is kept to pharmaceuticals and healthcare, where the volumes are largest and the structuring most developed.

The through-line is a single reframing. A minimum guarantee is not a term, it is a short option position, written by whoever stands behind the floor. Read it that way and most of the confusion resolves, because you stop asking what the guarantee promises and start asking what it costs, who wrote it, and what happens to it in default.

Four instruments, one phrase

Start by refusing the collective noun. The following four things are all called minimum guarantees, and conflating them is the source of most bad structuring conversations.

The licence minimum (GMR or MAR). Written by the licensee in favour of the licensor, inside the underlying licence, long before any financier appears. A University of California licence taken by Cepheid required a minimum annual royalty payable even when earned royalties fell short, creditable against earned royalties until consumed.

NIH and PHS licences run the same way, with a nonrefundable minimum annual royalty creditable against earned royalties, and a University of Missouri licence describes it plainly as a payment in advance of royalties yet to accrue. This floor is diligence collateral, not financing. It matters to a downstream buyer only because it sets a contractual worst case on the stream being acquired, one step upstream of the monetization.

The minimum return, or true-up. Written by the company selling the royalty in favour of the investor, inside the financing. This is the floor that debt-ifies. The cleanest disclosed example is the Liquidia revenue interest financing with HealthCare Royalty, where aggregate payments to HCRx are capped at 175% of amounts advanced, but Liquidia must make a true-up payment if HCRx's internal rate of return is below a threshold when the cap is reached, 16% on newer tranches and 18% on older ones.

A true-up keyed to a minimum IRR is a guaranteed return in the literal sense: the asset's cash flows are topped up out of the company's pocket until the investor clears a floored yield.

The scheduled minimum, or fixed amortization. Written into the instrument itself as fixed payments that fall due on a calendar rather than on sales.

The same Liquidia agreement carries a modified fixed payment schedule and a one-time fixed payment that was deferred rather than waived, and REGENXBIO's limited-recourse royalty bond with HealthCare Royalty carries a principal amount and accrued interest, which is scheduled debt service by another name. A calendar payment is the hardest floor of all, because it does not even wait for the shortfall to be measured.

The milestone calibrated as a floor. Written as contingent upside but set so far in the money that it is functionally certain. When Theravance sold its residual Trelegy royalty to GSK, it separately held 150 million dollars in Trelegy milestones from Royalty Pharma requiring, in its own words, minimal to no growth over the prior year to be achieved.

Compare a genuine upside milestone, such as the Tysabri milestones of 250 and 400 million dollars payable only if sales exceeded set levels. Same label, opposite economics: one is a near-certain floor dressed as upside, the other is real optionality. The milestone-as-floor is the sell side's favourite device precisely because it delivers downside protection to the buyer while, if drafted carefully, preserving sale characterization.

| Instrument | Written by | Protects | Typical form | Sale/loan lean |

|---|---|---|---|---|

| Licence minimum (GMR / MAR) | Licensee | Licensor | Creditable annual floor | Upstream of the financing |

| Minimum return / true-up | Seller | Investor | Top-up to a floored IRR | Loan-leaning |

| Scheduled minimum | Seller | Investor | Calendar-based fixed payment | Loan |

| Milestone-as-floor | Payer | Investor | In-the-money contingent payment | Sale-preserving |

The rest of this piece is about the middle two rows, because those are the ones that move an instrument across the boundary.

The floor is a written put

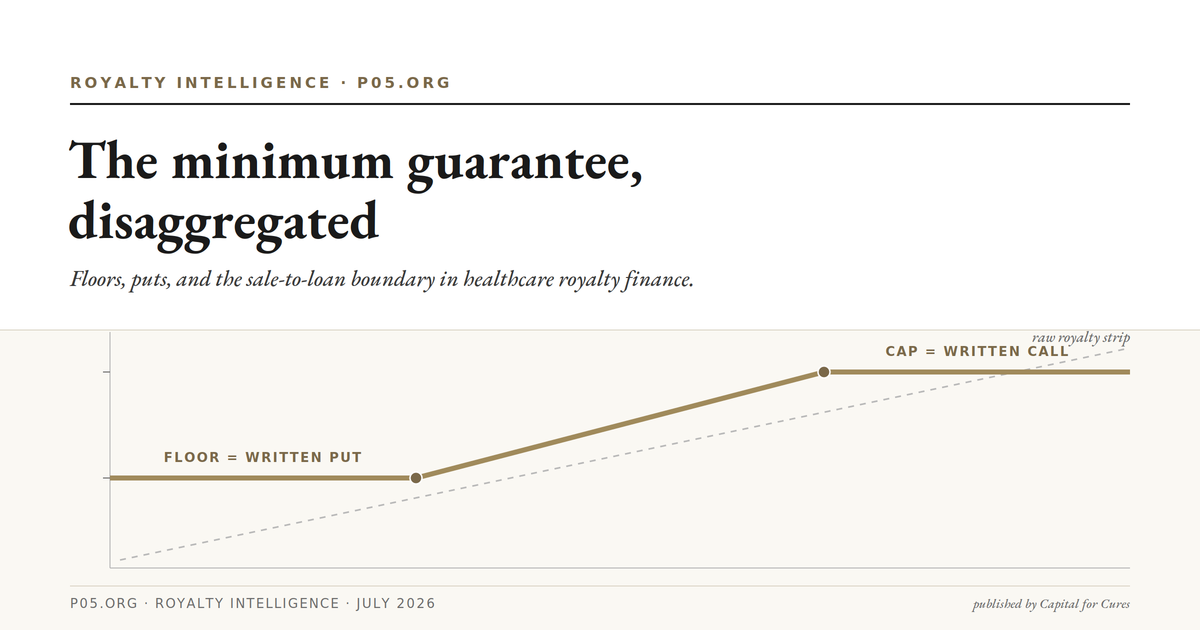

The most useful way to hold all four instruments at once is to stop treating the floor as a promise and start treating it as an option leg.

A financed royalty with both a cap and a floor is a collar on the realized return. The investor is long the raw royalty strip, short a call struck at the cap, and long a put struck at the floor. The seller holds the mirror: long the call it wrote away above the cap, short the put it wrote to create the floor.

The minimum guarantee is that put. The Liquidia structure is a textbook collar, the 175% cap is the written call and the IRR true-up is the written put, with the raw revenue interest sitting between them.

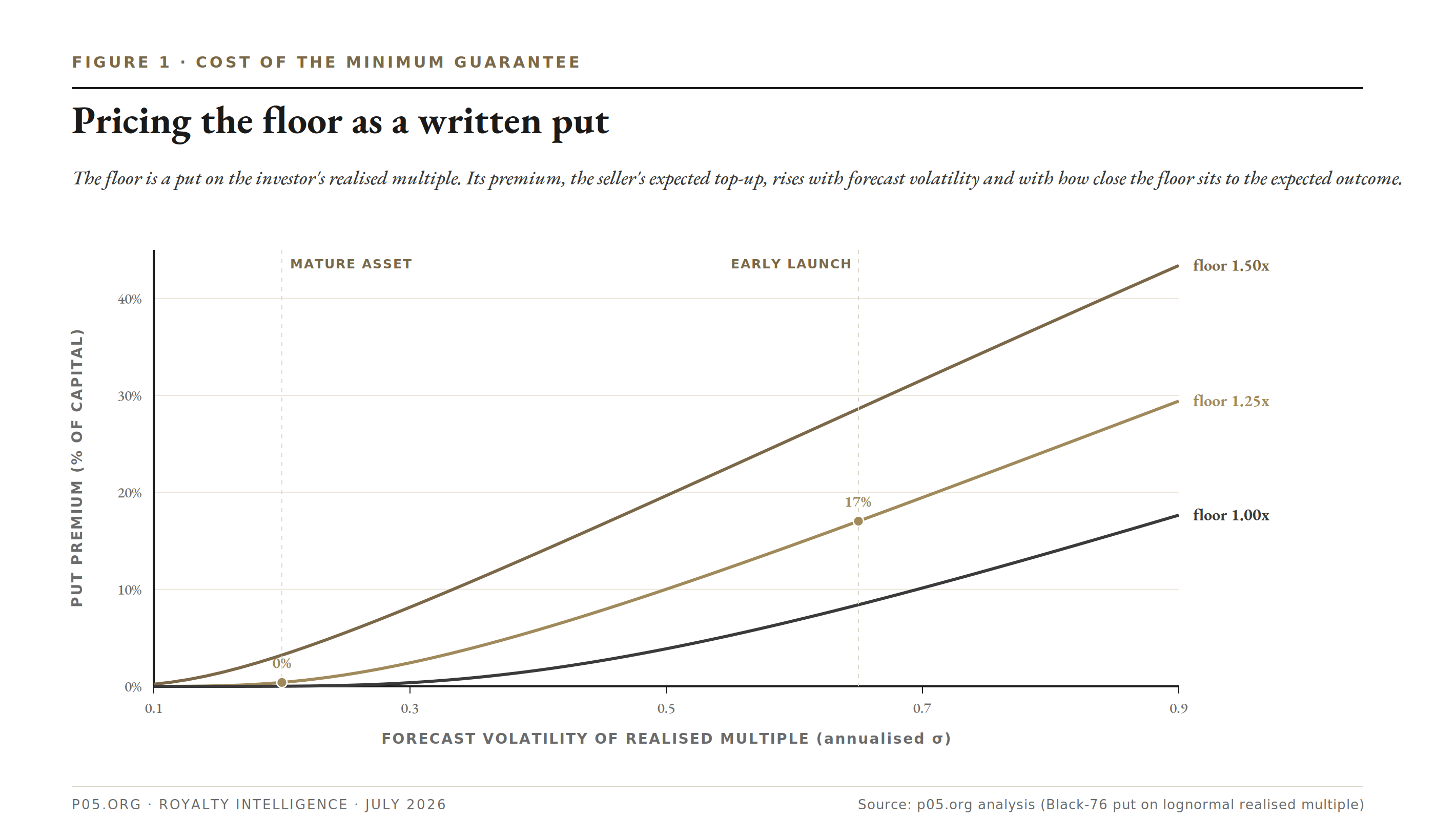

Once the floor is a put, its price follows the usual variables, and this is where the market's intuition is uneven. The value of the written put rises with the volatility of the sales path, with its moneyness relative to expected sales, and with term. That single fact explains the two poles of current practice.

Figure 1. The minimum guarantee priced as a put on the investor's realised multiple (expected 1.80x). The premium, the seller's expected top-up, rises with forecast volatility and with how close the floor sits to the expected outcome.

At the de-risked end, a floor set at or below an already-cleared sales base is a deep out-of-the-money put with almost no value. That is exactly why the Theravance milestone could be calibrated to require minimal to no growth: on a mature product like Trelegy, the sales distribution is tight and the floor is cheap to grant, so the seller hands over meaningful downside protection at trivial cost to itself.

At the early-launch end, forecast dispersion is wide, as the launch-forecasting literature has documented repeatedly, so a floor anywhere near the expected case is a valuable put. The seller either surrenders a large slice of upfront value to write it, or the investor prices a high effective yield for the protection, which is one reason development-stage synthetic deals lean so heavily on caps rather than floors.

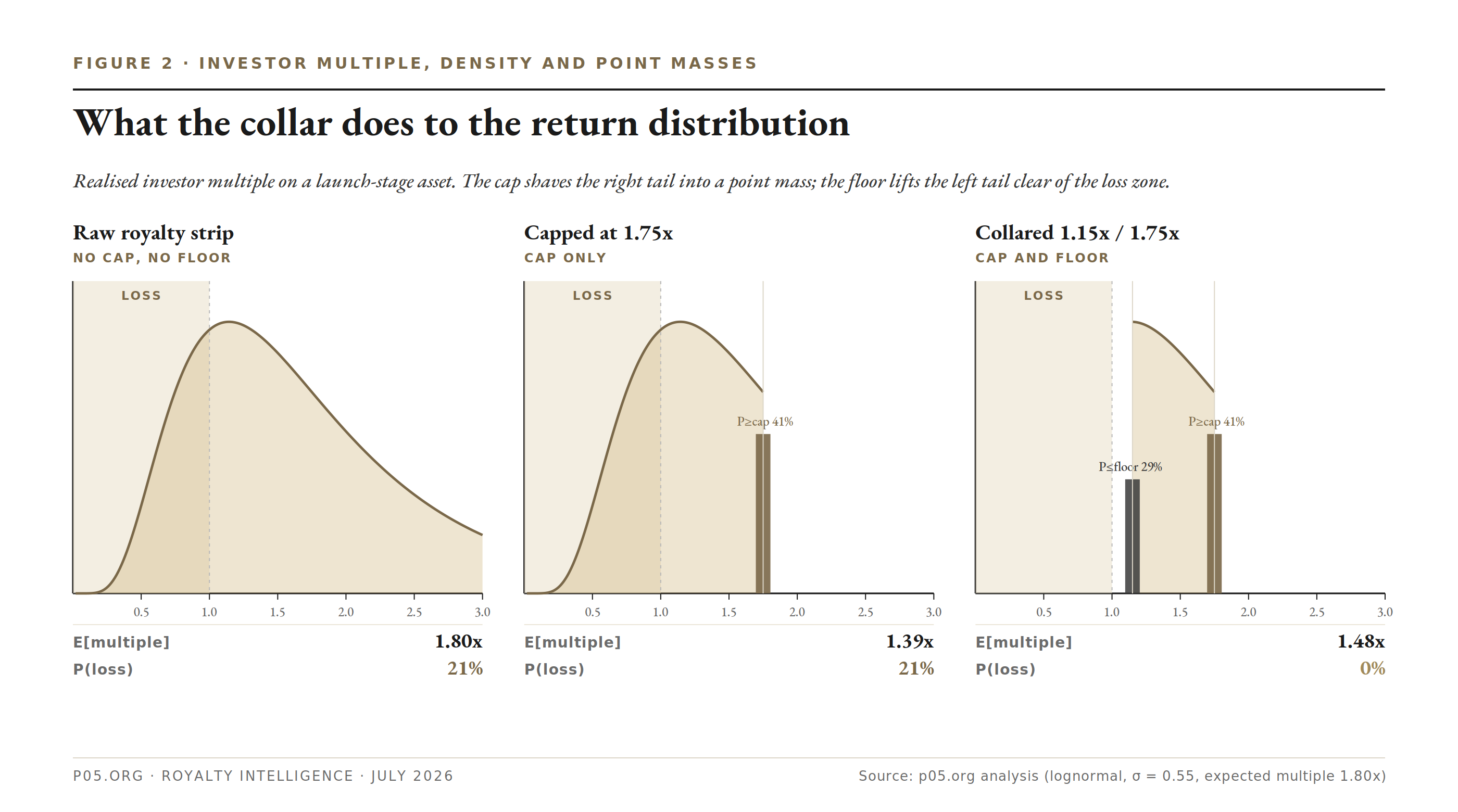

Figure 2. Realised investor multiple on a launch-stage asset (lognormal, sigma 0.55). The cap shaves the right tail into a point mass; the floor lifts the left tail clear of the loss zone, moving expected value and loss probability with it.

The practical lesson for underwriters is to price the two legs separately. The market has become fluent at valuing the cap, a median return cap around 2.0 to 2.25 times is now standard, but it still tends to treat the floor as a binary drafting point rather than as a written option whose premium should be visible in the discount rate or the upfront.

A floor granted on a volatile launch asset is not a free comfort clause. It is a short put, and it should be reserved and priced like one.

Hard, soft, and the recharacterization boundary

The floor's option value is only half the story. The other half is what the floor does to the legal character of the deal, and here the distinction that governs everything is hard versus soft.

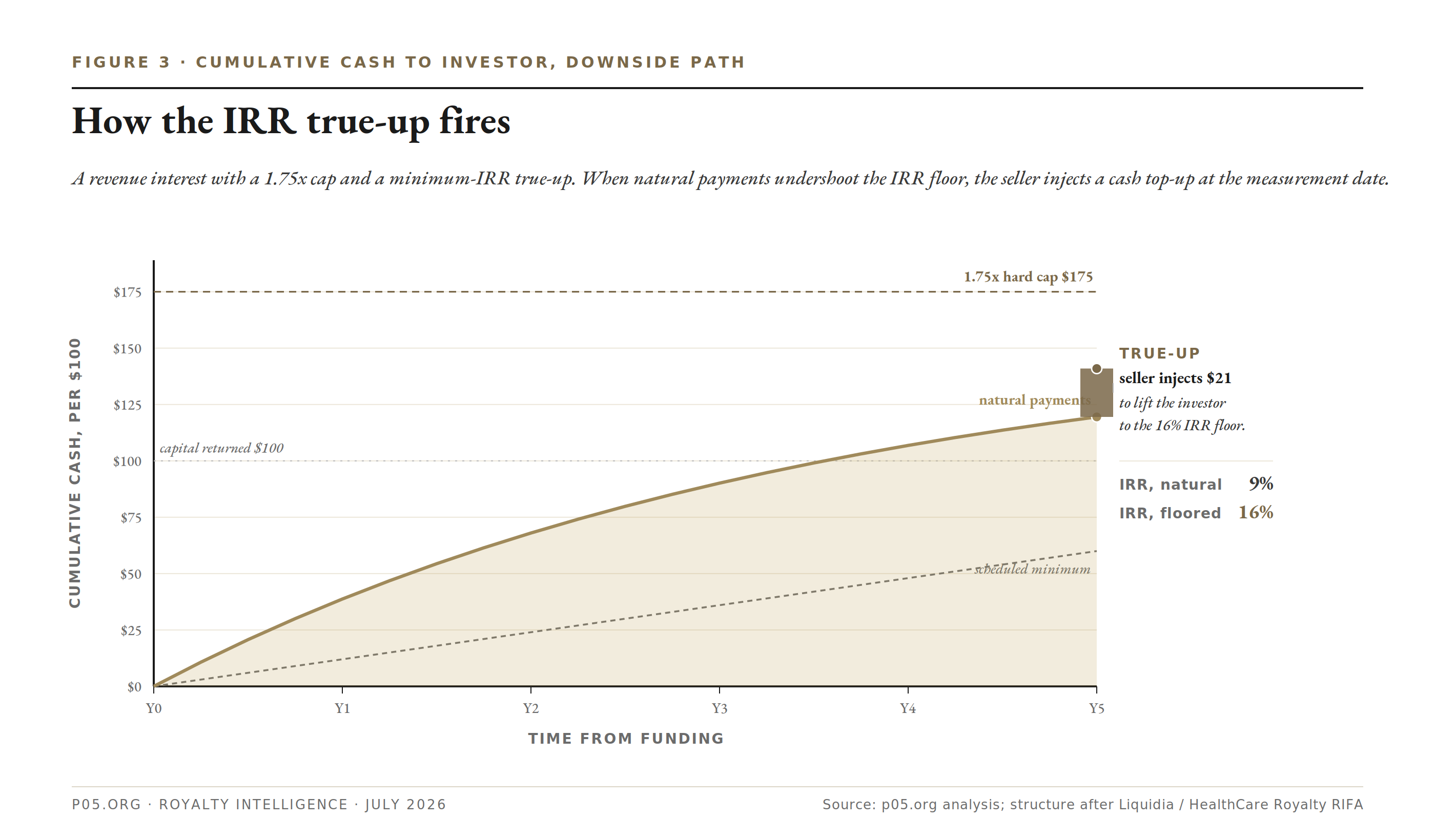

A soft minimum improves the investor's return only from the asset itself. It extends the tail, raises the cap, or grants payment priority until a target multiple is reached, but every dollar still comes out of product cash flows. Risk of ultimate shortfall stays with the investor. A hard minimum reaches past the asset to the company's balance sheet: a cash true-up, a repurchase obligation, a scheduled payment that falls due regardless of sales.

Risk of shortfall shifts back to the seller. The Liquidia IRR true-up is a hard minimum. A tail extension that only lengthens the period over which the same royalties are collected is soft.

Figure 3. A revenue interest with a 1.75x cap and a minimum-IRR true-up. When natural payments undershoot the IRR floor, the seller injects a cash top-up at the measurement date. Illustrative, after the Liquidia / HealthCare Royalty structure.

The reason this line matters is that a hard minimum is what tips a monetization from true sale to secured loan, with consequences that survive the parties' stated intent. Courts run a fact-intensive, multi-factor recharacterization test, and the eight factors reduce to how risk is allocated: recourse to the seller or a guarantor, retention of a repurchase option, the buyer's power to alter pricing, retention of excess collections, and the conduct of the parties.

As the case law puts it, calling a transaction a true sale does not make it one, and where credit recourse sits with the seller a court is likely to find a secured loan regardless of the label. A hard minimum is recourse. It is the single feature most likely to collapse the sale.

This is why the structuring is a genuine tension rather than a preference. Bolstering the buyer's recovery in a seller bankruptcy argues for exactly the features, top-up payments, automatic put or acceleration rights, fixed minimums, that maximise the claim, and those same features are what defeat true-sale treatment.

The market's response is to hedge both ways: to keep the minimum soft where sale treatment is the priority, and where a hard floor is unavoidable, to protect the buyer through structure rather than promise. In practice that means a backup security interest in the royalties, and often in the underlying IP and regulatory approvals, plus a bankruptcy-remote SPV holding the licence, so that a recharacterized sale still leaves the investor as a perfected secured creditor rather than an unsecured one.

Two healthcare-specific wrinkles sharpen the point. First, the bankruptcy protections differ by structure. In a traditional monetization the licensee holds section 365(n) rights to retain the licence so long as it keeps paying, which shelters the assignee even if the seller rejects the agreement.

In a synthetic royalty the buyer has no such shelter, so it depends more heavily on the security package, which raises the stakes on getting characterization right.

Second, the case record is now live, not theoretical: the Athenex and Infinity bankruptcies put royalty-monetization treatment and contract rejection directly in front of the courts, which is why the current generation of agreements is drafted with the recharacterization factors explicitly in mind.

The accounting fork the floor decides

For the seller, the presence and hardness of the minimum is the variable that selects among four completely different accounting outcomes. This is where the floor stops being abstract.

The starting point is that sale accounting is the exception, not the rule. As PwC puts it, getting to sales accounting for a royalty monetization is difficult and rarely achieved, particularly where the seller retains the IP underlying the royalties. Most healthcare royalty sellers therefore land in one of three non-sale outcomes, and the minimum is what pushes them between them.

The first non-sale outcome is deferred income: the upfront is recognized over time as the royalties are paid, with imputed interest under the units-of-revenue approach. The catch is that puts and calls typically preclude deferred income treatment, and a hard minimum is functionally a put. So the moment a cash true-up or repurchase enters, deferred income is usually off the table.

The second is a financial liability under the debt guidance, accounted for with the effective interest method and complicated by embedded-derivative analysis and cash-flow modelling for the interest accrual. This is the outcome that produces the non-cash royalty revenue and non-cash interest expense gross-up familiar from monetizer financials. A hard floor lands here.

The third applies only to development-stage funding and is the one most often mis-analysed. Under ASC 730-20, R&D funding is not a liability if, at inception, the R&D risk is substantive and success is not yet probable, so that genuine risk transfers to the investor. But that conclusion breaks the instant a floor appears: the same guidance records a liability where it is probable the entity will repay regardless of outcome, or where there is a severe economic penalty for non-repayment, or intent to repay.

A minimum guarantee is precisely a mechanism that makes repayment probable regardless of outcome, so it converts an at-risk R&D funding arrangement into debt. This is not hypothetical: Ligand recorded a one-time charge in connection with a royalty financing to fund a Phase 3 study, accounted for as an R&D funding arrangement under ASC 730-20, which is the same regime read from the funder's side.

| Seller outcome | What triggers it | P&L consequence |

|---|---|---|

| Sale accounting | Genuine risk transfer, IP usually not retained | Upfront gain |

| Deferred income | Sale of future revenue, no puts/calls or hard minimum | Revenue recognized over time, imputed interest |

| Financial liability | Hard minimum, put, repurchase, retained risk | Debt with effective-interest expense, embedded derivatives |

| R&D funding (ASC 730-20) | Development-stage, substantive risk transfer | Not a liability, unless a floor makes repayment probable |

The single sentence to carry away: a hard minimum almost always forces the transaction out of sale and deferred-income treatment and into liability accounting, with all the interest-expense drag that implies.

The tax line, which need not agree with the accounting

Tax characterization runs a parallel sale-versus-loan test, and it can land differently from GAAP on the same facts.

The tax question is whether the upfront is proceeds of a sale or the principal of a loan, and the doctrine turns on whether the buyer bore genuine risk of non-payment. The governing intuition comes from cases well outside pharma but directly on point: in Stranahan the sale of future dividends was respected as a sale because a real risk existed that the dividends might not be declared, and in Cotlow the assignment of insurance renewal commissions was a sale because the buyer bore renewal risk.

Invert that logic and a minimum guarantee is corrosive to sale treatment for tax, because it removes the very non-payment risk that makes the transfer a sale. A hard floor pushes toward loan characterization, in which the upfront is borrowing, the royalty payments carry imputed interest, and original-issue-discount mechanics can apply.

The consequences diverge from the accounting in ways worth flagging. Sale treatment can yield capital rather than ordinary character, and for a qualifying patent holder the section 1235 rules can treat a transfer of patent rights as a sale of a capital asset, a result a hard minimum can forfeit.

Because the tax and accounting tests weigh risk transfer through different lenses, a deal can be a financing for book and a sale for tax, or the reverse, and the minimum guarantee is often the fact that splits them. Sophisticated sellers model both lines before agreeing a floor, not after.

Does the floor even help the buyer

The sell side treats a minimum guarantee as a giveaway that improves the buyer's deal. Often it does not, and this is the analysis most memos skip.

A floor lowers the variance of the investor's cash flows from the asset, which in isolation should compress the required return and lift the advance rate. But it does so by substituting the seller's credit for the asset's performance. The floor is only ever as good as the entity standing behind it, so a hard minimum does not reduce risk, it transforms asset risk into counterparty risk.

Whether that is an improvement depends entirely on whose credit you are now underwriting.

For a strong, cash-generative seller the swap is real. Theravance's Trelegy floor is reliable because the product already throws off the cash and the milestone counterparty is GSK and Royalty Pharma, investment-grade payers who will be solvent in the scenarios where the floor is tested. For a pre-revenue, single-product developer the swap is close to illusory.

The scenario in which the buyer needs the floor, the product underperforming, is the same scenario in which the developer is least able to honour it, so the guarantee evaporates exactly when it is called. A minimum from a weak issuer is downside protection that fails in the down state, which is to say it is not protection at all unless it is backed by a security interest and a bankruptcy-remote structure that let the buyer realise on collateral rather than rely on a promise.

This is why real minimum guarantees cluster in two places and almost nowhere else. They appear in strong-seller monetizations, where the corporate credit genuinely beats the standalone asset, and in explicitly debt-structured deals, royalty bonds and revenue interests with fixed schedules and true-ups, where the buyer wanted a loan with liens all along and the floor is just the coupon made explicit. The rating logic points the same way.

Rated healthcare royalty paper earns its rating from pool diversification and structural protection, reserve accounts, cash traps, coverage triggers, not from a corporate minimum written by a weak originator, and a floor from an investment-grade parent functions less like a guarantee than like a wrap that lifts the paper toward the parent's own credit.

The underwriting discipline follows directly. Never credit a floor without pricing the guarantor. If the guarantor's standalone credit is weaker than the asset's standalone risk, the minimum adds cost without adding protection, and the only version worth having is the soft one that keeps the deal a sale.

Where the 2025 to 2026 market actually sits

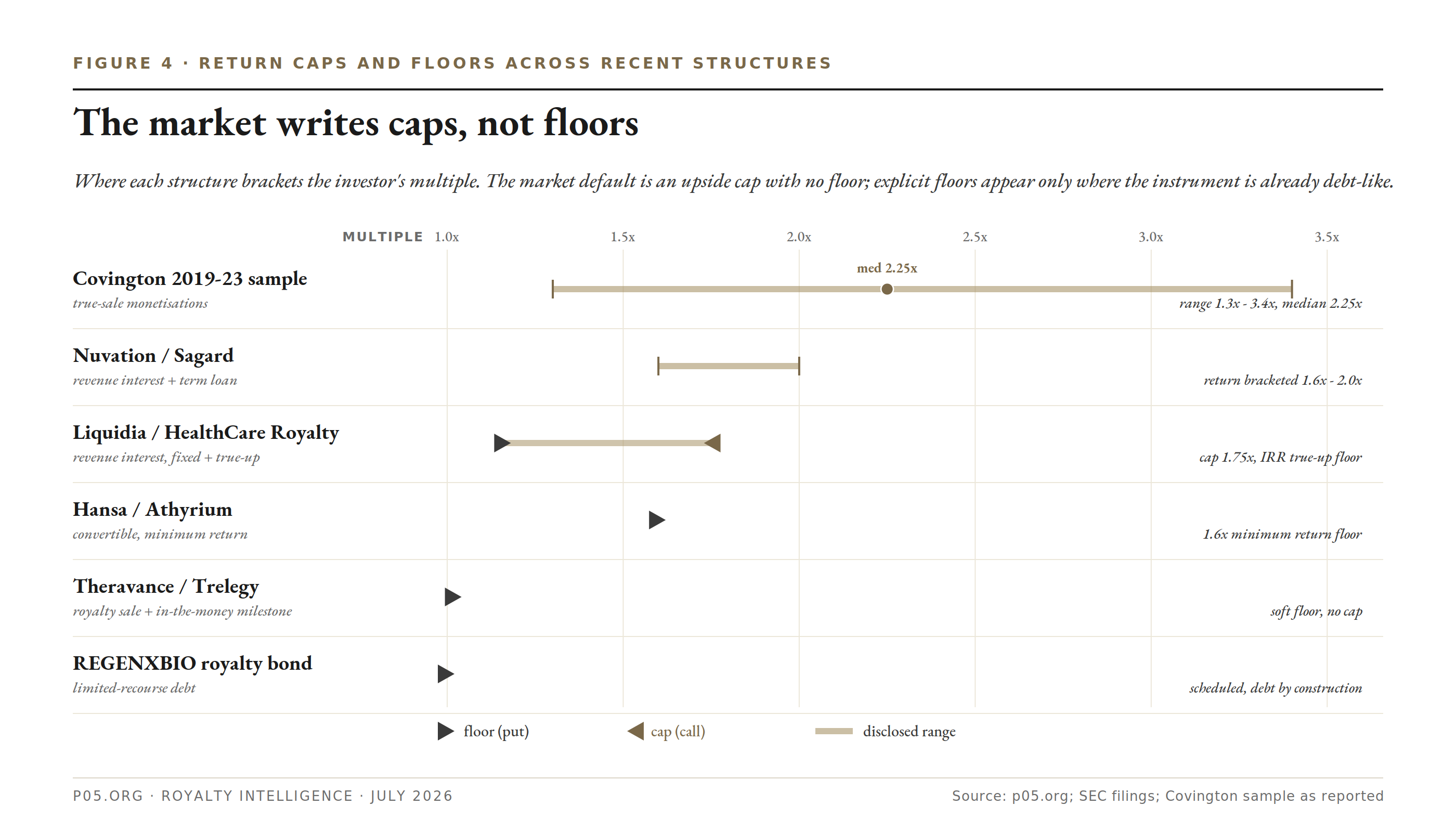

Against all of that, the observable market is conservative in a specific and revealing way. The base case remains the floorless true sale with a return cap, ninety-five percent of a 2019 to 2023 sample were structured as true sales with no fixed repayment obligation, no financial covenants, and a median cap around 2.25 times. The market shares upside through the cap and declines to write the put, which is the correct default given everything above.

The floors that do appear are the engineered exceptions, and each one is built to survive the boundary it crosses. REGENXBIO's limited-recourse royalty bond is openly debt, so recharacterization is moot. The Liquidia IRR true-up sits in a revenue interest that already carries liens and fixed payments, so the hard minimum is consistent with the instrument's debt character.

The Theravance milestone-as-floor is soft and deep in the money, so it protects the buyer without breaking the sale. The 1.6 times minimum return in the Hansa convertible and the 1.6 to 2.0 times bracket in the Nuvation revenue interest are return brackets on instruments that were never meant to be pure sales. In every case the floor is matched to an instrument that can carry it. Deal trackers reporting that floors and caps together are now increasingly common are describing this: not a market that has grown careless about the put, but one that has learned to place it where it belongs.

| Deal | Instrument | Hard or soft | Cap | Accounting lean |

|---|---|---|---|---|

| Liquidia / HealthCare Royalty | Revenue interest, fixed schedule plus IRR true-up | Hard | 1.75x | Liability |

| REGENXBIO / HealthCare Royalty | Limited-recourse royalty bond | Hard (scheduled) | n/a | Debt |

| Theravance / GSK, Royalty Pharma (Trelegy) | Royalty sale plus in-the-money milestone | Soft | n/a | Sale-preserving |

| Hansa / Athyrium | Convertible with minimum return | Hard | 1.6x floor | Debt |

| Nuvation / Sagard | Revenue interest plus term loan | Mixed | 1.6-2.0x | Liability |

Figure 4. Where recent structures bracket the investor's multiple. The default is an upside cap with no floor; explicit floors appear only where the instrument is already debt-like.

Verdict

Stop reading the minimum guarantee as a promise and start reading it as a short option leg, written by whoever stands behind the floor, and then locate that leg on the sale-to-loan axis. Those two moves answer almost every question the term raises.

The option view tells you the floor's price: cheap and deep out of the money on a de-risked stream like Trelegy, expensive and near the money on a volatile launch, and in both cases a premium that should show up in the discount rate rather than hiding in a comfort clause.

The sale-to-loan location tells you the rest: a soft minimum keeps the deal a sale, preserves deferred-income accounting, protects sale characterization for tax, and leaves the investor bearing asset risk; a hard minimum is recourse, which recharacterization doctrine punishes, liability accounting forces onto the balance sheet with imputed interest, tax treats as borrowing, and which only helps the buyer at all if the guarantor's credit genuinely beats the asset it is standing behind.

The market has internalised most of this already, which is why it defaults to caps and writes floors only where the instrument can carry them.

For the underwriter, the discipline compresses to two questions asked in order. What is the put worth, and who wrote it. Answer those and you have priced the floor, characterized the deal, and decided whether the guarantee is protection or theatre. Read the floor before the rate. The rate tells you what the deal is called; the floor tells you what it is.

All information in this report was accurate as of the research date and is derived from publicly available sources including SEC filings, accounting and tax guidance from major professional-services firms, law firm analyses of royalty-monetization structuring and bankruptcy, company disclosures, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, tax, or financial advice. The author is not a lawyer, accountant, or financial adviser.