The Floor, Not the Dream: Royalty Financing on the Asset That Missed Its Projection

A drug that misses its billion-dollar consensus still writes real cash every quarter. Royalty capital never priced the story, only the floor left behind. When that floor is a cheap, de-risked asset, when it is a value trap, and what a decade of deals and the forecast data actually show.

A drug launches into a consensus that says a billion dollars at peak. Three years later it is running at three hundred million, the sell-side has stopped updating the model, and the equity is down seventy percent. It is still writing real cash every quarter.

The instinct is that a miss disqualifies the asset. That instinct is too quick, and so is its opposite, that a cheap floor must be a bargain.

The projection that failed was the equity story, and royalty capital never priced the equity story. It prices the floor that remains after the story is gone. A drug that has fallen from a billion-dollar consensus to a three-hundred-million run-rate has spent its binary risk, published an observable base, and turned itself from a forecast into a fact. Whether that fact is a durable floor or a way station on the road to zero is the whole underwriting question. It is a different question from the one that broke the stock, and it has two ways to be answered wrongly: dismissing a financeable floor, or paying for one that is not there.

This piece sits alongside the CFO's guide to royalty financing and the balance-sheet companion. Neither turns on how the asset performed against its launch model. This one does nothing else.

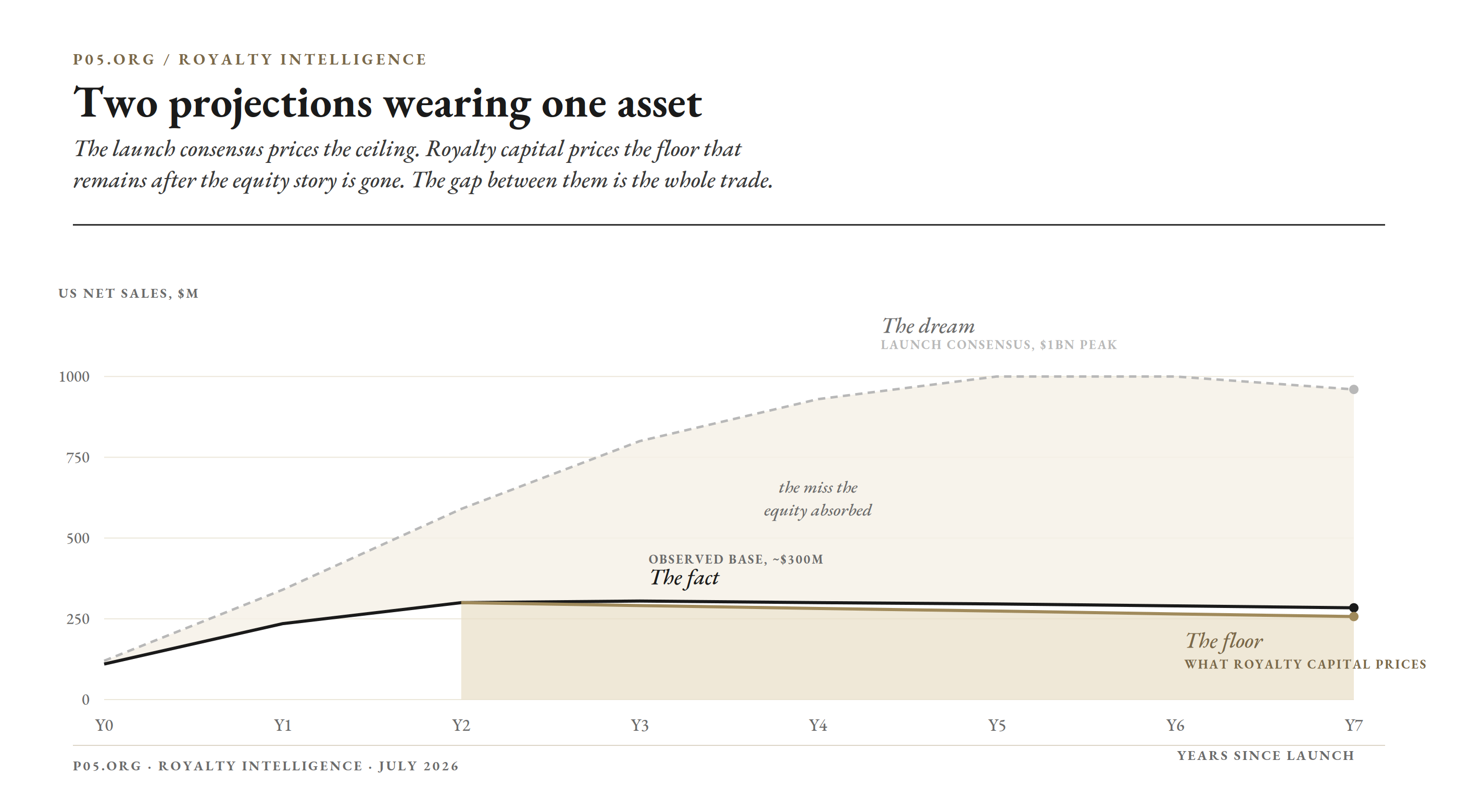

Two Projections Wearing One Asset

Every commercial drug carries two forecasts that are rarely reconciled. The launch consensus is a story about the ceiling. The royalty underwriting is a bet on the floor. On an underperformer they diverge, and the divergence is where the question lives.

Figure 1 · Two projections: the dream, the fact, and the floor

| Dimension | Launch consensus (equity story) | Royalty underwriting (financing) |

|---|---|---|

| What it prices | Peak potential, the ceiling | The durable base, the floor |

| Time horizon | The growth years ahead | Cash collectible before exclusivity ends |

| Bias | Optimistic, drawn to a presumed mean | Conservative, downside-weighted |

| Who relies on it | Equity holders, the acquirer who paid up | The buyer putting cash at risk |

A pre-launch asset cannot be underwritten off a base, because there is no base, only the binary. An asset three years in market has handed the underwriter the one thing the model most wants and can least fabricate: a run-rate that already survived contact with the world. The launch deck is evidence of what people hoped; the trailing prescription data is evidence of what the stream is worth.

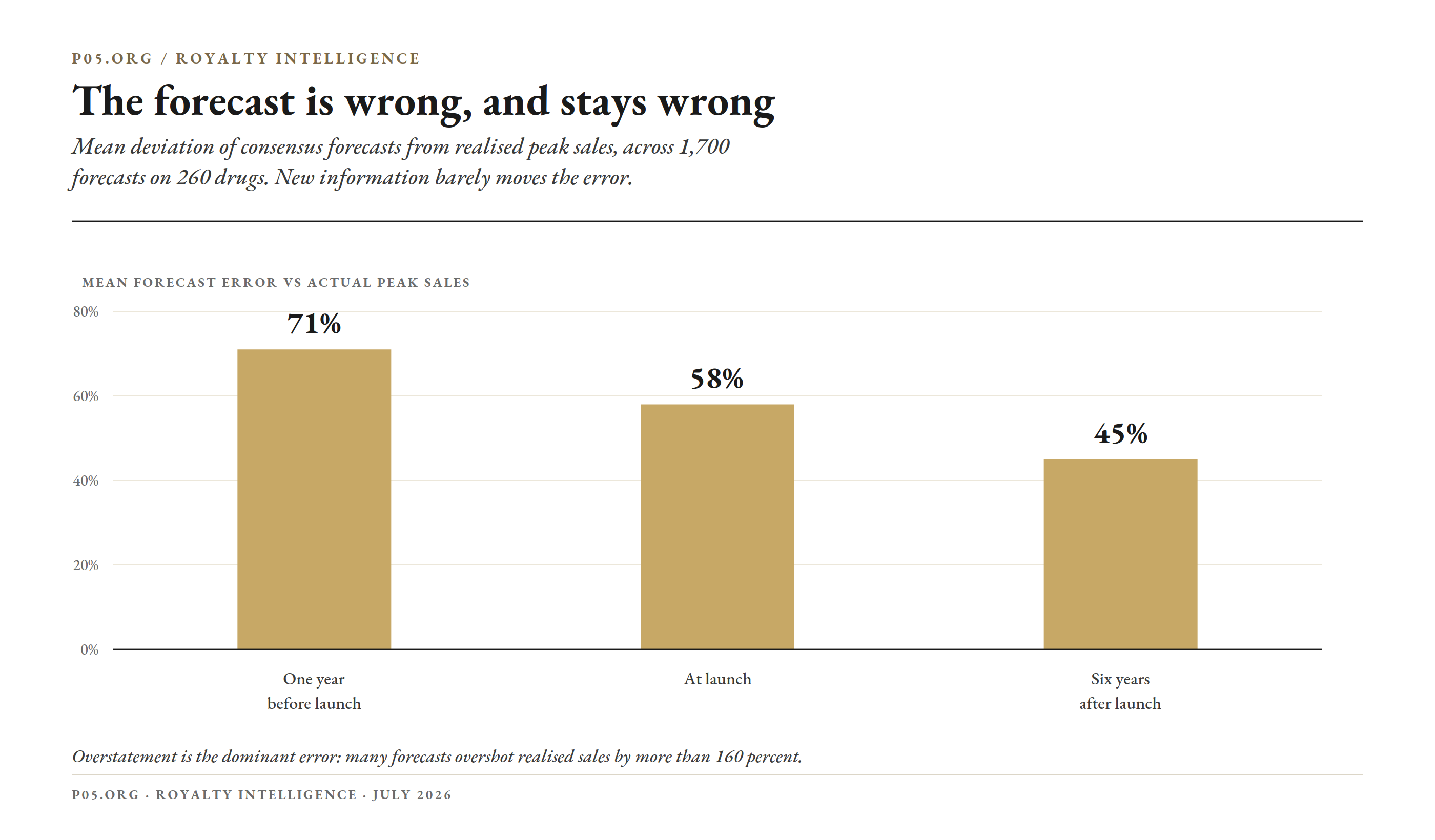

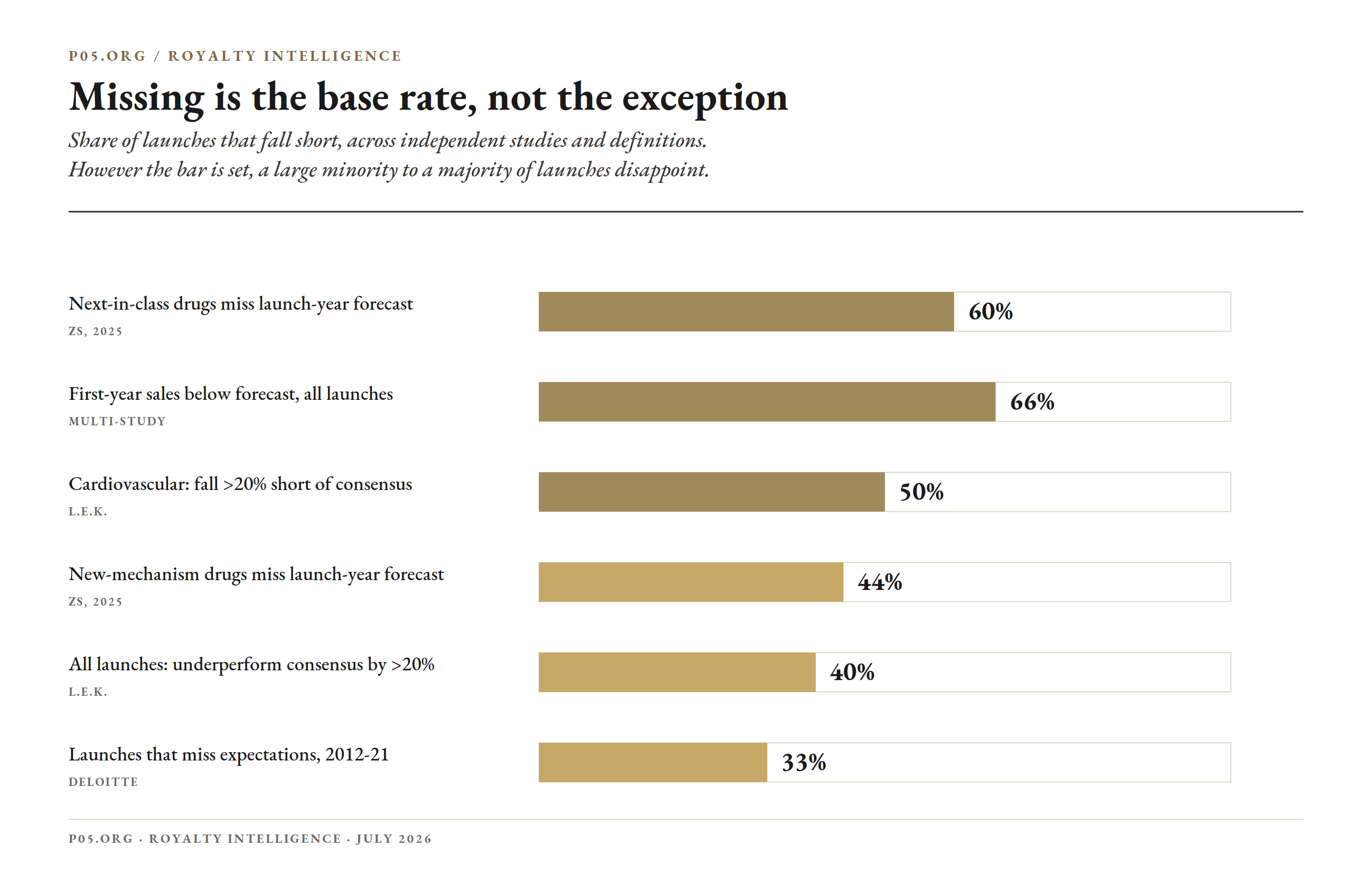

How Often the Number Is Missed

Disappointment is not the accident of a single asset. It is the base rate, and the evidence is consistent across decades and data sets.

Figure 2 · The forecast is wrong, and stays wrong

| Study | Scope | Headline finding |

|---|---|---|

| McKinsey / Nature Reviews Drug Discovery | 1,700 forecasts, 260 drugs | Peak-sales error 71% pre-launch, 58% at launch, 45% six years on; many overstated by more than 160% |

| L.E.K. Consulting | 450+ launches, 2004 to 2019 | About half miss by more than 20%; roughly 40% miss even the at-launch consensus; over 70% under 250m US in year two |

| Simon-Kucher | 50 US drugs, first five years | Only 12% within 25% of actual; 32% overshot by 2x or more, 28% undershot by 2x or more |

| Deloitte | 284 US drugs, 2012 to 2021 | Roughly one-third miss; a first-year miss tends to persist |

| ZS, by archetype | Launch year vs consensus | Next-in-class miss about 60%; new-mechanism 44%; first-in-disease 26% |

| IQVIA | Post-2020 launches, 8 key markets | 19% below benchmark at month six; latest cohort 42% below, and worsening |

Figure 3 · Missing is the base rate, not the exception

The error runs in both directions, and that matters more than the average. A peer-reviewed study of 102 Austrian reimbursement forecasts found a median overestimation of 33 percent, yet nearly 56 percent of products were off by more than 100 percent too high or 50 percent too low. On average the consensus is optimistic, but a large minority of apparent underperformers are future winners the market underrated, as Immunomedics was before Trodelvy. That is the catch for a floor-buyer. The same dispersion that makes cheap floors common also means some of those cheap assets are about to recover, and separating a permanent underperformer from a temporary one is the whole game.

For a disciplined underwriter this is raw material rather than a warning, but only to the extent the cause of the miss can be read correctly. Where it cannot, the same market of broken launch stories is a market of traps.

Why the Underperformer Comes Knocking

When a launch misses, an equity raise sells the most shares at the lowest price, and lenders demand tight covenants or decline. Royalty capital is the release valve: non-dilutive, indifferent to the share price, and scaled to the product's own cash flows. As BioSpace put it, it has become a lifeline.

That lifeline has never been larger. Royalty Pharma's January 2026 market update put total royalty-funding volume at a record 10 billion dollars in 2025, roughly 40 percent above the prior five-year average, with synthetic royalties driving the growth.

Goodwin counts about 29.4 billion dollars of biopharma royalty financing from 2020 to 2024, more than double the prior five years, and notes the model spreading into Europe through recent deals for GENFIT, Heidelberg Pharma, Ferring, and BRAIN Biotech.

One caution sits underneath the pitch. Sometimes the company monetises because it needs capital. Sometimes it monetises because it has quietly lost faith and wants to bank value before the base erodes. Identical term sheets, opposite risk. Telling them apart is the buyer's first job.

What the Buyer Underwrites

The buyer is not underwriting the recovery. It is underwriting the floor and pricing the recovery, if any, as free option value. A de-risked underperformer can be a cleaner candidate than a pre-launch asset with a glittering consensus, because it has already spent its binary.

Gibson Dunn's overview shows funds favouring exactly these commercial-stage, de-risked assets and pushing binary, pre-approval exposure into debt-like structures.

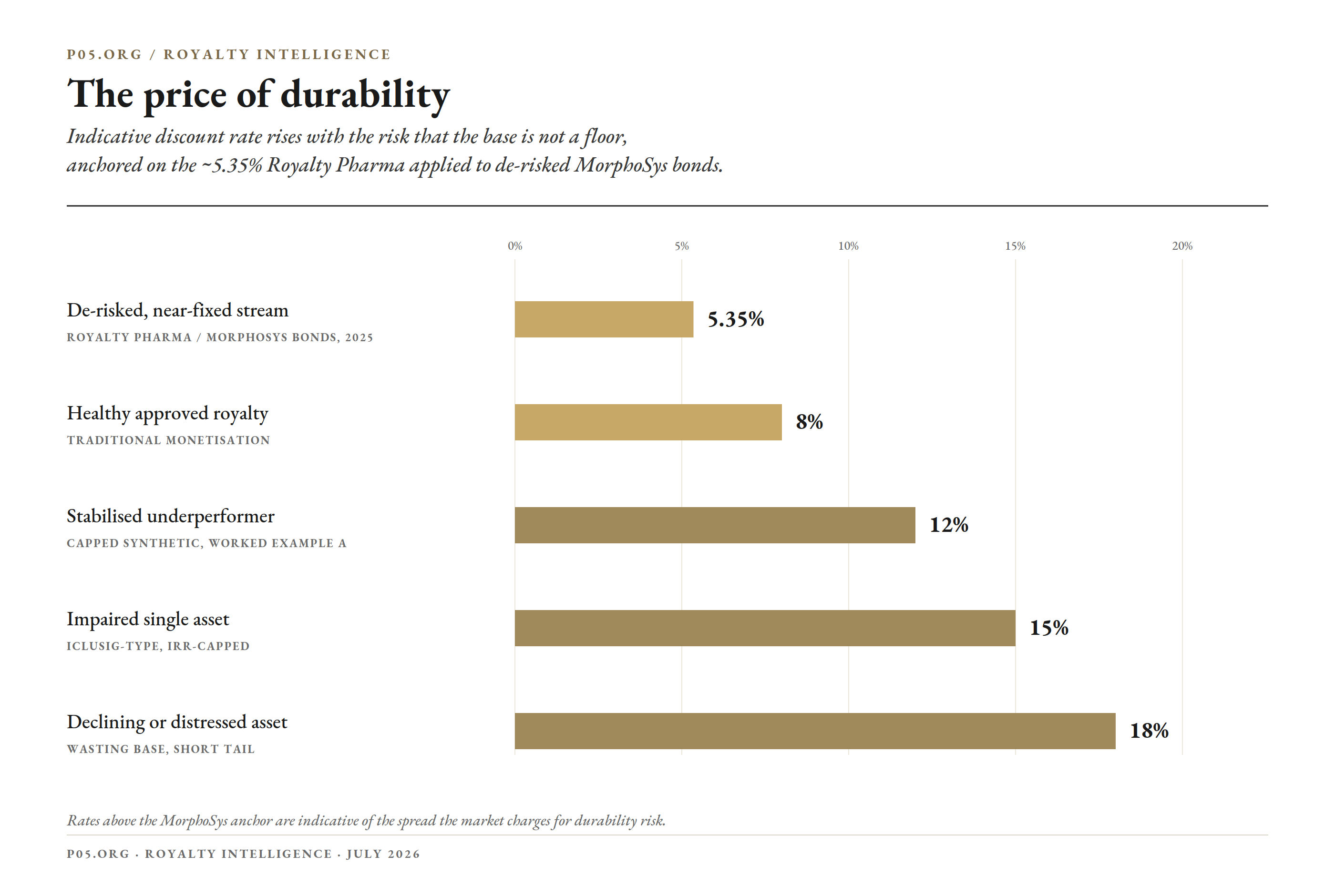

Two levers do the pricing. The forward curve is rebuilt from the observed base rather than the launch model, and the discount rate is where durability risk shows up as a number.

When Royalty Pharma sold its de-risked MorphoSys development-funding bonds in January 2025, it took 511 million dollars, for total proceeds of about 530 million on a 300 million investment, at a discount rate around 5.35 percent. Impaired single assets clear far above that. The spread is the price of one question: is the base a plateau or a slope.

That spread is compensation, not a markup for its own sake. Implied returns on impaired assets run into the teens because a real share of them keep falling, so the discount that makes a floor look cheap is also the market's estimate of how often the floor gives way. The seller feels the gap as a loss; the buyer treats it as a margin of safety; whether the safety is real is not known until the base holds or does not.

Figure 4 · The price of durability Graphic placeholder

The Problem the Buyer Cannot Model Away

The seller knows why the drug missed. The buyer has to infer it, and the seller has every incentive to present a reversible miss where the truth is structural. This is the adverse-selection problem Lo and Thakor place at the centre of biopharma financing: the assets most eagerly offered are disproportionately the ones the seller is most worried about.

So the diligence is commercial, not financial. Decompose the miss into its cause, then classify the cause. That classification, not the run-rate, decides whether the base is a floor.

| Cause of the miss | Reversible or structural | Effect on the floor |

|---|---|---|

| Slow ramp, undermarketing | Often reversible | Floor may be understated; upside is free option |

| A competitor still taking share | Structural, ongoing | Floor erodes on a schedule to model |

| Payer or formulary exclusion | Semi-structural | Floor real but capped below the launch case |

| Label restriction or safety signal | Structural but stable | Lower floor, but observable and durable |

| Category-wide demand collapse | Structural, continuing | Not a floor at all; a slope, priced as one |

The last row is the trap. A category in decline gives a trajectory, not a floor, and an underwriter who treats the current reading as a plateau will overpay.

Structure Settles the Disagreement

Seller and buyer need not agree on durability. The structure lets them disagree and still transact, by allocating the risk explicitly. Covington found, across 39 monetisations, a median upfront of 128.4 million dollars, capped-deal returns around a 2.25 times median, 95 percent true sales, and no financial covenants.

| Feature | Seller of a missed asset wants | Buyer of a missed asset wants |

|---|---|---|

| Guaranteed minimum | Yes, convert uncertainty into fixed cash | No, or only for a lower headline |

| Cap on total return | Indifferent or opposed | Yes, limit payout if the asset recovers |

| Threshold before royalty flows | Opposed, wants first-dollar coverage | Yes, avoid the tail of a decline |

| Upfront vs back-end | Front-loaded, bank value now | Back-loaded or milestone-linked |

| Change-of-control | Opposed, preserves M&A optionality | Yes, a put or lump sum on sale |

| Legal form | True sale, risk off the books | Whatever prices the risk, often debt-like |

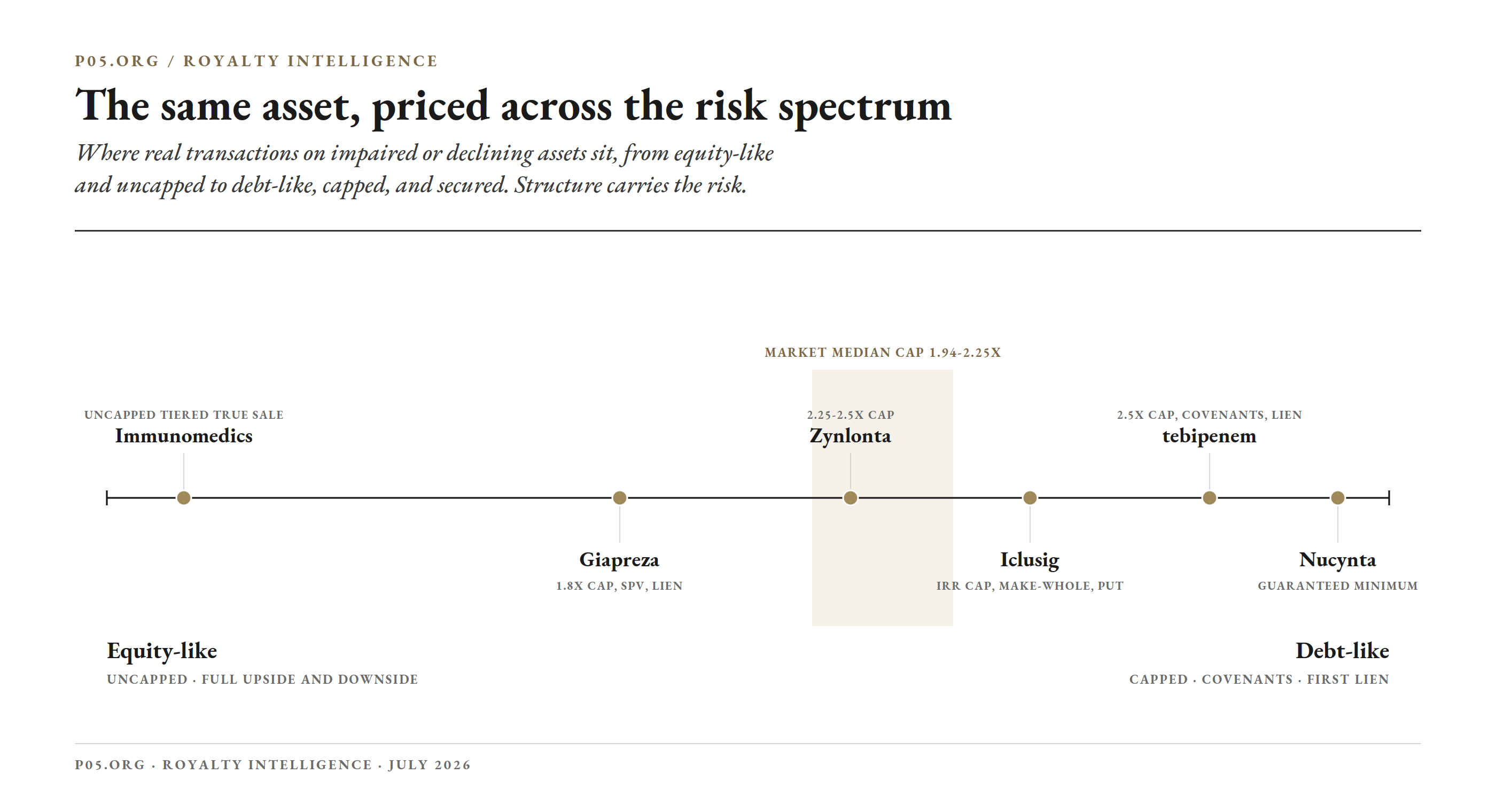

The same 125-million-dollar cheque takes different shapes: uncapped 8.75 percent on BioCryst's Orladeyo (equity-like), a capped 12 percent with covenants and a lien on Spero's tebipenem (debt in all but name), and a 1.8 times-capped step-up on Giapreza in between. On a healthy blockbuster the structure is close to a formality. On an underperformer it is the deal.

Figure 5 · The same asset, priced across the risk spectrum

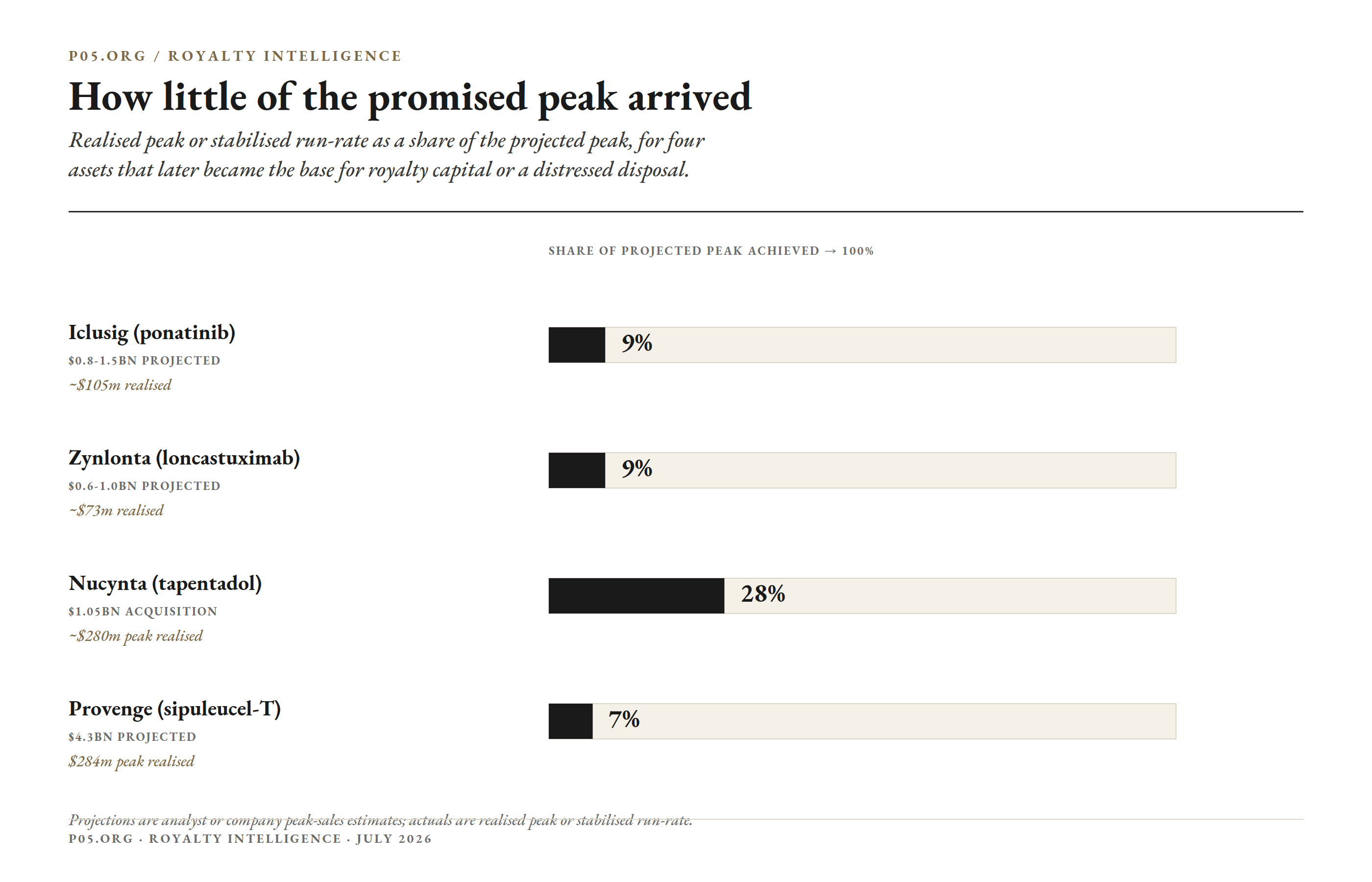

What Missing Looks Like in Practice

Each asset below reached the market on a projection in the high hundreds of millions or billions, then settled at a fraction of it before becoming the base for royalty capital or a distressed sale.

Figure 6 · How little of the promised peak arrived

| Transaction | Projection vs actual | Why it missed | Structure | Outcome |

|---|---|---|---|---|

| Iclusig, ARIAD to PDL (2015) | 0.8 to 1.5bn projected; ~105m | Safety signal, label cut to T315I | Up to 200m; royalty 2.5 to 7.5% to a fixed IRR; five-year make-whole; change-of-control put | Impaired but financeable when capped and protected; Takeda bought ARIAD for 5.2bn and the put fired |

| Nucynta, Depomed to Collegium (2017 to 2020) | 1.05bn acquisition; ~280m peak, then decline | Opioid-market collapse | 135m per year guaranteed minimum, later removed; outright sale at 375m | The minimum held only until the base fell far enough to force renegotiation; a slope ended in disposal |

| Zynlonta, ADC to HealthCare Royalty (2021, amended 2026) | 0.6 to 1.0bn US potential; ~70m | CAR-T and bispecific crowding | 225m upfront, 7 to 10% capped 2.25 to 2.5x; 2026 recut CoC from 750m to 150m plus warrants | Durability risk realised; the buyer repriced its floor and took equity for what it gave up |

| Coherus, Loqtorzi and Udenyca to Barings (2024) | Declining biosimilar, early IO asset | Non-core, maturing; strategic pivot | 37.5m royalty to a hard cap plus a term loan; Udenyca later sold to Intas for up to 558.4m | Non-core stream monetised to retire costly debt and fund a pivot |

| Immunomedics to Royalty Pharma (2018) | Doubted pre-Trodelvy; later a Gilead franchise | Cash-strapped, unproven at deal time | Tiered 4.15 to 1.75% plus 75m equity at a premium, for 175m | The upside caught: Gilead bought Immunomedics for ~21bn, but the seller banked only the floor |

| Provenge, Dendreon (2014) | Up to 4.3bn projected; 283.7m, collapsing | ~93k price, ~77% COGS, oral competitors | Chapter 11; worldwide rights to Valeant for 400m | A slope, not a floor: refuse it, or price a wasting asset with a low cap and short tail |

| Clovis, Rubraca in Chapter 11 (2022 to 2023) | Blockbuster-class PARP hopes; sub-scale | Out-competed within its class; label restriction | 363 sale; Rubraca to Pharma& for 70m upfront, up to 135m | Competitive erosion inside a class ends where a category collapse does: disposal, not royalty |

| Achaogen, Zemdri after approval (2018 to 2019) | Approved novel antibiotic; ~0.8m in early sales | Structural antibiotic-market failure | Chapter 11 nine months post-launch; assets auctioned for ~16m | Some approved assets have no financeable floor at all; the answer is to decline |

| PhaseBio, SFJ (2022) | Development-stage; contested in bankruptcy | Chapter 11, recharacterisation fight | Multiple-of-capital return up to ~500%; settlement kept 2.5% over 300m for the estate | Why buyers demand true-sale isolation and clean security |

| Ligand acquires XOMA (2026) | Many small, uncertain royalties | Portfolio dilutes single-asset binary risk | ~739m at 39 a share plus a CVR; 120+ assets | Diversification prices the adverse selection that single-asset diligence cannot fully resolve |

A few of these mark the range. Iclusig is the archetype of an impaired asset financed anyway: projected at up to 1.5 billion dollars, cut to a T315I-restricted label after vascular events above 27 percent, settled near 105 million, and still monetised through an IRR-capped royalty with a make-whole and a change-of-control put that paid out when Takeda bought ARIAD. Nucynta shows the arc: a 1.05-billion-dollar acquisition, a guaranteed minimum, that minimum renegotiated away as the opioid market collapsed, and an outright sale at 375 million.

Provenge and Rubraca are the disposals, from different causes. Dendreon's vaccine, projected as high as 4.3 billion, reached 283.7 million and sold to Valeant for 400 million out of bankruptcy, undone by price and cost of goods. Clovis's Rubraca, a blockbuster-class PARP hope, was out-competed inside its class and sold for 70 million in a bankruptcy auction. Immunomedics is the counterweight: a doubted developer that sold Royalty Pharma a royalty for 175 million, then became a 21-billion-dollar Gilead franchise, the seller having banked only the floor while the buyer kept the upside.

When There Is No Floor at All

The trap in the diligence table is a mispriced slope: a base that looks flat but is not. There is a harder case, where the base was never there to begin with.

Achaogen won FDA approval for the antibiotic Zemdri in 2018, launched it, and booked roughly 800,000 dollars of sales before filing for Chapter 11 nine months later. Its assets were auctioned for about 16 million. The problem was not the drug, which treats carbapenem-resistant infections the world urgently needs. It was the market. Novel antibiotics are held in reserve, reimbursed poorly, and used sparingly, so approval buys almost no commercial floor, and most small-company antibacterials approved since 2010 have ended in bankruptcy or a loss.

For a royalty underwriter, the antibiotic case is the reminder that "approved and on the market" is not the same as "financeable." Where the category structurally denies the asset a floor, there is nothing to price, and the discipline is to say so rather than build a curve off a number that will not hold.

Three Worked Hypotheticals

Same starting point in every case: a drug that launched into a one-billion-dollar consensus and settled at three hundred million.

| Scenario | Seller motive | Structure | Illustrative upfront | Risk allocation |

|---|---|---|---|---|

| A. Stabilised plateau | Non-dilutive cash, no covenants | 9% synthetic, capped 1.75x, SPV and lien | ~180m | Debt-like; floor priced conservatively, upside capped |

| B. Recovery option | Exit a view, take clean cash | Uncapped true sale | ~230m | Buyer keeps all recovery; adverse-selection risk highest |

| C. Seller-protected floor | Predictable cash, no variability | 11% with a guaranteed minimum, capped 2.0x | ~150m | Behaves like debt; recharacterisation and minimum-default risk |

The recovery option is where the adverse-selection warning is loudest: a seller willing to leave all the upside on the table may know something about the readout that the buyer does not.

When It Works, and When It Is a Trap

It works when the miss is real, the cause is understood, and the base is genuinely a floor. The binary is spent, the price is low because the equity story is broken, and the upside beyond the floor is free option value. Iclusig, once its restricted label defined a stable population, qualified. So, for a time, did Nucynta.

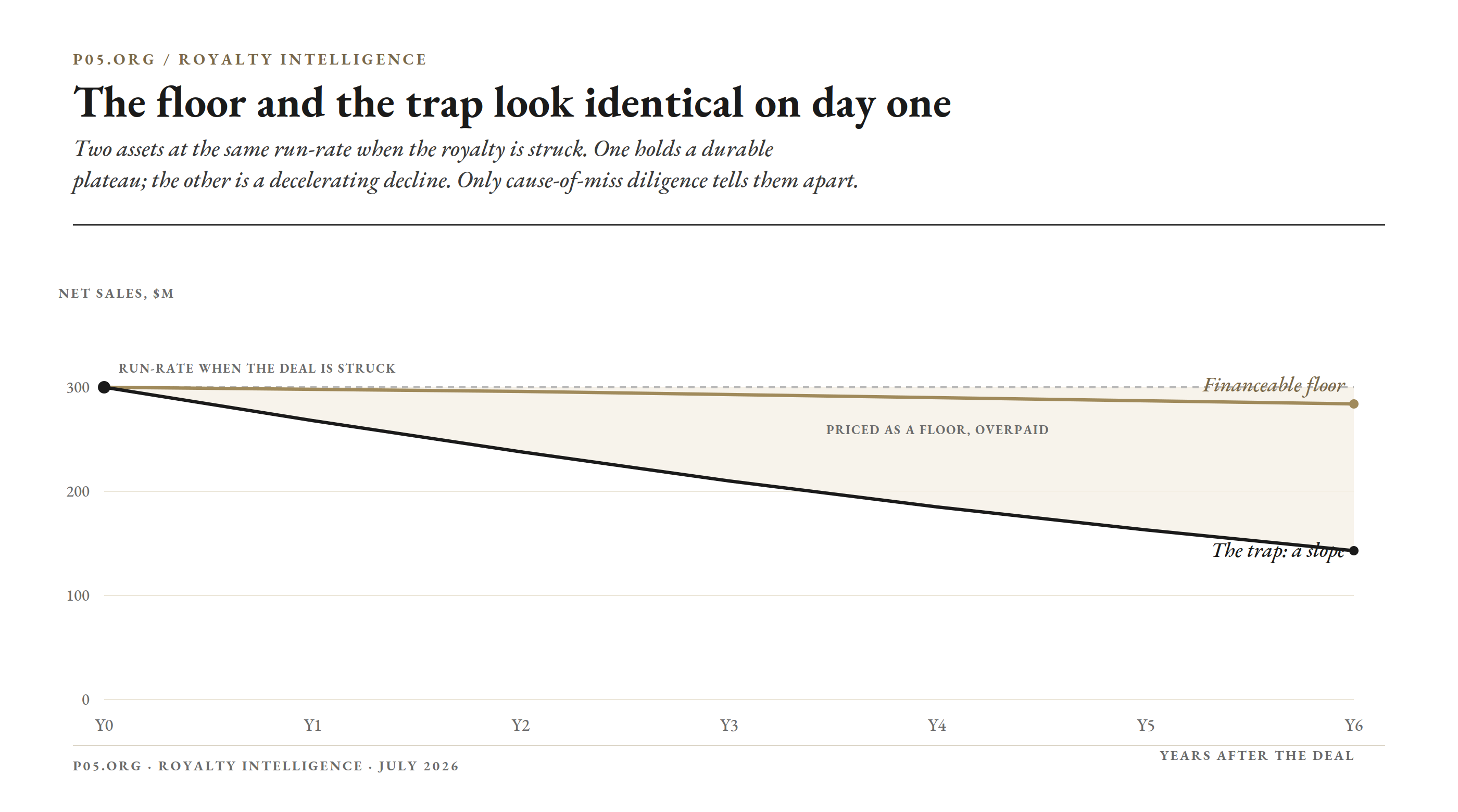

Figure 7 · The floor and the trap look identical on day one

It is a trap when the asset is still declining, the run-rate is a photograph of a moving object, and the seller is monetising to get out before the number falls further. Provenge is the pure form. The tell is the alignment of the seller's motive with the buyer's blind spot: the company that has concluded the base will keep eroding is the one most eager to convert it into fixed cash today, and its term sheet looks identical to a company simply raising money against a stable stream. Distinguishing the two is not a matter of reading the model. It is a matter of understanding, better than the seller would like, why the number is where it is.

Opportunity, or Not

Whether a missed asset is a bargain or a value trap has no general answer. It has a per-deal answer, and both sides of the table can get it wrong.

The case for is the one this piece has laid out. The binary is spent, the equity has already taken the loss, the price reflects a broken story rather than a broken asset, and a conservatively priced floor leaves any recovery as free option value. In a record ten-billion-dollar market, buyers with strong commercial diligence can find real mispricings the crowd overlooks.

The case against is that the discount is compensation, not a gift. Implied returns run into the teens because a meaningful share of these assets keep declining, and the buyer cannot see the cause of the miss as clearly as the seller can. The market's own recent history shows floors that proved too high: HealthCare Royalty accepted a smaller change-of-control payment and took warrants on Zynlonta, and Collegium's guaranteed minimum on Nucynta was renegotiated away, each a buyer repricing a floor that sagged. The published successes also carry survivorship bias, since the Immunomedics outcome is memorable precisely because it is rare.

The seller can be wrong too. Monetising at the floor banks certainty but forfeits the recovery, and if the asset turns out to be a future winner, the price looks cheap in hindsight, as Immunomedics' royalty did once Trodelvy arrived. The CFO's guide makes the same point from the issuer's chair: above a modest spread to alternative capital, a royalty can destroy value rather than create it.

The honest summary is that this is a pricing problem, not a free lunch and not a trap. The edge belongs to whichever side reads the cause of the miss more accurately, and on a given deal that can be the buyer, the seller, or neither.

The Pattern

Underperformance does not close the royalty market to an asset. It changes which structure the asset qualifies for, and which party carries the durability risk. A stabilised miss can become a cheap royalty; an impaired asset a capped and protected one; a structurally declining asset a disposal; an asset with no commercial floor, a pass; a doubted asset that recovers, a ceiling the buyer never paid for.

The funds arriving to finance a company that just missed its number are not making a charitable exception, and they are not guaranteed a bargain either. They are pricing a floor the equity market forgot the asset still had, and the same discount that marks value also marks the risk that the floor keeps falling. The evidence says the miss was the likeliest outcome all along, and that the consensus which set the expectation was imprecise in both directions. The task on the other side of the table is to know which situation is actually on offer, because the term sheets look the same, and the outcomes do not.

All information in this article was accurate as of the research date and is derived from publicly available sources including SEC filings, company press releases, law firm and consulting publications, academic literature, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, accounting, tax, or financial advice. The author is not a lawyer, accountant, tax adviser, or financial adviser.