The Other Royalty Markets: Seeds, Traits, and Platform Biotech

The royalty economies in seeds, crop traits, fruit varieties, and bioprocessing platforms are just as real and just as patent-backed, with court records, license terms, and recent transactions to prove it, and almost no financing market on top.

The pharmaceutical royalty market spent two decades turning the future sales of approved drugs into a financeable asset class. It now has specialist funds, rated securitizations, and a routine monetization market. A university can sell a discovery royalty for hundreds of millions of dollars in an afternoon.

This piece asks whether the same logic travels. Drugs are not the only patent-protected products that throw off a defined-term royalty. Seeds do. Engineered crop traits do. Branded fruit varieties do. So do the chemistries underneath modern biologic drugs.

Each has a royalty economy that is real, sizable, and legally enforced. In several cases it is documented down to the per-unit rate, in court filings and license agreements. Almost none of them has a financing market sitting on top.

This is a survey, not an argument. It maps where royalty cash flows actually exist outside pharma, jurisdiction by jurisdiction. It looks at the enforcement record, the little financing activity that has been tried, and where the gap is widest.

The pharmaceutical comparison runs underneath throughout. It is the one case where the gap has fully closed, so it sets the test every other vertical has to pass.

One point is worth previewing. The size of a royalty economy and its financeability are nearly unrelated. The largest non-pharma royalty market is the least likely to ever need a financing layer. The one with the cleanest financing case is among the smaller.

What makes a royalty financeable

The test is the same in every market. A royalty stream is financeable when four things hold at once.

First, the right is defined and enforceable, so a buyer knows what it is buying and can defend it in court. Second, the term is long and predictable, so the cash flows extend far enough to discount. Third, the payer is diversified or creditworthy, so no single failure sinks the stream. Fourth, a collection mechanism already exists, so the cash arrives without the buyer building the plumbing.

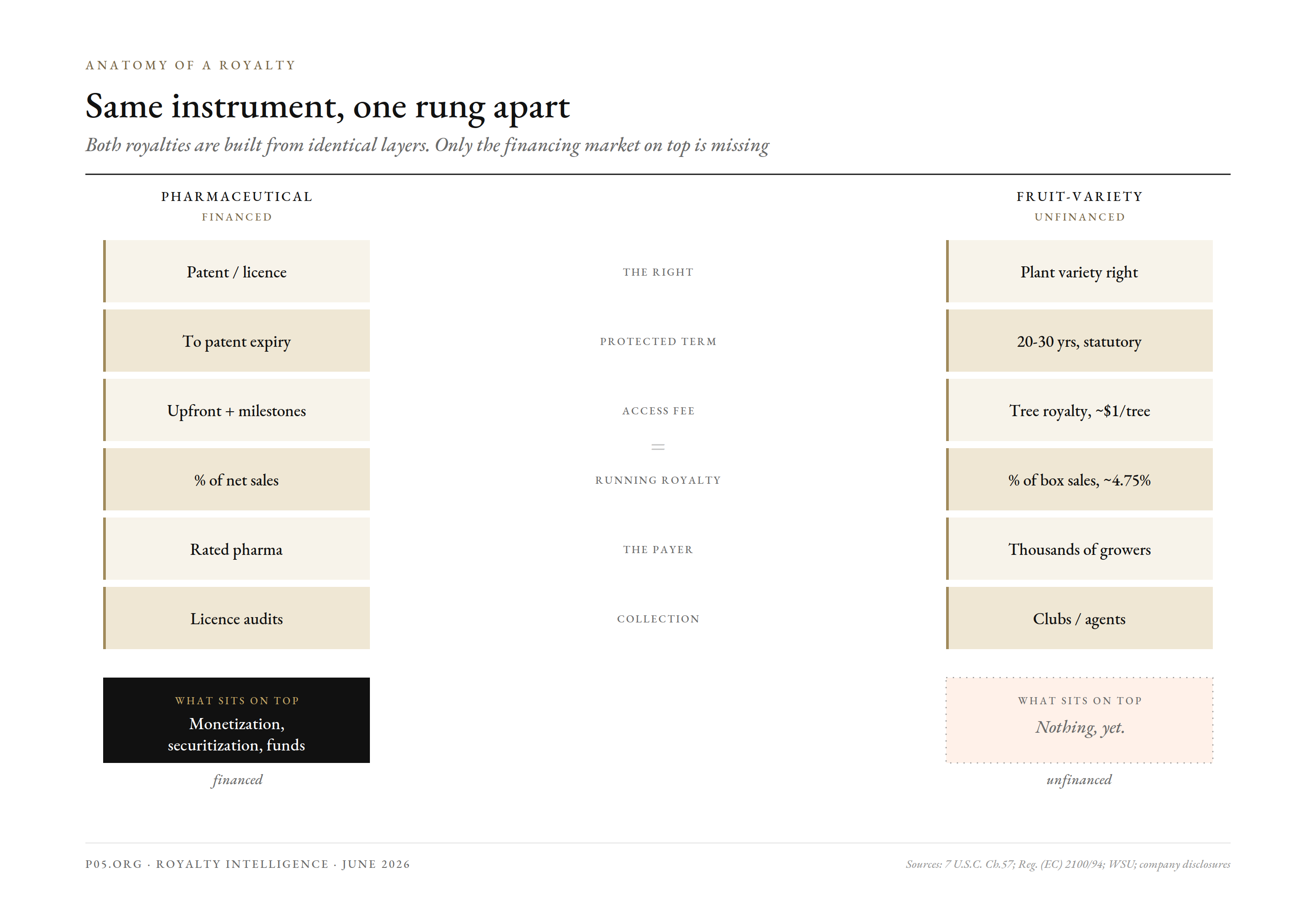

Pharmaceutical royalties clear all four cleanly. A patent or licence defines the right. The term runs to patent expiry, often a decade or more out. The payer is usually a large, rated pharma counterparty. And the cash flows through an established licence-accounting apparatus with audit rights.

That combination is why the asset class became financeable, and why an arranger turns up to write the cheque.

The interesting fact about the other verticals is that several clear the same four tests on paper, with enforcement records to back them, and still have almost no buyers.

Seeds and plant variety rights

The cleanest non-pharma analog to a drug royalty is a plant variety right. Unlike most of what follows, its enforceability has been tested at the highest courts in three jurisdictions.

Plant variety protection is a formal IP regime, parallel to patents. It is run through UPOV internationally, the CPVO in the European Union, and the Plant Variety Protection Office at the USDA in the United States.

A certificate grants the breeder an exclusive right over the propagating material of a new variety. The term is typically 20 years for most crops and 25 for vines and trees under the US statute, and longer elsewhere. That is comparable to or longer than what most drug patents deliver after clinical development eats the early years.

The term lengths matter for discounting, so they are worth setting out.

| Jurisdiction | Most crops | Trees / vines | Recent change |

|---|---|---|---|

| US (PVPA) | 20 years | 25 years | Stable |

| EU (Reg. 2100/94) | 25 years | 30 years | Stable |

| Japan (PVPSA) | 25 years | 30 years | 2026 bill to add 10 years |

| New Zealand (PVR Act) | 25 years | 30 years | 2025 extension, SunGold to 2046 |

The United States: tested to the Supreme Court

The US case is the most litigated. That matters, because litigation is where the enforceability of a royalty stops being theoretical.

Two regimes protect seed innovation. The Plant Variety Protection Act, codified at 7 U.S.C. Chapter 57, covers sexually reproduced varieties. Its remedy at section 2564 lets a court award up to three times the royalty lost, plus costs. Utility patents, separately, protect the engineered traits.

The enforcement record is concrete. In Asgrow v. Winterboer, the Supreme Court read the saved-seed exemption narrowly, limiting a farmer to saving only enough seed to replant his own holding.

In Syngenta v. Delta Cotton, the Federal Circuit confirmed that selling protected wheat in a propagable form, without notice of its status, is infringement.

The landmark is Bowman v. Monsanto Co., 569 U.S. 278 (2013). A unanimous Court, in an opinion by Justice Kagan, held that patent exhaustion does not let a farmer reproduce patented seed by planting and harvesting it.

The damages are worth stating precisely, because they show the per-farmer scale of a single trait royalty. The district court awarded Monsanto $84,456 against one Indiana grower, and both the Federal Circuit and the Supreme Court left it standing.

The right survives even when the patented article replicates itself in a field. That is about as robust as an enforceable IP right gets.

The branded-fruit layer is where the cash flows turn genuinely large. Cosmic Crisp, the WSU-bred WA 38 apple, reads almost exactly like a pharmaceutical royalty stack: a fee at propagation, an ongoing fee, and a percentage on net sales. The university holds the rights; a specialist agent, Proprietary Variety Management, collects.

| Cosmic Crisp (WA 38) royalty component | Term |

|---|---|

| Tree royalty (on planting) | $1.00 per tree |

| Production royalty (annual, from year 2) | $2.00 per tree per year |

| Fruit royalty (box sales over $20) | 4.75% of box sale price |

| Trees planted in Washington | 22 million+ |

| Recent-season production | ~12 million 40-lb boxes |

| Cumulative royalties to WSU since 2017 | ~$28 million |

| FY2025 royalties to WSU | $8 million+ |

| Washington exclusivity | extended to 2032 (April 2026) |

In April 2026, rather than let the Washington-exclusive window lapse in 2027, WSU extended grower exclusivity to 2032. It deliberately lengthened the protected stream.

The founding precedent is older and cleaner. The University of Minnesota's Honeycrisp showed a land-grant university could patent a cultivar and collect a per-tree royalty across the whole national planting base. Cornell, private clubs, and breeders worldwide followed.

The European Union: the Nadorcott line

The EU regime is, if anything, more centralized than the US one. Its enforcement record is just as concrete, anchored in a long-running mandarin dispute.

Community Plant Variety Rights are governed by Regulation (EC) No 2100/94 and run centrally by the CPVO. A single application yields a right across all member states. EU law has compelled royalty payment on protected varieties since 1994, restricting the old farmers' privilege to save seed except for defined small farmers.

Collection on farm-saved seed runs through established agents: Sicasov in France, STV in Germany, BSPB in the UK before its EU exit. The right, the term, and the plumbing are all in place by statute.

The enforcement record centres on the Nadorcott mandarin. Its rights are held by Nadorcott Protection and managed in Spain and Portugal by the Club de Variedades Vegetales Protegidas. Two CJEU rulings came out of growers cultivating it without a licence.

In CVVP v Martínez Sanchís (C-176/18, December 2019), the Court clarified the scope of the holder's right over propagating versus harvested material. The right over harvested fruit is conditional and narrower than the right over the trees.

In José Cánovas Pardo v CVVP (C-186/18, October 2021), the Court ruled on the limitation period. The three-year clock runs from the holder's knowledge of the infringement, and ongoing cultivation generates fresh, separately actionable infringements.

The message to holders is that delay erodes recoverable royalties. A pharmaceutical royalty buyer would recognize it from any licence-audit dispute. The same variety has also survived repeated validity challenges, with the General Court dismissing a nullity appeal as recently as September 2024.

The point is not the botany. It is that the EU royalty right has been litigated to the Union's highest court, and held. The apple-club ecosystem, Kanzi and Pink Lady among them, runs on the same tree-plus-fruit model.

Japan: the Shine Muscat lesson

Japan supplies the clearest cautionary tale of what happens when a valuable variety royalty is not protected where it needs to be.

Shine Muscat is a premium seedless grape, bred over three decades by Japan's National Agriculture and Food Research Organization. It was registered domestically in 2006 but not registered internationally within the six-year UPOV novelty window.

By around 2012 it was effectively unprotected outside Japan. Growers in China and South Korea began propagating it legally and at scale, paying no royalty. A grape that sells for tens of dollars a bunch at home became a mass-market product abroad at a fraction of the price.

The loss was a consequence of a missing registration, not a missing right. The cash flow was financeable in principle, and simply went uncollected.

The policy response makes the value explicit. The Plant Variety Protection and Seed Act was revised in December 2020, effective April 2021. It lets breeders designate which countries a registered variety may be exported to, with a list of more than 2,500 covered varieties including Shine Muscat.

Enforcement followed fast. Within months, authorities were investigating a propagator who had grafted and resold Shine Muscat seedlings online at half price.

As of early 2026, Japan has advanced legislation to add ten more years of breeder-rights protection. A country does not legislate twice in five years to protect a cash flow it thinks is immaterial.

Korea: dependence to sovereignty

Korea is the reverse mirror of Japan. The same royalty economics run the other way, within a single generation.

Until around 2005, roughly 90% of strawberries grown in Korea were Japanese varieties, mainly Akihime. When Japanese holders began seeking royalties, Korean public institutions accelerated domestic breeding. The Nonsan Strawberry Experiment Station released the Seolhyang variety in 2005.

The shift was near-total. Domestic-variety adoption now runs above 96%, and the royalty outflow has largely gone. Korea is now a net recipient, with varieties such as Maehyang and Geumsil grown under licence across Asia and Oceania.

Korean strawberry exports themselves reached roughly $70 to $72 million in the most recent year. The arc is a real-time demonstration: a variety royalty is a collectible, cross-border cash flow that governments treat as strategic and legislate to protect.

The seed verdict

Pull the four jurisdictions together and plant variety rights clear all four financeability tests, with documentary backing.

The right is defined by statute and upheld to the Supreme Court in the US, the Court of Justice in the EU, and through criminal enforcement in Japan. The term is long, 20 to 30 years and lengthening. The payer base, thousands of growers, is about as diversified as a royalty pool can be. The collection infrastructure already exists and already audits.

On enforceability and structure, the seed royalty is the equal of a pharmaceutical one. What is missing is the financing market, which is the next section.

The financing market that mostly is not there

This is the part the survey points at. The seed royalty clears every structural test, so the question is simple: who finances it, and how does that compare with pharma?

The honest answer: the activity is thin, indirect, and almost entirely equity rather than royalty monetization. The contrast with pharma is stark.

What pharma does, as the benchmark

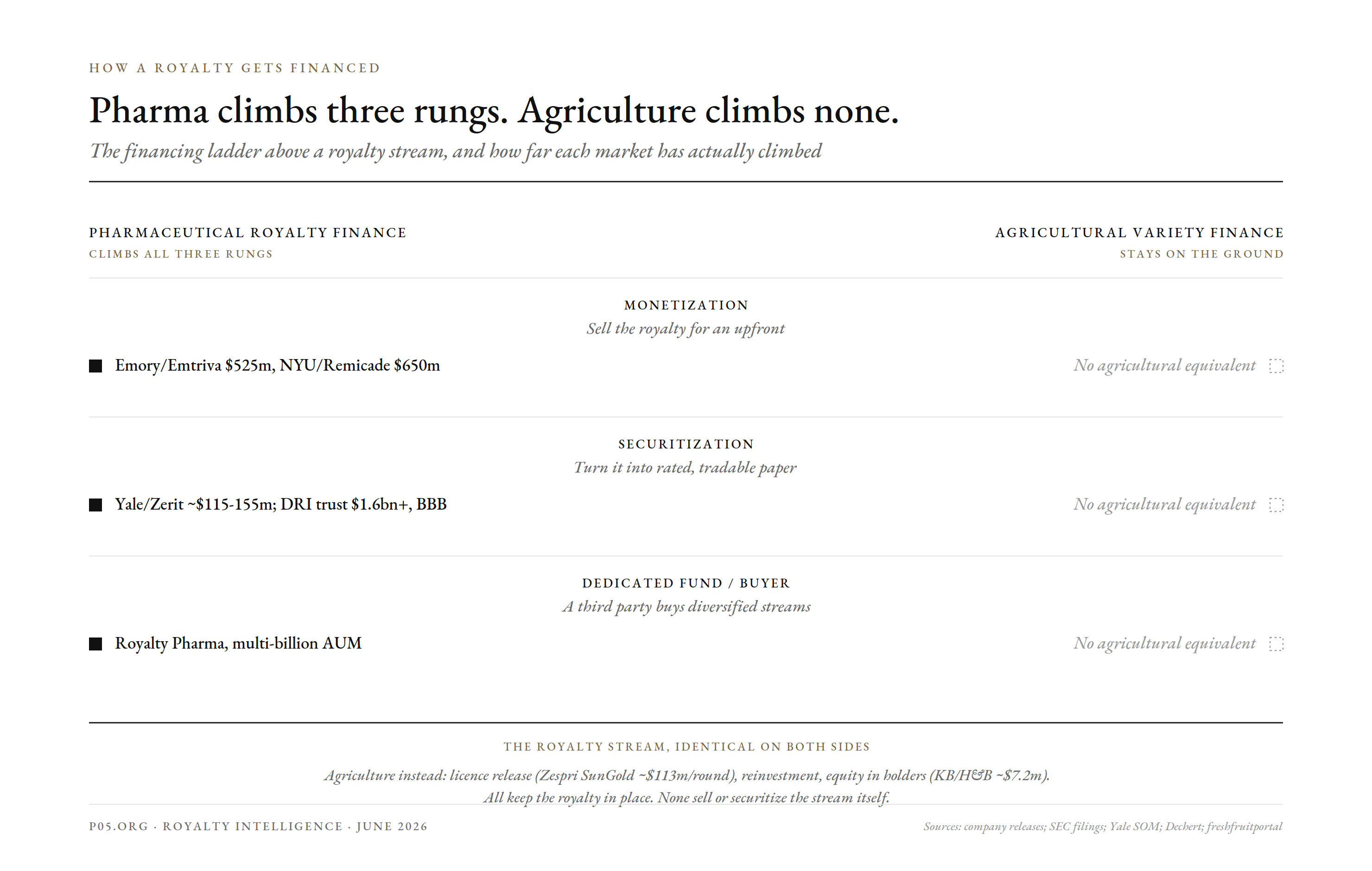

In pharma, financing a discovery royalty is routine. It runs through three channels.

The first is outright monetization, an institution selling its royalty for an upfront. In 2005, Emory University sold its Emtriva royalty to Gilead and Royalty Pharma for $525 million, reportedly the first such deal done by auction.

In 2007, NYU sold part of its Remicade royalty to Royalty Pharma for $650 million, on a stream that had already paid it some $360 million. The same buyers have done structurally identical deals with Memorial Sloan Kettering, Duke, Colorado, and the UK's Kennedy Trust.

The second is securitization, turning the royalty into rated paper. Yale was the pioneer: in 2000-2001 it securitized its Zerit royalty through the BioPharma Royalty Trust, raising $115-155 million against a stream then running about $40 million a year.

That single-asset deal went into early amortization almost at once, when Zerit sales disappointed. The market learned, and moved to diversified pools. DRI Capital's master trust has issued more than $1.6 billion across eight securitizations since 2005, with a 2017 series rated BBB.

The third is the dedicated fund, the Royalty Pharma model of permanent capital buying diversified royalties at scale.

| Pharma royalty financing channel | Representative deal | Upfront |

|---|---|---|

| Outright monetization | NYU / Remicade (2007) | $650 million |

| Outright monetization | Emory / Emtriva (2005) | $525 million |

| Single-asset securitization | Yale / Zerit (2000-01) | ~$115-155 million |

| Diversified securitization | DRI Capital master trust (since 2005) | $1.6 billion+ across 8 series |

| Dedicated fund | Royalty Pharma (ongoing) | multi-billion AUM |

Each channel exists because a specialist buyer base and an arranger layer were built over two decades. Now hold that template against agriculture.

What agriculture does instead

There is no agricultural equivalent of the Emory or NYU monetization. No agricultural Yale-style securitization. No agricultural Royalty Pharma.

A university with a blockbuster drug royalty sells it for a nine-figure upfront. A university with a blockbuster apple or grape royalty, WSU with Cosmic Crisp, NARO with Shine Muscat, funds its next breeding programme out of current receipts. The arranger that turns up in one case does not turn up in the other.

What does exist is a scattering of adjacent structures. They solve pieces of the problem without being royalty monetization.

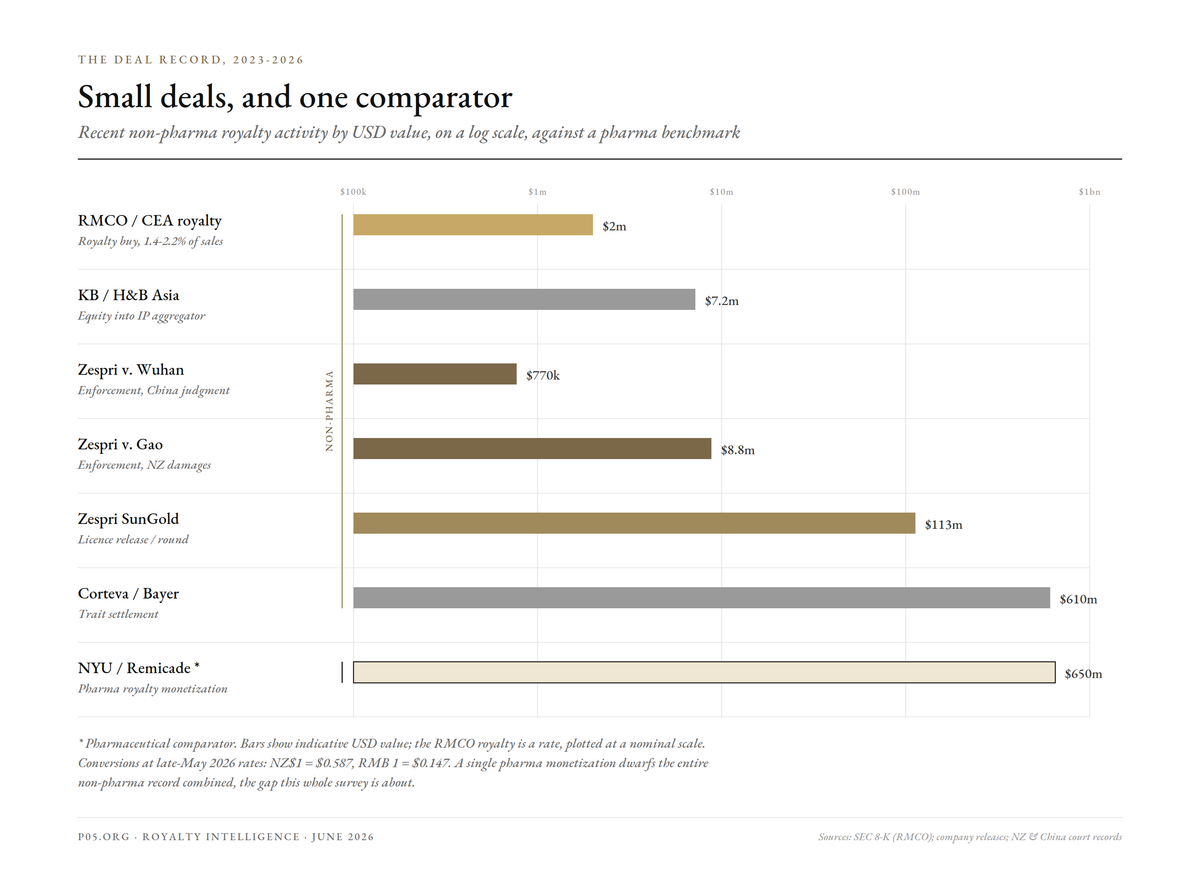

Licence release. The closest thing to a structured monetization is the Zespri SunGold (Gold3) licence release. Zespri sells future access to its protected variety for upfront cash, at scale, every year.

Growers pay around NZ$270,000 (~$159,000) per hectare for the right to plant it. A single 2018/19 release round raised roughly NZ$192.6 million (~$113 million) in gross licence revenue.

The economics now dominate the company. Roughly 75% of Zespri's income comes through protected varieties, and in 2025 licence revenue drove net profit up 80% to NZ$280 million (~$164 million). Growers pay an ongoing 3% royalty on top, split with the breeder, Plant and Food Research.

But note what this is not. Zespri is monetizing its own variety to its own growers, not selling the stream to an outside buyer. It is self-financing, not a financing market.

Reinvestment. A second structure recycles royalty income into the next generation of varieties. Plant and Food Research runs an explicit Kiwifruit Royalty Investment Programme, co-investing with Zespri and, on apples, with T&G Global on Envy.

This treats variety royalties as a deliberate investable asset. But it is internal reinvestment, not the sale or securitization of the royalty itself.

Equity in holders. The third structure is where the only fresh outside capital is actually arriving. It tells you the market is forming on the equity side, not the royalty side.

In November 2025, KB Investment, part of Korea's KB Financial Group, led a 10 billion won (~$7.2 million) round into H&B Asia. H&B aggregates IP in club fruit varieties, holds rights to 58 of them including the Envy apple, and was founded by the former head of Zespri's Korea office.

KB became the second-largest shareholder. The signal is clear: financial capital now sees variety IP as an asset class. But KB bought equity in the company that holds the royalties, not the royalty streams. It is the agricultural equivalent of buying Royalty Pharma stock, not a royalty.

One actual royalty buy. The single recent transaction that is a true third-party royalty purchase is small, and instructive because it is so rare.

In October 2024, Royalty Management Holding Corporation (Nasdaq: RMCO), a small Indiana firm, bought an equity interest plus a royalty stream on patented controlled-environment-agriculture consumables. The royalty runs at 1.4% to 2.2% of sales, disclosed in an SEC 8-K.

It is a real outside buyer acquiring a defined agricultural royalty, the correct structure. But the scale, a sub-$60 million-market-cap acquirer and one undisclosed counterparty, underlines the absence of an institutional market rather than contradicting it. One micro-cap doing one small deal is the exception that proves how empty the field is.

Enforcement as price discovery. The other recent activity is enforcement. It matters because damages reveal what a variety royalty is worth, priced in the negative.

The last three years produced a run of cases, almost all on Zespri's SunGold, whose unauthorized plantings in China now exceed the entire New Zealand area.

A New Zealand court awarded Zespri roughly NZ$15 million (~$8.8 million) against Haoyu Gao for taking protected vines to China. In 2025, in the first significant win inside China, the Wuhan court ordered a grower to pay RMB 5.246 million (~$0.77 million), enabled by China's 2022 Seed Law reforms.

These are not financing transactions. But they price the right. A court putting a NZ$15 million or RMB 5.2 million number on infringement of a single fruit variety is the clearest statement that the underlying stream is a substantial, defensible asset, the same asset no one is yet financing.

| Agricultural variety financing structure | Example | What it is | What it is not |

|---|---|---|---|

| Third-party royalty buy | RMCO / CEA, 1.4-2.2% of sales (2024) | Outside buyer of a defined royalty | Institutional scale |

| Licence release for upfront cash | Zespri SunGold (~$113M / round) | Holder selling its own variety | Sale to a financial buyer |

| Royalty reinvestment programme | Plant & Food kiwifruit programme | Recycling royalty income | A tradable royalty |

| Equity into variety-IP aggregator | KB into H&B Asia (~$7.2M, 2025) | Equity in the holder | Purchase of the stream |

| Breeder/grower co-investment | T&G Global on Envy | Shared-cost development | Third-party royalty finance |

USD conversions at late-May 2026 rates: NZ$1 = $0.587, RMB 1 = $0.147, KRW 10bn as the disclosed ~$7.2 million.

So the difference is not subtle. Pharma has outright royalty sales, securitizations, and dedicated funds. Agriculture has self-financing, internal reinvestment, and a little equity into the holding companies.

The instrument that defines pharmaceutical royalty finance, a third party buying a defined stream for an upfront and bearing its performance, is essentially absent in agriculture. The underlying right is just as enforceable.

The industry has named the gap itself. Growers' associations describe the trouble of funding a new club variety in its early years, when volumes are too small to throw off the royalties needed for the rollout. Funding it out of current returns, they say, is the wrong approach. That is exactly the upfront-against-future-royalty problem monetization solves in pharma, and that no one is solving here.

Crop traits: the largest, least financeable market

A step removed from the variety is the trait, the engineered genetic input licensed into seeds across the industry. This is a far larger royalty economy than fruit varieties. And it is almost the opposite of financeable, despite its size.

The trait market among the majors is enormous, and structured as cross-licensing and per-acre trait fees. Corteva's recent disclosures give the clearest numbers.

Its comprehensive settlement with Bayer, a one-time $610 million payment, finalized in late 2025, resolved all freedom-to-operate litigation. It pulled Corteva's path to royalty neutrality forward to 2026, from a net outflow of roughly $700 million five years before.

Corteva has set a goal of a $1 billion net royalty income position by 2035 and a shift to net out-licensor. It is spinning its seed business into a standalone company in the second half of 2026, with corn-trait out-licensing expected as early as 2027.

These figures describe a royalty economy of hundreds of millions to a billion dollars a year, at a single company.

So what kind of market is this? Vast, patent-backed, enforceable to the Supreme Court via Bowman. But concentrated in a handful of counterparties, Corteva, Bayer, a few others, who trade traits among themselves under multi-year cross-licences.

That concentration is the opposite of the diversified-payer property that makes a stream financeable on its own. A trait royalty is creditworthy because the payer is an investment-grade major, not because the pool is granular. And an investment-grade major funds itself far more cheaply at the corporate level than any monetization would clear.

So the largest non-pharma royalty market is among the least likely to ever need a financing layer. It is the same cost-of-capital reason the largest pharmaceutical holders do not securitize their own books. Size and financeability point in opposite directions here.

A note on crop protection. Agrochemical active ingredients carry royalty-bearing licences, but the market trades more often as outright divestment, the active ingredient and its registrations sold as a package. That is M&A, not royalty finance, and the portfolios sit with a few majors.

Platform and bioprocessing: the closest analog

The vertical closest to pharma is not agricultural at all. It is the platform layer underneath modern biologic drugs: the conjugation chemistries, linkers, and bioproduction tools licensed program by program into other companies' medicines.

The antibody-drug-conjugate toolkit is the cleanest example. Synaffix, a Lonza company since 2023, licenses its site-specific conjugation platform, GlycoConnect, HydraSpace, and toxSYN linker-payloads, to drug developers.

The terms are pure pharma: an upfront, then clinical, regulatory, and commercial milestones, then royalties on net sales. The structure is identical to a pharmaceutical licence because it effectively is one.

The 2023 SOTIO agreement carried up to $740 million plus royalties across three ADC programs. The January 2026 multi-target deal with Sidewinder Therapeutics, backed by OrbiMed, extended the same structure across multiple bispecific programs.

In each case the licensor takes no clinical risk on any one molecule. It earns a royalty wherever its chemistry ends up in an approved drug, across however many programs license it.

This is the strongest adjacency in the survey, because it is barely an adjacency at all. A platform royalty is patent-protected, runs on net drug sales, and carries the same milestone-and-tiered-royalty terms as a pharmaceutical licence. It spreads across many programs and counterparties, so it is better diversified than the single-drug royalties that dominate pharma deal flow.

To a buyer that already underwrites pharmaceutical streams, it needs almost no new machinery. It is the same instrument, one rung up the supply chain. That is why this layer, rather than seeds, is where the pharmaceutical royalty market is most likely to extend first.

The precedent outside pharma: music

Surveys of white space are stronger when they can point to where the thing has actually happened. For non-pharma IP royalties, that place is music. The lesson is double-edged.

Music royalties have been bundled into rated, tradable, securitized paper over the last several years. Diversification across hundreds of thousands of songs is what lets no single track sink the structure.

It proves that royalty cash flows from outside pharma can be made into investment-grade instruments, when the pool is granular enough. The binding constraint is diversification and structure, not the nature of the right.

The qualifier is that music has a property the other verticals only partly share. A catalog of a million songs is granular in a way a portfolio of a few dozen fruit varieties is not. Granularity is what makes the rated-paper math work.

The lesson matches what pharma learned the hard way with Yale's Zerit trust. A single-asset securitization is fragile. Investment-grade ratings on volatile cash flows come from stacking diversification and structural protection, as DRI's pooled trust and the music ABS both show.

If a non-pharma royalty financing market is ever built, it will be built by aggregating many small streams, not by single-asset deals. That is the same conclusion the oil-and-gas securitization market reached. It is the central design constraint for anyone who would build the missing agricultural layer.

Where the gap is widest

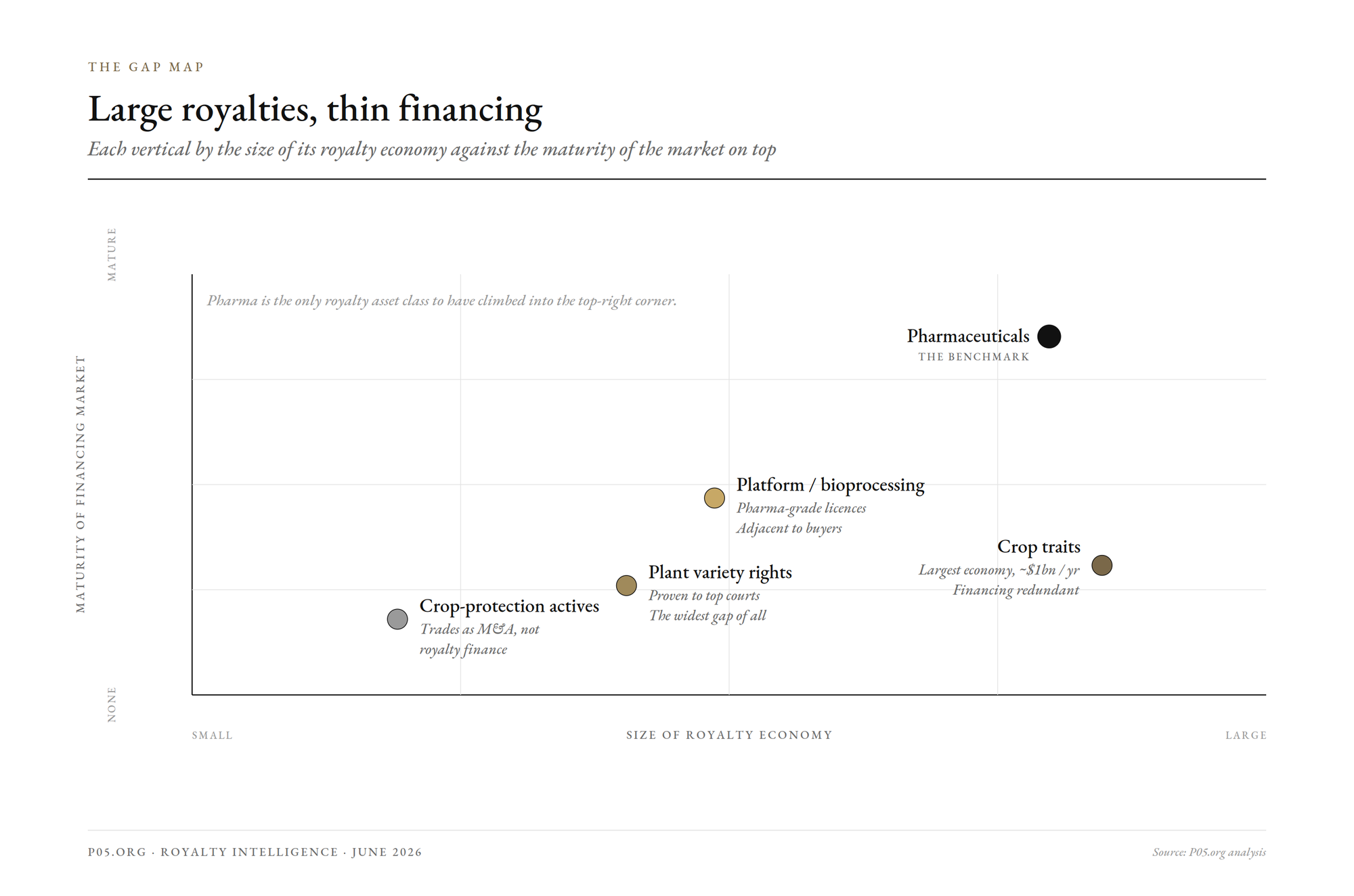

The verticals sort into a clear order, by the distance between the royalty economy that exists and the financing market that does not.

| Vertical | Royalty economy | Enforceability | Financing market | Gap |

|---|---|---|---|---|

| Platform / bioprocessing | Large, growing | Pharma-grade licences | Adjacent to pharma buyers | Smallest |

| Plant variety rights | Large, documented | Supreme Court / CJEU upheld | Equity into holders only | Widest interesting |

| Crop traits | Largest ($1bn+/yr) | Bowman, to Supreme Court | Redundant, cheap corporate funding | Structural, not a gap |

| Crop-protection actives | Real | Patent-backed | M&A, not royalty finance | Outside scope |

Platform and bioprocessing has the smallest gap. The streams are structurally identical to pharmaceutical royalties, diversified across programs, and evaluable by the existing buyer base with no new tooling. If any non-pharma royalty becomes financeable soon, this is it, because it is barely non-pharma.

Plant variety rights have the widest interesting gap. The cash flows clear all four tests. Enforceability is proven to the highest courts in the US, the EU, and Japan. The collection infrastructure is built. The per-unit economics are documented to the dollar.

Yet the only financing activity is equity into holders, licence self-financing, and internal reinvestment, never the monetization or securitization that pharma's universities have done since 2000. This is the purest case of a real, proven royalty economy with no financing market on top.

Crop traits have the largest economy and the least need for financing, concentrated among investment-grade majors who fund themselves more cheaply than any monetization would clear. Crop-protection actives sit mostly outside royalty finance, trading as M&A.

The common thread runs through pharma too. A royalty becomes financeable not when the cash flow exists, which it does everywhere here, but when a diversified pool meets a buyer whose cost of capital makes monetizing it worthwhile, and an arranger willing to aggregate.

Pharma assembled all three over two decades. The platform layer has the streams and the buyers, and waits on aggregation. Seeds have the streams, the enforceability, and the infrastructure, and wait on the buyer and the arranger that pharma's universities found years ago.

The verdict

The royalty economy is far larger than the royalty financing market. Most of the difference sits outside pharmaceuticals.

Seeds, crop traits, branded fruit varieties, and bioprocessing platforms all generate patent-backed, defined-term royalty streams. For plant variety rights, the enforceability and the collection plumbing are not just present but proven in court, across the US, the EU, and Japan, with Korea's move from royalty dependence to sovereignty as a live demonstration.

What is missing is not the cash flow, and not the legal right. It is the financing layer that pharmaceutical royalties spent two decades building, the layer that lets an Emory or NYU turn a discovery royalty into a nine-figure upfront, or a Yale into rated paper.

The only fresh capital arriving in agriculture buys equity in the companies that hold variety IP, not the royalties themselves. The market is forming one layer above where pharma's did.

Whether the missing layer gets built depends on the same arithmetic that built it in pharma, and on the lesson both music and Yale's Zerit teach: aggregate, do not single-asset.

The platform streams are closest to crossing over, because they are pharmaceutical royalties in all but name. The seed and variety streams are the most structurally sound case of a financing market that does not yet exist, proven cash flows in search of an arranger. The trait economy, for all its size, may never need one.

Taking stock in 2026: real, enforceable, documented royalties almost everywhere, and a financing market almost nowhere. The open question is which of these verticals, if any, follows the path pharma already walked.

All information in this report was accurate as of the research date and is derived from publicly available sources including court opinions, regulatory guidance, university and industry disclosures, SEC filings, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.