The Re-Rate: How a Royalty Rate Changes Over a Deal's Life

The rate quoted on a press release is a headline. What is actually paid is a function with arguments, and most of those arguments are drafted to move it.

A royalty re-rates in two distinct places. The first is inside the underlying licence, where tiers, base adjustments, step-downs and erosion triggers fire by contract over the product's commercial life. The second is inside the monetisation, where a fund and a seller re-cut the economics of an interest that has already been sold. The two are easy to conflate because both are quoted as a percentage of net sales, a point worked through in Why a Licensing Royalty and a Financing Royalty Are Not the Same Thing. This piece takes them in turn.

The market in the second category is large and growing. Aggregate royalty-finance transaction value reached roughly $6.5 billion in 2025, up from about $5.7 billion in 2024 and under $200 million a year in the early 2000s, the trajectory traced in The State of the Pharmaceutical Royalty Market, May 2026. Each of those transactions priced a re-rate schedule of one kind or another.

The mechanisms divide cleanly between the two categories. Numbers one through seven below live in the commercial licence; the monetisation re-rates sit on top of them.

| # | Mechanism | What triggers it | Effect on the rate |

|---|---|---|---|

| 1 | Net-sales tiers | Cumulative annual sales cross a band | Rate steps up (licence) or down (synthetic) |

| 2 | Combination-product base | Product sold inside a combination | Royalty base shrinks by an allocation fraction |

| 3 | Royalty term | A patent, time or exclusivity leg expires | Stream ends, country by country |

| 4 | Patent step-down / no valid claim | Patent lapses or does not cover the product | Rate cut to the know-how level |

| 5 | Generic / biosimilar erosion | Competitor unit share crosses a threshold | Rate cut by a fixed proportion |

| 6 | Stacking offset | Licensee in-licenses a third-party patent | Third-party royalty deducted, capped |

| 7 | Floor and cumulative cap | Reductions accumulate | Decline halts at a contractual minimum |

Part I. The in-licence re-rate

1. Net-sales tiers

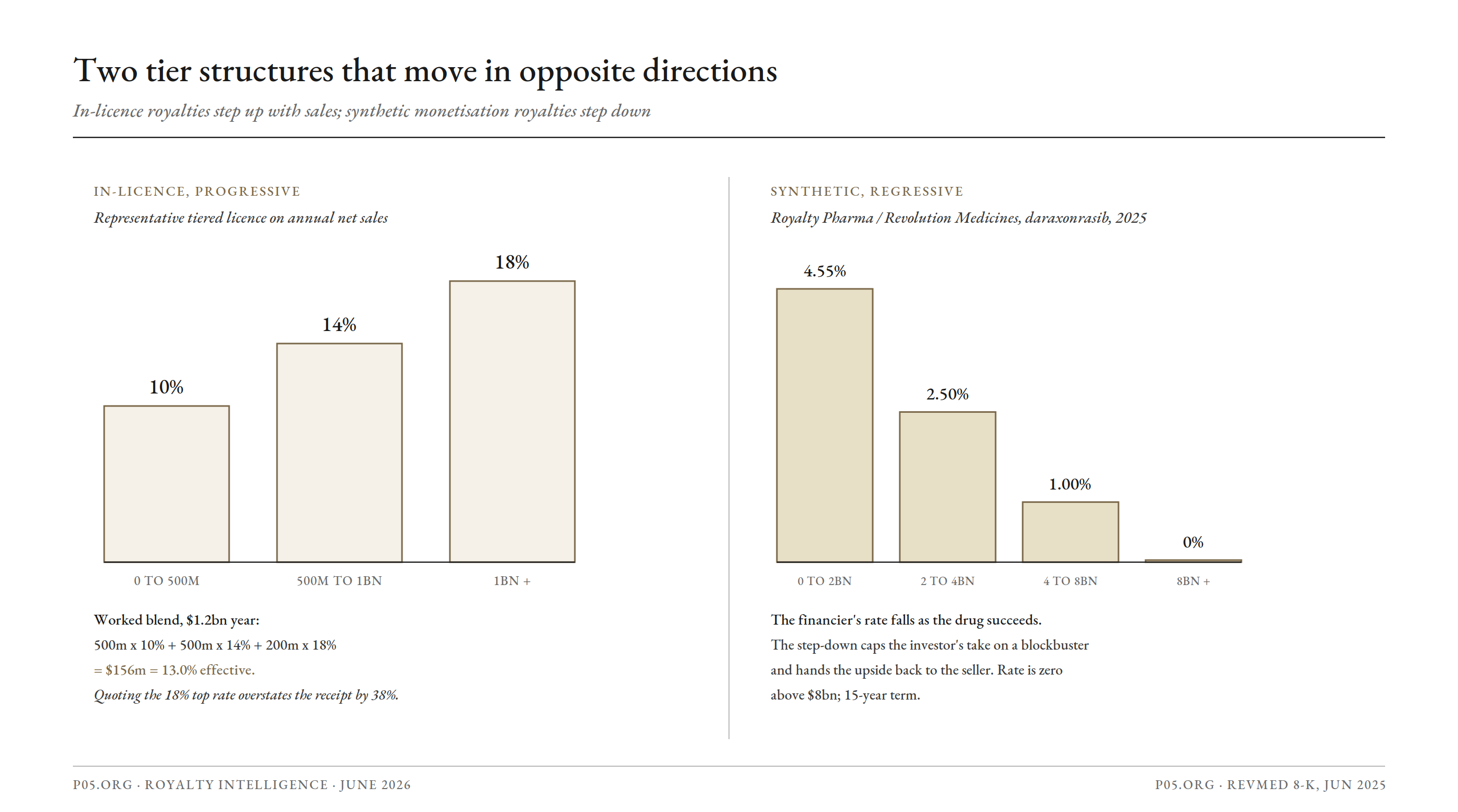

The first re-rate is built in deliberately. Rather than a flat percentage, tiered structures apply different rates to different annual net-sales bands, so the rate the licensor earns rises as the product grows. The tiers are almost always incremental rather than cliff, meaning the higher rate applies only to the marginal dollar above each threshold, never retroactively to the whole base.

The distinction is the difference between the headline and the cash flow. A representative schedule, applied to a $1.2 billion year, produces a blended rate well below its own top tier.

| Net-sales band | Marginal rate | Royalty on the band |

|---|---|---|

| 0 to 500m | 10% | $50.0m |

| 500m to 1bn | 14% | $70.0m |

| 1bn and above (here 200m) | 18% | $36.0m |

| Total | 13.0% blended | $156.0m |

The bands reset each January. The rate therefore returns to the bottom tier at the start of every year and climbs as cumulative sales accrue, which produces a quarterly sawtooth in receipts that is a function of the calendar rather than demand. The synthetic mirror image of this structure, where the rate falls as sales rise, is covered in Part II and shown alongside it below.

2. The combination-product base

Before any rate is applied, the base it applies to can itself be adjusted. When the licensed product is sold inside a combination, a fixed-dose pairing, a device-plus-drug, or a multi-analyte diagnostic, royalties are paid on a fraction of the combination price rather than the whole. Contracts define that fraction in one of three ways.

| Situation | Allocation fraction |

|---|---|

| Components sold separately | A / (A+B) by selling price, where A is the licensed component |

| Not sold separately | Cost-based fraction (relative allocated or direct manufacturing cost) |

| Diagnostics | Medicare-allowable-rate split, often floored at "never less than 33%" |

Because this adjustment changes the base and not the stated rate, it does not appear as a rate change at all, yet it can move the effective rate as much as any explicit reduction. The mechanics are the same ones that govern the multi-component products examined in How Veterinary Royalty Deals Are Built.

The combination base is also where a current dispute sits. Royalty Pharma holds a royalty on Vertex's cystic-fibrosis franchise under which, for combination therapies, sales are allocated equally to each active ingredient and royalties are paid only on the royalty-bearing components. Vertex's newer triple Alyftrek contains deutivacaftor, a deuterated form of ivacaftor.

Royalty Pharma values the blended Alyftrek royalty at roughly 8 percent on the basis that deutivacaftor is the same as ivacaftor and therefore royalty-bearing; Vertex has paid roughly 4 percent, treating it as not royalty-bearing. Royalty Pharma commenced the contractual dispute-resolution process in late 2025. The effective rate on a multi-billion-dollar product turns on whether one deuterated analogue counts as the same molecule.

3. The royalty term

The term sets how long anything is owed, and it is the re-rate that ends the stream. It is rarely a single date. The standard construction is a "later-of" across three legs, computed separately for each country and product.

| Leg | Ends on |

|---|---|

| Patent | Expiry of the last valid claim covering the product in that country |

| Time | A fixed period, commonly ten years from first commercial sale in that country |

| Exclusivity | Expiry of all regulatory exclusivity in that country |

The term is the latest of the three, so a global stream does not stop on one day; it decays as territories roll off. The time leg exists because of US patent-misuse law, where the position differs from Europe and remains live in the courts.

| Authority | Year | Holding |

|---|---|---|

| Brulotte v. Thys | 1964 | No royalties on a US patent after it expires |

| Kimble v. Marvel | 2015 | Reaffirmed Brulotte; a hybrid step-down to a know-how rate is permitted |

| Ares Trading v. Dyax (3d Cir.) | 2024 | Reach-through royalties on pre-expiry use of a patented platform survive expiry |

Europe imposes no equivalent limit on royalty-term length, which is one reason an ex-US tail can run longer than the US stream in the same contract.

4. The patent step-down and the no-valid-claim cut

The hybrid licence is the workaround Brulotte produced. It makes the royalty consideration for patent and know-how together, then steps the rate down on patent expiry to a lower figure representing the know-how alone; the illustration drawn from Kimble itself is 5 percent stepping to 4 percent.

The narrower and far more common form is the no-valid-claim reduction, which cuts the rate country by country whenever the product is not covered by a valid claim in the market of sale, whether because a patent was invalidated, a claim never issued, or nothing was filed there. The size of the cut is a percentage of the otherwise-applicable tier and is redacted in most public filings.

5. Generic and biosimilar erosion

Patent expiry and competitor entry are separate events, and the contract treats them separately, keying the erosion trigger to the competitor's actual unit share rather than to any patent date.

For small molecules, the construction is usually a single threshold: in one Jazz / Codiak agreement, once generic or biosimilar units cross a defined share of total unit sales in a country, the royalty there is cut by a fixed proportion, and a 10 percent threshold triggers several quarters earlier than a 40 percent one. Biologics are handled with more gradation: a typical biosimilar clause in Roche, Immunocore and Lilly agreements scales the reduction to the biosimilar's valid-claim status and share, reflecting the slower, shallower erosion that biologics see relative to small molecules.

6. Stacking offsets

The reductions above are triggered by the calendar or a competitor. The stacking offset is triggered by the licensee itself, when it has to in-license a third party's patent to sell the product. A royalty-stacking clause then lets it offset those third-party royalties against the primary licensor's, commonly up to half, so a 10 percent primary rate against a 2 percent third-party licence becomes 8 percent under a full offset.

Two factors set the size of the effect. The first is whether the third-party patent is genuinely blocking, meaning the product infringes it, or merely an improvement. The second is a documented second-order effect: anti-stacking clauses can increase total stacking, because a later licensor that expects its rate to be partly absorbed by the offset has reason to demand more. The same study reports such clauses in about one in six percentage-royalty contracts.

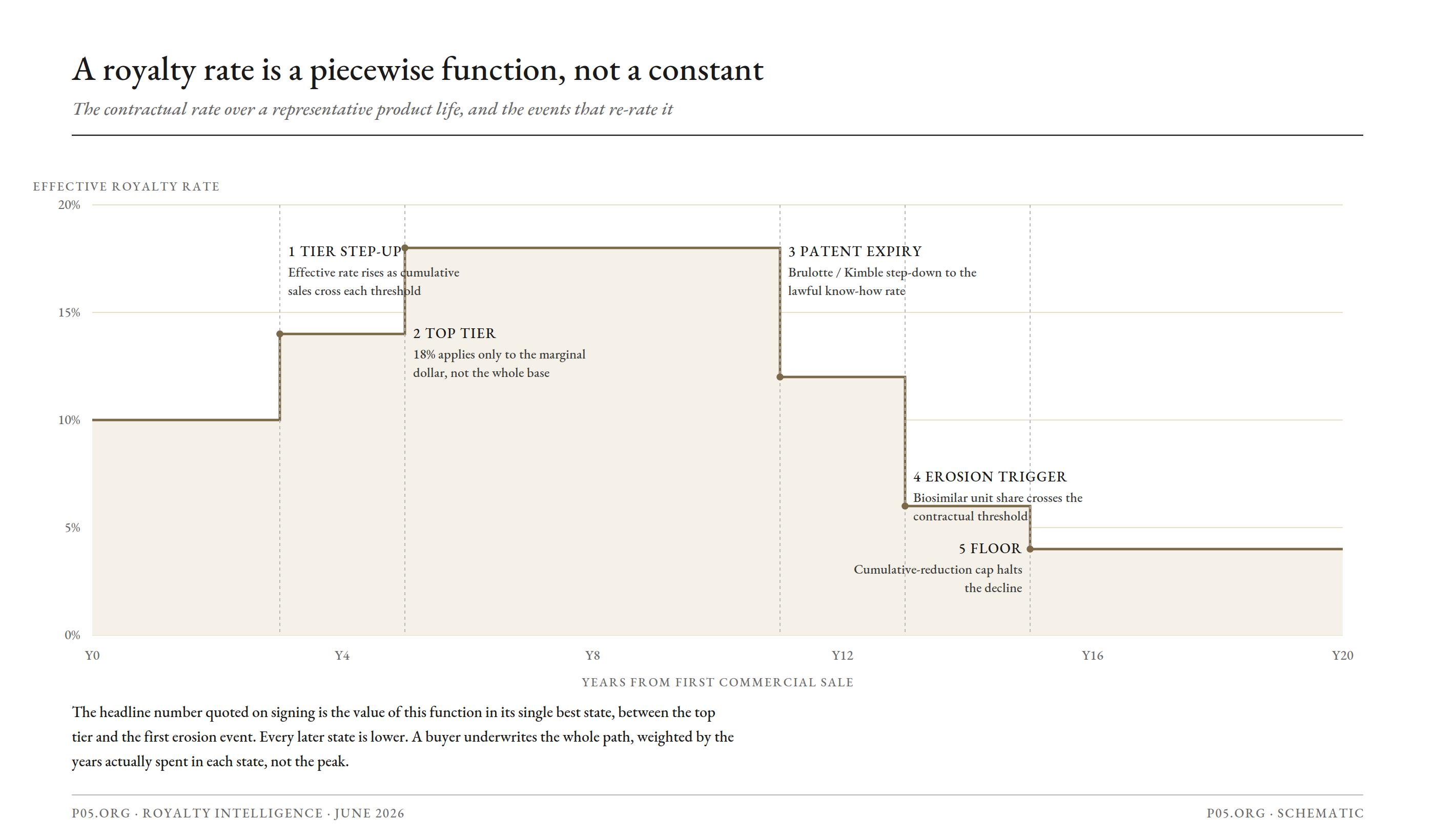

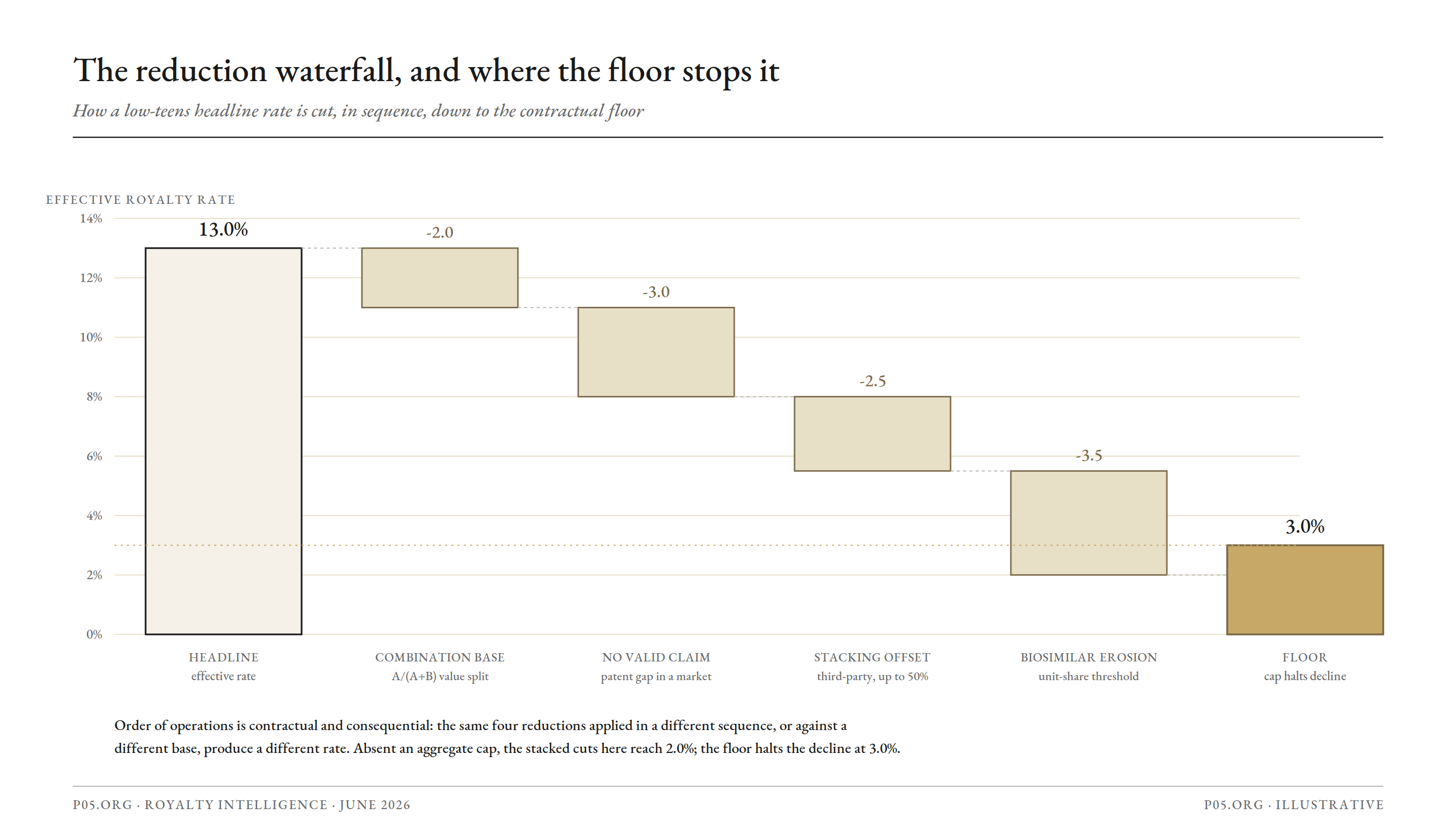

7. The floor, the cumulative cap, and order of operations

The reductions do not run to zero, because the licensor negotiates a floor. It usually takes two forms in the same agreement: an aggregate cap, under which the combined cuts cannot take the rate below a stated fraction of the headline, and an absolute floor, a minimum running royalty that holds regardless of how many triggers fire.

When several reductions apply in the same quarter, the order in which they are calculated changes the result. Agreements that specify the sequence and supply a worked exhibit settle the point at signing; those that leave it open leave room for the audit disputes that follow. The waterfall below shows a headline effective rate cut through four reductions until the floor halts the decline.

Part II. The monetisation re-rate

A royalty deal rarely ends at signing. Once an interest is sold, the parties often return and re-cut it, and the 2025-26 vintage of structures runs to step-up and step-down rates, staged tranches, put and call rights, return caps, debt-like covenants and make-whole payments. Every such structure sits somewhere on three axes.

| Dimension | Options |

|---|---|

| Source | Traditional (monetising an existing licence royalty) or synthetic (selling a slice of the company's own future sales) |

| Return | Usually capped at a multiple of the investment (a MOIC cap) |

| Post-cap | No tail (the stream reverts entirely to the seller) or tail (the fund keeps a residual share) |

Synthetic royalties step down where licences step up

The clearest structural contrast in the market is directional. An in-licence royalty steps up with sales to share the upside with the originator. A synthetic royalty, sold on the company's own future sales, commonly does the opposite.

The June 2025 Royalty Pharma and Revolution Medicines agreement is the reference case. Royalty Pharma funds up to $1.25 billion for tiered royalties on daraxonrasib over a fifteen-year term, and the rate falls as sales rise.

| Annual net sales | Royalty rate |

|---|---|

| 0 to 2bn | 4.55% |

| 2bn to 4bn | 2.50% |

| 4bn to 8bn | 1.00% |

| Above 8bn | 0% |

The regressive schedule caps the financier's take on a blockbuster and returns the upside to the company. The structure also gates activation: the funding is split into five $250 million tranches, the first two payable before FDA approval, and royalty obligations begin only after approval. A senior secured loan of up to $750 million sits alongside it, and by an April 2026 amendment the funded amount had reached $500 million.

The time-stepped multiple

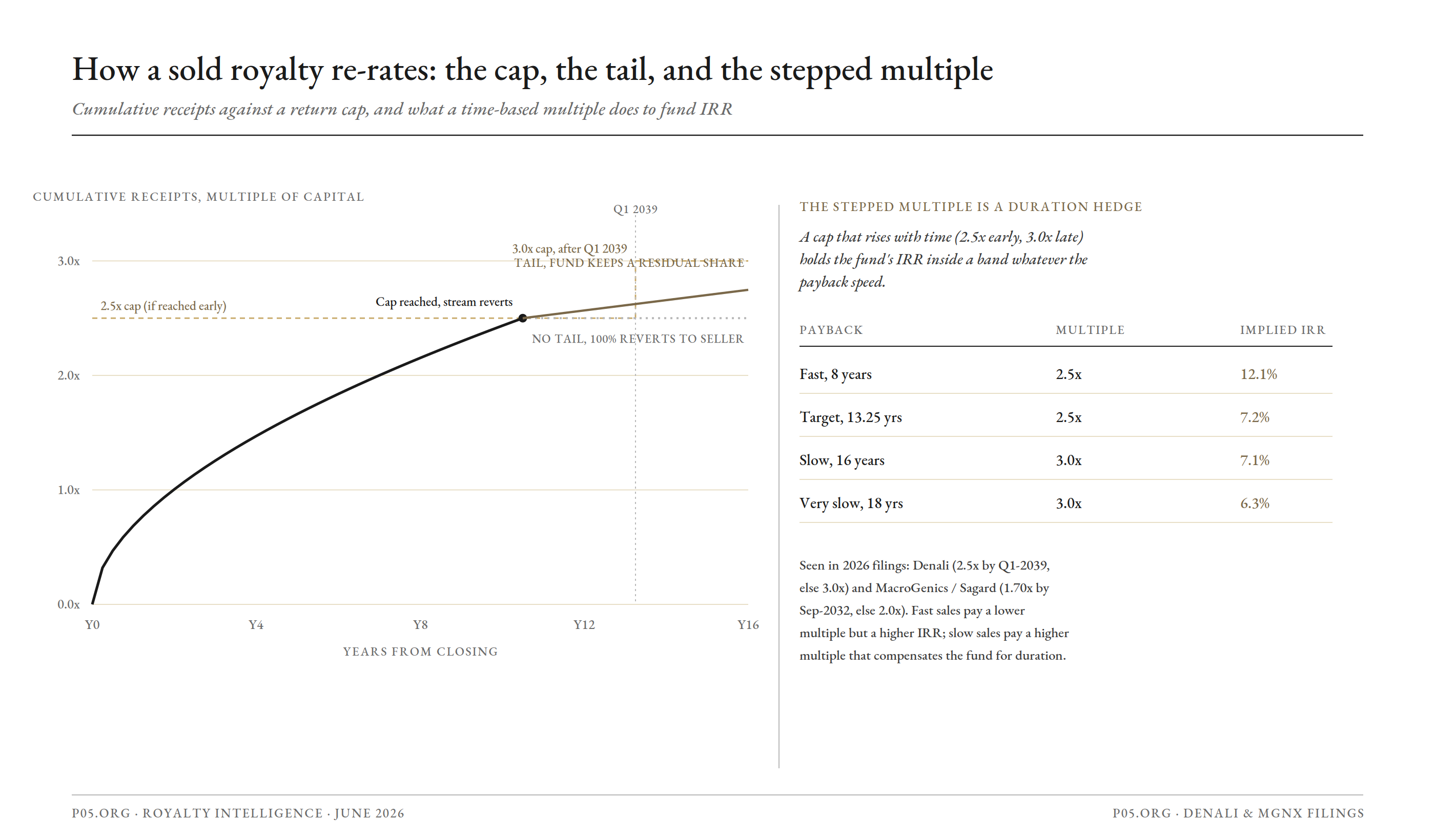

A return cap that rises with time is now a recurring feature, and it appears in nearly identical form across deals and across years. It re-rates the deal by reference to how fast the fund is repaid rather than to anything in the underlying licence.

| Deal | Date | Capital | Cap |

|---|---|---|---|

| AnaptysBio / Sagard (Jemperli) | 2023, amended 2024 | $250m, then +$50m | $600m by 31 Mar 2031, else $675m |

| Royalty Pharma / Denali (tividenofusp alfa) | Dec 2025 | $200m + $75m on EMA approval | 2.5x by Q1 2039, else 3.0x |

| MacroGenics / Sagard (ZYNYZ) | May 2026 | +$60m, to $130m aggregate | 1.70x by 30 Sep 2032, else 2.0x |

The AnaptysBio sequence is the fullest illustration of a stream re-rated over time. AnaptysBio first sold Sagard its 8 percent Jemperli royalty on sales below $1 billion for $250 million, retaining the 12 to 25 percent tiers above that level. A 2024 amendment added $50 million and reset the payoff to the time-stepped cap shown above. Successive documents restructured who owned which slice of the same GSK payment obligation, each amendment a re-rate of the last.

Expressed as an internal rate of return, the multiple and the date together describe a band rather than a point. Reaching the lower multiple early implies a higher IRR over a shorter hold; taking longer allows the higher multiple, which raises the absolute return as the hold extends. The chart works the Denali band.

Suppression, buy-outs, and basket swaps

Three further structures complete the toolkit, each re-rating a sold interest without touching the underlying licence rate.

| Structure | Example | Mechanic |

|---|---|---|

| Temporary suppression | Apellis / Sobi (2025) | Royalty cut to 10% of the contractual amount from 1 Jul 2025 for an upfront; resumes once a bought-out amount reaches a hard cap |

| Cap plus buy-out | Candel (Feb 2026) | Royalty runs from first US sale to a $250m cap; a change of control triggers a timing-based buy-out; conditioned on FDA approval by a set date |

| Basket swap | XOMA / Takeda (2025) | Takeda's royalty and milestone obligations on Mezagitamab reduced; XOMA gains rights across nine development-stage assets |

In the suppression case, the rate actually paid during the window is a tenth of the contractual rate, returning to full once the cap is met. Amendments of this kind can also surface in distress: when Clearside Biomedical entered Chapter 11 in late 2025, equity holders focused on a September 2025 amendment to its HealthCare Royalty Partners agreement that had waived a contingent payment, the kind of pre-petition re-rate that the value-break analysis in that piece turns on.

The 2025-26 deal tape

The structures above sit in a market that consolidated through the period, tracked week to week in the Weekly Term Sheet.

| Date | Parties | Asset | Headline value |

|---|---|---|---|

| Feb 2025 | Royalty Pharma / Biogen | litifilimab | up to $250m R&D funding |

| Jun 2025 | Royalty Pharma / Revolution Medicines | daraxonrasib | $2.0bn ($1.25bn synthetic + $750m loan) |

| Mid 2025 | KKR / HealthCare Royalty Partners | platform | majority stake |

| 2025 | BridgeBio / HCRx + Blue Owl | Beyonttra (EU) | $300m |

| 2025 | BeOne / Royalty Pharma | Amgen Imdelltra | up to $950m |

| Q4 2025 | Blackstone / Merck | sac-TMT | $700m synthetic |

| Nov 2025 | Blackstone / Royalty Pharma | Alnylam Amvuttra | $310m |

| Dec 2025 | Royalty Pharma / Denali | tividenofusp alfa | $275m |

| Dec 2025 | Royalty Pharma / PTC | Evrysdi | $240m + up to $60m |

| Apr 2026 | Ligand / XOMA Royalty | 200+ asset portfolio | ~$739m + litigation CVR |

| May 2026 | MacroGenics / Sagard | ZYNYZ | +$60m, to $130m |

Royalty Pharma reported $2.6 billion deployed in 2025 and portfolio receipts up 16 percent to $3.25 billion. How a transaction of this kind tends to move the seller's equity is the subject of Royalty Financing and the Share Price.

Negotiating positions

Each mechanism allocates risk between the two sides, and the bargaining runs along predictable lines.

| Mechanism | Licensor / seller position | Licensee / buyer position |

|---|---|---|

| Tiers | High thresholds, steep step-ups, annual reset | Low step-ups, lifetime cumulative thresholds |

| Combination base | Price-based A/(A+B), high floor fraction | Cost-based fraction, no floor, licensee determination |

| Royalty term | Longest later-of leg, long fixed period | Strict tie to patent life, short fixed period |

| Patent step-down | Small step-down, broad know-how definition | Large step-down, narrow know-how definition |

| Generic / biosimilar | High share threshold, small cut | Low share threshold, large cut |

| Stacking offset | Shallow cap, blocking patents only, review rights | Deep cap, all third-party licences, no review |

| Floor and cap | High floor, low aggregate reduction cap | No floor, deep aggregate cap |

The single measure that reconciles all of these terms is the effective royalty rate: the one rate that, applied to projected lifetime net sales, reproduces the present value of every tiered, based, stepped and reduced payment. On the monetisation side the analogue is the MOIC cap together with the time to reach it.

Where the re-rate sits in a monetisation

Two features recur in the purchase agreements that buy these streams. The seller is typically required to notify the buyer of any actual or potential royalty reductions, permitted ones included, for the life of the stream; and counsel examine title, liens and the reduction provisions of the underlying licence as part of the technical review. The same documents carry the assignment and change-of-control language examined in Anti-Pledge Provisions in Pharmaceutical Royalty Financing, and, where the stream is leveraged or wrapped, interact with the structures set out in Capitalising the Royalty Stream and Insuring the Royalty Stream.

The contractual items that, together, define the schedule of states a rate moves through:

| Item | Where it sits | What it governs |

|---|---|---|

| Royalty term, by country | Definitions | When each territory's stream ends |

| Tier schedule and reset | Royalty section | The blended rate at a given sales level |

| Combination-product fraction | Net sales definition | The base the rate is applied to |

| No-valid-claim and step-down | Reduction section | The rate where patents lapse or do not cover |

| Generic / biosimilar trigger | Reduction section | The rate and timing after competitor entry |

| Stacking offset and cap | Reduction section | Deductions for third-party royalties |

| Floor and aggregate cap | Reduction section | The minimum the rate can reach |

| MOIC cap, tail, tranches | Purchase agreement | The monetisation return and its duration |

Summary

A royalty rate is a piecewise function of time, cumulative sales, patent status, competitor share, third-party licensing and the royalty base, bounded below by a floor. In a monetisation, a further set of terms, the cap, the tail, the multiple, the suppression window, the buy-out, sits on top of that function and can be re-cut by amendment after signing. The headline rate is the value of the function in a single state. The mechanisms above describe the other states and the events that move between them.

All information in this report was accurate as of the research date and is derived from publicly available sources including court opinions, regulatory guidance, academic literature, SEC filings, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.