The Royalty Spin-Off: When a Biotech Separates Its Royalties From Its Pipeline

A drug-discovery company that out-licenses an asset to a larger partner ends up holding two very different things.

One is a royalty on the partner's future sales, a contractual cash flow with a defined lifespan. The other is the rest of the pipeline, a set of programmes whose value depends on clinical and regulatory outcomes.

On a single balance sheet the two sit together. In a spin-off, they are pulled apart into two publicly traded companies, with the royalty placed in an entity that does little except collect and distribute it.

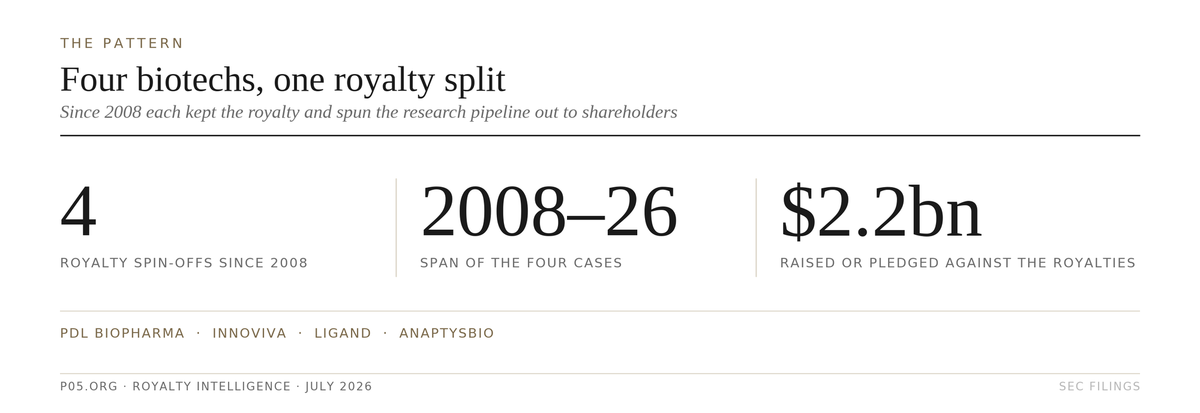

The pattern: four royalty spin-offs since 2008, and roughly $2.2bn raised or pledged against the royalties.

This structure has appeared four times over roughly eighteen years, and the shape has been consistent each time.

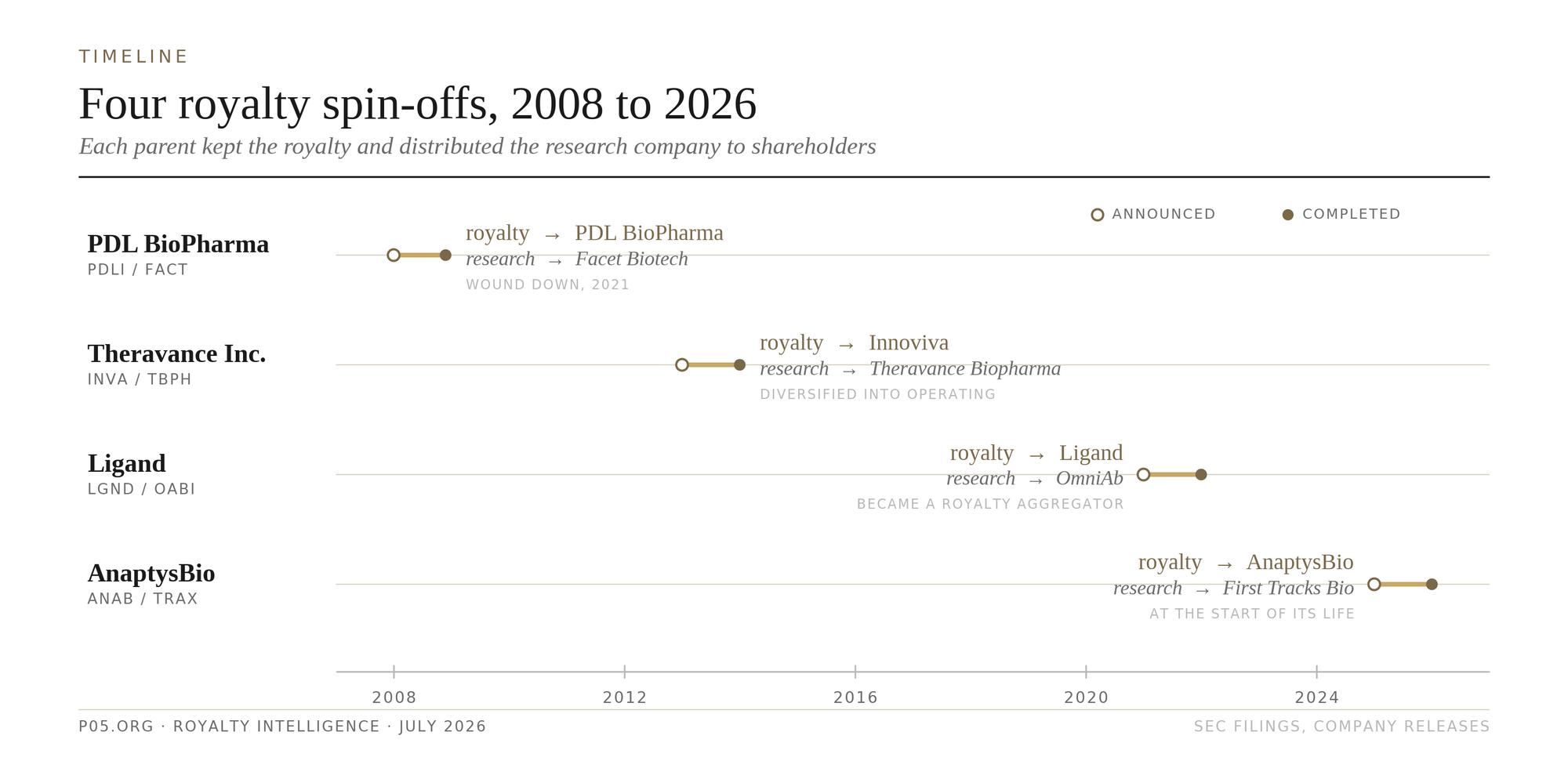

The company that keeps the royalty is the parent, or RemainCo, which retains the original listing and usually the name. The research operations are packaged into a new company, the SpinCo, and distributed to existing shareholders as a stock dividend.

The royalty entity is left with minimal staff, and its stated job is to return the value of the royalty to shareholders.

The four instances are PDL BioPharma's spin-off of Facet Biotech in 2008, Theravance's spin-off of Theravance Biopharma in 2014, Ligand's spin-off of OmniAb in 2022, and AnaptysBio's spin-off of First Tracks Biotherapeutics in 2026.

| Parent (year announced) | Royalty entity (RemainCo) | Research entity (SpinCo) | Tickers |

|---|---|---|---|

| PDL BioPharma (2008) | PDL BioPharma | Facet Biotech | PDLI / FACT |

| Theravance Inc. (2013) | Innoviva (renamed 2016) | Theravance Biopharma | INVA / TBPH |

| Ligand (2021) | Ligand | OmniAb | LGND / OABI |

| AnaptysBio (2025) | AnaptysBio | First Tracks Biotherapeutics | ANAB / TRAX |

The remainder of this piece takes each in turn, sets out how the royalties pay, and closes on the common rationale and the range of outcomes.

Related manoeuvres: pivots and aggregators

The scope here is narrow on purpose: a biotech that separated a royalty into its own listed company alongside a separate research company.

A larger group of firms became royalty-focused by a different route, converting a single existing company into a royalty-driven business without any separation. These are close in spirit to the spin-offs but structurally distinct, and they are worth naming because they are often discussed alongside them.

Zymeworks. In November 2025 it announced a shift to a royalty-driven model, keeping its internal research and pipeline while reinvesting licensing cash to compound and acquire royalty streams. Its filings describe it as a hybrid royalty aggregator and biotech developer, and in June 2026 it made its first acquisition, of Theravance Biopharma.

XOMA Royalty. It pivoted in 2017 from internal drug development to a pure-play royalty aggregator, buying milestone and royalty rights from capital-constrained biotechs and holding almost no research operations, before being acquired by Ligand in July 2026.

Ligand. It is a pivot as well as a spin-off. Beyond separating OmniAb, it transformed over the 2016 to 2022 period from a formulation-technology business into an active royalty aggregator, and has continued to buy royalties and, with XOMA, whole aggregators.

Halozyme. It generates royalties through platform licensing rather than acquisition or separation, its ENHANZE drug-delivery technology producing a royalty on each partnered product. That is an origination model rather than a pivot from traditional development.

PDL BioPharma, a second time. After its antibody-humanization royalties matured, it tried between roughly 2013 and 2016 to reinvent itself as an acquirer of new royalties and income-generating assets, buying royalty streams and making structured loans, before abandoning the effort. Some of those royalties later passed to SWK Holdings, a smaller listed specialty-finance company focused on sub-25-million-dollar royalty purchases, which itself monetised most of its own book in 2025.

Enzon. It became a royalty-collecting company between 2009 and 2013 by selling its operating business and winding down clinical activity, rather than by spinning a research company out to shareholders.

Platform companies that build a royalty book from their own IP

A further group builds a royalty portfolio from a proprietary technology platform rather than by separation or acquisition. These are IP-rich companies that license a platform broadly and collect royalties across many partnered products, while in most cases continuing to develop or sell products of their own, the same hybrid shape as Zymeworks.

Antibody engineering. Xencor licenses its XmAb Fc and bispecific platform to multiple partners and holds royalties on marketed products including Ultomiris and Monjuvi, alongside its own clinical pipeline. In March 2026 its licensee Alexion took the position that it owes no further US royalties on Ultomiris and does not intend to make US payments, while continuing to pay outside the United States.

Genmab collects royalties of up to 20 percent from Johnson & Johnson on Darzalex and 22 to 26 percent outside the US and Japan on epcoritamab, plus milestones from its DuoBody and HexaBody partnerships. Its roughly 8 billion dollar acquisition of Merus, announced in September 2025, is described by the company as accelerating a shift towards a wholly owned model.

Drug delivery and formulation. Halozyme licenses its ENHANZE technology into partner products and reported 867.8 million dollars of royalty revenue in 2025. Ligand licenses its Captisol formulation technology alongside its acquired royalty book.

Medical-device coatings. Surmodics licenses its hydrophilic and performance coatings to device makers, reporting 37.4 million dollars of coating royalties and licence fees in fiscal 2024. It was taken private by the investment firm GTCR in late 2025 after the transaction cleared a Federal Trade Commission challenge in court.

Pure IP licensing. ERS Genomics, a private company founded by the CRISPR co-inventor Emmanuelle Charpentier, licenses the foundational CRISPR/Cas9 patent estate it manages, more than 130 patents worldwide, to companies across research and applied fields, with no product business of its own.

Its US position is contested: in March 2026 the Patent Trial and Appeal Board again awarded priority in eukaryotic cells to the Broad Institute, a ruling the patent owners have disputed through successive appeals. It is the clearest example of an IP estate monetised into a royalty stream with nothing else attached, the model the hybrids above run alongside their own products.

What does not fit. Companies such as BridgeBio sell their own product royalties for upfront cash as a financing tool while remaining developers and commercialisers, so they are royalty sellers rather than royalty companies. And holding companies such as Fortress Biotech, PureTech Health and Roivant retain royalties and equity in operating companies they found and spin out, but were built that way from inception rather than by dividing an existing combined business.

None of these fits the specific structure of the four cases below, which is a single company splitting into a royalty entity and a research entity.

The royalty assets and cash flows at a glance

The four royalty companies differ widely in what they hold and how much it produces, from a broad book of low-rate antibody royalties to a single high-rate stream that is still ramping.

| Royalty company | Principal royalty assets | Royalty rate | Reported royalty revenue |

|---|---|---|---|

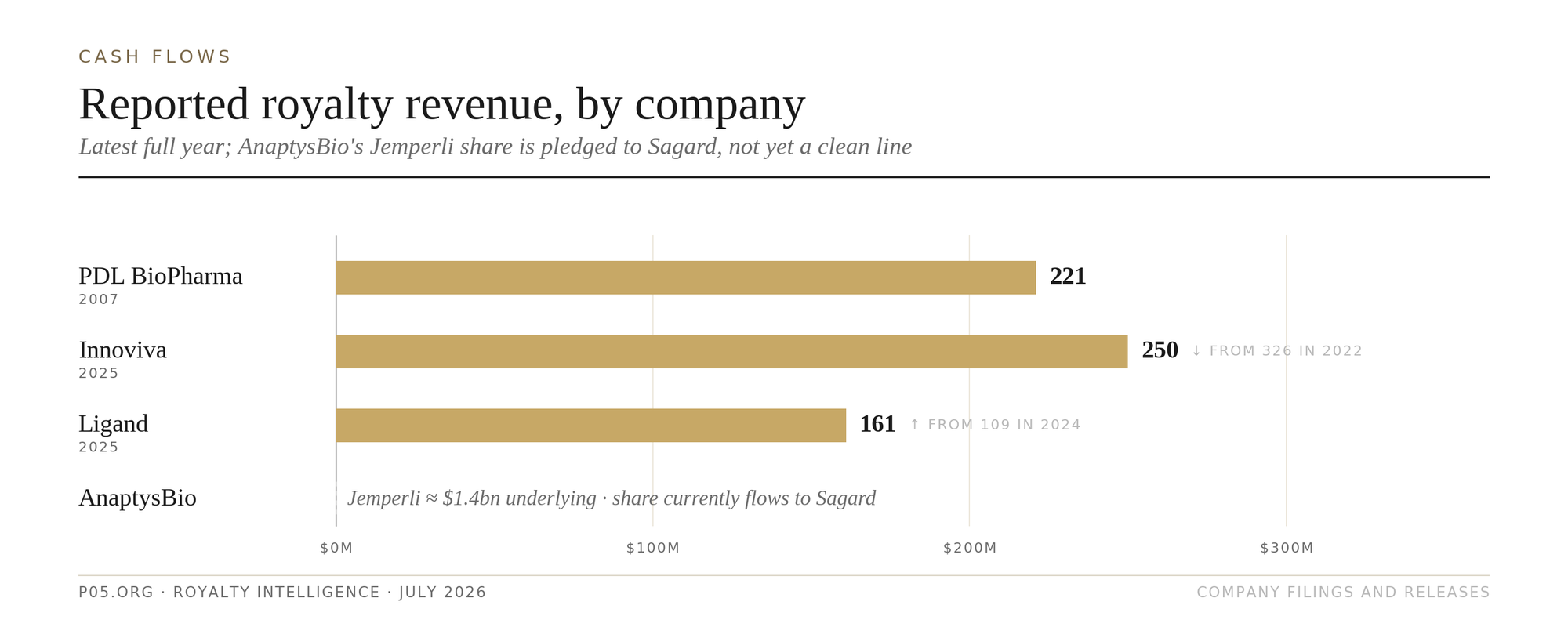

| PDL BioPharma | Avastin, Herceptin, Lucentis, Xolair, Synagis, Tysabri and other humanized antibodies (Queen et al. patents) | ~1% to 3% | 221 million dollars (2007); 270 to 280 million estimated (2008) |

| Innoviva | Relvar/Breo Ellipta, Anoro Ellipta (and a former Trelegy interest) | Breo 15% then 5%; Anoro 6.5% to 10% | 326 million dollars (2022); ~250 million (2025) |

| Ligand | Kyprolis, Filspari, Qarziba, Ohtuvayre, Capvaxive and around a dozen core assets | Kyprolis 1.5% to 3%; mostly low single digit | 109 million dollars (2024); 161 million (2025) |

| AnaptysBio | Jemperli (dostarlimab), imsidolimab | Jemperli 8% to 25% tiered; imsidolimab 10% | Jemperli underlying at a ~1.4 billion dollar run rate; the AnaptysBio share is pledged to Sagard until 600 million is repaid |

Reported royalty revenue by company. Different years and bases; AnaptysBio's Jemperli share is pledged to Sagard and not yet a clean line.

How the royalties actually pay

A few mechanics recur across all of these companies, and they matter more than the headline rate.

Tiered rates. Most of these royalties step up or down with sales rather than sitting at a single number.

Jemperli pays AnaptysBio 8 percent on the first billion dollars of annual sales, then 12, 20 and 25 percent on higher bands, so the blended rate rises as the drug grows. Breo works the other way, paying Innoviva 15 percent on the first 3 billion dollars of annual sales and 5 percent above that, so the blended rate falls as volume climbs. Anoro tiers from 6.5 to 10 percent.

Reading a tiered royalty means knowing both the rate and where current sales sit on the ladder.

How a tiered royalty pays. Jemperli's rate rises with sales, Breo's falls above the first $3bn.

Royalty, profit share, or milestone. These are three different things that often travel together.

A royalty is a percentage of a partner's net sales. A profit share, such as Theravance Biopharma's 35 percent of US Yupelri profits, is a percentage of net profit after costs, so it moves with margins as well as sales. A milestone is a one-off payment triggered by an event, an approval or a sales threshold, such as the up to 35 million dollars imsidolimab can pay AnaptysBio, or the 100 million dollar Trelegy milestone due in 2027.

A royalty company's cash is usually a mix of all three.

The payment lag. Royalties are self-reported. The licensee sells the drug, tallies net sales each quarter, and pays the following quarter, so the holder receives cash one period behind the underlying sales and relies on the partner's accounting.

This is why royalty companies hold audit rights, and why reported figures sometimes include catch-up payments once a partner reconciles.

Duration and the cliff. A royalty runs for a defined term, typically the later of the last patent's expiry or a fixed number of years from first commercial sale, then steps down or ends.

PDL's royalties were scheduled to fall within a few years of its 2008 split because the Queen patents expired in 2009. Innoviva's Breo and Anoro royalties run into the early 2030s. The term, not the current rate, sets how long the stream is worth anything.

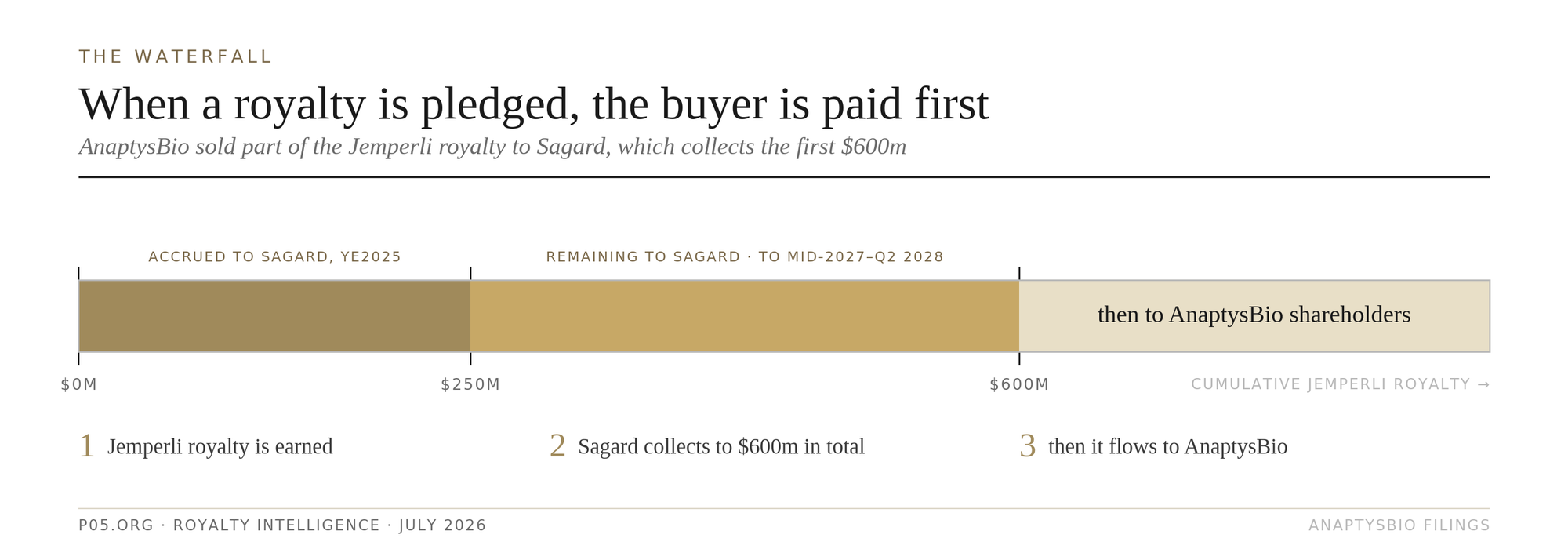

The waterfall when a royalty is pledged. A royalty company that has already monetised part of its stream shares the cash in a set order.

AnaptysBio sold part of the Jemperli royalty to Sagard, which collects Jemperli royalties until it has received a cumulative 600 million dollars. Until that is repaid, AnaptysBio's own shareholders sit behind Sagard.

A monetisation of this kind usually caps the buyer's return rather than transferring the stream outright. Zymeworks' 250 million dollar note with Royalty Pharma is repaid out of 30 percent of the Ziihera royalty and capped at 1.65 then 1.925 times the amount advanced.

The clean headline rate can therefore belong, for a period, to someone other than the company that reports it.

The order of payment. Sagard collects the first $600m of Jemperli royalties before AnaptysBio's shareholders.

Audits and disputes. Because royalties are self-reported against contract language written years earlier, rate and duration are periodically contested.

St. Jude Medical asserted that its royalty on Kensey Nash's Angio-Seal device should fall from 6 to 2 percent and end earlier than Kensey Nash argued. In March 2026, Alexion took the position that it owes no further US royalties to Xencor on Ultomiris. Neither the rate on paper nor the reported number is always the settled one.

PDL BioPharma and Facet Biotech, 2008

The template was set by PDL BioPharma, formerly Protein Design Labs, which held the Queen et al. antibody-humanization patents and collected royalties from numerous licensees whose antibody drugs used the technology.

On 10 April 2008 PDL announced its intention to spin off its biotechnology operations into a separate publicly traded company, apart from the royalty assets, which would remain with PDL.

The company transferred its research operations to a new entity, Facet Biotech, and on 18 December 2008 distributed one Facet share for every five PDL shares. Facet traded on Nasdaq as FACT; the royalty company retained the PDL BioPharma name and the PDLI ticker.

PDL's board described the reasoning in terms that recur in every later case. According to chairman Brad Goodwin, the separation would let investors invest in and realise the benefits of each asset fully and independently, would better allow PDL to return the value of the royalty assets to its stockholders, and would enable Facet to create value through disciplined R&D.

The registration statement noted that the two businesses were readily separable, with the royalty business focused exclusively on the collection of royalties, the granting of licenses, and the maintenance and enforcement of the Queen et al. patents.

The royalties came from a portfolio of humanized antibodies. In 2007 PDL earned 221 million dollars on worldwide sales of eight licensed products, including Genentech's Avastin, Herceptin, Xolair, Raptiva and Lucentis, MedImmune's Synagis, Elan's Tysabri and Wyeth's Mylotarg, and it guided to 270 to 280 million dollars for 2008.

The rates were low, generally between 1 and 3 percent: Herceptin paid a flat 3 percent on product manufactured outside the United States and about 1 percent on US product, while Avastin and Lucentis paid around 1 percent and Tysabri 3 percent.

Ahead of the separation PDL also paid a 500 million dollar special cash dividend, of 4.25 dollars a share, funded from earlier asset sales. The underlying Queen et al. patents expired in December 2009, with supplementary protection certificates extending certain products in Europe into 2014, so the royalty stream was scheduled to decline within a few years of the split.

Facet was capitalised with roughly 400 million dollars and led by Faheem Hasnain; John McLaughlin became CEO of the PDL royalty company.

Facet was later the subject of a rejected hostile bid from Biogen Idec in 2009 and was acquired by Abbott in 2010. PDL, having disclosed that it was also evaluating a sale or securitisation of the royalty assets, continued as a royalty company until its patents expired, after which it moved to wind down and dissolved in 2021.

Theravance and Theravance Biopharma, 2013 to 2014

Theravance Inc. had a long-running partnership with GSK on a respiratory franchise, including Relvar and Breo, Anoro, and an interest in Trelegy.

In April 2013 it announced a plan to split into two companies, and it used the same labels AnaptysBio would adopt twelve years later, calling one entity "Royalty Management Co" and the other "Theravance Biopharma."

The separation completed in 2014, and the parent, which retained the GSK royalty interests, renamed itself Innoviva in 2016. As in the PDL case, the royalty company was the RemainCo and the research operations were the SpinCo, which traded as TBPH.

The royalty assets were GSK respiratory inhalers. On Relvar and Breo Ellipta the company receives 15 percent on the first 3 billion dollars of annual global net sales and 5 percent above that; on Anoro Ellipta the rate tiers from 6.5 to 10 percent; and it had held a 15 percent interest in Trelegy Ellipta.

Total royalty revenue was 326 million dollars in 2022, including a partial-year 72 million from Trelegy before that interest was sold, then 253 million in 2023 and 256 million in 2024, with Breo contributing about 208 million and Anoro about 48 million in 2024, and roughly 250 million in 2025. Innoviva had paid GSK 220 million dollars in milestone fees on the products' launches, which it amortises against the royalties.

The research spin-off, Theravance Biopharma, retained its own commercial economics, including a 35 percent share of US profits on the COPD inhaler Yupelri, marketed with Viatris, and a royalty on the antibiotic Vibativ.

The two companies then followed separate paths. GSK sold its 32 percent stake in Innoviva for 392 million dollars in 2021.

In 2022, Innoviva and Theravance Biopharma jointly sold the Trelegy royalty to Royalty Pharma for 1.31 billion dollars upfront plus up to 300 million in milestones, with Theravance Biopharma surrendering 85 percent of its interest for 1.1 billion and Innoviva 15 percent for 282 million.

Theravance Biopharma sold its remaining Trelegy interest to GSK for 225 million dollars in June 2025 as the first step of a strategic review, and in June 2026 agreed to be acquired by Zymeworks.

Innoviva did not remain a pure royalty vehicle. It used the GSK cash flow to build an operating business, Innoviva Specialty Therapeutics in critical care and infectious disease, and to make a series of strategic equity investments.

For 2025 it reported 411 million dollars of revenue and 271 million of net income, with its specialty unit growing US sales 47 percent to 119 million, while the GSK royalty base declined to 250 million. The company that began as a royalty RemainCo now describes itself as a diversified biopharmaceutical company.

Ligand and OmniAb, 2022

Ligand's separation is a variant of the same structure. Ligand held a portfolio of royalties (on drugs including Amgen's Kyprolis) alongside its Captisol formulation business and the OmniAb antibody-discovery platform.

In November 2021 it announced plans to split into two companies, one holding OmniAb and the other holding the royalties, Captisol, and the Pelican protein-expression platform.

The OmniAb separation was executed through a merger with a special-purpose acquisition company, and completed on 1 November 2022 as a tax-free spin-off, with OmniAb trading as OABI and Ligand retaining the LGND ticker.

CEO John Higgins said the company was left with a diversified portfolio of growing royalty revenue and a large portfolio of late-stage programmes. The stated rationale, as with the earlier cases, was dedicated operational focus, business-specific capital allocation, and clearer investment profiles for each company.

Ligand's royalties are spread across a larger number of smaller assets. Its anchor is a 1.5 to 3 percent tiered royalty on Amgen's multiple-myeloma drug Kyprolis, alongside streams on Travere's Filspari, Recordati's Qarziba, Verona's Ohtuvayre and Merck's Capvaxive, among roughly a dozen core assets, plus its Captisol formulation business.

Royalty revenue was 109 million dollars in 2024 and 161 million in 2025, and the company held about 733 million dollars of cash at the end of 2025.

The spin-off, OmniAb, kept the antibody-discovery platform, which at separation had more than 55 partners and over 250 programmes in development and earns its own milestones and royalties as those partnered antibodies advance.

The distinction worth noting is that Ligand did not reduce itself to a minimal-staff royalty shell. It retained an operating royalty-and-technology business and subsequently expanded it, completing the acquisition of the royalty aggregator XOMA Royalty in July 2026, which took its portfolio past 200 assets.

AnaptysBio and First Tracks Biotherapeutics, 2026

The most recent case, and the one that used the term "royalty management company" explicitly, is AnaptysBio.

Its principal royalty is on Jemperli (dostarlimab), the PD-1 antibody it discovered and licensed to GSK, on a tiered ladder of 8 percent on the first billion dollars of annual sales, 12 percent from one to one and a half billion, 20 percent from there to two billion, and 25 percent above the top tier. A second, smaller royalty is on imsidolimab, licensed to Vanda for up to 35 million dollars in milestones and a 10 percent royalty.

On 29 September 2025 AnaptysBio announced its intent to separate into what it labelled "Royalty Management Co" and "Biopharma Co," the same two labels Theravance had used in 2013. The separation completed on 20 April 2026.

Shareholders received one First Tracks Biotherapeutics share (Nasdaq: TRAX) for every AnaptysBio share. The pipeline went into First Tracks with roughly 180 million dollars of cash and a two-year runway, seeded partly by a 145 million dollar private placement led by EcoR1 Capital, and the royalty company retained the AnaptysBio name and the ANAB ticker.

First Tracks' lead programme, rosnilimab, had completed a Phase 2b rheumatoid-arthritis trial and was in a Phase 2 ulcerative-colitis trial, with ANB033 (a CD122 antagonist in coeliac disease and eosinophilic oesophagitis) and ANB101 (a BDCA2 modulator) in Phase 1.

The royalty entity was structured to be small. It is expected to run with fewer than ten staff operating as contractors, under 10 million dollars of annual operating expense, and an EBIT margin above 95 percent, holding roughly 140 to 145 million dollars of net cash and retaining the group's net operating loss carryforwards.

It authorised a 100 million dollar buyback and added Susannah Gray, a former chief financial officer of Royalty Pharma, to its board.

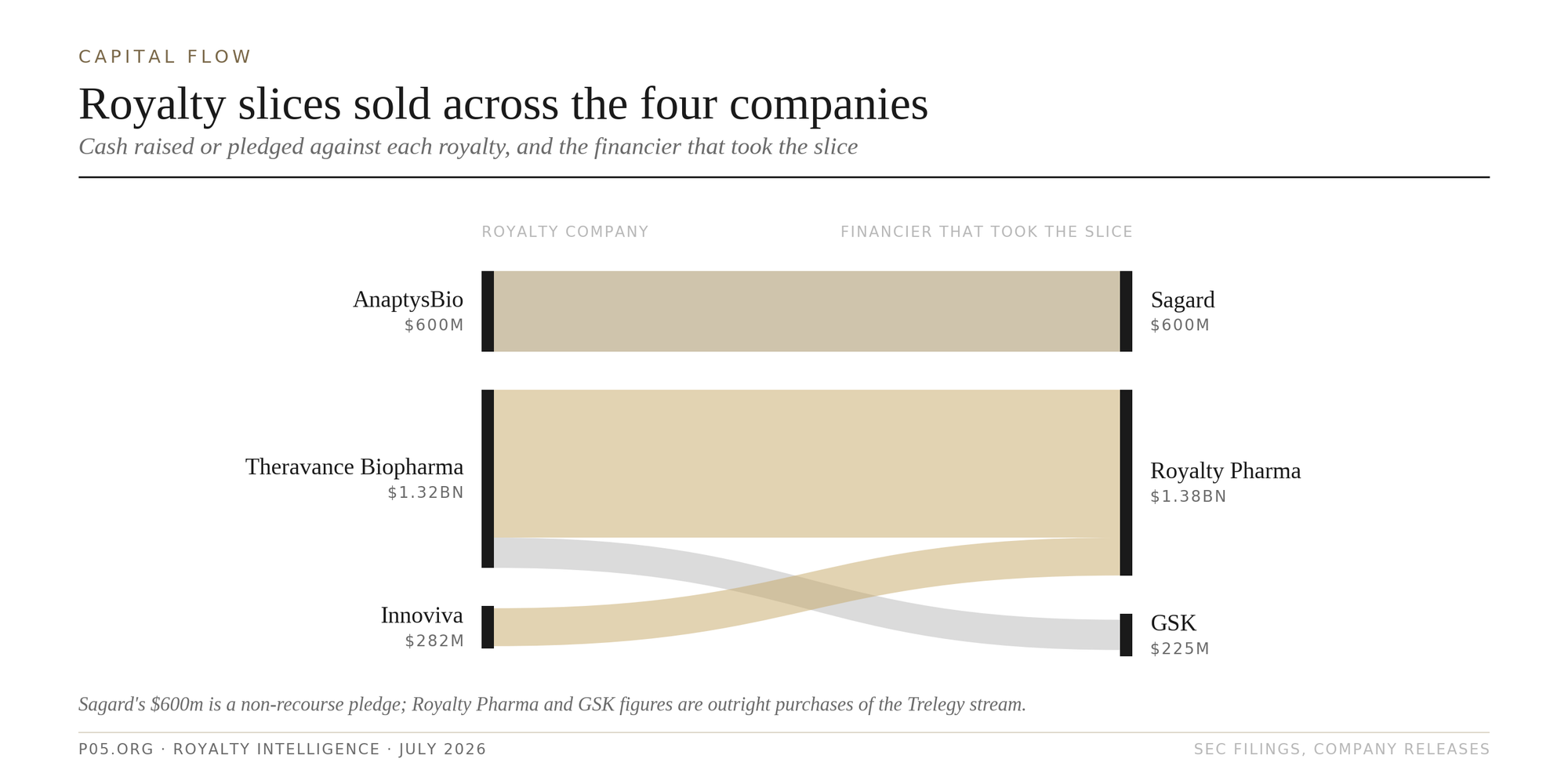

One feature of the AnaptysBio royalty is that it is partly encumbered. Before the split, the company had monetised part of the Jemperli stream through non-recourse financings with Sagard, which receives Jemperli royalties until it has collected a cumulative 600 million dollars.

Anaptys estimated that Sagard had accrued about 250 million dollars through the end of 2025 and expected the 600 million to be paid down between mid-2027 and the second quarter of 2028. Until then, the royalty company's shareholders are behind Sagard in the order of payment.

Jemperli exited the fourth quarter of 2025 at a roughly 1.4 billion dollar annual run rate, and the company projects royalties above 390 million dollars a year at GSK's peak sales guidance of more than 2.7 billion.

Royalty slices sold across the four companies, and the financier that took each slice.

The stated rationale

The reasons given for these separations have been consistent across all four, and they are documented in the companies' own filings rather than inferred.

The central argument is valuation. A royalty is a defined cash flow that can be valued on its receipts; a clinical pipeline is valued on the probability-weighted outcomes of its trials.

The companies argue that holding both inside one entity prevents investors from valuing either cleanly, and that separating them lets each attract the investors suited to its risk profile. AnaptysBio put it as letting investors align their investment philosophies and portfolio allocation with each company; PDL and Ligand used near-identical language.

A second, related point is capital allocation. The royalty company can return cash to shareholders through buybacks without the competing demand of funding R&D, while the research company can raise and spend capital on its pipeline without being judged on royalty metrics.

All four royalty entities have or had buyback programmes, and the research spin-offs were each capitalised with dedicated cash (Facet with about 400 million dollars, First Tracks with about 180 million).

Tax treatment varies and is not incidental. Ligand's OmniAb separation was structured to be tax-free. AnaptysBio disclosed that its separation was expected to be a taxable event, which it said it worked to minimise, and it structured the royalty company to retain the group's net operating losses.

The range of outcomes

The four cases have produced different results, which is the most useful thing to note about the structure, because the separation itself does not determine what follows.

PDL BioPharma ran as a royalty company for more than a decade, then wound itself down and dissolved in 2021 once the patents underlying its royalties expired. Its research spin-off, Facet, was acquired within two years of separation.

Innoviva, the Theravance royalty company, moved in the opposite direction, using its royalty cash to build an operating business and a portfolio of investments, so that it is now a diversified operating company rather than a pure royalty vehicle. Its research spin-off, Theravance Biopharma, agreed to be acquired in 2026 after a strategic review.

Ligand remained a royalty-and-technology company after spinning off OmniAb and then grew into an active royalty aggregator, most recently by acquiring XOMA Royalty. Its spin-off, OmniAb, continues as an independent antibody-discovery company.

AnaptysBio, the most recent, is at the start of its life as a royalty company, with its principal royalty still ramping and partly pledged to a prior financier. Its research spin-off, First Tracks, began independent operations in April 2026.

The common thread is the structure, not the destination. A biotech that separates its royalty from its pipeline creates a clean royalty company and a focused research company, but that royalty company can subsequently wind down, diversify into operations, or expand into an aggregator.

Which of those occurs has depended on the durability of the underlying royalty and the choices of the people running it, rather than on the separation itself.

All information in this article was accurate as of the research date and is derived from publicly available sources including SEC filings and company press releases. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.