The Weekly Term Sheet (2026-W28)

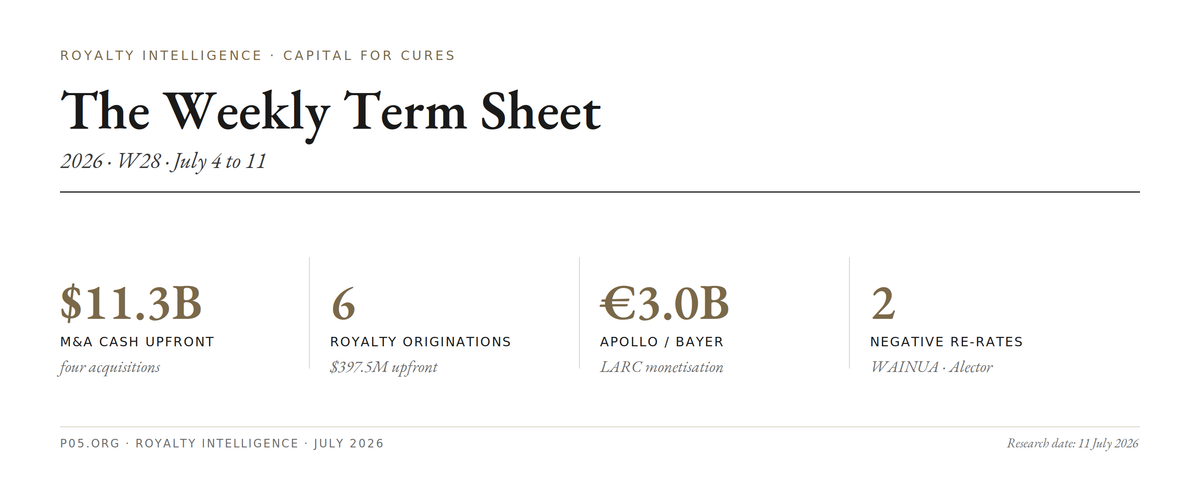

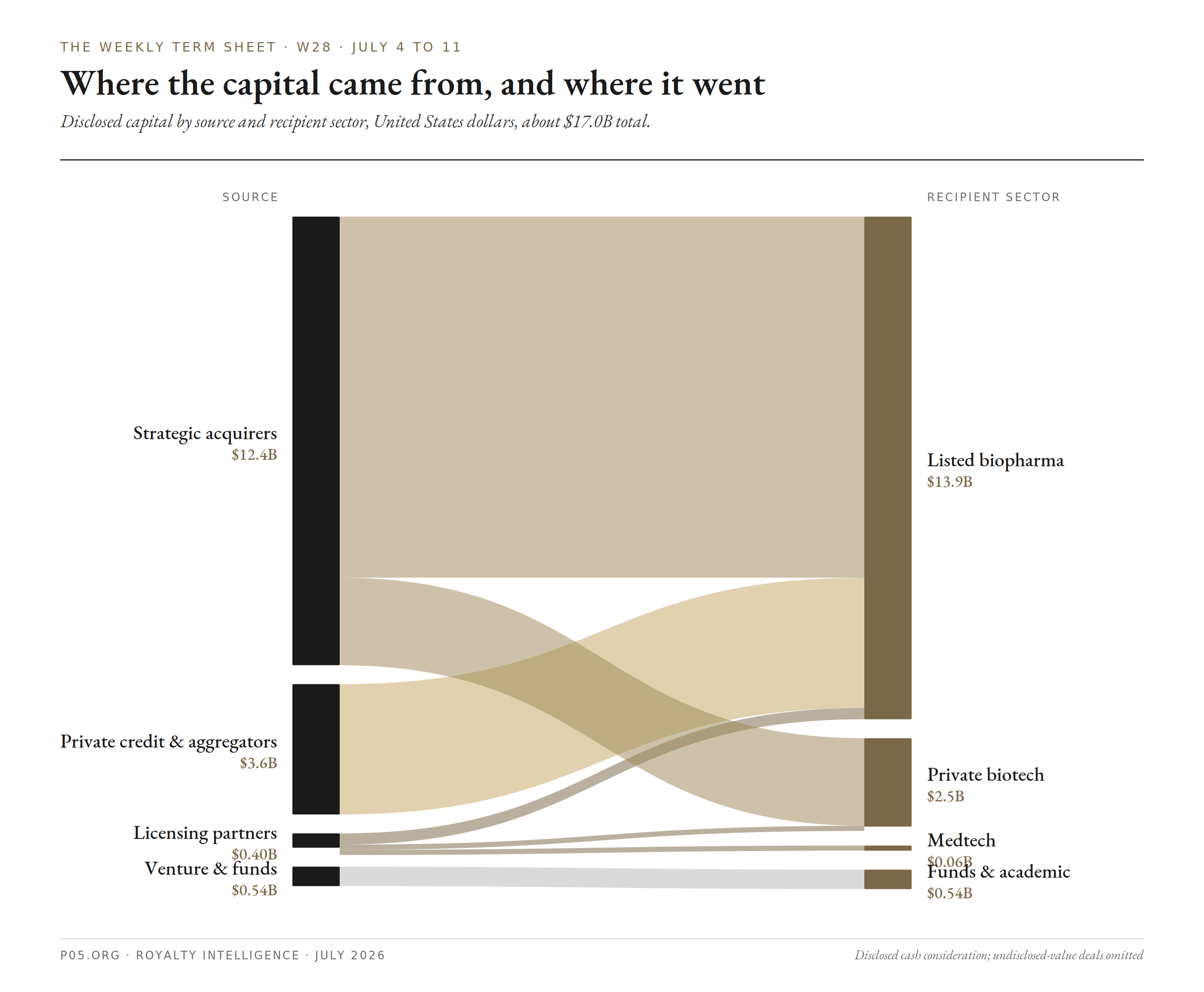

The week in numbers

July 4 to July 11, 2026: four acquisitions, six royalty-bearing originations, one synthetic royalty (Oberland / MeiraGTx), one €3.0B structured-equity monetisation (Apollo / Bayer), one structured-credit refinancing (OrbiMed / TOI), one milestone cash event (Aligos), and two negative royalty re-rates (Ionis WAINUA, GSK / Alector). No royalty monetisation or secondary stream purchase by a dedicated aggregator.

Window totals

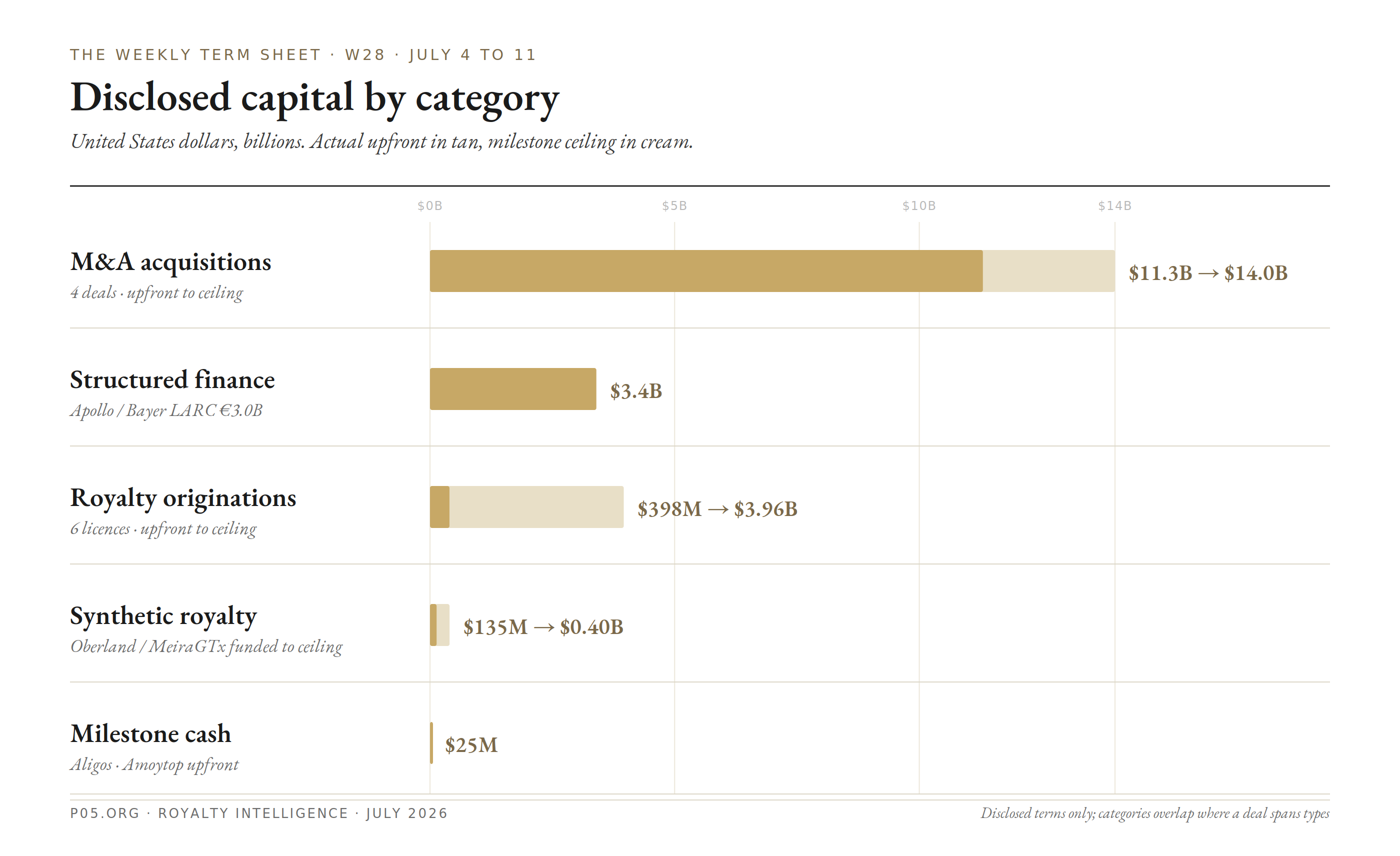

- M&A (4 acquisitions): about $11.3B upfront (up to about $14.0B with milestones); Tarsus / iRenix carries a low-to-mid single-digit revenue share to former iRenix holders; no CVR on the other three

- Royalty-bearing originations (6 streams): $397.5M combined cash upfront (up to about $3.96B with milestones); includes one medical-device origination (Alcon / RxSight); two with no cash upfront (Argent / Splash, Simcere / Schrödinger)

- Synthetic royalty (1): Oberland / MeiraGTx, $135M funded (up to $400M, of which up to $375M non-dilutive plus up to $25M equity)

- Structured finance (4 facilities): Apollo / Bayer LARC €3.0B (about $3.4B) minority-equity monetisation, Vertex $4.5B acquisition bridge, Oberland / MeiraGTx royalty note, OrbiMed $75M term loan

- Royalty re-rates (3 positive, 2 negative, plus 2 clinical): Vera TRUTAKNA (live), Genmab Tepkinly, MacroGenics Zynyz positive; Ionis WAINUA and GSK / Alector negative; clinical: Kailera / Hengrui HRS-7535 (positive), BMS Krazati KRYSTAL-10 (negative)

- Milestone cash (1): Aligos, $25M Amoytop upfront

- Equity financings (3 private rounds): FORE $67.4M (round to $110M), Cyllene €33M, Healome £2M

- New funds and capital (2 vehicles, 1 capex): Genesys up to C$40M, B Capital Ascent III $500M, Polpharma €60M

- Royalty paper transferred via M&A: one. No running product royalty travels with Vertex / Crinetics, Novartis / Myricx, or Incyte / Vega, but Tarsus / iRenix creates a new royalty leg: former iRenix holders retain a low-to-mid single-digit revenue share on future IRX-101 net sales.

- Aggregator activity: one primary origination (Oberland / MeiraGTx). No Royalty Pharma, HealthCare Royalty, Blackstone, Ligand, or DRI print, and no secondary purchase of an existing stream. Apollo's High Grade Capital Solutions platform printed the window's largest structured-finance deal, the €3.0B (about $3.4B) Bayer LARC monetisation, though as ring-fenced minority equity rather than a royalty-stream purchase.

- Public offerings: none priced by a pharma or biotech name in the window.

M&A and Restructuring

Vertex / Crinetics Pharmaceuticals: $10.0B All-Cash Endocrinology Acquisition (Mon July 6)

Vertex Pharmaceuticals (Nasdaq: VRTX) entered a definitive agreement to acquire Crinetics Pharmaceuticals (Nasdaq: CRNX) for $85.00 per share in cash, a total equity value of about $10.0B, or about $8.8B net of estimated cash acquired (Crinetics release; Crinetics 8-K; Bloomberg).

The price is a 102% premium to the $42.03 July 6 close; Crinetics shares more than doubled after hours while Vertex fell about 2%. Both boards approved unanimously. Closing is targeted for Q3 2026, subject to a Crinetics shareholder vote and regulatory clearances, and is not subject to a financing condition (Fierce Pharma).

The commercial asset is PALSONIFY (paltusotine), a once-daily oral therapy for acromegaly, FDA-approved in September 2025 and recently approved by the EMA, priced at $290,000 per year in the US and reporting first-quarter sales of $10.7M (up from $5.4M the prior quarter). The pipeline asset is atumelnant, a once-daily oral ACTH-receptor antagonist in Phase 3 for congenital adrenal hyperplasia, with additional potential in Cushing's syndrome. Vertex cites combined peak-sales potential of more than $5B, with management and sell-side notes weighting most of that toward atumelnant, the later-stage and higher-risk asset. Vertex frames endocrine as a fifth portfolio pillar alongside cystic fibrosis, hematology, pain, and renal.

No external running royalty travels: both lead assets were discovered in-house on Crinetics' platform. Vertex is funding the purchase with cash on hand plus debt, supported by a $4.5B committed bridge from Bank of America, N.A. and Morgan Stanley Senior Funding, Inc.

- Acquirer: Vertex Pharmaceuticals (Nasdaq: VRTX; Boston; Executive Chairman Jeffrey Leiden, President and CEO Reshma Kewalramani)

- Target: Crinetics Pharmaceuticals (Nasdaq: CRNX; San Diego; endocrine-disease focus)

- Structure: All-cash merger; $85.00 per share; about $10.0B equity value, about $8.8B net of estimated cash acquired; 102% premium to the $42.03 July 6 close; no CVR; no financing condition

- Financing: Cash on hand plus debt, supported by $4.5B of fully committed bridge financing from Bank of America, N.A. and Morgan Stanley Senior Funding, Inc.

- Commercial asset: PALSONIFY (paltusotine): once-daily oral therapy for acromegaly; FDA-approved September 2025, EMA-approved, under review in other markets; US list price $290,000 per year; Q1 sales $10.7M (up from $5.4M)

- Pipeline asset: Atumelnant: once-daily oral ACTH-receptor antagonist; Phase 3 in congenital adrenal hyperplasia; additional potential in Cushing's syndrome

- Peak-sales frame: More than $5B combined peak-sales potential (Vertex), weighted toward atumelnant; endocrine positioned as a fifth pillar alongside CF, hematology, pain, and renal

- Royalty: No external running royalty travels; PALSONIFY and atumelnant homegrown on the Crinetics platform

- Condition / timing: Crinetics shareholder approval, antitrust and regulatory clearances; close targeted Q3 2026

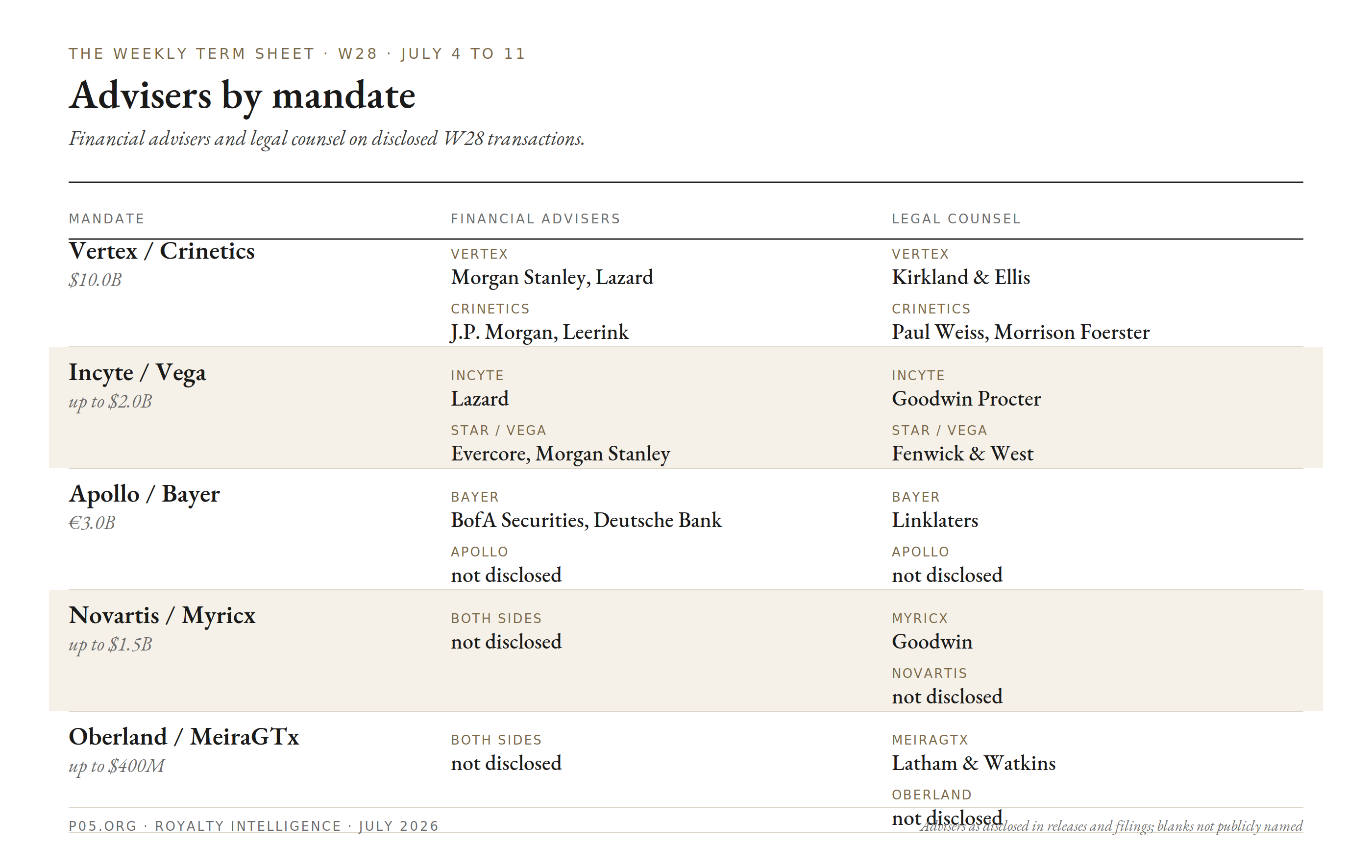

- Advisers: Vertex: Morgan Stanley & Co. LLC and Lazard (financial), Kirkland & Ellis LLP (legal). Crinetics: J.P. Morgan Securities LLC and Leerink Partners LLC (financial), Paul, Weiss, Rifkind, Wharton & Garrison LLP and Morrison Foerster LLP (legal)

- Date: Mon July 6, 2026

Novartis / Myricx Bio: Up-to-$1.5B NMTi ADC-Payload Acquisition (Mon July 6)

Novartis (SIX: NOVN; NYSE: NVS) entered an agreement to acquire privately held, UK-based Myricx Bio for USD 1.1B upfront plus up to USD 400M in milestones, up to $1.5B total (Novartis release; Myricx release; Imperial).

The transaction is expected to close in H2 2026, subject to regulatory approvals.

Myricx brings two lead ADC assets and a first-in-class N-myristoyltransferase inhibitor (NMTi) payload platform, a chemistry positioned against resistance to established payload classes such as TOPO-1 inhibitors, with potential across multiple solid tumours (lead programmes targeting B7-H3 and HER2).

Myricx was founded in 2019 as a spin-out from Imperial College London's Department of Chemistry and the Francis Crick Institute, on more than two decades of NMT research by founders Professor Ed Tate, Dr Andrew Bell, and Dr Roberto Solari, with support from Cancer Research UK. It raised a GBP 90M (about $114M) Series A in mid-2024, led by Novo Holdings and Abingworth, joined by British Business Bank, Cancer Research Horizons, Eli Lilly, Brandon Capital, and Sofinnova Partners. Cancer Research Horizons described the $1.1B upfront as the largest ever paid for a preclinical biotech.

No external running royalty travels, as Novartis acquires the whole company and the assets are preclinical. The upstream academic and charity origination economics (Imperial College London, the Francis Crick Institute, CRUK and Cancer Research Horizons) are retained by those holders under the original spin-out and licensing terms.

- Acquirer: Novartis (SIX: NOVN; NYSE: NVS; Fiona Marshall, President of Biomedical Research)

- Target: Myricx Bio (private; UK; 2019 Imperial College London and Francis Crick Institute spin-out; CEO Mohit Rawat)

- Structure: Company acquisition; USD 1.1B cash upfront plus up to USD 400M milestones (up to USD 1.5B total); no CVR disclosed

- Platform: First-in-class NMTi (N-myristoyltransferase inhibitor) ADC payload chemistry, positioned against resistance to TOPO-1 and other established payload classes

- Lead assets: Two lead ADCs (programmes targeting B7-H3 and HER2) plus the broader NMTi payload platform; preclinical

- Origination: Founded 2019 on more than 20 years of NMT research (Prof Ed Tate, Dr Andrew Bell, Dr Roberto Solari) at Imperial and the Francis Crick Institute, with CRUK support; GBP 90M (~$114M) Series A mid-2024, led by Novo Holdings and Abingworth, joined by British Business Bank, Cancer Research Horizons, Eli Lilly, Brandon Capital, and Sofinnova

- Royalty: No external running royalty travels; upstream academic and charity economics (Imperial, Francis Crick, CRUK and Cancer Research Horizons) retained by those holders

- Condition / timing: Customary closing conditions including regulatory approvals; close targeted H2 2026

- Advisers: Myricx: Goodwin (legal). Novartis advisers not disclosed in the announcement

- Date: Mon July 6, 2026

Incyte / Vega Therapeutics: $1.25B Von Willebrand Disease Acquisition Closed (Mon July 6)

Incyte (Nasdaq: INCY) completed its acquisition of Vega Therapeutics, Inc., a wholly owned subsidiary of Star Therapeutics, LLC, for $1.25B upfront plus up to $750M in sales milestones to Star, up to $2.0B total (Incyte 8-K).

The transaction was signed June 8, 2026 and closed July 6, 2026.

The asset is VGA039, an anti-Protein S monoclonal antibody with a novel mechanism across bleeding disorders, in the Phase 3 VIVID-6 study (a global single-arm cross-over trial) for von Willebrand disease.

The upfront is recognised as a one-time research and development charge. No royalty is disclosed on VGA039, so no royalty layer travels with the acquisition.

- Acquirer: Incyte (Nasdaq: INCY; Wilmington, DE; CEO Bill Meury)

- Target: Vega Therapeutics, Inc. (a wholly owned subsidiary of Star Therapeutics, LLC)

- Structure: Acquisition; $1.25B upfront cash plus up to $750M in sales milestones to Star Therapeutics (up to $2.0B total); no CVR

- Timeline: Signed June 8, 2026; closed July 6, 2026

- Asset: VGA039: anti-Protein S monoclonal antibody; Phase 3 VIVID-6 (global single-arm cross-over) in von Willebrand disease

- Accounting: Upfront recognised as a one-time R&D charge in FY2026

- Royalty: None disclosed on VGA039

- Advisers: Incyte: Lazard (financial), Goodwin Procter (legal). Star / Vega: Evercore and Morgan Stanley (financial), Fenwick & West (legal)

- Date: Closed Mon July 6, 2026

Tarsus / iRenix Medical: Up-to-$565M Ophthalmic Acquisition Carrying a Royalty Leg (Announced Wed July 8)

Tarsus Pharmaceuticals (Nasdaq: TARS) acquired privately held, clinical-stage iRenix Medical, Inc., the developer of IRX-101, an investigational ocular antiseptic, under an Agreement and Plan of Merger entered and completed on July 6, 2026 and announced on July 8 (Tarsus release; Tarsus 8-K).

The consideration is about $75M upfront, split evenly as $37.5M in cash and $37.5M in Tarsus common stock, plus up to $490M in approval and commercial milestones (up to about $565M total). The structure also carries a royalty leg: former iRenix equityholders may receive low-to-mid single-digit revenue sharing on certain future IRX-101 net sales, alongside the milestones.

IRX-101 is a stable aqueous chlorine dioxide solution designed to reduce post-procedural pain and corneal toxicity in patients receiving intravitreal therapy, a high-volume ophthalmic setting. In a Phase 2b/3 study it showed statistically significant reductions in post-procedural pain and corneal toxicity, and Tarsus, working from an FDA-aligned programme, plans to start a Phase 3 trial in early 2027.

- Acquirer: Tarsus Pharmaceuticals, Inc. (Nasdaq: TARS; Irvine, CA; therapeutic eyecare)

- Target: iRenix Medical, Inc. (private, Delaware; clinical-stage ophthalmic biopharmaceutical)

- Structure: Merger; about $75M upfront ($37.5M cash, $37.5M Tarsus stock), up to $490M in approval and commercial milestones (up to about $565M total), plus low-to-mid single-digit revenue sharing to former iRenix holders on certain future net sales

- Asset: IRX-101: investigational ocular antiseptic (stable aqueous chlorine dioxide) to reduce post-procedural pain and corneal toxicity after intravitreal therapy; Phase 2b/3 positive; Phase 3 planned early 2027

- Royalty: Low-to-mid single-digit revenue share to former iRenix equityholders on future IRX-101 net sales; a royalty leg created by the acquisition

- Timeline: Merger agreement signed and closed July 6, 2026; announced July 8, 2026

- Advisers: Not disclosed in sources reviewed; Fortis Advisors LLC acts as securityholders' representative

- Date: Announced Wed July 8, 2026

Royalty-Bearing License-Outs

Chia Tai Tianqing / AstraZeneca: Ex-China TQC3721 PDE3/4 Inhibitor Licence, Up to About $2.1B (Wed July 8)

Sino Biopharmaceutical (HKEX: 1177), through its subsidiary Chia Tai Tianqing Pharmaceutical Group Co., Ltd. (CTTQ), entered an exclusive licence agreement with AstraZeneca (LSE/STO/Nasdaq: AZN) for the development, manufacturing, and commercialisation of the group's inhaled dual PDE3/4 inhibitor TQC3721 (Sino Biopharmaceutical announcement; Fierce Biotech).

AstraZeneca receives an exclusive licence to develop, manufacture, and commercialise TQC3721 outside China, and also gains exclusive global rights for certain future development programmes. Sino Biopharmaceutical is eligible for a $200M upfront payment, up to $1.9B in development, regulatory, and sales milestones (up to about $2.1B total), plus tiered royalties up to double-digit percentages on annual net sales of TQC3721 products. The agreement is subject to customary closing conditions, including regulatory clearances.

TQC3721 is a highly differentiated inhaled PDE3/4 inhibitor discovered and developed by the group. By balancing inhibition of PDE3 (bronchodilation) and PDE4 (anti-inflammation), it is designed to deliver synergistic bronchodilatory and anti-inflammatory effects.

The nebulised formulation is in a Phase 3 trial in China for chronic obstructive pulmonary disease, having generated a potential best-in-class Phase 2b profile (Luo Z, et al, ERS 2025, Amsterdam), and a dry powder inhaler formulation is in Phase 2 in China. It has the potential to become the first domestically developed inhaled dual PDE3/4 inhibitor approved in China.

The structure repeats the window's inverse-China pattern seen in Everest and Travere, but at a much larger scale: a China-based originator out-licenses ex-China rights to a multinational, retains its home market, and keeps the royalty leg on the partnered territories.

For AstraZeneca, TQC3721 is a late-stage challenger to Merck & Co's Ohtuvayre (ensifentrine), the first-in-class inhaled PDE3/4 agent that anchored Merck's roughly $10B acquisition of Verona Pharma, which closed in October 2025. This is Sino Biopharmaceutical's second out-licensing transaction with a multinational this year, following a February 2026 licensing collaboration with Sanofi.

The same July 8 announcement carried a separate item that creates no new royalty leg for CTTQ or GSK but does carry a downstream royalty read-through: Sino Biopharmaceutical broadened its GSK alliance, with CTTQ securing exclusive mainland-China commercialisation rights to GSK's inhalers Trelegy Ellipta (fluticasone furoate, umeclidinium, and vilanterol; COPD and asthma) and Anoro Ellipta (umeclidinium and vilanterol; COPD).

CTTQ handles import, distribution, hospital access, and promotion, and recognises the product sales revenue in China, a supply-based commercialisation model rather than a royalty or profit split (Reuters via Regional Media News). No upfront, milestone, or royalty terms were disclosed.

It extends the GSK and CTTQ collaboration beyond the May 2026 bepirovirsen hepatitis B supply deal into respiratory, and is included here for completeness as a same-day China commercialisation arrangement, not a royalty origination.

The royalty relevance sits downstream: Trelegy's royalty economics were largely monetised in July 2022, when Theravance Biopharma sold about 85% of its sales-based Trelegy royalty rights to Royalty Pharma for roughly $1.11B, Royalty Pharma holding the near-term royalty and Theravance retaining 85% of the outer-year royalties (ex-US from July 1, 2029, US from January 1, 2031). Higher CTTQ-driven China volume on Trelegy, a roughly $3B global-sales brand in 2025, therefore reads through as an ex-US positive to that pre-existing Trelegy royalty stack, first to Royalty Pharma and, from mid-2029, to Theravance's retained interest, rather than to GSK or CTTQ. Anoro Ellipta (about $542M in 2025 global sales) carries no comparable third-party royalty.

- Licensor / originator: Sino Biopharmaceutical Limited (HKEX: 1177; Cayman-incorporated) via Chia Tai Tianqing Pharmaceutical Group Co., Ltd. (CTTQ); retains China rights; Chairwoman Tse, Theresa Y Y

- Licensee: AstraZeneca (LSE/STO/Nasdaq: AZN); ex-China rights to develop, manufacture, and commercialise TQC3721, plus exclusive global rights to certain future development programmes

- Structure: Exclusive licence; $200M upfront, up to $1.9B in development, regulatory, and sales milestones (up to about $2.1B total), plus tiered royalties up to double-digit percentages on annual net sales to Sino Biopharmaceutical and CTTQ; subject to customary closing conditions including regulatory clearances

- Asset: TQC3721: inhaled dual PDE3/4 inhibitor for chronic respiratory disease; nebulised formulation in Phase 3 in China for COPD, dry powder inhaler in Phase 2; potential best-in-class Phase 2b profile (ERS 2025)

- Royalty: Tiered royalties up to double-digit percentages to Sino Biopharmaceutical and CTTQ on ex-China net sales; the China-based originator retains the royalty leg on AstraZeneca's territories

- Competitive frame: Late-stage challenger to Merck & Co's Ohtuvayre (ensifentrine), which anchored Merck's about $10B Verona Pharma acquisition (closed October 2025)

- Context: Sino Biopharmaceutical's second multinational out-licence this year, after a February 2026 Sanofi collaboration

- Advisers: Not disclosed in the announcement

- Date: Wed July 8, 2026

Astex / Genentech: Fragment-Derived Breast-Cancer Discovery Licence, Up to More Than $490M (Mon July 6)

Astex Pharmaceuticals (Cambridge, UK; a wholly owned subsidiary of Japan's Otsuka Pharmaceutical) entered an exclusive, worldwide research collaboration and licence agreement with Genentech, a member of the Roche Group, on a small molecule discovery programme against a cell-cycle-dependent regulator in breast cancer (Astex release; pharmaphorum).

Astex receives $25M upfront and is eligible for further preclinical, clinical, regulatory, and sales milestones totalling more than $490M (about $515M headline), plus tiered royalties on net sales.

Astex grants Genentech an exclusive licence to compounds from its existing breast-cancer programme and collaborates on lead optimisation. Genentech is solely responsible for preclinical and clinical development and worldwide commercialisation.

Astex's Pyramid fragment-based platform has produced three approved oncology drugs through prior partnerships: ribociclib (Kisqali, Novartis), erdafitinib (Balversa, Janssen), and capivasertib (Truqap, AstraZeneca).

The programme licensed to Genentech originated under Astex's strategic alliance agreement with Newcastle University and Cancer Research Horizons, so an upstream academic royalty and milestone entitlement sits beneath Astex's tiered royalty from Genentech. The specific target was described only as a cell-cycle-dependent regulator, not named.

Genentech separately disclosed about 103 role reductions the same day.

- Licensor: Astex Pharmaceuticals (Cambridge, UK; wholly owned subsidiary of Otsuka Pharmaceutical; President Michelle Jones)

- Licensee: Genentech, a member of the Roche Group (Head of Roche Corporate Business Development Boris L. Zaitra)

- Structure: Exclusive worldwide research collaboration and licence; $25M upfront, up to more than $490M in preclinical, clinical, regulatory, and sales milestones (about $515M headline), plus tiered royalties on net sales to Astex

- Asset: Fragment-derived small molecule against an unnamed cell-cycle-dependent regulator in breast cancer; discovery-stage, from Astex's Pyramid FBDD platform

- Responsibilities: Genentech leads all preclinical and clinical development and worldwide commercialisation; Astex collaborates on lead optimisation

- Royalty (two layers): Tiered royalties to Astex from Genentech; upstream royalty and milestone entitlement to Newcastle University and Cancer Research Horizons under Astex's strategic alliance

- Platform track record: Astex Pyramid FBDD has produced three approved oncology drugs via prior partners: ribociclib (Kisqali, Novartis), erdafitinib (Balversa, Janssen), capivasertib (Truqap, AstraZeneca)

- Advisers: Not disclosed

- Date: Mon July 6, 2026

Everest Medicines / Travere Therapeutics: $112.5M Civorebrutinib Ex-China Licence Closed (Tue July 7)

Everest Medicines (HKEX: 1952) closed its previously announced exclusive licensing and collaboration agreement with Travere Therapeutics (Nasdaq: TVTX) for civorebrutinib (also known as EVER001), an oral covalent reversible Bruton's tyrosine kinase (BTK) inhibitor in development for renal disease (Everest release).

The licence covers the US and global markets excluding Greater China and certain countries in East and Southeast Asia, which Everest retains.

Everest receives a $112.5M upfront on closing and is eligible for up to about $1.03B in clinical development, regulatory, and commercial milestones across up to five indications. Travere pays tiered royalties on net sales in its licensed territories, ranging from high single-digit to double-digit percentages based on annual net sales thresholds.

The structure is the inverse of the week's other China-linked out-licence: a China-based originator licenses ex-Greater China rights to a US partner and retains both its home-market rights and the royalty leg on the partnered territories.

- Licensor / originator: Everest Medicines (HKEX: 1952; Shanghai; retains Greater China and certain East and Southeast Asian markets)

- Licensee: Travere Therapeutics (Nasdaq: TVTX; US and global markets excluding Greater China and certain East and Southeast Asian countries)

- Structure: Exclusive licensing and collaboration; $112.5M upfront on closing, up to about $1.03B in clinical, regulatory, and commercial milestones across up to five indications, plus tiered royalties to Everest

- Asset: Civorebrutinib (EVER001): oral covalent reversible BTK inhibitor for renal disease

- Royalty: Tiered royalties to Everest on Travere territory net sales, high single-digit to double-digit percentages by annual net sales threshold

- Timeline: Previously announced; closed July 7, 2026

- Advisers: Not disclosed

- Date: Tue July 7, 2026

Argent BioPharma / Splash Beverage Group: Worldwide CannEpil Licence, 15% Net-Revenue Royalty (Mon July 6)

Argent BioPharma (ASX: RGT) entered a binding global licensing agreement giving Splash Beverage Group (NYSE American: SBEV) exclusive worldwide rights to CannEpil, a proprietary compounded cannabinoid formulation (CBD and THC isolates) for drug-resistant and refractory epilepsy, seizure disorders, and related neurological conditions (Splash 8-K exhibit; GlobeNewswire).

CannEpil is already available in several markets including Ireland, the United Kingdom, Germany, and Australia, and is manufactured to EU-GMP standards. The licence covers all global territories, future product improvements, and next-generation developments, and carries sublicensing rights on an initial twenty-year term.

The consideration carries no cash upfront. It is structured as a tri-party cancellation and exchange agreement dated July 6, 2026 among Argent, Mercer Street Global Opportunity Fund, and Splash: Mercer Street, Argent's secured convertible-note holder, forgives US$5.5M of Argent-issued convertible notes, and in exchange Splash issues Mercer Street US$5.5M of stated-value Series D convertible preferred (5,500 shares).

This extinguishes Argent's Mercer secured note and its associated security interests. Separately, C/M Capital Partners committed a $1M strategic investment to Splash.

Splash's press release described the debt forgiven as approximately $5M; Argent's release and the exchange agreement state US$5.5M. The licence remains subject to conditions precedent, including completion of the Mercer debt exchange.

The exchange removes Argent's principal secured liability; its later convertible facilities with C/M Capital Master Fund and WVP Emerging Manager Onshore Fund remain in place.

Argent receives a 15% royalty on Splash's worldwide net revenue from CannEpil, running until the longer of ten years after first commercial sale in each country or patent expiry there, retains ownership of existing and future CannEpil IP, and will manufacture the product for Splash. Splash committed to commercially reasonable efforts toward a Phase 1 trial within 24 months, a Phase 2 within 48 months, and an NDA thereafter, and bears development and regulatory responsibility from here.

The structure transfers commercialisation and development risk to Splash while Argent retains the IP, the manufacturing role, and a flat double-digit royalty. The upfront is balance-sheet consideration, the removal of a secured convertible note, rather than cash proceeds.

- Licensor / originator: Argent BioPharma Limited (ASX/LSE: RGT; retains CannEpil IP; manufactures under EU-GMP)

- Licensee: Splash Beverage Group, Inc. (NYSE American: SBEV; exclusive worldwide commercialisation, initial twenty-year term, sublicensing rights)

- Asset: CannEpil: compounded cannabinoid formulation (CBD and THC isolates) for drug-resistant and refractory epilepsy; marketed in Ireland, the UK, Germany, and Australia; US development-stage

- Structure: No cash upfront. Tri-party cancellation and exchange (Argent, Mercer Street, Splash), dated July 6, 2026: Mercer Street forgives US$5.5M of Argent convertible notes in exchange for US$5.5M stated-value Splash Series D convertible preferred (5,500 shares), extinguishing Argent's Mercer secured note; C/M Capital Partners separately commits $1M to Splash. Splash's release states approximately $5M forgiven; Argent and the exchange agreement state US$5.5M

- Royalty: 15% of Splash worldwide net revenue to Argent, until the longer of ten years after first commercial sale per country or patent expiry

- Conditions: Licence subject to conditions precedent, including completion of the Mercer debt exchange. Removes Argent's principal secured liability; its C/M Capital Master Fund and WVP Emerging Manager Onshore Fund convertible facilities remain in place

- Development commitments: Splash to use commercially reasonable efforts: Phase 1 within 24 months, Phase 2 within 48 months, NDA after successful trials

- Advisers: Not disclosed

- Date: Mon July 6, 2026

Simcere / Schrödinger: Global Discovery and Development Collaboration, Milestones Plus Tiered Royalties (Fri July 10)

Simcere Pharmaceutical Group (HKEX: 2096) and Schrödinger (Nasdaq: SDGR) entered a global drug discovery and development collaboration under which Schrödinger leads computational drug design and optimisation for the joint research programmes, and Simcere leads subsequent preclinical and clinical development after the discovery phase (Simcere release).

Schrödinger is eligible to receive discovery, development, and commercial milestones across all programmes in the collaboration, plus tiered royalties on net sales. No upfront figure, milestone ceiling, target, or therapeutic area was disclosed. Zhou Gaobo, Simcere Chief Investment Officer, and Karen Akinsanya, Schrödinger President and Head of Therapeutics R&D, were quoted on the agreement.

This is a computational-platform origination in which the software and design partner (Schrödinger) retains the royalty leg while the development partner (Simcere) takes programmes into the clinic. Schrödinger's other disclosed collaborations of this type, with Novartis, Eli Lilly, Otsuka, and Structure Therapeutics, run milestones plus low-single-digit to low-double-digit royalties, but the Simcere terms are not public, so no economics are inferred here.

- Discovery / royalty holder: Schrödinger, Inc. (Nasdaq: SDGR; New York; leads computational drug design and optimisation; President and Head of Therapeutics R&D Karen Akinsanya)

- Development partner / originator: Simcere Pharmaceutical Group (HKEX: 2096; Nanjing; leads preclinical and clinical development; Chief Investment Officer Zhou Gaobo)

- Structure: Global drug discovery and development collaboration; discovery, development, and commercial milestones plus tiered royalties on net sales to Schrödinger; upfront, milestone ceiling, targets, and therapeutic area not disclosed

- Royalty: Tiered royalties to Schrödinger on net sales of products emerging from the collaboration; tiers not disclosed

- Advisers: Not disclosed

- Date: Fri July 10, 2026

Alcon / RxSight: Adjustable-Intraocular-Lens Royalty License, Up to $200M Plus Royalties (Mon July 6)

Alcon (SIX/NYSE: ALC) and RxSight, Inc. (Nasdaq: RXST) entered a non-exclusive license and co-development collaboration to jointly develop adjustable presbyopia-correcting intraocular lenses (PCIOLs), combining RxSight's post-operative light-adjustable technology with Alcon's PCIOL optical designs (RxSight 8-K exhibit 99.1; Alcon release).

Under the agreement, dated June 30, 2026 and announced July 6, RxSight receives a $60M upfront payment and is eligible for up to $140M in development and regulatory milestones (up to $200M total), plus royalties on net sales of the co-developed, globally commercialised PCIOL products. Alcon leads global commercialisation, leveraging its established eye-care footprint, while RxSight is responsible for development, manufacturing, and US device support.

The companies' release does not state the royalty tier; trade coverage reported a 30% royalty to RxSight (TipRanks), which is not confirmed in the primary release and is flagged as such here.

The royalty leg sits with RxSight, the developer and manufacturer, on a co-developed medical-device platform, an origination in the medtech corner of this publication's scope rather than a small-molecule or biologic out-licence. RxSight's light-adjustable lens allows surgeons to fine-tune a patient's refractive outcome after cataract surgery using post-operative light treatments, and the collaboration is designed to bring that adjustability to Alcon's PCIOL optics. RxSight released preliminary second-quarter results the same day, under which it began recognising revenue from the Alcon collaboration.

- Licensor / royalty holder: RxSight, Inc. (Nasdaq: RXST; Aliso Viejo, CA; ophthalmic medical device company; President and CEO Ron Kurtz); retains development, manufacturing, US device support, and the royalty leg

- Licensee: Alcon (SIX/NYSE: ALC; CEO David J. Endicott); leads global commercialisation

- Structure: Non-exclusive license and co-development collaboration, dated June 30, 2026; $60M upfront to RxSight, up to $140M in development and regulatory milestones (up to $200M total), plus royalties on net sales

- Asset: Co-developed adjustable presbyopia-correcting intraocular lenses (PCIOLs), combining RxSight's post-operative light-adjustable technology with Alcon's PCIOL optics; development-stage

- Royalty: Royalties on net sales of the globally commercialised co-developed PCIOLs to RxSight; tier not stated in the release, reported at 30% by trade coverage (TipRanks), unconfirmed

- Advisers: Not disclosed in the announcement

- Date: Mon July 6, 2026

Royalty Re-Rates and Milestone Cash

Aligos / Amoytop: Pevifoscorvir $25M China Upfront Booked, China BTD Granted (Mon July 6)

Aligos Therapeutics (Nasdaq: ALGS) announced it had received the $25M upfront under its April 16, 2026 exclusive Greater China licence of pevifoscorvir sodium (an oral capsid assembly modulator for chronic hepatitis B) to Xiamen Amoytop Biotech, and that the asset had been granted Breakthrough Therapy Designation by China's NMPA Center for Drug Evaluation (Aligos release).

Under the licence, Aligos is eligible for up to $420M in clinical, regulatory, and sales milestones plus tiered high-single-digit royalties on Amoytop's territory net sales, and retains all rights in the US, Europe, South Korea, Japan, and other markets. Both the cash receipt and the China BTD were announced July 6. Shares rose about 16% to 21% after hours; the non-dilutive cash extends Aligos's runway into Q4 2026.

- Royalty holder / originator: Aligos Therapeutics (Nasdaq: ALGS; retains US, EU, South Korea, Japan, and other rights)

- Counterparty: Xiamen Amoytop Biotech (Greater China licensee: mainland China, Taiwan, Hong Kong, Macau)

- Asset: Pevifoscorvir sodium: oral capsid assembly modulator for chronic hepatitis B; Phase 2b SUPREME ongoing (second interim expected H2 2026, topline 2027)

- Event: Receipt of the $25M upfront under the April 16, 2026 licence, plus China NMPA Breakthrough Therapy Designation (July 6)

- Royalty: Tiered high-single-digit royalties to Aligos on Amoytop territory net sales; up to $420M in milestones

- Treatment: A cash and regulatory event on a live out-licence; not a new stream

- Date: Mon July 6, 2026

Vera Therapeutics / TRUTAKNA: FDA Accelerated Approval Brings a Licensed Royalty to Life (Tue July 7)

The FDA granted accelerated approval to TRUTAKNA (atacicept-vymj), a once-weekly subcutaneous BAFF and APRIL dual inhibitor, to reduce proteinuria in adults with primary IgA nephropathy at risk of disease progression (Vera release).

Approval rested on a prespecified interim analysis of the ongoing Phase 3 ORIGIN 3 trial (first 203 participants), in which TRUTAKNA achieved a 46% reduction from baseline in proteinuria and a statistically significant 42% reduction versus placebo (p<0.0001) at 36 weeks. The label is under the accelerated pathway on a proteinuria surrogate; a confirmatory eGFR analysis is planned for Q3 2026, with a potential sBLA in Q4 2026 to convert to full approval.

The royalty read-through runs through Vera's licence, not a monetisation. Vera licensed atacicept from Merck KGaA, Darmstadt, Germany (via Ares Trading S.A.) under the Ares Agreement dated October 29, 2020, and holds global development and commercialisation rights, so Vera is the royalty payor. Per Vera's SEC filings, Vera paid $25M on the technology transfer and a $15M milestone on BLA acceptance in January 2026; the July 7 approval triggers a $20M US regulatory-approval milestone to Ares, within up to $141.5M of further filing and approval milestones for other regions and indications and up to $515M of net-sales milestones.

Vera then owes tiered royalties of low-double-digit to mid-teen percentages on annual net sales, and mid-single-digit to low-double-digit on sublicensing income (Vera 10-K FY2025). Atacicept originated as a TACI-Ig fusion protein at ZymoGenetics, which was acquired by Bristol-Myers Squibb in 2010; a live upstream royalty is not established from Vera's current filings.

- Event: FDA accelerated approval of TRUTAKNA (atacicept-vymj) in primary IgA nephropathy, on an ORIGIN 3 prespecified interim analysis

- Royalty payor: Vera Therapeutics (Nasdaq: VERA; Brisbane, CA; holds global rights; Founder and CEO Marshall Fordyce)

- Royalty payee / licensor: Merck KGaA, Darmstadt, Germany, via Ares Trading S.A. (Ares Agreement, October 29, 2020)

- Milestone triggered: $20M US approval milestone to Ares on this approval; $15M BLA-acceptance milestone paid January 2026; $25M paid on technology transfer (2020); within up to $141.5M of further filing/approval milestones and up to $515M of net-sales milestones

- Royalty: Tiered royalties to Ares (Merck KGaA) on Vera net sales, low-double-digit to mid-teen percentages; mid-single-digit to low-double-digit on sublicensing income (Vera SEC filings)

- Upstream: Atacicept created as a TACI-Ig fusion protein at ZymoGenetics, acquired by Bristol-Myers Squibb in 2010; a live upstream royalty is not established from Vera's current filings

- Next catalyst: ORIGIN 3 eGFR analysis targeted Q3 2026; potential sBLA Q4 2026 for full approval

- Treatment: A licensed royalty going live on approval; not a new origination or a monetisation

- Date: Tue July 7, 2026

Synthetic Royalty and Structured Finance

Oberland Capital / MeiraGTx: Up-to-$400M Multi-Product Synthetic Royalty (Tue July 7)

Oberland Capital Management agreed to invest up to $400M in MeiraGTx Holdings (Nasdaq: MGTX), comprising up to $375M in non-dilutive capital for capped royalty payments plus up to $25M in equity (MeiraGTx release).

The structure is a staged, multi-product synthetic royalty. The initial $135M funded at signing is $125M in exchange for low single-digit royalties on the included products plus a $10M equity investment.

Four further layers are available at MeiraGTx's option or by mutual agreement: $50M on AAV2-hAQP1 Phase 2 AQUAx2 data in 2027, $50M on bota-vec regulatory approval in 2027, $50M on AAV2-hAQP1 regulatory approval in 2028, and a further $100M for new products or business development. Oberland also holds the right to purchase an additional $15M in equity.

Following approval, Oberland receives low single-digit capped royalties on the net sales of three gene-therapy products: AAV2-hAQP1 (grade 2/3 late radiation-induced xerostomia), botaretigene sparoparvovec (bota-vec, X-linked retinitis pigmentosa), and AAV-AIPL1 (LCA4). Royalty payments are capped at a multiple of the amounts funded, and MeiraGTx can buy back the entire funded royalty note at any time by paying certain specified amounts, with flexible provisions for a potential change of control.

This is the window's one primary-market royalty origination by a dedicated aggregator, and the first synthetic royalty of the compilation. The structure is capped, buyback-enabled, and milestone-staged across multiple pre-approval products.

- Funder: Oberland Capital Management LLC (healthcare structured-finance firm; AUM in excess of $3.5B)

- Recipient / originator: MeiraGTx Holdings plc (Nasdaq: MGTX; London and New York; CEO Alexandria Forbes)

- Structure: Up to $400M: up to $375M non-dilutive for capped royalties, plus up to $25M equity. Initial $135M funded ($125M royalties, $10M equity). Optional tranches: $50M on AQUAx2 data (2027), $50M on bota-vec approval (2027), $50M on AAV2-hAQP1 approval (2028); further $100M by mutual agreement; $15M additional equity option

- Royalty: Low single-digit capped royalties to Oberland on net sales of AAV2-hAQP1 (radiation-induced xerostomia), bota-vec (XLRP), and AAV-AIPL1 (LCA4) after approval; capped at a multiple of amounts funded

- Flexibility: MeiraGTx buyback right on the funded royalty note at any time; provisions for potential change of control

- Disclosure: Terms detailed in a Form 8-K filed the same day

- Advisers: Latham & Watkins LLP served as legal counsel to MeiraGTx (team led by Keith Halverstam, with Jennifer Yoon, Jing Cao, and Will Sedgwick). Oberland Capital counsel not disclosed

- Date: Tue July 7, 2026

OrbiMed / The Oncology Institute: $75M Term-Loan Refinancing of an $86M Convertible Note (Tue July 7)

The Oncology Institute (Nasdaq: TOI), a value-based community oncology group, completed a strategic refinancing with OrbiMed, repaying the outstanding balance of its $86M senior secured convertible note held by Deerfield Partners (TOI release).

TOI repaid the Deerfield note with a new $75M OrbiMed term loan maturing in 2031, together with about $11M of cash from its balance sheet, without raising additional equity. Management framed the transaction as increasing liquidity, improving operating flexibility, and extending debt maturities, with committed funding from two healthcare financing institutions and no dilution to existing shareholders. Matthew Rizzo of OrbiMed was cited on the firm's support for TOI's next phase of growth.

This is structured credit rather than a royalty. It is included because OrbiMed is a dedicated healthcare structured-finance house that also originates royalties and synthetic royalty structures, and because the facility is a term-loan refinancing that replaces a convertible instrument with straight, longer-dated debt against a services provider rather than a product asset. No royalty leg, no product economics, and no stream travels.

- Lender: OrbiMed (healthcare investment and structured-finance firm; Matthew Rizzo)

- Borrower: The Oncology Institute, Inc. (Nasdaq: TOI; Cerritos, CA; value-based community oncology; CEO Daniel Virnich)

- Structure: New $75M OrbiMed term loan maturing 2031, plus about $11M of balance-sheet cash, repaying an $86M senior secured convertible note held by Deerfield Partners; no new equity issued

- Purpose: Increases liquidity, extends debt maturities, and improves operating flexibility; committed non-dilutive funding

- Royalty: None; corporate structured credit against a services provider, no product royalty leg

- Treatment: A refinancing by an aggregator that also originates royalties; not a royalty origination or monetisation

- Date: Tue July 7, 2026

Apollo / Bayer: €3.0B Structured-Equity Monetisation of the LARC Contraceptives Franchise (Fri July 10)

Bayer (ETR: BAYN) secured €3.0B (about $3.4B) in equity capital, signing an agreement with Apollo Global Management (NYSE: APO) on Friday July 10 under which Apollo-managed funds and affiliates take a minority, non-controlling stake in a newly established entity holding Bayer's long-acting reversible contraceptives (LARC) business (Apollo release; Bayer EQS release).

Bayer retains a majority stake and complete operational control, the LARC activities remain part of the Bayer Pharmaceuticals Division core business, and the entity stays fully consolidated in Bayer Group's financial statements.

The LARC portfolio comprises the hormonal intrauterine systems Mirena, Kyleena, and Jaydess/Skyla plus the subdermal implant Jadelle. The franchise generated about €1.37B (about $1.55B) in 2025 sales, up roughly 8% to 12% year on year, Bayer's fourth-largest product category and the dominant position in the category worldwide. First-quarter 2026 LARC sales were €316M, down about 10%.

Rather than sell a royalty stream or issue synthetic royalties on the LARC products, Bayer ring-fenced the franchise into a separate entity and sold a minority, non-controlling equity stake to Apollo while keeping consolidation and control. The structure carries no royalty, milestone, or contingent-value leg; the sole disclosed financial term is the €3.0B upfront equity infusion. The investment is structured through Apollo's High Grade Capital Solutions platform (Partner Jamshid Ehsani).

Bayer framed the deal as a strategic financing solution to strengthen its capital structure and financial flexibility as it manages increased liquidity requirements this year tied to bond maturities and Roundup glyphosate litigation, per CFO Judith Hartmann. The transaction is expected to close in Q3 2026, subject to antitrust approval and customary closing conditions.

- Investor: Apollo Global Management (NYSE: APO) via Apollo-managed funds and affiliates; High Grade Capital Solutions platform; Partner Jamshid Ehsani

- Recipient / originator: Bayer AG (ETR: BAYN; Leverkusen; CFO Judith Hartmann); retains majority stake and complete operational control

- Structure: Minority, non-controlling equity stake in a newly ring-fenced entity holding Bayer's LARC business; €3.0B (about $3.4B) equity; entity fully consolidated in Bayer Group accounts

- Franchise: Long-acting reversible contraceptives: Mirena, Kyleena, Jaydess/Skyla (hormonal intrauterine systems), Jadelle (subdermal implant); about €1.37B in 2025 sales; Bayer's fourth-largest product category

- Royalty: None; no royalty, milestone, or contingent-value leg; sole disclosed term is the €3.0B equity infusion

- Purpose: Strengthen capital structure and financial flexibility amid bond maturities and Roundup litigation

- Treatment: A structured minority-equity monetisation of marketed-product economics; not a royalty sale or synthetic royalty

- Advisers: Bayer: BofA Securities and Deutsche Bank (financial), Linklaters LLP (legal). Apollo advisers not disclosed

- Timing: Signed Fri July 10, 2026; close expected Q3 2026 subject to antitrust approval

- Date: Fri July 10, 2026

Funds and Capital

Genesys University Seed Fund: TTO Licensing Revenue Recycled Into Venture Capital, Up to C$40M (Wed July 8)

The University of Toronto and McMaster University anchored the Genesys University Seed Fund, a life sciences seed vehicle managed by Toronto venture firm Genesys Capital, marking the first time either university has backed a venture capital fund (University of Toronto). T

he fund targets up to C$40M and has held a first close representing more than C$30M of commitments. It provides early-stage capital to life sciences startups, mainly spinouts from the two schools.

U of T is committing up to C$8M (about 20% of the fund) and McMaster C$5M, with the Temerty Group, Venture Ontario, and RBC among additional backers. The structure is what makes it relevant here rather than the size. Both universities are financing their stakes out of the licensing revenue their technology transfer offices collect on campus patents, and, as limited partners, they will direct fund returns back into further research, a licensing-income-to-venture recycling loop. This is not a royalty transaction and no stream is bought or sold, but it is a direct read on how TTOs are converting patent income into venture exposure over their own spinouts.

Genesys will charge a 2% management fee and 20% carried interest, standard venture economics, and will co-invest on some fund deals from its roughly C$150M core fund. The manager's track record includes two Genesys-launched companies that sold for ten-figure sums, Inversago Pharma (acquired by Novo Nordisk in 2023) and Fusion Pharmaceuticals (acquired by AstraZeneca in 2024 for US$2B, one of the largest university-linked exits in Canadian history and the route by which McMaster, where Fusion was based, entered the fund).

The launch sits against a structural gap this publication tracks: Canadian research universities each typically generate about C$10M or less in annual licensing revenue, a fraction of US peers such as MIT (US$60.9M in 2025), Stanford (US$87M), and Harvard (US$95.5M five-year average). University-anchored seed funds that recycle licensing income are one mechanism for narrowing that gap, and they enlarge the upstream pool of academic assets that later generate the royalty streams this publication follows.

- Fund: Genesys University Seed Fund; early-stage life sciences seed vehicle; mainly U of T and McMaster spinouts

- Manager: Genesys Capital (Toronto; co-founder and managing director Kelly Holman); about C$150M core fund co-invests on some deals

- Size: Up to C$40M target; first close above C$30M

- Anchors and LPs: University of Toronto (up to C$8M, about 20%), McMaster University (C$5M), Temerty Group, Venture Ontario, RBC

- Economics: 2% management fee, 20% carried interest

- Manager track record: Inversago Pharma (Novo Nordisk, 2023) and Fusion Pharmaceuticals (AstraZeneca, 2024, US$2B)

- Date: Wed July 8, 2026

B Capital Ascent Fund III: $500M Early-Stage AI Close, Healthcare One of Four Verticals (Mon July 6)

B Capital, the US and Singapore multi-stage firm co-founded by Eduardo Saverin and Raj Ganguly, held the oversubscribed final close of B Capital Ascent Fund III at its $500M hard cap, roughly double the $254M Ascent Fund II from July 2022 (Business Wire). The Cayman-domiciled fund writes seed, Series A, and Series B cheques into AI-driven companies across healthcare, enterprise, energy, and frontier technology in North America and Asia, and has already backed more than 20 companies including Apptronik, Havoc AI, and Star Catcher. The firm manages more than $12B.

It is included as a capital-formation signal, not a royalty item. Ascent Fund III is a diversified early-stage AI vehicle rather than a life sciences fund, healthcare is one of four verticals, and it creates no royalty leg. The vehicle more relevant to this publication is B Capital's separate Healthcare Fund II, in market with a $250M target, alongside its Global Growth Fund IV ($1.25B target), MESA Fund I (Middle East and South Asia), and Climate Fund I.

- Fund: B Capital Ascent Fund III, L.P.; early-stage AI vehicle; seed, Series A, Series B; Cayman-domiciled

- Manager: B Capital (US and Singapore; co-founders Eduardo Saverin and Raj Ganguly, co-CEOs; chair and GP Howard Morgan); more than $12B AUM

- Size: $500M hard cap, oversubscribed final close; about double the $254M Ascent Fund II (July 2022)

- Focus: Healthcare, enterprise, energy, and frontier technology across North America and Asia; healthcare one of four verticals

- Date: Mon July 6, 2026

Polpharma Group: €60M Kazakhstan Generics Manufacturing Expansion (Wed July 8)

Polpharma Group, the Polish generics and pharmaceutical group, announced a new €60M project to expand production capacity in Shymkent, Kazakhstan, introduce advanced technologies, and further localise manufacturing to international GMP standards, through its Polpharma Santo subsidiary (Qazinform). The commitment was disclosed at the 38th Plenary Session of Kazakhstan's Foreign Investors' Council, where President Kassym-Jomart Tokayev awarded Polpharma supervisory board chairman Jerzy Starak the Order of Dostyk II Degree.

It is a manufacturing localisation capital deployment, not a royalty, licence, or M&A transaction, and it creates no stream. It is included as an emerging-market capital-formation signal: Polpharma Santo, whose Kazakh operations trace to 1882 and which joined Polpharma Group in 2011, has now invested more than $130M in local facilities, produces roughly every fifth medicine package used in Kazakhstan, and in 2025 became the first Central Asian pharmaceutical company to hold an EU GMP certificate. Kazakhstan's pharmaceutical manufacturing investment more than tripled from $46.9M in 2023 to $142.8M in 2025, so the project reads as part of a broader Central Asian localisation and pharmaceutical-security push rather than a financing event this publication would score.

- Investor: Polpharma Group (Poland) via Polpharma Santo (Kazakhstan; part of Polpharma Group since 2011)

- Structure: New €60M capital investment to expand Shymkent production capacity and localise manufacturing to GMP standards; disclosed at Kazakhstan's Foreign Investors' Council

- Context: Polpharma Santo has invested more than $130M locally since 2011, holds a 2025 EU GMP certificate (first in Central Asia); Kazakh pharma manufacturing investment tripled to $142.8M in 2025

- Date: Wed July 8, 2026

Regulatory Read-Through

The window's most consequential approval for royalty purposes, the FDA's accelerated approval of Vera Therapeutics' TRUTAKNA (atacicept-vymj) in IgA nephropathy on July 7, is treated above under Royalty Re-Rates and Milestone Cash, since it triggers a milestone to licensor Merck KGaA and starts a live royalty rather than only re-rating an existing one.

The MHRA approved Zynyz (retifanlimab) as the first UK treatment for adults with advanced Merkel cell carcinoma, granted to Incyte Biosciences UK Ltd via the International Recognition Procedure, with a 53.5% response rate (GOV.UK).

Retifanlimab was originally developed by MacroGenics and licensed to Incyte under an October 2017 exclusive global collaboration and licence agreement, so the approval re-rates MacroGenics' royalty on the asset. The specific royalty tier is not confirmed from a primary filing.

Separately, on July 6 the European Commission granted marketing authorisation for Tepkinly (epcoritamab) in combination with lenalidomide and rituximab (R2) for adults with relapsed or refractory follicular lymphoma, the first bispecific-based therapy approved in Europe in the second-line setting, on the Phase 3 EPCORE FL-1 trial (NCT05409066), where fixed-duration Tepkinly plus R2 improved progression-free survival and response versus R2, with about three in four patients reaching a complete response (Genmab release; AbbVie release).

Epcoritamab, a CD3-by-CD20 T-cell-engaging bispecific built on Genmab's DuoBody platform (EPKINLY in the US and Japan, TEPKINLY in the EU), is co-developed and co-commercialised with AbbVie under their June 2020 collaboration, in which AbbVie paid $750M upfront against up to about $3.15B in milestones. The two companies share US and Japan commercial economics, with AbbVie leading commercialisation elsewhere and Genmab receiving tiered royalties on rest-of-world net sales, so the EU second-line expansion re-rates Genmab's ex-US and ex-Japan royalty leg on an already-marketed asset. The specific royalty tier is per Genmab's financial reporting rather than restated here from a primary filing. A licensed royalty and profit-share re-rate on a live product.

Separately, the FDA accepted Pharvaris's NDA for deucrictibant immediate-release capsule (20 mg) for on-demand treatment of hereditary angioedema attacks, setting a PDUFA target action date of April 23, 2027 (Pharvaris release). The pivotal Phase 3 RAPIDe-3 trial reported a median time to complete symptom resolution of 11.95 hours. A commercial read-through; no royalty layer disclosed.

On July 7 the FDA granted Rare Pediatric Disease Designation to PRG S&Tech's Trineumin, a small molecule modulating the abnormal TbetaR1-RKIP protein interaction in NF2, for neurofibromatosis type 2. On approval, an RPDD asset earns a Priority Review Voucher, a transferable and saleable instrument. Trineumin also holds FDA Orphan Drug and Fast Track designations and a Korean MFDS therapeutic-use approval, and is in Phase 1/2a.

Also on July 7 the FDA granted Rare Pediatric Disease Designation to Vanda Pharmaceuticals' VCA-894A (Nasdaq: VNDA), an investigational 2'-O-methoxyethyl phosphorothioate antisense oligonucleotide targeting a cryptic splice-site variant within IGHMBP2 that causes Charcot-Marie-Tooth disease, axonal, type 2S (CMT2S), an ultra-rare inherited neuropathy with estimated prevalence below 1 in 1,000,000 (Vanda release). As with Trineumin, the designation makes Vanda potentially eligible for a transferable, saleable Priority Review Voucher on approval. The programme is patient-specific, developed for a variant not yet observed in any other patient, so the PRV optionality rather than a commercial franchise is the royalty-adjacent read-through.

The window's one negative royalty re-rate landed on July 9, when Ionis Pharmaceuticals (Nasdaq: IONS) and partner AstraZeneca (LSE/Nasdaq: AZN) reported that the Phase 3 CARDIO-TTRansform trial of WAINUA (eplontersen), an antisense oligonucleotide TTR silencer, did not meet its primary endpoint of a composite of cardiovascular mortality and recurrent cardiovascular events up to Week 140 in transthyretin-mediated amyloid cardiomyopathy (ATTR-CM) (Ionis release; AstraZeneca 6-K).

CARDIO-TTRansform enrolled 1,432 patients across 130 sites in 20 countries, the largest ATTR-CM trial to date; in a contemporary population where a majority were already on a TTR stabiliser, adding eplontersen gave no statistically significant benefit, though a prespecified monotherapy subgroup showed a nominally significant reduction. Full data are set for the European Society of Cardiology Congress in August 2026. Ionis shares fell about 20% and AstraZeneca about 9% to 10% on the readout.

The royalty read-through is negative. Eplontersen is developed and commercialised under the December 2021 Ionis and AstraZeneca global agreement ($200M upfront, up to $485M in regulatory-approval milestones and up to $2.9B in sales-based milestones, later up to about $3.6B in total milestone and other payments after the 2023 Latin America expansion), under which the two share US economics and AstraZeneca holds ex-US commercialisation rights, with Ionis taking tiered royalties up to the mid-20% range on US sales and up to the high teens ex-US (Ionis SEC filings).

WAINUA is already approved for hereditary transthyretin amyloidosis with polyneuropathy (Wainzua in the EU) in more than 20 countries and is generating a live Ionis royalty, so the failure does not remove the existing stream. It does two things: it forecloses the ATTR-CM approval that would have unlocked part of the up-to-$485M regulatory-milestone ladder, and it caps the far larger sales-based royalty and milestone upside by closing off the cardiomyopathy indication, the setting analysts had modelled toward roughly $2B in peak sales.

It also strengthens the incumbents Ionis and AstraZeneca had aimed at, Pfizer's tafamidis, BridgeBio's acoramidis, and Alnylam's TTR silencers. A licensed royalty whose growth ceiling re-rates downward on a late-stage miss, with no milestone triggered, not a monetisation or a new stream.

The window's second negative re-rate is a full royalty extinguishment. On July 8, Alector (Nasdaq: ALEC) disclosed, in a Form 8-K under Item 1.02, that GSK (through Glaxo Wellcome UK Limited) had served written notice on July 6, 2026 to terminate the companies' July 2021 collaboration and license agreement (amended May 2023) covering the progranulin-elevating monoclonal antibodies latozinemab and nivisnebart, with the termination effective January 2, 2027 after a 180-day notice period (Alector Q1 2026 10-Q; Alector Form 8-K, Item 1.02, filed July 8).

The termination follows the collapse of both partnered programmes: latozinemab missed its clinical co-primary endpoint in the Phase 3 INFRONT-3 trial in frontotemporal dementia with a progranulin mutation (FTD-GRN) in October 2025, a failure that prompted Alector to cut close to half its workforce, and nivisnebart was discontinued in the Phase 2 PROGRESS-AD trial in early Alzheimer's disease in April 2026 after a pre-specified interim futility analysis.

The royalty read-through is negative and terminal. Under the 2021 agreement, Alector received $700M upfront and was eligible for up to about $1.5B in development, regulatory, and commercialisation milestones, most of which remain unpaid.

Outside the United States, GSK held commercialisation responsibility and Alector was eligible for double-digit tiered royalties on ex-US net sales (per Alector's Q1 2026 10-Q), with a US cost and profit-share alongside GSK. With both antibodies out of active development and the agreement terminating, that ex-US royalty leg and the remaining milestone ceiling are extinguished rather than merely re-rated downward.

No milestone is triggered by the termination, and the $700M upfront, already received in 2021 and 2022, is not clawed back. Separately, on July 8 Alector repaid in full and terminated its Hercules Capital loan and security agreement, returning $10,428,827.77 of principal plus accrued interest and end-of-term and prepayment charges, removing its principal debt obligation as it reassesses its remaining research and preclinical pipeline.

- Event: GSK notice (July 6, disclosed July 8) terminating the July 2021 Alector collaboration and licence agreement, effective January 2, 2027

- Royalty holder: Alector (Nasdaq: ALEC; South San Francisco); eligible for double-digit tiered ex-US royalties under the terminated agreement

- Counterparty: GSK (LSE/NYSE: GSK) via Glaxo Wellcome UK Limited; held ex-US commercialisation

- Assets: Latozinemab and nivisnebart, progranulin-elevating monoclonal antibodies; both out of active development after INFRONT-3 (FTD-GRN, October 2025) and PROGRESS-AD (early Alzheimer's, April 2026) failures

- Original economics: $700M upfront (received 2021 and 2022), up to about $1.5B in milestones (largely unpaid), double-digit tiered ex-US royalties to Alector, US cost and profit-share

- Royalty impact: Ex-US royalty leg and remaining milestone ceiling extinguished; no milestone triggered; upfront not clawed back

- Related: Alector repaid and terminated its Hercules Capital loan ($10,428,827.77 principal plus charges) on July 8

- Treatment: A negative re-rate that eliminates a licensed royalty outright; not a monetisation or a new stream

- Date: Notice Mon July 6, 2026; disclosed Wed July 8, 2026

Three clinical readouts re-rated royalty-adjacent assets without moving capital. Positive: Kailera and Hengrui's HRS-7535 posted China Phase 3 topline (HARBOR-1 obesity, OUTSTAND-2 T2D) on the oral GLP-1 agonist, de-risking the asset Kailera licensed from Hengrui ex-Greater China in May 2024 (tiered royalties to Hengrui), with no milestone triggered.

Negative: BMS's Krazati (adagrasib) KRYSTAL-10 missed in second-line KRAS G12C colorectal cancer, capping the Zai Lab and BMS Greater China royalty relationship (Zai holds the May 2021 licence), with no milestone triggered. Monitored: Can-Fite completed enrolment for the interim analysis of its pivotal Phase 3 psoriasis trial of piclidenoson, out-licensed for psoriasis across nine countries with double-digit royalties to Can-Fite on approval.

Standard disclaimer

This Weekly Term Sheet is provided for informational purposes only. It does not constitute investment advice, an offer to sell or a solicitation of an offer to buy any security, or a recommendation regarding any investment. Data and disclosures are sourced from public company filings, press releases, and credible secondary reporting. Capital for Cures AG does not warrant the accuracy or completeness of information presented. Readers are advised to consult primary source documentation before making any investment, partnership, or commercial decision. Capital for Cures AG and its principals may hold positions in companies referenced.