The Secured Term Loan in Royalty Finance

The least glamorous instrument in the toolkit, dissected down to the coupon

Royalty finance gets written about through its friendliest instrument, the true sale.

That is the one that makes the press releases: non-dilutive, off the balance sheet, no covenants, no maturity.

The larger and quieter flow is its opposite. A senior secured term loan, lent against the same product cash flows, carrying a lien, a coupon, an amortisation schedule, and an acceleration clause.

It is priced and papered like leveraged credit, because that is what it is.

The interesting part is not whether it counts as royalty finance. It is how finely engineered the thing actually is: the tranches, the floors, the make-wholes, the lockouts, and the four extra points of interest that switch on the day the borrower trips.

This piece takes it apart.

The legal machinery that sits underneath it, recharacterisation risk, intercreditor priority, springing liens, behaviour in distress, I have covered separately in The Royalty as a Credit Derivative and the companion piece on first-priority and springing liens. I will point back to those rather than repeat them. Here the subject is the instrument.

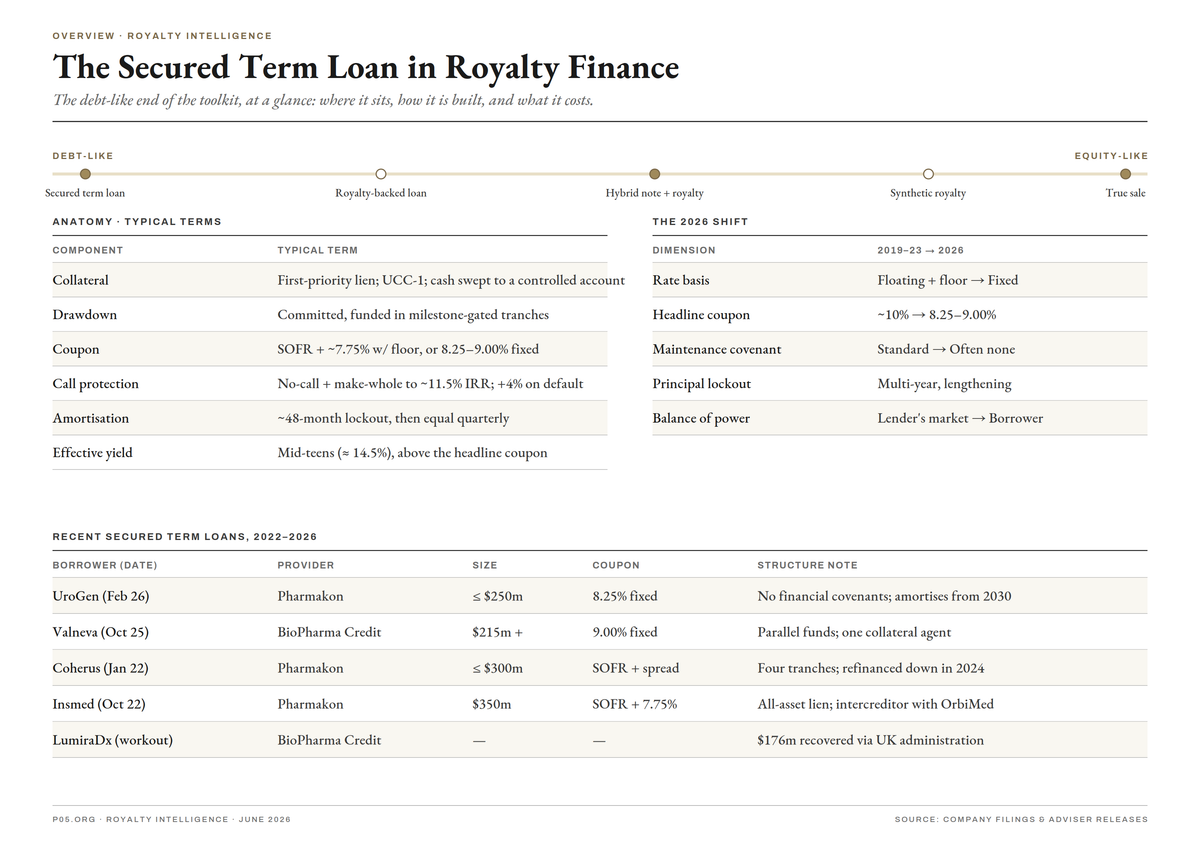

The short version

- The royalty toolkit runs on a spectrum from debt-like to equity-like. The secured term loan sits at the far debt-like end: capped return, hard collateral, real covenants, foreclosure on default.

- Two models share the name. A loan to the operating company secured by everything (the Pharmakon and BioPharma Credit model), and a loan to a royalty owner secured only by the stream (the Oberland model). They diverge sharply in a default.

- The mechanics are granular and worth knowing line by line: milestone-gated tranches, floating-plus-floor or fixed coupons in the high single digits, original issue discount, exit fees, make-wholes to a target IRR, a roughly four-point default step-up, and a multi-year principal lockout.

- The effective yield to the lender lands in the mid-teens, well above the headline coupon, once discount, fees, and warrants are counted.

- The 2026 story is borrower-friendly drift: coupons fixed as base rates eased, and the minimum-revenue covenant, once standard, has thinned to the point of disappearing for the strongest credits.

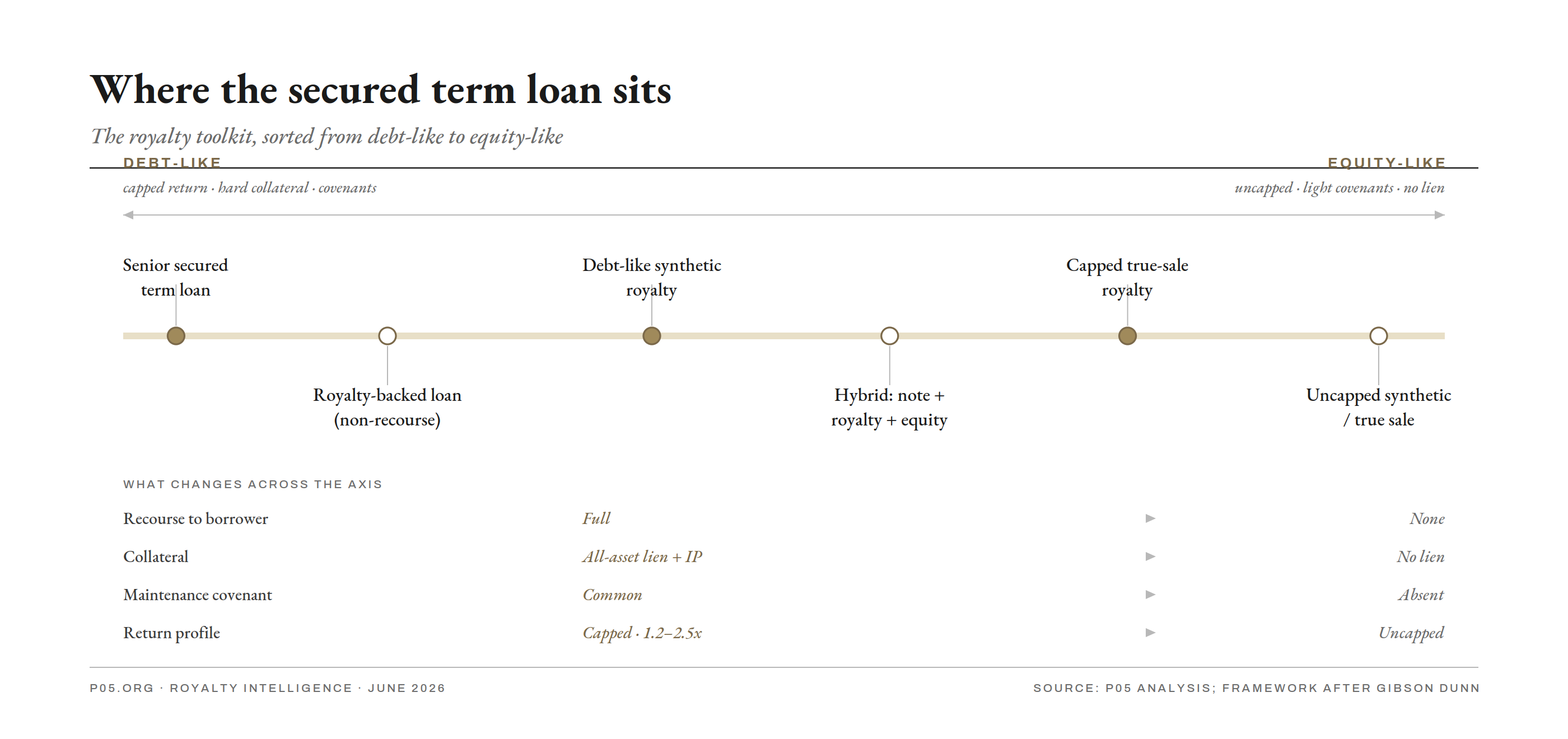

Where it sits

Start with the map, because the term loan is defined by what it is not.

Every product-level royalty instrument can be placed on one axis, running from debt-like to equity-like, depending on how much of the asset's risk the financier actually takes. Gibson Dunn's taxonomy is the cleanest version of this.

At the equity-like end, an uncapped synthetic or true-sale royalty: light covenants, no lien, the investor keeps the blockbuster upside and eats the downside.

At the debt-like end, the secured term loan: capped return, a first-priority lien, a covenant package, and the right to accelerate and foreclose.

The royalty toolkit, sorted from debt-like to equity-like. Move from right to left and recourse, collateral, and covenants all intensify while the return caps out.

The thing to hold onto is that the move along that axis is a single trade, repeated. The borrower gives up upside and accepts constraints, and in exchange the cost of capital falls.

A secured term loan is the cheapest non-dilutive money a company with real product cash flow can raise, precisely because it surrenders the most: a lien on the business, a coupon that must be paid in cash, and a lender who can step in if the numbers slip.

Two instruments travel under the single name "royalty-secured term loan," and they are not the same credit.

- Borrower-level and all-asset. A loan to the operating company, secured by a first-priority lien on substantially all of its assets, the product IP, the regulatory approvals, the receivables, guaranteed across the group. The royalty or product revenue is the reason the lender is comfortable, but the collateral is the whole enterprise. This is the Pharmakon and BioPharma Credit model.

- Royalty-level and asset-specific. A loan to a royalty owner, secured only by a discrete stream and the contracts behind it. Oberland Capital describes its own version plainly: principal and interest are drawn solely from royalties received, the loan is typically non-recourse to the holder, and once it is repaid the owner keeps every future royalty. That is closer to a project financing wrapped around one cash flow than to a corporate loan.

The distinction is invisible at signing and decisive in bankruptcy.

The first lender forecloses on a company. The second forecloses on a contract. Both call it a senior secured term loan.

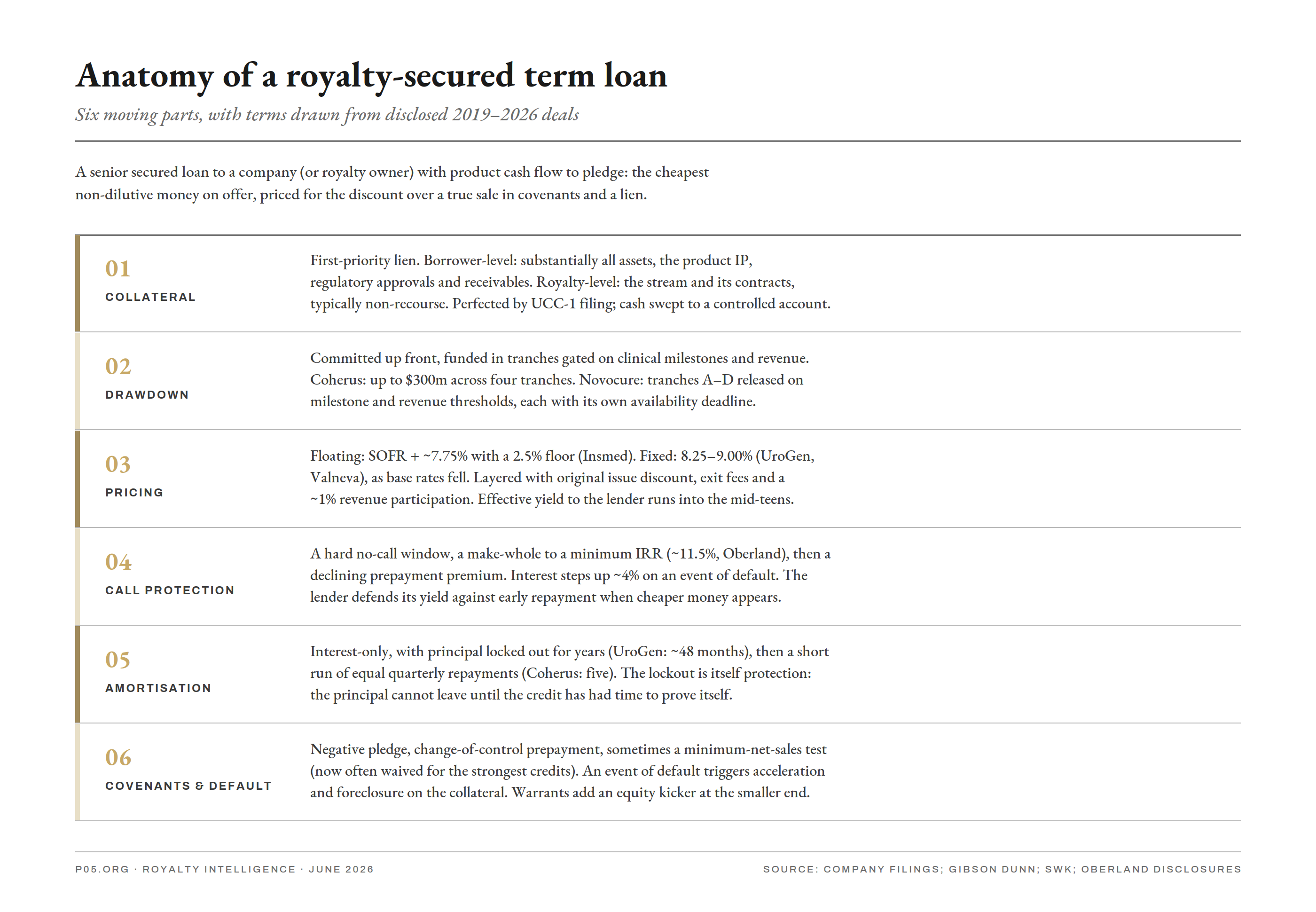

The instrument, line by line

Six parts do almost all the work. None of them is complicated on its own. The craft is in how they are tuned against each other, and the tuning is visible in the disclosed terms.

Six moving parts, with parameters drawn from disclosed 2019 to 2026 deals.

1. The collateral package is the deal

Everything else is pricing arranged around it.

- On a borrower-level loan the lender takes a first-priority lien on substantially all assets, but what it actually cares about is narrower: the acquired payments, plus the machinery that produces them, the patents and know-how, the regulatory filings and approvals, the in-licences and out-licences.

- A lien on the cash without a lien on the source is a claim on a stream you cannot redirect.

- The cash is then ring-fenced through a controlled or lockbox account, so the lender can intercept it the moment something breaks rather than chase it through the borrower's operating accounts.

- Perfection runs through UCC Article 9: financing statements filed, account control agreements taken, security interests recorded against the IP. Botch the perfection and a "secured" lender wakes up in a bankruptcy as an unsecured one, behind everyone who filed correctly.

The 2019 BioDelivery Sciences facility is a textbook specimen of the borrower-level form: subsidiary guarantees, a first-priority interest in essentially everything, and mandatory prepayment on a change of control.

Where the lender will not take the IP up front, it sometimes reserves the right to. A springing lien grants a security interest in the intellectual property automatically on a trigger, the loan balance crossing a threshold, or a performance covenant breaking, so the borrower keeps a clean IP estate while healthy and the lender's claim hardens the instant it is not. I went through the mechanics of those, and of the negative-pledge and intercreditor architecture that sits alongside them, in the liens piece.

2. Drawdown is staged, not lump-sum

These loans are committed in full and funded in tranches, gated on milestones. The lender underwrites risk in slices; the borrower avoids paying for capital before it needs it.

- Coherus borrowed under a January 2022 Pharmakon facility of up to $300 million across four tranches: $100 million at closing (of which $81.9 million immediately repaid an existing HealthCare Royalty term loan), another $100 million by April, a further $50 million in September, and a final $50 million tranche that lapsed undrawn.

- Novocure's 2024 facility of up to $400 million split into tranches A through D, with the later tranches of up to $50 million each releasing only on defined clinical milestones and revenue thresholds, each with its own availability deadline.

The headline number is a ceiling. The funded number proves itself in instalments.

3. Pricing is a stack, not a coupon

The floating template, dominant when base rates were high, is a wide margin over SOFR with a floor.

- Pharmakon's $350 million loan to Insmed priced at SOFR plus 7.75 percent with a 2.5 percent SOFR floor. The floor is not incidental: it guarantees the lender a minimum base even if rates collapse, which is exactly what began to happen across 2025.

- As base rates eased, fixed coupons returned, in the 8.25 to 9.00 percent range (UroGen, Valneva).

A disclosed Oberland senior secured note from the same era shows the full apparatus at the smaller end:

- interest of 7.5 percent over the greater of LIBOR or a 2.0 percent floor, which produced an all-in rate around 9.5 percent in early 2022 and climbed past 11.2 percent as base rates rose;

- seven-year tranches;

- a paired revenue participation adding roughly another point of interest, payable as a percentage of net revenues subject to an annual cap;

- a make-whole guaranteeing the lender a minimum 11.5 percent internal rate of return if repaid early;

- a default rate that steps up the coupon by four percentage points;

- and warrants struck off a trailing 45-day average price.

On top of the stated rate, original issue discount means the loan funds below par, and exit or success fees are keyed to repayment.

The result is that the effective yield runs well above the coupon. SWK Holdings, which writes smaller secured and royalty deals, reported a portfolio effective yield around 14.5 percent and targets mid-teens unlevered returns. That, not the 8 or 9 on the cover, is the asset class.

4. Call protection defends the yield

A lender underwriting a mid-teens return over five years does not want to be repaid in eighteen months when the borrower's stock recovers and cheaper money appears. So the agreement stacks defences:

- a hard no-call window during which prepayment is barred;

- a make-whole that pays the lender its foregone interest (or, as in the Oberland note, tops the return up to a contractual minimum IRR) if repayment comes early;

- a declining prepayment premium thereafter.

The amortisation profile is itself protection. When UroGen refinanced with Pharmakon in 2026, principal repayment was set to begin only in 2030; the principal is locked away for years before it can start leaving.

5. Amortisation is back-loaded and brief

The common shape is interest-only for a long stretch, then a short, sharp run of equal repayments.

- Coherus's terms call for five equal quarterly payments of principal beginning only after the 48-month anniversary of the first tranche.

- UroGen's repay in four equal quarterly instalments from 2030.

The lockout serves both sides: the borrower gets years of runway with only coupon to service, and the lender keeps its capital deployed and protected through the period when the credit is least proven.

6. Covenants and the default trigger are where the discount is earned

The classic package, again visible in BioDelivery, pairs a financial maintenance covenant, there a minimum net sales test, with a thicket of negative covenants: limits on new debt and liens (the negative pledge), on asset sales, on restricted payments, on changes of control.

The distinction a credit analyst should never blur is incurrence versus maintenance.

- An incurrence covenant bites only when the borrower acts.

- A maintenance covenant is tested every quarter whether the borrower acts or not, and a minimum-revenue or minimum-liquidity test is the single most dangerous line in the document for a launch-stage company, because it converts a slow commercial ramp into an event of default.

And the event of default is the whole point. On a breach, a payment miss, a change of control, or an IP challenge that impairs the collateral, the lender can accelerate the loan and foreclose. That remedy, absent from a true-sale royalty, is the entire reason the loan is cheaper.

At the smaller and earlier end, lenders also take warrants, an equity kicker that turns a fixed-return instrument into something with a tail.

Two houses, two styles

The instrument has two dominant practitioners, and their houses build it differently.

Pharmakon Advisors, manager of the BioPharma Credit funds, is the borrower-level lender at scale. Established in 2009, its funds have committed up to $11 billion across roughly 68 investments.

Its portfolio reads like a roster of commercial-stage names that needed non-dilutive cash against approved-product revenue: Collegium, Insmed, Coherus, BioCryst, Evolus, OptiNose, UroGen, Immunocore, ImmunoGen, Akebia, and others, alongside purchased royalty streams.

The structures are recognisably the same animal each time: a large committed facility, milestone tranches, a SOFR-plus-floor or fixed coupon, a multi-year lockout, an all-asset lien, and a designated collateral agent when two of its funds lend in parallel.

Oberland Capital is the structured-hybrid house. It rarely hands over a plain loan.

Its signature is to stack instruments into one bespoke package: a secured note, a revenue or royalty participation, and an equity slice or warrant, tuned so the blended cost of capital fits the borrower. The disclosed note above, with its 11.5 percent make-whole IRR and its revenue participation and its warrants, is the template. Its May 2025 financing for ClearPoint Neuro combined a secured note, a tiered royalty interest, and an equity purchase in a single deal.

The point of the hybrid is to tune price: pure secured debt is cheap but rigid, a royalty layer shares upside for a lower coupon, an equity slice aligns the financier with a recovery.

The reason the two houses matter to a borrower is the default. A Pharmakon-style all-asset lien means that if the loan breaks, the lender has a claim on the company. An Oberland-style royalty-level, non-recourse structure means that if the stream underperforms, the lender's recovery is bounded by the stream, and the rest of the business is, in principle, out of reach.

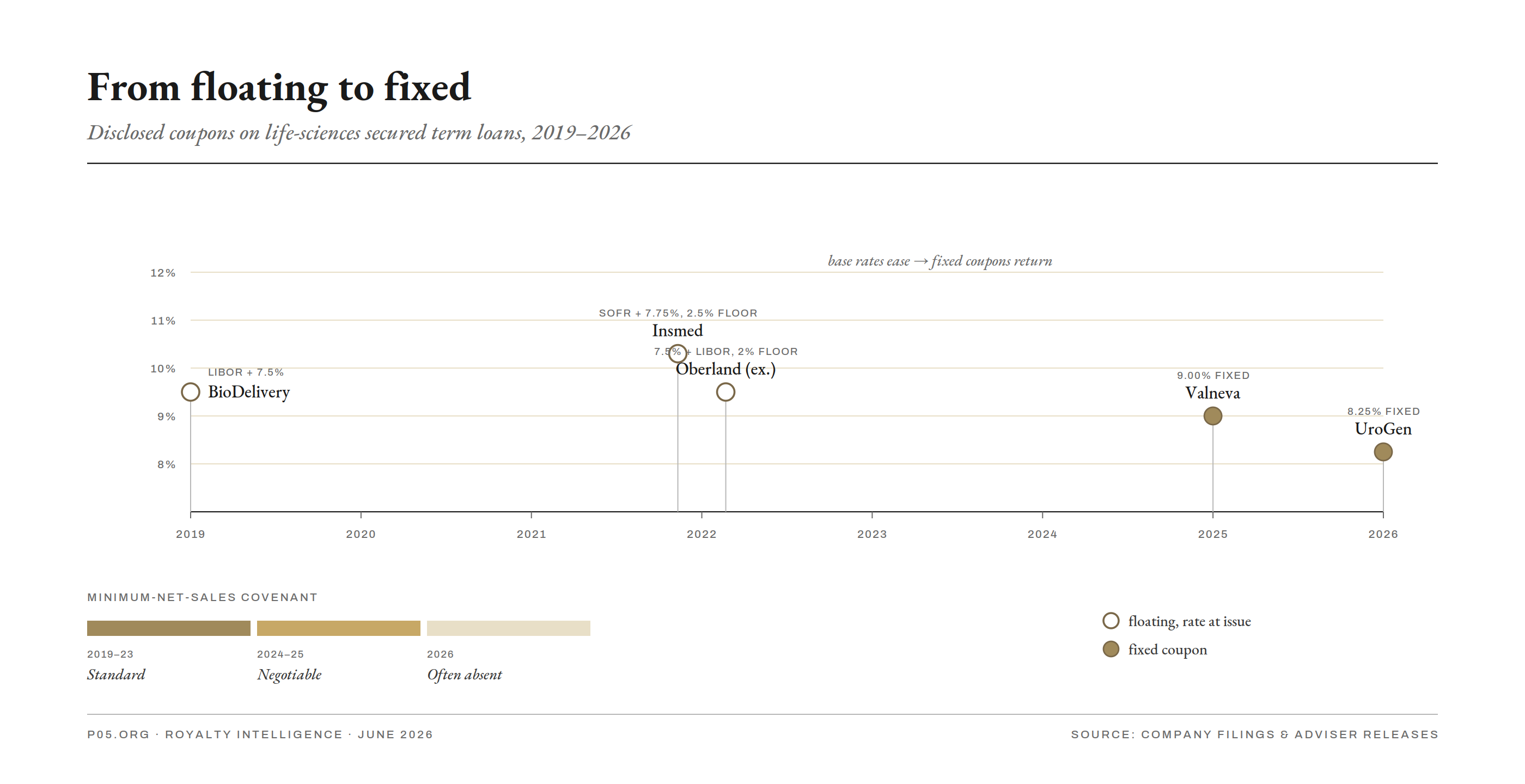

From floating to fixed

The asset class did not change shape across 2024 to 2026. It changed terms, in the borrower's favour, and the direction of the drift says something about the supply of capital.

Disclosed coupons at issue, 2019 to 2026, and the parallel erosion of the minimum-revenue covenant.

As SOFR came down from its 2023 peak, the floating-plus-floor template that defined the 2022 vintage gave way to fixed coupons.

- Valneva's October 2025 facility from BioPharma Credit carries a flat 9.00 percent to a 2030 maturity.

- UroGen's February 2026 refinancing locked in 8.25 percent fixed across the whole balance.

A fixed coupon at that level is a wager by both sides on where rates settle, and it removes the borrower's exposure to a SOFR spike; lenders accepted it because the alternative was watching a floating yield erode beneath them.

The covenant moved at the same time, and further. The minimum-net-sales maintenance test, standard in the 2019 to 2023 vintage, became negotiable, then for the strongest credits absent. UroGen's amended facility carries no financial covenants at all.

When the best borrowers can drop the maintenance covenant entirely, the marginal borrower can at least loosen it. That is the texture of a lender's market giving ground.

What did not move, by a single basis point, is the legal line underneath. Lower rates and thinner covenants do not soften recharacterisation risk, because that risk lives in bankruptcy doctrine, not in the rate environment. I will come back to why the secured term loan is, on that one question, the safest instrument in the toolkit.

The deals, read closely

Coherus: the full lifecycle in one borrower

The January 2022 facility (up to $300 million, four tranches) was classic balance-sheet debt against a commercial biosimilars business, and its first act was to refinance away an older HealthCare Royalty loan, lender displacing lender.

By May 2024, as Coherus pivoted to oncology, it restructured again: the Pharmakon term debt was cut to a new $38.7 million loan maturing in 2029, paired with a $37.5 million royalty monetisation on future LOQTORZI and UDENYCA sales.

The arc is the point. A secured term loan is not a one-time event; it is refinanced, resized, repaid, and reshaped as the borrower's commercial story changes, often by the same lender swapping one structure for another.

UroGen: the covenant-light turn made concrete

The February 2026 refinancing amended and restated a 2024 Pharmakon loan into a senior secured facility of up to $250 million.

The first $200 million funded at closing, refinancing the legacy $125 million facility and handing the company roughly $75 million of fresh capital; a second $50 million tranche is drawable at the company's discretion through mid-2027. Fixed 8.25 percent, principal locked out to 2030, and no financial covenants.

It is the secured term loan stripped of the one feature that historically separated it from the friendlier instruments. The lien and the acceleration right remain. The leash is simply much longer.

Valneva: the parallel-fund mechanic

The 2025 facility had the listed BPCR vehicle fund $30 million and the parallel BioPharma-V fund put in $185 million side by side, with BPCR as collateral agent, and up to $285 million more reserved for future business development, releasable only by mutual agreement.

Two things are worth lifting out:

- The parallel structure lets a manager spread a large ticket across vehicles while giving the borrower a single point of contact and one agent to enforce the security.

- The business-development tranche is an option on the relationship: capital pre-negotiated but uncommitted, so the borrower can fund an acquisition quickly without reopening the agreement.

When the loan breaks

The case for the secured term loan is made not in the deals that perform but in the ones that do not, because that is where the lien earns its coupon. The same lender's book shows both outcomes.

Akebia: the amend-and-extend

When its loan approached maturity ahead of an uncertain FDA decision on vadadustat, Pharmakon amended the agreement rather than enforce it: maturity pushed out, quarterly principal deferred.

A secured lender with a real lien has the luxury of patience. It can nurse a borrower through a binary event because, if the event goes the wrong way, it still sits first in line. The borrower gets runway; the lender protects a recovery it might otherwise have crystallised at a loss.

LumiraDx: the foreclosure

When the diagnostics company failed, the loan did not evaporate. The collateral was realised through a UK administration, and BioPharma Credit recovered $176 million from the administrator across the second half of 2024.

That is the secured term loan doing exactly what it is built to do in the bad state: convert a lien into cash through an insolvency process, ahead of unsecured creditors and equity. A true-sale royalty holder in the same wreck would have been litigating over whether it owned the stream at all.

The contrast with the equity-like end is the whole argument. The defaults that have scarred royalty investors, the acceleration and step-in fights and the disputes over who owns a stream once a company files, are concentrated in the structures that reached for off-balance-sheet treatment while keeping loan-like protections. The secured term loan does not have that problem, for a simple reason.

The one line that still matters

A secured term loan and a true-sale royalty can deliver almost identical cash flows. The difference only surfaces in bankruptcy, and it is binary.

- True sale: the stream left the company's estate at closing, and the buyer owns it.

- Loan: the stream never left; it is collateral, inside the estate, subject to the automatic stay, and the "purchase" payments may be attacked as preferences.

The trap, which I worked through in The Royalty as a Credit Derivative, is that a court decides which one it was, and it is not bound by the label on the document. It looks at how the risk was actually allocated, recourse, who bears the loss, whether the return is fixed, whether there is a fixed-price repurchase right, and recharacterises a "sale" as a disguised loan when the substance is lending.

That is why prudent synthetic-royalty buyers file backup liens even on deals papered as sales: so that if the sale is recharacterised, they are at least perfected secured lenders rather than unsecured ones.

Here is the quiet advantage of the instrument in this piece. The secured term loan has no recharacterisation risk, because there is nothing to recharacterise. It is openly a loan, openly collateralised, openly perfected. It accepts on-balance-sheet debt treatment and gives up the off-balance-sheet accounting that tempts the synthetic structures into trouble.

In exchange, it gets the one thing that actually pays out in a default: an unambiguous, first-priority, enforceable lien.

The synthetic royalty spends its life trying to prove it is not a loan. The secured term loan never has to, and recovers more when it matters.

What it means

For borrowers. This is the cheapest non-dilutive money available to a company with real product cash flow, and the discount over a true sale is paid for in covenants and a lien. In 2026 that price has fallen: fixed coupons in the high single digits, principal locked out for years, and, for the strongest credits, no maintenance test.

- The clause to fight over is not the coupon but the minimum-revenue covenant, which can turn a slow launch into a default. Strike it if you can; if you cannot, set the threshold against a downside case, not the plan.

- Read the call protection before the rate, because a make-whole to a target IRR can make an early refinancing far more expensive than the headline coupon suggests.

For lenders. The return lives in the collateral package and the call protection, not the coupon.

- Perfect everything, sweep the cash to a controlled account, take the IP and approvals into the lien and not just the stream, and reserve a springing lien where the borrower will not grant IP security up front.

- The covenant erosion that wins deals on better optics is real margin surrendered: a loan with no maintenance test cannot be accelerated until a payment is actually missed, by which point the recovery is harder and the borrower's options are fewer.

- Patience in a workout is a privilege the lien buys; price it.

For investors and analysts. When a company announces "non-dilutive financing," read the structure before the adjective.

- A true sale removed an asset from the estate. A secured term loan added senior debt on top of it, ahead of the equity in every downside. The two have opposite implications for residual value, and the disclosure that tells them apart is the collateral and covenant language, not the headline.

- A fixed coupon and a dropped maintenance covenant are not generosity; they are the current price of a lender's market, and they will re-price when capital tightens.

The verdict

The secured term loan is the least glamorous instrument in royalty finance and, by volume, one of the most important. It is where companies with proven cash flow go for the cheapest non-dilutive capital, and it is engineered like the leveraged credit it is, down to the floor on the floating rate and the four points that switch on at default.

Everything that matters is in two places. The collateral package, which decides what the lender controls when the stream is the only thing worth controlling. And the loan-versus-sale line, which the term loan settles in its own favour by simply being, and admitting to being, a loan.

In 2026 the terms have moved toward the borrower. The lien underneath has not moved at all.

Reflects publicly available information as of June 2026, derived from company releases, SEC filings, adviser publications, court and administration filings, and financial news reporting. Transaction terms are as disclosed by the parties or their advisers; figures for individual deals are approximate and as reported. Information may have changed since publication. For informational purposes only; not investment, legal, or financial advice. The author is not a lawyer or financial adviser.