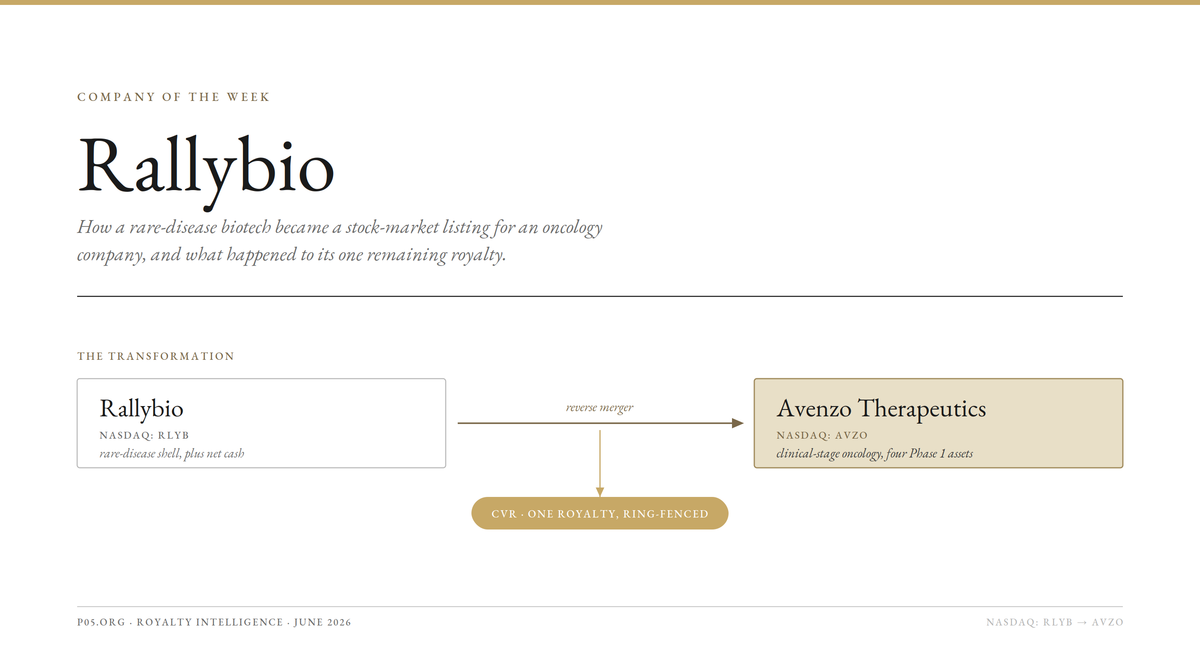

Company of the week: Rallybio

Rallybio is a New Haven rare-disease biotech that lost its lead program in 2025, sold what it could, and by mid-2026 had been reduced to a stock-market listing and a pile of cash that an oncology company, Avenzo Therapeutics, is now reversing into. Its surviving royalty stack is a single early-stage interest, ring-fenced inside a contingent value right.

Rallybio Corporation (Nasdaq: RLYB) spent most of its public life as a clinical-stage rare-disease company built around the prevention of fetal and neonatal alloimmune thrombocytopenia (FNAIT). As of June 2026 it is something else entirely: a near-empty public shell, valued at roughly $15 million in its latest merger math, being taken over by an oncology developer that will assume its Nasdaq listing and rename itself.

For a royalty-intelligence reader the interesting question is not the science but the cash-flow residue. When a biotech is hollowed out into a shell, its development-stage royalty and milestone entitlements do not disappear. They get isolated, valued, and assigned, usually to legacy shareholders through a contingent value right (CVR). Rallybio is a clean worked example of that mechanic, and of how thin the surviving royalty stack can be once the operating company is gone.

This piece does three things: it explains, plainly, what a reverse merger is and why a failed biotech becomes a vehicle for one; it traces Rallybio's specific path from a failed FNAIT lead to two back-to-back merger attempts; and it follows the money, showing exactly which royalty interests survive, where they sit, and which direction they flow.

At a glance

| Item | Detail |

|---|---|

| Company | Rallybio Corporation (Nasdaq: RLYB), New Haven, Connecticut |

| Original focus | Rare diseases: complement dysregulation and hematology |

| Former lead | RLYB212 (anti-HPA-1a antibody for FNAIT prevention), discontinued Apr 2025 |

| Current status | Public shell undergoing reverse merger into Avenzo Therapeutics |

| Surviving royalty | REV102: low single-digit on Recursion net sales (held in a CVR) |

| Combined company | Avenzo Therapeutics, Nasdaq: AVZO, clinical-stage oncology |

| Legacy holders keep | ~2.8% of the combined company, plus a contingent value right |

From FNAIT lead to strategic pivot

Rallybio's flagship was RLYB212, a monoclonal anti-HPA-1a antibody intended to prevent FNAIT, a rare condition in which maternal antibodies attack fetal platelets. In April 2025 the company discontinued RLYB212 after second-trimester pharmacokinetic data from the sentinel participant in its Phase 2 trial showed the dose regimen could not reach the target concentration range of 6 to 10 ng/mL, nor even the 3 ng/mL minimum the company believed was needed for efficacy.

Losing RLYB212 removed the company's most advanced and most differentiated asset. Alongside it came a 40% workforce reduction of nine positions. The narrative re-centred on what remained:

| Program | Mechanism / target | Indication focus | Stage at pivot |

|---|---|---|---|

| RLYB116 | Long-acting C5 complement inhibitor | PNH, antiphospholipid syndrome, gMG | Phase 1 |

| RLYB332 | Long-acting anti-matriptase-2 antibody | Iron-overload diseases | Preclinical |

| REV102 | Oral ENPP1 inhibitor (Recursion JV) | Hypophosphatasia (HPP) | IND-enabling |

RLYB116 eventually produced a clean readout: in February 2026 Rallybio reported positive Phase 1 data showing complete and sustained inhibition of terminal complement. By then, however, the company had already run a reverse stock split and was pursuing a strategic transaction rather than its own Phase 2. The science worked; the standalone company did not survive it.

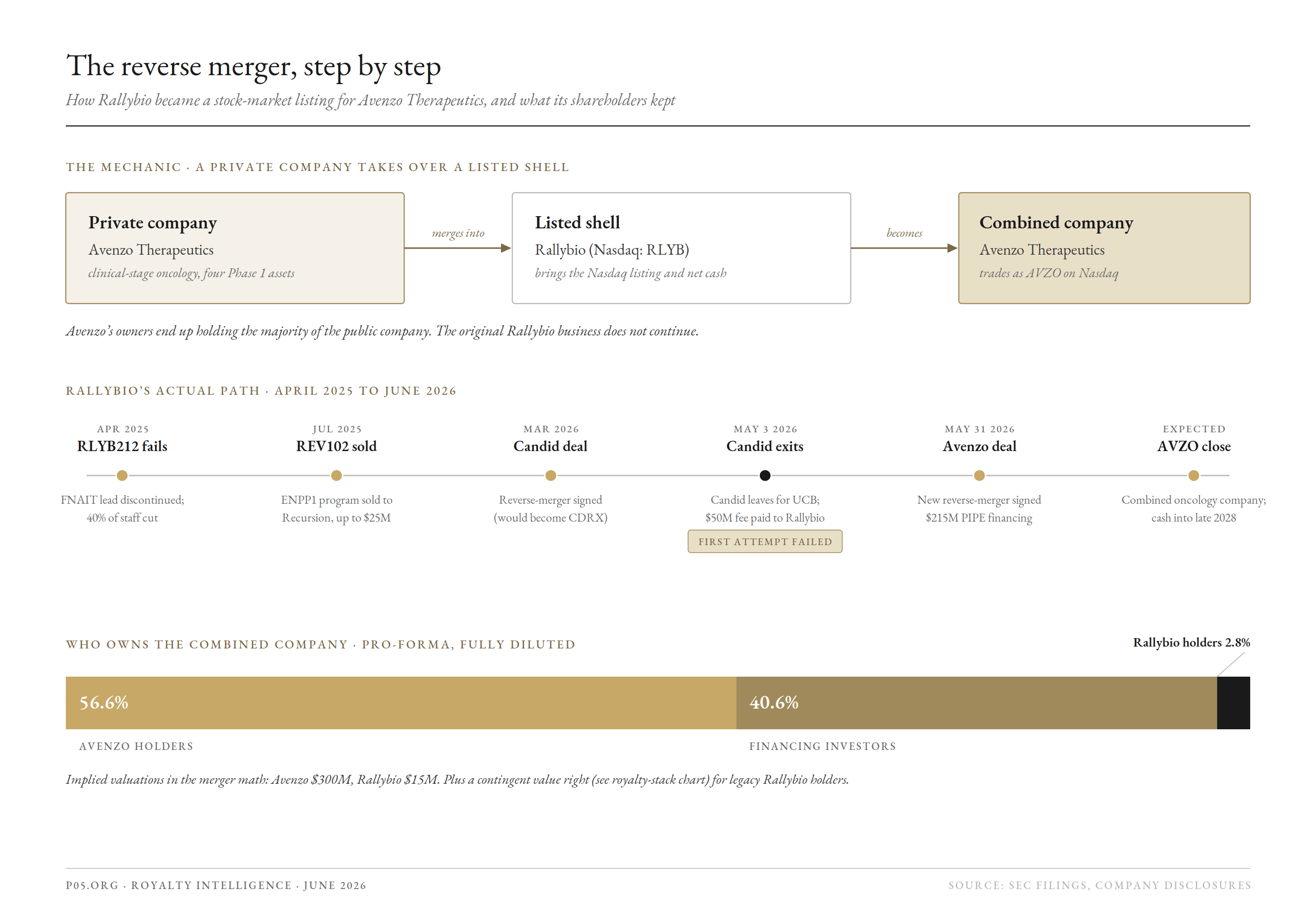

What a reverse merger actually is

Because this is the entire story of Rallybio in 2026, it is worth stating the mechanic precisely before getting to the specifics.

A reverse merger is how a private company becomes publicly traded without an IPO. Instead of selling new shares to the public, the private company merges into an existing listed company, and the private company's owners receive enough new stock to end up holding the majority. The listed company contributes two things of value: its Nasdaq listing and whatever net cash it has left. Everything else about it, including its name, its management, and often its pipeline, is replaced.

The reverse-merger mechanic and Rallybio's actual path, April 2025 to June 2026. Source: SEC filings, company disclosures.

The three roles in the Rallybio transaction map cleanly onto that structure:

| Role | Party | What it brings | What happens to it |

|---|---|---|---|

| Private company | Avenzo Therapeutics | Oncology pipeline, management, $215M new financing | Survives; its owners take majority control |

| Listed shell | Rallybio (RLYB) | Nasdaq listing, net cash | Identity dissolved; renamed |

| Combined company | Avenzo Therapeutics (AVZO) | All of the above | Trades publicly as the surviving business |

Why does a failed biotech make a good shell? Because it has the one thing a private company cannot easily buy: a clean, compliant Nasdaq listing, plus cash that an acquirer would otherwise have to raise. A biotech whose science has stalled but whose balance sheet and listing are intact is, in effect, a pre-built public vehicle. Rallybio fit the profile precisely after April 2025.

The two merger attempts, side by side

Rallybio did not pivot to oncology in one clean step. It signed one reverse merger, watched it collapse, collected a large break fee, and signed a different one four weeks later.

The first deal, with Candid Therapeutics (an autoimmune T-cell engager developer), was signed in March 2026. It fell apart on May 3, 2026, when Candid terminated to accept a competing offer from UCB S.A., triggering a $50 million termination fee payable to Rallybio. Rallybio then signed with Avenzo on May 31, 2026.

| Candid deal (failed) | Avenzo deal (live) | |

|---|---|---|

| Signed | March 2026 | May 31, 2026 |

| Combined name / ticker | Candid Therapeutics / CDRX | Avenzo Therapeutics / AVZO |

| Therapeutic area | Autoimmune (T-cell engagers) | Oncology (small molecules + ADCs) |

| Concurrent financing | $505M+ | $215M |

| Outcome | Terminated; Candid chose UCB | Proceeding |

| Effect on Rallybio | $50M termination fee received | Reverse merger, legacy assets to a CVR |

The episode matters because it changed what Rallybio was worth. A shell's value in a reverse merger is essentially its net cash plus the cleanliness of its listing. The $50 million break fee improved the cash side materially, and arrived precisely as the company needed a new partner.

The Avenzo transaction is anchored by a $215 million private placement whose investors include Blackstone Multi-Asset Investing, T. Rowe Price Investment Management, Vivo Capital, OrbiMed, SR One, and Foresite Capital. On a fully diluted basis, pre-merger Avenzo holders are expected to own about 56.6%, financing investors about 40.6%, and pre-merger Rallybio holders about 2.8%, on assumed valuations of $300 million for Avenzo and $15 million for Rallybio. Combined cash is expected to fund operations into late 2028.

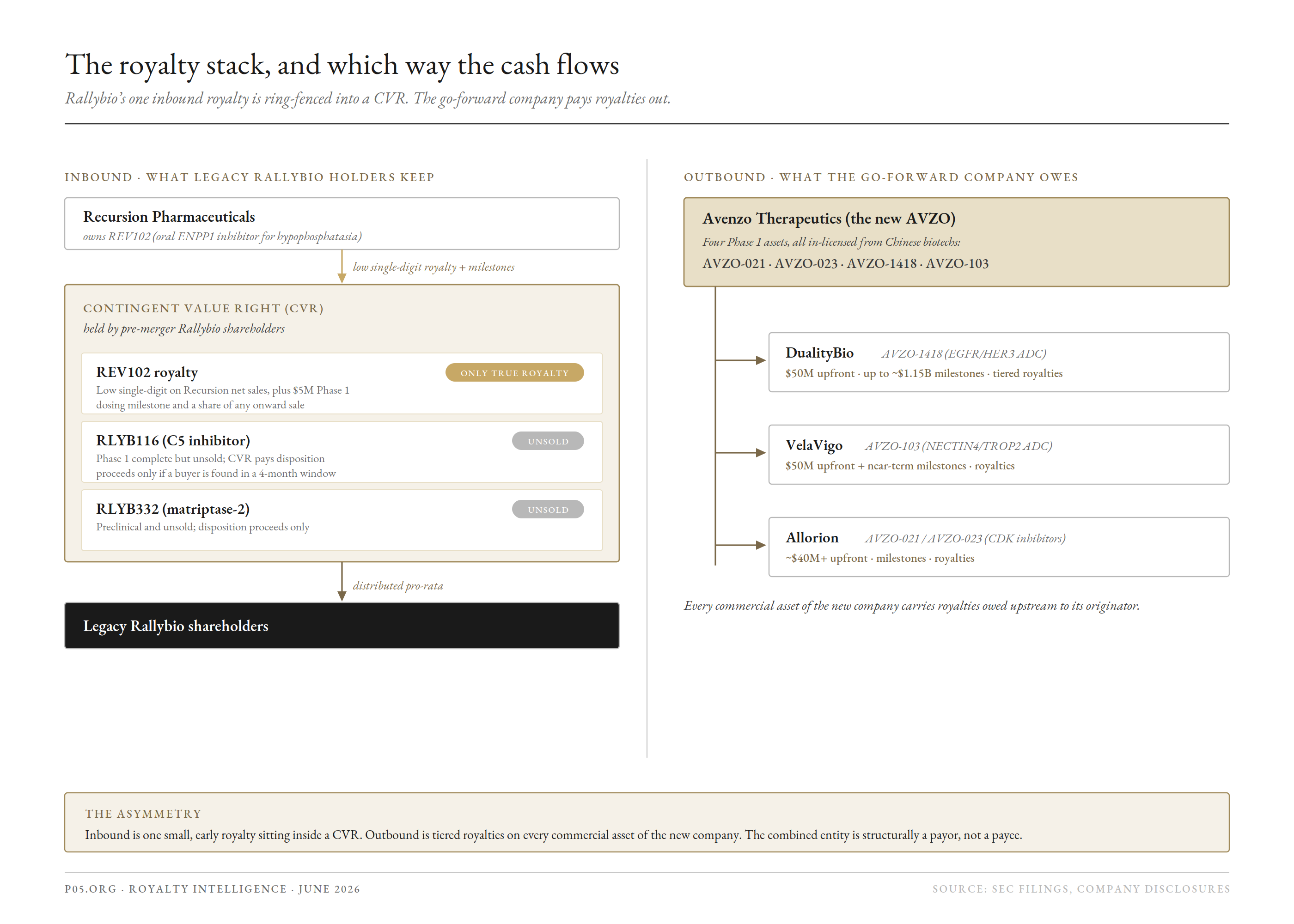

The royalty stack: one residual interest, ring-fenced

Here is the part that matters for a royalty desk, and it is worth being exact about, because the headline ("rare-disease biotech merges with oncology company") obscures it entirely.

Where Rallybio's cash flows actually go: one thin inbound royalty ring-fenced into a CVR, against the new company's outbound royalty obligations. Source: SEC filings, company disclosures.

The only part of Rallybio's portfolio that ever became a true royalty stream is REV102, an oral ENPP1 inhibitor for hypophosphatasia that came out of a joint venture with Recursion Pharmaceuticals (the JV originated with Exscientia, which Recursion absorbed). In July 2025 Rallybio sold its interest in REV102 to Recursion for up to $25 million. The structure:

| REV102 sale component | Amount | Status |

|---|---|---|

| Upfront equity | $7.5M | Paid (Jul 2025) |

| Preclinical milestone (additional studies) | $12.5M | Paid (Sep 2025) |

| Phase 1 dosing milestone | $5M | Contingent; Phase 1 expected 2H 2026 |

| Royalty on net sales | Low single-digit | Contingent on approval and sales |

| Share of onward-sale proceeds | Undisclosed | Contingent on Recursion selling REV102 |

REV102 itself remains in IND-enabling studies, with Phase 1 expected in the second half of 2026 into a diagnosed HPP population of more than 7,800 patients across the US and EU5.

That single low-single-digit royalty is the whole inbound stack. The other two assets, RLYB116 and RLYB332, are not royalties at all; they are unsold programs that may or may not fetch a price.

Where the stack lives now: the CVR

To separate the old business from the new one, the merger establishes a contingent value right program for existing Rallybio shareholders. The legacy royalty and programs do not travel into the oncology company. They are ring-fenced and assigned to the people who owned Rallybio before the merger.

Per the CVR terms, holders receive a pro-rata share of net proceeds Rallybio collects from two sources:

| CVR contents | What it pays on | Certainty |

|---|---|---|

| REV102 (Recursion agreement) | The $5M dosing milestone, low single-digit royalties, and any cash from Recursion under the July 2025 purchase agreement | Low: pre-clinical, long-dated |

| RLYB116 (C5 inhibitor) | Disposition proceeds, if a buyer is found | Conditional: unsold, 4-month effort window after closing |

| RLYB332 (matriptase-2) | Disposition proceeds, if a buyer is found | Conditional: preclinical, unsold |

For four months after closing, Rallybio is to use commercially reasonable efforts to dispose of the legacy assets to a third party it had already been in discussions with. Nothing about that sale, or its price, is contracted.

So the entire surviving royalty stack is: one low-single-digit royalty on a preclinical asset that has not dosed a human, plus two unsold programs, all parked in a CVR whose value depends on a four-month disposition window. It is small, early, and contingent.

The go-forward company is a royalty payor, not a payee

The royalty lens inverts when you look at what Rallybio is becoming. Avenzo is a study in the China-to-West licensing model. It was founded in 2022 by former Turning Point Therapeutics executives Athena Countouriotis and Mohammad Hirmand (Turning Point was acquired by Bristol Myers Squibb for $4 billion), had raised roughly $446 million before this transaction, and built its pipeline by in-licensing four assets from three Chinese biotechs.

Its four Phase 1 programs:

| Program | Modality | Origin | Status / near-term milestone |

|---|---|---|---|

| AVZO-021 | CDK2 inhibitor | Allorion (Guangzhou) | ORION-1 fulvestrant combination enrolling; updated Phase 1 data at ASCO 2026 |

| AVZO-023 | CDK4 inhibitor | Allorion | ORION-1 combination; preliminary data late 2026 |

| AVZO-1418 | EGFR/HER3 bispecific ADC | DualityBio (HK-listed) | AVENTINE-1 monotherapy, 30+ patients, NSCLC signal; Fast Track in EGFRm TKI-pretreated NSCLC; data 2H 2026 |

| AVZO-103 | NECTIN4/TROP2 ADC | VelaVigo (Shanghai) | BEACON-1 Phase 1; Fast Track in post-enfortumab vedotin urothelial; data 2H 2026 |

Each in-license carries economics that flow upstream. These are obligations the combined company owes, not income it earns:

| Originator | Asset(s) | Avenzo's upstream obligation |

|---|---|---|

| DualityBio | AVZO-1418 | $50M upfront, up to ~$1.15B milestones, tiered royalties on sales outside Greater China |

| VelaVigo | AVZO-103 | $50M upfront plus near-term milestones, royalties |

| Allorion | AVZO-021 / AVZO-023 | ~$40M+ upfront, milestones, royalties |

The asymmetry is the point. Anyone modelling the combined company's economics is modelling assets that owe royalties upstream to their Chinese originators, not assets that generate royalties. The combined entity is structurally a payor.

Red team vs blue team

Risk analysis (red team)

The operating company is effectively gone. At roughly 2.8% pro-forma ownership and a $15 million implied valuation, pre-merger Rallybio holders are minority passengers in an oncology company they did not underwrite. The rare-disease franchise they backed no longer exists as a going concern.

The royalty stack is one early, small interest. The REV102 royalty is low single-digit on a preclinical asset that has not entered the clinic. Its risk-adjusted value is modest and its timeline is long, and it sits behind a $5 million dosing milestone that has not yet triggered.

The CVR may pay little or nothing. Its value depends on selling RLYB116 and RLYB332 within a four-month window and on REV102 advancing. None of that is contracted. A clean Phase 1 for RLYB116 helps, but an unpartnered C5 inhibitor in a competitive complement field is not a guaranteed sale at an attractive price.

The company changed direction twice in two months. A signed merger with Candid collapsed in early May, and a different merger with Avenzo was signed at the end of May. The $50 million fee softened the outcome, but the sequence reflects a company being shopped, not a thesis being executed.

The go-forward entity is a royalty payor. For anyone attracted by the biotech's cash flows, the Avenzo pipeline owes tiered royalties and large milestones upstream to DualityBio, VelaVigo, and Allorion. The combined company's value is in clinical assets carrying licensing obligations, not in a royalty book.

Opportunities and mitigants (blue team)

The break fee was real, non-dilutive cash. The $50 million Candid termination fee arrived without issuing equity and strengthened the balance sheet at the moment Rallybio most needed it, improving its standing as a merger counterparty.

RLYB116 is a de-risked, sellable asset. Complete and sustained terminal complement inhibition in Phase 1 is a clean result in a field with multiple commercial precedents. That is the kind of asset that can find a buyer, which is exactly what the CVR needs.

The CVR is genuine optionality at near-zero cost basis. Legacy holders retain upside on REV102 royalties and on any legacy-asset sale without funding continued development. If REV102 reaches the market through Recursion, the royalty pays for years with no further investment.

REV102 has a credible path. It is positioned as a potential first oral disease-modifying therapy for HPP, with Phase 1 expected in the second half of 2026 and a defined diagnosed population. Each clinical step lifts the value of both the milestone and the royalty inside the CVR.

The reverse merger preserves listing value. Rather than winding down, Rallybio is monetising its listing and cash into a stake in a financed oncology company with four Phase 1 programs, two carrying FDA Fast Track designations, and runway into late 2028.

| Risk | Concern |

|---|---|

| Minority position | Pre-merger holders own about 2.8% of the combined company |

| Thin royalty stack | One low single-digit, pre-clinical REV102 royalty |

| Uncertain CVR | Legacy-asset sale and REV102 progress both unguaranteed |

| Strategic whiplash | Two merger paths inside two months |

| Royalty direction | Go-forward company owes royalties upstream, not down |

| Opportunity | Observation |

|---|---|

| Non-dilutive cash | $50M Candid break fee strengthened the balance sheet |

| Sellable asset | RLYB116 Phase 1 result supports a disposition |

| Cheap optionality | CVR retains upside with no further funding required |

| REV102 path | First oral HPP candidate, Phase 1 expected 2H 2026 |

| Listing preserved | Stake in a financed oncology company, runway to late 2028 |

Conclusion

Rallybio is a case study in what happens to a development-stage royalty interest when the company that created it does not survive. The science partly worked: REV102 was monetised cleanly, and RLYB116 produced a clean Phase 1. The company did not. By June 2026 Rallybio is a public shell being absorbed by Avenzo Therapeutics, its rare-disease identity replaced by a China-licensed oncology pipeline, its former shareholders reduced to a small minority of the combined company plus a contingent value right.

For a royalty desk the lesson is structural rather than scientific. The only durable royalty Rallybio ever held, the low single-digit REV102 interest, does not move into the oncology company. It is isolated into a CVR alongside two unsold programs, where its value depends on a four-month disposition window and on a preclinical asset reaching the clinic. That is the entire surviving royalty stack: small, early, and contingent. The go-forward company, meanwhile, is a net payer of royalties to its originators. The interesting cash flows here are the ones leaving, not the ones arriving.

The near-term tests are concrete. Whether RLYB116 and RLYB332 are sold inside the post-closing window, and at what price, will set most of the CVR's value. Whether REV102 doses its first Phase 1 patient on schedule in the second half of 2026 will determine whether the one real royalty in the stack ever starts to matter. Both will be visible within twelve months. Until then, Rallybio is best understood not as a biotech but as a disposition in progress, with a thin royalty residue parked in a box for the people who used to own it.

All information in this article was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, and financial news reporting. Specific terms of the REV102 royalty, the Avenzo upstream licensing economics, and the contingent value right are summarised from public disclosures and may not reflect the full executed agreements. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.