The Skinny-Label Question Comes to One First Street: What Hikma v. Amarin Means for Pharmaceutical Royalty Financing

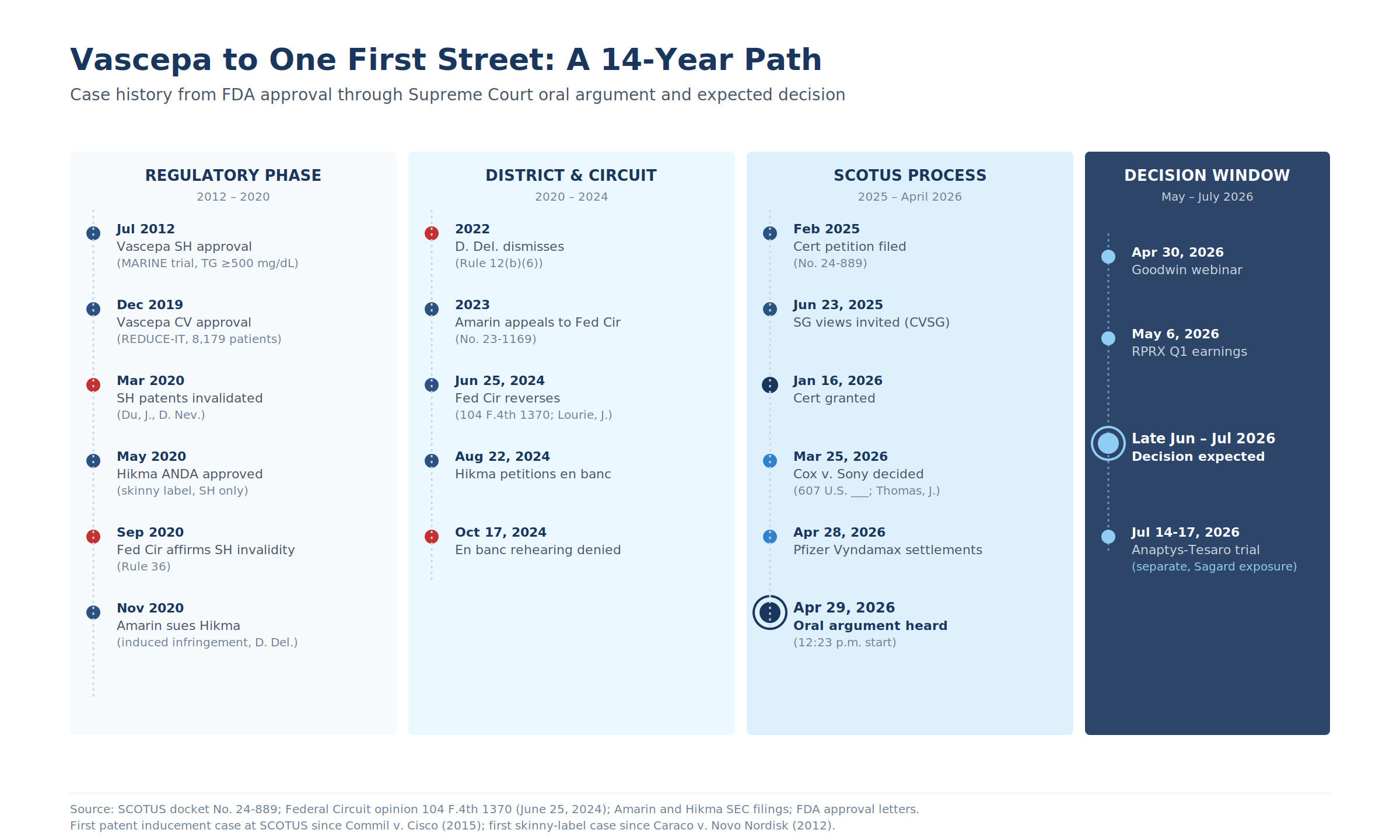

On Wednesday, April 29, 2026, the Supreme Court of the United States heard oral argument in Hikma Pharmaceuticals USA Inc. v. Amarin Pharma, Inc. (No. 24-889).

It is the Court's first patent inducement case since Commil v. Cisco (2015) and its first skinny-label case since Caraco v. Novo Nordisk (2012). On a quiet read, it is the most consequential structural legal event of the week for anyone who underwrites royalties on commercial-stage pharmaceutical assets. The Court granted certiorari on January 16, 2026 and a decision is expected before the summer recess in late June or early July 2026.

This piece is a structural reading of the case for the royalty-fund audience. The aim is neutral: to surface what the doctrine actually controls, where the cash flows sit, and which underwriting assumptions are now genuinely at stake.

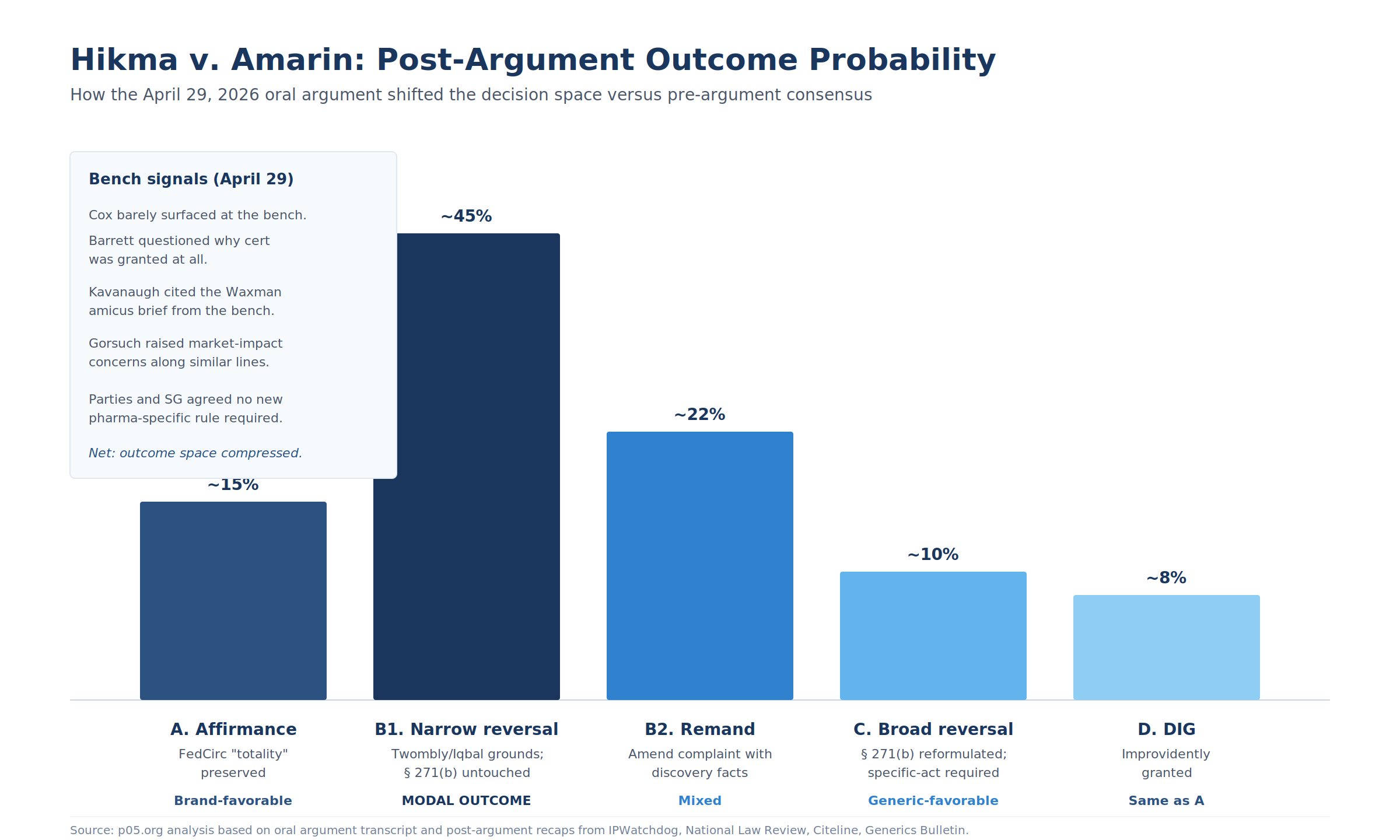

The bench-question signal from yesterday's argument has shifted the analytical picture meaningfully versus pre-argument expectations. The temporal coincidence of the SCOTUS argument with the April 28 Pfizer Vyndamax ANDA settlements (covered separately in this week's Term Sheet) places two opposite-sided answers to the same structural question inside a single 24-hour window. That alone deserves attention.

Figure 1: Case history from FDA approval through Supreme Court oral argument and expected decision window.

1. The Mechanics: Vascepa, the SH/CV Split, and Why Method-of-Use Patents Carry Royalties

Vascepa (icosapent ethyl) is a high-purity omega-3 product originally approved by the FDA in July 2012 for severe hypertriglyceridemia (the "SH" indication, triglycerides at or above 500 mg/dL).

In December 2019, following the Reduce-It trial (an 8,179-patient outcomes study representing more than $300M of Amarin investment), Amarin obtained a second approval for cardiovascular risk reduction (the "CV" indication, triglycerides at or above 150 mg/dL with established CV disease or diabetes plus other risk factors).

The CV indication, won at substantial trial cost, drives the overwhelming majority of Vascepa prescriptions. By 2020, more than 90 percent of Vascepa sales were CV-driven, and more than 75 percent of icosapent ethyl prescribing is for the CV indication.

The legal architecture matters here. The original SH-related patents were invalidated as obvious following adverse litigation in the District of Nevada (affirmed by the Federal Circuit in 2020). What remained were the CV method-of-use patents (US 9,700,537 and US 10,568,861, with additional CV-method continuations issuing through 2024).

In other words: the protection that survived was a method-of-use layer covering a later-developed indication, not composition-of-matter. This is the precise structural posture that royalty funds underwrite across a meaningful share of their commercial-stage portfolios. The CV moat is a method-of-use moat.

The Hatch-Waxman skinny-label pathway, codified at 21 U.S.C. § 355(j)(2)(A)(viii) (the "section viii" carveout), allows a generic ANDA filer to omit patented method-of-use indications from its label and seek FDA approval only for the unpatented indication(s). Hikma did exactly this: in May 2020, Hikma received FDA approval for a generic icosapent ethyl with a label limited to SH.

What turned a routine carveout into a Supreme Court case was conduct outside the FDA submission. According to the Federal Circuit opinion (104 F.4th 1370, June 2024), Amarin's complaint alleged:

- Press release framing. Hikma described its product as the "generic version of" or "generic equivalent to" Vascepa, without specifying that its product was approved for fewer indications than the branded reference.

- Sales data. Hikma cited US sales numbers for the entire Vascepa franchise across multiple press releases (the Federal Circuit specifically referenced the $919M figure in Hikma's March 2020 release and the $1.1B figure in a later release, both of which "accounted for sales of Vascepa for all uses"), in a market where the CV indication "undisputedly made up more than 75 percent" of sales.

- Website materials. Hikma's site asserted AB therapeutic-equivalence rating in language that implied a "therapeutic category" broader than its approved SH indication.

- Label content. The skinny label allegedly omitted a "CV Limitation of Use" that would have signaled the generic was not approved for cardiovascular risk reduction. The label also retained statin-interaction warnings and a reference to the Reduce It trial.

The District of Delaware dismissed at the Rule 12(b)(6) pleadings stage. The Federal Circuit reversed unanimously (panel: Chief Judge Moore, Lourie writing, Albright sitting by designation), holding that the totality of Hikma's communications, taken alongside the label, "at least plausibly" alleged active inducement of healthcare providers' direct infringement under 35 U.S.C. § 271(b).

Judge Lourie explicitly distinguished the case from a GSK v. Teva-style scenario where the allegation rests on a label that is "not skinny enough"; this, the Federal Circuit said, was "a run-of-the-mill" induced infringement case grounded on the totality. En banc rehearing was denied October 17, 2024.

Hikma's defense rests on the structural feature that Hatch-Waxman requires the generic label to mirror the brand label with FDA-approved carveouts. In many states, automatic generic substitution laws further channel skinny-label generics into prescriptions for the patented indication regardless of any generic conduct.

Multiple other manufacturers (per DrugPatentWatch, at least seven and as many as ten depending on commercial-launch status) sell generic icosapent ethyl with materially identical skinny labels and have not been sued by Amarin.

2. The Question Presented and the Cox Backdrop

Hikma's question presented frames the issue cleanly: when a generic drug label fully carves out a patented use, are allegations that the generic drugmaker calls its product a "generic version" and cites public information about the drug (e.g., sales) enough to plead induced infringement of the patented use, where the complaint does not allege any instruction or other statement encouraging or even mentioning the patented use?

The most consequential pre-argument legal context was Cox Communications, Inc. v. Sony Music Entertainment, 607 U.S. ___ (March 25, 2026). Justice Thomas wrote for the Court (joined by Roberts, Alito, Kagan, Gorsuch, Kavanaugh, and Barrett); Justice Sotomayor concurred only in the judgment, joined by Justice Jackson, expressly disagreeing with the majority's two-prong framing.

The operative holding: secondary liability requires either inducement (active steps to encourage infringement) or tailoring (a service "not capable of substantial or commercially significant non-infringing uses"), drawing analogies to 35 U.S.C. § 271(b) and § 271(c) respectively. The operative Cox formulation, drawn from Grokster, is that liability requires "an affirmative intent that the product be used to infringe."

Dennis Crouch's pre-argument analysis at PatentlyO framed the doctrinal question precisely and predicted the Court would not be able to ignore Cox: "There are many parallels between Cox and Hikma, and the patentee (Amarin) will need to distinguish the two in order to win." The Solicitor General had supported the accused infringers in both cases.

The big-firm previews from Finnegan, Crowell & Moring, and Morrison Foerster all leaned directionally toward reversal on the strength of the Cox template.

That was the pre-argument frame. What actually happened at the bench yesterday was different in important ways.

3. What the April 29 Argument Revealed

The oral argument transcript (subject to final review at time of writing) and the first wave of analytical recaps from IPWatchdog, National Law Review, Citeline's Pink Sheet, and Generics Bulletin converge on a picture that differs from the pre-argument consensus in three respects.

First, Cox barely surfaced. The bench questioning did not center on the secondary-liability template that the legal commentariat had expected to dominate. The Justices framed the case as a Hatch-Waxman policy dispute and a Twombly/Iqbal pleading-standard dispute, not a § 271(b) doctrinal reformulation case. Crouch's central pre-argument analytical bet, that Amarin would struggle to distinguish Cox, was not the lever pulled at the bench.

Second, multiple Justices questioned why cert was granted. Per the National Law Review recap, "Justice Coney Barrett asked whether this case is really just about the plausibility standards set out in the Twombly and Iqbal cases. She and at least one other Justice questioned why cert. was even granted in the case." That is a meaningful tell. It raises the probability of a narrow Twombly-grounded reversal or, in the limit, a dismissal as improvidently granted, neither of which would meaningfully reshape § 271(b) doctrine.

Third, the bench skepticism cut against affirmance, not toward broad reversal. Justice Kavanaugh cited the amicus brief filed by former Congressman Henry Waxman (yes, the Waxman of Hatch-Waxman) directly from the bench, noting that the brief argued the Federal Circuit's decision "threatens to decimate the compromise at the heart of the Hatch-Waxman Act" and that generics have saved the United States $3.4 trillion over the past 10 years.

Kavanaugh added that he didn't "want to put too much faith in a former Congressman's brief about his own statute," but the citation alone signaled where his concern was directed: at affirmance, not at the Cox bridge. Justice Gorsuch also raised market-impact concerns along similar lines (pressing Huston on a Twombly antitrust analogy at transcript pp. 51–53).

The IPWatchdog recap headline captures the directional read: "Justices Voice Concern that Upholding CAFC's Hikma 'Skinny Label' Ruling Will Harm Generics Industry."

A few specific exchanges worth noting:

- Chief Justice Roberts challenged Deputy Solicitor General Malcolm Stewart on whether the government's "clearly reveal a purpose of infringement" standard amounted to "a pretty broad safe harbor." Stewart responded that "it is supposed to be a difficult standard for the pleader to satisfy, but I think that's for design. The Court has said when a product is capable of both infringing and non-infringing uses, it's important that a patent on one method of use not become a de facto monopoly on the product as a whole." Stewart held the position; Roberts did not press further. Justice Alito's questioning of Stewart focused on different hypotheticals later in the argument (a "Vascepa is approved to treat cardiovascular risks" hypo and an icosapent-ethyl studies hypo).

- Charles B. Klein for Hikma conceded that the Court would not need to change existing inducement standards for Hikma to prevail, framing Hikma's statements as so "anodyne" (a term Klein attributed to the government's brief) that no doctrinal reformulation was required. Justices Thomas and Sotomayor both pressed on this, suggesting they were not entirely persuaded that the conduct cleared the existing bar.

- Michael Huston for Amarin anchored on the $300M Reduce-It trial investment, arguing the Hatch-Waxman limitation on generic marketing is "the only thing that makes it economically rational for a branded company like Amarin" to invest in discovering new indications for existing drugs. The Justices appeared skeptical that Hikma's specific statements were directed at physicians (versus investors), but Huston argued plausibly that this is a fact question for discovery. Huston's fallback position, urging remand rather than dismissal, may turn out to be the median outcome.

- The parties and the SG agreed that no new pharmaceutical-specific rule was required. That convergence shapes what the opinion is likely to say. The Court is not being invited to write new patent-inducement doctrine; it is being invited to apply existing doctrine more carefully to skinny-label facts.

The honest read is that the argument did not produce a clear directional signal on the merits. Citeline's Pink Sheet headline ("Could Generics Maintain Carve-Out Authority No Matter The Decision?") captures something important: the practical generic-side outcome on the carve-out pathway may turn out to be insulated from the formal doctrinal ruling.

If the Court rules narrowly on Twombly/Iqbal grounds without disturbing § 271(b), generics that conduct themselves cleanly will continue to launch under section viii, and brand owners that can plead specific affirmative acts will still have a litigation lever.

For the royalty-fund audience, the practical implication is that the most aggressive scenarios on either end of the spectrum are now less likely than they appeared a week ago.

4. The Revised Outcome Space

The pre-argument three-scenario framework needs revision in light of the bench signal. Here is the updated decision space:

Figure 2: How the April 29 oral argument shifted the decision space versus pre-argument consensus. Modal outcome is now B1 (narrow Twombly/Iqbal reversal) at ~45 percent.

| Scenario | Definition | Direction | Post-argument likelihood |

|---|---|---|---|

| A. Affirmance | Federal Circuit "totality" preserved; Amarin complaint proceeds | Brand-favorable. Pleading-stage robustness preserved on MOU patents. | Lower than pre-argument. Kavanaugh and Gorsuch's Hatch-Waxman policy concerns cut against affirmance. |

| B1. Narrow reversal on Twombly/Iqbal grounds | Reverse on Amarin facts only; the specific allegations do not satisfy plausibility; § 271(b) doctrine untouched | Generic-favorable on facts; GSK v. Teva preserved as precedent. Modest impact on MOU enforcement going forward. | Now the median expected outcome. Barrett's framing pushes here. |

| B2. Reversal with remand for amendment | Court agrees current complaint insufficient but permits amendment with the additional facts Amarin says discovery has produced | Mixed. Amarin lives to fight another day. Royalty-fund cash flows minimally disturbed. | Live secondary outcome. Huston positioned for this. |

| C. Broad reversal | § 271(b) reformulated to require specific affirmative act pointing to patented use, with causation | Strongly generic-favorable. MOU patents on later indications become near-uncollectible against carved-out generics. | Lower than pre-argument. The bench did not embrace the SG's expansive label-irrelevance position. |

| D. DIG (improvidently granted) | Court dismisses without reaching merits | Federal Circuit decision stands; same NAV impact as Scenario A. | Possible but unlikely after full briefing and divided argument. Barrett floated the question; the Court rarely follows through. |

The aggregate read post-argument: the modal outcome is now a narrow ruling (B1 or B2) that disposes of the case on pleading-standard grounds without a doctrinal earthquake.

Scenarios A and C, which would generate the largest royalty NAV swings in either direction, are both less likely than they appeared a week ago. The cash-flow asymmetry on most counterparty exposures has compressed.

5. What the Doctrine Actually Controls

Before reaching the vehicle-by-vehicle analysis, two clarifications are useful.

At stake. The pleading standard for induced infringement under § 271(b) as applied to skinny-label facts. In a narrow ruling, this still matters, because it sets the litigation-cost floor for brand-side enforcement. A high pleading bar deters brand suits and protects skinny-label launches; a low bar preserves brand leverage in settlement negotiations.

Not at stake. The validity or scope of the underlying CV method-of-use patents. The right to file under section viii. The Hatch-Waxman framework as a whole. State automatic-substitution laws. Direct infringement liability against prescribers.

Most importantly: any ruling here applies to all § 271(b) cases, not just pharmaceutical ones, but the bench made clear it is not looking to write new general doctrine.

The practical implication is subtle. A narrow ruling on Twombly/Iqbal grounds does not formally narrow MOU enforcement; it raises the litigation-cost barrier brand owners face. That barrier still has value to royalty-fund counterparties, because most royalty NAV depends on the deterrent effect of enforceability rather than on actual enforcement.

A skinny-label generic that knows it can be plausibly sued at the pleading stage is more likely to launch with cleaner conduct, which protects the patented use de facto even if it does not formally bar entry. This is the "label-plus" residual that Crouch flagged in his pre-argument writing and that the Court appears unlikely to disturb.

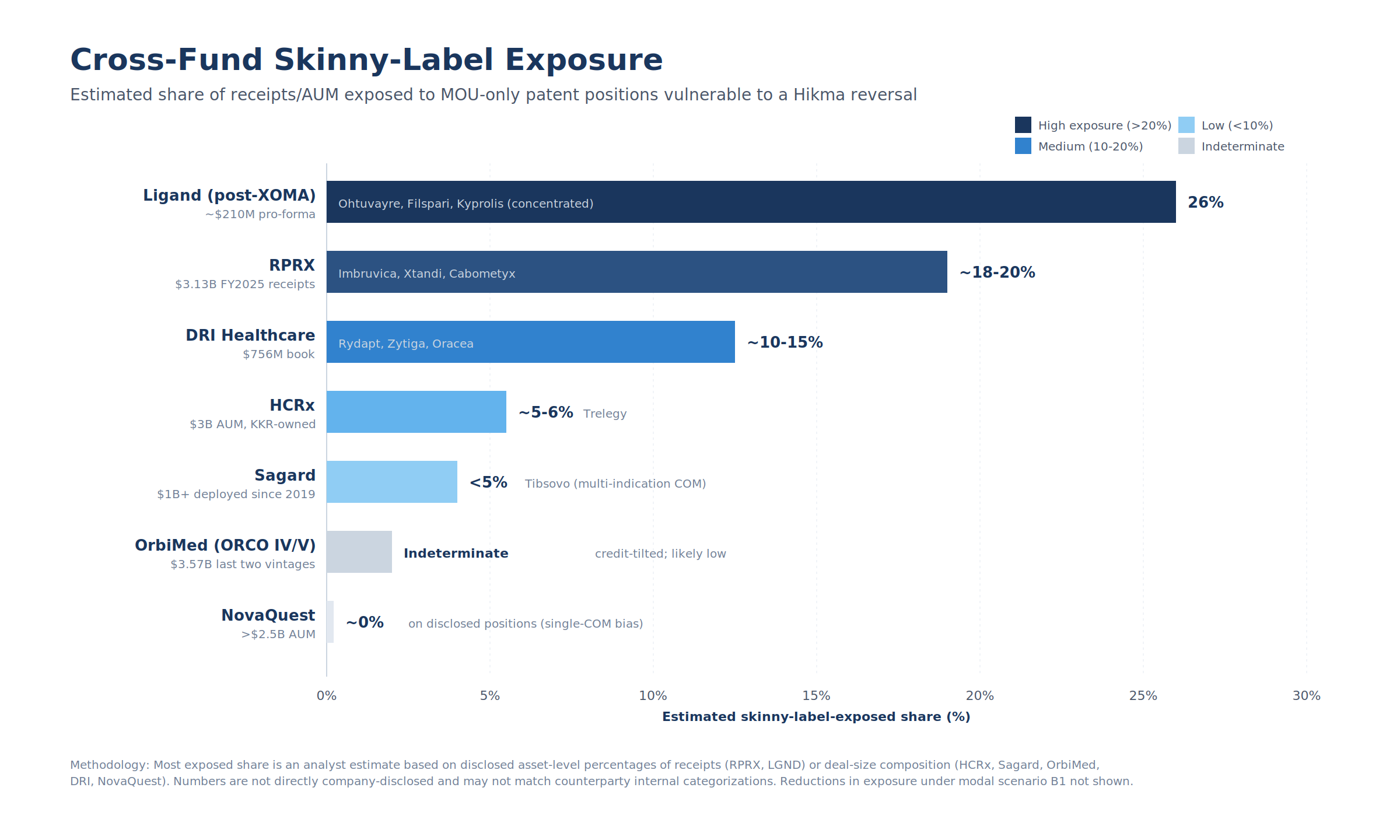

6. Royalty Vehicle Stress Test: Pre-Decision Hedge Book

What follows is a Red Team / Blue Team reading of the listed and major private royalty vehicles, framed first as a pre-decision hedge book and then as a post-decision repricing matrix (Section 7). Time horizon throughout: through 2035. The compression of outcome space described above means most NAV impact estimates have been moderated relative to a pre-argument reading.

Figure 3: Estimated share of receipts/AUM exposed to MOU-only patent positions vulnerable to a Hikma reversal. Ligand post-XOMA carries the highest concentration; Sagard, NovaQuest, and OrbiMed are structurally insulated.

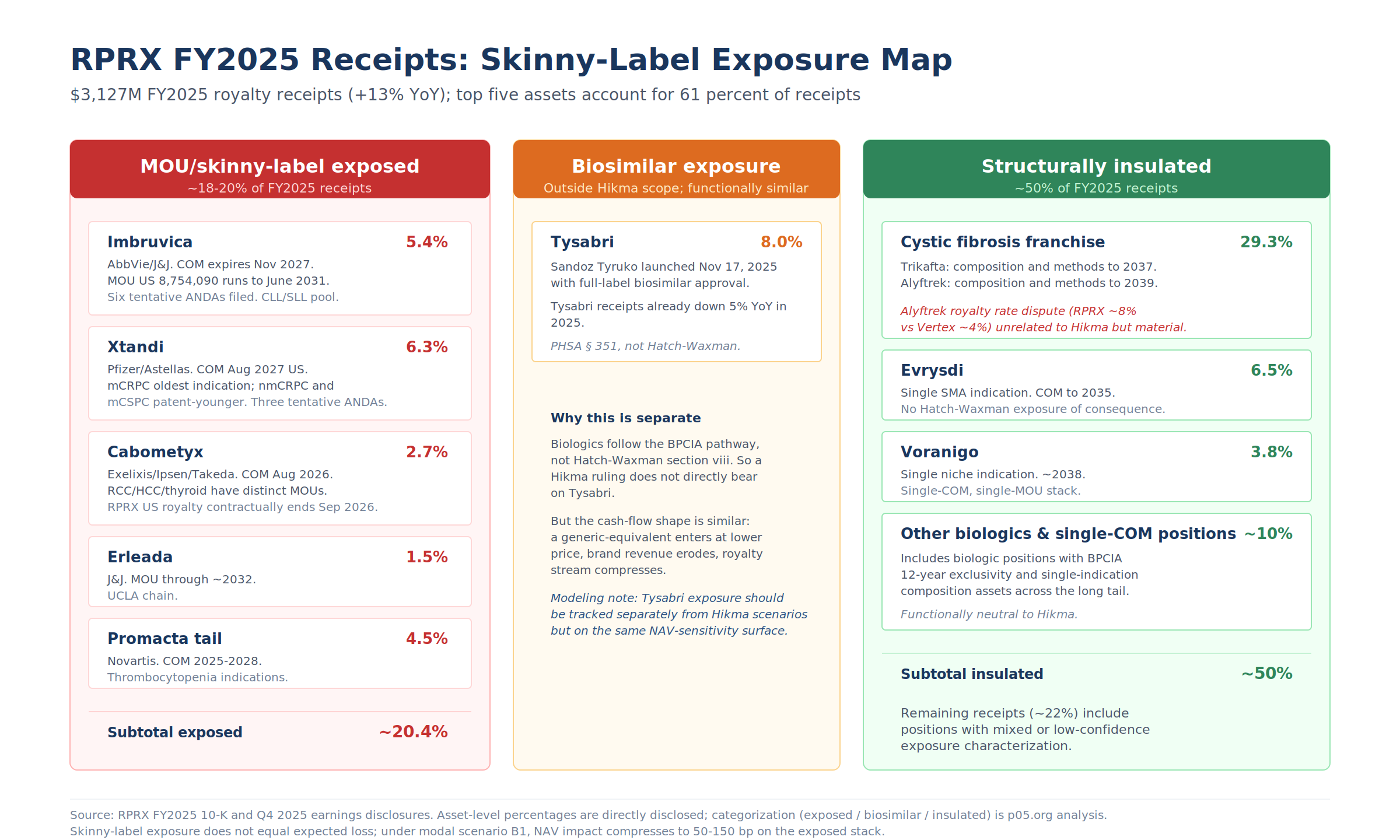

6.1 Royalty Pharma (NASDAQ: RPRX)

FY2025 royalty receipts of $3,127M (+13% YoY) place RPRX as the price-setter for the listed-royalty universe. The top five assets account for 61 percent of receipts. The skinny-label exposure is concentrated, not distributed.

Figure 4: $3,127M FY2025 royalty receipts mapped by exposure category. Three categories: MOU/skinny-label exposed (~18-20%), biosimilar-exposed (Tysabri, ~8%, outside Hikma scope but functionally similar), and structurally insulated (~50%, dominated by the cystic fibrosis franchise).

Material method-of-use exposure (~18-20 percent of FY2025 receipts). In rough order of vulnerability:

- Imbruvica (5.4 percent of receipts; AbbVie/J&J): composition-of-matter expires November 2027; method-of-use US 8,754,090 runs to June 2031. Six tentative ANDAs already filed. CLL/SLL is the principal commercial pool. RPRX duration estimate of "2027–2032" could collapse toward 2027 under a broad reversal but is more likely to hold under the modal narrow-ruling outcome.

- Xtandi (6.3 percent; Pfizer/Astellas): composition expires August 2027 US, 2026 EU/JP. mCRPC is the oldest, most-vulnerable indication; nmCRPC and mCSPC are patent-younger. Three tentative ANDAs.

- Cabometyx (2.7 percent; Exelixis/Ipsen/Takeda): composition (US 7,579,473) expires August 2026; Delaware 2025 ruling and Cipla settlement push entry to ~2030/2031. RCC, HCC, and thyroid carry distinct method-of-use patents. The RPRX US royalty contractually ends September 2026 regardless.

- Erleada (1.5 percent; J&J): MOU through ~2032. UCLA chain.

- Promacta tail (4.5 percent; Novartis): composition 2025–2028; thrombocytopenia indications.

Material biosimilar exposure, separately. Tysabri (8.0 percent of receipts) faces Sandoz Tyruko, which launched November 17, 2025 with full-label biosimilar approval. Tysabri receipts were already down 5 percent YoY in 2025. This is outside the Hikma doctrinal scope but functionally similar in cash-flow terms.

Structurally insulated (~50 percent of receipts). The cystic fibrosis franchise (29.3 percent, with composition and methods running to 2037 for Trikafta and 2039 for Alyftrek), Evrysdi (6.5 percent, single SMA indication, COM to 2035), Voranigo (3.8 percent, single niche indication, ~2038), and the biologic positions are essentially neutral to Hikma.

One sleeper risk worth flagging. The Alyftrek royalty rate dispute between RPRX (claiming ~8 percent blended on the basis that deutivacaftor is royalty-bearing) and Vertex (paying ~4 percent, treating deutivacaftor as non-royalty-bearing) is a contractual matter unrelated to Hikma but material to NAV in its own right.

RPRX commenced contractual dispute resolution per the Q4 2025 communication. Authors and analysts modeling Hikma sensitivity should not conflate the two.

Pre-decision posture for RPRX equity: long with put-spread overlay through July 2026 expiry, optionally paired with calls on the Indian generic basket (Sun, Lupin, Dr Reddy's) for asymmetry. The narrowed outcome space reduces the value of large directional hedges.

Management commentary on the May 6, 2026 Q1 call (post-argument, pre-decision) is worth pulling for tone on duration assumptions.

6.2 Ligand Pharmaceuticals (NASDAQ: LGND), pre and post XOMA close

LGND's FY2025 royalty receipts of $176.9M gross (+48 percent YoY) and the April 27, 2026 announcement of the XOMA acquisition (~$739M equity, $39 per share, expected Q3 2026 close) recast the second-largest listed royalty vehicle in a single move.

The combined book carries more than 200 royalty assets. Pro-forma TTM royalty income approximates $210M before synergies (LGND's standalone 2026 royalty revenue guidance is $225-250M). Asset-level percentages cited below are estimates derived from LGND disclosures and analyst breakdowns rather than directly company-reported splits.

Most exposed assets.

- Ohtuvayre (8.4 percent of LGND receipts, rapidly growing; Verona, now Merck post the October 2025 acquisition): the original ensifentrine composition patent already expired in 2020. The product depends on an NCE-1 layer through June 2028 (5-year NCE following June 26, 2024 approval, less the one-year paragraph IV ANDA window), polymorph patent '047 to 2031 (with PTE potentially to 2036), and method-of-use claims extending into the late 2030s/early 2040s. A single primary indication today (COPD) with non-CF bronchiectasis in Phase 2. Merck's $10B Verona acquisition is, in part, a wager on polymorph-and-MOU enforceability against carved-out generic ensifentrine. Hikma outcomes touch this directly.

- Filspari (18.1 percent; Travere with CSL Vifor and Chugai): NCE-1 through February 2027. Estimated generic launch September 2031. Only one Orange Book patent listed (a thin thicket). With FSGS approval added April 13, 2026 alongside IgAN, the indication-bifurcation pattern that Hikma concerns becomes potentially relevant.

- Kyprolis (20.1 percent, the single largest LGND position; Amgen/Ono/BeOne): US composition expires December 7, 2027 following the 2020 Cipla loss. Captisol formulation patents extend the patent thicket meaningfully past the COM cliff, with method-of-making coverage running into the early 2040s plus a contractual royalty tail. This is the critical mitigant: Kyprolis is exposed at the COM cliff but the formulation moat is genuine.

Least exposed. Capvaxive (5.7 percent), Rylaze (7.5 percent), and Vaxneuvance (4.2 percent) are all biologics or vaccines with 12-year BPCIA exclusivity and structurally insulated from skinny-label dynamics.

XOMA addition. XOMA's largest publicly disclosed asset is the Vabysmo royalty (0.5 percent of net sales for ten years from first commercial sale per jurisdiction, expiring approximately January 2032). This is a contractual cap that binds before any patent expiry, so Hikma is functionally irrelevant to it. The CVR component of the LGND-XOMA deal, tied to XOMA's Tremfya litigation against Janssen, is the asymmetric instrument worth holding through the Q3 2026 close.

Pre-decision posture for LGND equity: long with hedges concentrated on Ohtuvayre (Merck puts) and Filspari, with Capvaxive/Rylaze/Vaxneuvance as ballast. The XOMA close is a separate transaction risk.

6.3 XOMA Royalty (NASDAQ: XOMA), pre-close

The pre-close XOMA position is largely about the LGND buyout price ($39 per share) and the Tremfya CVR. Hikma is not material to XOMA pre-close because Vabysmo (the largest contributor) is a biologic with a contractual cap binding before patent expiry.

6.4 Healthcare Royalty Partners (HCRx)

HCRx is private, with KKR taking majority ownership in July 2025. The portfolio includes more than $7B deployed across 110+ products since 2006, with current AUM around $3B. The skinny-label exposure as a share of deal size is approximately 5 to 6 percent.

Most exposed position: the $200M Trelegy Ellipta Royalty Notes (originated March 2020 from Theravance), thematically the closest analog to GSK v. Teva given that both Trelegy and the Coreg carvedilol asset trace to the same therapeutic family. Movantik, Relistor, and the Mycapssa positions carry mid-tier MOU exposure.

Least exposed: the QS-21/Shingrix royalty ($230M, January 2018 from Agenus), which is a vaccine adjuvant license with no skinny-label vector available. Vaccines do not follow Hatch-Waxman; PHSA § 351(a) applies, and there is no biosimilar shingles vaccine in the US.

KKR, as majority owner since July 2025, now wears the policy risk on Trelegy. There is no listed instrument for direct hedging of HCRx exposure.

6.5 Sagard Healthcare Royalty Partners

Sagard is structurally the most insulated of the private funds covered. The $1B+ deployed since January 2019 has emphasized biologics (Jemperli, ZYNYZ, Hemgenix), single-indication composition assets (Tibsovo, Voquezna, taletrectinib), and formulation/device positions (Tyvaso DPI).

The Jemperli royalty (originated October 2021 with AnaptysBio for $250M upfront plus a $50M 2024 amendment, total cap approximately $600M) is a biologic with US composition to 2035 and EU to 2036. None of the disclosed Sagard positions has meaningful skinny-label exposure.

The dominant Sagard risk vector is the AnaptysBio-Tesaro/GSK Delaware Chancery dispute over alleged exclusivity breach (KEYNOTE trials with Keytruda) and CRE failure. Trial is set for July 2026, with a pre-trial blow to Tesaro reported April 2026.

This is a contractual matter, not a Hikma matter, but it sits on the same sensitivity surface for the Jemperli stream's terminal value. The composition of the Sagard book is consistent with European/Canadian capital base preferences (Power Corp of Canada parent).

6.6 NovaQuest Capital Management

NovaQuest's $2.5B+ AUM is heavily weighted toward Phase III at-risk development funding and royalty monetization on single-COM assets (EVRENZO/roxadustat, Rozlytrek/entrectinib, RTX/resiniferatoxin in Grünenthal's Phase III osteoarthritis pain program). None of the disclosed positions has material skinny-label exposure.

6.7 DRI Healthcare Trust (TSX: DHT.UN)

DRI is, perhaps surprisingly, the most directly Hikma-exposed of the listed and quasi-listed peers. The Q3 2025 disclosure (28 royalty streams on 21 products, total cash receipts $43.6M, royalty book $756.4M intangible plus $55.4M financial) supports an analyst-derived portfolio composition of approximately 50–55 percent biologics (no skinny-label exposure), 35–40 percent COM small molecules, and 10–15 percent MOU/formulation-vulnerable positions. DRI itself does not publish this categorization.

Most exposed assets in the DRI book.

- Rydapt (midostaurin, Novartis): multi-indication MOU asset with AML versus systemic mastocytosis carve-out potential.

- Zytiga (abiraterone, J&J): COM already expired; the active patent layer is the Zytiga + prednisone combination MOU.

- Oracea (subantimicrobial doxycycline, Galderma): a textbook formulation/MOU position with multiple ANDAs filed.

- Omidria (Rayner Surgical): a formulation/combo position with mid-tier exposure.

Least exposed. The Casgevy royalty stream (Vertex/CRISPR Therapeutics, structured as a share of fixed Cas9 license fees acquired October 2024 for $57M and running through ~Q1 2034 rather than as a sales-linked royalty), the Eylea inventor royalty streams (contractually expiring Q1 2027 per the DRI Q3 2025 MD&A), Spinraza, Xolair, Empaveli/Syfovre, Vonjo, and the Ekterly and veligrotug additions are insulated.

6.8 OrbiMed Royalty & Credit Opportunities (ORCO IV / V)

The $3.57B deployed across the last two ORCO vintages is heavily tilted toward senior secured credit with warrants, rather than pure royalty monetization. Disclosed positions include AVITA Medical (Recell, device) and Poxel TWYMEEG (imeglimin).

The senior secured credit posture is asymmetric: a Hikma shock impacts collateral value and equity-like warrant upside rather than a clean royalty NAV. Material skinny-label exposure is indeterminate but probably low.

6.9 Cross-fund summary

| Fund | Capital base | Skinny-label-exposed share | Most exposed asset(s) |

|---|---|---|---|

| RPRX | $3.3B FY2025 receipts | ~18–20% of receipts | Imbruvica, Xtandi, Cabometyx |

| Ligand (post-XOMA) | ~$210M pro-forma royalty | ~26% (concentrated) | Ohtuvayre, Filspari |

| HCRx | ~$3B AUM, $7B+ deployed | ~5–6% by deal size | Trelegy |

| Sagard | $1B+ deployed since 2019 | <5% | Tibsovo (multi-indication COM) |

| NovaQuest | >$2.5B AUM | ~0% on disclosed | None publicly |

| DRI Healthcare | $756M book, $43.6M Q3 2025 receipts | ~10–15% of cash receipts | Rydapt, Zytiga, Oracea |

| OrbiMed | $3.57B last two vintages | Indeterminate; likely low | n/d |

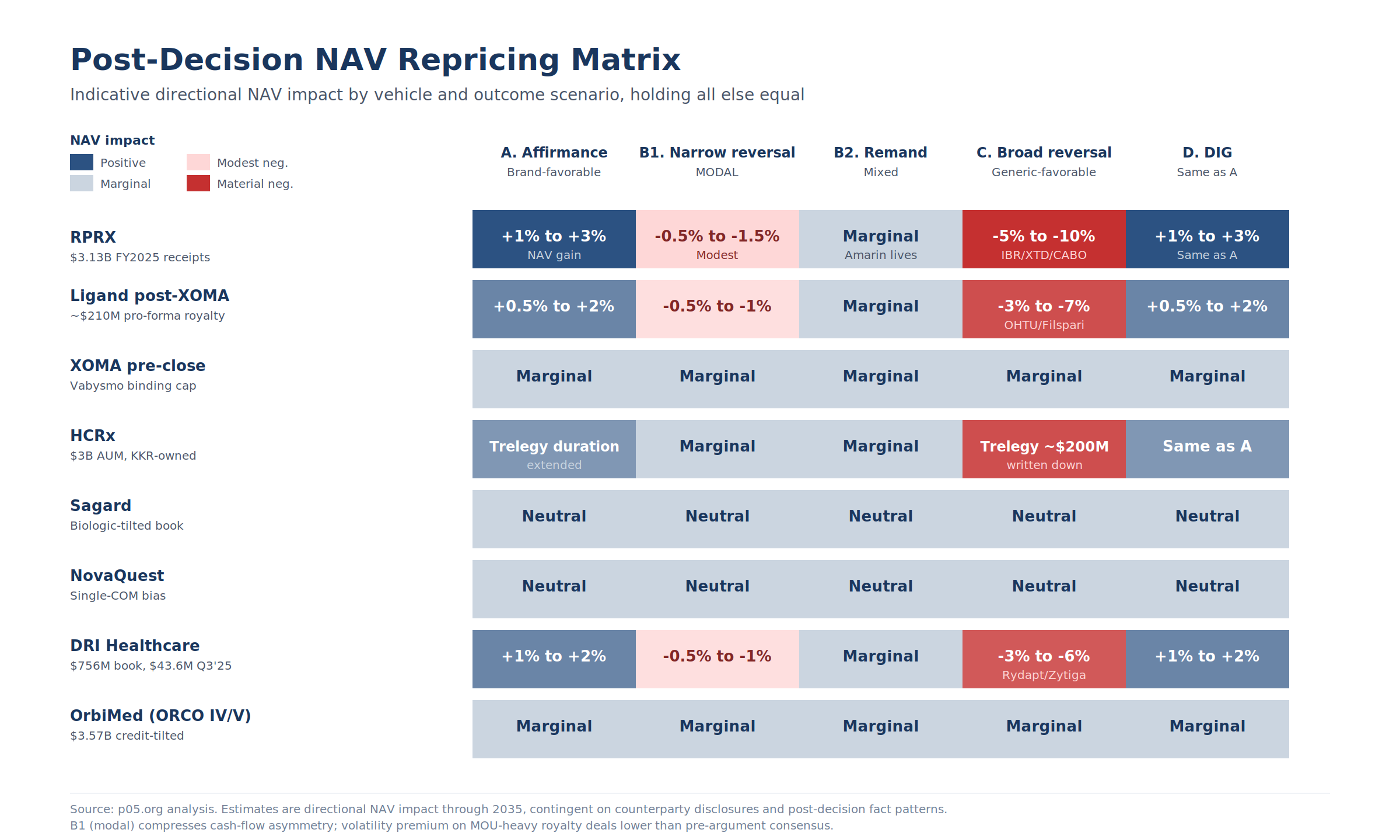

7. Post-Decision Repricing Matrix

The directional NAV impact of each scenario, holding all else equal. The post-argument compression of outcome space means the modal scenario (B1, narrow Twombly/Iqbal reversal) carries materially smaller NAV impact than either A or C.

Figure 5: Indicative directional NAV impact by vehicle and outcome scenario through 2035. Sagard, NovaQuest, XOMA pre-close, and OrbiMed sit on a flat line across all scenarios; RPRX, Ligand, HCRx, and DRI carry the asymmetric exposure.

| Vehicle | A. Affirmance | B1. Narrow Twombly reversal (modal) | B2. Reversal with remand | C. Broad reversal | D. DIG |

|---|---|---|---|---|---|

| RPRX | +1% to +3% NAV | -0.5% to -1.5% (modest) | Marginal (Amarin lives) | -5% to -10%, concentrated in Imbruvica, Xtandi, Cabometyx | Same as A |

| Ligand post-close | +0.5% to +2% | -0.5% to -1% | Marginal | -3% to -7%, concentrated in Ohtuvayre/Filspari | Same as A |

| XOMA pre-close | Marginal | Marginal | Marginal | Marginal | Marginal |

| HCRx | Trelegy duration extended | Marginal | Marginal | Trelegy duration compressed; ~$200M position written down | Same as A |

| Sagard | Neutral | Neutral | Neutral | Neutral | Neutral |

| NovaQuest | Neutral | Neutral | Neutral | Neutral | Neutral |

| DRI | +1% to +2% | -0.5% to -1% | Marginal | -3% to -6%, concentrated in Rydapt, Zytiga, Oracea | Same as A |

| OrbiMed | Marginal | Marginal | Marginal | Marginal | Marginal |

The bench-question signal compresses the expected-value impact across the listed-fund universe.

If B1 is the modal outcome, RPRX takes a 50 to 150 basis-point NAV hit on its Imbruvica/Xtandi/Cabometyx stack, not the 500 to 1,000 basis-point hit a broad reversal would generate. LGND's Ohtuvayre/Filspari concentration sees a similar compression.

The asymmetric upside for funds in Scenario A is also smaller than the asymmetric downside in Scenario C, so the volatility premium that should be priced into MOU-heavy royalty deals over the next two months is now lower than it was a week ago.

Indicative cash-flow magnitudes through 2035: under the modal B1 scenario, RPRX cumulative cashflow loss versus base case falls in the $50M to $150M range, not the $400M to $700M range that a broad reversal (Scenario C) would produce. For LGND post-XOMA close, the corresponding range is $10M to $30M under B1 versus $50M to $100M under C. For HCRx, B1 leaves the Trelegy position essentially intact; C drives a ~$60M cumulative cashflow loss against base case.

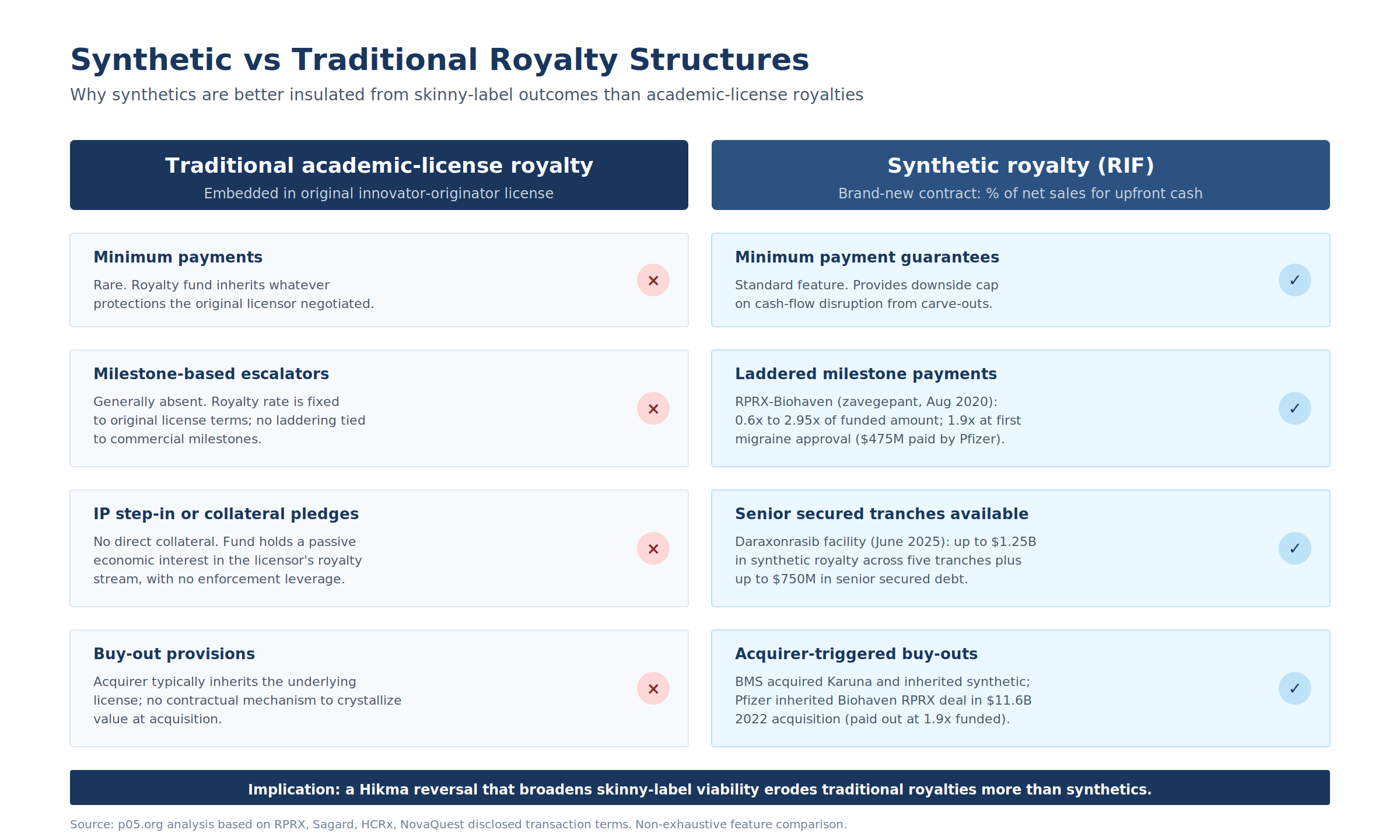

8. The Synthetic vs. Traditional Royalty Differential

A subtle but important structural observation rarely surfaced in Hikma commentary: synthetic royalties (revenue interest financings, RIFs) are systematically better insulated from skinny-label outcomes than traditional academic-license royalties.

Figure 6: Why synthetics are better insulated. Traditional royalties inherit whatever protections the original licensor negotiated; synthetics are negotiated fresh with minimum payments, milestone escalators, collateral pledges, and buy-out provisions.

Traditional royalties are embedded in the original innovator-originator license. The royalty fund inherits whatever protections the original licensor negotiated, often without minimum payments and without IP step-in rights.

Synthetic royalties are brand-new contracts between commercial-stage companies and capital providers, structured as the sale of a percentage of top-line net sales for upfront cash. The provider does not take a license to the IP, but typically negotiates four protective layers:

- Minimum payment guarantees, rare in traditional structures.

- Milestone-based escalators, often laddered. The RPRX-Biohaven zavegepant August 2020 ladder ran from 0.6x to 2.95x of funded amount (1.9x at first migraine approval = $475M paid by Pfizer post the Biohaven acquisition in March 2023). The RPRX-PureTech KarXT deal of March 2023 ($100M upfront with up to $400M in milestones plus a 3 percent royalty) ran through PureTech Health, which held the underlying Karuna royalty.

- IP step-in or collateral pledges. The Daraxonrasib facility (June 24, 2025) is structured as up to $2B in total commitments, comprising up to $1.25B in synthetic royalty financing across five $250M tranches plus up to $750M in senior secured debt. The Zymeworks Ziihera March 2026 transaction ($250M as a non-recourse royalty-backed note) gives RPRX 30 percent of worldwide royalties.

- Buy-out provisions. BMS acquired Karuna and inherited the synthetic obligation; Pfizer inherited the Biohaven RPRX deal in the $11.6B 2022 acquisition.

The implication for Hikma: any reversal that broadens skinny-label viability would erode the terminal value of traditional academic-license royalties more than synthetics, because synthetics' minimums and buyout triggers cap downside.

Authors and analysts modeling Hikma should distinguish portfolio composition by structure as well as by therapeutic area. The compressed outcome space post-argument reduces the magnitude of this differential but not the direction.

A related observation worth flagging: Q1 2026 deal flow data suggests synthetic royalty origination is accelerating, with Royalty Pharma's January 11, 2026 Teva TEV-'408 deal (up to $500M for vitiligo) being notable as a major generic firm using synthetic capital.

The bid-ask spread on private royalty deals has likely tightened for COM-protected, single-indication, and biologic positions and likely widened for MOU-heavy or skinny-label-vulnerable positions, but no fund has publicly quantified this, and the post-argument compression of outcome space should narrow the wider end of that spread.

9. The Negative Space: GLP-1s, Aducanumab, and What Royalty Funds Don't Hold

It is worth noting what the Hikma outcome will not affect, because the absence reveals something about the structure of the royalty market itself.

The largest therapeutic-area cashflow opportunity of the decade, the GLP-1 class, is structurally unavailable to the disclosed royalty buyers. Semaglutide and tirzepatide are owned by vertically integrated originators (Novo and Lilly) with strong COM patent positions.

The original MGH/Mojsov-Habener liraglutide royalty ended around 2011 at first patent expiry and did not flow to semaglutide. There is no public RPRX, HCRx, or Sagard GLP-1 royalty position. Whatever the Hikma outcome, the GLP-1 cashflow does not pass through the listed-royalty universe.

Aducanumab royalty economics moved in the opposite direction often assumed: under the March 14, 2022 Biogen-Eisai amendment, Eisai stepped down from a profit-share into a tiered (2-8 percent) royalty effective January 1, 2023, before Biogen discontinued Aduhelm in January 2024.

Lecanemab (Leqembi) is held by Eisai/Biogen with BioArctic, which has not publicly monetized.

10. Three Things to Watch Between Now and the Decision

The Court is expected to issue its decision before the summer recess in late June or early July 2026. The argument transcript is available on supremecourt.gov; audio posts Friday end-of-week.

The Goodwin webinar with Wiesen, Santos, and Jay tomorrow (April 30) will be the first big-firm post-argument unpack; Crouch's PatentlyO recap should land in the next 24 to 48 hours.

Three things to watch in the eight to ten weeks before the opinion:

- The May 6, 2026 Royalty Pharma Q1 earnings call. Post-argument, pre-decision. Management is likely to be asked about MOU duration assumptions on Imbruvica/Xtandi/Cabometyx. The tone of the response (confident, hedged, or cautious) will be the first market-priced read on how the listed-fund universe is interpreting the bench signal.

- Anaptys-Tesaro/GSK trial in July 2026. Sagard's $250M-$600M Jemperli position depends on the contractual outcome here, separate from Hikma. The combination of a Hikma decision in early July and the Anaptys trial in mid-July creates a concentrated repricing window for any fund with both exposures.

- Q2 2026 royalty deal flow. If MOU-heavy assets become harder to price between argument and decision, the visible deal-flow composition should shift toward COM-protected and biologic positions. Watch Royalty Pharma's announced transactions and any new HCRx/Sagard/DRI activity for evidence.

The honest read is that yesterday's argument did not produce the Cox-driven doctrinal earthquake the legal commentariat predicted. The bench framed this as a Hatch-Waxman policy case and a Twombly/Iqbal pleading case, with multiple Justices openly questioning whether cert should have been granted at all.

The most likely outcome is now a narrow ruling that adjusts the pleading-standard floor without rewriting § 271(b). For royalty-fund counterparties, that compresses the cash-flow asymmetry on most exposed assets and reduces both the upside in Scenario A and the downside in Scenario C.

The decision, when it lands in early July, will still be one of the more useful natural experiments in pharmaceutical-royalty underwriting that this market has had in some years, but its magnitude is now likely to be smaller than the pre-argument consensus suggested.

This piece is part of an ongoing series at p05.org on the structural legal events shaping pharmaceutical royalty financing. Nothing in this article constitutes legal or investment advice. Royalty fund counterparty exposures discussed here are based on publicly available portfolio disclosures and regulatory filings and should be independently verified.