The Tax Architecture of Royalty Funds: How Jurisdiction Shopping Shapes Pharmaceutical Finance

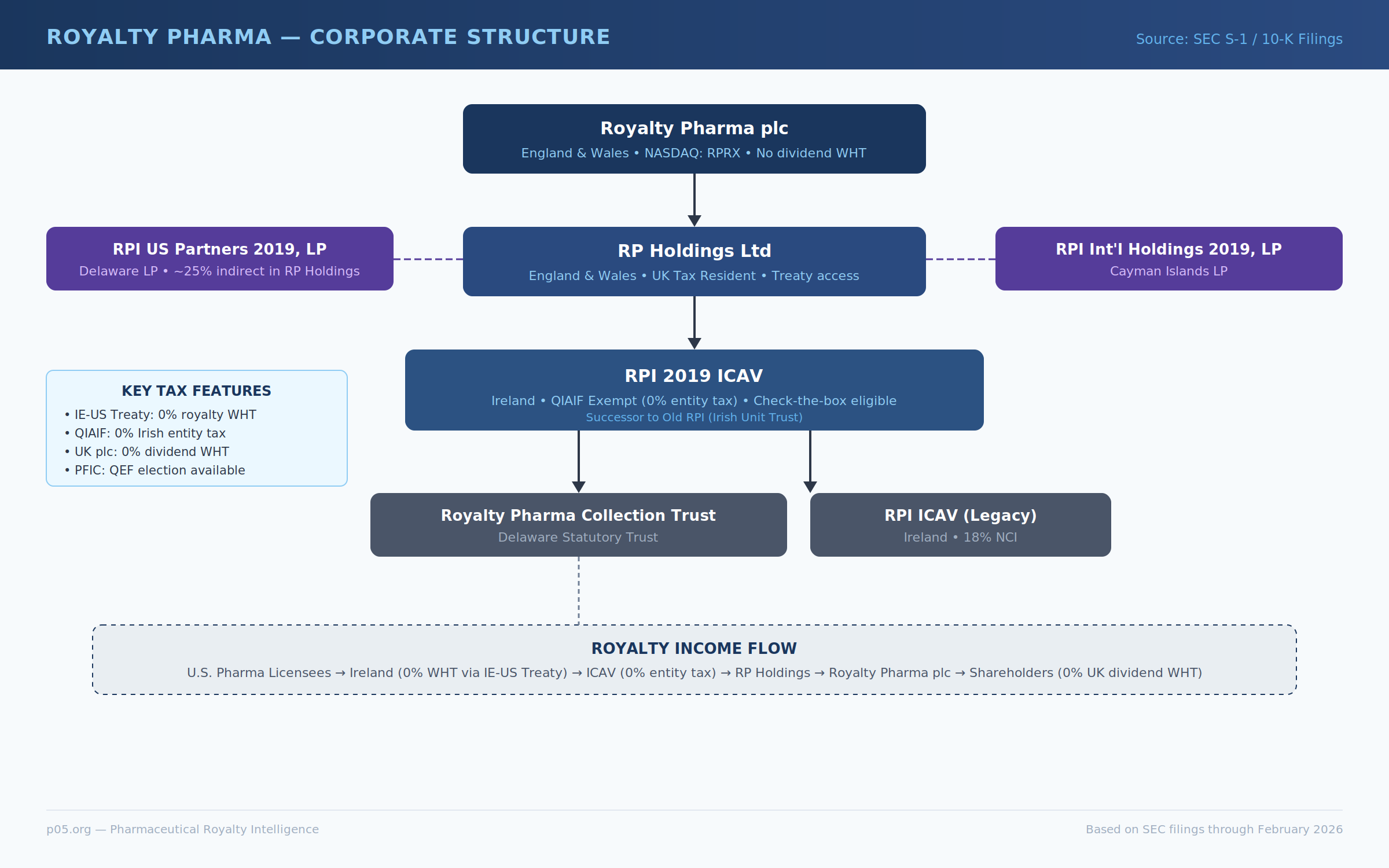

When Royalty Pharma filed its S-1 prospectus ahead of its 2020 IPO, the organizational chart told a story that no amount of financial modeling could fully capture. At the top sat Royalty Pharma plc, an English public limited company incorporated under the laws of England and Wales. Beneath it, Royalty Pharma Holdings Ltd, also English and UK tax resident. Below that, the entity that actually held the royalties: Royalty Pharma Investments 2019 ICAV, an Irish collective asset management vehicle. Off to the side, RPI US Partners 2019, LP, a Delaware limited partnership, and RPI International Holdings 2019, LP, a Cayman Islands exempted limited partnership. Feeding into the structure were Delaware statutory trusts, Irish unit trusts, and a collection trust.

This was not an accident. Every entity in that chain existed for a reason, and that reason was almost always tax.

The pharmaceutical royalty market has matured into a multi-billion-dollar asset class, but one dimension remains surprisingly underexamined: the fund-level tax architecture that determines how much of a royalty stream actually reaches investors. A 5% royalty on a blockbuster drug generating $10 billion in annual sales produces $500 million in gross receipts. Whether the fund retains $500 million, $425 million, or $375 million depends almost entirely on where and how the acquisition vehicle is domiciled, how royalty payments are characterized, and which treaty networks the fund can access.

For royalty financing experts, this is where competitive advantage lives.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or investment advice. The author is not a lawyer or financial adviser. All information presented here is derived from publicly available sources including SEC filings, court decisions, tax treaty texts, and regulatory guidance. Details of specific transactions and tax rules may have changed since publication. Readers should conduct their own due diligence and consult with qualified legal and financial professionals before making any investment or business decisions.

Why Fund Domicile Is a First-Order Investment Decision

In most asset classes, fund structure is an administrative detail. In pharmaceutical royalties, it is a primary determinant of returns.

The reason is mechanical. Pharmaceutical royalties are passive income streams paid across borders. A U.S. pharmaceutical company paying royalties to a fund domiciled in Ireland faces different withholding tax obligations than if that same fund were domiciled in the Cayman Islands, Luxembourg, or Delaware. The treaty network accessible to the fund vehicle determines the withholding rate at source. The fund's domestic tax treatment determines whether income is taxed again at the entity level. And the fund's characterization under the tax laws of its investors' home jurisdictions determines whether income is taxed a third time on distribution.

The potential for double or triple taxation on the same royalty dollar makes jurisdiction selection the single most consequential structural decision a royalty fund makes. As I discussed in my earlier analysis of cross-border pharmaceutical royalty transactions, treaty relief can reduce withholding from 30% to zero on qualifying payments. At fund scale, those basis points compound into hundreds of millions of dollars over a portfolio's life.

Royalty Pharma: The English-Irish Architecture

Royalty Pharma's structure is the industry's most visible case study in jurisdictional optimization, and its evolution across three decades illustrates how fund architecture responds to changing tax regimes.

The Pre-IPO Structure

Before going public in 2020, Royalty Pharma operated as a series of entities anchored by Royalty Pharma Investments, an Irish unit trust commonly known as "Old RPI." The choice of an Irish unit trust was deliberate. Ireland's Qualifying Investor Alternative Investment Fund (QIAIF) regime provides a range of tax-free legal wrappers, including the unit trust format, which are exempt from Irish income tax, capital gains tax, and corporation tax on their investment activities. The fund itself pays no entity-level tax.

Royalty payments flowing into the Irish unit trust from U.S. pharmaceutical companies benefited from the Ireland-U.S. tax treaty, which reduces withholding tax on royalties to 0%. The combination of zero withholding at source and zero entity-level tax in Ireland meant the full gross royalty payment reached the fund's investors, who then paid tax only in their home jurisdictions.

The structure also utilized RPI Finance Trust and the Royalty Pharma Collection Trust, both Delaware statutory trusts. Delaware statutory trusts offer remarkable flexibility under the check-the-box regulations: a DST can elect to be treated as a grantor trust, partnership, or corporation for federal tax purposes, depending on the needs of the structure. For non-resident alien beneficiaries of self-settled trusts, no U.S. income tax or filing obligations arise at the trust level.

The IPO Reorganization

The 2020 IPO required a fundamental restructuring. Royalty Pharma plc was incorporated in England and Wales to serve as the publicly listed parent, while a new entity, Royalty Pharma Investments 2019 ICAV, replaced the old Irish unit trust as the primary royalty-holding vehicle.

The shift from an Irish unit trust to an Irish Collective Asset-management Vehicle (ICAV) was significant. The ICAV, introduced by Ireland in 2015, was designed specifically to attract fund domiciliation from traditional offshore jurisdictions. Its critical advantage for U.S. investors is the ability to make a "check-the-box" election for U.S. tax purposes, something an Irish public limited company cannot do. This election allows the ICAV to be treated as a partnership or disregarded entity for U.S. federal tax purposes, avoiding the Passive Foreign Investment Company (PFIC) regime that would otherwise impose punitive taxation on U.S. shareholders.

Royalty Pharma's tax information page confirms that the company is treated as a PFIC for U.S. federal income tax purposes, and provides annual PFIC Information Statements enabling shareholders to make Qualified Electing Fund (QEF) elections. This illustrates a persistent structural tension: the English plc parent cannot check the box, so U.S. shareholders must navigate PFIC compliance even though the underlying Irish vehicle was designed to avoid precisely this problem.

Why England and Wales?

The choice of an English plc for the public listing entity rather than a U.S. corporation deserves scrutiny. England and Wales impose no withholding tax on dividends paid to non-residents, which means distributions from Royalty Pharma plc to its global shareholder base flow without source-country withholding. A U.S. C-corporation paying dividends to foreign shareholders would face withholding obligations under various treaties, typically ranging from 5% to 30%.

Equally important, RP Holdings, the English private limited company sitting between the plc and the Irish ICAV, is described in SEC filings as "U.K. tax resident." The UK's extensive treaty network provides additional flexibility for routing royalty income from jurisdictions where the Ireland-source treaty might be less favorable, or where the UK treaty provides more robust protection against withholding.

The layered structure, English plc over English private limited company over Irish ICAV over Delaware trusts and Cayman partnerships, creates multiple treaty access points. Each layer can potentially claim benefits under a different bilateral treaty depending on where a specific royalty originates.

The 2025 Internalization

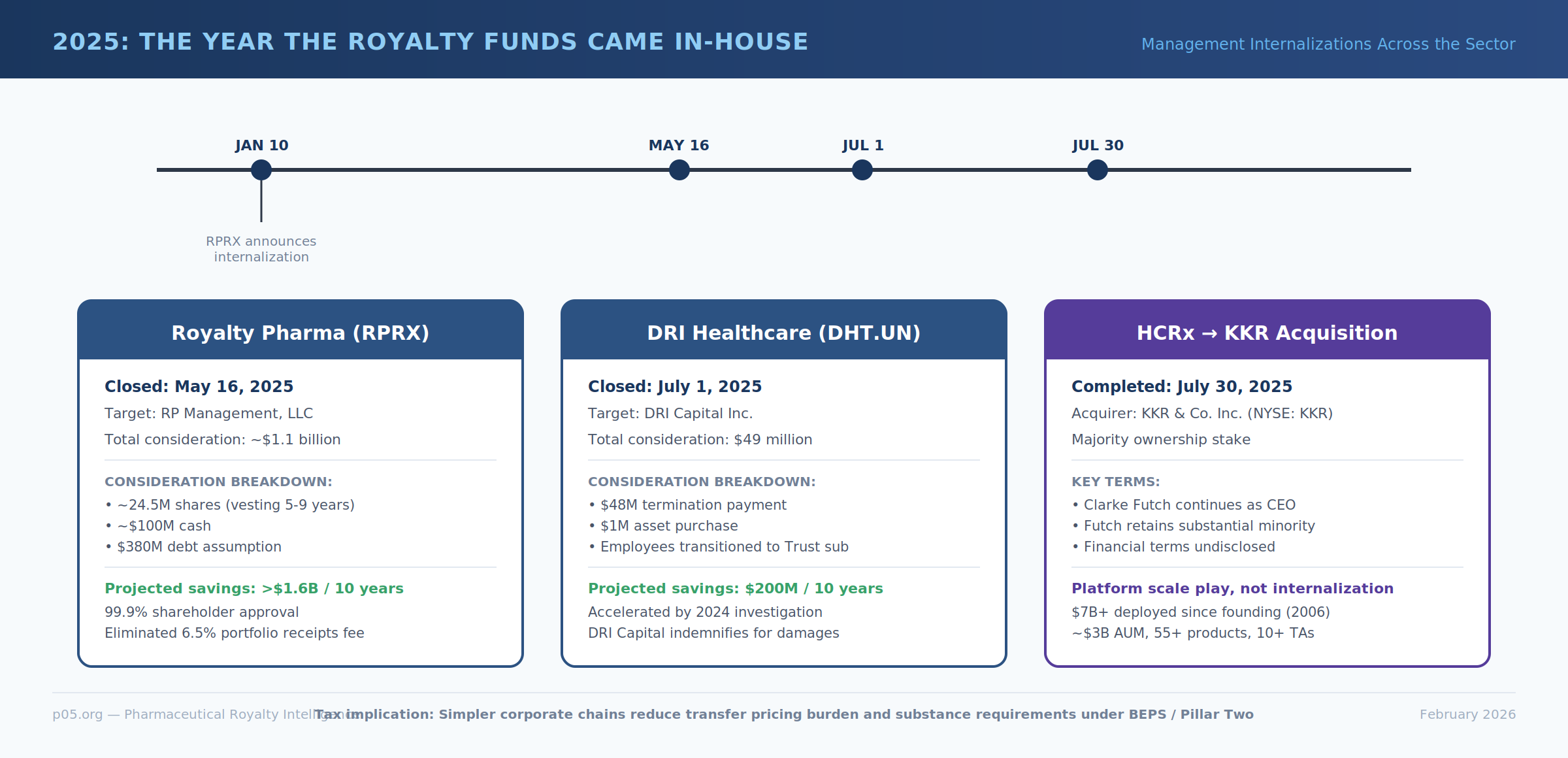

In January 2025, Royalty Pharma announced it would acquire its external manager, RP Management, LLC, for approximately $1.1 billion in total consideration: ~24.5 million shares of Royalty Pharma equity vesting over 5 to 9 years, ~$100 million in cash, and assumption of $380 million in Manager debt. The transaction closed on May 16, 2025 with 99.9% shareholder approval.

This is significant from a tax structuring perspective because RP Management had been a Delaware LLC sitting outside the corporate structure. Management fees (6.5% of quarterly portfolio receipts) flowed from the Irish ICAV up through RP Holdings to Royalty Pharma plc and then out to the Manager as a deductible expense. Post-internalization, all employees work directly for Royalty Pharma, the management fee has been extinguished, and the simplified structure reduces the number of intercompany payments that would otherwise need to satisfy transfer pricing and substance requirements. The company projects cumulative cash savings exceeding $1.6 billion over ten years from eliminating the external fee arrangement, with operating costs as a percentage of portfolio receipts declining meaningfully from 2026 onward.

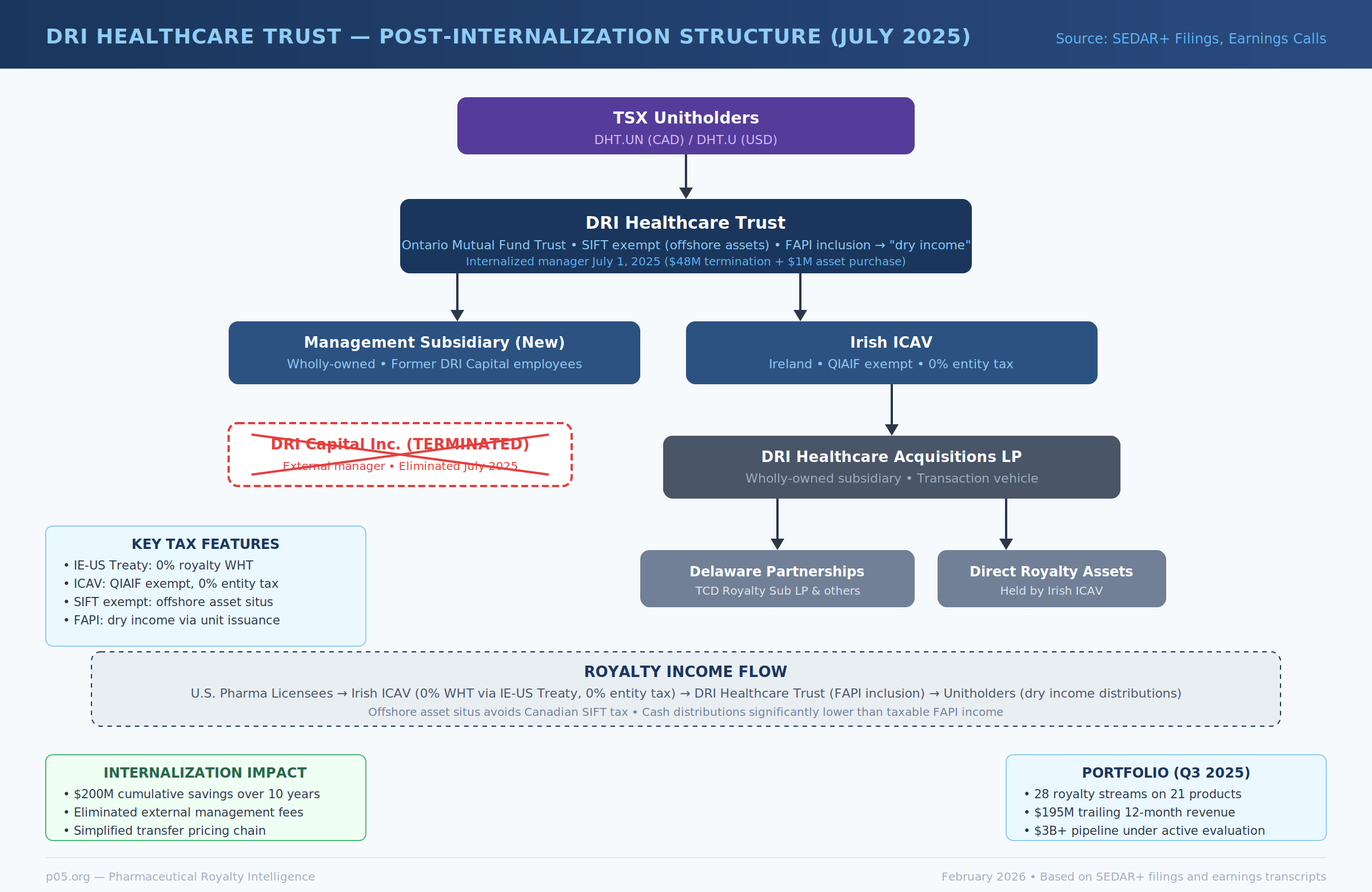

DRI Healthcare Trust: The Canadian-Irish Hybrid

DRI Healthcare Trust, listed on the Toronto Stock Exchange (TSX: DHT.UN), takes a different approach that exploits the intersection of Canadian trust law, Irish corporate tax rules, and the Ireland-U.S. tax treaty. Its 2025 internalization of DRI Capital makes this an opportune moment to examine the structure in its current form.

As described in its IPO prospectus analysis, DRI established a wholly-owned Irish subsidiary to acquire pharmaceutical royalties either directly or through purchasing the LP units and general partner interests of Delaware partnerships holding such royalties. Notably, DRI's Q1 2025 earnings call confirmed that the royalty IP sits below the Trust in an Irish ICAV and other sub-entities, making it structurally parallel to Royalty Pharma's choice of the ICAV format. The acquisition vehicle for new transactions is DRI Healthcare Acquisitions LP, a wholly-owned subsidiary of the Trust. The Irish ICAV collects royalty income, primarily U.S.-sourced, under the Ireland-U.S. treaty's 0% withholding rate.

The structure exploits a distinctive feature of Canadian tax law. DRI Healthcare Trust is structured as a mutual fund trust for Canadian purposes. Because its assets are held offshore through the Irish ICAV, it falls outside the scope of Canada's Specified Investment Flow-Through (SIFT) tax, which would otherwise impose entity-level tax on publicly traded trusts distributing certain types of income. The offshore situs of assets provides an exemption.

Income earned by the Irish ICAV constitutes Foreign Accrual Property Income (FAPI) under Canadian controlled foreign corporation rules. This income is attributed to the Canadian trust regardless of whether it is distributed. The trust then faces a structural mismatch: its taxable income (FAPI inclusions) significantly exceeds its cash distributions. To resolve this, DRI makes "dry income" distributions through additional unit issuances that are promptly consolidated back to the original number of units. Unitholders receive taxable income allocations even when they receive no cash, a feature that has implications for the investor base the trust can attract.

The 2025 Internalization

On July 1, 2025, DRI Healthcare completed the internalization of its investment management function. The Trust terminated the management agreement with DRI Capital Inc. for a $48 million termination payment and acquired the relevant assets of DRI Capital for $1 million. All DRI Capital employees transitioned to a newly-incorporated, wholly-owned subsidiary of the Trust. The move was accelerated by a 2024 internal investigation into irregularities related to certain consulting expenses charged by the former CEO, which led to financial restatements.

From a tax structuring perspective, the internalization simplifies the corporate chain. Pre-internalization, management fees flowed out to DRI Capital Inc., an entity sitting outside the Trust's corporate umbrella. Post-internalization, all management functions are performed within the Trust's subsidiaries, eliminating external fee payments that would otherwise need to satisfy arm's-length pricing requirements. DRI projects the internalization will deliver $200 million in cumulative savings over 10 years.

The architecture achieves several objectives simultaneously: zero withholding on U.S.-source royalties via the Irish treaty, QIAIF-eligible treatment at the Irish ICAV level, and SIFT tax avoidance through offshore asset situs. As of Q3 2025, the portfolio generated $195 million in trailing twelve-month revenue across 28 royalty streams on 21 products.

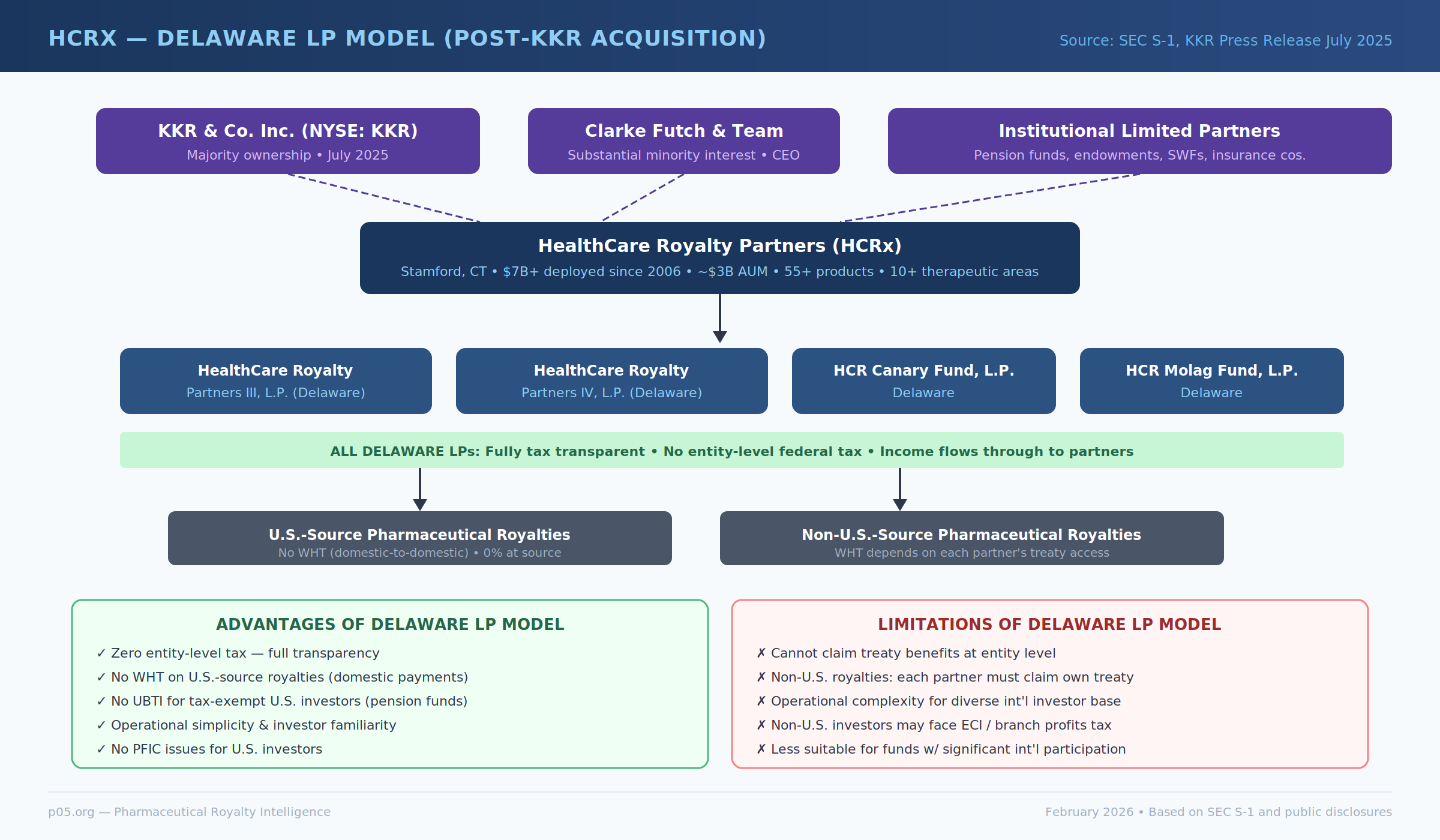

Healthcare Royalty Partners: The Delaware LP Model

HealthCare Royalty Partners (HCRx), now majority-owned by KKR following a July 2025 acquisition, historically operated through a constellation of Delaware limited partnerships: HealthCare Royalty Partners III, L.P., HealthCare Royalty Partners IV, L.P., HCR Canary Fund, L.P., HCR Molag Fund, L.P., and numerous others, as disclosed in the company's S-1 filing. KKR's acquisition of a majority ownership stake, with CEO Clarke Futch retaining a substantial minority interest and continuing to lead the team, positions HCRx to scale its platform significantly, having deployed over $7 billion in capital since its founding in 2006 and currently managing approximately $3 billion in assets across more than 55 products.

The Delaware LP model represents the purest domestic approach. Delaware limited partnerships are tax transparent: they file informational returns but pay no entity-level federal tax. Income flows through to the partners, who pay tax in their home jurisdictions at their applicable rates. For U.S. institutional investors such as pension funds (which may be tax-exempt) and endowments, this transparency is optimal because it avoids creating unrelated business taxable income (UBTI) that would compromise their tax-exempt status, provided the partnership's income is properly characterized.

The key tax planning question for a domestic LP holding royalty assets is the characterization of income. Royalties received directly by a U.S. partnership from U.S. pharmaceutical companies face no withholding at source (domestic-to-domestic payments). But when the LP acquires royalties on drugs sold globally, payments originating from foreign sources may carry withholding tax from the source country. A Delaware LP cannot claim treaty benefits in its own right because it is tax transparent; instead, each partner must independently qualify for treaty relief based on their own residency and treaty entitlements.

This creates a significant limitation for international investors. A German pension fund investing in a Delaware LP that receives royalties from a Swiss pharmaceutical company would need to claim benefits under the Germany-Switzerland treaty, not a U.S.-Switzerland treaty. The operational complexity of coordinating treaty claims across a diverse investor base is one reason why offshore structures (Ireland, Luxembourg) are often preferred for funds with significant international participation.

The 2021 reorganization merged the Legacy HCR Partnerships into HCRX Investments HoldCo, L.P., a single Delaware limited partnership, in preparation for a potential public listing. The "Up-C" structure contemplated would have placed Healthcare Royalty, Inc., a Delaware corporation, atop the partnership, mirroring the approach used by many private equity firms going public.

Luxembourg: The Fund Structuring Capital of Europe

Luxembourg is the dominant jurisdiction for European alternative investment fund structuring, and its toolkit is particularly well-suited to pharmaceutical royalty funds serving institutional investors.

The SCSp and SCS: Tax Transparency at Scale

The Société en Commandite Spéciale (SCSp), introduced in 2013, has become the default vehicle for private equity and alternative credit funds in Luxembourg. The SCSp is a special limited partnership without legal personality, governed by a contractual limited partnership agreement (LPA) that mirrors Anglo-Saxon LP conventions.

The SCSp's defining characteristic is full tax transparency. The partnership itself is not subject to Luxembourg corporate income tax, municipal business tax, or net wealth tax. Distributions to non-resident limited partners are not subject to Luxembourg withholding tax. Income and gains are attributed directly to the partners, who are taxed in their home jurisdictions as if they held the underlying assets directly.

For a pharmaceutical royalty fund, this means a Luxembourg SCSp holding royalty rights on a German-patented drug would not itself pay tax on the royalty income. Instead, each limited partner would be treated as receiving their proportionate share of the German-source royalty. A U.S. pension fund partner could claim benefits under the Germany-U.S. treaty. A UK insurance company could claim benefits under the Germany-UK treaty. The fund vehicle itself imposes no additional tax layer.

However, there is a critical limitation. Because the SCSp is tax transparent, it cannot itself claim treaty benefits or EU directive protections. It cannot access the Luxembourg-Germany treaty to reduce withholding on German-source royalties. This is a fundamental trade-off: transparency eliminates entity-level taxation but also eliminates entity-level treaty access.

The Soparfi and SICAR: Opacity with Treaty Access

For funds that need entity-level treaty access, Luxembourg offers the Société de Participations Financières (Soparfi), an ordinary fully taxable commercial company, and the Société d'Investissement en Capital à Risque (SICAR), a risk capital investment company.

A Soparfi structured as an SA or SARL is subject to the full Luxembourg corporate tax regime (aggregate rate of approximately 24.94%) but can access Luxembourg's extensive treaty network of over 80 bilateral treaties. Critically for royalty funds, Luxembourg does not impose withholding tax on outbound royalty payments, regardless of whether the recipient is in a treaty jurisdiction. This zero outbound royalty withholding, combined with treaty-reduced or eliminated inbound withholding, makes Luxembourg an attractive intermediate holding jurisdiction.

A SICAR structured as a corporate entity (SA, SARL, or SCA) follows the ordinary tax regime but benefits from a critical exception: income derived from qualifying investments in risk capital is exempt from Luxembourg tax. If pharmaceutical royalties qualify as risk capital returns, the SICAR could receive royalty income free of Luxembourg tax while still accessing Luxembourg's treaty network to reduce source-country withholding.

The RAIF (Reserved Alternative Investment Fund), introduced in 2016, provides additional flexibility. A RAIF adopting the SIF model is exempt from corporate income tax and municipal business tax, paying only a 0.01% annual subscription tax on net assets. A RAIF adopting the SICAR model benefits from the risk capital exemption while retaining treaty access.

The Reverse Hybrid Trap

Luxembourg's implementation of ATAD 2 anti-hybrid rules introduced a significant risk for SCSp-based fund structures. A "reverse hybrid" arises when an entity is treated as tax transparent in its jurisdiction of establishment (Luxembourg) but as opaque by its investors' home jurisdictions. If non-resident investors holding 50% or more of interests treat the SCSp as opaque, the SCSp becomes subject to Luxembourg corporate income tax on income that is not taxed in any other jurisdiction.

For pharmaceutical royalty funds, this means careful structuring is required to ensure that the major investors' home jurisdictions respect the SCSp's transparency. An exemption applies if the SCSp qualifies as a collective investment vehicle (CIV), which requires meeting specific diversification and investor eligibility criteria. Funds that fail the CIV test and have predominantly opaque-treated investors could face unexpected Luxembourg taxation, negating the transparency benefit that motivated the Luxembourg domicile in the first place.

Ireland: Treaty Access Meets Fund Exemption

Ireland's appeal for royalty fund structures rests on three pillars: a broad treaty network with favorable royalty provisions, entity-level tax exemptions for qualifying funds, and structures specifically designed for U.S. investor compatibility.

The QIAIF Regime

Ireland's Qualifying Investor Alternative Investment Fund regime provides five tax-free legal wrappers: the ICAV, Investment Company, Unit Trust, Common Contractual Fund (CCF), and Investment Limited Partnership (ILP). These vehicles are exempt from Irish income tax, capital gains tax, and corporation tax on their investment returns.

For pharmaceutical royalty funds, the ICAV has become the dominant choice, largely because of its U.S. tax treatment. Unlike an Irish public limited company, which is treated as a corporation for U.S. tax purposes, the ICAV can make a check-the-box election to be treated as a partnership or disregarded entity. This eliminates PFIC concerns for U.S. investors and allows income to flow through without entity-level taxation in either Ireland or the United States.

The Common Contractual Fund (CCF) offers an alternative for institutional investors. The CCF is tax transparent, meaning investors are treated as directly owning the underlying assets. This transparency is recognized in many jurisdictions, allowing institutional investors to claim treaty benefits based on their own residency rather than the fund's Irish domicile.

The Ireland-U.S. Treaty: Zero Withholding on Royalties

The crown jewel for pharmaceutical royalty funds domiciled in Ireland is the Ireland-U.S. income tax treaty, which reduces withholding tax on royalties paid from the U.S. to Irish residents to 0%. Given that the majority of global pharmaceutical royalty streams originate from U.S. licensees or U.S.-headquartered pharmaceutical companies, this single treaty provision is worth hundreds of millions of dollars annually across the industry.

Ireland has similar 0% royalty withholding provisions in treaties with Germany, the United Kingdom, France, and Switzerland, covering essentially all major pharmaceutical markets. The combination of zero inbound withholding and zero entity-level tax creates what is effectively a zero-tax conduit for royalty income, a feature that has not escaped the attention of international tax authorities.

Active Trading vs. Passive Income

A structural nuance with significant tax implications: Ireland taxes royalty income earned by Irish companies at 25% when classified as passive income. However, where an Irish company is considered to be carrying on an IP trade, that company's royalty income may be taxed at Ireland's 12.5% corporation tax rate on trading income. And where the company qualifies for the Knowledge Development Box (KDB), the effective rate drops to 10%.

For QIAIF-exempt vehicles, this distinction is largely academic since the exemption overrides both rates. But for Irish royalty companies operating outside the QIAIF regime, whether royalty acquisition and management constitutes "trading" or "passive investment" can swing the effective tax rate from 10% to 25%, a difference of 15 percentage points on every dollar of royalty income.

The Treaty Network as Competitive Moat

The practical impact of fund domicile becomes clearest when you map specific transactions against the treaty networks available to different structures.

Scenario: Acquiring a Royalty on a Drug Marketed by a Swiss Company

A Swiss pharmaceutical company (Roche, Novartis) owes royalties to the fund. Without treaty relief, Switzerland imposes no withholding tax on outbound royalty payments to residents of treaty countries where the treaty provides for 0% withholding.

| Fund Domicile | Treaty WHT Rate | Entity-Level Tax | Net to Investors |

|---|---|---|---|

| Ireland (QIAIF) | 0% (CH-IE treaty) | 0% (exempt) | ~100% |

| Luxembourg (Soparfi) | 0% (CH-LU treaty) | ~24.94% (unless exemption applies) | ~75% |

| Luxembourg (SCSp) | Look-through to partners | 0% (transparent) | Varies by investor |

| Delaware LP | Look-through to partners | 0% (transparent) | Varies by investor |

| Cayman Islands | 0% (no treaty, but CH has no WHT on royalties) | 0% (no tax) | ~100% |

| UK (trading company) | 0% (CH-UK treaty) | 25% (or 10% Patent Box) | 75-90% |

Scenario: Acquiring a Royalty on a Drug Marketed by a German Licensee

Germany imposes a 15.825% withholding tax (including solidarity surcharge) on royalties paid to non-residents. Treaty relief is essential.

| Fund Domicile | Treaty WHT Rate | Entity-Level Tax | Net to Investors |

|---|---|---|---|

| Ireland (QIAIF) | 0% (DE-IE treaty) | 0% (exempt) | ~100% |

| Luxembourg (Soparfi) | 0% (DE-LU treaty) | 0% (EU I&R Directive) | ~100% |

| Luxembourg (SCSp) | Look-through to partners | 0% (transparent) | Varies by investor |

| Delaware LP | Look-through to partners | 0% (transparent) | Varies by investor |

| Cayman Islands | 15.825% (no treaty) | 0% (no tax) | ~84% |

| UK | 0% (DE-UK treaty) | 25% (or 10% Patent Box) | 75-90% |

The Cayman Islands structure, which works perfectly for Swiss-source royalties, hemorrhages value on German-source royalties. A fund holding a diversified global portfolio must optimize across all source countries simultaneously, which is precisely why Ireland (with 76+ tax treaties) and Luxembourg (with 80+ treaties) dominate fund structuring.

The Substance Requirements: Post-BEPS Reality

The era of letterbox entities claiming treaty benefits is over. Every major jurisdiction now enforces substance requirements that royalty funds must satisfy to access reduced withholding rates.

Germany's Section 50d(3): The Gold Standard for Anti-Treaty Shopping

Germany's anti-treaty shopping provision, Section 50d(3) of the Income Tax Act, is arguably the most aggressive anti-abuse rule affecting royalty fund structures. The provision denies treaty benefits to foreign recipients that are "interposed entities" lacking genuine economic substance.

The German Federal Tax Office (BZSt) examines whether the recipient has its own business operations, employees, and office space, and whether the entity's income is predominantly passed through to non-treaty-eligible owners. An Irish ICAV claiming 0% withholding on German-source royalties must demonstrate that it is not merely a conduit channeling income to Cayman Islands or other non-treaty investors.

The practical requirements are demanding. German tax authorities have released updated guidance and questionnaires requiring detailed disclosure of the fund's ownership structure, management activities, and the treaty status of its ultimate investors. Funds with significant non-treaty investor participation may be denied treaty benefits on the portion of income attributable to those investors.

Germany's Royalty Barrier: Targeting Preferential Regimes

Germany's "royalty barrier" (Section 4j ITA) adds another layer of complexity. This provision disallows the German payer's tax deduction for royalties paid to related parties in jurisdictions with preferential tax regimes, currently defined as effective tax rates below 15%.

The controversial dimension is Germany's application of the royalty barrier to payments benefiting from the U.S. FDII regime (Foreign-Derived Intangible Income), which provides an effective rate of approximately 13.125% on qualifying income. German tax auditors have begun treating FDII as a "preferential regime," potentially denying deductions for royalty payments to U.S. recipients benefiting from FDII.

While the royalty barrier primarily targets related-party payments and may not directly apply to arm's-length royalty acquisitions by financial investors, it signals Germany's willingness to override treaty provisions in pursuit of base erosion concerns.

The Principal Purpose Test: OECD's Catch-All

Since Luxembourg signed the Multilateral Instrument (MLI) in 2017, most of its bilateral treaties now include the Principal Purpose Test (PPT). The PPT entered into force in Luxembourg on 1 January 2020 and denies treaty benefits when obtaining the benefit was one of the principal purposes of an arrangement.

For a Luxembourg Soparfi holding pharmaceutical royalties, the PPT requires demonstrating that the Soparfi has genuine business reasons for its Luxembourg domicile beyond tax optimization. Fund managers must document the commercial rationale for the Luxembourg structure, including access to Luxembourg's legal framework, investor preferences, regulatory considerations, and operational requirements.

Notably, the United States did not sign the MLI, which means U.S. bilateral treaties are not affected by the PPT. The Luxembourg-U.S. treaty, dating to 1962 with subsequent protocols, does not contain a PPT provision, though it does include limitation on benefits (LOB) clauses that perform a similar function.

Pillar Two: The 15% Floor and Its Impact on Fund Structures

The OECD's Pillar Two global minimum tax, now being implemented across jurisdictions, fundamentally alters the calculus for low-tax fund structures.

The Basic Mechanism

Pillar Two imposes a minimum 15% effective tax rate on multinational enterprises with consolidated group revenues exceeding €750 million. The rules operate through three mechanisms: the Qualified Domestic Minimum Top-up Tax (QDMTT), which allows source countries to claim the first right to tax undertaxed profits; the Income Inclusion Rule (IIR), which allows the parent company's jurisdiction to impose top-up tax; and the Undertaxed Profits Rule (UTPR), which serves as a backstop.

Ireland legislated for Pillar Two effective 1 January 2024 for the IIR and 1 January 2025 for the UTPR. Luxembourg has similarly implemented the rules, including a QDMTT.

Impact on Royalty Fund Structures

For pharmaceutical royalty funds exceeding the €750 million revenue threshold, Pillar Two has several implications.

Irish QIAIF vehicles that currently pay 0% entity-level tax may be subject to a QDMTT bringing their effective rate up to 15%, assuming Ireland exercises its right to collect the top-up tax domestically. This would eliminate the zero-tax benefit that makes Ireland attractive, though it would not necessarily make Ireland less competitive than other jurisdictions since the 15% floor applies globally.

Luxembourg SCSp structures face a different concern. Because the SCSp is tax transparent, Pillar Two generally looks through to the partners. The minimum tax would apply at the partner level, not the fund level, which means the SCSp structure remains viable as long as each partner is subject to at least a 15% effective rate in their home jurisdiction.

The December 2025 Side-by-Side package introduced safe harbors that effectively exempt U.S.-parented multinational groups from the IIR and UTPR, given the U.S. qualification for the Qualified SbS Regime. For Royalty Pharma, whose English plc parent sits atop the structure, the question is whether the UK (which has implemented all three Pillar Two mechanisms) would impose top-up tax on the Irish subsidiary's income.

The practical effect is that the zero-tax Irish fund vehicle may no longer provide a zero-tax outcome for large, publicly listed royalty platforms. Smaller funds below the €750 million threshold remain unaffected, creating a scale-dependent tax advantage for emerging royalty investors over established platforms.

The Competitive Edge: What Actually Matters

After mapping the treaty networks, substance requirements, and anti-avoidance rules, a clear hierarchy of fund structuring approaches emerges.

For Funds with Primarily U.S.-Source Royalties

Ireland dominates. The Ireland-U.S. treaty's 0% royalty withholding rate, combined with the QIAIF exemption and check-the-box compatibility for U.S. investors, makes Ireland the path of least resistance. DRI Healthcare Trust and Royalty Pharma both anchor their structures in Irish entities for precisely this reason.

For Funds with Diversified European Royalties

Luxembourg and Ireland are both viable, with the choice depending on investor composition. Funds with predominantly institutional investors from treaty jurisdictions can use a Luxembourg SCSp for full transparency and partner-level treaty access. Funds needing entity-level treaty claims benefit from Ireland's QIAIF (tax exempt, with treaty access) or Luxembourg's Soparfi/SICAR structures.

For Funds Targeting Non-Treaty Source Countries

The analysis becomes more complex. Some emerging pharmaceutical markets (e.g., India, China, Brazil) impose significant withholding on royalties with limited treaty relief. In these cases, the fund's ability to negotiate contractual gross-up provisions or structure payments as service fees rather than royalties may be more important than the fund's domicile.

For U.S.-Only Domestic Funds

Delaware LPs remain optimal. No withholding on domestic royalties, full transparency, and no entity-level tax. The simplicity and investor familiarity of the Delaware LP explain why HCRx operated through this structure for nearly two decades.

Looking Forward: Convergence Toward a 15% World

The trajectory of international tax reform points toward a world where the effective tax rate floor converges on 15% for all large multinational enterprises. For pharmaceutical royalty funds, this means the era of zero-entity-level-tax structures may be ending for the largest players.

The 2025 wave of management internalizations across the sector — Royalty Pharma's $1.1 billion acquisition of RP Management in May, DRI Healthcare's $49 million termination of DRI Capital in July, and KKR's majority acquisition of HCRx — reflects a broader structural maturation. These internalizations simplify corporate chains, eliminate external fee flows that require transfer pricing justification, and reduce the number of intercompany transactions that must satisfy substance requirements under BEPS and Pillar Two frameworks. In a post-ATAD, post-MLI, post-Pillar Two world, simpler structures are easier to defend.

But nuance persists. The 15% minimum applies only to enterprises above the €750 million revenue threshold. The definition of "revenue" for a royalty fund, and whether gross royalty receipts or net income constitutes the relevant measure, remains subject to interpretation. Safe harbors for investment funds and collective investment vehicles may carve out substantial portions of the royalty fund universe from Pillar Two's reach.

Moreover, even in a 15% minimum tax world, the difference between 15% and 25% or 30% remains enormous at scale. A fund paying 15% on $500 million in annual royalty income retains $425 million. A fund paying 25% retains $375 million. Over a 15-year drug lifecycle, that $50 million annual differential compounds to $750 million in additional value available for deployment, distribution, or reinvestment.

The fund managers who understand these structural mechanics, and who build their vehicles to navigate the intersection of treaty networks, substance requirements, anti-avoidance rules, and minimum tax regimes, will continue to deliver meaningful alpha to their investors. In pharmaceutical royalties, as in the drugs themselves, the formulation matters as much as the active ingredient.

This article builds on the analysis presented in Cross-Border Pharmaceutical Royalty Transactions and Royalties That Wake Up: How Change-of-Control Triggers Reshape Pharma Deal Economics.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or investment advice. The author is not a lawyer or financial adviser. All information presented here is derived from publicly available sources including SEC filings, court decisions, tax treaty texts, and regulatory guidance. Details of specific transactions and tax rules may have changed since publication. Readers should conduct their own due diligence and consult with qualified legal and financial professionals before making any investment or business decisions.