The Vintage Year Problem in Royalty Funds: Why 2021 Burned Brightest

Overview

In private equity and royalty finance, the term "vintage year" refers to the calendar year in which a fund first deploys capital. It anchors a transaction in time, binding it to the macroeconomic environment, prevailing discount rates, and asset valuations of that particular moment. For pharmaceutical royalty funds, vintage year matters enormously because royalties are, at their core, long-duration instruments: their present value is acutely sensitive to the rate at which future cash flows are discounted back to today.

The 2021 vintage may turn out to be the most challenged deployment year in royalty finance in at least a decade. Not because the underlying drugs necessarily failed, but because of a more structural problem: deals were priced in a world of near-zero interest rates, inflated biotech valuations, and compressed risk premiums that no longer exist. When that world ended abruptly in 2022, the retrospective economics of those transactions deteriorated sharply.

This article examines the mechanics of why 2021 is the most stressed vintage, whether 2022, 2023, 2024, and 2025 vintages face related problems, and what the implications are for the royalty finance market through 2026 and beyond.

The 2021 Biotech Boom: What Made It Exceptional

To understand why 2021 royalty deals are challenged, you first need to understand how extraordinary the conditions were in which they were struck.

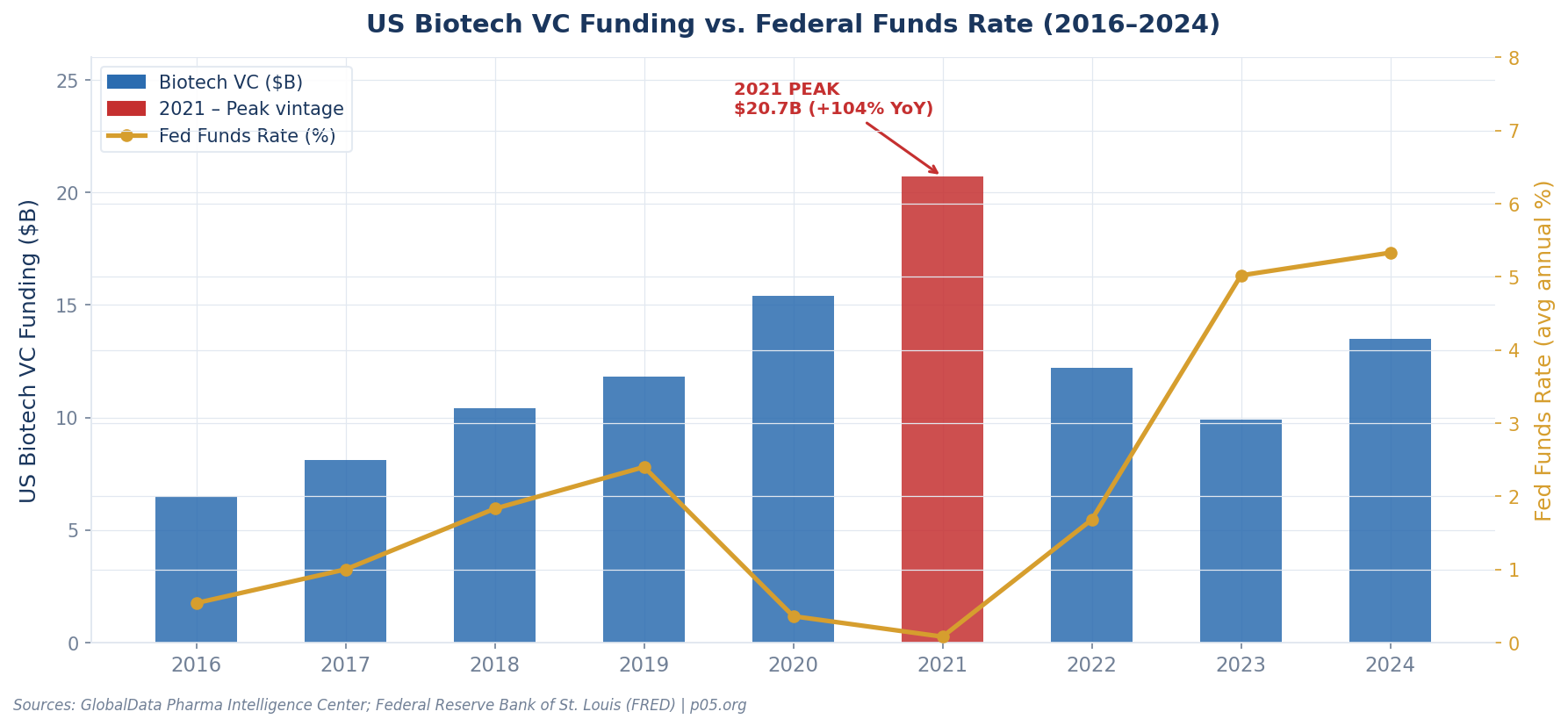

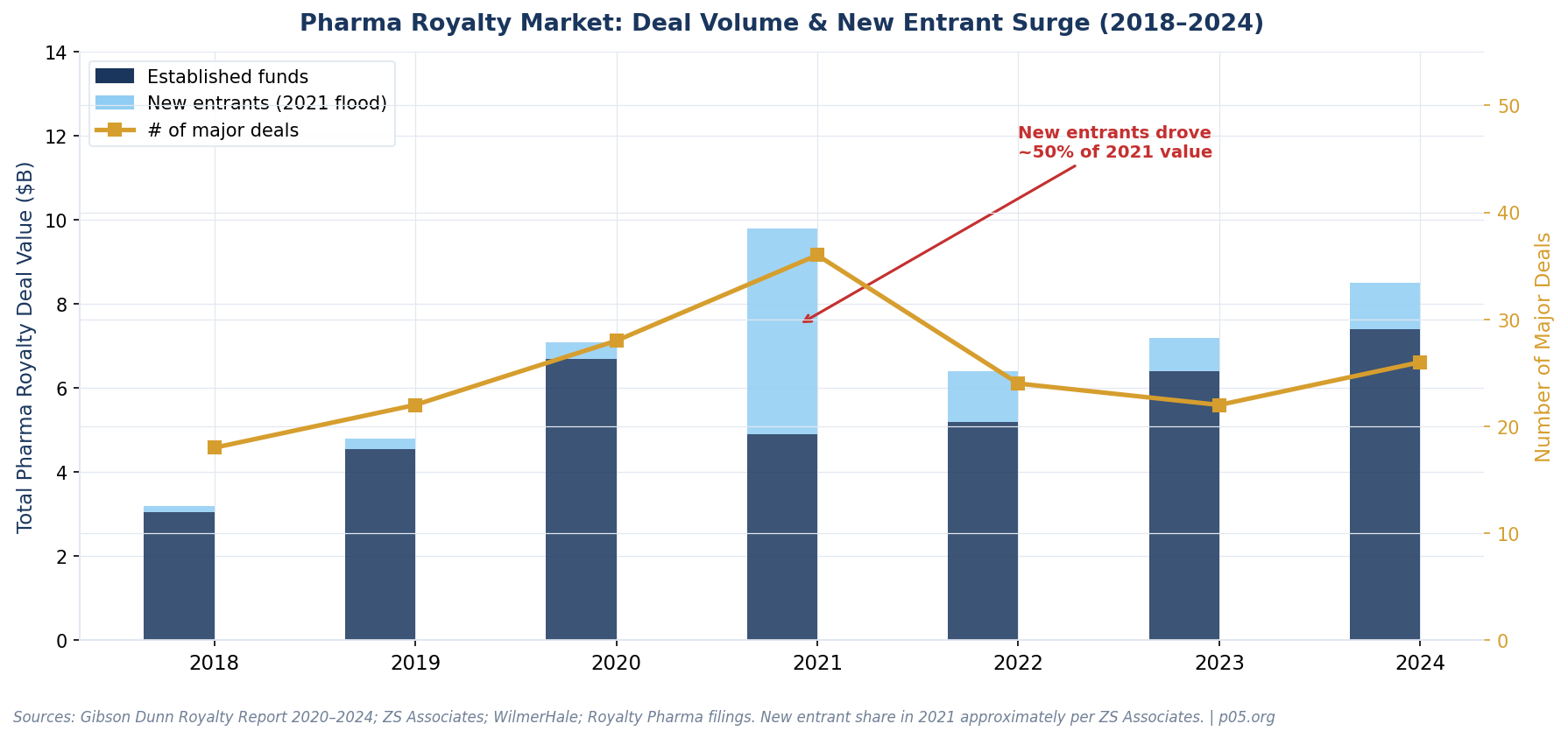

In 2021, venture financing for US-headquartered companies with innovator drugs peaked at approximately $20.7 billion, a 104% increase from the prior year. This was not a gradual build — it was a step-change driven by a collision of factors unlikely to repeat in combination:

Monetary policy at historic extremes. The Federal Reserve held the federal funds rate near zero throughout 2020 and 2021. In a zero-rate environment, the net present value of long-dated cash flows — exactly the kind royalty investors depend on — is artificially elevated. When you discount a royalty stream at 7% instead of 12%, the upfront price you can justify paying increases by 20–30% depending on duration.

COVID-19 capital surge. The pandemic created a perception that biotech was recession-proof and structurally undervalued. Investors flooded the sector. The Nasdaq Biotechnology Index peaked in February 2021 at levels not seen before or since, then gave back most of those gains over the following two years.

IPO fever inflating comparables. Biotech IPOs soared, with 114 companies going public in 2021 alone. Many were early-stage assets with thin data packages. Their inflated market caps became the comparables royalty funds used to underwrite entry multiples. If a pre-commercial biotech was trading at $2 billion in the public markets, royalty investors priced their streams accordingly.

New entrants compressing pricing. Per ZS Associates analysis, new investors drove nearly half of total royalty market value in 2021. Competition for deals compresses pricing — in this case, meaning investors accepted lower implied IRRs in exchange for access to coveted assets.

The result: a market in which royalty funds deployed capital at rich multiples, compressed discount rates, and optimistic revenue projections. It felt rational at the time. It does not look rational in retrospect.

The Core Mechanic: Why Discount Rate Shifts Hurt Royalties So Much

A pharmaceutical royalty is, at its economic core, a discounted cash flow instrument. Its value is the present value of all future royalty payments, discounted at a rate that reflects the cost of capital and the risk profile of the underlying asset.

When risk-free rates rise sharply — as they did from near zero to over 5% during 2022–2023 — two things happen simultaneously to 2021-vintage royalty deals.

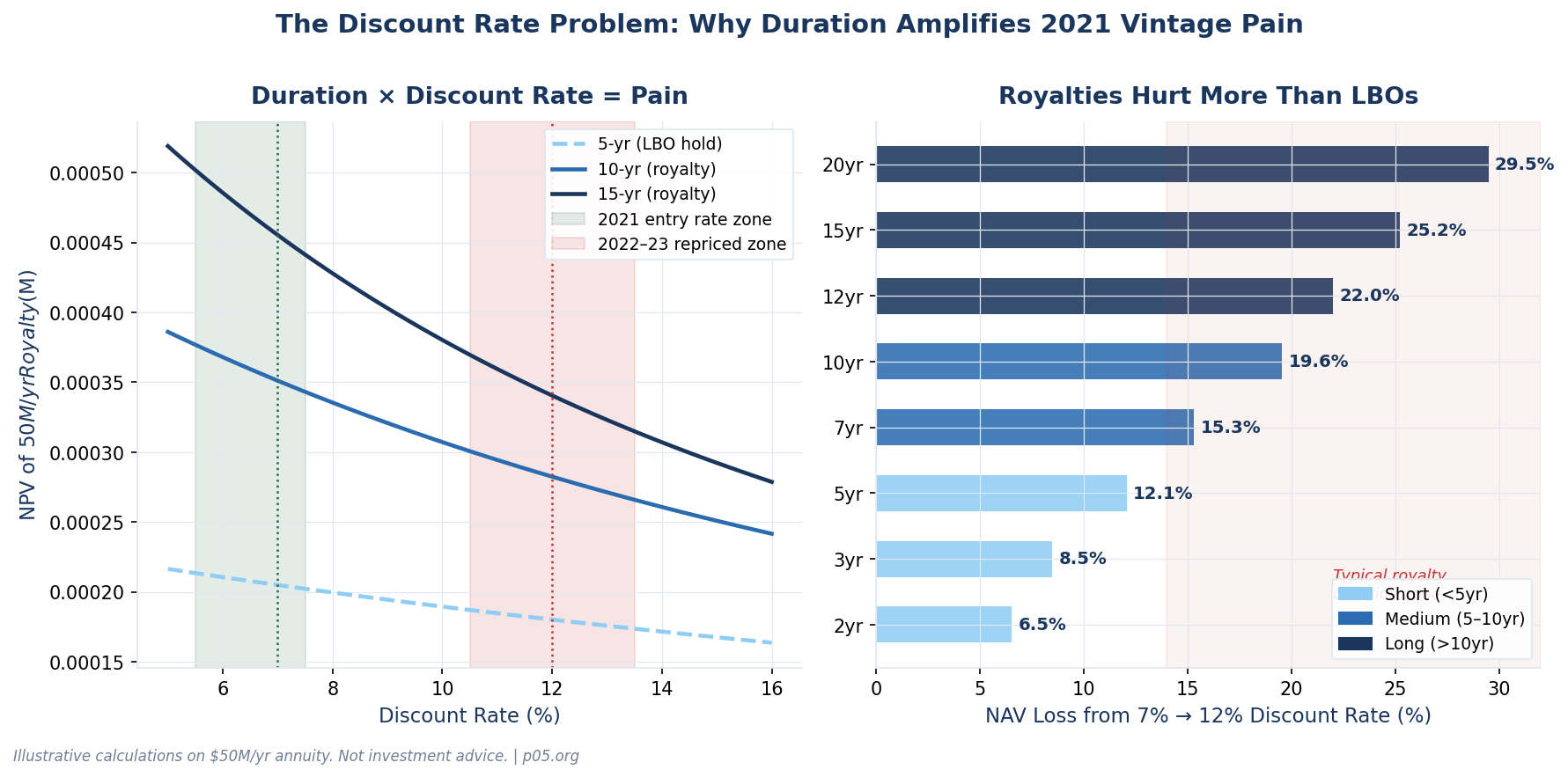

First, the discount rate at which investors must now price comparable cash flows rises. For a typical commercial-stage royalty fund, the cost of capital shifted from roughly 7–9% in 2021 to 11–13% by late 2022. A 3% rise in the risk-free rate feeds directly through to the discount rate applied to any pharma asset, mechanically reducing NPV by 15–25% depending on duration.

Second, the opportunity cost of deployed capital rises. An LP who committed to a royalty fund in 2021 can now earn 5%+ risk-free on US Treasuries. The royalty fund's hurdle rate — the minimum return required to justify the illiquidity premium — has risen. Deals priced to deliver 8% look inadequate when risk-free alternatives offer 5%.

The right panel of the chart above shows the critical insight: the longer the royalty term, the worse the damage. A 3-year LBO-style hold loses 7% of its value when the discount rate moves from 7% to 12%. A 15-year royalty loses 20%. Duration is the amplifier. This is why 2021 royalty vintages are more distressed than 2021 private equity vintages, even when the underlying assets are performing identically to plan.

Not Just 2021: The Full Vintage Year Map

The vintage year problem is not binary. Different deployment cohorts face different combinations of risk, and the picture becomes more nuanced when you look across years.

2019 and Prior: Well-Positioned

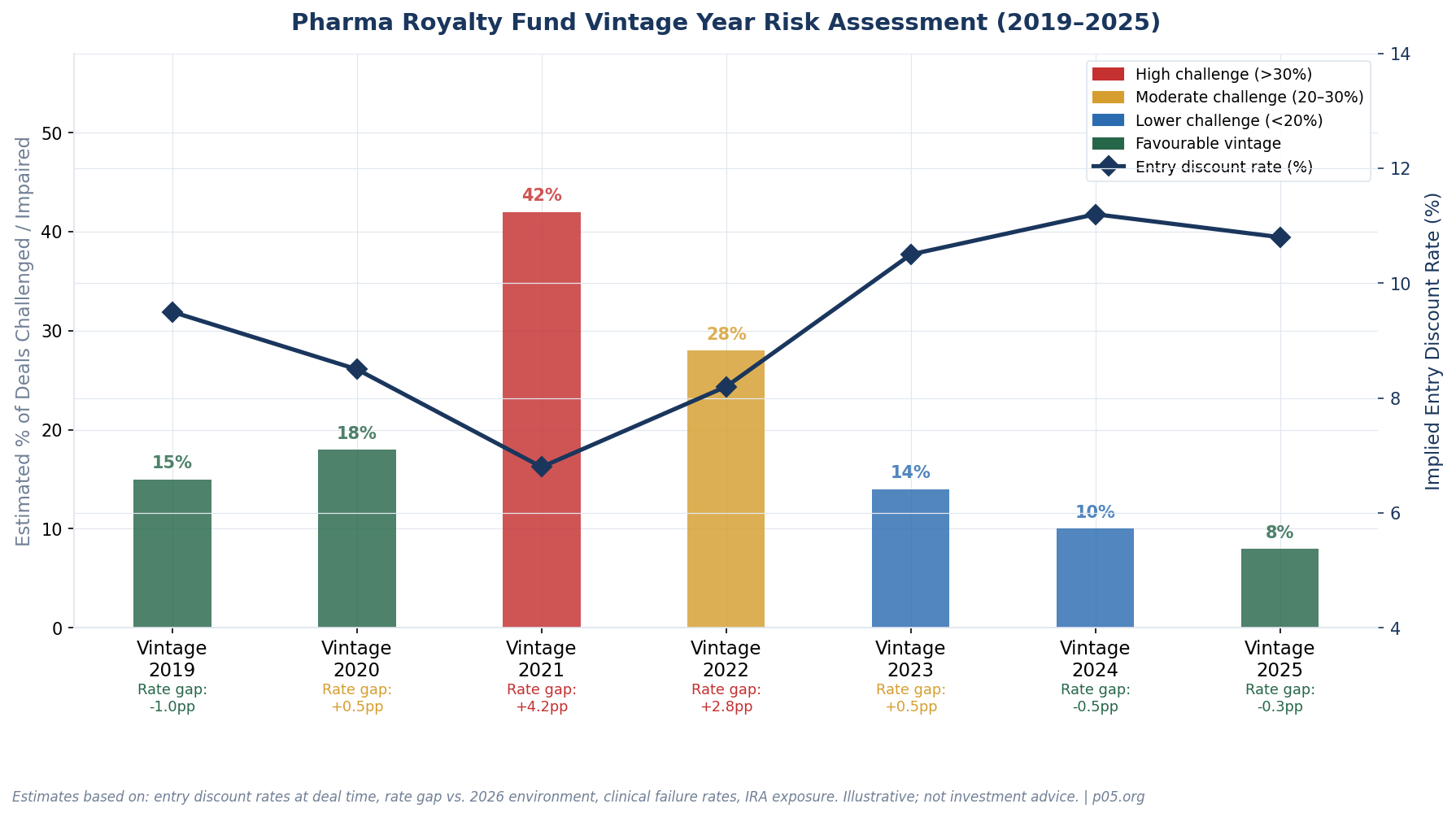

Deals struck in 2018 and 2019 used discount rates of 9–10%, roughly in line with today's normalized rate environment. Many of these royalties are now well into their cash flow generation phase, and the rate differential between entry pricing and current reality is minimal. The main risk for this cohort is simple: normal clinical and commercial execution risk. There is no structural headwind.

2020: Mildly Exposed

The 2020 cohort has mixed characteristics. Deals struck in early 2020 (Q1) were underwritten at pre-COVID discount rates. Those struck in Q3–Q4 2020 benefited from the emerging low-rate environment but also captured assets at valuations before the full speculative bubble developed. The gap between entry discount rates (~8.5%) and today's environment (~10.5%) is manageable for deals where the drugs are performing.

2021: The Most Challenged Vintage

The 2021 cohort carries the confluence of every headwind simultaneously. Entry discount rates compressed to 6–7%, biotech valuations were at peak, new competition flooded the market, IRA risk was not yet priced in, and the rate cycle was about to inflict maximum damage on long-duration assets. Our estimate is that roughly 40% of major 2021-vintage royalty deals face some form of material impairment — either mark-to-market losses on rate repricing, commercial underperformance, clinical failure, or IRA-driven revenue ceiling effects.

The single largest 2021 royalty transaction illustrates the anatomy of a vintage year problem deal with unusual precision. In July 2021, Royalty Pharma deployed up to $2.025 billion in a structured partnership with MorphoSys AG, providing $1.425 billion upfront plus $350 million in development funding bonds and $100 million in equity. The deal packaged four assets into a single transaction:

Tremfya (guselkumab): 100% of MorphoSys's 1.5% royalty on J&J's IL-23 inhibitor, which was already commercialised at deal time. This component has proved the deal's saving grace — Tremfya received FDA approval for ulcerative colitis in September 2024 and Crohn's disease in March 2025, with J&J guiding to $10 billion+ peak sales. The Tremfya royalty stream alone is now estimated to be worth multiples of what RPRX paid for it in 2021.

Gantenerumab: 60% of MorphoSys's tiered 5.5–7% royalty on Roche's anti-amyloid Alzheimer's antibody, which analysts were projecting at $10 billion peak sales in 2021. In November 2022, Roche announced the Phase 3 GRADUATE trials showed only a 6–8% relative reduction in clinical decline — not statistically significant. The royalty was written off.

Otilimab: 80% of MorphoSys's royalty on GSK's anti-GM-CSF antibody in rheumatoid arthritis, terminated in October 2022 after Phase 3 showed limited efficacy. Write-off: $160 million in Q3 2022.

Pelabresib / CPI-0209: 3% of net sales royalty on MorphoSys/Constellation's BET inhibitor programs in myelofibrosis and haematological malignancies, where clinical development remains ongoing.

The MorphoSys transaction is a rare window into how a single 2021 deal can produce radically divergent outcomes within the same portfolio — one transformative winner (Tremfya, now outperforming by an estimated 154% vs. original underwriting), two permanent write-offs (gantenerumab and otilimab), and one still-uncertain development asset. The aggregate deal return is being rescued almost entirely by one drug receiving indications that did not exist when the deal was priced. Most 2021-vintage portfolios do not have a Tremfya to offset their gantenerumabs.

2022: Transitional and Overlooked

2022 is an underappreciated problem vintage. Deals were priced when rates were already rising — the Fed began hiking in March 2022 — but many underwriting models still used peak-2021 consensus forecasts as their base case. Through August 2022, biotech IPOs had dropped 78% from a year prior, but the royalty market remained relatively active. The rate gap between 2022 entry pricing (~8–9%) and the terminal 2023 rate environment (~11–12%) was not as extreme as 2021's, but it is not trivial for long-duration assets. The IRA was also passed in August 2022, meaning deals struck before that date did not fully account for its commercial implications.

The unusually high rate of debt financing in 2021–2022 culminated in 41 biotech bankruptcies in 2023, up from 20 in 2022 and 9 in 2021 — a direct echo of excess 2021 leverage that hit counterparty credit quality and dragged development-stage royalties.

2023: A Recalibrated Cohort

2023 is when discipline returned. Rising interest rates had made debt financing less attractive to borrowers and lenders pulled back on venture lending, pushing more biotech companies toward royalty financing — but this time, sellers came with lower leverage in the transaction. Entry discount rates for 2023 deals moved to 10–11%, reflecting the new rate reality. IRA risk was better understood and modeled. The Gibson Dunn Royalty Report covering 2020–2024 notes that milestone-heavy transactions grew at 33% annually over the five-year period, with buyers lowering their upfront risk exposure. The 2023 cohort is not problem-free — drugs can still fail, competitive landscapes can change — but the structural headwinds from rate compression and inflated entry pricing are largely absent.

2024 and 2025: Favourable Entry Conditions

Royalty deal volume is estimated at around $14 billion annually as of 2024, driven by the continued difficulty biotech companies face in accessing equity and IPO markets. The deals being struck now are being written at entry rates of 10–12%, against conservative revenue forecasts shaped by 2021's sobering lessons. IRA pricing uncertainty is now modeled explicitly. The 2024–2025 vintage represents, in many ways, the mirror image of 2021: disciplined entry conditions, a realistic rate environment, and sellers who are negotiating from a weaker position. Royalty Pharma's 2024 Investor Day reported that over 90% of transactions since 2020 exceeded their approximately 7% cost of capital on a portfolio basis — but that figure will be skewed heavily toward the most recent and best-structured deals.

The Market's New Entrant Problem

The vintage year problem falls disproportionately on the class of investors who entered the royalty market in 2021.

Established platforms — Royalty Pharma, Healthcare Royalty Partners (HCRx), DRI Healthcare Trust, XOMA Royalty, Oberland Capital — have diversified portfolios spanning multiple vintage years, deal structures, and therapeutic areas. A single challenged 2021 position is one line item among many. Moreover, these firms have the deal flow history to know which assets to avoid.

For newer entrants who raised capital in 2020–2021 and deployed it quickly, the math is harder. A concentrated fund with 8–12 positions, several of which are development-stage 2021 vintages priced at compressed discount rates, faces the possibility of producing sub-par returns across a material portion of its portfolio.

As one market observer noted: "If you look at hard data in the long run, 2020–2021 was an outlier. Venture financing and other financial transactions in the life sciences space at that time were two, if not three times above where they were on their historical trajectory."

The firms that entered royalty finance as opportunistic capital allocators during the 2021 boom — primarily non-specialist private equity and hedge funds seeking yield in a zero-rate world — are the ones most likely to be quietly working through portfolio impairments without the benefit of institutional royalty expertise or portfolio diversification.

Three Failure Modes, Ranked by Severity

The vintage year problem manifests differently depending on deal structure and asset stage. Three primary failure modes affect 2021-era transactions, with different probabilities of recovery.

Failure Mode 1: Discount Rate Repricing (Recoverable Over Time)

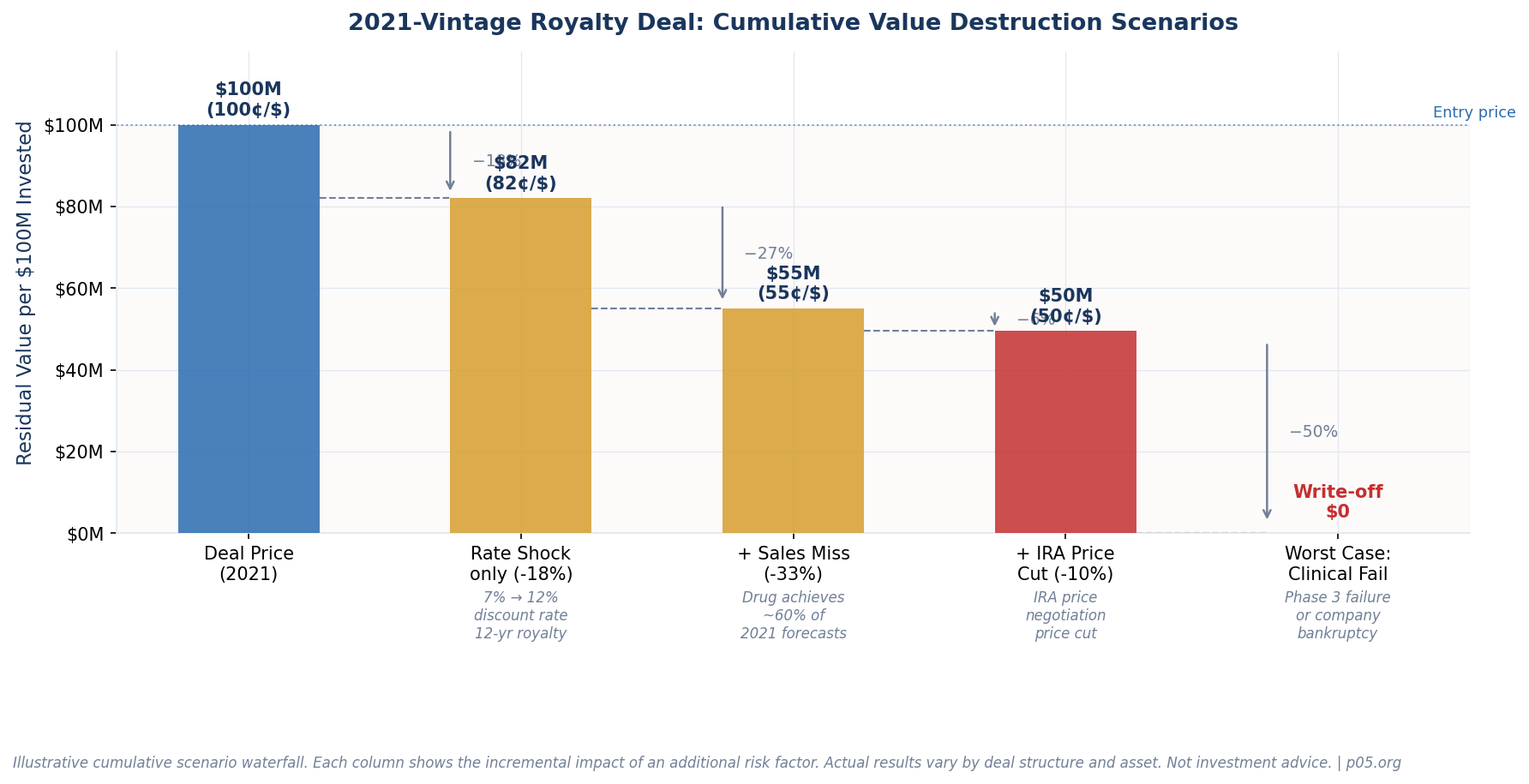

The most mechanical problem: deals priced at 6–7% are now worth less because the market requires 10–12% returns on similar risk profiles. A 12-year royalty repriced from 7% to 12% loses approximately 20% of its original NPV — purely from the rate change, before any drug-specific underperformance.

This failure mode is uncomfortable but not terminal. If the royalty stream delivers its projected cash flows, the investor's ultimate IRR still proves out. The investor must accept lower mark-to-market NAV and a longer J-curve than originally modeled, but real money is not destroyed. Time heals this variant.

Failure Mode 2: Commercial Underperformance (Partially Recoverable)

The 2021 bull market produced analyst consensus forecasts with aggressively optimistic peak-sales assumptions. The NASDAQ biotech index lost 14% of its value through August 2022 alone, reflecting widespread earnings disappointment in the sector. Drugs that achieved 50–70% of projected peak sales deliver proportionally less royalty income, and there is no acceleration mechanism in a pure royalty structure.

A $100M investment in a 5% royalty priced against $1.2B peak sales delivers roughly $60M/year at peak. If the drug tops out at $600M, the investor receives $30M/year — and the original deal economics are deeply impaired on any reasonable discount rate assumption.

Failure Mode 3: Clinical Failure and IRA Impact (Permanent Impairment)

The hardest failure mode: the drug either never reached approval or faces structural revenue constraints from the Inflation Reduction Act. In FY 2022, Royalty Pharma recorded a $616 million non-cash GAAP impairment — concentrated in three 2021-era positions:

The gantenerumab write-off (Roche's Alzheimer's candidate, GRADUATE trial failure November 2022) and otilimab termination (GSK, $160 million write-off Q3 2022) both flowed from the MorphoSys deal described above. Gavreto (pralsetinib, Blueprint Medicines) contributed commercial underperformance impairment as competitive dynamics in RET-mutant NSCLC deteriorated.

The industry-wide context frames why these failures were predictable in aggregate even if not individually: overall clinical trial failure rates run at approximately 90%, with Phase 3 failure rates for CNS programmes specifically running at around 85%. Any 2021-vintage portfolio with meaningful development-stage exposure was statistically likely to encounter at least one permanent write-off.

The Omecamtiv Mecarbil case is instructive for a different reason — it illustrates the messy middle ground between clean failure and clean success. Royalty Pharma originally invested $100 million in Cytokinetics' heart failure programme in 2017, then expanded to a $450 million commitment in 2022 when the drug was in late-stage development.

The FDA rejected the application. Rather than a clean write-off, the position was restructured in 2024: RPRX committed an additional $100 million for a new Phase 3 trial, with contractual downside protection requiring Cytokinetics to pay back $237.5–275 million over 4.5–5.5 years if the new trial also fails. The position is neither written off nor performing — it sits in an extended hold, consuming additional capital and management attention, with the original 2022 deployment now representing a version of the sunk cost problem common across distressed development-stage royalties.

The IRA introduces a subtler but equally permanent impairment channel. Royalties on large-selling branded drugs in IRA-eligible indications — cardiovascular, metabolic disease, oncology — face a structural revenue ceiling that was not incorporated into 2021 underwriting models.

The royalty investor bears 100% of the proportional impact: a 20% negotiated price reduction translates directly to a 20% reduction in royalty income with no offset. The other documented development-stage failures in RPRX's 2021-adjacent portfolio — BioCryst's BCX9930 (Factor D inhibitor, discontinued), vosaroxin (oncology), and Merck KGaA's anti-IL-17 nanobody M1095 — follow the same pattern of permanent capital impairment with no recovery mechanism.

RPRX as Market Barometer

Royalty Pharma is the most visible and data-rich entity through which to observe vintage year stress — not because it is necessarily the most impaired, but because it is publicly listed and reports GAAP financials quarterly.

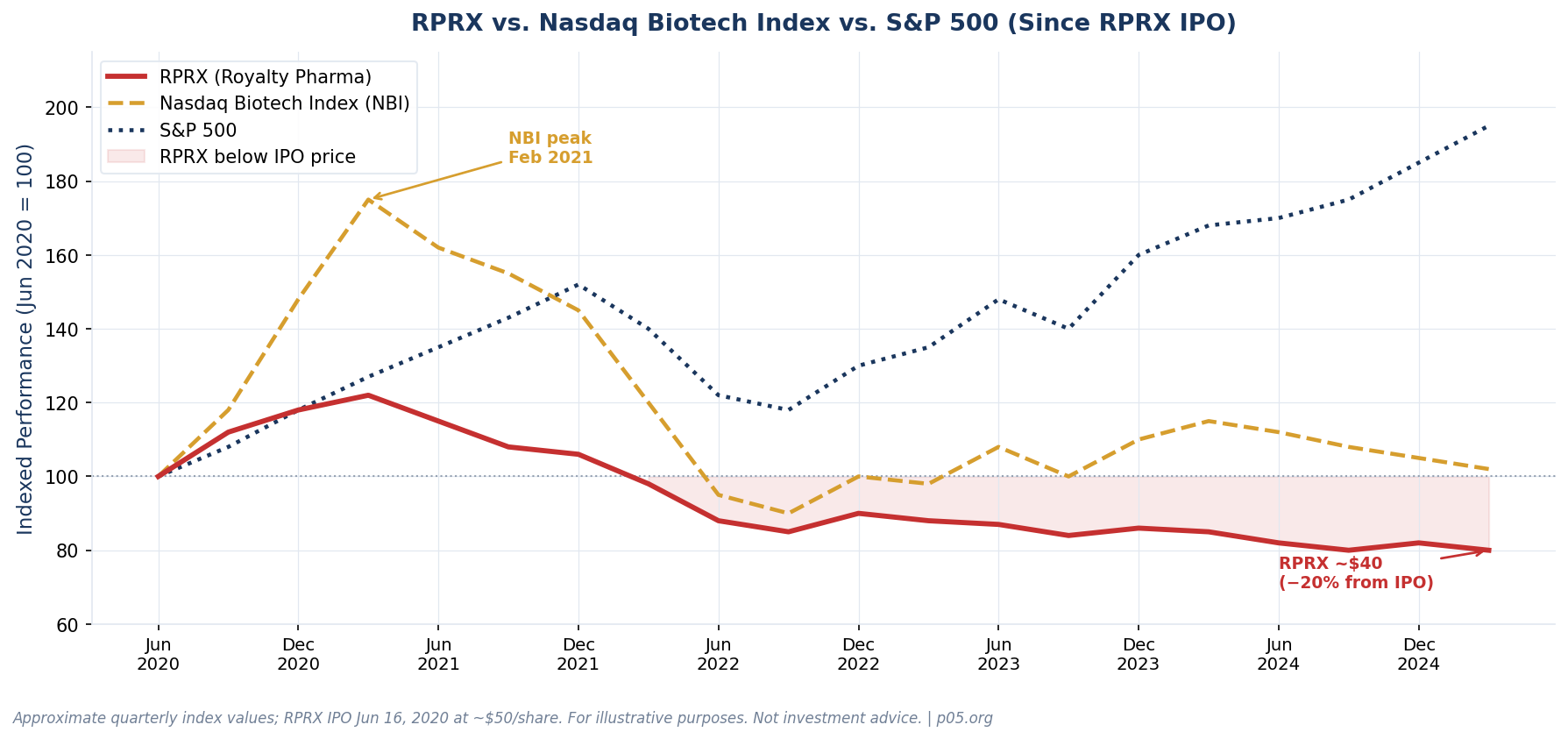

RPRX priced its IPO at approximately $50 per share in June 2020. As of early 2026 it trades near $40 — approximately 20% below the IPO price. Yet the underlying cash flow engine has been growing throughout. Annual Portfolio Receipts tell the story of a business performing operationally while the equity market prices it at a higher cost of capital:

| Year | Portfolio Receipts | Top Contributors |

|---|---|---|

| 2020 | $1.80B | CF franchise $498M, Imbruvica $332M, HIV $294M, Tysabri $199M |

| 2021 | $2.13B | CF franchise $642M, Imbruvica $351M, Tysabri $208M, Promacta $149M |

| 2022 | $2.21B (+ $458M Biohaven) | CF franchise $729M, Imbruvica $299M, Tysabri $191M, Trelegy $126M |

| 2023 | $3.05B (+ $475M Zavzpret) | CF franchise $775M, Imbruvica $248M, Trelegy $160M, Evrysdi $104M |

| 2024 | $2.80B | CF franchise $831M, Trelegy $229M, Evrysdi $177M, Tremfya $112M |

The recurring royalty base — stripping out one-time Biohaven and Zavzpret milestone payments — grew at a healthy mid-single-digit rate through 2024. The portfolio is performing. The equity discount reflects something else: the market applying a higher discount rate to the entire future royalty stream than RPRX's own internal model implies, and pricing in the known impairments on development-stage positions without full credit for newer commercial additions like Tremfya's expanded indications.

The market is discounting the entire future royalty stream at a materially higher rate than RPRX's own internal model implies.

In January 2025, Royalty Pharma announced a $3 billion share repurchase program, explicitly stating that shares were trading at a discount to intrinsic value. That is a sophisticated way of acknowledging that the outside discount rate and the inside discount rate disagree — and the market, incorporating the new rate reality, is pricing the portfolio conservatively.

This dynamic affects every royalty fund, public or private. Private funds carry NAV marks set by their own models, often with less market discipline applied. LPs in 2021-vintage private royalty funds should scrutinize those marks carefully.

Will 2021 Vintages Eventually Recover?

The answer depends entirely on which failure mode dominates.

Rate-driven impairment only: These deals are recovering slowly as time passes and cash flows accrue. The further into the royalty term, the smaller the impact of a given discount rate change on residual value. By year 8–10 of a 15-year royalty, the compounding effect of rates normalizing and cash flows arriving erodes most of the original mark-to-market loss. Patient capital wins here.

Commercial underperformance: These deals require the drug to find its market. Some will. Royalties on drugs with genuine clinical differentiation but sluggish early launches often inflect after 3–5 years as prescriber adoption broadens. Where the drug failed to differentiate or lost competitive position permanently, the loss is real but partial — unlike clinical failure, at least some cash flows arrive.

The BioCryst/Orladeyo royalty, where RPRX participated in two transactions in December 2020 and November 2021, is an example where consensus sales forecasts at deal time have been revised downward but the drug remains commercially viable with a growing patient base — impaired versus original underwriting, but not written off.

Clinical failure or IRA structural impairment: These are permanent. The capital is either written off or subject to an ongoing haircut that cannot be undone by market improvement. These are the deals that define the worst outcomes in the 2021 cohort. Gantenerumab and otilimab — both 2021-era positions, both from the same MorphoSys transaction — represent the clean version of this failure mode.

The Omecamtiv Mecarbil situation represents a more expensive version: capital not written off but locked in a multi-year restructuring that consumes management attention and additional funding while the original thesis waits for a second chance.

A reasonable estimate, based on the clinical failure rates of development-stage assets, the IRA exposure profile of 2021-era royalty targets, and the commercial performance data now available for 2021-vintage drugs: approximately 35–45% of major 2021 deals face some form of meaningful economic impairment versus original underwriting assumptions, across all three categories.

What the Market Has Learned: The Post-2022 Deal

The royalty finance market has responded to 2021's lessons with measurable structural changes.

Per the Gibson Dunn Royalty Finance Report 2020–2024, milestone-heavy transactions have grown significantly — buyers paying less upfront and tying additional capital deployment to clinical and commercial success points. Synthetic royalty structures, which include stronger downside protections and more bespoke cash flow architecture, grew at 33% compound annual growth rate over the five-year period.

The market's structural evolution is evident in recent large transactions. Royalty Pharma's $250M agreement with Zymeworks in March 2026 — structured as a non-recourse royalty-backed note against Ziihera's worldwide royalties — reflects the increasingly sophisticated deal architecture now standard in the market. The key features that distinguish post-2022 deals from their 2021 predecessors:

- Higher entry discount rates: 10–12% vs. 6–8% in 2021

- Milestone-contingent tranches: Capital deployed in stages against clinical/commercial success

- IRA haircuts baked in: Revenue models now explicitly discount IRA-eligible products

- Conservative peak sales assumptions: 2021 consensus forecasts have been systematically revised downward

- Stronger spring mechanisms: More deals include underperformance triggers, catch-up provisions, and reversion features (see our analysis of spring-loaded clauses)

Implications Across Stakeholders

For royalty fund LPs: NAV marks from 2021-vintage funds deserve scrutiny. The question is not only whether the drugs are performing but what discount rate is being used to value the portfolio. A fund applying 2021-era discount rates to 2021 assets is carrying paper valuations that do not reflect current market conditions. The shift in investor focus toward DPI over TVPI that characterizes broader private equity in 2024–2025 applies equally to royalty funds: realized cash matters more than modeled future value.

For biotech companies seeking royalty financing today: The market is disciplined but active. Royalty financing volume recovered to approximately $14 billion annually in 2024, and the secular drivers remain intact — 85% of approved drugs now originate from emerging biopharma, creating an ever-growing pool of royalty streams. Companies that structure deals thoughtfully — milestone tranches, tiered rates with caps, IRA-adjusted projections — will find competitive capital. Those seeking 2021-era terms will not.

For secondary market buyers: The 2021 vintage creates a genuine secondary opportunity. Funds that deployed heavily in 2021 and face LP pressure for distributions may accept secondary pricing below carrying value. The bid-ask spread reflects the ongoing discount rate disagreement — but in a normalizing rate environment, that gap is slowly closing. HCRx's recent $3 billion majority acquisition by KKR signals that institutional capital sees long-term value in royalty platforms even through the vintage year adjustment.

For the market overall: The secular thesis is intact. Royalty financing volume grew at 45% CAGR over 2018–2022 as an alternative to dilutive equity. The drivers — innovation-led biopharma, non-dilutive capital demand, institutional appetite for yield with pharma credit — have not changed. The 2021 lesson is about price discipline and rate sensitivity, not about the asset class itself.

Conclusion

The vintage year problem in pharma royalty funds is real, but it is not uniformly distributed. 2021 is the most challenged cohort because it concentrated every adverse factor simultaneously: minimum entry discount rates, maximum competitive pressure, peak biotech valuations, and optimistic revenue forecasts — all right before the most aggressive rate hiking cycle in four decades.

2022 is a secondary problem vintage, partially masked by the fact that its challenges are less extreme and its deal structures began improving mid-cycle. 2023 and beyond represent a genuine recalibration: higher entry rates, more conservative underwriting, better deal architecture, and sellers negotiating from a weaker position.

The distinguishing feature of royalty instruments, versus shorter-duration private capital strategies, is that the pain arrives slowly and heals slowly. A challenged buyout can exit in four years. A royalty tied to a drug with ten years of patent life remaining must navigate an extended mark-to-market period before cash flows either vindicate or condemn the original thesis.

For the 2021 cohort, the answer will be written over the next five to eight years — one royalty payment at a time. For new entrants who priced deals in that environment without the structural protections and conservative assumptions now considered market-standard, the vintage year problem will be a defining chapter in how the royalty finance industry learned to price long-duration assets in a world where interest rates can, and do, move.

All information in this article is accurate as of March 2026 and is derived from publicly available sources including company SEC filings, press releases, financial research reports, and industry data. Information may have changed since publication. I am not a lawyer or financial adviser. Nothing in this article constitutes investment, legal, or financial advice.

Member discussion