The Weekly Term Sheet (2026-W27)

The week in numbers

June 28 to July 3, 2026: four acquisitions (Zymeworks with Theravance ~$929M, Ipsen with Kartos $450M upfront, Ipsen with Memo Therapeutics EUR 200M upfront, United Therapeutics with Thymmune $140M upfront), one medtech divestiture (Pacira with Zimmer Biomet, up to $140M), one all-stock reverse-merger closing (Liminatus with InnocsAI, ~$320M implied),

one medtech CDMO acquisition (Kimball with Helvoet, EUR 90M), one biologics manufacturing divestiture (MacroGenics with Bora, $122.5M), one continuous-glucose-monitoring letter of intent (ALR Technologies with CGM Medical Technology), two M&A completions (Aptose with Hanmi, Aurobindo with Lannett),

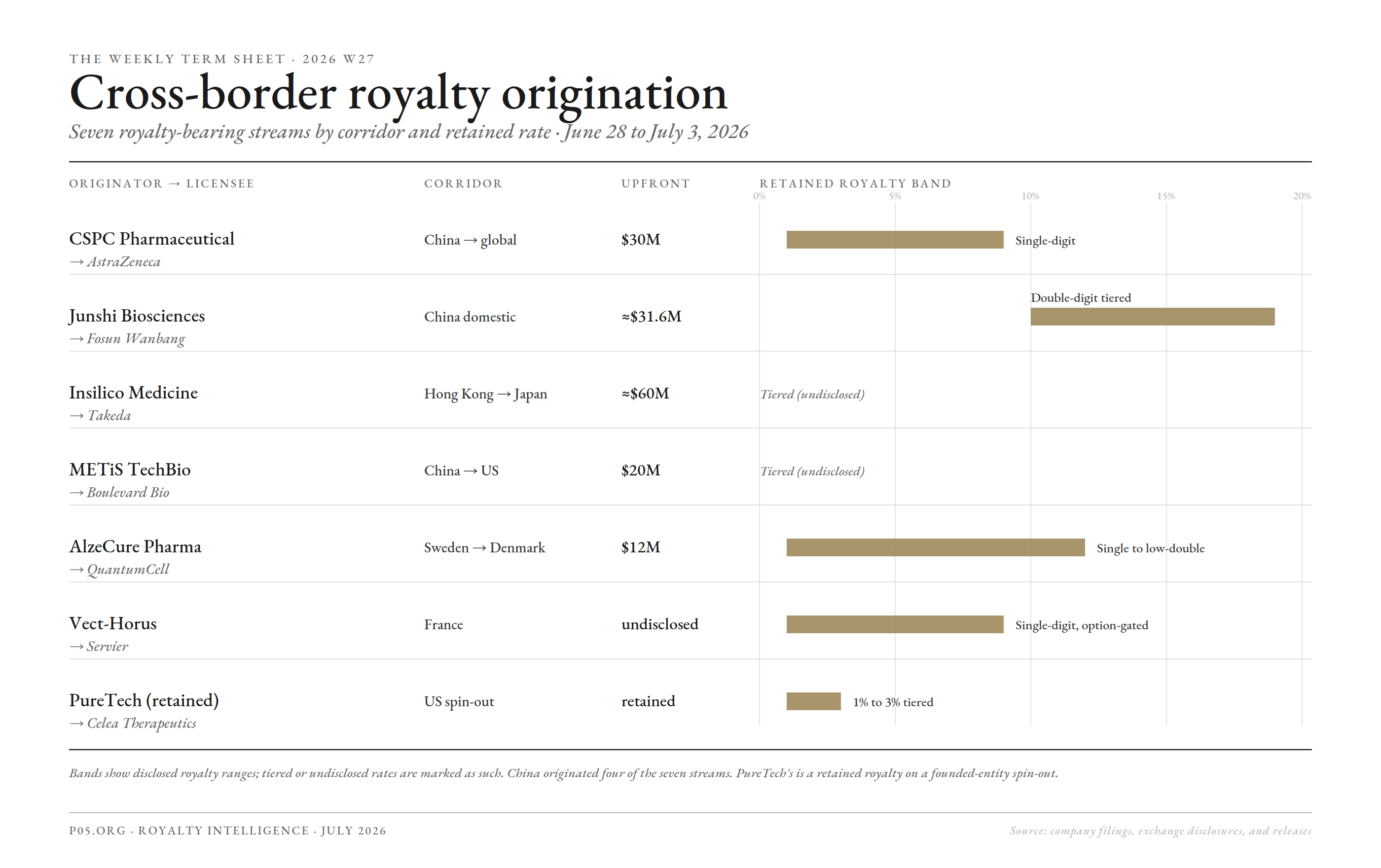

seven royalty-bearing originations (METiS with Boulevard Bio, AlzeCure with QuantumCell, Vect-Horus with Servier, Insilico with Takeda, CSPC with AstraZeneca, Junshi with Fosun Wanbang,

and PureTech's retained royalty on the Celea spin-out), one CDMO platform revenue-share (Lonza with Nona, undisclosed), two commercialisation handoffs (Lilly with Innovent, Orion with Shilpa Medicare), one dedicated-aggregator royalty financing (Ligand with Zerion), and one acquisition-financing facility (OMERS funding Zymeworks).

On the capital-formation and re-rate side: one de-SPAC (Talawar with JATT II ~$285M), one Hong Kong IPO (Alebund ~$164M), two royalty re-rates (AbbVie and Genmab epcoritamab, and Vertex and CRISPR's Casgevy paediatric expansion), two further label expansions on marketed assets (Novartis's Itvisma in EU SMA, Novo Nordisk's Wegovy in UK MASH), two milestone events on live stacks ($100M AbbVie to REGENXBIO, $75M DRI Healthcare to Viridian), and about $3.0B in equity financings led by BridgeBio's $1B convertible preferred, Abivax's $920M follow-on, PureTech's $180M Celea Series Seed, and Neurogene's ~$135M follow-on, plus a $27.5M Fosun strategic equity investment into AriBio, Scribe Therapeutics' up-to-$75M IPO filing, and an undisclosed Pyrotech venture round.

No standalone royalty monetisation or secondary purchase of an existing stream by a dedicated aggregator was signed in the window. The one aggregator royalty print is Ligand with Zerion (undisclosed); HealthCare Royalty's participation in the BridgeBio preferred is an equity investment, not a royalty purchase.

- Zymeworks / Theravance Biopharma (June 29): $17.00 per share cash (~$929M) plus a CVR, OMERS-financed. Acquires a 35% Yupelri profit share, an up-to-~20% Vibativ royalty, and a $100M contingent Trelegy milestone. A royalty portfolio moving via M&A. Close Q3 2026.

- Ipsen / Kartos Therapeutics (June 29): $450M upfront, up to $1.75B total; oral MDM2 inhibitor navtemadlin (Phase 3 myelofibrosis). Equity acquisition, no retained royalty. Close Q3 2026.

- Ipsen / Memo Therapeutics AG (July 1): EUR 200M upfront, over EUR 700M total (~$800M); potravitug, a first-in-class anti-BK polyomavirus antibody (Phase II complete). Ipsen's second buyout of the window; no royalty on the acquired asset. Close Q3 2026.

- United Therapeutics / Thymmune Therapeutics (July 2): $140M cash upfront, up to $300M with earn-outs to end-2031; preclinical iPSC-derived thymic cell therapy THY-100 (congenital athymia). Full acquisition, worldwide rights, no royalty or equity terms disclosed.

- Pacira BioSciences / Zimmer Biomet (June 30): up to $140M for the iovera° cryoneurolysis device ($70M upfront plus up to $70M in revenue-based milestones through 2031). A marketed medtech stream converting to a capped, synthetic-royalty-style receivable. Close Q3 2026.

- Kimball Electronics / Helvoet Polymer Technologies (closed July 1): EUR 90M (~$103M), about 9x estimated CY2026 adjusted EBITDA; a European medical CDMO (elastomer and polymer components, microfluidics, diagnostics, drug delivery) bought from Hydratec Industries, over 70% medical revenue. A differentiated medtech vertical, no royalty layer.

- Liminatus Pharma / InnocsAI (closing July 2): all-stock reverse merger, 1.6B shares at $0.20 (~$320M implied), for InnocsAI's oncology cell and biologic therapy assets, with a proceeds-based CVR. A pre-revenue Nasdaq microcap combination; no cash, no royalty layer.

- METiS TechBio / Boulevard Bio (June 30): $20M upfront, up to $1.6B, tiered royalties to METiS; preclinical trispecific TCE MTS-128 (autoimmune). A China-outbound AI-platform out-licence.

- AlzeCure / QuantumCell (July 1): USD 12M upfront (USD 5M as equity), tiered royalties (single-digit to low-double-digit), over USD 2.2B headline; NeuroRestore platform, lead ACD856. A Swedish-to-Danish out-licence.

- Vect-Horus / Servier (June 30): research evaluation and exclusive licence-option on the VECTrans blood-brain-barrier platform for Servier oligonucleotides in rare CNS disease; single-digit royalties on exercise. Terms undisclosed, option-gated.

- Lonza / Nona Biosciences (July 1): Lonza (SIX: LONN) licenses IP rights to Nona's single-domain-antibody blood-brain-barrier platform for upfront and option fees, with both sharing revenue on future third-party licences; a bilateral tech exchange (Harbour Mice HCAb for Lonza's GS and GlycoConnect systems). A CDMO-to-originator platform layer, undisclosed.

- Insilico Medicine / Takeda (July 1): AI drug-discovery collaboration on the Pharma.AI platform; ~$60M near-term, up to ~$600M, tiered royalties to Insilico, with Takeda taking exclusive worldwide rights. A Hong Kong-to-Japan forward royalty origination.

- CSPC Pharmaceutical / AstraZeneca (July 2): $30M upfront, up to $540M development and $1.2B sales milestones (~$1.77B headline), single-digit royalties to CSPC; siRNA renal-disease discovery on CSPC's platform, AstraZeneca optioning global or ex-China rights, CSPC retaining China. A China-outbound royalty origination.

- Junshi Biosciences / Fosun Wanbang (June 30): RMB 215M (~$31.6M) upfront plus development and sales milestones and double-digit tiered royalties to Junshi; Greater China rights to roconkibart (JS005, anti-IL-17A mAb, Phase 3 psoriasis). A China-domestic royalty-bearing licence.

- PureTech / Celea Therapeutics (July 2): $180M Series Seed spin-out (RA Capital, Leaps by Bayer, PureTech, a US healthcare fund, a sovereign wealth fund) plus asset transfer of deupirfenidone (LYT-100, IPF); PureTech contributes $30M, holds 35.4% fully diluted, and retains tiered royalties of 1% to 3% plus up to $190M in milestones. A retained-royalty origination on a founded-entity spin-out.

- Eli Lilly / Innovent (June 30): commercialisation-rights transfer for Verzenios (abemaciclib) in mainland China; Innovent takes sole commercialisation, Lilly stays MAH. Terms undisclosed.

- Orion Pharma / Shilpa Medicare (June 30): European commercialisation of Shilpa's in-development IV nivolumab (Opdivo) biosimilar; Orion distributes, Shilpa supplies for development and regulatory milestones. Terms undisclosed.

- Ligand / Zerion Pharma (June 30): undisclosed royalty financing plus equity on Zerion's Dispersome platform. A dedicated-aggregator royalty print.

- Talawar / JATT II (June 29): ~$285M de-SPAC ($225M PIPE, Access Biotechnology-led) to list as TLWR; preclinical anti-IL-13 x anti-IL-18 bispecific TALA-125. No royalty layer.

- Alebund Pharmaceuticals HKEX IPO (June 29): ~HK$1.283B gross (~US$164M), up ~104% on debut; a China renal-disease developer (lead AP301, hyperphosphataemia). Primary equity, no royalty layer.

- Nuvectis Pharma $100M follow-on (June 29): 5.0M shares at $20.00; funds NXP900, NXP100, NXP200 (the latter two Haisco ex-China in-licences). No royalty layer.

- Neurogene ~$134.8M follow-on (priced June 30, closed July 2): 3.5M shares at $30.00 plus pre-funded warrants, underwriter option exercised in full; up to ~$134.8M net funds NGN-401 (Rett syndrome gene therapy) into Q1 2029. No royalty layer.

- Scribe Therapeutics S-1, up to $75M (filed July 2): proposed Nasdaq IPO (SCTX) for a Phase 1 CRISPR cardiovascular biotech, lead STX-1150 using ELXR epigenetic PCSK9 silencing. No royalty on the offering, though Scribe holds an upstream royalty-bearing CRISPR licence with Lilly and Prevail.

- BridgeBio Pharma $1B convertible preferred (July 1): ~$933.9M funded at close ($800M Sixth Street, $133.9M HealthCare Royalty); 7.00% dividend, permanent equity. Funds the Attruby ramp plus three US launches. The largest financing of the week; HCRx deploys via equity, not a royalty.

- Abivax $920M follow-on (July 1 to 2): upsized $800M ADS offering priced July 1 at $125.00/ADS; greenshoe exercised in full July 2 for $920M (€807M) gross. Funds obefazimod commercialisation and development. No royalty layer.

- Flare Therapeutics $85M Series C (June 30): insider-led (Third Rock, Nextech); funds the ARON degrader FX-111. No royalty layer.

- Beeline Medicines $126.3M Series A extension (June 30): Bain, CPP Investments, BMS; funds afimetoran toward a 2H 2026 lupus readout. Pipeline in-licensed from BMS (upstream interest).

- Xellar Biosystems ~$50M round (June 29): venture financing for the 3D Bio Intelligence platform. No royalty layer.

- Fosun Pharma / AriBio $27.5M strategic equity investment (July 3): $7.5M first tranche then $20M second; Fosun becomes AriBio's third-largest shareholder. Follows May's up-to-$4.7B AR1001 global option and licence (low-double-digit royalty on exercise). Equity leg, royalty sits upstream in the licence.

- Pyrotech (Beijing) Biotechnology venture round (July 3): China pyroptosis and innate-immunity platform (co-founders Feng Shao, TJ Deng; lead ALPK1 agonist PTT-936). Round size undisclosed in accessible sources. No royalty layer.

- Smaller equity, no royalty layer: Elicio ~$15M registered direct (July 2), Cereno ~SEK 60M (June 30), and five microcaps (CollPlant, FibroBiologics, Akari, Hofseth BioCare, XTL).

- AbbVie / Genmab epcoritamab re-rate (June 29): positive Phase 3 PFS in r/r DLBCL; re-rates Genmab's 50:50 US and Japan profit share and 22% to 26% ex-US royalty on EPKINLY. No new capital.

- AbbVie / REGENXBIO $100M milestone (June 29): first patient dosed in the Phase IIb/III sura-vec diabetic retinopathy trial triggers a $100M payment to REGENXBIO on a live royalty stack; a second identical milestone to follow.

- DRI Healthcare / Viridian $75M milestone (June 29): on the Lumvoa approval, DRI pays Viridian $75M and holds a tiered US royalty (7.5% top tier) under its October 2025 synthetic royalty. An aggregator-to-originator milestone.

- Eisai / BioArctic Leqembi (June 30): a conference-data announcement (AAIC), not a discrete royalty event; BioArctic holds milestones plus a royalty on global Leqembi net sales.

- Vertex / CRISPR Casgevy paediatric expansion (July 1): FDA clears Casgevy for ages 2 and older in sickle cell disease and transfusion-dependent beta-thalassemia (via a Commissioner's National Priority Voucher), adding ~5,500 eligible US children. Re-rates the Vertex and CRISPR 60:40 profit share on a commercial asset. No new capital.

- Novartis / Itvisma EC approval (July 2): European Commission approves Itvisma (onasemnogene abeparvovec) for 5q SMA patients aged 2 and older, a broad-population label expansion on the STEER data (2.39-point HFMSE gain). Profit read-through, no new capital.

- Novo Nordisk / Wegovy MASH UK (July 3): UK MHRA grants conditional approval of semaglutide (Wegovy) in MASH with moderate-to-advanced fibrosis, a NICE appraisal ongoing for NHS access. A label expansion, no new capital.

M&A and restructuring:

- Zymeworks / Theravance Biopharma acquisition (June 29): ~$929M cash plus a CVR, OMERS-financed; a Yupelri, Vibativ, and Trelegy royalty portfolio moving via M&A

- Ipsen / Kartos Therapeutics acquisition (June 29): $450M upfront, up to $1.75B; navtemadlin in Phase 3 myelofibrosis, no retained royalty

- Ipsen / Memo Therapeutics AG acquisition (July 1): EUR 200M upfront, over EUR 700M total (~$800M); potravitug (anti-BK polyomavirus), no royalty on the asset

- United Therapeutics / Thymmune Therapeutics acquisition (July 2): $140M cash upfront, up to $300M with earn-outs to end-2031; preclinical iPSC thymic cell therapy THY-100 (congenital athymia), no royalty or equity terms disclosed

- Pacira BioSciences / Zimmer Biomet iovera° divestiture (June 30): up to $140M; a marketed medtech stream with a synthetic-royalty-style milestone tail

- Liminatus Pharma / InnocsAI all-stock merger (closing July 2): 1.6B shares at $0.20 (~$320M implied) for InnocsAI's oncology cell and biologic therapy assets, plus a proceeds-based CVR; a pre-revenue Nasdaq microcap combination, no cash, no royalty layer

- Kimball Electronics / Helvoet Polymer Technologies acquisition (closed July 1): EUR 90M (~$103M), about 9x estimated CY2026 adjusted EBITDA; a European medical CDMO in elastomer and polymer components, microfluidics, diagnostics, and drug delivery, over 70% medical revenue, no royalty layer

- MacroGenics / Bora Pharmaceuticals GMP manufacturing divestiture (closed July 2): $122.5M (before fees, subject to post-closing adjustments) for MacroGenics' Rockville, MD biologics drug-substance facility and Frederick, MD warehouse, sold to Bora Biologics USA; ~140 employees transfer alongside a long-term CDMO supply agreement; a manufacturing carve-out, no royalty layer

- Aptose Biosciences / Hanmi Pharmaceutical take-private (closing ~July 3): C$2.41 per share (~28% premium to the 30-day VWAP); moves the milestone-bearing tuspetinib (frontline AML) under Hanmi, a November 2025 deal closing

- Aurobindo Pharma USA / Lannett completion (effective June 29): Lannett becomes a wholly owned Aurobindo subsidiary after FTC clearance; US generics and specialty, no royalty layer, a prior deal now completing

- ALR Technologies SG / CGM Medical Technology letter of intent (June 30): 200M ALRT shares plus up to US$45M (a US$40M unsecured non-interest-bearing earn-out note for the Singapore entity, up to US$5M for the Shenzhen assets funded largely as 25% of free cash flow); a continuous-glucose-monitoring vertical integration, structured as an LOI (definitive agreements targeted July to August 2026), no royalty layer

Royalty-bearing license-outs and platform layers (upfront, then milestones, then royalty):

- METiS TechBio / Boulevard Bio MTS-128 out-licence (June 30): $20M upfront, up to $1.6B, tiered royalties; China-outbound AI-platform out-licence

- AlzeCure / QuantumCell NeuroRestore out-licence (July 1): USD 12M upfront, tiered royalties, over USD 2.2B headline; Swedish-to-Danish out-licence

- Vect-Horus / Servier VECTrans licence-option (June 30): CNS-delivery option; single-digit royalties on exercise, undisclosed

- Lonza / Nona Biosciences BBB platform deal (July 1): Lonza licenses IP rights to Nona's single-domain-antibody blood-brain-barrier platform for upfront and option fees, with the two sharing revenue on future third-party licences; a bilateral CDMO-to-originator platform layer, undisclosed

- Insilico Medicine / Takeda AI discovery collaboration (July 1): ~$60M near-term, up to ~$600M, tiered royalties; Hong Kong-to-Japan origination

- CSPC Pharmaceutical / AstraZeneca siRNA collaboration (July 2): $30M upfront, up to $540M development and $1.2B sales milestones (~$1.77B), single-digit royalties to CSPC; China-outbound siRNA renal origination, China rights retained

- Junshi Biosciences / Fosun Wanbang roconkibart licence (June 30): RMB 215M (~$31.6M) upfront plus milestones and double-digit tiered royalties to Junshi; Greater China rights to anti-IL-17A mAb JS005

- PureTech / Celea Therapeutics spin-out and retained royalty (July 2): $180M Series Seed plus asset transfer; PureTech retains 1% to 3% tiered royalties and up to $190M milestones on deupirfenidone (LYT-100, IPF), plus 35.4% equity

- Eli Lilly / Innovent Verzenios China commercialisation (June 30): sole China commercialisation, Lilly stays MAH; terms undisclosed

- Orion / Shilpa Medicare nivolumab biosimilar (June 30): exclusive European commercialisation; terms undisclosed

Structured finance and non-dilutive debt:

- OMERS Life Sciences / Zymeworks acquisition financing (June 29): $350M non-recourse note, 75% of Yupelri cash flows assigned

- Ligand / Zerion Pharma Dispersome royalty financing (June 30): royalty financing plus equity, undisclosed; a dedicated-aggregator royalty print

Financings:

- Talawar / JATT II de-SPAC (June 29): ~$285M ($225M PIPE); preclinical bispecific TALA-125, no royalty layer

- Alebund Pharmaceuticals HKEX IPO (June 29): ~US$164M gross, up ~104% on debut; China renal disease, no royalty layer

- BridgeBio Pharma $1B convertible preferred (July 1): ~$934M at close (Sixth Street, HealthCare Royalty); the largest financing of the week, HCRx via equity not a royalty

- Abivax $920M follow-on (July 1 to 2): upsized $800M ADS offering priced July 1 at $125.00, greenshoe exercised in full July 2 for $920M (€807M) gross; funds obefazimod. No royalty layer

- Cereno Scientific ~SEK 60M directed issue (June 30): premium-priced raise, no royalty layer

- Flare Therapeutics $85M Series C (June 30): insider-led (Third Rock, Nextech); FX-111, no royalty layer

- Beeline Medicines $126.3M Series A extension (June 30): Bain, CPP Investments, BMS; afimetoran, upstream BMS interest

- Xellar Biosystems ~$50M round (June 29): 3D Bio Intelligence platform, no royalty layer

- Fosun Pharma / AriBio $27.5M strategic equity investment (July 3): $7.5M first tranche then $20M second; Fosun becomes AriBio's third-largest shareholder, following May's AR1001 global option and licence

- Pyrotech (Beijing) Biotechnology venture round (July 3): China pyroptosis and innate-immunity platform, lead ALPK1 agonist PTT-936; round size undisclosed, no royalty layer

- Nuvectis Pharma $100M follow-on (June 29): funds NXP900, NXP100, NXP200; no royalty layer

- Elicio Therapeutics $15M registered direct (July 2): 4,380,313 shares, two new institutions plus an existing holder; funds a Phase 1 in KRAS-driven cancers. No royalty layer

- Neurogene ~$134.8M follow-on (priced June 30, closed July 2): 3.5M shares at $30.00 plus pre-funded warrants, underwriter option exercised in full for up to ~$134.8M net; funds NGN-401 (Rett syndrome gene therapy) into Q1 2029. No royalty layer

- Scribe Therapeutics S-1, up to $75M (filed July 2): proposed Nasdaq IPO (SCTX) for a Phase 1 CRISPR cardiovascular biotech, lead STX-1150 using ELXR epigenetic PCSK9 silencing to lower LDL-C; no royalty on the offering, though Scribe holds an upstream royalty-bearing CRISPR licence with Lilly and Prevail

- Microcap raises (no royalty layer): CollPlant, FibroBiologics, Akari, Hofseth BioCare, XTL; sub-$10M, warrant-heavy

Royalty re-rates (no new capital):

- AbbVie / Genmab epcoritamab EPCORE DLBCL-4 Phase 3 (June 29): positive Phase 3 PFS in r/r DLBCL; re-rates Genmab's ex-US EPKINLY royalty

- AbbVie / REGENXBIO $100M sura-vec milestone (June 29): first-patient dosing triggers $100M on a live REGENXBIO royalty stack

- Eisai / BioArctic Leqembi (June 30): AAIC data announcement, not a discrete event; BioArctic royalty on Leqembi

- DRI Healthcare / Viridian $75M Lumvoa milestone (June 29): milestone on the Lumvoa launch; DRI's tiered 7.5% US royalty now live

- Vertex / CRISPR Casgevy paediatric expansion (July 1): FDA clears Casgevy for ages 2 and older in SCD and TDT, adding ~5,500 eligible US children; re-rates the Vertex and CRISPR 60:40 profit share on a commercial asset

- Novartis / Itvisma EC approval (July 2): European Commission approves Itvisma (onasemnogene abeparvovec) for 5q SMA patients aged 2 and older on the STEER data, a broad-population label expansion; profit read-through, no new capital

- Novo Nordisk / Wegovy MASH UK authorisation (July 3): UK MHRA grants conditional approval of semaglutide (Wegovy) in MASH with moderate-to-advanced fibrosis, a NICE appraisal ongoing; a label expansion

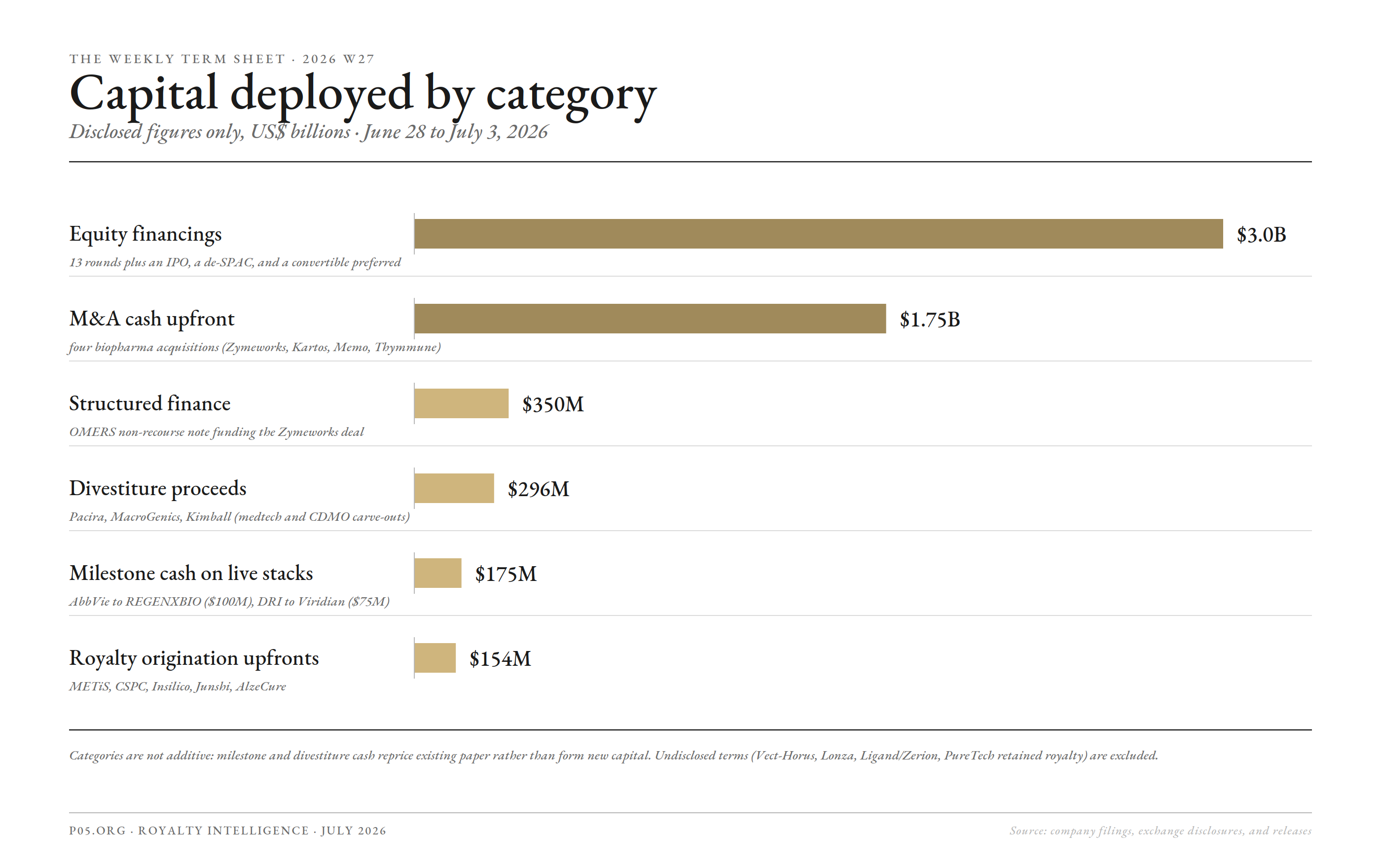

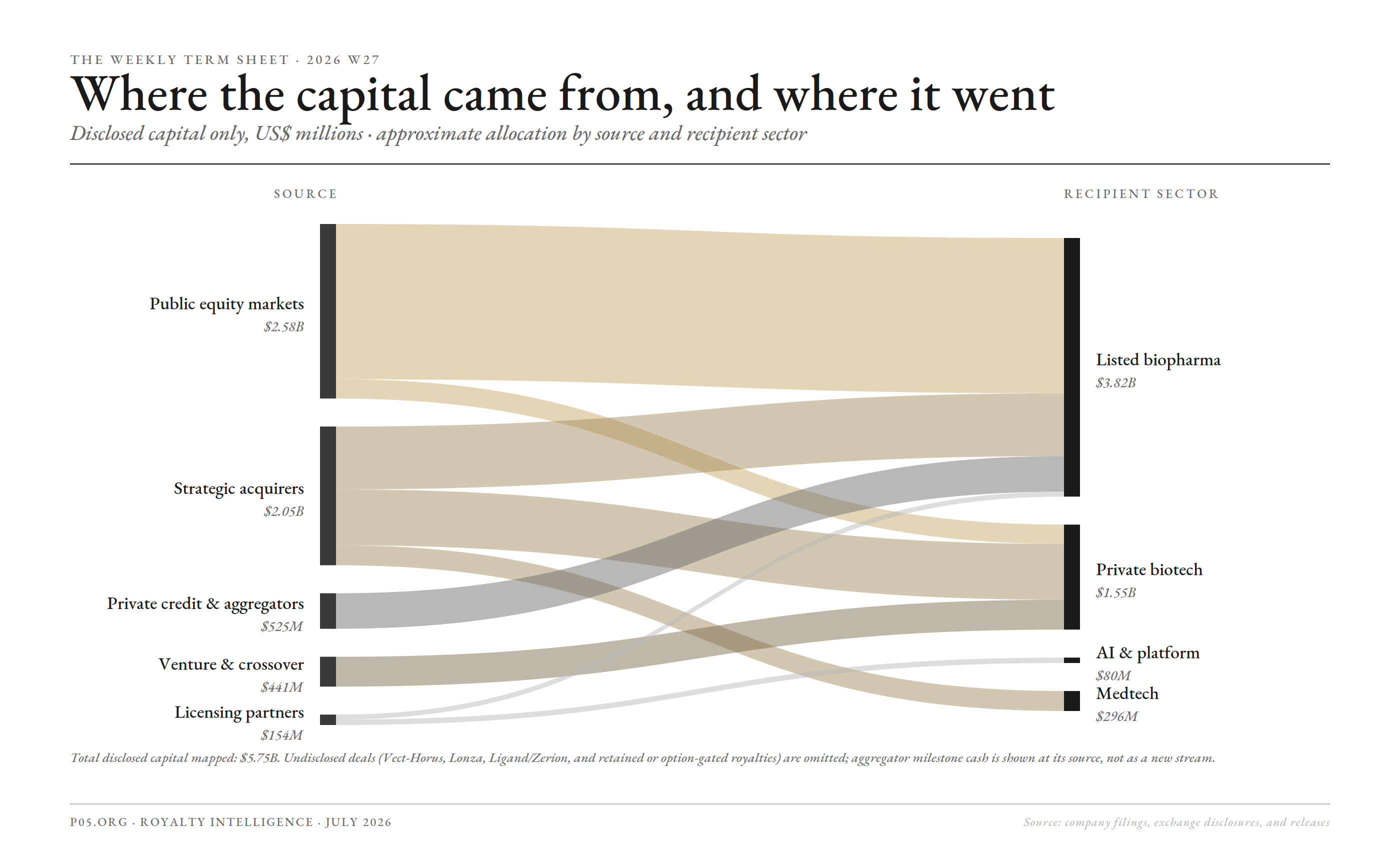

Window totals

Disclosed figures only; deals with undisclosed terms are excluded from the totals below. A six-day window (Sunday to Friday), with most deal flow in the closing three days.

- M&A cash: ~$1.75B upfront across four acquisitions (Zymeworks ~$929M, Kartos $450M, Memo EUR 200M, United Therapeutics / Thymmune $140M). Ceilings up to ~$3.78B+ with milestones. Separately, the Liminatus / InnocsAI all-stock reverse merger closed July 2 (~$320M implied, no cash, no royalty), and Kimball / Helvoet added a EUR 90M (~$103M) medtech CDMO acquisition (closed July 1, no royalty). MacroGenics divested its Rockville, MD GMP biologics manufacturing operations to Bora Pharmaceuticals for $122.5M (closed July 2, a manufacturing carve-out plus a long-term CDMO supply agreement, no royalty). ALR Technologies also signed a letter of intent for CGM Medical Technology (Singapore and Shenzhen), a continuous-glucose-monitoring vertical integration for 200M shares plus up to US$45M, structured with an earn-out and a free-cash-flow share rather than a royalty.

- Medtech divestiture: up to $140M, Pacira / Zimmer Biomet iovera° ($70M upfront plus up to $70M in revenue milestones). A synthetic-royalty-style tail.

- Royalty-bearing originations: seven forward streams. METiS ($20M upfront), AlzeCure (USD 12M), Vect-Horus (undisclosed, option-gated), Insilico / Takeda (~$60M near-term), CSPC / AstraZeneca ($30M upfront, single-digit), Junshi / Fosun Wanbang (RMB 215M ~$31.6M, double-digit tiered), and PureTech's retained 1% to 3% royalty on the Celea spin-out. All future streams, not aggregator purchases. Separately, Lonza / Nona added a CDMO-to-originator platform revenue-share on future third-party out-licences (undisclosed, not a product royalty).

- Royalty paper transferred (via M&A): the Zymeworks / Theravance deal moves a 35% Yupelri profit share and an up-to-~20% Vibativ royalty, plus a one-time $100M Trelegy milestone. The running Trelegy royalty stays with RPRX.

- Re-rates and milestone cash: epcoritamab re-rated (Genmab 50:50 US and Japan, 22% to 26% ex-US royalty), and Casgevy re-rated on its FDA paediatric expansion to ages 2 and older (Vertex and CRISPR 60:40 profit share); plus label expansions on marketed assets for Novartis's Itvisma (EU 5q SMA) and Novo Nordisk's Wegovy (UK MASH), and $100M AbbVie to REGENXBIO and $75M DRI to Viridian, both on live stacks. BioArctic and Leqembi are flagged ahead of AAIC.

- Structured finance: two prints. OMERS $350M non-recourse note (funds the Zymeworks deal); Ligand royalty financing of Zerion's Dispersome platform (undisclosed).

- Equity financings: ~$3.0B, led by BridgeBio's ~$934M convertible preferred, Abivax's $920M follow-on (full greenshoe), and PureTech's $180M Celea Series Seed. Then Talawar ~$285M, Alebund ~$164M, Neurogene ~$135M, Beeline $126.3M, Nuvectis $100M, Flare $85M, Xellar ~$50M, Fosun / AriBio $27.5M, Elicio ~$15M, Cereno ~$6M, Pyrotech (undisclosed), and five microcaps. Scribe Therapeutics filed an up-to-$75M IPO S-1 (not yet priced). No royalty origination on the raises themselves; PureTech's is the exception, carrying its retained Celea royalty.

- Aggregator royalty originated: one (Ligand / Zerion, undisclosed). No secondary stream purchase by Royalty Pharma, HealthCare Royalty, or Blackstone this window; HCRx's BridgeBio stake is equity, not a royalty buy.

- Closings (prior deals): SERB completed its €115M acquisition of European and MENA Idefirix (imlifidase) rights from Hansa Biopharma (July 1; a May 2026 licensing and rights transfer). Hanmi completed its C$2.41-per-share take-private of Aptose (TSX delisting ~July 3), moving the milestone-bearing tuspetinib under Hanmi. Aurobindo Pharma USA completed its $250M acquisition of Lannett (effective June 29, post-FTC, with a four-product divestiture to Quagen). None is a new origination.

M&A and Restructuring

Zymeworks / Theravance Biopharma: Royalty-Portfolio Acquisition, ~$929M Plus a CVR (Mon June 29)

Zymeworks Inc. (Nasdaq: ZYME; Vancouver, BC) entered a definitive agreement to acquire Theravance Biopharma, Inc. (Nasdaq: TBPH; Dublin, Ireland) for $17.00 per share in cash, an equity value of about $929M, plus a contingent value right on ampreloxetine (BioSpace; Theravance release; Zymeworks release).

The $17.00 price is a 22% premium to Theravance's March 3, 2026 close (the day it disclosed the ampreloxetine CYPRESS Phase 3 failure) and a 10% premium to its volume-weighted average since, but about a 4% discount to the prior Friday's close. Zymeworks announced a November 2025 pivot to a royalty-driven model around lead asset Ziihera; closing is targeted for H2 2026, subject to a Theravance shareholder vote and HSR clearance, with matching $32.515M termination and reverse-termination fees.

Yupelri (revefenacin), the only nebulised LAMA approved in the US, is the durable asset: a 35% Theravance profit share (~$60M to $70M a year). The Trelegy line is a one-time $100M RPRX milestone, not a running royalty; Vibativ (up to ~20% from Cumberland) is the one running royalty; and a CVR routes 80% of any future ampreloxetine proceeds to legacy holders. Terms in the table below.

| Term | Detail |

|---|---|

| Acquirer | Zymeworks Inc. (Nasdaq: ZYME; Vancouver, BC; pivoting to a royalty-driven model around Ziihera) |

| Target | Theravance Biopharma, Inc. (Nasdaq: TBPH; Dublin, Ireland; Strategic Review Committee advised by Lazard) |

| Structure | $17.00 per share in cash (about $929M equity value) plus a CVR; 22% premium to the March 3, 2026 post-CYPRESS close, about a 4% discount to the prior Friday |

| Financing | A $350M non-dilutive, non-recourse note from OMERS Life Sciences, with 75% of Yupelri profit-share cash flows contractually assigned to OMERS to service the debt; secured on Theravance's Yupelri-related assets; merger not conditioned on financing; $32.515M termination and reverse-termination fees |

| Approved asset | Yupelri (revefenacin): nebulised LAMA for COPD; 35% Theravance economic interest under a Viatris profit-share; $266.6M 2025 US net sales (up 12%); ~$60M to $70M annualised cash flow; up to $125M US commercial milestones plus royalties |

| Trelegy interest | A single $100M contingent milestone receivable from Royalty Pharma, expected Q1 2027, gated on GSK's 2026 Trelegy net-sales thresholds. The underlying TRC royalty (6.5% to 10%) was already sold to RPRX in 2022 to 2023; Theravance monetised its outer-year residual for $225M in 2025 |

| Vibativ royalty | Up to ~20% on net sales of Vibativ (telavancin) from Cumberland; the one running royalty in the package |

| CVR | 80% of net proceeds from any future ampreloxetine licence, divestiture, or monetisation over ten years to legacy Theravance shareholders; 20% to Zymeworks |

| Other | ~$2.5B in Irish tax attributes; R&D assets retained for potential externalisation |

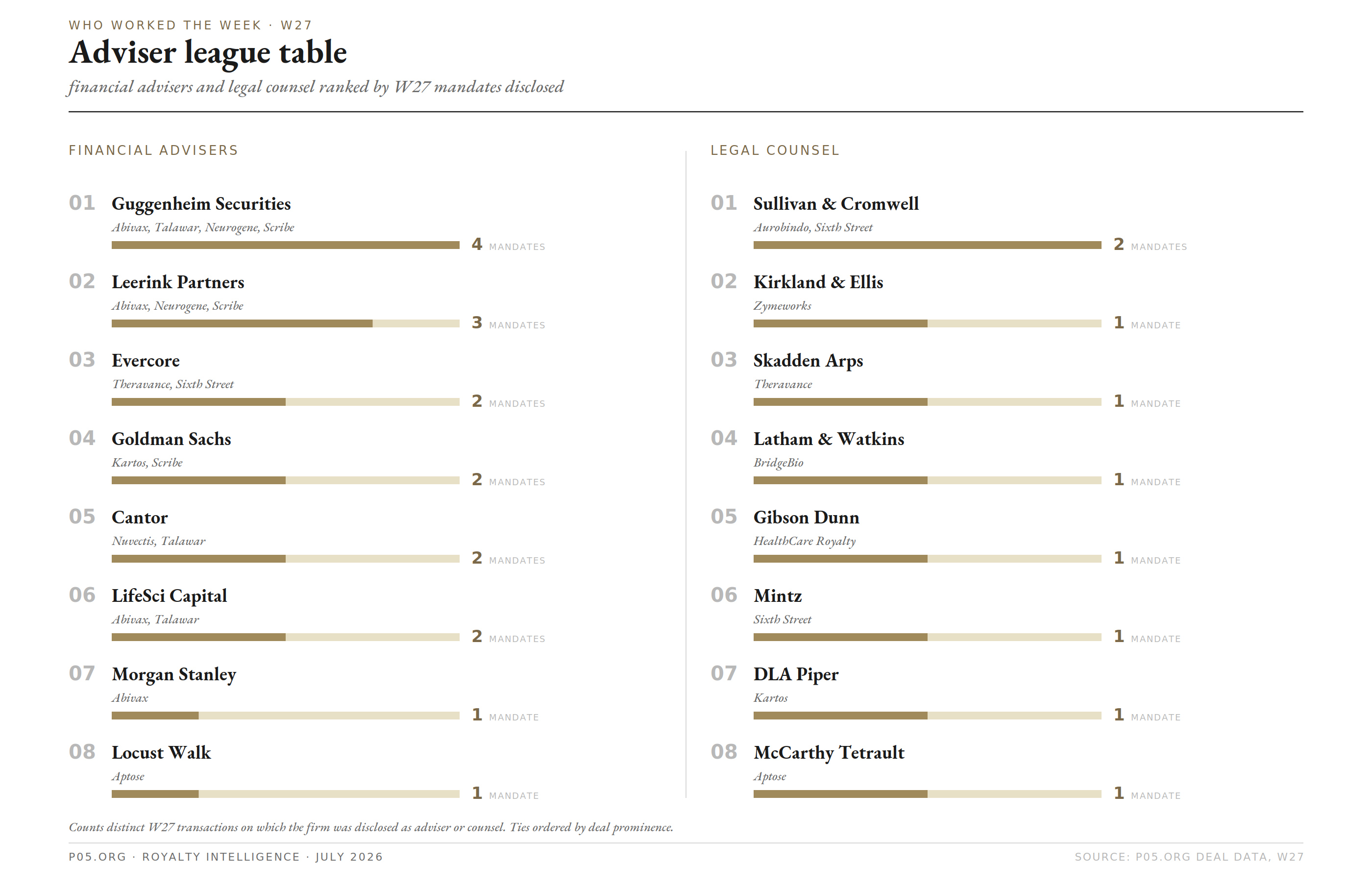

| Advisers | Zymeworks: TD Cowen and MTS Health Partners (financial; TD Cowen on the OMERS royalty note), Kirkland & Ellis (legal), Matheson (Irish tax). Theravance: Lazard (lead financial) and Evercore (financial), Skadden Arps (legal). OMERS Life Sciences: Sidley Austin (legal), Maples and Calder (Ireland) and Davies Ward Phillips & Vineberg (Irish counsel) |

| Date | Mon June 29, 2026 |

Ipsen / Kartos Therapeutics: Navtemadlin Myelofibrosis Acquisition, Up to $1.75B (Mon June 29)

Ipsen (Euronext Paris: IPN) entered a definitive agreement to acquire Kartos Therapeutics, Inc. (Redwood City, CA; clinical-stage), for $450M upfront and up to $1.3B in further payments including a significant regulatory-approval milestone and sales-based commitments, up to $1.75B total (BioSpace).

The centrepiece is navtemadlin, an oral MDM2 inhibitor in Phase 3 (POIESIS, 600+ patients) as a ruxolitinib add-on for high-risk myelofibrosis, with a potential 2028 launch. Navtemadlin (AMG-232 / KRT-232) was in-licensed from Amgen in the 2016 agreement that founded Kartos, so an undisclosed upstream Amgen royalty and a Tempus companion-diagnostic collaboration travel with the asset.

| Term | Detail |

|---|---|

| Acquirer | Ipsen (Euronext Paris: IPN; CEO David Loew) |

| Target | Kartos Therapeutics, Inc. (Redwood City, CA; clinical-stage; advisers Goldman Sachs and PJT Partners) |

| Structure | Equity acquisition; $450M upfront plus up to $1.3B in milestones (up to $1.75B total) |

| Asset | Navtemadlin (AMG-232 / KRT-232): oral MDM2 inhibitor restoring p53 activity |

| Lead indication / stage | High-risk myelofibrosis, ruxolitinib add-on; Phase 3 POIESIS (600+ patients, 250+ sites); potential launch as early as 2028 |

| Upstream economics | An Amgen royalty from the 2016 founding license travels with the asset; a Tempus CDx collaboration also travels |

| Condition / timing | Subject to HSR clearance; closing targeted Q3 2026; accretive to Ipsen core operating income from 2029 |

| Royalty | No retained Kartos royalty; an undisclosed upstream Amgen royalty (2016 founding license) travels with navtemadlin |

| Advisers | Ipsen: Orrick Herrington & Sutcliffe (legal); no financial adviser disclosed. Kartos: Goldman Sachs and PJT Partners (UK) (financial), DLA Piper (legal) |

| Date | Mon June 29, 2026 |

Ipsen / Memo Therapeutics AG: Potravitug BK Polyomavirus Acquisition, Over EUR 700M (Wed July 1)

Ipsen (Euronext Paris: IPN) entered a definitive share purchase agreement to acquire all issued and outstanding shares of Memo Therapeutics AG (Schlieren / Zurich, Switzerland; private, late-stage antibody company), a second Ipsen buyout in the same week after Kartos (Ipsen release).

Shareholders receive EUR 200M at close on a cash-free, debt-free basis, plus over EUR 500M in deferred development, regulatory-approval, and sales-based milestones, for a total potential consideration in excess of EUR 700M (about $800M).

The asset is potravitug, a first-in-class human monoclonal antibody neutralising BK polyomavirus (BKPyV) in kidney transplant recipients, a serious and frequent post-transplant infection with no targeted approved treatment. The totality of evidence from the Phase II SAFE KIDNEY II trial (90 US patients) supports a pivotal Phase II/III start later in 2026.

Potravitug was discovered on Memo's proprietary DROPZYLLA antibody-discovery platform, so no upstream third-party running royalty travels with it. As a condition precedent to closing, all Memo assets and employees unrelated to potravitug, including the DROPZYLLA platform, the oncology programs, the Ono collaboration,

and the February 2026 CSL recombinant-polyclonal-IgG option (up to CHF 265M, single-digit royalty), transfer to a newly incorporated company, Memorises Bio, retained by existing Memo shareholders. Kurma Partners co-led the May 2024 Series C extension; other backers include Ysios Capital, Pureos Bioventures, Swisscanto, Vesalius Biocapital, and Adjuvant Capital.

| Term | Detail |

|---|---|

| Acquirer | Ipsen (Euronext Paris: IPN; CEO David Loew) |

| Target | Memo Therapeutics AG (Schlieren / Zurich, Switzerland; private, late-stage antibody company) |

| Structure | Share purchase; EUR 200M upfront (cash-free, debt-free at close) plus over EUR 500M in milestones, over EUR 700M total (about $800M) |

| Asset | Potravitug: first-in-class human anti-BK polyomavirus (BKPyV) neutralising antibody |

| Lead indication / stage | BKPyV-associated nephropathy in kidney transplant recipients; Phase II SAFE KIDNEY II complete, pivotal Phase II/III to start later in 2026; up to ~$2B peak-sales potential |

| Carve-out | Non-potravitug assets and employees, including the DROPZYLLA platform, oncology programs, the Ono collaboration, and the CSL option-to-license, transfer to Memorises Bio, a NewCo retained by existing Memo shareholders |

| Condition / timing | Subject to customary closing conditions; closing targeted Q3 2026; impact factored into Ipsen's full-year guidance |

| Royalty | No royalty on the acquired asset (potravitug homegrown on DROPZYLLA); the one live royalty tail (CSL option, single-digit royalty) stays with the seller-retained Memorises Bio |

| Advisers | Ipsen: Bredin Prat (Paris) and Lenz & Staehelin (Switzerland) (legal); no financial adviser disclosed. Memo: Centerview Partners (financial), Goodwin (London) and Baker McKenzie (Switzerland) (legal) |

| Date | Wed July 1, 2026 |

Pacira BioSciences / Zimmer Biomet: iovera° Cryoneurolysis Divestiture, Up to $140M (Tue June 30)

Pacira BioSciences (Nasdaq: PCRX) agreed to divest its iovera° cryoneurolysis device business to Zimmer Biomet (NYSE: ZBH) for up to $140M: $70M upfront plus up to $70M in revenue-based milestones (Pacira 8-K via Stock Titan; MassDevice). Zimmer Biomet acquires all rights to develop, manufacture, and commercialise iovera°, an FDA-cleared, drug-free focused-cold nerve-block device.

The milestone tail is structured as revenue thresholds: tranches of $18.5M, $23.5M, or $28.0M if annual iovera° net revenue reaches $50.0M, $60.0M, or $70.0M in any year from 2027 to 2031. The companies will also collaborate on a spasticity program, with Pacira eligible for incremental compensation contingent on a successful registrational study and regulatory approval. iovera° grew about 6% to $24.2M in 2025 net sales; Pacira originally obtained it through its 2019 Myoscience acquisition (~$220M). About 66 employees (~8% of Pacira's workforce) are expected to transfer; RBC Capital Markets advised Pacira, which will apply the upfront to pay down its senior secured revolving credit facility.

| Term | Detail |

|---|---|

| Seller | Pacira BioSciences (Nasdaq: PCRX; adviser RBC Capital Markets) |

| Acquirer | Zimmer Biomet (NYSE: ZBH) |

| Structure | Asset divestiture; $70M upfront plus up to $70M in revenue-based milestones (up to $140M) |

| Asset | iovera°: FDA-cleared, drug-free focused-cold cryoneurolysis nerve-block device |

| Milestone tail | Tranches of $18.5M / $23.5M / $28.0M as annual iovera° net revenue reaches $50M / $60M / $70M in any year 2027 to 2031; plus contingent spasticity-program compensation on a successful registrational study and approval |

| Base revenue | iovera° net sales ~$24.2M in 2025 (up ~6%); acquired by Pacira via the 2019 Myoscience deal (~$220M) |

| Condition / timing | Closing targeted Q3 2026; ~66 Pacira employees expected to transfer; upfront applied to Pacira's revolver |

| Royalty | No running royalty; the revenue-based milestone tail functions as a capped synthetic royalty on iovera° net sales through 2031 |

| Advisers | Pacira: RBC Capital Markets (exclusive financial), Perkins Coie (legal). Zimmer Biomet: Ice Miller (legal); no financial adviser disclosed |

| Date | Tue June 30, 2026 |

United Therapeutics / Thymmune Therapeutics: iPSC Thymic Cell-Therapy Acquisition, Up to $300M (Thu July 2)

United Therapeutics (Nasdaq: UTHR) acquired privately held, preclinical-stage Thymmune Therapeutics in a full acquisition of worldwide rights to all Thymmune assets (United Therapeutics via Business Wire; BioSpace).

United Therapeutics paid $140M in cash upfront, subject to post-closing adjustments, plus earn-out payments to former Thymmune equityholders of up to $160M tied to clinical and regulatory milestones by the end of 2031, for up to $300M total.

The lead asset, THY-100, is in preclinical development for congenital athymia, an ultra-rare condition in which infants are born without a functional thymus; Thymmune's proprietary process converts iPSCs into thymic cells that can restore healthy T-cell function. The acquisition extends United Therapeutics' organ-manufacturing and immunomodulatory platform into thymic regenerative medicine, complementing its UThymoKidney xenotransplantation programme.

No royalty terms or equity components were disclosed, so no royalty travels with the asset; it is a straight M&A cash acquisition alongside the two Ipsen buyouts.

| Term | Detail |

|---|---|

| Acquirer | United Therapeutics (Nasdaq: UTHR; organ alternatives and regenerative medicine; ~$1.28B cash at March 31, 2026) |

| Target | Thymmune Therapeutics, Inc. (private, preclinical; founder and CEO Stan Wang) |

| Structure | Full acquisition of worldwide rights; $140M cash upfront (post-closing adjustments) plus up to $160M earn-out by end-2031, up to $300M total |

| Asset | THY-100: iPSC-derived thymic cell therapy generating an in vivo neo-thymus |

| Lead indication / stage | Congenital athymia; preclinical; broader potential in transplant tolerance and immune-mediated disease |

| Royalty | None disclosed; no royalty or equity terms travel with the acquired asset |

| Strategic fit | Complements UThymoKidney and UHeart xenotransplantation programmes; adds a cellular immunology layer for post-transplant tolerance |

| Advisers | Not disclosed by either party |

| Date | Thu July 2, 2026 |

Liminatus Pharma / InnocsAI: All-Stock Reverse Merger, ~$320M Implied (Closing Thu July 2)

Liminatus Pharma (Nasdaq: LIMN), a pre-revenue clinical microcap, amended its merger agreement with InnocsAI to close ahead of stockholder approval, issuing 1,600,000,000 shares at $0.20 (about $320M implied) for InnocsAI's oncology cell and biologic therapy assets, with a proceeds-based contingent value right (BioSpace).

| Term | Detail |

|---|---|

| Listco | Liminatus Pharma (Nasdaq: LIMN; pre-clinical, pre-revenue) |

| Target | InnocsAI (oncology cell and biologic therapy assets) |

| Consideration | All-stock: 1,600,000,000 shares at $0.20 (~$320M implied); a proceeds-based CVR |

| Cash / royalty | No cash; no royalty layer |

| Advisers | Not disclosed |

| Date | Closing Thu July 2, 2026 |

Kimball Electronics / Helvoet Polymer Technologies: European Medical CDMO Acquisition, EUR 90M (Closed Wed July 1)

Kimball Electronics, Inc. (Nasdaq: KE; Jasper, IN) acquired Helvoet Polymer Technologies B.V. (Alken, Belgium) and its Indian affiliate Helvoet Rubber & Plastics Technologies from Hydratec Industries N.V. (Euronext Amsterdam) for EUR 90M (~$103M), about 9x Helvoet's estimated calendar-2026 adjusted EBITDA, funded with cash and existing credit lines with roughly EUR 1.8M held in escrow (Business Wire; Kimball 8-K via Stock Titan).

Helvoet is a medical contract development and manufacturing specialist in elastomer and polymer components, microfluidics, diagnostics, and drug delivery, with about $56M in calendar-2025 revenue, a mid-teens EBITDA margin, and over 70% of revenue from medical customers. The deal extends Kimball's medical manufacturing platform into higher-margin proprietary components. No royalty layer. Advisers: MP Corporate Finance (Helvoet), Roth Capital Partners (Kimball).

| Term | Detail |

|---|---|

| Acquirer | Kimball Electronics, Inc. (Nasdaq: KE; Jasper, IN) |

| Target | Helvoet Polymer Technologies B.V. (Alken, Belgium) plus Helvoet Rubber & Plastics Technologies (India), from Hydratec Industries N.V. |

| Structure | Cash acquisition, EUR 90M (~$103M), ~9x estimated CY2026 adjusted EBITDA; ~EUR 1.8M escrow |

| Target profile | Medical CDMO: elastomer and polymer components, microfluidics, diagnostics, drug delivery; ~$56M CY2025 revenue, mid-teens EBITDA margin, >70% medical revenue |

| Royalty | None |

| Advisers | MP Corporate Finance (Helvoet); Roth Capital Partners (Kimball) |

| Date | Closed Wed July 1, 2026 |

MacroGenics / Bora Pharmaceuticals: GMP Biologics Manufacturing Divestiture, $122.5M (Closed Thu July 2)

MacroGenics, Inc. (Nasdaq: MGNX; Rockville, MD) completed the sale of its GMP drug-substance manufacturing operations to Bora Pharmaceuticals (TWSE: 6472; OTCQX: BORAY), through Bora's wholly owned subsidiary Bora Biologics USA, LLC, for total consideration of $122.5M before transaction fees and subject to customary post-closing adjustments (MacroGenics via GlobeNewswire; Stock Titan).

The transaction covers MacroGenics' Rockville, Maryland biologics drug-substance facility and its Frederick, Maryland warehouse, with about 140 MacroGenics employees hired by Bora. The parties simultaneously entered a long-term CDMO service agreement under which Bora provides process development and drug-substance production for MacroGenics' pipeline; with the close, Bora Biologics operates about 20,000 litres of single-use bioreactor capacity across Rockville, MD and San Diego, CA plus a Taiwan development site.

A manufacturing carve-out that converts an in-house cost base into an outsourced supply relationship; no royalty or profit-share attaches to the sale, and MacroGenics' partnered royalty economics are unaffected.

| Term | Detail |

|---|---|

| Seller | MacroGenics, Inc. (Nasdaq: MGNX; Rockville, MD) |

| Acquirer | Bora Pharmaceuticals (TWSE: 6472; OTCQX: BORAY), via Bora Biologics USA, LLC |

| Structure | Asset sale; $122.5M total consideration (before fees, subject to post-closing adjustments) plus a long-term CDMO supply agreement |

| Assets | Rockville, MD biologics drug-substance facility and Frederick, MD warehouse; ~140 employees transfer to Bora |

| Strategic fit | Adds a second active US drug-substance site for Bora Biologics (~20,000 L single-use capacity across Rockville, MD and San Diego, CA, plus a Taiwan development site) |

| Royalty | None; a manufacturing carve-out, MacroGenics' partnered royalty streams unaffected |

| Advisers | Not disclosed by either party |

| Date | Closed Thu July 2, 2026 |

Aptose Biosciences / Hanmi Pharmaceutical: Tuspetinib Take-Private (Closing ~Fri July 3)

Hanmi Pharmaceutical (KRX: 128940) completed its take-private of Aptose Biosciences (San Diego and Toronto) at C$2.41 per share, a roughly 28% premium to Aptose's 30-day VWAP, with the TSX delisting expected on or about July 3, 202

6. First announced November 19, 2025 and amended in February 2026, the deal cleared Aptose shareholders and a final court order on March 31, 2026 and Korean regulatory review (Aptose via BioSpace). It moves the milestone-bearing tuspetinib (a myeloid kinase inhibitor in frontline AML) fully under Hanmi. A 2025 transaction now completing.

| Term | Detail |

|---|---|

| Acquirer | Hanmi Pharmaceutical (KRX: 128940) |

| Target | Aptose Biosciences (San Diego / Toronto) |

| Structure | Take-private, C$2.41 per share (~28% premium to 30-day VWAP); TSX delisting ~July 3 |

| Timeline | Announced Nov 19, 2025; amended Feb 2026; shareholder and court approval Mar 31, 2026; Korean clearance received |

| Asset | Tuspetinib: myeloid kinase inhibitor, frontline AML (milestone-bearing) |

| Royalty | None disclosed; asset moves under Hanmi |

| Advisers | Aptose (Special Committee and Company): Locust Walk (financial adviser and independent valuator), McCarthy Tétrault (legal). Hanmi Purchaser: Stikeman Elliott (legal) |

| Date | Closing ~Fri July 3, 2026 |

Aurobindo Pharma USA / Lannett: US Generics Acquisition Completion (Effective Mon June 29)

Aurobindo Pharma USA completed its acquisition of Lannett Company (from Lannett Seller Holdco) for $250M on a cash-free, debt-free basis, with Lannett becoming a wholly owned subsidiary (renamed Lannett Company LLC), after US Federal Trade Commission clearance on June 18, 2026 that required divesting four generic products (to Quagen), effective June 29, 2026 (Drug Store News). Sullivan & Cromwell advised Aurobindo (legal); the seller's advisers were not disclosed. A US generics and specialty combination; no royalty layer, a prior deal now completing.

ALR Technologies SG / CGM Medical Technology: Continuous Glucose Monitoring Vertical Integration, Letter of Intent (Tue June 30)

ALR Technologies SG (OTC: ALRTF), a diabetes-management company, signed a letter of intent to acquire 100% of CGM Medical Technology Singapore and the assets of CGM Medical Technology Shenzhen, bringing in-house the continuous glucose monitor technology behind its GluCurve Pet CGM and a planned human CGM. A diagnostics and medtech vertical integration, structured as a letter of intent rather than a definitive agreement, with an earn-out and a free-cash-flow share rather than a product royalty.

| Term | Detail |

|---|---|

| Acquirer | ALR Technologies SG (OTC: ALRTF; diabetes management; Chairman and CEO Sidney Chan) |

| Target | CGM Medical Technology Singapore (100% equity) and CGM Medical Technology Shenzhen (assets) |

| Structure | Letter of intent, not yet definitive; aggregate 200,000,000 ALRT ordinary shares plus up to US$45M |

| Consideration detail | Singapore: 200M shares plus a US$40M unsecured, non-interest-bearing earn-out promissory note. Shenzhen: up to US$5M (about US$1M at closing, up to US$4M paid as 25% of ALRT free cash flow), gated on reaching 300,000 CGMs per month capacity |

| Asset | Continuous glucose monitor IP and manufacturing for the GluCurve Pet CGM and a planned human CGM |

| Royalty | None; the contingent consideration is an earn-out and a free-cash-flow share, not a product royalty |

| Timeline | Definitive agreement for Singapore targeted by July 31, 2026 (completion ~Aug 31); Shenzhen by Aug 31, 2026 (completion ~Jan 31, 2027) |

| Advisers | Not disclosed |

| Date | Tue June 30, 2026 |

Royalty-Bearing License-Outs and Platform Layers

METiS TechBio / Boulevard Bio: MTS-128 Trispecific TCE Global Out-Licence, Up to $1.6B (Tue June 30)

METiS TechBio (HKEX: 7666; Hong Kong and Shanghai; AI-driven drug-design and delivery company, listed May 13, 2026) entered an exclusive global licensing agreement granting Boulevard Bio (US; backed by Deerfield Management) worldwide development, manufacturing, and commercialisation rights to MTS-128, a proprietary trispecific T-cell engager for autoimmune disease developed on METiS's NanoForge platform (PR Newswire).

MTS-128 is a preclinical, AI-designed three-target binder; $20M upfront, up to $1.6B, tiered royalties to METiS. A US-China cross-border deal amid heightened scrutiny of outbound technology transfers.

| Term | Detail |

|---|---|

| Licensor / originator | METiS TechBio (HKEX: 7666; Hong Kong and Shanghai; NanoForge AI platform) |

| Licensee / partner | Boulevard Bio (US; Deerfield Management backed; worldwide rights) |

| Asset | MTS-128: preclinical trispecific (three-target) T-cell engager for autoimmune disease; AI-designed via NanoForge |

| Geography | Worldwide |

| Economics | $20M upfront; up to $1.6B in development, regulatory, and commercial milestones; tiered royalties to METiS on net sales |

| Royalty | Tiered royalties on net sales to METiS (rate band undisclosed); outbound to METiS |

| Date | Tue June 30, 2026 |

AlzeCure Pharma / QuantumCell: NeuroRestore Global Out-Licence, Up to USD 2.2B+ (Wed July 1)

AlzeCure Pharma (Nasdaq First North Growth Market Stockholm: ALZCUR; Huddinge, Sweden) entered a licensing agreement granting Danish QuantumCell global rights to the NeuroRestore platform, including the clinical-stage lead candidate ACD856, in a deal valued at a total of over USD 2.2 billion (BioStock).

USD 12M upfront (USD 5M as a direct equity investment in AlzeCure at a 30% premium to the ten-day VWAP), milestones, and tiered royalties (single-digit to low-double-digit). ACD856 is a first-in-class Trk-PAM (TrkA and TrkB positive allosteric modulator), developed in-house to clinical phase, with potential in Alzheimer's, Parkinson's, and depression. AlzeCure's second out-licence in three weeks, after the early-June ACD680 Alzstatin licence to Eli Lilly (up to USD 1B, excluding royalties).

| Term | Detail |

|---|---|

| Licensor / originator | AlzeCure Pharma (Nasdaq First North Stockholm: ALZCUR; Huddinge, Sweden) |

| Licensee / partner | QuantumCell (Denmark; global rights) |

| Asset | NeuroRestore platform, lead ACD856: first-in-class Trk-PAM (TrkA and TrkB positive allosteric modulator); clinical stage |

| Geography | Global |

| Economics | USD 12M upfront (USD 5M as a direct equity investment in AlzeCure at a 30% premium to ten-day VWAP); defined clinical and commercial milestones; tiered royalties single-digit to low-double-digit on net sales; total headline over USD 2.2B |

| Indications | Alzheimer's disease, Parkinson's disease, depression |

| Royalty | Tiered royalties, single-digit to low-double-digit, on global net sales to AlzeCure |

| Advisers | AlzeCure: ABG Sundal Collier (financial), Cirio Law and Synch Law (legal); FNCA Sweden AB (Certified Adviser). QuantumCell: not disclosed |

| Date | Wed July 1, 2026 |

Eli Lilly / Innovent Biologics: Verzenios (Abemaciclib) China Commercialisation, Terms Undisclosed (Tue June 30)

Eli Lilly (NYSE: LLY) and Innovent Biologics (HKEX: 1801) entered a commercialisation agreement under which Innovent takes sole commercialisation rights (importation, marketing, distribution, and promotion) for Verzenios (abemaciclib) in mainland China, while Lilly remains the Marketing Authorisation Holder responsible for manufacturing, supply, and development (PR Newswire).

No financial terms were disclosed: no upfront, no milestones, and no royalty, margin, or profit-split direction is public. Verzenios is an oral CDK4/6 inhibitor already approved and NRDL-reimbursed in China (since 2021) for HR-positive, HER2-negative breast cancer, and recorded roughly RMB 1.5B (about $221M) in 2025 China sales per PharmCube data cited by Jefferies. This is distinct from the broader historical Lilly and Innovent collaboration.

| Term | Detail |

|---|---|

| Licensor / MAH | Eli Lilly (NYSE: LLY; retains manufacturing, supply, and development; Marketing Authorisation Holder) |

| Commercialisation partner | Innovent Biologics (HKEX: 1801; sole China commercialisation: import, marketing, distribution, promotion) |

| Asset | Verzenios (abemaciclib): oral CDK4/6 inhibitor; HR-positive, HER2-negative breast cancer; marketed, NRDL-reimbursed in China since 2021 |

| Structure | Commercialisation-rights transfer on a marketed product; terms undisclosed (no upfront, milestone, or royalty/margin split public) |

| Base revenue | ~RMB 1.5B (about $221M) 2025 China sales (PharmCube via Jefferies) |

| Royalty | None disclosed; likely a supply or transfer-price arrangement rather than a royalty, and no royalty layer should be assumed without disclosure |

| Date | Tue June 30, 2026 |

Orion Pharma / Shilpa Medicare: European Nivolumab Biosimilar Commercialisation, Terms Undisclosed (Tue June 30)

Orion Pharma (Helsinki: ORNBV) and Shilpa Biologicals Private Limited, a wholly owned subsidiary of Shilpa Medicare (NSE: SHILPAMED), entered an agreement to commercialise Shilpa's intravenous nivolumab biosimilar (a biosimilar of Bristol Myers Squibb's Opdivo, an anti-PD-1 immune checkpoint inhibitor) in Europe (Orion via GlobeNewswire). Orion gains the exclusive right to distribute, market, and sell the product across Europe; Shilpa supplies the product and is entitled to receive certain development and regulatory milestone payments from Orion.

No financial terms were disclosed: no upfront, no milestone quantum, and no royalty, margin, or profit-split direction is public. The biosimilar is still under development at Shilpa, so this is a forward, supply-based commercialisation build rather than a transfer of a marketed asset. It extends a standing Orion and Shilpa partnership (the two already collaborate on other products) into immuno-oncology and supports Orion's stated push into the Continental European hospital segment. For the royalty desk, the milestones run from Orion to the supplier and there is no disclosed running royalty; the economics are more supply-and-distribution than royalty.

| Term | Detail |

|---|---|

| Commercialisation partner | Orion Pharma (Helsinki: ORNBV; Espoo, Finland; exclusive European distribution, marketing, and sales) |

| Supplier / licensor | Shilpa Biologicals, subsidiary of Shilpa Medicare (supplies product; receives development and regulatory milestones from Orion) |

| Asset | Intravenous nivolumab biosimilar (anti-PD-1; reference product Opdivo); in development, various oncology indications |

| Territory | Europe |

| Structure | Exclusive commercialisation and supply agreement; terms undisclosed (no upfront, milestone quantum, royalty, or margin split public) |

| Royalty | None disclosed; milestones payable by Orion to the supplier, not a running royalty, and no royalty layer should be assumed without disclosure |

| Strategic context | Extends the standing Orion / Shilpa partnership into immuno-oncology; supports Orion's Continental European hospital-segment strategy |

| Date | Tue June 30, 2026 |

Vect-Horus / Servier: VECTrans CNS Oligonucleotide Delivery Licence-Option (Tue June 30)

Vect-Horus (private; Marseille, France; a CNRS and Aix-Marseille University spinout building the VECTrans blood-brain-barrier shuttle platform) entered a research evaluation and exclusive licence-option agreement with Servier to apply VECTrans to Servier's oligonucleotide therapeutics for rare neurological and neurodevelopmental CNS disorders (Vect-Horus release).

Vect-Horus receives research and exclusivity fees during the option period. On option exercise, it is eligible for an upfront payment, development, regulatory, and commercial milestones, and single-digit royalties on annual net sales of any resulting products. No cash figures were disclosed. This extends a standing 2019 Servier scientific collaboration and follows Vect-Horus's CNS-delivery licences with Ionis (2024) and Novo Nordisk (2023). Preclinical; the royalty is real but option-gated, a forward contingent stream rather than a signed running royalty.

| Term | Detail |

|---|---|

| Licensor / platform | Vect-Horus (private; Marseille; VECTrans BBB-shuttle delivery platform) |

| Partner | Servier (foundation-governed international group; Global Head of Neurology Nitza Thomasson) |

| Structure | Research evaluation plus exclusive licence-option; Servier may advance selected programs to development and commercialisation |

| Asset | Servier oligonucleotide therapeutics for rare neurological and neurodevelopmental CNS disorders, delivered across the blood-brain barrier via VECTrans |

| Economics | Research and exclusivity fees during the option period; on exercise, upfront plus development, regulatory, and commercial milestones (amounts undisclosed) |

| Royalty | Single-digit royalties to Vect-Horus on annual net product sales, contingent on option exercise; a forward, option-gated stream |

| Stage | Preclinical / discovery |

| Date | Tue June 30, 2026 |

Insilico Medicine / Takeda: Pharma.AI Drug-Discovery Collaboration, Up to ~$600M plus Tiered Royalties (Wed July 1)

Insilico Medicine (HKEX: 3696; clinical-stage generative-AI drug discovery, Main Board listing December 30, 2025) entered a strategic collaboration with Takeda (JPX: 4502) to apply its end-to-end Pharma.AI platform to discover clinically differentiated drug candidates across Takeda therapeutic areas (Insilico via PR Newswire). Insilico leads AI-driven discovery to identify molecules meeting predefined scientific and early-development criteria; Takeda applies its global development capabilities to advance selected candidates through clinical validation and takes exclusive worldwide rights to develop, manufacture, and commercialise the resulting therapeutics.

Insilico receives about $60M in project initiation fees, near-term payments, and milestones, and is eligible for success-based preclinical, clinical, commercial, and sales milestones that could bring total deal value to about $600M, plus tiered royalties on future net sales. This is a forward, multi-program royalty origination rather than a single-asset out-licence: targets and lead series are not yet disclosed, so the royalty is real but discovery-stage and success-gated.

For the royalty desk it echoes the METiS / Boulevard shape (a Hong Kong-listed AI-design platform originating a tiered royalty to a larger partner), here running Hong Kong-to-Japan, and it fits the broader AI-discovery deal wave (Insilico's own $2.5B SK Biopharmaceuticals collaboration was signed at BIO on June 22, outside this window). The near-term cash is disclosed; the ceiling is milestone-loaded.

On the rate, the only comparable Insilico deal that discloses a band is the June 2026 SK Biopharmaceuticals CNS collaboration (up to $2.5B, single-digit royalties on net sales); across the rest of Insilico's book (Lilly, Menarini, Exelixis, Sanofi) the royalty is described only as tiered. Read against those comps, and given Takeda takes exclusive worldwide rights and carries all development and commercialisation, the undisclosed Takeda royalty most plausibly sits in the single-digit range, an inference benchmarked to SK Biopharmaceuticals rather than a disclosed term.

The about $60M near-term is a strong near-term component for a discovery collaboration (roughly three times the Menarini upfront), while the about $600M ceiling is modest against the SK Bio and Lilly collaborations, consistent with a Takeda-defined-target discovery deal rather than a named clinical asset.

| Term | Detail |

|---|---|

| Originator / platform | Insilico Medicine (HKEX: 3696; Pharma.AI: target identification, generative chemistry, molecule optimisation) |

| Partner | Takeda (JPX: 4502; exclusive worldwide rights to develop, manufacture, and commercialise selected candidates) |

| Structure | Strategic AI drug-discovery collaboration and licence; Insilico leads discovery, Takeda leads development and commercialisation |

| Economics | About $60M in project initiation fees, near-term payments, and milestones; up to about $600M total including success-based preclinical, clinical, commercial, and sales milestones |

| Royalty | Tiered royalties to Insilico on future net sales; multi-program, discovery-stage, success-gated. Rate band undisclosed; benchmarked to the single-digit band disclosed in Insilico's June 2026 SK Biopharmaceuticals collaboration (inference, not a disclosed term) |

| Asset | Not disclosed; candidates to be discovered across Takeda therapeutic areas via Pharma.AI |

| Stage | Discovery |

| Date | Wed July 1, 2026 |

CSPC Pharmaceutical / AstraZeneca: siRNA Renal-Disease Collaboration, Up to $1.77B plus Single-Digit Royalties (Thu July 2)

CSPC Pharmaceutical Group (HKEX: 1093) entered a strategic collaboration, option and license agreement with AstraZeneca (LSE / Nasdaq: AZN) to jointly discover and develop preclinical siRNA candidates for chronic kidney diseases across multiple indications, using CSPC's siRNA discovery platform and extrahepatic targeted delivery platform (BioSpace).

AstraZeneca pays $30M upfront and is on the hook for up to $540M in development milestones and up to $1.2B in sales milestones (about $1.77B headline), with single-digit royalties to CSPC on net sales. The parties work on two renal targets; AstraZeneca holds an option to license worldwide or ex-China rights, and CSPC retains rights to one asset in China. For the royalty desk this is a third China-outbound origination this week, alongside METiS and Insilico, and CSPC's fourth AstraZeneca deal in roughly a year (after the 2025 $5.3B AI research pact, the January 2026 up-to-$1.85B obesity peptide deal with $1.2B upfront, and a mid-2026 $110M oral chronic-disease programme).

| Term | Detail |

|---|---|

| Licensor / originator | CSPC Pharmaceutical Group (HKEX: 1093; siRNA discovery and extrahepatic targeted delivery platforms; AI-enabled molecular design) |

| Licensee / partner | AstraZeneca (LSE / Nasdaq: AZN; option to license worldwide or ex-China rights) |

| Asset | Preclinical siRNA candidates for chronic kidney diseases, multiple indications, two targets |

| Geography | Global option to AstraZeneca; CSPC retains China rights to one asset |

| Economics | $30M upfront; up to $540M development milestones; up to $1.2B sales milestones (~$1.77B headline) |

| Royalty | Single-digit royalties to CSPC on net annual sales of products reaching the market |

| Stage | Preclinical |

| Date | Thu July 2, 2026 |

Junshi Biosciences / Fosun Wanbang: Roconkibart (Anti-IL-17A) Greater China Licence, RMB 215M Upfront plus Double-Digit Royalties (Tue June 30)

Shanghai Junshi Biosciences (HKEX: 1877; SSE: 688180) entered a license agreement granting Fosun Wanbang Pharma Group (a wholly-owned subsidiary of Fosun Pharma, HKEX: 02196; SSE: 600196) the right to develop, register, manufacture, and commercialise roconkibart (JS005, an anti-IL-17A monoclonal antibody) in the Greater China region (mainland China, Hong Kong, Macao, and Taiwan) (Junshi via GlobeNewswire).

Junshi receives an upfront payment of RMB 215M (about $31.6M), plus development and sales milestones and double-digit tiered royalties on net sales. Roconkibart is in Phase 3 for plaque psoriasis (with reported 91% PASI 90 at week 16 and 65% PASI 100 at week 52 in the 150mg arm) and under regulatory review; ankylosing spondylitis is in Phase 2. This is a China-domestic royalty-bearing licence in which the innovator (Junshi) retains the royalty and hands commercial execution to Fosun Wanbang, distinct from the more common China-outbound structure. The signing date is June 30 per the HKEX filing; the press release carried July 1.

| Term | Detail |

|---|---|

| Licensor / originator | Shanghai Junshi Biosciences (HKEX: 1877; SSE: 688180; anti-IL-17A originator, retains royalty) |

| Licensee / partner | Fosun Wanbang Pharma Group (wholly-owned by Fosun Pharma; Greater China development, registration, manufacturing, commercialisation) |

| Asset | Roconkibart (JS005): anti-IL-17A monoclonal antibody; Phase 3 plaque psoriasis (under review), Phase 2 ankylosing spondylitis |

| Geography | Greater China (mainland China, Hong Kong, Macao, Taiwan) |

| Economics | RMB 215M (~$31.6M) upfront plus development and sales milestones |

| Royalty | Double-digit tiered royalties to Junshi on net sales |

| Date | Tue June 30, 2026 (announced July 1) |

PureTech / Celea Therapeutics: $180M Spin-Out With a Retained 1% to 3% Royalty on Deupirfenidone (Thu July 2)

PureTech Health (LSE: PRTC), a hub-and-spoke biotherapeutics company, completed the spin-out of its Founded Entity Celea Therapeutics through a $180M Series Seed Preferred financing and an associated transfer of the deupirfenidone asset from PureTech (PureTech via BioSpace; Investegate). Participants were RA Capital Management, Leaps by Bayer, PureTech, a large US-based healthcare fund, and a sovereign wealth fund; the Series Seed Preferred priced at $1.93 per share, with an initial $75M invested on June 29.

The structure matters more than the headline. PureTech contributed $30M to the round, reserved a further $70M from existing cash for potential future support, holds 35.4% of Celea's fully diluted share capital, and, critically for the royalty desk, is entitled to tiered royalties of 1% to 3% on annual net sales plus up to $190M in milestone payments. Deupirfenidone (LYT-100) is a deuterated form of pirfenidone in development as a next-generation antifibrotic for idiopathic pulmonary fibrosis, with FDA and European Commission Orphan Drug Designation; the Phase 3 SURPASS-IPF trial is targeted to start early Q3 2026.

This is the PureTech monetisation archetype: an originator seeding a founded entity with third-party capital while retaining equity plus a royalty on the out-transferred asset, the same shape that produced its Karuna (KarXT, sold to Bristol Myers Squibb) and Seaport economics. This is a royalty-bearing origination through a retained stream, with the $180M itself raised as equity.

| Term | Detail |

|---|---|

| Originator / royalty holder | PureTech Health (LSE: PRTC; hub-and-spoke; retains 35.4% equity plus royalty) |

| Founded entity | Celea Therapeutics (independent clinical-stage respiratory company; CEO Sven Dethlefs) |

| Structure | $180M Series Seed Preferred ($1.93/share; initial $75M June 29) plus asset transfer of deupirfenidone from PureTech |

| Investors | RA Capital Management, Leaps by Bayer, PureTech ($30M), a large US healthcare fund, a sovereign wealth fund |

| Asset | Deupirfenidone (LYT-100): deuterated pirfenidone, next-generation antifibrotic; FDA and EC Orphan Drug Designation |

| Indication / stage | Idiopathic pulmonary fibrosis; Phase 3 SURPASS-IPF targeted for early Q3 2026 |

| Royalty | Tiered royalties of 1% to 3% to PureTech on annual net sales, plus up to $190M in milestones |

| PureTech position | 35.4% of Celea fully diluted; further $70M reserved; runway extended at least through end-2028 |

| Date | Thu July 2, 2026 |

Lonza / Nona Biosciences: Blood-Brain-Barrier Platform Licence and Revenue Share (Wed July 1)

Lonza (SIX: LONN) licensed certain IP rights to Nona Biosciences' single-domain-antibody blood-brain-barrier crossing technology, paying upfront and option fees to Nona (a wholly owned subsidiary of HBM Holding, HKEX: 02142), with both parties sharing revenue from future third-party licensing agreements generated through the collaboration (AllSci).

Structured as a bilateral technology exchange rather than a conventional platform licence: Nona contributes its Harbour Mice heavy-chain-only antibody platform for BBB-crossing candidate discovery, while Lonza contributes its GS Gene Expression System and GlycoConnect bioconjugation technology for candidate optimisation. No lead asset has been disclosed. The signal for the newsletter is a CDMO moving from pure contract manufacturing toward owning monetisable IP: a CDMO-to-originator platform layer that sits in the same blood-brain-barrier delivery cluster as Vect-Horus / Servier and the BioArctic franchise. Terms undisclosed, revenue-share on future out-licences.

| Term | Detail |

|---|---|

| Parties | Lonza (SIX: LONN) and Nona Biosciences (subsidiary of HBM Holding, HKEX: 02142) |

| Structure | IP licence plus bilateral technology exchange; upfront and option fees to Nona; shared revenue on future third-party licences |

| Contributions | Nona: Harbour Mice HCAb platform for BBB-crossing discovery. Lonza: GS Gene Expression System and GlycoConnect bioconjugation |

| Asset | Blood-brain-barrier delivery platform; no lead asset disclosed |

| Royalty | Revenue-share on future out-licences (rate undisclosed), not a product royalty |

| Date | Wed July 1, 2026 |

Structured Finance and Non-Dilutive Debt

Ligand / Zerion Pharma: Dispersome Royalty Financing Plus Equity, Undisclosed (Tue June 30)

Ligand Pharmaceuticals (Nasdaq: LGND) completed a combined royalty financing and equity investment in Zerion Pharma A/S (private; Copenhagen; a 2019 University of Copenhagen spin-out) to advance Zerion's Dispersome solubility and bioavailability platform toward first regulatory approvals (Zerion release). Ligand invested an undisclosed amount and in return takes a share of future Dispersome royalty income plus an equity position in Zerion.

Dispersome uses beta-lactoglobulin as a carrier to formulate poorly soluble small molecules into stable, high-drug-load amorphous systems. Zerion already licenses it to Hovione (a JV managing the IP), Insud Pharma, Aché, and dsm-firmenich, each carrying royalties back to Zerion; Ligand's investment sits on top of that base and extends its aggregator model into a platform-level royalty.

| Term | Detail |

|---|---|

| Financier / aggregator | Ligand Pharmaceuticals (Nasdaq: LGND; royalty aggregator, 100+ assets) |

| Recipient / originator | Zerion Pharma A/S (private; Copenhagen; University of Copenhagen spin-out) |

| Asset | Dispersome platform: beta-lactoglobulin-carrier amorphous formulation technology for poorly soluble small molecules |

| Structure | Combined royalty financing plus equity investment; Ligand funds development and first approvals, taking a share of future Dispersome royalty income plus an equity stake |

| Economics | Investment amount undisclosed; royalty share and equity percentage not disclosed |

| Pre-existing royalty base | Dispersome licences to Hovione (JV), Insud Pharma, Aché, dsm-firmenich, each carrying licence fees and royalties to Zerion |

| Royalty | Share of future Dispersome royalty income to Ligand (percentage undisclosed), plus an equity stake; layered over Zerion's existing partner royalties |

| Date | Tue June 30, 2026 |

Financings

Talawar Therapeutics / JATT II Acquisition Corp: ~$285M De-SPAC With a $225M PIPE (announced Mon June 29)

Talawar Tx Inc. (private; first spinout of London-based biotech builder Khanda Therapeutics) and JATT II Acquisition Corp (Nasdaq: JATT; a Cayman-incorporated SPAC) entered a definitive business combination agreement; the combined company will trade on Nasdaq as TLWR, with closing targeted for H2 2026 (JATT II Form 425, SEC).

About $285M (no redemptions): $60M JATT II trust plus a concurrent $225M PIPE at $10.00, led by Access Biotechnology with Bain Capital Life Sciences, Deep Track, RA Capital, Janus Henderson, Vianti, and Farallon; a $125M minimum-cash condition. Lead asset TALA-125 is a preclinical anti-IL-13 x anti-IL-18 bispecific for atopic dermatitis (clinic Q1 2027).

| Term | Detail |

|---|---|

| Company | Talawar Tx Inc. (private; first Khanda Therapeutics spinout; CEO Marc Schegerin) |

| Vehicle | JATT II Acquisition Corp (Nasdaq: JATT; combined company to trade as TLWR) |

| Structure | De-SPAC; ~$285M combined (no redemptions): $60M JATT II trust plus a $225M PIPE at $10.00 per share; $125M minimum-cash closing condition |

| PIPE syndicate | Access Biotechnology (lead); Bain Capital Life Sciences, Deep Track, RA Capital, Janus Henderson, Vianti, Farallon |

| Asset | TALA-125: preclinical anti-IL-13 x anti-IL-18 bispecific for atopic dermatitis; clinic targeted Q1 2027 |

| Advisers | Placement agents (PIPE): Guggenheim Securities, Cantor, LifeSci Capital. Legal: Cooley (Talawar), Greenberg Traurig (JATT II), Davis Polk & Wardwell (placement agents) |

| Date | Announced Mon June 29, 2026; close targeted H2 2026 |

Beeline Medicines: $126.3M Series A Extension, Over a BMS Upstream Interest (Tue June 30)

Beeline Medicines (private; a Bain Capital-founded autoimmune and inflammatory-disease company) raised a $126.3M Series A extension, bringing total Series A funding to $426.3M, from Bain Capital, CPP Investments, Bristol Myers Squibb, and management (BioSpace; Fierce Biotech).

Proceeds fund pivotal development of afimetoran, an oral, once-daily, equipotent TLR7/8 inhibitor, with a Phase 2 systemic lupus erythematosus readout expected 2H 2026. Beeline debuted in April 2026 with a $300M Series A led by Bain Capital, built around five programs in-licensed from Bristol Myers Squibb; CEO is Saqib Islam (formerly of SpringWorks, sold to Merck KGaA for $3.9B in April 2025).

| Term | Detail |

|---|---|

| Company | Beeline Medicines (private; Bain Capital-founded; CEO Saqib Islam) |

| Structure | $126.3M Series A extension; total Series A now $426.3M |

| Syndicate | Bain Capital, CPP Investments, Bristol Myers Squibb, plus management |

| Asset | Afimetoran: oral once-daily TLR7/8 inhibitor; Phase 2 SLE readout expected 2H 2026 |

| Upstream interest | Pipeline built on five programs in-licensed from Bristol Myers Squibb (BMS is both licensor and equity holder), so a BMS upstream royalty/economic interest likely travels with the assets |

| Date | Tue June 30, 2026 |

Flare Therapeutics: $85M Insider-Led Series C (Tue June 30)

Flare Therapeutics Inc. (private; Cambridge, MA; a Third Rock Ventures-founded transcription-factor drug-discovery company) closed an $85M Series C led by existing investors and named Anna Protopapas, former Mersana Therapeutics CEO, as chief executive (BioSpace).

Led by Third Rock Ventures and Nextech Invest, with Pfizer Ventures, Eli Lilly, Novartis, Boxer, GordonMD, Invus, Casdin, Agent Capital, and Eventide. Flare will concentrate on FX-111, a first-in-class ARON degrader for prostate cancer, with a Phase 1A start targeted for Q3 2026.

| Term | Detail |

|---|---|

| Company | Flare Therapeutics Inc. (private; Cambridge, MA; incoming CEO Anna Protopapas) |

| Structure | Insider-led $85M Series C |

| Syndicate | Third Rock and Nextech (co-leads); Pfizer Ventures, Eli Lilly, Novartis, Boxer, GordonMD, Invus, Casdin, Agent Capital, Eventide |

| Asset | FX-111: ARON degrader for AR-driven prostate cancer; Phase 1A targeted Q3 2026 |

| Use of proceeds | Advance FX-111 to proof of concept; preclinical ARON RIPTAC program |

| Date | Tue June 30, 2026 |

Xellar Biosystems: ~$50M Venture Round (Mon June 29)

Xellar Biosystems raised approximately $50M in Series A and A+ financing to advance its 3D Bio Intelligence preclinical platform (PR Newswire). Investors were not disclosed; no royalty layer is attached to the round itself.

| Term | Detail |

|---|---|

| Company | Xellar Biosystems (private) |

| Structure | Venture round, ~$50M |

| Asset / platform | 3D Bio Intelligence preclinical platform |

| Royalty layer | None on the financing; afimetoran in-licensed from BMS (upstream interest) |

| Date | Mon June 29, 2026 |

Cereno Scientific: ~SEK 60M Directed Share Issue (Tue June 30)

Cereno Scientific AB (Nasdaq First North Growth Market Stockholm: CRNO B; Gothenburg, Sweden) carried out a directed share issue of SEK 60M at SEK 5.10 per share, about a 4% premium to the prior close, subscribed by existing shareholders and one new investor (BioStock).

A deliberately limited raise to strengthen Cereno's hand in ongoing partnering, ahead of a global Phase IIb of CS1 in pulmonary arterial hypertension. The company reported its strongest-ever partnering interest after BIO 2026.

| Term | Detail |

|---|---|

| Company | Cereno Scientific AB (Stockholm First North: CRNO B; Gothenburg, Sweden; CEO Sten R. Sörensen) |

| Structure | Directed share issue; SEK 60M at SEK 5.10 (about a 4% premium); existing holders plus one new investor |

| Pipeline | CS1 (PAH; Phase IIb planned), CS014 (PH-ILD; Phase 1 PK bridging), CS585 (antiphospholipid syndrome; preclinical) |

| Use of proceeds | Partnering and business-development processes from a stronger negotiating position |

| Date | Tue June 30, 2026 |

Alebund Pharmaceuticals: HKEX Main Board IPO, ~HK$1.283B Gross (Mon June 29)

Alebund Pharmaceuticals (Jiangsu) Limited (HKEX: 09637) listed on the Hong Kong main board on June 29, a China renal-disease drug developer (PR Newswire). The global offering was 56,755,400 H shares at HK$22.60, for gross proceeds of about HK$1.283B (about US$164M) before the greenshoe; a full 8,513,300-share over-allotment would lift the total to about HK$1.475B (about US$189M). The stock closed its first day at HK$46.00, up about 104%.

The book was heavily oversubscribed and anchored by a cornerstone group including GIC, Loomis Sayles, RTW, SymBiosis, Tencent, and Cormorant. Proceeds fund a renal pipeline led by AP301 (oral phosphate binder, China Phase 3 complete, NDA planned), plus AP306 (pan-phosphate transport inhibitor; ex-Greater China rights licensed to R1 Therapeutics in an out-of-window March 2026 deal), AP303 (dual PPAR agonist), and AP308 (engineered IgA protease), alongside the commercial ESA Mircera. Primary equity capital, no royalty origination.

| Term | Detail |

|---|---|

| Company | Alebund Pharmaceuticals (Jiangsu) Limited (HKEX: 09637; Shanghai; founded 2018) |

| Structure | Global offering / H-share IPO; 56,755,400 shares at HK$22.60 |

| Gross proceeds | ~HK$1.283B (~US$164M) pre-greenshoe; ~HK$1.475B (~US$189M) if the 8,513,300-share over-allotment is fully exercised |

| Debut | Closed first day at HK$46.00, up ~104% |

| Cornerstones | GIC, Loomis Sayles, RTW, SymBiosis, Tencent, Cormorant, and others |

| Syndicate | Joint managers BOCI Asia, CLSA, Huatai Financial, Jefferies, and Merrill Lynch (Asia Pacific); Jefferies (Hong Kong) as stabilising manager |

| Pipeline | AP301 (hyperphosphataemia, Phase 3 complete), AP306, AP303, AP308; commercial product Mircera |

| Royalty angle | None from the IPO; AP306 ex-Greater China rights were licensed to R1 Therapeutics in March 2026, outside this window |

| Date | Mon June 29, 2026 |

Nuvectis Pharma: $100M Follow-On Offering (Mon June 29)

Nuvectis Pharma (Nasdaq: NVCT; Fort Lee, NJ) priced an underwritten offering of 5,000,000 shares at $20.00, for gross proceeds of $100M, with a 30-day option for up to 750,000 more shares; the offering was expected to close on or about July 1 (Nuvectis via GlobeNewswire). Cantor was sole bookrunner, with H.C. Wainwright, Laidlaw, Lucid Capital Markets, Maxim, Roth, and Titan Partners as co-managers.

Proceeds fund NXP900 (oncology) plus NXP100 (Complement Factor B inhibitor) and NXP200 (BRAF inhibitor), the two assets in-licensed ex-China from Haisco on June 22 (out of window). A primary equity raise, no royalty layer, though the upsized round follows the Haisco in-licence that carries its own upstream economics.

| Term | Detail |

|---|---|

| Company | Nuvectis Pharma (Nasdaq: NVCT; Fort Lee, NJ; clinical-stage, immune-complement and oncology) |

| Structure | Underwritten follow-on; 5,000,000 shares at $20.00; up to 750,000-share greenshoe |

| Gross proceeds | $100M before the greenshoe; expected close on or about July 1 |

| Bookrunner | Cantor (sole); co-managers H.C. Wainwright, Laidlaw, Lucid Capital Markets, Maxim, Roth, Titan Partners |

| Use of proceeds | NXP900, NXP100 (Complement Factor B inhibitor), NXP200 (BRAF inhibitor) |

| Royalty angle | None on the raise; NXP100 and NXP200 were in-licensed ex-China from Haisco on June 22 (out of window), carrying upstream Haisco economics |

| Date | Mon June 29, 2026 |

BridgeBio Pharma: $1B Convertible Preferred Equity, Sixth Street and HealthCare Royalty (Wed July 1)