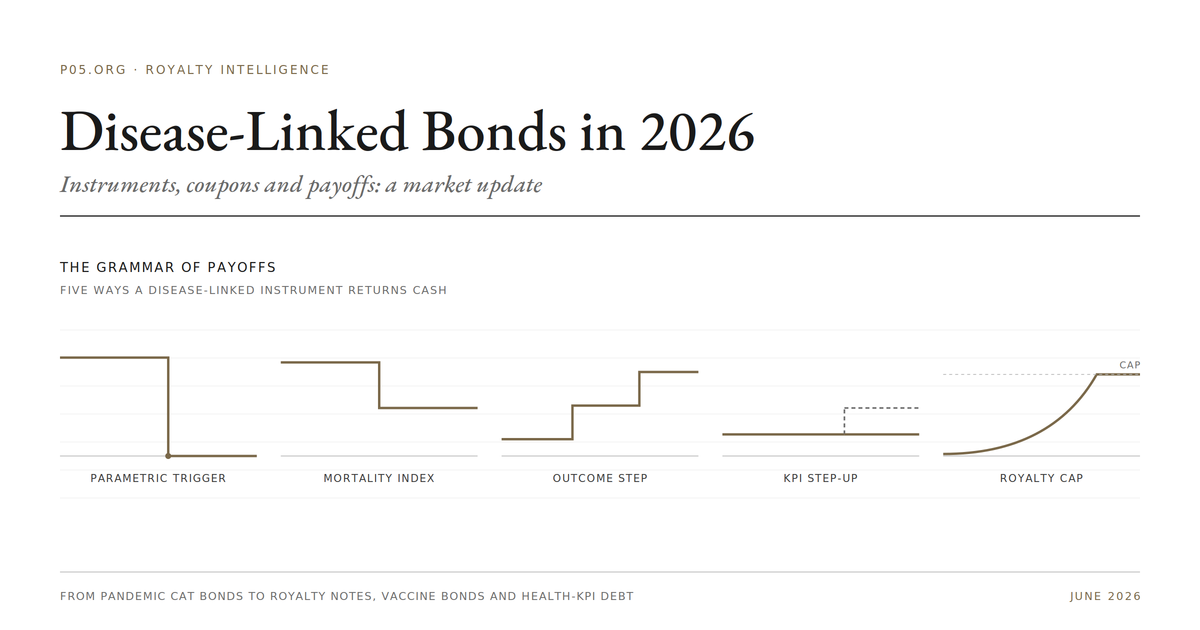

Disease-Linked Bonds: Instruments, Coupons, and Payoffs

Since the September 2025 analysis, the disease-linked bond category has separated into families that no longer behave alike. Instruments that place principal at risk on a parametric trigger or a measured outcome saw little or no new issuance in 2024 to 2026. Instruments that rest on a sovereign credit, a donor pledge, or a defined revenue line continued to price. The sections below give the current terms: sizes, coupons, spreads, repayment caps, step-ups, and payout schedules.

1. Research-Funding Bonds: A California Revival

Research-funding bonds are general-obligation bonds. Investors bear the issuing government's credit risk, not research risk. The 2026 development is the return of the model as a live ballot instrument in California, with revenue-participation and pricing terms attached to an otherwise standard GO structure.

The California Immunology Research and Cures Initiative

The California Secretary of State certified the measure for the 3 November 2026 ballot on 24 June 2026, after the proponents submitted more than the 546,651 valid signatures required. It authorises USD 8.4 billion in state general-obligation bonds for immunology and immunotherapy research.

| Term | Detail |

|---|---|

| Instrument | State general-obligation bond |

| Amount | USD 8.4 billion |

| Use of proceeds | Split 50/50: a University of California-affiliated research institute and a competitive grant programme |

| Mandate | At least half to cancer, heart disease, and Alzheimer's research |

| Pricing condition | Resulting drugs sold in California at 20% below the national average price |

| Revenue participation | 10% of licensing proceeds earmarked to repay the bond |

| Repayment cost | Roughly USD 500m per year for about 25 years (Legislative Analyst's Office, as reported) |

| Principal funder | Dr Gary K. Michelson, via the Michelson Center for Public Policy |

| Anchor backers | Alzheimer's Association, Parkinson Association of Northern California |

| Early voting | 5 October 2026 |

Three features bear on the credit and the politics. First, the 10% licensing recoupment is a revenue participation, not a risk transfer: the state retains the research risk and the bulk of any upside, and the rating treatment runs to the GO pledge rather than the recoupment.

Second, the 20% pricing discount reduces the same licensing revenue the recoupment is meant to capture, and a commercial partner asked to develop a funded asset will model it as a permanent haircut on part of the California market.

Third, half the proceeds flow to a single named institute, the California Institute of Immunology and Immunotherapy, which the principal funder chairs. Concentrating half of a multibillion-dollar pool in one institution is the configuration that produced governance problems at the Texas precedent, discussed below. Senator Scott Wiener, sponsor of the rival measure, argued the initiative is too narrow and should have been folded into a broader science bond.

The Wiener Science Bond (SB 895): Did Not Qualify

A broader competing measure failed to reach the ballot. SB 895, the California Science and Health Research Bond Act, would have authorised a USD 12 billion bond (reduced from an original USD 23 billion) to create a California Foundation for Science and Health Research, covering health, agriculture, pandemic threats, and wildfire resilience.

It passed the Senate 29 to 9 on 27 May 2026, sponsored by the University of California, the United Auto Workers, and the Union of American Physicians and Dentists. It then failed to clear the Assembly before the 25 June deadline to qualify for November.

Legislative staff cited constrained state bonding capacity and competing priorities, including an USD 11 billion housing bond. SB 895 carried the same drug-discount and recoupment provisions as the immunology measure, plus a tie-in to the state's CalRx public manufacturing initiative.

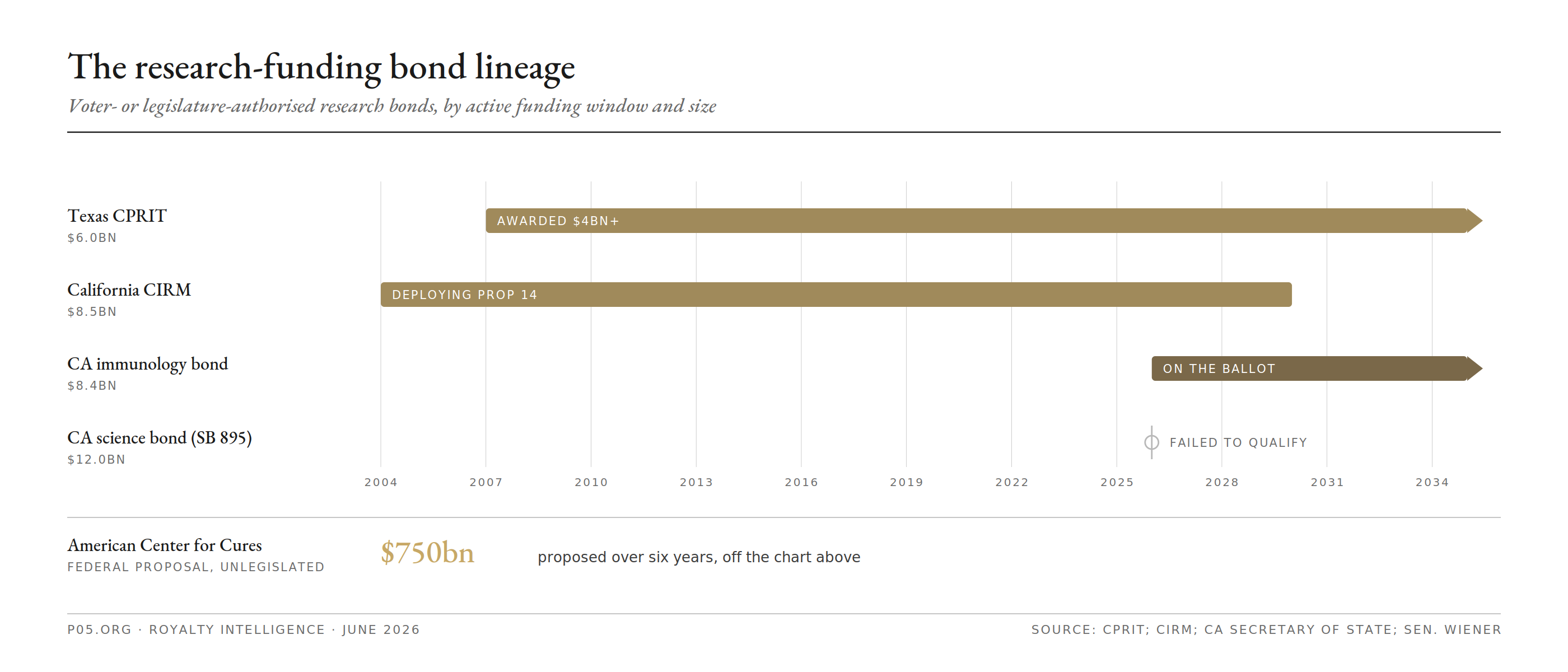

The Established and Proposed Models

The California measures sit within an existing lineage of voter- or legislature-authorised research bonds.

| Programme | Authority and year | Size | Repayment source | Status, mid-2026 |

|---|---|---|---|---|

| Texas CPRIT | Prop 15 (2007), Prop 6 (2019) | USD 6.0bn lifetime | Texas general revenue | Over USD 4bn awarded; final grant issuance projected early 2030s |

| California CIRM | Prop 71 (2004), Prop 14 (2020) | USD 8.5bn lifetime | California general revenue | Deploying Prop 14; finite runway |

| CA immunology bond | Initiative, Nov 2026 | USD 8.4bn | State revenue plus 10% of licensing | On the ballot |

| CA science bond (SB 895) | Legislature, sought Nov 2026 | USD 12bn | State revenue plus recouped royalties | Failed to qualify |

| American Center for Cures | Federal proposal | USD 750bn over six years | Licensing income and healthcare savings | Proposal only |

CPRIT is the second-largest public funder of cancer research in the United States after the National Cancer Institute. It has passed USD 4 billion in cumulative awards and projects a final grant issuance in the early 2030s. Its early years included a 2012 to 2013 grant-management episode that triggered a funding freeze and governance reform, the precedent now cited against the single-institute design of the California immunology measure.

CIRM increased certain award rounds in 2025 in response to federal cuts and is managing toward exhaustion of its Proposition 14 authority. The Weisbach federal proposal, at USD 750 billion over six years with interest serviced from licensing income and principal repaid from projected healthcare savings, remains unlegislated.

2. Pandemic Risk Transfer: Dead in Bond Form, Alive in Insurance

No dedicated pandemic or infectious-disease catastrophe bond has priced in 2024, 2025, or 2026. The World Bank's Pandemic Emergency Financing Facility closed on 30 April 2021 and was not replaced. For reference, the original PEF terms and outcome:

| PEF term | Class A | Class B |

|---|---|---|

| Amount | USD 225m | USD 95m |

| Coupon | 6-month USD LIBOR + 6.50% | 6-month USD LIBOR + 11.10% |

| Term | 3 years (Jul 2017 to Jul 2020) | 3 years |

| April 2020 payout | About 44% of principal | 100% of principal |

| Total paid (bonds plus USD 105m swaps) | USD 195.8m to 64 IDA countries |

The issue was twice oversubscribed at launch, drawing about USD 1.2 billion of orders against USD 425 million of risk, with Swiss Re Capital Markets as sole bookrunner.

The institutional successor, the World Bank-hosted Pandemic Fund (launched November 2022), uses no bond financing. It is a grant facility.

| Pandemic Fund | Detail |

|---|---|

| Structure | Grants, funded by sovereign and philanthropic contributions |

| Seed capital | About USD 2bn in the first year, from 27 contributors |

| Rounds 1 and 2 | USD 885m in grants, mobilising about USD 6bn in co-financing, 75 countries |

| Round 3 (allocated 12 Feb 2026) | USD 499.6m to 20 projects, mobilising over USD 4bn in co-financing |

Parametric infectious-disease risk transfer did not disappear; it moved from the bond market to sovereign insurance. The African Risk Capacity, a specialised agency of the African Union, launched a sovereign parametric epidemic product in 2022 covering Ebola, Marburg, and meningitis, with Senegal the first country to take cover at about USD 5 million.

Like a cat bond, it pays out on a pre-agreed outbreak size; unlike a cat bond, the risk sits with a member-funded mutual insurer rather than capital-markets investors. ARC plans to extend the product to additional diseases in 2026, with Lassa fever, Crimean-Congo haemorrhagic fever, and Rift Valley fever under consideration.

The only capital-markets instruments still carrying pandemic exposure are legacy mortality catastrophe bonds in run-off.

| Mortality bond | Detail |

|---|---|

| Swiss Re Vita Capital VI (2021) | USD 120m, about 3% coupon; first Vita to include COVID deaths (from 2022); marked down on excess mortality |

| Matterhorn Re 2020-2 | Carried COVID mortality exposure |

| Swiss Re recovery across the two | About USD 151m |

| Securian / Minnesota Life (Jan 2021) | USD 100m mortality bond cancelled over investor COVID-exposure concerns |

For context, the broader catastrophe-bond market set a record in 2025, with roughly USD 25.6 billion of new 144A issuance and outstanding paper above USD 60 billion (Artemis). The growth perils are property, cyber, and wildfire; pandemic risk is absent from new issuance.

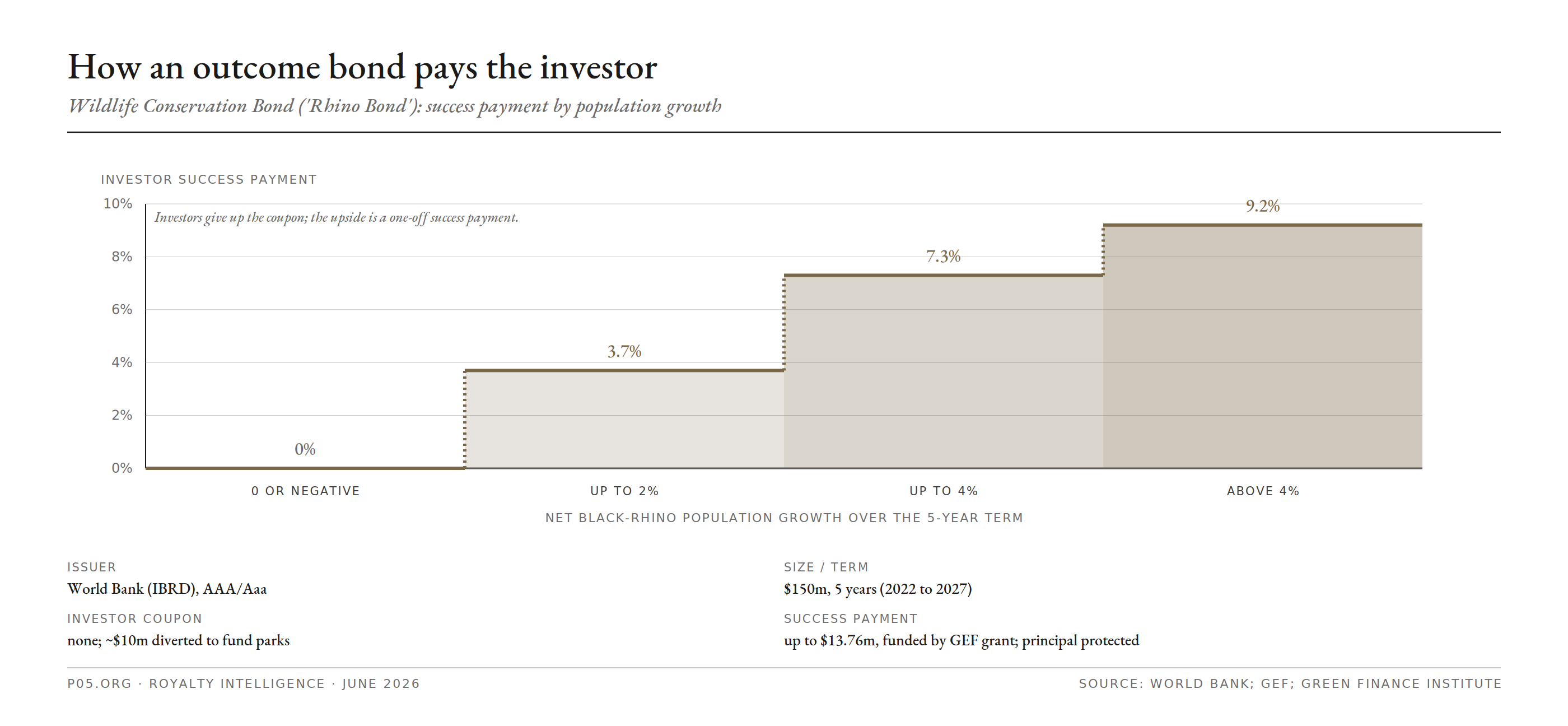

3. World Bank Outcome Bonds: The Investment-Grade Relative of the Health DIB

The development impact bond has a larger, investment-grade cousin: the World Bank (IBRD) outcome bond. Principal is protected by IBRD's AAA/Aaa rating, while the coupon is partly or wholly at risk and linked to a measured outcome.

The structure has been used once for health (a COVID-19 UNICEF bond) and once for a health-adjacent purpose (a clean-water project that, by the World Bank's account, addresses waterborne disease responsible for an estimated 9,000 deaths a year in Vietnam), and it continued to print in 2026.

In the Wildlife Conservation Bond ("Rhino Bond"), investors forgo a normal coupon; the foregone coupons fund the underlying activity, and a separate success payment, funded by a third-party grant, pays out on a measured result.

The success payment follows a tiered schedule keyed to the net black-rhino population growth rate over the term (World Bank):

| Net population growth | Investor success payment |

|---|---|

| Zero or negative | 0% |

| Up to 2% | About 3.7% |

| Up to 4% | About 7.3% |

| Above 4% | About 9.2% |

The template carried later issues, including two in the current window.

| Outcome bond | Date | Amount | Term | Outcome link |

|---|---|---|---|---|

| Vietnam water purifier | 2024 | ~USD 50m | 5 years | Clean-water delivery, carbon units |

| UNICEF bond | 2021 | structured note | n/a | COVID-19 response |

| Amazon Reforestation-Linked | Aug 2024 | USD 225m | n/a | Carbon-removal units, Brazil |

| Spekboom Restoration | 23 Apr 2026 | USD 120m | 14 years (to 2040) | Native-plant restoration, South Africa |

The Amazon bond pays a fixed guaranteed component plus a variable component tied to the generation of verified carbon-removal units. The Spekboom bond, the World Bank's longest-dated outcome bond, uses the same fixed-plus-variable design with full principal protection.

No pure disease-outcome bond has been issued since the UNICEF COVID-19 note, but this is the structure a health outcome bond would most plausibly reuse, and the rhino schedule is the template for how investor return would be tied to a health metric.

4. Vaccine Frontloading Bonds: Active, at Tight Spreads

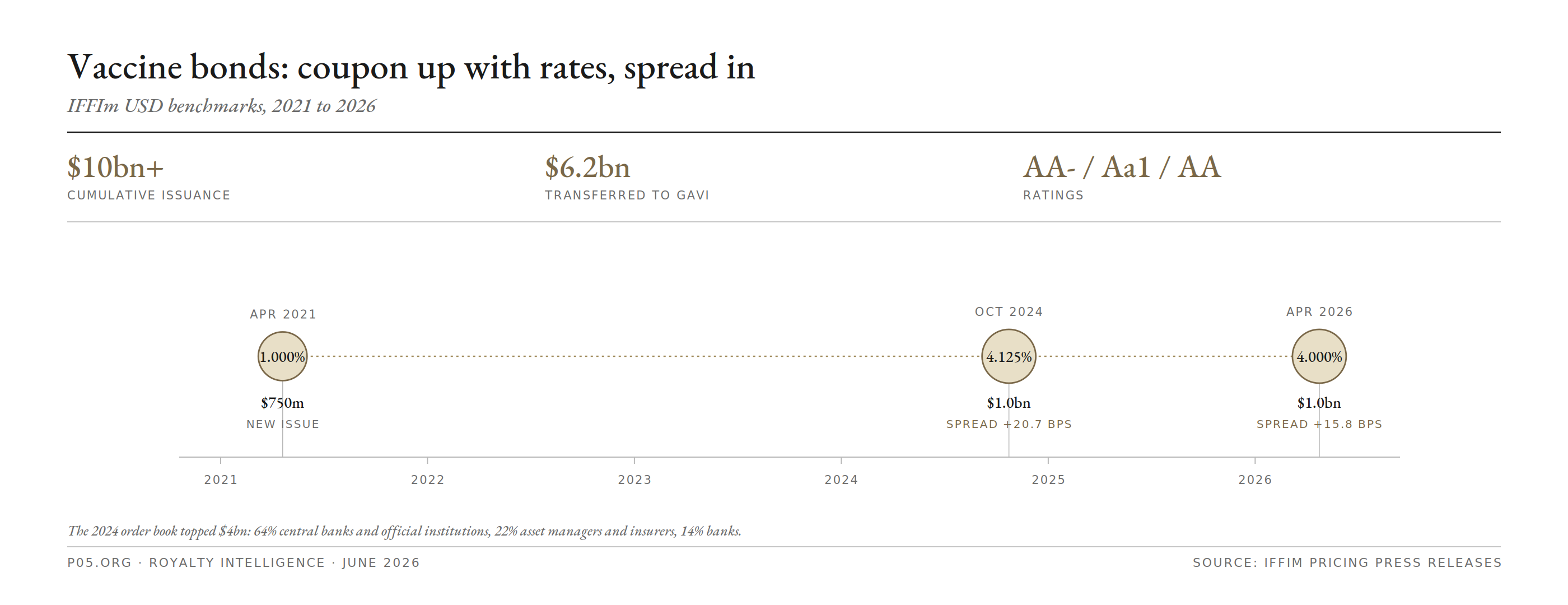

The International Finance Facility for Immunisation converts long-dated sovereign donor pledges into immediately available cash for Gavi by issuing highly rated bonds. It priced again in April 2026 at a 4.0% semi-annual coupon and a 15.8 basis-point spread to Treasuries, with coupon payment dates of 29 April and 29 October.

| IFFIm benchmark | Date | Amount | Maturity | Coupon (s/a) | Re-offer yield | Spread vs UST |

|---|---|---|---|---|---|---|

| 5-year USD | 22 Apr 2026 | USD 1.0bn | 29 Apr 2031 | 4.000% | 4.068% | +15.8 bps |

| 3-year USD | 23 Oct 2024 | USD 1.0bn | 29 Oct 2027 | 4.125% | 4.222% | +20.7 bps |

| 5-year USD | Apr 2021 | USD 750m | 21 Apr 2026 | 1.000% | priced 99.704 | n/a |

The October 2024 benchmark drew an order book above USD 4 billion (BofA Securities, HSBC, and TD Securities as lead managers), allocated roughly 64% to central banks and official institutions, 22% to asset managers and insurers, and 14% to banks.

| IFFIm programme | Detail |

|---|---|

| Cumulative issuance | Over USD 10bn since 2006 |

| Raised from investors | About USD 9.7bn |

| Transferred to Gavi | About USD 6.2bn, roughly one-sixth of Gavi's budget |

| Funding to CEPI | About USD 272m |

| Donor pledges backing the facility | USD 9.7bn through 2037, from 11 sovereign donors |

| Ratings | AA- / Aa1 / AA (Fitch / Moody's / S&P) |

The repayment source is the donor pledge stream, now under pressure. At Gavi's June 2025 replenishment for 2026 to 2030:

| Gavi 6.0 replenishment | Detail |

|---|---|

| Target | USD 11.9bn |

| Raised | Over USD 9bn |

| Largest donor | United Kingdom, USD 1.7bn |

| Gates Foundation | USD 1.6bn |

| United States | Signalled withdrawal; previously about 12% of funding; lost its board seat by early 2026 |

Outstanding IFFIm bonds are over-collateralised by the broader pledge pool and are not impaired by a single donor's withdrawal. The exposure is to the size of the programme the bonds fund, not to the bonds' repayment.

5. Sustainability-Linked Health Bonds: The Coupon Step-Up Resolves

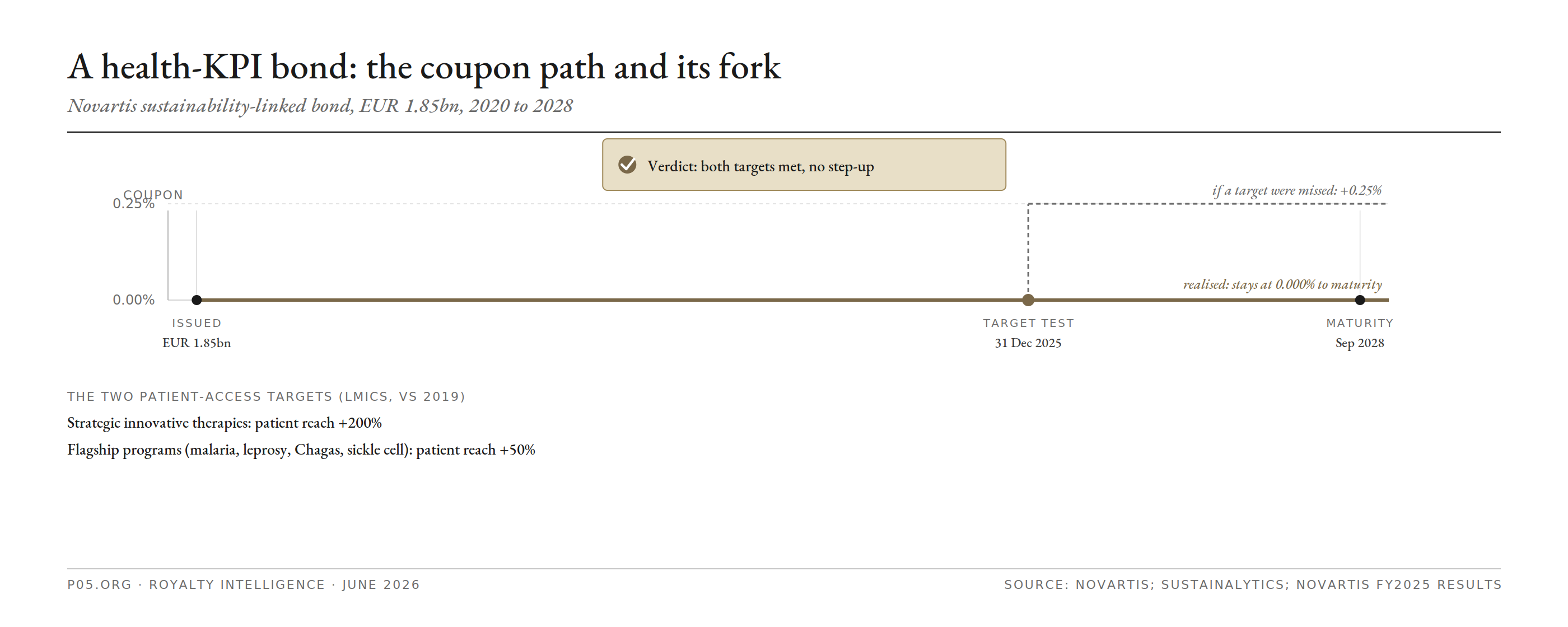

A separate family ties a corporate issuer's coupon to a health key performance indicator. The reference instrument is the Novartis sustainability-linked bond of September 2020, the first in the healthcare industry. Investors bear the issuer's credit, and the coupon steps up if a patient-access target is missed.

| Novartis sustainability-linked bond | Detail |

|---|---|

| Issuer / size | Novartis Finance, EUR 1.85bn |

| Tenor | 23 Sep 2020 to 23 Sep 2028 |

| Coupon | 0.000% |

| KPI 1 | Strategic innovative therapies, patient reach +200% in LMICs by 2025 (vs 2019) |

| KPI 2 | Flagship programs (malaria, leprosy, Chagas, sickle cell), patient reach +50% |

| Step-up | +0.25% from the first coupon after 31 Dec 2025 if either target is missed |

The structure inverts the usual incentive: bondholders are compensated more if the issuer fails its social target. The verdict is now in. On 31 December 2025, Novartis confirmed it had met both 2025 patient-access targets, so no step-up applies and the bond continues to pay 0.000% to maturity. The instrument illustrates the mechanism and its limit: the contingent cost (0.25% on EUR 1.85 billion, about EUR 4.6 million a year) is small relative to the issuer's funding base, which is the usual critique of sustainability-linked structures. No comparably scaled health-KPI SLB has followed in the pharmaceutical sector.

6. Health Social and Development Impact Bonds: Still Marginal

The outcome-based instruments remain small and under-evidenced. The most current review, by Plankó and colleagues in BMC Public Health (16 March 2026), found that the cost savings to government used to justify social impact bonds for health prevention are rarely realised in practice.

A companion scoping review of SIBs for non-communicable diseases recorded the scale.

| Health SIB evidence (NCD scoping review) | Detail |

|---|---|

| Instruments identified | 11, across 8 countries |

| Average private investment | About USD 2.0m |

| Met all target outcomes | 3 of 11 |

| Common problems | Conflicts of interest, weak public disclosure |

The terminology has spread faster than the instruments: Social Outcome Partnerships in the United Kingdom, contrats à impact in France, Pay for Success in the United States, Social Benefit Bonds in Australia. The reference health development impact bonds remain the Cameroon cataract bond, the Utkrisht maternal-health bond in Rajasthan, and the ICRC humanitarian bond. No major new health DIB launched in 2025 or 2026.

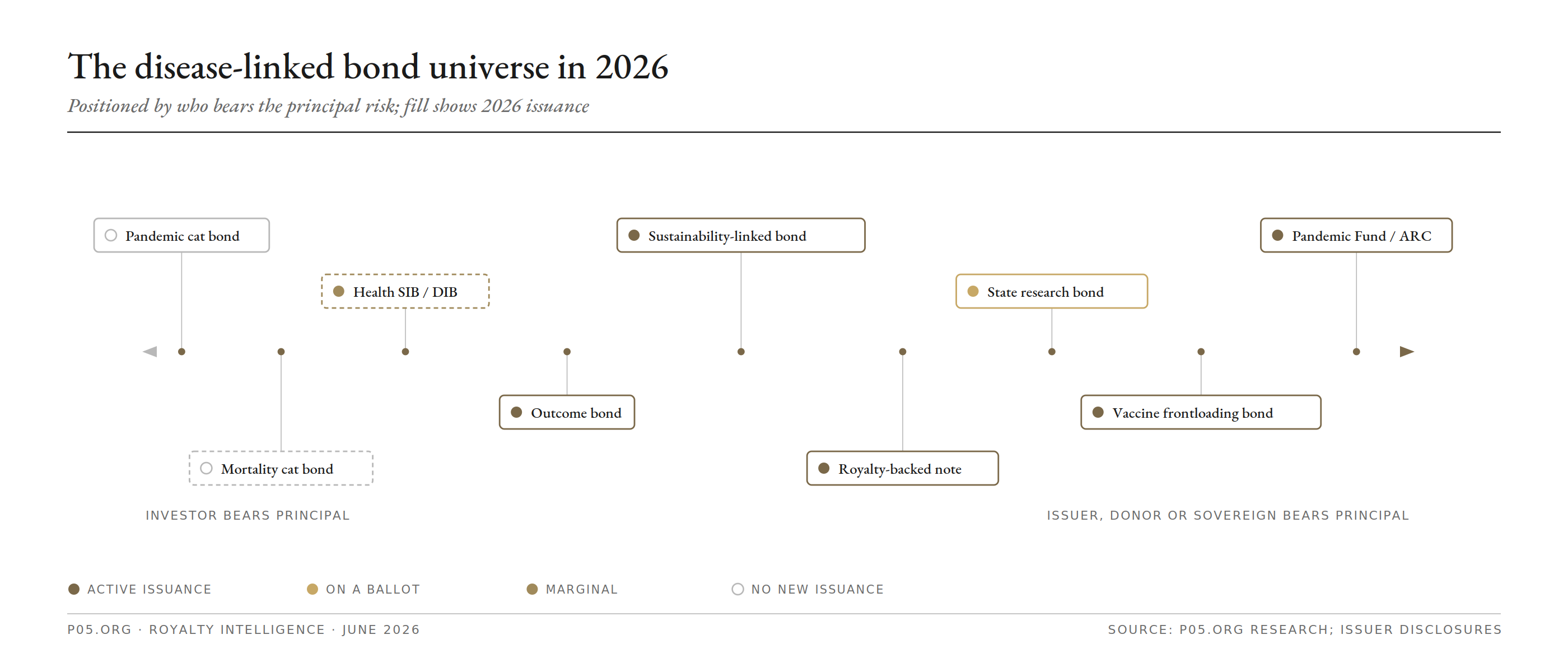

7. Summary: Where the Risk Sits

| Family | 2026 status | Principal at risk on | Return mechanism |

|---|---|---|---|

| Pandemic cat bond | No issuance | Parametric trigger | High coupon, principal loss on trigger |

| Mortality cat bond | Run-off | Mortality index | Coupon, principal loss on index breach |

| Sovereign epidemic insurance (ARC) | Active, expanding | Member-funded mutual | Parametric payout on outbreak size |

| Pandemic Fund | Active (grants) | Not applicable | Not applicable |

| State research bond | On a ballot | Issuer credit | GO coupon, plus optional revenue recoupment to the state |

| Outcome bond | Active | Outcome (coupon only) | Principal protected, success payment on a measured result |

| Vaccine frontloading bond | Active | Donor credit | Fixed coupon, tight supranational spread |

| Royalty-backed note | Active | Product revenue | Tiered royalty to a MOIC cap |

| Sustainability-linked health bond | Active | Issuer credit | Coupon step-up if KPI missed |

| Health SIB / DIB | Marginal | Measured outcome | Outcome-contingent payment |

Every family that places principal at risk on a trigger or a measured outcome saw little or no new issuance in 2026. Every family that rests on a sovereign, a donor, or a defined revenue line continued to price. Outcome bonds and sustainability-linked bonds occupy the middle, protecting principal and placing only the coupon at risk.

8. What Would Change the Picture

- A yes vote on the California immunology bond in November would make the state cures bond a replicable template. The signal to watch afterward is whether the 20% pricing discount deters the commercial partners the recoupment depends on.

- Any new pandemic or epidemic catastrophe bond from a reinsurer or multilateral would end the no-issuance pattern, and would appear first in the insurance-linked securities market. ARC's planned 2026 disease expansion is the nearest live development, though in insurance rather than bond form.

- A sustained United States withdrawal from Gavi would not impair outstanding IFFIm bonds but would shrink the programme they fund.

- A health-linked World Bank outcome bond, reusing the UNICEF COVID-19 precedent with a defined health metric, is the most likely route to a new disease-outcome instrument at investment grade.

All information in this article was accurate as of the research date and is derived from publicly available sources including official ballot filings and Legislative Analyst's Office materials, World Bank, GEF, IFFIm, ARC, and corporate issuer disclosures, company filings, peer-reviewed literature, and financial news reporting. Coupon, spread, step-up, and repayment terms are as reported at pricing and may have changed. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.