When Does the Money Stop? Modeling Royalty Stream Expiry in Pharmaceutical Transactions

The single most consequential variable in any royalty valuation is the terminal date — the point at which cash flows cease. Getting this wrong by even two years can shift an asset's net present value by 15–25%. Yet the mechanics of royalty expiry remain among the least well-understood aspects of pharmaceutical deal structuring, because the answer to "when does this royalty end?" is almost never as simple as "when the patent expires."

This article examines how royalty stream duration is determined, how it varies across deal architectures, what legal constraints apply to post-patent royalties, how the institutional royalty funds approach duration modeling, and where the analytical alpha resides for investors and transaction structurers.

The Default Assumption — and Why It Is Usually Wrong

The instinctive assumption — royalty term equals patent term — holds in a meaningful minority of deals, particularly older university out-licenses and composition-of-matter-linked agreements. But in practice, pharmaceutical license agreements define royalty obligations independently from patent life. The royalty term is a contractual construct. Patents may set a ceiling, a floor, or neither.

Royalty Pharma's 2025 10-K states this with precision: the duration of a royalty can be based on regulatory and marketing approval dates, patent expiration dates, the number of years from first commercial sale, the first date of manufacture of the patent-protected product, the entry of generics, or a contractual date arising from litigation — all impacted by the point in the product's life cycle at which the royalty is acquired. Royalty Pharma further notes that where a royalty term is linked to the existence of valid patents, management is required to make judgments about the patent providing the strongest protection to align the period over which it forecasts expected future cash flows to the royalty term. It is common for the latest-expiring patent in effect at acquisition to be extended, adjusted, or replaced with newer-dated patents in subsequent periods.

The estimated weighted average duration of Royalty Pharma's portfolio is approximately 13 years based on projected cumulative cash royalty receipts, per its UK Annual Report. Several of its marketed royalties have unlimited durations and could provide cash flows for many years after key patents have expired.

This is not a theoretical concern. It is the central modeling challenge for every participant in the royalty financing market.

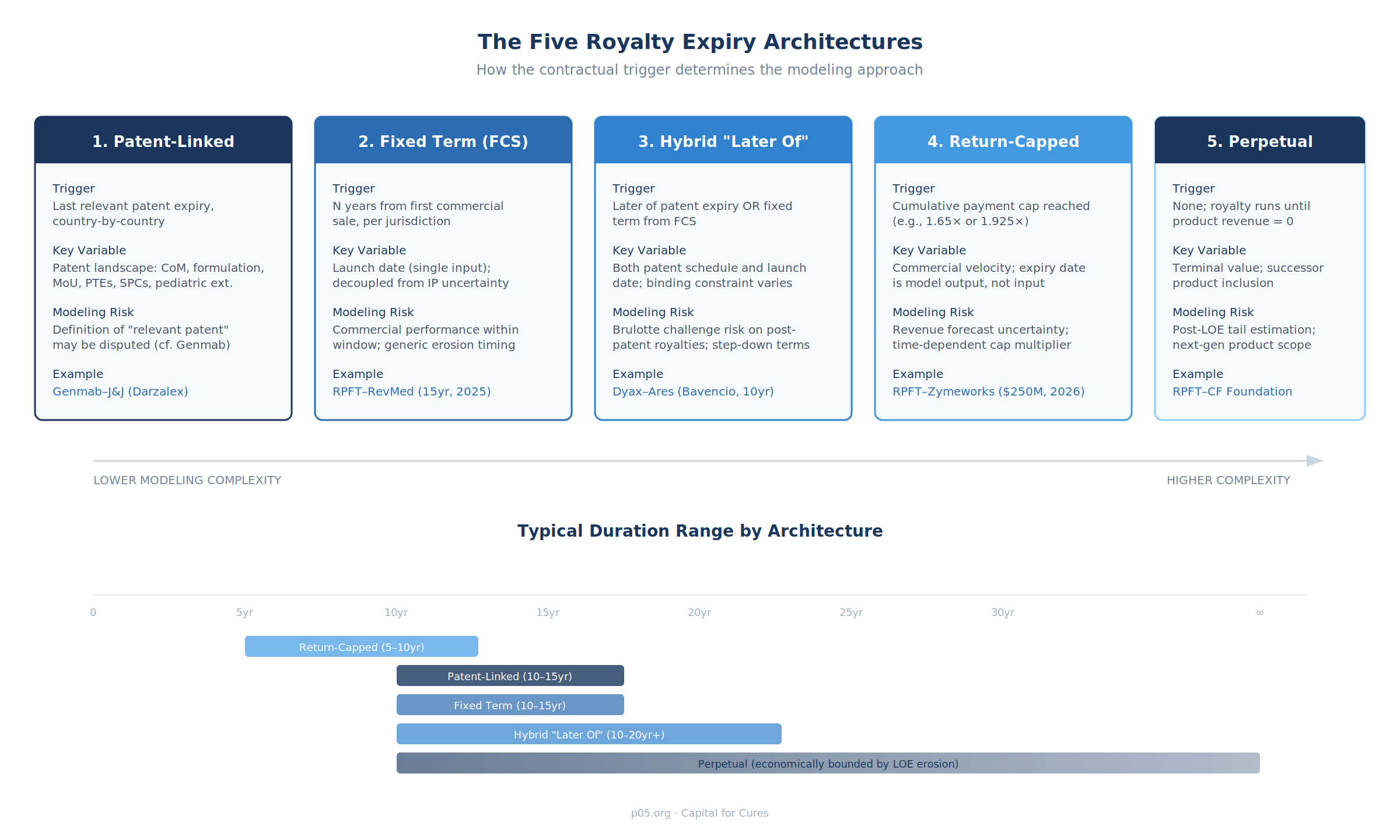

The Five Expiry Architectures

Across the pharmaceutical royalty market, five distinct expiry architectures account for the vast majority of transactions. Each creates a fundamentally different modeling challenge and risk profile.

1. Patent-Linked Expiry

Royalties terminate on a country-by-country basis upon expiration of the last relevant patent in each jurisdiction. This is the most common structure in university out-licenses, composition-of-matter deals, and older pharma-to-pharma agreements.

The Genmab–Janssen daratumumab license illustrates the mechanics and the risks. The license agreement specifies that Janssen's royalty obligation expires country-by-country on the later of 13 years after first commercial sale or upon expiration of the last-to-expire relevant Genmab-owned patent. The composition-of-matter patents did not begin to expire until March 2026, with U.S. patents (including patent term extensions) expiring around 2029 and European patents around 2031.

This structure became the subject of binding arbitration in 2020–2022, when the parties disputed whether "relevant patent" included Janssen-owned formulation patents covering the subcutaneous formulation of daratumumab (DARZALEX FASPRO), which would not expire until the mid-2030s, or only Genmab-owned patents. The tribunal ruled in Janssen's favour: the royalty obligation extends only through the last-to-expire relevant Genmab-owned patent, not Janssen's own patents.

The financial significance of this distinction is material. On a product generating over $10 billion in annual global revenue, the difference between a royalty terminating in the late 2020s versus the mid-2030s represents billions of dollars in present value. Genmab disclosed in its annual filing that it expects royalties to begin to decline materially in 2029 following the expiration of U.S. patent rights — a statement that effectively signals the binding constraint for valuation purposes.

Modeling implications. Patent-linked royalties require a granular, jurisdiction-by-jurisdiction patent schedule that accounts for patent term extensions (PTEs under Hatch-Waxman in the US, limited to 5 years), supplementary protection certificates (SPCs in Europe, up to 5 years plus an additional 6-month pediatric extension), and any pediatric exclusivity extensions (6 months in the US). The "patent expiry date" is not a single number — it is a matrix of dates, and the definition of "relevant patent" in the license agreement determines which entries in that matrix control the royalty term.

2. Fixed Term from First Commercial Sale

Royalties run for a defined number of years from the date of first commercial sale in each country, regardless of patent status. This structure decouples the royalty term from IP uncertainty entirely, making it the cleanest to model but also the most exposed to commercial performance risk within the window.

The Royalty Pharma–Revolution Medicines transaction announced in June 2025 is the clearest recent example of this architecture at scale. Royalty Pharma committed up to $1.25 billion in exchange for tiered royalties for a fixed term of 15 years on worldwide annual net sales of daraxonrasib, with the royalties decreasing based on sales tiers and falling to zero for sales above $8 billion. The $1.25 billion synthetic royalty component is structured into five tranches of $250 million each, with the first two tranches payable prior to FDA approval.

The SEC filing specifies the termination mechanics with jurisdiction-level precision: royalties on U.S. sales end 15 years after the first commercial sale of daraxonrasib in the United States; royalties outside the United States end 15 years after the first commercial sale in the European Union. The companion molecule, zoldonrasib (RMC-9805), has a more complex trigger: its royalty term ends 15 years after the earlier of its approval in an overlapping indication with daraxonrasib or the first commercial sale of daraxonrasib — a "first-to-trigger" mechanism that ties the companion product's royalty window to the lead product's timeline.

The resulting royalty duration is estimated at 2038–2041 depending on launch timing across jurisdictions.

Modeling implications. The modeling advantage is that the key input is a single variable per jurisdiction (expected launch date) rather than a full patent landscape analysis. The modeling risk shifts entirely to commercial performance, generic/biosimilar erosion timing within the window, and whether the 15-year window extends far enough beyond loss of exclusivity to capture meaningful tail value. The tiered structure (royalties decreasing with sales, zero above $8 billion) creates a concave payoff profile that must be modeled with explicit sales scenarios, not point estimates.

3. Hybrid "Later Of" Clauses

The most sophisticated and increasingly common structure in pharma licensing defines the royalty term as the later of two or more triggers — typically the later of patent expiry or a fixed number of years from first commercial sale. This creates an asymmetric duration profile: the royalty has a guaranteed minimum life (the fixed-term floor) and a contingent extended life (the patent ceiling, or vice versa).

The Dyax–Ares collaboration agreement governing Bavencio (avelumab) is the textbook example — and one that generated significant litigation. Ares agreed to pay royalties on net sales of therapeutic antibody products developed from Dyax-discovered antibody fragments until the later of the expiration of the licensed patents and ten years after the first commercial sale. The licensed CAT patents expired in 2018, but the first commercial sale of Bavencio occurred in 2017, extending the royalty obligation to 2027 — nine years beyond patent expiry. The contract did not include a royalty step-down when the licensed patents expired, a structural choice that became the basis for Ares's Brulotte challenge (discussed below).

A variant of this structure appears in the Genmab–Janssen agreement, where the royalty term runs country-by-country on the later of 13 years after first sale or the expiration of the last-to-expire relevant patent — but also includes customary reduction events. The royalties are subject to reduction upon patent expiration or invalidation in the relevant country and upon the first commercial sale of a biosimilar product in that country for as long as the biosimilar remains for sale. This creates a three-layered duration model: the term is the later of two triggers, but the rate steps down upon the occurrence of specified events within that term.

Modeling implications. "Later of" structures create a two-scenario framework where both patent landscape and launch timeline must be modeled simultaneously. The binding constraint will differ by country — in a jurisdiction where the product launched early and patents were extended, the patent prong may control; in a jurisdiction where launch was delayed and no PTE was granted, the fixed-term prong controls. The royalty rate may also vary within the term if step-down provisions apply, creating a kinked cash flow profile that requires separate pre- and post-step-down modeling.

4. Return-Capped Structures

In royalty-backed note financings and certain synthetic royalty transactions, the royalty stream does not expire on a calendar date — it expires when a cumulative payment cap is reached. The duration is therefore a function of commercial velocity, not calendar time or patent status. The "expiry date" is an output of the model, not an input.

The Royalty Pharma–Zymeworks $250 million non-recourse royalty-backed note from March 2026 uses this architecture with a time-dependent cap multiplier. Royalty Pharma receives 30% of worldwide tiered royalties on Ziihera (zanidatamab) until cumulative payments reach 1.65× the note amount ($412.5 million) if achieved by December 31, 2033, or 1.925× ($481.25 million) if achieved at any time thereafter. Full royalty rights revert to Zymeworks once the cap is reached. Zymeworks described this structure as creating a longer-term duration than a traditional royalty loan, with duration risk shared between the parties.

The NANOBIOTIX–HealthCare Royalty agreement from October 2025 adds a further structural layer: after the return cap is reached (approximately 1.75× MOIC if repayment is completed by end of 2030, increasing to 2.50× MOIC thereafter), a reduced royalty tail period commences. This tail period entitles HCRx to a predefined, reduced share of royalties not to exceed $14.9 million per year, and expires 10 years after the first commercial sale of JNJ-1900 (NBTXR3) in the US. The structure thus creates two sequential duration phases: a return-capped phase and a fixed-term tail phase.

The GENFIT–HealthCare Royalty agreement from January 2025 introduces an annual sales cap overlay: HCRx receives royalties on Iqirvo (elafibranor) only up to an annual maximum based on €600 million in net sales, with GENFIT retaining 100% of royalties above that threshold. The cumulative payment to HCRx is capped at a maximum value and subject to time limits, after which all future royalties revert to GENFIT.

Modeling implications. Return-capped structures require a revenue forecast model that calculates cumulative royalty payments year by year and determines when the cap is breached. The time-dependent multiplier in the Zymeworks deal creates a step function: the IRR to the investor is materially higher if the cap is reached before 2033 (1.65×) versus after (1.925×), meaning the model must assess the probability of early versus late cap attainment. The tail period in the NANOBIOTIX deal requires a second-phase model layered on top of the first. In all cases, the sensitivity of the duration to commercial assumptions is much higher than in patent-linked or fixed-term structures.

5. Perpetual Royalties

Some royalties have no contractual end date. They run in perpetuity — or more precisely, until the underlying product generates no further revenue.

Royalty Pharma's interest in the Vertex cystic fibrosis franchise is the most significant perpetual royalty in the pharmaceutical market. The royalties are perpetual and not tied to patent expirations — they originated from the Cystic Fibrosis Foundation's funding of Vertex's CF programme and were acquired by Royalty Pharma across multiple transactions. In its 10-K, Royalty Pharma notes that while the royalty is perpetual, it estimates expected Trikafta patent expiration in 2037 and potential generic entry thereafter leading to sales decline. For Alyftrek, which incorporates deutivacaftor, Royalty Pharma has applied an end date of 2039–2041 for purposes of accreting income over the royalty term.

The perpetual nature of this royalty creates a distinctive valuation challenge: the question is not "when does the royalty end?" but "what is the terminal value of an indefinite cash flow stream subject to competitive erosion?" Royalty Pharma has publicly argued that deutivacaftor is the same as ivacaftor and is therefore royalty-bearing, which would result in a blended royalty of approximately 8% for Alyftrek — a position that, if upheld, extends the economic life of the perpetual royalty to a next-generation product with its own patent estate and exclusivity period.

Modeling implications. Perpetual royalties require explicit terminal value assumptions. The standard approach is to model cash flows explicitly through the expected period of patent protection, then apply a post-LOE erosion curve to model the tail. The discount rate applied to the perpetual tail should reflect the heightened uncertainty of post-LOE cash flows. The successor product question — whether next-generation formulations or combinations fall within the royalty-bearing definition — is a legal and contractual determination that can have multi-billion-dollar valuation consequences, and must be modeled as a probability-weighted scenario rather than a binary assumption.

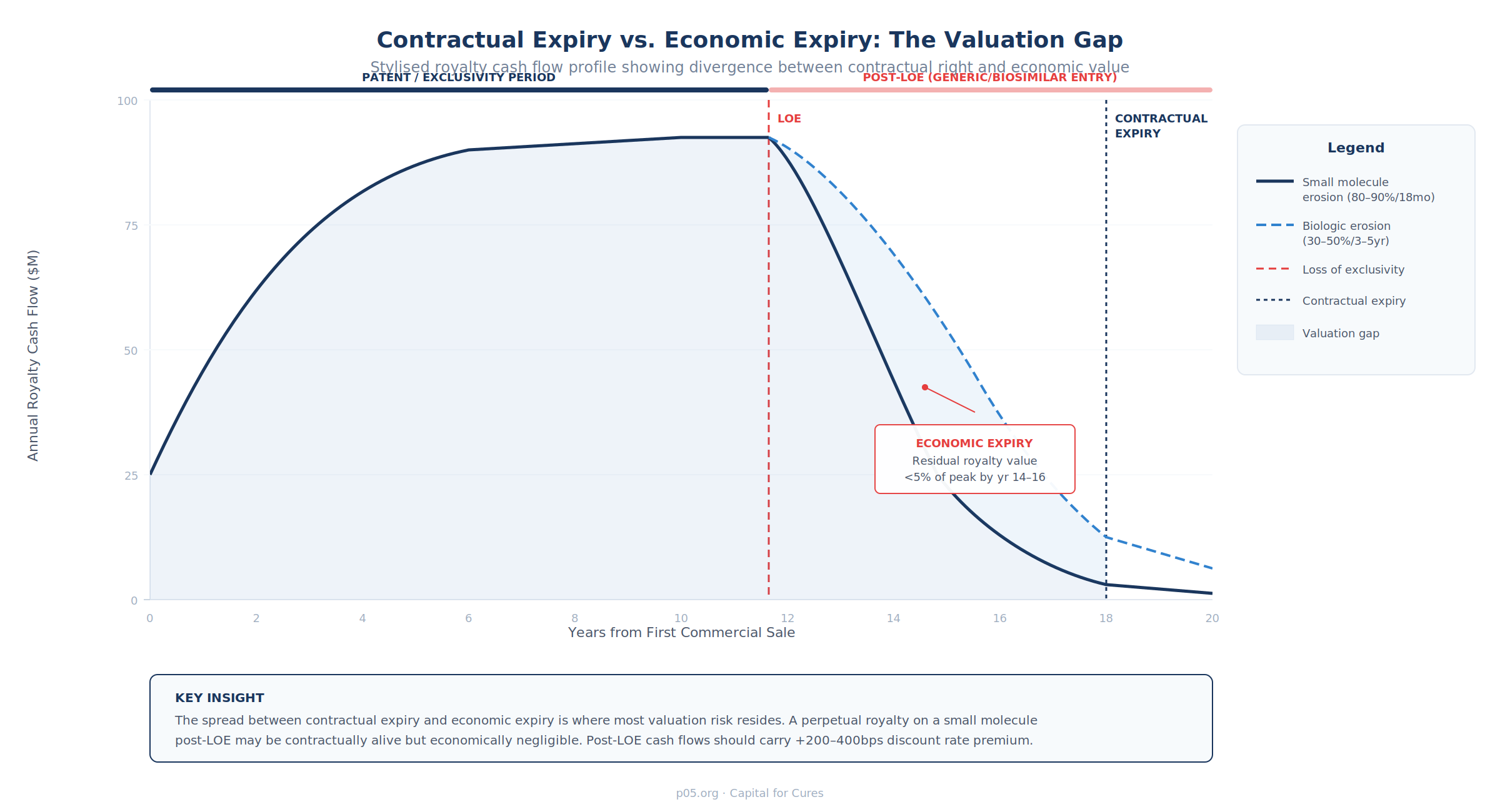

Contractual Expiry vs. Economic Expiry: Where the Valuation Risk Lives

The critical analytical distinction is between the contractual right to receive royalties and the economic value of that right given competitive dynamics. A royalty that survives patent expiry but sits on a product facing generic or biosimilar competition is worth far less than its pre-LOE headline rate implies.

Generic Erosion Dynamics

The post-LOE erosion profile is determined primarily by two factors: molecule type and competitive entry dynamics.

Small molecules. The empirical evidence is extensive and the pattern well-characterised. Revenue erosion of 70–90% typically occurs within the first 12–18 months of generic entry in the US. The depth and speed of erosion are strongly correlated with the number of generic entrants: the first generic entrant (often with 180-day exclusivity under Hatch-Waxman) may capture modest share with a limited price discount, but the entry of a second and third competitor triggers what has been described as a "competitive collapse" in pricing. In markets with 10 or more generic competitors, prices can decline by 90% or more from the branded level.

The shape of the erosion curve is further modulated by formulation complexity (oral solid dosage forms erode faster than complex injectables), payer substitution policies (mandatory generic substitution accelerates erosion), and brand loyalty dynamics. Lipitor (atorvastatin) exhibited near-vertical revenue decline; Advair (fluticasone/salmeterol), with its complex inhaler device, followed a much shallower trajectory over several years.

Biologics. Biosimilar erosion follows a fundamentally different dynamic. Typical year-one erosion is 20–40%, with the full erosion curve extending over 3–7 years rather than 12–18 months. The slower pace reflects manufacturing complexity limiting the number of entrants, the absence of automatic substitution in most jurisdictions (interchangeability designation is rare), physician and patient switching inertia, and the ability of reference product manufacturers to maintain formulary access through rebate strategies and patient support programmes.

The Humira (adalimumab) biosimilar entry — the largest biologic LOE event to date — demonstrated that even with multiple biosimilar entrants, the reference product can retain meaningful market share for several years through formulary management and patient programme retention.

Erosion modeling approaches. Three quantitative approaches are standard:

First, empirically derived price erosion curves based on historical analogs, matched by therapeutic area, formulation type, and competitive landscape. The key insight from a 2025 PubMed analysis of 140 originator drugs is that post-LOE sales decline follows a predictable but heterogeneous trajectory best modeled using a three-parameter exponential decay function, with subgroup variation by year of generic entry, therapeutic class, and product-specific features.

Second, Bass diffusion models, which approach the problem from the generic entrant's perspective — modeling the uptake and adoption of the generic product through a population based on "innovation" (early adopters switching independently) and "imitation" (later adopters switching based on peer behaviour) coefficients. The standard meta-analysis parameters (p = 0.03, q = 0.38) provide a reasonable baseline but should be calibrated to therapeutic-area-specific analogs.

Third, Monte Carlo simulation of generic entry timing, layering probability distributions over the date of first generic entry, the number of entrants over time, and the resulting price and volume impact. This approach is particularly valuable for biologics where the timing and probability of biosimilar entry is less certain than for small molecules.

The IRA as a Non-Patent LOE Event

The Inflation Reduction Act of 2022 introduced a new, non-patent-based mechanism for revenue reduction that must be incorporated into any forward-looking royalty duration model. Medicare price negotiation applies to small molecules selected 9 years post-approval and biologics 13 years post-approval. The negotiated price, once effective, applies to Medicare Part D (and from 2028, Part B) purchases. For products where Medicare represents a significant share of volume, the IRA negotiation creates a revenue inflection point that is independent of patent status and may precede, coincide with, or follow patent expiry.

The modeling implication is that the revenue base on which the royalty is calculated may decline before the royalty term expires, even absent generic entry. This is a form of "economic compression" that reduces the present value of post-IRA-negotiation royalty cash flows.

The Brulotte Constraint: Post-Patent Royalties Under US Law

For royalties that extend beyond patent expiry — either through "later of" clauses, fixed-term structures, or perpetual terms — the legal enforceability under US law has been an active area of litigation, and the September 2024 Third Circuit decision in Ares Trading S.A. v. Dyax Corp. represents the most significant clarification in a decade.

The Brulotte/Kimble Framework

The Supreme Court's 1964 decision in Brulotte v. Thys Co. established that royalties calculated based on post-expiration use of a patented invention are unenforceable per se — they constitute an impermissible extension of the patent monopoly. The 2015 Kimble v. Marvel Entertainment, LLC decision affirmed and clarified this rule, identifying several permissible structures: deferred payments for pre-expiration use amortised over a post-expiration period; royalties running until the latest-running patent in the licensed portfolio expires; royalties tied to non-patent rights (copyrights, trademarks, trade secrets) with appropriate structuring; and business arrangements involving equity or joint ventures that allocate commercialisation risk.

The Ares v. Dyax Decision (3d Cir. 2024)

The Third Circuit's September 2024 decision addressed a set of facts common in pharmaceutical deal-making and provided critical guidance for royalty structurers.

Dyax had a phage display antibody fragment discovery platform. In 2006, Ares entered a collaboration agreement under which Dyax used the platform to identify antibody fragments targeting PD-L1 for Ares. Dyax granted Ares a license to the platform patents (the CAT patents). Ares agreed to pay royalties on net sales of therapeutic antibody products developed from Dyax-discovered antibodies until the later of patent expiry and ten years after first commercial sale. The CAT patents expired in 2018. Bavencio launched in 2017. The royalty obligation therefore extended to 2027 — nine years beyond patent expiry. The agreement did not include a royalty step-down upon patent expiry.

The Third Circuit held that Brulotte was inapplicable. The court reasoned that the royalty obligation was not calculated based on activity requiring post-expiration use of the inventions covered by the CAT patents. Ares never practiced the licensed patents to develop Bavencio; the manufacture and sale of Bavencio did not practice the phage display inventions. The royalties were effectively reach-through royalties — compensation for a product whose discovery was enabled by practicing the patented technology, but whose manufacture and sale does not itself require practicing that technology.

Implications for Royalty Duration Modeling

The Ares v. Dyax decision has two practical implications for duration modeling:

First, for reach-through royalties and platform technology licenses — increasingly common in antibody discovery, mRNA technology, gene therapy, and AI-driven drug discovery — the Brulotte constraint does not apply where the royalty-bearing product does not itself practice the licensed patents. Parties are free to agree to any royalty term they wish, including terms extending well beyond patent expiry without a step-down. This expands the available duration of royalty streams in platform licensing deals.

Second, for direct product-patent licenses — where the royalty-bearing product does practice the licensed patents — the standard market solution remains the post-patent step-down. As Freshfields noted, in life sciences deals involving both patent and know-how licenses, it is customary to reduce royalties upon patent expiry, with the residual rate attributed to the know-how component. The typical step-down is 30–50% of the pre-expiry rate. Modeling post-patent cash flows for these structures requires a two-rate framework: the full rate through patent expiry, and the stepped-down rate from patent expiry to the end of the contractual term.

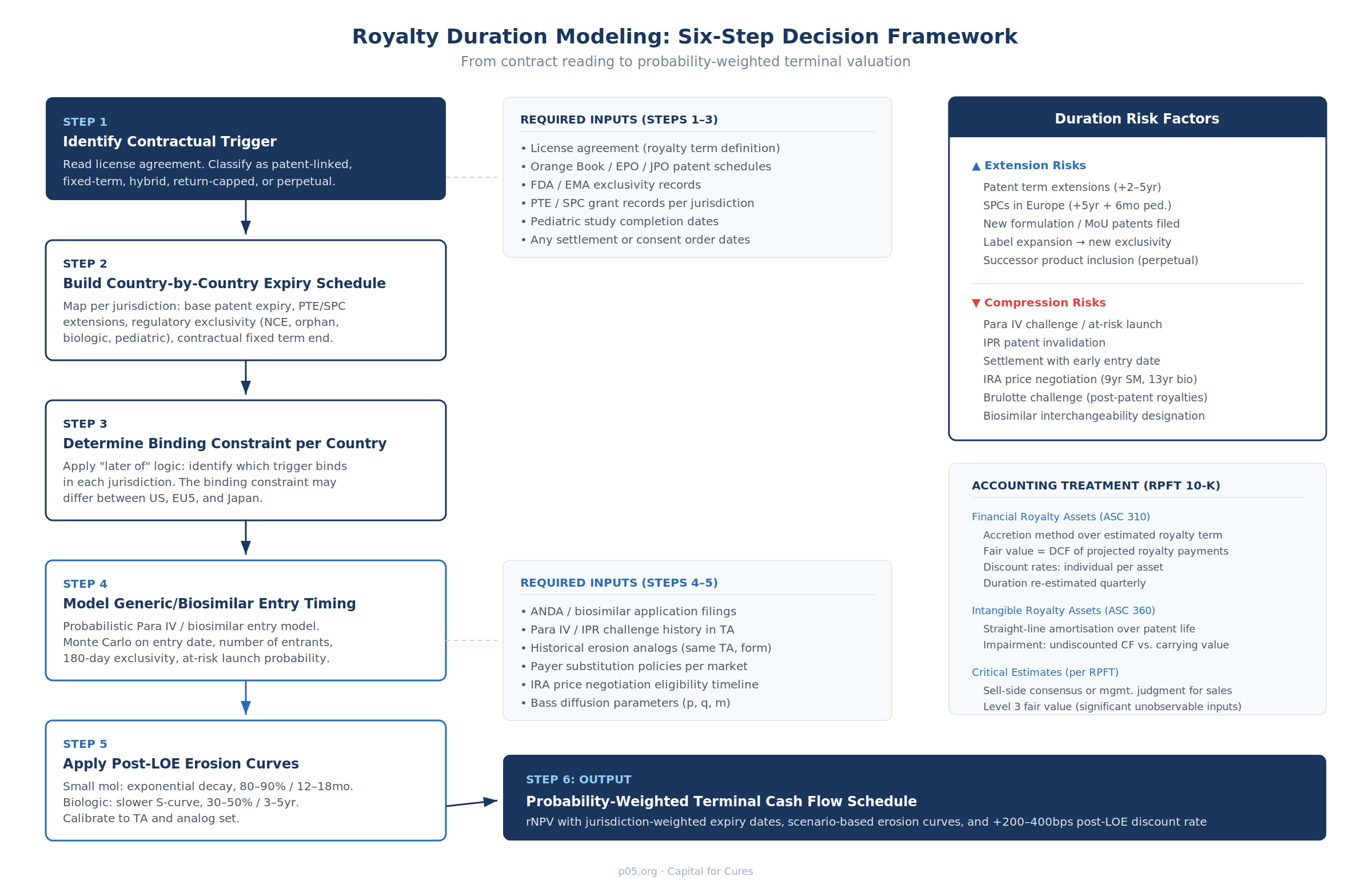

The Modeling Framework

Step 1: Identify the Contractual Trigger

Read the license agreement. Classify the expiry architecture as patent-linked, fixed-term, hybrid, return-capped, or perpetual. If patent-linked, determine precisely how "relevant patent" is defined — the Genmab–Janssen arbitration demonstrates that this single definitional question can shift the royalty duration by five or more years on a multi-billion-dollar product.

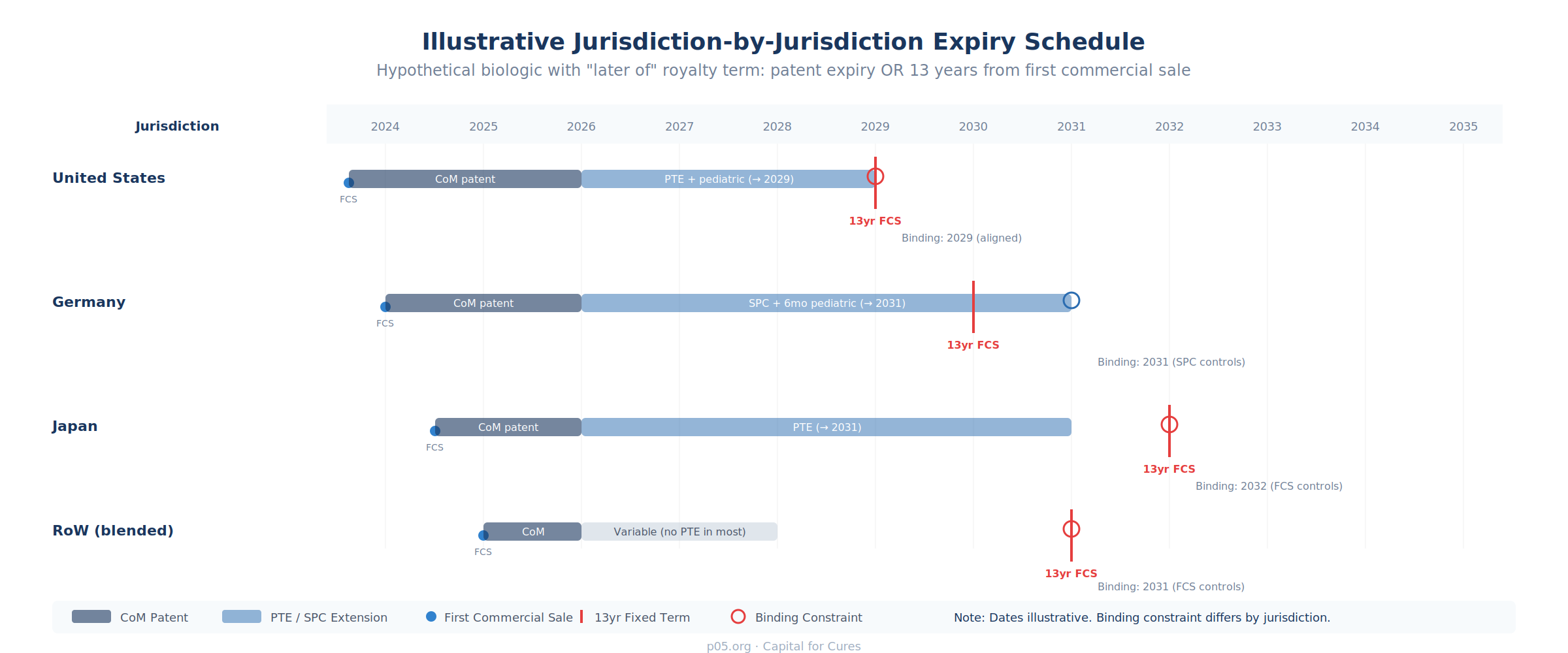

Step 2: Build Country-by-Country Expiry Schedules

For patent-linked and hybrid structures, construct a jurisdiction-by-jurisdiction matrix mapping the following for each major market (US, EU5, Japan, and RoW at minimum):

The key data sources are the FDA Orange Book (US patent and exclusivity listings), the European Patent Office and national SPC registers (EU patent and SPC data), the Japan Patent Office (JPO patent data), and the relevant regulatory authority's exclusivity records. Patent term extensions must be individually verified: in the US, the Hatch-Waxman PTE is limited to a maximum of 5 years and cannot extend the total patent life beyond 14 years from FDA approval; in Europe, SPCs can extend protection by up to 5 years (plus a 6-month pediatric extension where applicable).

Step 3: Determine the Binding Constraint per Country

Apply the "later of" (or other contractual) logic to each jurisdiction. The binding constraint — the trigger that actually determines when royalties cease in that country — may differ across jurisdictions. In the illustrative schedule above, the US binding constraint is the PTE-extended patent plus pediatric exclusivity (2029), while Japan's binding constraint is the 13-year fixed term from first commercial sale (2032) because the PTE-extended patent (2031) expires earlier than the fixed-term end date.

Step 4: Model Generic/Biosimilar Entry Timing

Construct a probabilistic model of the date of first generic or biosimilar entry in each major jurisdiction. Key inputs include: the number of ANDA or biosimilar applications filed or expected; historical Paragraph IV challenge success rates in the therapeutic area; the strength of secondary patent protection (formulation, method-of-use, device patents); settlement patterns (including agreements permitting early generic entry, as with the Merck–Januvia settlement permitting generic launch in May 2026); and any at-risk launch probability assessments.

Run Monte Carlo simulation across these inputs to generate a probability-weighted distribution of generic entry dates. The divergence between the nominal patent expiry date and the probable LOE date — which can be three to seven years for a well-constructed patent thicket, or negative two years for a portfolio vulnerable to inter partes review — is a critical source of model sensitivity.

Step 5: Apply Post-LOE Erosion Curves

Layer the generic/biosimilar erosion model onto the revenue forecast from the LOE date forward. The erosion curve should be calibrated to the specific molecule type, formulation, therapeutic area, and competitive dynamics:

| Parameter | Small Molecule | Biologic |

|---|---|---|

| Year 1 revenue retention | 10–30% | 60–80% |

| Time to 90% erosion | 12–24 months | 5–7 years |

| Key erosion driver | Automatic substitution, price collapse | Physician switching, formulary negotiations |

| Number of entrants at Year 1 | 3–10+ | 1–3 |

| Model type | Exponential decay | Modified S-curve / Bass diffusion |

| Interchangeability impact | N/A (automatic substitution) | Accelerates erosion by 20–40% |

For perpetual royalties, the erosion curve does not terminate the cash flow stream — it asymptotically approaches zero while the contractual right persists. The tail value of a perpetual royalty post-LOE may be minimal in absolute terms but can have non-trivial present value if the discount rate applied to the tail is insufficiently high.

Step 6: Construct the Probability-Weighted Terminal Cash Flow Schedule

Combine the outputs of Steps 3–5 into a single probability-weighted cash flow schedule. For each jurisdiction:

- Pre-LOE cash flows are discounted at the base royalty discount rate (reflecting product-level commercial risk, counterparty credit risk, and deal-specific structural features).

- Post-LOE cash flows should carry a discount rate premium of 200–400bps above the pre-LOE rate, reflecting the heightened uncertainty of generic competition dynamics, or alternatively should be modeled as probability-weighted scenarios (base/upside/downside) with explicit generic entry timing and erosion depth assumptions per scenario.

Royalty Pharma's 10-K discloses that the fair value of its financial royalty assets is calculated using projected royalty payments based on sell-side equity research analysts' consensus forecasts (or, where unavailable, management judgment), discounted to present value using individual discount rates per asset, and classified as Level 3 within the fair value hierarchy since the inputs are both significant and unobservable.

How the Institutional Royalty Funds Model Duration

Royalty Pharma (RPFT)

Royalty Pharma's accounting framework distinguishes between two asset classifications that embed different duration treatments:

Financial royalty assets (the majority of the portfolio) are accounted for under ASC 310, using the effective interest method. Income is accreted over the estimated royalty term. Management applies an estimated end date for each asset — which may be a patent expiry date, a contractual end date, or (for perpetual royalties) an applied end date based on estimated LOE and competitive dynamics. These estimates are periodically reviewed and updated as new information emerges. When royalties are received for financial royalty assets that have been fully amortised, the income is recognised as "Other royalty income."

Intangible royalty assets (currently limited to the Januvia/Janumet DPP-IV patents) are accounted for under ASC 360, using straight-line amortisation over the expected patent lives. The impairment test compares the carrying value with estimated future undiscounted cash flows. Critical estimates include changes in product demand, marketing strategy, pricing and reimbursement, and country-specific patent expiry dates.

The Q1 2025 10-Q provides asset-level duration estimates. Several entries are notable for duration variability: the Vertex CF franchise is perpetual, with an applied income accretion end date of 2035 that is periodically reviewed; the Alyftrek royalty is perpetual, with an estimated duration of 2039–2041 based on expected patent expiry and generic entry; and the Erleada royalty is perpetual with an applied end date.

HealthCare Royalty (HCRx)

HCRx's deal structures reveal a preference for capped return architectures with explicit duration boundaries. The REGENXBIO agreement (May 2025, up to $250 million) uses a bond structure where HCRx receives quarterly interest payments derived solely from royalty and milestone revenue, with the principal amount representing the cap. The NANOBIOTIX deal adds a royalty tail post-cap. The GENFIT deal adds annual sales caps. In each case, the duration is bounded by either the cumulative return cap, a time limit, or both — creating a defined maximum duration that limits downside but also caps upside relative to a perpetual or patent-linked structure.

Duration Variability: A Comparative Summary

| Deal Type | Typical Duration | Key Driver | Duration Certainty | Recent Example |

|---|---|---|---|---|

| University out-licence | Patent life (10–15yr from launch) | Last-to-expire relevant patent | Medium (patent challenges) | Genmab–J&J (Darzalex) |

| Synthetic royalty purchase | Fixed term (10–15yr from FCS) | Contractual term | High (launch date only) | RPFT–Revolution Medicines (15yr, 2025) |

| Royalty-backed note | Until return cap (5–10yr typical) | Commercial velocity | Low (revenue-dependent) | RPFT–Zymeworks (1.65×/1.925×, 2026) |

| Foundation/charitable royalty | Perpetual | No contractual end | Very low (LOE + successor) | RPFT–CF Foundation (Vertex CF) |

| Platform technology licence | Later of patent/fixed term | Hybrid | Medium (dual-trigger) | Dyax–Ares (Bavencio, 10yr + patent) |

| Capped royalty bond + tail | Cap then fixed tail | Cap + fixed tail | Medium | HCRx–NANOBIOTIX (cap + 10yr tail, 2025) |

| Royalty bond with sales cap | Until cumulative cap | Revenue; annual ceiling | Low | HCRx–GENFIT (€185M, annual cap, 2025) |

Conclusion

The answer to "when does this royalty end?" is architectural: it depends on which of the five expiry frameworks the deal employs, which country you are modeling, what the relevant patent landscape looks like in that country, how generic or biosimilar competition is likely to develop, and — in several landmark cases — what an arbitration tribunal or federal circuit court decides that "relevant patent" means.

The analytical alpha in royalty valuation lives in the spread between contractual expiry and economic expiry. A perpetual royalty on a small molecule product facing imminent LOE has a contractual duration of infinity and an economic duration of perhaps two to three years. A return-capped note on a pre-launch biologic has no defined contractual duration — it could be five years or fifteen — but the economic duration is bounded by the commercial trajectory of a single asset.

The institutional royalty funds have built sophisticated infrastructure around this problem: probabilistic patent models, Monte Carlo generic entry simulations, jurisdiction-by-jurisdiction expiry matrices, and periodic re-estimation of duration assumptions embedded in their financial reporting frameworks. For entrants to the market — whether biotech CFOs structuring their first royalty transaction, university tech transfer offices negotiating license terms, or investors evaluating a royalty acquisition — the starting point must be the license agreement itself, not any assumption about what "royalty term" typically means.

Because in pharmaceutical royalty financing, there is no typical.

All information in this article was accurate as of the publication date and is derived from publicly available sources including SEC filings, company press releases, regulatory announcements, legal firm publications, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.