Company of the week: Aktis Oncology

Aktis Oncology is a Boston radiopharmaceutical developer that did the opposite of last week's subject. Where Rallybio was hollowed into a shell and its one thin royalty ring-fenced into a contingent value right, Aktis spent 2024 and 2025 building a platform that big pharma paid to access, then opened 2026 with the year's first biotech IPO. For a royalty desk it is the cleaner, right-way-up version of the same diagram: a company that earns royalties on assets it licenses out while keeping full product economics on the pipeline it keeps.

Aktis Oncology, Inc. (Nasdaq: AKTS) is a clinical-stage company developing targeted alpha radiopharmaceuticals, drugs that ferry an alpha-emitting isotope directly into a tumor and deposit dense, hard-to-repair radiation damage over just a few cell diameters. Its differentiator is the delivery vehicle: a proprietary miniprotein radioconjugate platform that sits between antibodies and peptides, small enough to penetrate tumors quickly but engineered to internalise and stay put once it binds.

The science is the headline everywhere else. For this publication the interesting question is the cash-flow architecture around it. Aktis has structured its business so that one set of targets is licensed to Eli Lilly under a deal carrying tiered royalties and up to roughly $1.2 billion in milestones, while a second, separate set of targets, its own clinical pipeline, is retained outright with no upstream royalty burden at all. That split is the whole story for a royalty reader, and it is worth tracing precisely.

This piece does three things: it explains what Aktis actually is and how the miniprotein platform is meant to work; it follows the money through four private rounds and a January 2026 IPO to see who owns it; and it maps the royalty stack in both directions, showing where Aktis is a payee, where it keeps everything, and why that is unusual for a company this early.

At a glance

| Item | Detail |

|---|---|

| Company | Aktis Oncology, Inc. (Nasdaq: AKTS), Boston, Massachusetts |

| Founded | August 2020, incubated by MPM Capital (now MPM BioImpact) |

| Focus | Targeted alpha radiopharmaceuticals for solid tumors |

| Platform | Proprietary miniprotein radioconjugate platform, isotope-agnostic, actinium-225 |

| Lead program | [225Ac]Ac-AKY-1189, Nectin-4, Phase 1b (NECTINIUM-2), prelim data Q1 2027 |

| Second program | [225Ac]Ac-AKY-2519, B7-H3, Phase 1b in mCRPC, data 2027 |

| Partner | Eli Lilly discovery collaboration, $60M upfront, up to ~$1.2B milestones plus royalties |

| Capital raised | ~$346M private across four rounds, plus $318M IPO (~$365M with greenshoe), Jan 2026 |

| Status (Jun 2026) | Public, ~$1.3B market cap, cash of ~$538M (Mar 31), runway into 2028 |

What Aktis is, plainly

Radiopharmaceuticals work by attaching a radioactive isotope to a targeting molecule that homes in on a tumor. The field's commercial proof points are Novartis's Pluvicto and Lutathera, both beta-emitters. Aktis is betting on a different isotope class. Alpha-emitters such as actinium-225 release their energy over a far shorter range, producing dense double-strand DNA breaks that a cancer cell struggles to repair, in principle a more potent and more localised kill.

The hard part has never been the isotope; it is the targeting. Antibodies bind well but are large, slow to penetrate tumors, and linger in healthy tissue, a problem when the payload is radiation. Peptides penetrate fast but wash out before they do enough damage. Aktis's answer is the miniprotein: a chain of amino acids smaller than an antibody but larger than a peptide, engineered to penetrate quickly, internalise into the cancer cell, and be retained long enough for the alpha emission to matter, while clearing rapidly from everywhere else.

The platform is isotope-agnostic and theranostic: the same targeting miniprotein can carry an imaging isotope to confirm the tumor is lit up before a therapeutic dose is given. Aktis says it screens more than six billion variants across roughly 100 protein scaffolds, using generative AI and computational chemistry to find selective binders. None of this is in-licensed from a university in any disclosed agreement; it was built internally inside the MPM incubator. That detail matters later.

The pipeline: two owned programs, one partnered black box

Aktis runs three distinct streams, and they sit very differently on the royalty ledger.

| Program | Target | Stage / trial | Near-term milestone | Ownership |

|---|---|---|---|---|

| AKY-1189 | Nectin-4 | Phase 1b, NECTINIUM-2 (~150 patients) | Preliminary data Q1 2027 | Wholly owned by Aktis |

| AKY-2519 | B7-H3 | Phase 1b in mCRPC, basket trial late 2026 | Imaging/dosimetry, data 2027 | Wholly owned by Aktis |

| Lilly targets | Undisclosed | Discovery, Aktis to first human imaging | First milestone achieved | Licensed to Lilly |

[225Ac]Ac-AKY-1189 is the lead. It targets Nectin-4, the same antigen behind Pfizer and Astellas's antibody-drug conjugate Padcev (enfortumab vedotin), which did roughly $1.9 billion in 2024 sales. Around 80 to 90 percent of urothelial cancer patients express Nectin-4. The Phase 1b NECTINIUM-2 trial is enrolling about 150 patients across urothelial, triple-negative breast, non-small cell lung, colorectal, cervical, and head and neck cancers, with preliminary results expected in the first quarter of 2027. In February 2026 the FDA granted AKY-1189 Fast Track designation in metastatic urothelial cancer after progression on prior therapy.

[225Ac]Ac-AKY-2519 targets B7-H3, a protein common to aggressive tumors that respond poorly to checkpoint inhibitors. It has entered Phase 1b in metastatic castration-resistant prostate cancer, with a parallel basket trial in other solid tumors planned for late 2026 and first-in-human imaging and dosimetry data already reported. Both lead programs are wholly owned; neither carries an option or royalty owed to another party.

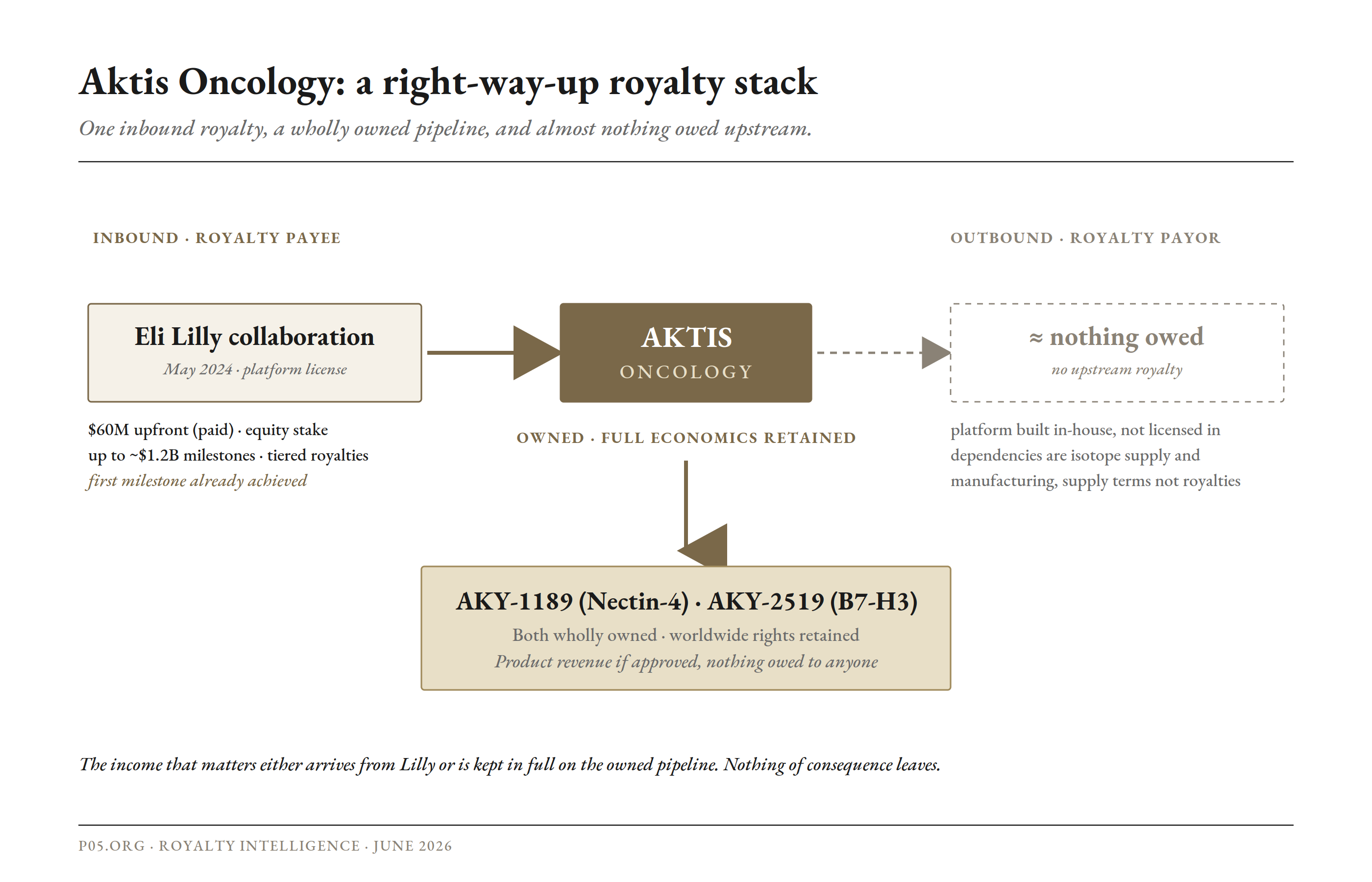

The third stream is the Lilly collaboration, and it is deliberately walled off from the first two. Aktis applies its platform to a defined set of targets that Lilly selects, targets that sit outside Aktis's own pipeline, and carries them through initial human imaging. From Phase 1 onward, Lilly owns development and worldwide commercialisation. That is the stream that generates royalties.

The royalty stack: a payee that kept its own book

Here is the part that matters for a royalty desk, and it is the mirror image of last week's Rallybio.

Aktis's royalty position has three layers, and the unusual feature is how clean each one is.

Inbound, the Lilly royalty. In May 2024 Aktis signed a licence, research and collaboration agreement with Eli Lilly. Aktis received a $60 million upfront cash payment plus an equity investment, and is eligible for up to roughly $1.1 to $1.2 billion in preclinical, clinical, regulatory and commercial milestones, plus tiered royalties on net sales. Aktis does discovery through first human imaging; Lilly does everything from Phase 1 to market. By May 2026, management said the first milestone had already been achieved. This is a genuine inbound royalty entitlement, originated by licensing out a slice of platform capacity that Aktis was never going to develop itself.

Owned, the internal pipeline. AKY-1189 and AKY-2519 are not royalty assets at all. Aktis retains worldwide rights, which means that if either reaches market the company collects product revenue, not a royalty, and owes nothing upstream on them. For a royalty buyer this is the important distinction: these are not licensable income streams today, they are wholly owned development assets whose value would be realised through product sales or an outright sale or partnering event later.

Outbound, almost nothing. Because the miniprotein platform was built in-house rather than in-licensed from an academic institution, Aktis carries no disclosed upstream royalty obligation on its core technology. Its dependencies are operational, not financial: actinium-225 isotope supply, which is genuinely constrained, and manufacturing, which Aktis is addressing by building its own cGMP radiopharmaceutical facility due online in the second half of 2026. Those are supply contracts, not royalty stacks.

| Direction | Source | What flows | Certainty |

|---|---|---|---|

| Inbound | Lilly collaboration | Up to ~$1.2B milestones plus tiered royalties on Lilly sales | Validated, first milestone hit; long-dated |

| Owned | AKY-1189, AKY-2519 | Full product economics if approved, worldwide rights retained | Early; Phase 1b, no efficacy data yet |

| Outbound | Core platform | No disclosed upstream royalty obligation | Clean; dependencies are supply and manufacturing |

The contrast with Rallybio's go-forward entity is exact. Avenzo, the oncology company reversing into the Rallybio shell, is a structural royalty payor: every asset in its pipeline owes tiered royalties upstream to the Chinese biotechs it licensed from. Aktis is the inverse. It is a net payee on the partnered stream and an unencumbered owner on its own. The cash flows of interest here are the ones arriving, or the ones Aktis keeps entirely, not the ones leaving.

Following the money: four rounds and the year's first IPO

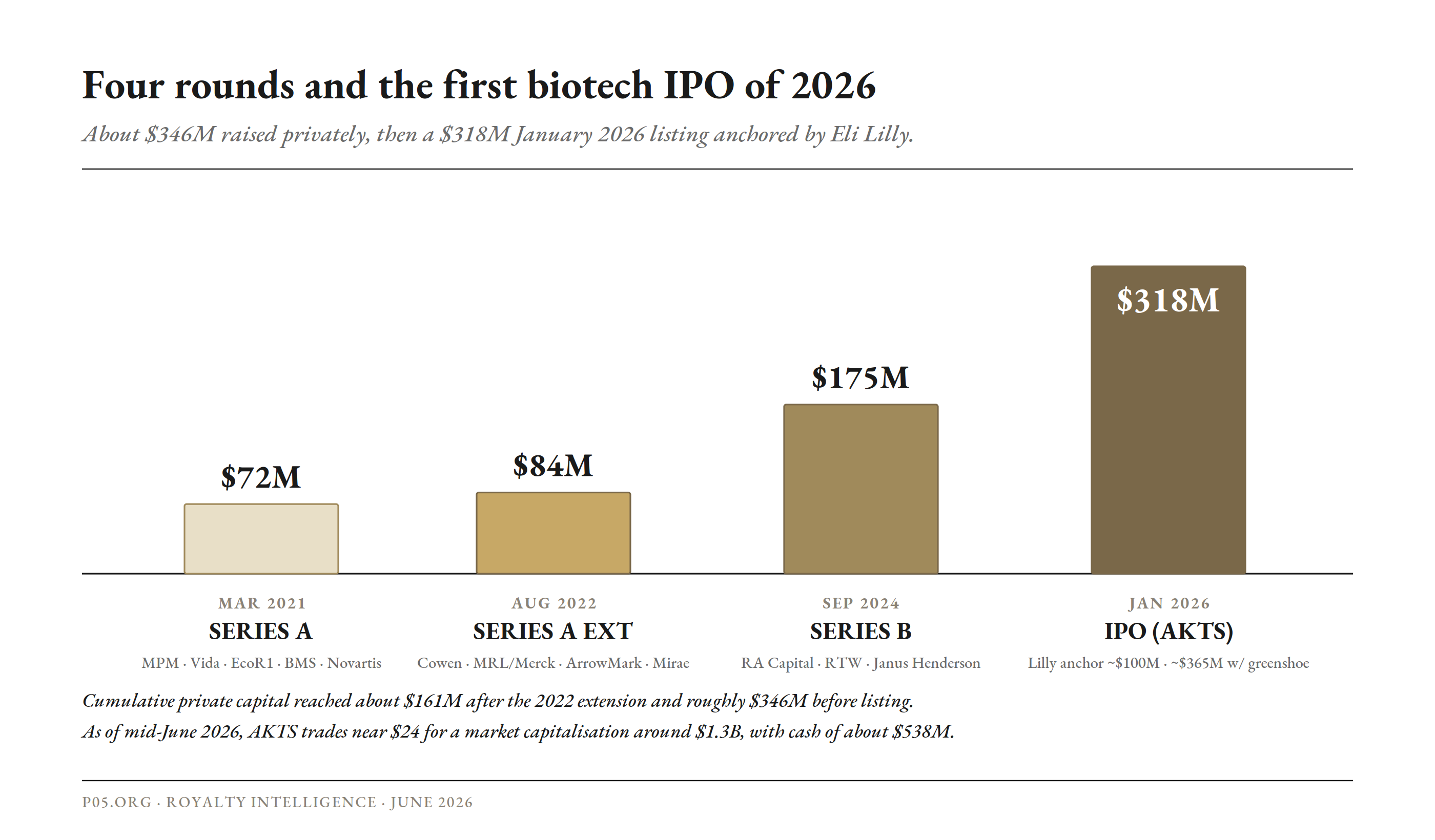

Aktis was founded in August 2020 by Todd Foley of MPM (now chair), MPM advisor Patrick Baeuerle, and Vida Ventures partner Brian Goodman, and incubated inside MPM. The financing history is a steady escalation of blue-chip crossover and strategic capital.

| Round | Date | Amount | Notable participants |

|---|---|---|---|

| Series A | Mar 2021 | $72M | MPM, Vida Ventures, EcoR1, Octagon, TCG Crossover, Bristol Myers Squibb, Novartis |

| Series A extension | Aug 2022 | $84M | Cowen Healthcare, MRL Ventures (Merck), ArrowMark, Mirae Asset, Timefolio, Pappas Capital |

| Series B | Sep 2024 | $175M | Led by RA Capital; co-led RTW, Janus Henderson; T. Rowe Price, Avidity; BMS, Lilly, MRL re-up |

| IPO | Jan 2026 | $318M | 17.65M shares at $18; Lilly anchored ~$100M (about one third) |

The private rounds totalled roughly $346 million. The investor list is the tell: three of the largest oncology pharmas, Bristol Myers Squibb, Novartis, and Merck (via its MRL Ventures Fund), all took strategic stakes, and Lilly converted its 2024 collaboration into an equity relationship that it then doubled down on at the IPO. When BMS, Novartis, Merck, and Lilly are all on the cap table of one small radiopharma company, the platform is being validated by the buyers most likely to acquire it.

The January 2026 IPO was the first biotech listing of the year and the third largest since the start of 2024. Aktis upsized to 17.65 million shares at $18, the top of the range, raising $318 million at roughly a $1 billion valuation, after Lilly stepped in to anchor the book with about $100 million. With the underwriters' overallotment fully exercised, aggregate gross proceeds reached about $365.4 million; J.P. Morgan, BofA Securities, Leerink Partners and TD Cowen ran the book, and the stock began trading on January 9. Before the offering, MPM held 17.4 percent and Vida 9.5 percent. Proceeds were earmarked at roughly $140 to $150 million for the AKY-1189 Phase 1b, $70 to $80 million for AKY-2519, and the balance for general corporate purposes, with runway into 2028.

As of mid-June 2026 the stock trades around the low $20s for a market capitalisation near $1.3 billion, against cash of about $538 million reported at the end of the first quarter. Collaboration revenue was modest, around $6.5 million for 2025, which is the accounting trace of the Lilly upfront and milestone recognition rather than any product income.

The wider context: a field being bought up

Aktis raised and listed into a radiopharmaceutical land grab. The sector has drawn an unusual run of large acquisitions as big pharma races to build alpha and beta capabilities.

| Acquirer | Target | Value | Date |

|---|---|---|---|

| Bristol Myers Squibb | RayzeBio | ~$4.1B | Late 2023 |

| Eli Lilly | Point Biopharma | ~$1.4B | Dec 2023 |

| AstraZeneca | Fusion Pharmaceuticals | ~$2B | Mar 2024 |

| Novartis | Mariana Oncology | ~$1B | May 2024 |

That backdrop is double-edged for Aktis. It explains why the company could raise $346 million privately and list successfully when the IPO window was otherwise shut, and it makes Aktis itself an obvious acquisition candidate. It also means the company competes for isotope supply, manufacturing capacity, and clinical talent against acquirers with far deeper balance sheets, including Lilly, which is both a partner and, through its own Nectin-4 and radioligand ambitions, a potential competitor.

Red team vs blue team

Risk analysis (red team)

No efficacy data exists yet. Both owned programs are in Phase 1b. AKY-1189's preliminary readout is not expected until the first quarter of 2027, and AKY-2519's data follows. Everything about the equity story and the value of the owned pipeline rests on dose-escalation results that have not arrived. Imaging and dosimetry are encouraging but are not anti-tumor activity.

The partner is also a competitor. Lilly validated the platform, anchored the IPO, and pays the royalties, but Lilly also owns Point Biopharma and is building its own radioligand franchise. A partner that large can reprioritise, and the targets it selected under the collaboration are an undisclosed black box whose progress Aktis does not control.

Isotope and manufacturing risk is real. Actinium-225 supply is constrained industry-wide. Aktis is mitigating by building its own cGMP facility, but that plant is not yet operational, and a radiopharmaceutical company that cannot reliably source and manufacture its isotope has no product regardless of how good the biology is.

The royalty stream is long-dated and indirect. The Lilly royalty is tiered and contingent on Lilly carrying undisclosed targets all the way to market. The milestones are real and the first has triggered, but commercial royalties are years away and depend on a third party's execution.

Crowded targets. Nectin-4 is already addressed by Padcev, a multi-billion-dollar ADC, and B7-H3 is a popular target across modalities. Aktis is betting that an alpha radioconjugate is differentiated enough to matter in fields where antibody approaches already have a head start.

Opportunities and mitigants (blue team)

The cap table is an acquisition thesis in itself. Bristol Myers Squibb, Novartis, Merck, and Lilly all hold equity. In a sector where each of those names has spent one to four billion dollars on a radiopharma acquisition in the last three years, a validated platform with two owned clinical assets is a natural target.

The royalty stack is the right way up. Aktis earns royalties on the Lilly stream while retaining full economics on its own pipeline and owing nothing upstream on its core technology. That is a structurally cleaner position than most platform biotechs, which typically license in foundational IP and carry an upstream burden.

It is well capitalised through the key readouts. With roughly $538 million in cash and runway into 2028, Aktis can reach AKY-1189 and AKY-2519 data without an immediate financing overhang, a luxury most clinical-stage radiopharma names lack.

The platform is reusable. A single validated miniprotein engine can generate program after program against new targets. The Lilly deal already monetised one slice of that capacity without touching the owned pipeline, and the same model can be repeated with other partners.

Theranostic de-risking. Because the same miniprotein can carry an imaging isotope, Aktis can confirm tumor targeting in patients before therapeutic dosing, a built-in mechanism for selecting responders and reducing late-stage failure risk that pure therapeutic modalities do not have.

| Risk | Concern |

|---|---|

| No efficacy yet | Both owned programs Phase 1b, first data Q1 2027 |

| Partner is competitor | Lilly partners, invests, and competes in radioligands |

| Isotope / manufacturing | Actinium-225 constrained; in-house plant not yet live |

| Long-dated royalty | Lilly royalties contingent and years away |

| Crowded targets | Nectin-4 and B7-H3 already heavily pursued |

| Opportunity | Observation |

|---|---|

| Acquisition appeal | BMS, Novartis, Merck, Lilly all on the cap table |

| Clean royalty stack | Earns on Lilly stream, owns pipeline, owes nothing upstream |

| Well capitalised | ~$538M cash, runway into 2028 through key readouts |

| Reusable platform | One engine, repeatable partnered and owned programs |

| Theranostic selection | Image-then-treat reduces late-stage failure risk |

Conclusion

Aktis Oncology is a useful counterpoint to last week's Rallybio precisely because it occupies the opposite end of the same diagram. Rallybio ended its independent life as a shell, its single royalty thin, preclinical, and ring-fenced into a contingent value right for people who used to own it. Aktis begins its public life with a validated platform, two wholly owned clinical programs, a partnered royalty stream that has already paid its first milestone, and the deepest pharma names in oncology on its cap table.

For a royalty desk the lesson is again structural rather than scientific. Aktis is the rare early-stage company sitting on the correct side of every royalty relationship it has: a payee on the Lilly collaboration, an unencumbered owner of its own pipeline, and a payor of essentially nothing upstream because it built its platform rather than licensing it in. The income that matters here either arrives from Lilly or is retained in full on the owned assets. Nothing of consequence leaves.

The near-term tests are concrete and close. Whether AKY-1189 shows anti-tumor activity in its Phase 1b readout in the first quarter of 2027 will set the value of the lead owned asset. Whether AKY-2519 follows, whether the in-house manufacturing facility comes online on schedule in the second half of 2026, and whether the constrained actinium-225 supply holds, will decide whether the platform can actually deliver product.

And whether one of the four pharmas already on the register decides to buy the whole thing, in a sector that has shown it will pay billions for less, is the question hanging over every line of the cap table. Until then, Aktis is best understood not as a science story but as a cleanly structured platform that earns where it licenses and keeps where it owns, which is a more durable royalty position than most companies twice its age ever reach.

All information in this article was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings (including the Aktis S-1 and Form 10-K), and financial news reporting. Specific terms of the Eli Lilly collaboration, including the precise milestone ceiling and royalty tiers, are summarised from public disclosures and may not reflect the full executed agreement. Market data and share prices are as of mid-June 2026 and will have moved since. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.