What the back end of a royalty is actually made of

A pharmaceutical royalty is a claim on protected sales.

Strip away the science and the structuring and what a buyer is really pricing is a window: the years between launch and the day a generic or biosimilar can lawfully take the market.

In the European Union, the instrument that sets the far edge of that window is rarely the patent. It is the supplementary protection certificate.

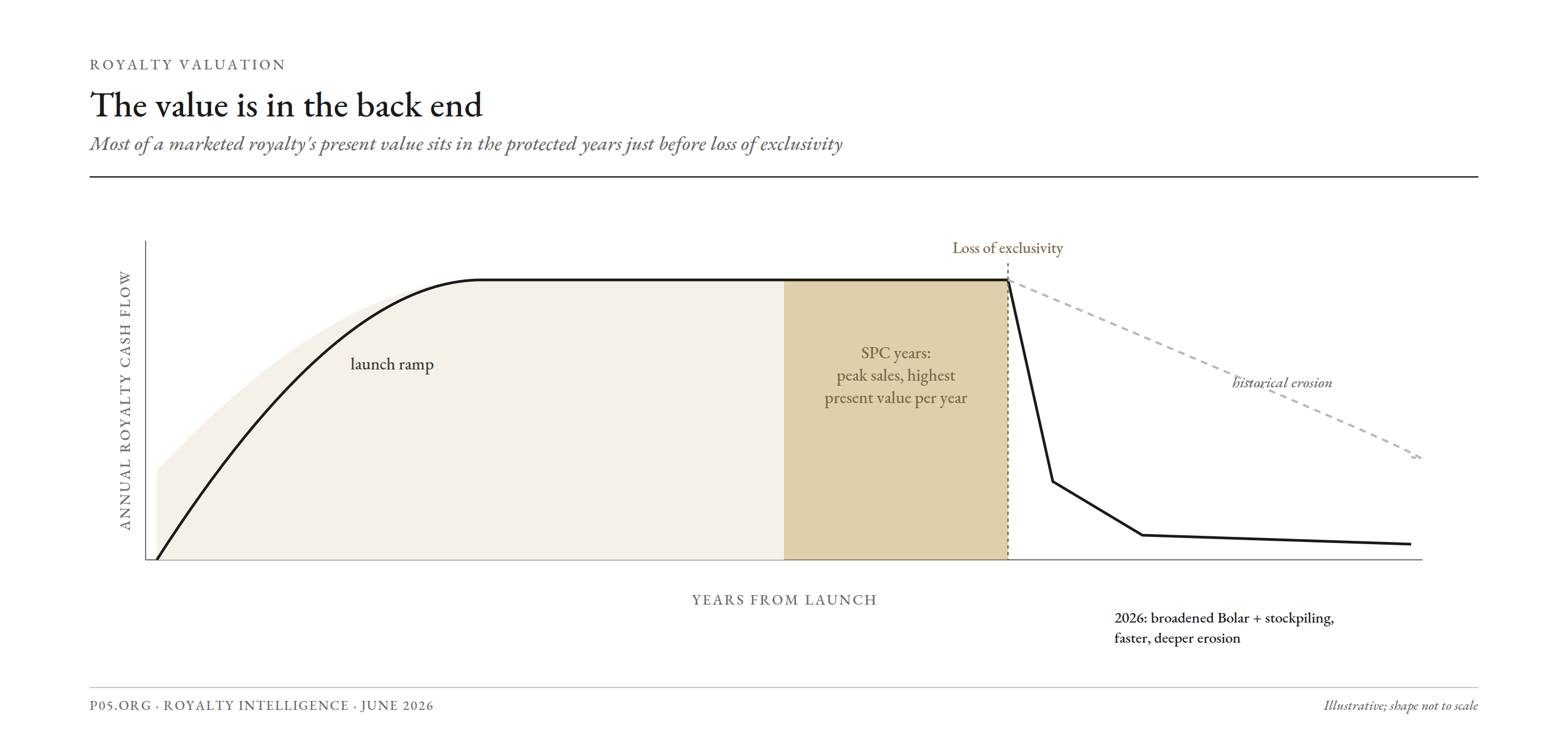

Most of a marketed royalty's value sits in those final protected years, after the launch ramp, before the cliff. That is the stretch the SPC governs. So a buyer who misreads the certificate, its term, its territory, or its validity, misreads the asset.

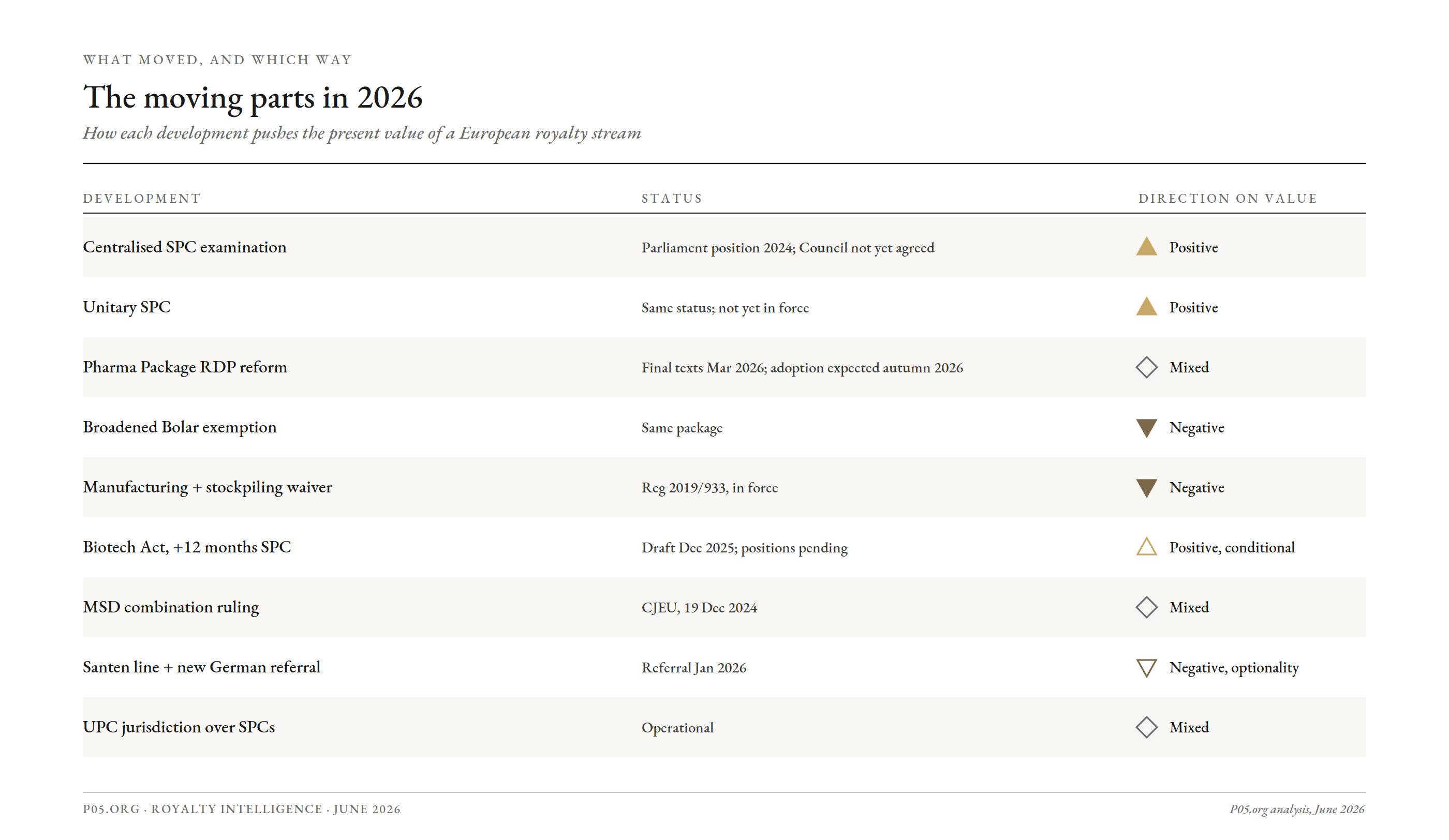

As of June 2026, the European SPC system is moving on every axis at once. A centralised grant procedure and a unitary certificate are stalled in Council. The Pharma Package has rewritten the parallel regulatory clock. The Biotech Act proposes to lengthen the certificate for some products and not others. The Court of Justice has reopened combination products, and a fresh German referral has reopened second medical use. The Unified Patent Court can now revoke SPCs across borders in a single action.

None of this is abstract for anyone underwriting European royalty cash flows. It is the discount rate, the terminal value, and the tail risk.

The short version

- An SPC is the back end of a European royalty. It usually defines the last and most valuable protected years of sales, so its term and validity dominate the net present value of a marketed or late-stage stream.

- A royalty over EU sales is not one cliff. It is a mosaic of national certificates with potentially different expiry dates and different validity outcomes. That fragmentation is a variance problem, not just an accounting one.

- The centralised examination procedure and the unitary SPC would compress that mosaic. They cleared the European Parliament in 2024 but, as of June 2026, the Council has still not landed a general approach. Nothing is in force.

- The 2026 Pharma Package rewrote the parallel regulatory clock (the new baseline is eight years of data protection plus one year of market protection, capped conditionally at eleven) and broadened the Bolar exemption. The practical effect is a steeper, faster cliff.

- The Biotech Act dangles an extra twelve months of SPC for qualifying biotech and advanced therapy products, conditioned on EU manufacturing. That lengthens the back end for some assets and not others.

- Validity is a discrete tail risk. The MSD combination ruling, the Santen line on first authorisation, a January 2026 referral reopening second medical use, and the UPC's new reach over SPCs all change the probability that a certificate survives to its nominal expiry.

- For the model, the SPC is not a refinement. It is one of the largest single inputs, through duration, through the validity haircut on the tail, and through the contractual rate step-downs it usually triggers.

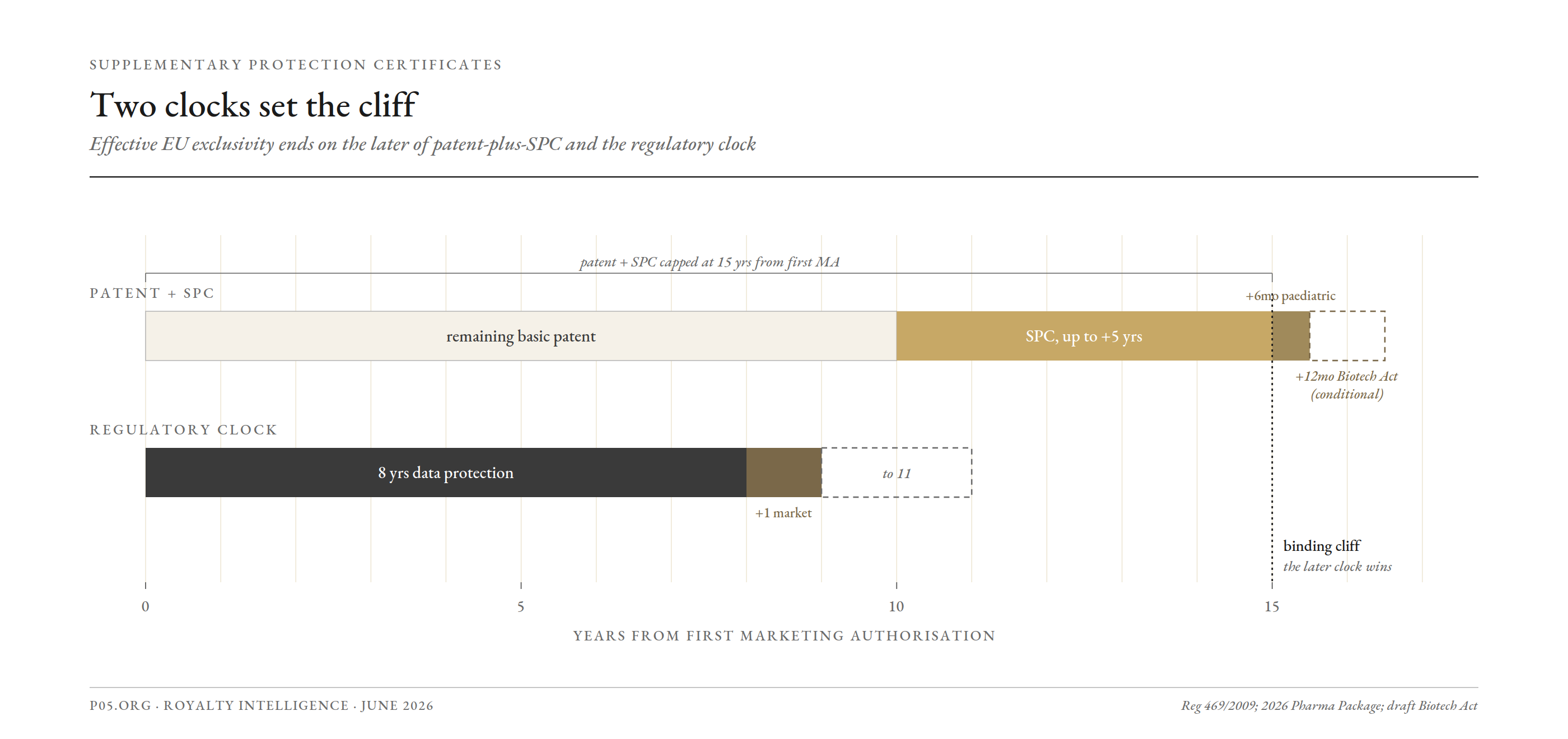

Two clocks, and which one binds

The single most common underwriting error in European royalty work is treating exclusivity as one number.

It is two.

The first clock is patent plus SPC. The basic patent runs twenty years from filing. The SPC, governed by Regulation (EC) No 469/2009 for medicinal products and Regulation (EC) No 1610/96 for plant protection products, then adds up to five further years to compensate for the time lost to marketing authorisation.

A paediatric extension under Regulation (EC) No 1901/2006 can add a further six months. The certificate is sui generis: it is not a patent, it has its own grant conditions, and it stands or falls on its own.

The second clock is regulatory. Data protection and market protection flow from the marketing authorisation, independent of any patent. A generic or biosimilar cannot rely on the originator's dossier, and cannot be sold, until that period runs.

The protected window for any given product in any given country ends on the later of the two.

For a small molecule with a strong composition-of-matter patent, the SPC usually binds. For a biologic, an older molecule with a thin patent, or a product whose patent is vulnerable, the regulatory clock often binds instead.

A royalty model that computes only one of these will misstate the cliff, sometimes by years and always in the direction that flatters the seller.

Both clocks are in motion in 2026. That is what makes this moment unusual.

The two clocks: effective EU exclusivity ends on the later of patent-plus-SPC and the regulatory clock.

The reform that has not arrived

The structural defect in the current system is simple to state.

The conditions for an SPC are harmonised across the Union, but the certificates are still granted nationally, one office at a time. A sponsor seeking EU-wide coverage files separately in each member state, pays separately, and lives with the possibility that the same certificate is granted in one country, refused in another, and later invalidated in a third.

For a royalty buyer, that is the mosaic: a basket of national rights with correlated but not identical fates.

In April 2023 the Commission proposed to fix this with four parallel instruments: a recast of the medicinal SPC regime introducing a centralised examination procedure (COM(2023) 231), the equivalent for plant protection products, and two further proposals creating a unitary SPC to sit on top of the unitary patent.

Under the centralised route, the EU Intellectual Property Office would examine the application with national examiners and issue a single opinion that binds the designated national offices, which then grant. For medicinal SPCs based on a European patent and a centralised marketing authorisation, the centralised route would be the only route.

The unitary SPC would extend a unitary patent across the participating states in one title, and a combined application would let an applicant request a unitary certificate plus national certificates for non-unitary states in one procedure.

The benefit to a financier is direct. One examination, one consistent outcome, fewer one-country knock-outs, and a public register that finally lets a buyer see the encumbrances without commissioning twenty-seven national searches.

The problem is that it has not happened.

The European Parliament adopted its first-reading position in 2024, notably declining to remove the controversial pre-grant opposition mechanism. Since then the file has sat in the Council's intellectual property working party.

The Danish Presidency put it on the agenda of seven working-party meetings in the second half of 2025, and in February 2026 the Presidency circulated a discussion paper to delegations. The Cyprus Presidency has carried the work into the first half of 2026.

As of June 2026 the Council has still not adopted a general approach, trilogue has not concluded, and no new regulation is in force.

Two unresolved questions keep it stuck.

The first is the choice of EUIPO as examiner. The EUIPO handles trademarks and designs and has no history of patent assessment, and parts of the profession, including the European Patent Institute, have argued the European Patent Office is the natural home for this work.

The second is the design of the remedies and opposition system. The fate of the withdrawn standard-essential-patent regulation, another file that tried to hand a patent-adjacent function to the EUIPO and collapsed, hangs over the discussion.

For now, the underwriting consequence is unchanged. European SPCs remain national rights. A royalty over EU sales is still a mosaic, and the buyer still prices the variance.

The cliff got steeper

While the SPC reform stalled, the parallel regulatory clock was rebuilt.

The 2026 Pharma Package, the largest overhaul of EU pharmaceutical law in two decades, reached provisional political agreement in trilogue on 11 December 2025, and the Council published the final compromise texts on 6 March 2026.

Formal adoption by both institutions is expected in the autumn of 2026, with a transitional period to follow. It recasts Directive 2001/83/EC and Regulation (EC) No 726/2004.

Three elements matter for the back end of a royalty.

First, the regulatory clock is shorter at baseline. The old eight-plus-two structure becomes eight years of data protection plus one year of market protection, with conditional add-ons that can rebuild the period up to a capped maximum of eleven years (the new "8+1+1+1" arithmetic).

For products where the regulatory clock binds, the default protected window contracts by a year unless the sponsor earns the extensions, for example by launching across member states or running an additional indication of significant clinical benefit. Breakthrough orphan products addressing a disease with no available treatment can reach up to eleven years of market exclusivity.

Second, the Bolar exemption is broadened. Under the agreed text, generic and biosimilar developers can carry out the steps needed for pricing, reimbursement, health-technology assessment and procurement before the originator's protection expires.

This does not shorten the certificate. It sharpens what happens the day after. Competitors arrive at the cliff already priced, assessed and tendered, so erosion is faster and deeper than under the old regime.

Third, the manufacturing and stockpiling waiver is already live and already biting the final stub. Regulation (EU) 2019/933 lets EU-based manufacturers make an SPC-protected product during the certificate's term for export to third countries throughout the term, and for stockpiling in the final six months before expiry to enable day-one EU launch.

The Commission was due to evaluate the waiver by 1 July 2024 and every five years after. The practical effect for a royalty buyer is that the last six months of an SPC are worth materially less than face, because day-one generic entry is now close to automatic.

Put together, the regulatory reform does not move the SPC expiry date. It changes the shape of the cash flow around it: a thinner terminal tail, a more vertical drop, and for some products a shorter protected window before the certificate even comes into play.

The back end could also lengthen, for some

Cutting the other way is the European Biotech Act, the first draft of which was published on 16 December 2025.

It proposes an additional twelve months of SPC protection for medicinal products developed through biotechnological processes and for advanced therapies, with a parallel incentive for certain veterinary products targeting zoonotic disease.

The conditions are demanding and deliberately industrial. To qualify, the product must contain a new active substance distinctly different from any already authorised in the Union, must show a distinctly different mechanism of action with safety and efficacy at least equivalent to existing treatments, must have been evaluated in clinical trials conducted in more than two member states, and must have at least one manufacturing step, excluding packaging and quality control, performed in the EU.

The European Medicines Agency would assess compliance and issue the certificate.

If adopted as drafted, the extension would likely lift qualifying SPCs from five years to six, with a paediatric six months potentially stacking on top, though the interaction between the various extensions and the ultimate ceiling is not yet resolved in the text.

The Council and Parliament have not finalised their positions. Health ministers were working toward a Council negotiating position around mid-2026, and a second-phase industrial Biotech Act is expected later in the year.

For a royalty underwriter, this is a conditional uplift, not a general one. It rewards assets with a genuine EU manufacturing footprint and penalises those without.

The same molecule licensed to a sponsor that manufactures in the Union and one that does not could carry a one-year difference in protected tail. That is a diligence item, not a footnote.

Validity is the jump risk

Term is the expected case. Validity is the tail.

An SPC can be granted and later revoked, and a royalty buyer should price that as a discrete, binary risk on the back end, country by country, because the grant conditions remain among the most litigated provisions in EU intellectual property law.

The Court of Justice has spent fifteen years circling Article 3(a), which requires the product to be protected by the basic patent. It set a two-part test in Teva v Gilead (C-121/17), then in Royalty Pharma (C-650/17) it rejected a "core inventive advance" test and held that the product must fall under the invention covered by the patent and be specifically identifiable to a skilled person.

The most recent installment, the joined cases C-119/22 and C-149/22 Merck Sharp & Dohme, decided on 19 December 2024, addressed combination products. The Court held that a combination of A and B is a different product from A alone for the purposes of Article 3(c), so a second certificate for the combination is not precluded even where A already had its own SPC, because whether two products are identical turns only on the active ingredients, irrespective of therapeutic application. On Article 3(a) it framed the question around the invention covered by the patent, a formulation national courts are still working out.

Article 3(d), the first-authorisation requirement, is the live wire.

In Santen (C-673/18), decided in 2020, the Court overruled its earlier Neurim ruling and held that the first marketing authorisation for the product as a medicinal product means the first authorisation ever, full stop. The consequence is that a genuinely new and valuable second medical use of a known active ingredient cannot support an SPC. That is a real and recurring value leak for repurposing-led assets.

In January 2026 the German Federal Patent Court referred the question back to the CJEU, this time in the human-versus-veterinary context, asking whether the Santen logic should hold where a later authorisation sits in a distinct regulatory regime. The referral reopens an issue many had treated as closed.

In the United Kingdom, the Court of Appeal in Merck Serono v Comptroller declined to depart from Santen, so for now the two jurisdictions remain aligned on second medical use, but the EU position is again in play.

Layered on top is a change in where validity gets decided.

The Unified Patent Court now has competence over SPCs granted on the basis of a European patent, with or without unitary effect. That cuts both ways for a royalty holder. A single central action can defend a certificate across all contracting states at once, but a single central revocation can also remove it everywhere in one stroke.

The mosaic that protected a stream from total loss, because no single national court could knock out the whole basket, is thinner where the underlying patents are litigated at the UPC.

The underwriting translation is straightforward. Each national SPC carries a probability of surviving to nominal expiry that is below one, and that probability is now a function of the specific Article 3 vulnerabilities of the certificate, the forum in which it may be attacked, and whether the asset depends on a combination claim or a second medical use.

A royalty model that assumes certain survival to the SPC expiry date is mispricing the tail.

The moving parts, and which way they push value

| Development (status, June 2026) | What it changes | Direction on royalty value |

|---|---|---|

| Centralised SPC examination (Parliament position 2024; Council not yet agreed) | One examination opinion binding national offices; single register | Positive once enacted. Lower variance, fewer one-country refusals, cleaner diligence. Not yet in force. |

| Unitary SPC (same status) | One certificate over unitary-patent states | Positive once enacted. Compresses the mosaic; concentrates both defence and attack. Not yet in force. |

| Pharma Package RDP reform (final texts March 2026; adoption expected autumn 2026) | Baseline regulatory clock 8+1, conditional to a cap of 11 | Mixed. Shorter default window where the regulatory clock binds; longer for sponsors who earn extensions. |

| Broadened Bolar exemption (same package) | Pricing, reimbursement, HTA and procurement prep allowed pre-expiry | Negative for the tail. Steeper, faster erosion at the cliff. |

| Manufacturing and stockpiling waiver (Reg 2019/933, in force) | Export throughout term; stockpiling in final 6 months | Negative for the stub. Final six months of an SPC discount toward day-one entry. |

| Biotech Act +12 months (draft Dec 2025; positions pending) | Extra year of SPC for qualifying biotech and ATMP products with EU manufacturing | Positive but conditional. Asset-specific uplift, not a general one. |

| MSD combination ruling (CJEU, Dec 2024) | Combination is a distinct product; second SPC possible | Mixed. Can preserve a combination tail, but Article 3(a) "invention" framing adds uncertainty. |

| Santen line and the new German referral (referral Jan 2026) | First-authorisation rule blocks second medical use SPCs; now back before the CJEU | Negative, with optionality. A leak for repurposing assets; a possible reopening to watch. |

| UPC jurisdiction over SPCs (operational) | Central enforcement and central revocation of EP-based SPCs | Mixed. Single defence or single loss; thinner mosaic protection. |

How each 2026 development pushes the present value of a European royalty stream.

How this prices: calculations, rates, and deals

Everything above resolves to a small number of inputs in a royalty model. It is worth being explicit about where the SPC actually enters the arithmetic, because it enters in more places than most term sheets acknowledge.

The term is most of the number

A royalty's present value is the discounted sum of the royalty rate applied to net sales over the protected window.

Two features of pharmaceutical revenue make the SPC years disproportionately valuable. They sit after the launch ramp, at or near peak sales. And they are the last protected cash flows before the cliff.

Discounting works against late years, since a euro in year nine is worth less than a euro in year three. But for a product that reaches peak four to six years after launch, the SPC years are the peak-sales years, so even after discounting at a low-to-mid-teens rate, each year of SPC term usually contributes more present value than any single early year.

The sensitivity is large and one-directional. Moving the effective loss-of-exclusivity date by twelve months adds or removes a near-peak year of royalty.

For a marketed stream discounted around ten to twelve percent, a single year of term at peak is frequently worth a high-single-digit to low-double-digit percentage of the whole valuation. The SPC term is not a refinement to the model. It is one of its largest single inputs.

Most of a marketed royalty's present value sits in the protected years just before loss of exclusivity.

Two clocks, one duration input

Because the effective cliff is the later of patent-plus-SPC and the regulatory clock, the duration that drives the model is a maximum of two moving numbers, taken product by product and country by country.

In 2026 both numbers are shifting. The Pharma Package can shorten the regulatory leg at baseline and lengthen it conditionally. The Biotech Act can add a year to the SPC leg for qualifying assets.

A model built on a single assumed cliff date, rather than an explicit maximum of two clocks, is not conservative. It is simply wrong in an unknown direction.

Validity is a haircut on the tail, not a footnote

There are two equivalent ways to price the chance that a certificate is revoked before its nominal expiry.

Apply a survival probability to the back-end cash flows, or raise the discount rate on the tail specifically. Either way, the back end is no longer carried at face.

The size of the haircut should track the actual vulnerability. A clean composition-of-matter SPC warrants a small adjustment. A certificate that rests on a combination claim, or that would depend on a second medical use, warrants a larger one, given the MSD and Santen lines and the open German referral.

Two refinements matter. The haircut is not the same in every country, because national outcomes have historically diverged. And the UPC correlates the haircut across its contracting states, because a single central revocation removes the certificate everywhere at once, so that portion of the risk cannot be diversified away inside one patent family.

The cliff shape sets the terminal value

Many models carry a post-expiry tail, a residual stream of branded sales that decays at some assumed rate after generic entry.

The broadened Bolar exemption and the stockpiling waiver have engineered faster day-one erosion than historical analogues imply. The honest terminal assumption in 2026 is a thinner tail and a steeper initial drop.

For an uncapped or true-sale royalty, that terminal assumption is real money. For a capped deal it usually does not bind, because the cap is reached, or not, well before the tail matters.

Rates and step-downs: the SPC is often written into the contract

The SPC is not only a valuation input. It is frequently a contractual trigger.

Licence agreements routinely define the royalty term, on a country-by-country basis, as the later of basic-patent expiry, SPC expiry, and regulatory exclusivity. Many add a step-down, where the rate falls to a lower tier on loss of exclusivity or first generic entry in a given market, rather than terminating outright.

For a buyer of an existing royalty, this means the SPC date does double duty. It sets when the cash flow ends or steps down, and it does so per territory. Reading which event cuts the rate, and where, is part of confirming the asset, not an afterthought to the valuation.

The mosaic in the model: country by country, sales weighted

European royalty bases are concentrated. A small set of markets, led by Germany, France, Italy and Spain, typically carries the majority of EU sales, with the rest spread thin.

Because national SPCs can expire on different dates, the cliff in the model is not one drop. It is a staggered series of drops, each weighted by that country's share of sales.

A unitary SPC would collapse much of that staggering into a single expiry for the unitary-patent states, lowering the variance a buyer has to price and simplifying the waterfall in any securitisation. Until it arrives, the staggered, sales-weighted cliff is the correct way to build the schedule, and a single blended date understates the dispersion.

Deal structures: where the SPC term actually lands

The same certificate matters differently depending on how the deal is cut.

- Capped synthetic royalties, struck to a money multiple such as 1.x times invested capital, often reach the cap before the cliff. Where they do, SPC term beyond the cap accrues to the seller, not the financier, so for the financier the certificate mainly affects the probability and timing of hitting the cap rather than the length of the tail.

- Uncapped or true-sale royalties expose the buyer to the whole back end. Here SPC term, validity and cliff shape are the return, and the analysis above applies in full.

- Change-of-control buybacks and reverse tiers do not move the loss-of-exclusivity date, but they change who holds the tail and on what terms, which is why they belong in the same conversation as the SPC schedule rather than a separate one.

A worked illustration

The numbers below are hypothetical and rounded, used only to show direction and rough magnitude.

Take a marketed product with around six hundred million euros of EU peak net sales and a six percent royalty, modelled at a ten percent discount rate, sitting today about five years from basic-patent expiry.

With a four-year SPC granted in the major markets, the protected window runs to roughly year nine, and the SPC adds four near-peak years to the tail. Drop the SPC from the model, whether through oversight or invalidation, and the window ends around year five, before peak even fully matures. Those four years are not marginal. They are the most valuable years in the schedule, and removing them can take a large fraction of the headline value with them.

Now layer the 2026 changes onto the same asset. Apply an eighty percent survival probability to the SPC years to reflect a combination-claim validity risk, and the tail is marked down accordingly. Steepen the post-expiry erosion for the broadened Bolar exemption, and the residual tail thins further. Qualify the product for the Biotech Act extension, and a fifth protected year comes back, partly offsetting the haircut.

The point of the exercise is not the figure. It is that four or five of the most important assumptions in the valuation all run through the SPC, and all of them moved in 2026.

If the reform passes: the counterfactual for financing

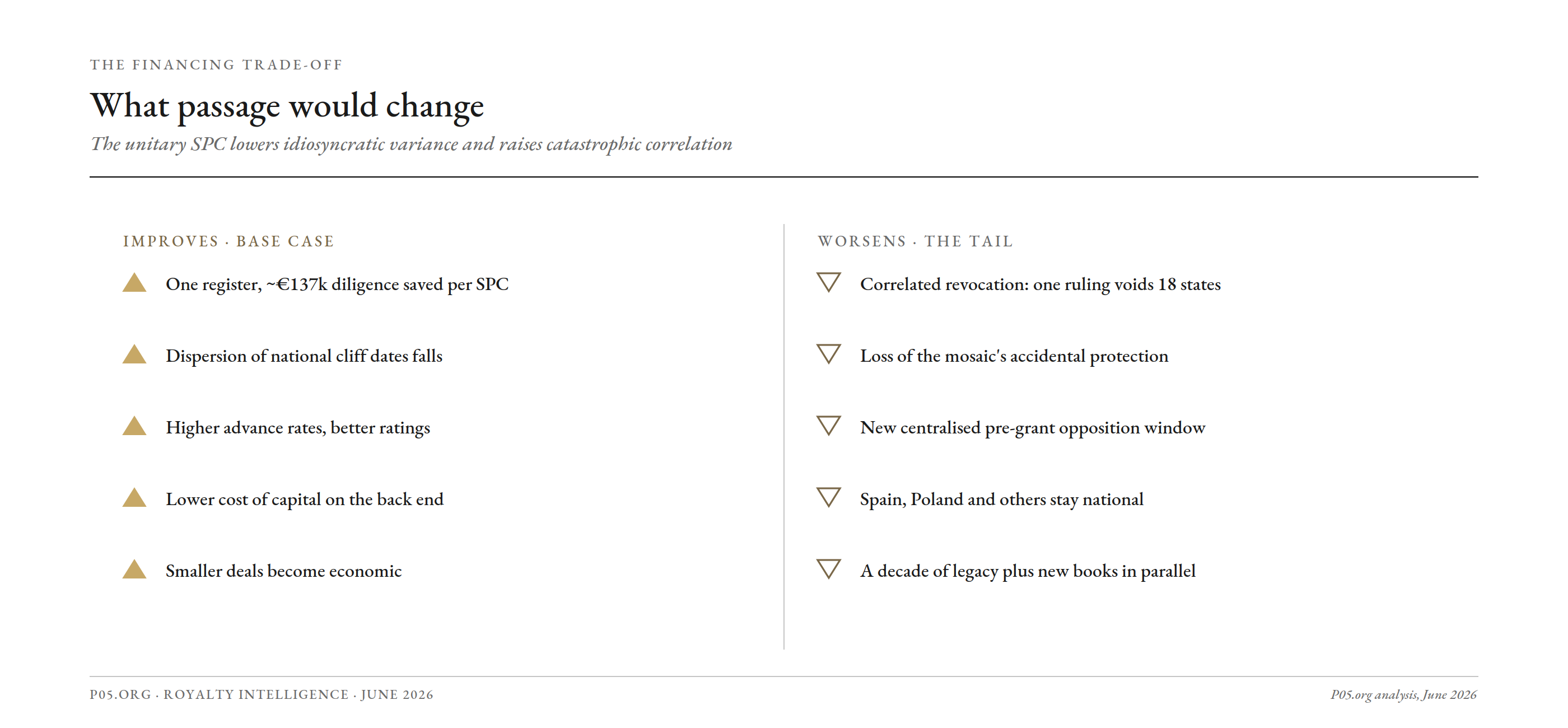

It is worth being precise about what the centralised procedure and the unitary SPC would and would not do, because the financing consequences follow directly from that distinction.

The reform is procedural, not substantive. The Commission was explicit that it does not alter the conditions for grant, the scope, or the effects of an SPC. Article 3 is untouched. The five-year cap is untouched. The fifteen-year-from-authorisation ceiling is untouched.

So the reform does not change the expected length of any certificate.

What it changes is four things a financier prices directly: the variance around the cliff, the cost of confirming it, the timing of when validity risk resolves, and the tradability of the collateral. For royalty work, those four are most of the bid.

Variance compression: one cliff, not a mosaic

Today, the same patent and the same authorisation can yield slightly different grant outcomes and expiry dates across national offices, which is what produces the staggered cliff.

A central examiner produces one opinion that binds the designated offices, and a unitary SPC is a single title with a single expiry and a single validity fate across the unitary-patent states. The cross-sectional dispersion of the back end collapses toward a single date.

This is the largest single valuation effect, and it is pure variance reduction. Lower variance on the tail means a lower risk premium on the back-end cash flows, which lifts present value without moving the expected term by a day. The terminal value firms up because the schedule stops being a probability cloud of national dates and becomes a line.

Diligence cost and the financeable universe

The Commission's own impact assessment estimated savings of around 137,000 euros per applicant for obtaining five-year SPC protection across all twenty-seven member states, the bulk of it on renewal fees avoided by holding one unitary title rather than a bundle of nationals.

For a financier the mirror saving is on the buy side. Confirming encumbrance and validity becomes a single-register lookup rather than a twenty-seven-jurisdiction counsel exercise.

Because diligence cost is largely fixed per deal, it weighs hardest on small deals, where it can be a meaningful fraction of the cheque. Lowering that fixed cost pulls the minimum economic deal size down and widens the financeable long tail, which is exactly the sub-scale band where most un-intermediated royalties actually sit. More streams become bankable, and pricing on them tightens.

When the risk resolves: a datable de-risking step

The centralised route has a defined sequence. The application is published, third parties can file observations within three months, the panel issues an examination opinion, and a pre-grant opposition can be filed within two months of a positive opinion before the certificate is granted. An expedited track, added by the Parliament, brings the first opinion forward to four months and the observation window to six weeks where the basic patent is close to expiry.

For a financier this creates a clean value step at a known point. A royalty monetised before the opposition window closes carries unresolved validity as a contingency. One bought after a clean grant through opposition is materially de-risked, on a datable event.

That is precisely the kind of discrete trigger that milestone-tranched and contingent structures are built around.

The caveat is real. The pre-grant opposition mechanism was retained over industry objection, and the standing concern is that third parties can use it to delay examination and consume part of the practical term. The de-risking step can therefore also be pushed out, and the delay itself is a cost to carry in the model.

The double edge: correlation and the single point of failure

Centralisation concentrates validity risk as much as it concentrates grant.

A central revocation, whether through an EUIPO invalidity action, a successful opposition, or a negative central opinion, removes the certificate everywhere at once. Layer that on the UPC's power to revoke the basic patent centrally, and the diversification that used to cap a loss, because no single national court could knock out the whole basket, is gone for centralised and unitary certificates.

For a single-asset stream, that raises tail severity: the loss on a validity failure is now total across the participating states, not partial.

For a portfolio or a securitisation, it changes the correlation assumption. National validity outcomes can no longer be treated as independent draws, so a rating model has to build in wrong-way correlation, and the diversification benefit of holding many EU streams shrinks where they share a centralised legal fate.

A further wrinkle: the Parliament left the EUIPO with competence over unitary-SPC invalidity alongside the UPC's competence over European-patent-based SPCs, so validity can be contested in more than one forum. An attempt to give the UPC sole competence, to avoid exactly this, did not pass. Dual-forum exposure is now a diligence and cost item rather than a hypothetical.

Tradability and perfection of security

A single registered title is far easier to assign, pledge and perfect a security interest over than a bundle of national certificates, each requiring its own national recordation.

That means cleaner true-sale and security opinions, faster and cheaper transfer, and a more liquid secondary market.

This is the structural unlock for the bundling thesis. Homogeneous, transparent, single-register collateral supports higher advance rates on a warehouse line and lower spreads on the paper that comes out the other end. It is the difference between pooling twenty-seven legal objects and pooling one.

What stays a mosaic

Two qualifications keep this honest.

The unitary SPC covers only the states inside the unitary patent system, currently seventeen. Spain, Poland, Croatia and the non-ratifiers stay national, so a combined application still bundles national certificates for them. Full-EU coverage remains a unitary core plus a residual mosaic.

And the reform is prospective. It governs how future certificates are granted, so a financed portfolio will hold legacy national SPCs alongside new centralised and unitary ones for years. Underwriters will track which regime each certificate sits in, by vintage, well into the next decade.

The reform does not lengthen the royalty. It makes the back end more certain, cheaper to confirm, resolved on a known date, and easier to sell, while quietly concentrating the risk of total loss. Expected term flat; variance, cost, timing and liquidity all move. For a royalty financier, that is most of what sets the price.

If the reform passes: the financing consequences

Everything to this point describes the world as it is, with the mosaic intact. It is worth being equally precise about the world the reform would create, because the centralised procedure and the unitary SPC are, at their core, a structured-finance event dressed as an administrative one.

A basket becomes a security

The reform's central financing effect is to convert a mosaic of idiosyncratic national exclusivity dates into a single, correlated cliff across the unitary block.

That block is large. As of 2026 the unitary patent and the Unified Patent Court cover eighteen member states, about eighty percent of EU GDP, following Romania's accession in September 2024. A unitary SPC would sit on top of a unitary patent and expire on one date across all of them, examined once and recorded once.

For anyone bundling royalty streams into tradable or rated paper, that uniformity is the prize. A security backed by a basket of cash flows is worth more, and easier to rate, when the back-end dates are the same number rather than a set of correlated national guesses.

The unitary SPC compresses a mosaic of national cliff dates into one block, but does not erase it.

Diligence collapses, and small deals become economic

Today a buyer confirming EU-wide coverage commissions national searches office by office. The Commission's own impact assessment put the cost of obtaining a five-year SPC across all twenty-seven member states at roughly one hundred and thirty-seven thousand euros per product, before the legal cost of reconciling divergent national outcomes.

The reform replaces that with a single application, a single examination opinion, and a single public register covering both unitary and centralised national certificates.

Lower fixed cost per asset changes which deals are worth doing. The fixed legal and diligence burden is what makes small royalty streams uneconomic to acquire one at a time. Compress it and the floor drops, which is precisely where the underserved long tail of sub-scale streams sits.

Variance down means advance rates up

Rated and warehouse-funded structures price the dispersion of the collateral's cash flows. A predictable weighted-average life and a tight distribution of cliff dates let a rating agency or a warehouse lender model the tail with less padding, which shows up as lower credit enhancement and a higher advance rate against the same cash flows.

The structural precedents are not in pharma. They are in music and other IP-backed asset-backed securities, where uniform, well-documented royalty streams have been bundled into rated paper for years. The barrier to importing that template into pharmaceutical royalties has always been the fragmentation of the underlying rights. The unitary SPC removes a large part of it.

The counterweight: correlation goes up

The same uniformity that helps the base case hurts the tail.

The reform centralises challenge as well as grant. The current proposal sets up a bifurcated system: invalidity of national SPCs granted through the centralised procedure runs through national courts including the UPC, while direct invalidity of a unitary SPC runs through the EUIPO and the General Court, with the UPC also able to rule on validity by counterclaim in infringement.

The practical consequence for a holder is that a single adverse decision can void the certificate across all eighteen states at once. The mosaic used to provide a crude form of protection, because no single national court could knock out the whole basket. That protection thins.

So the reform lowers idiosyncratic variance and raises catastrophic correlation. A portfolio that diversified across countries was partly diversifying across legal forums. After the reform, real diversification has to come from spreading across patent families and legal bases, not across borders.

What passage would change: lower idiosyncratic variance, higher catastrophic correlation.

The residual mosaic does not vanish

A unitary SPC is not an EU-wide SPC.

Spain, Poland and Croatia are not in the unitary system, and a further six states including Ireland have signed but not yet ratified. Spain in particular is a top-five EU pharmaceutical market that would remain on the national track. A combined application would yield a unitary certificate plus national certificates for the rest, so the model becomes one large unitary block plus a residual national set led by Spain.

Cleaner, in other words, but not clean. The buyer still underwrites Spain separately.

A new uncertainty window, and a decade of two books

Two frictions temper the upside.

The European Parliament kept the pre-grant opposition mechanism that much of the profession wanted removed. That introduces a centralised, visible window between application and grant in which third parties can attack the certificate, which improves transparency but adds a period of front-end uncertainty for any royalty struck before grant.

And the reform is forward-looking. Existing national SPCs are not converted, and stakeholders have criticised the absence of clear transitional provisions. The existing book of royalties stays on the mosaic. Only new certificates based on unitary patents get the unitary regime.

For most of the next decade an arranger therefore runs two books in parallel: legacy national-SPC assets that still need full mosaic diligence, and new unitary-SPC assets that do not. The benefits accrue slowly to the back book.

Net effect

If it passes, the reform is pro-liquidity and pro-volume. It lowers the cost of capital on the protected back end, which means higher prices to sellers, thinner spreads to pure financiers, larger volume, smaller viable deals, and a genuine path to securitisation.

From an administrative reform to the advance rate on a royalty book. Conditional on passage.

The winners are originators, arrangers and sellers. The pure spread buyer sees compression. And the whole upside is conditional on a file that, as of June 2026, is still stuck in the Council.

For now it is optionality on the value of a European royalty book, not a line in the model.

What it means

For originators and sellers. The SPC schedule is a representation, not a comfort line.

A sophisticated buyer will rebuild the protected window from the basic patent, the certificate term in each material country, the regulatory clock under the new Pharma Package arithmetic, and the specific Article 3 exposure of each certificate.

Sellers who present a single EU cliff date, rather than a country-by-country schedule with the binding constraint identified for each, will be discounted for the ambiguity they leave on the table. Where an asset can plausibly qualify for the Biotech Act extension, the EU manufacturing footprint is now a value driver worth documenting.

For financiers and underwriters. Price two clocks, not one, and take the later of them per product per country.

Treat SPC validity as a jump risk rather than a certainty, and size that risk to the actual vulnerability: combination claims and second medical use are softer than clean composition-of-matter cases.

Model the cliff as steeper than historical analogues imply, because the broadened Bolar exemption and the stockpiling waiver have engineered day-one entry. And note that the reform meant to help, the centralised and unitary SPC, is not here yet, so the mosaic risk that justifies country-level diligence is still fully present.

For investors in royalty paper and rated structures. The case for bundling and securitising European royalty streams improves materially once the unitary SPC and centralised examination land, because a tradable instrument backed by a basket of cash flows is worth more when the back-end exclusivity dates are consistent and the validity outcomes are correlated rather than idiosyncratic.

Until then, diversification across uncorrelated national validity outcomes is doing real work in any portfolio, and concentration into UPC-exposed assets quietly removes some of it.

The verdict

A European pharmaceutical royalty is priced on a window, and the supplementary protection certificate sets the far edge of that window.

In June 2026 that edge is being redrawn from several directions at once, and the directions do not all agree.

The reform that would make the back end cleaner and more consistent, the centralised procedure and the unitary certificate, has passed the Parliament and stalled in the Council, so the national mosaic and its variance are still the reality.

The reform that has actually arrived, the Pharma Package, leaves the certificate's term untouched but steepens the cliff around it and shortens the parallel regulatory clock at baseline.

The Biotech Act could lengthen the back end, but only for assets that manufacture in the Union and clear a high novelty bar.

And the case law has made validity a live question again, in combinations, in second medical use, and in where the fight now takes place.

The cash flow has not changed. What it is protected by has.

For anyone underwriting these streams, the work is the same as it has always been, done more carefully: find the binding clock, price the tail, and never trust a single cliff date.

Reflects publicly available information as of June 2026, derived from EU institutional sources, regulatory and legislative texts, court decisions, and specialist legal commentary. Legislative files described as pending or provisional may change before adoption. Illustrative figures are hypothetical and used only to show direction and magnitude. For informational purposes only; not investment, legal, or financial advice. The author is not a lawyer or financial adviser.