Fund of the week: Hercules Capital

Hercules Capital. NYSE: HTGC. The largest non-bank venture lender in the United States, and as of June 2026 a royalty originator.

What is Hercules Capital?

Hercules Capital (NYSE: HTGC) is a San Mateo-based business development company (BDC) and the largest non-bank venture lender in the United States. It provides senior secured venture growth loans to high-growth, venture capital-backed and growth-stage companies in technology and life sciences.

It was founded in December 2003 as Hercules Technology Growth Capital by Manuel Henriquez, began originating in October 2004, and went public in 2005. Since inception it has committed more than $27 billion to over 700 companies, crossing the $25 billion cumulative milestone in 2025.

The important structural point for this audience: Hercules is not a fund in the limited-partner sense. It is a permanently capitalised, internally managed, publicly traded vehicle whose investors are common shareholders rather than LPs.

Alongside it sits a second business, Hercules Adviser LLC, a registered investment adviser that runs private credit funds for institutional investors. The combined platform held approximately $6.1 billion of assets under management as of Q1 2026, up 21.8% year-over-year.

For most of its history Hercules has been a pure first-lien senior secured lender, not a royalty buyer. Its relevance to the royalty market was positional: it lends to the same commercial-stage and late-clinical biopharma names that do royalty monetisations, and it sits senior to (or beside) those royalty structures in the capital stack. That is still the dominant lens.

But the Beren Therapeutics financing announced on June 10, 2026 shows the line blurring: Hercules supplied up to $165 million as a hybrid of senior secured debt and royalty financing, including a $55 million royalty tranche written by Hercules itself. The firm is beginning to originate royalty paper inside its own structures, not merely lend alongside it. This piece is built around that shift.

This piece looks at who Hercules is, who funds it (in both senses), what its portfolio looks like, and what its royalty-adjacent exposure looks like, accurate as of June 2026.

Overview and investment focus

Hercules' model rests on four propositions.

First, that venture-backed and growth-stage companies need non-dilutive growth capital between equity rounds, and that a specialist lender can underwrite that risk better than a bank. The firm provides structured debt, typically first-lien senior secured floating-rate term loans with warrant coverage, in individual sizes generally between $20 million and $40 million, though facilities range much wider.

Second, that floating-rate, first-lien paper with covenants and milestone-gated draws produces durable risk-adjusted returns. As of Q1 2026, 88.6% of the debt portfolio was first-lien senior secured and 98.0% was floating-rate with interest rate floors.

Third, that warrants and small equity positions in the same borrowers convert credit risk into asymmetric upside on the winners. Hercules held warrant positions in 113 portfolio companies and equity positions in 73 companies as of Q1 2026.

Fourth, that a permanent-capital BDC balance sheet, supplemented by private credit funds, lets the platform hold paper through cycles and capture origination, fee, and prepayment economics that a fixed-life fund cannot.

The portfolio splits across two core verticals: technology (software, fintech, security, infrastructure) and life sciences (biopharmaceuticals, biotechnology tools, diagnostics, drug delivery, medical devices, therapeutics, and specialty pharmaceuticals), with a smaller sustainable and renewable technology book. For a royalty audience, only the life sciences vertical is directly relevant, and even there the relevance is structural rather than economic.

The headline Q1 2026 metrics:

| Metric (Q1 2026) | Value |

|---|---|

| Total investment income | $141.5M (record, +18.4% YoY) |

| Net investment income (NII) | $88.1M, or $0.48 per share |

| Total new debt and equity commitments | $1.81B (record, +77.8% YoY) |

| Total fundings | $706.4M |

| Net asset value (NAV) per share | $11.90 (down 1.9% from Q4 2025) |

| Total net assets | $2.2B |

| GAAP effective yield / core yield | 12.8% / 12.2% |

| Return on average equity / assets | 16.9% / 8.1% |

| Loans on non-accrual (at fair value) | 0.1% (one debt investment) |

Background and formation

Hercules was founded in 2003 by Manuel Henriquez, an experienced venture and specialty-finance investor, who built it into the dominant US venture debt franchise over a decade and a half. The firm renamed from Hercules Technology Growth Capital to Hercules Capital in 2016 to reflect its broadening beyond pure technology lending.

In March 2019, Henriquez voluntarily stepped aside as chairman and CEO after being charged in the Operation Varsity Blues college admissions scandal. He later pleaded guilty to conspiracy to commit wire fraud and money laundering and served a prison sentence.

The board elected then-Chief Investment Officer Scott Bluestein as interim CEO, made the appointment permanent in July 2019, and separated the chairman and CEO roles for governance reasons.

The transition held. Under Bluestein, who also retains the CIO title, Hercules has grown its balance sheet, launched a private credit franchise, and was named 2025 Americas BDC Manager of the Year by Private Debt Investor.

The platform's scale has grown steadily rather than through discrete fund vintages. The dollar trajectory below uses cumulative commitments and AUM rather than fund closings, because Hercules is permanently capitalised.

| Period | Cumulative debt commitments | Platform AUM (approx.) | Notes |

|---|---|---|---|

| Inception (2003) | First originations Oct 2004 | n/a | Founded as Hercules Technology Growth Capital |

| Mar 31, 2025 | >$22.0B to 680+ companies | >$5.0B | Hercules Adviser managing four private credit funds |

| Year-end 2025 | >$25.0B milestone crossed | ~$5.7B | >$3.9B new commitments in 2025 |

| Q1 2026 | >$27.0B to 700+ companies | ~$6.1B (+21.8% YoY) | Record quarterly commitments of $1.81B |

Limited partners and funder base

This is where Hercules differs most sharply from a private equity or royalty fund, and where the "LP" question has to be answered in two layers.

Two layers of capital. The public BDC is owned by the market; the institutional LPs sit one level down, inside the adviser.

Layer 1: the public BDC (common shareholders)

The Hercules Capital balance sheet is funded by public equity (187.2 million shares outstanding as of Q1 2026), unsecured notes, SBA debentures, and committed bank facilities with MUFG ($440M) and SMBC ($475M). There are no LPs. The equity investors are common shareholders who can enter and exit daily.

That shareholder base is unusually retail-heavy and index-driven, which is typical of high-yield BDCs. As of mid-2025, roughly 352 institutions held about 73 million shares, a minority of the float. The largest disclosed institutional holders are passive and quantitative rather than strategic: the VanEck BDC Income ETF (BIZD) and Van Eck Associates, index complexes, and quant managers including Two Sigma and Citadel. Hercules pays a base-plus-supplemental distribution of roughly $1.88 per share annually, a yield near 12%, which is the principal reason income investors hold it.

Layer 2: the private credit funds (institutional LPs)

The genuine LP relationships sit in Hercules Adviser LLC, the wholly owned RIA. In July 2025 Hercules Adviser held a first close of its fourth institutional private credit fund, Hercules Growth Lending Fund IV, bringing the adviser to four private credit vehicles with approximately $1.6 billion in committed debt and equity capital. These funds co-invest alongside the BDC, and a portion of each origination may be assigned to or directly originated by the Adviser Funds.

Hercules does not publish the LP roster for these private funds. Based on the structure and the firm's own language about "long-term support of our investors," the LP base is institutional: pensions, insurers, asset managers, and fund-of-funds seeking access to the venture-debt asset class without holding the public BDC. Specific names are not in the public record.

| Capital layer | Investor type | Disclosure |

|---|---|---|

| Hercules Capital BDC (equity) | Public common shareholders; index ETFs; quant funds; retail | Public; top holders via 13F |

| Hercules Capital BDC (debt) | Unsecured noteholders; SBA; MUFG and SMBC facilities | Public; disclosed in filings |

| Hercules Adviser private funds | Institutional LPs (four private credit funds, ~$1.6B) | Not publicly named |

The practical takeaway: there is no single LP base to map. The public vehicle is owned by the market; the institutional LP relationships live one level down, inside the adviser, and are undisclosed.

Portfolio of investments

The portfolio turns over far faster than a buyout fund's. Hercules describes its debt book as cycling roughly every 18 to 24 months, and early loan repayments are a recurring feature ($225.8 million in Q1 2026 alone). The life-sciences names below are the ones relevant to a royalty, BD, or biotech capital-markets reader.

| Company | Sector | Notes |

|---|---|---|

| Beren Therapeutics | Rare disease (specialty pharma) | Adrabetadex for infantile-onset Niemann-Pick disease Type C; up to $165M from Hercules as a hybrid senior secured debt and royalty facility, including a $55M royalty tranche, June 10, 2026; PDUFA target date November 17, 2026 |

| Viridian Therapeutics | Biotech (rare disease) | Thyroid eye disease; upsized to a $250M Hercules debt commitment in Q4 2025; also did a separate royalty financing with DRI Healthcare (see royalty stack below) |

| Senseonics | Medical device (diabetes) | Implantable continuous glucose monitoring; facility increased from $100M to $140M, May 2026 |

| MoonLake Immunotherapeutics | Clinical-stage biotech | Inflammatory disease; $300M debt commitment in Q1 2025 |

| enGene | Gene therapy | Expanded to a $125M Hercules facility in January 2026 |

| Tenpoint Therapeutics | Biotech (ophthalmology) | $235M Series B and credit facility, January 2026 |

| Corium Therapeutics Holdings | Specialty pharma | Markets and distributes AZSTARYS (ADHD); Hercules committed $185M from September 2021; acquired by Collegium for $650M cash (March 2026) |

| Alamar Biosciences | Proteomics / dx | Early disease detection; Hercules committed $30M from June 2022; IPO'd April 2026; Hercules holds Series C preferred warrants |

| TransMedics | Medical device | Organ transplant systems; long-term Hercules borrower |

| 23andMe | Genomics | Assets acquired by TTAM Research Institute for $305M (June 2025); a $5.1M Hercules legacy position |

Beyond life sciences, the book is heavily weighted to software and technology, which matters for the firm-level risk discussion in the red team section below.

Royalty stack analysis

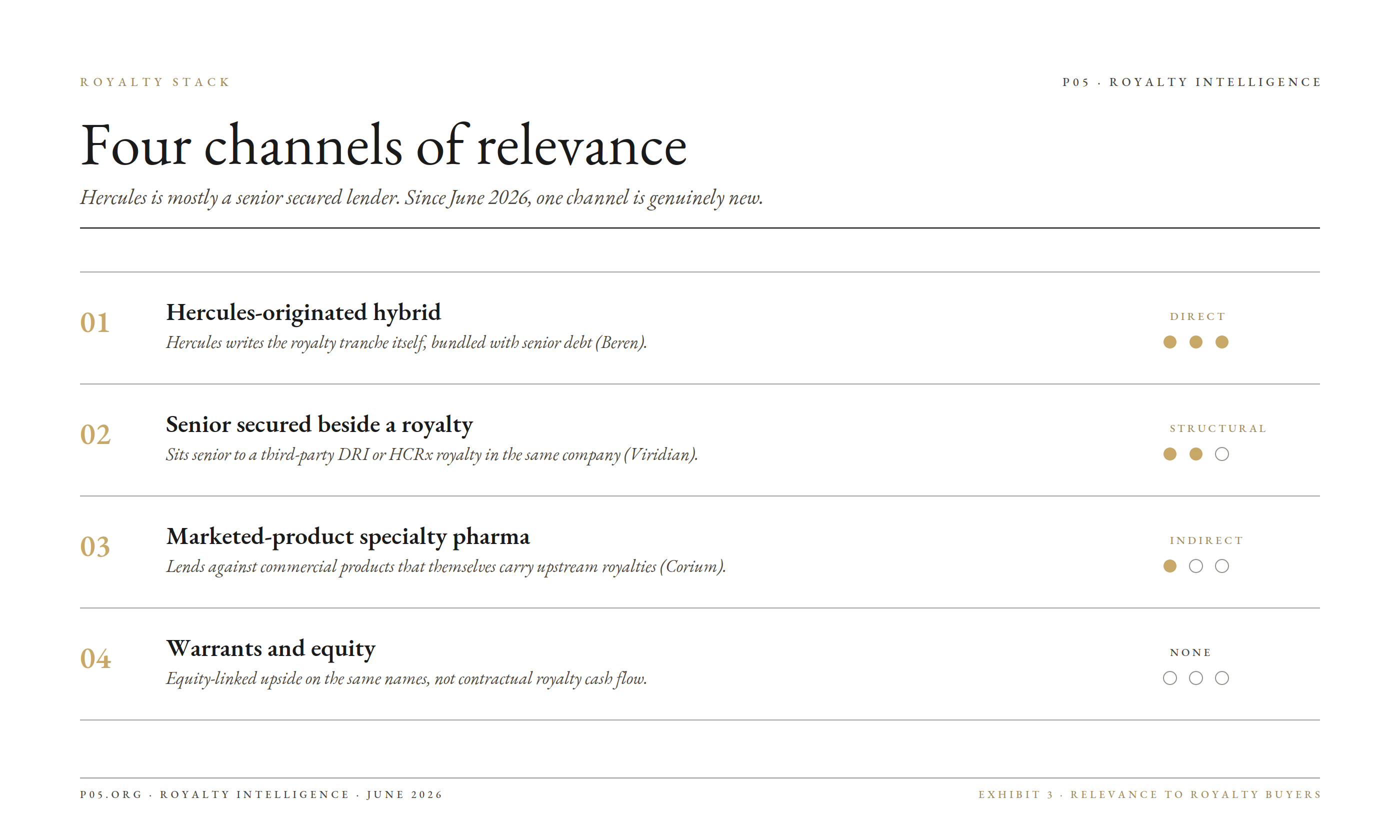

Until June 2026 the framing here was simple: Hercules did not own a royalty stack, did not buy traditional royalties from licensors, and did not purchase synthetic royalties on product revenue. The Beren Therapeutics financing complicates that. There are now four channels worth separating, the first of which is genuinely new.

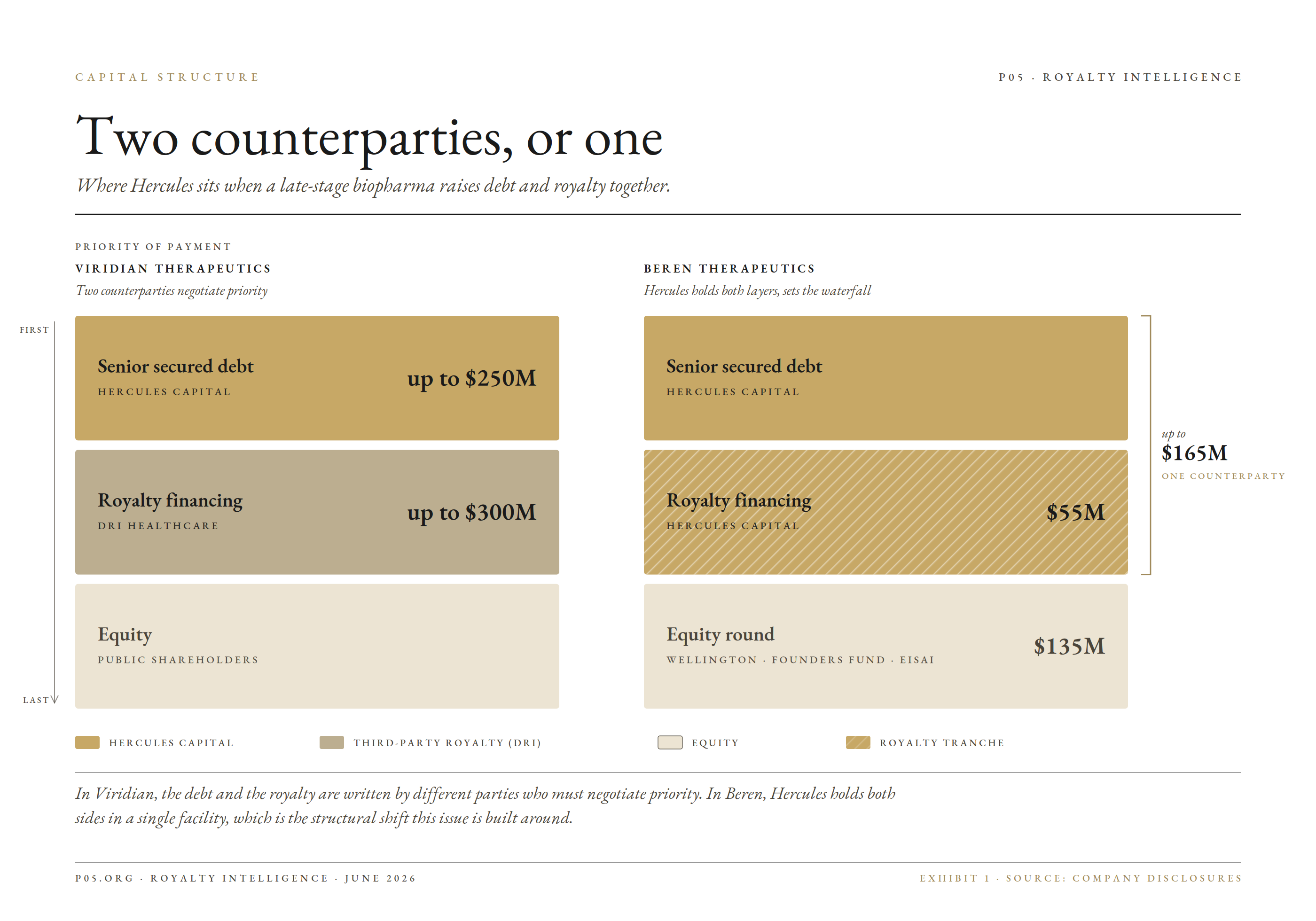

Two counterparties, or one. In Viridian the debt and royalty are written by different parties; in Beren, Hercules holds both sides in a single facility.

Channel 1: Hercules-originated hybrid credit-plus-royalty (the new model)

On June 10, 2026, Beren Therapeutics announced $300 million of total financing: a $135 million equity round (with Wellington Partners, JIC Venture Growth Investments, Founders Fund, Narya Capital, and Eisai) and up to $165 million from Hercules. The Hercules tranche is the notable part: it is a combination of senior secured debt and royalty-based funding, including a $55 million royalty financing written by Hercules. The capital backs commercial-readiness work for adrabetadex, Beren's investigational therapy for infantile-onset Niemann-Pick disease Type C, ahead of its November 17, 2026 PDUFA target date.

This is the structure royalty investors should watch. Hercules is no longer only the senior lender beside a royalty buyer; in Beren it is the royalty buyer too, bundling a revenue interest with senior secured debt in a single bilateral facility.

For a borrower facing a binary approval event, a one-counterparty package that blends debt and royalty is operationally simpler than running a separate royalty process alongside a DRI or an HCRx. For the royalty market, it means a large venture lender is now competing directly on royalty origination at the commercial-launch inflection point, financed off a permanent-capital balance sheet and an institutional private credit platform.

Royalty buyer view. A direct competitor on launch-stage royalty origination, not just a senior lender to underwrite around.

Channel 2: senior secured debt beside a third-party royalty monetisation

This remains the more common case. In late 2025, Viridian Therapeutics announced a royalty financing of up to $300 million with DRI Healthcare, taking $55 million upfront plus near-term milestones. In the same disclosure, Viridian noted an amended Hercules credit facility providing milestone-based access to capital, and Hercules separately upsized its commitment to $250 million.

The structure is the point. The royalty buyer (DRI) takes a revenue interest in veligrotug and VRDN-003. Hercules holds first-lien senior secured debt against the company. The two instruments coexist: the royalty is carved out of product revenue, while the secured lender holds priority on the broader asset base. For a royalty investor, this is the live tension in every late-stage biopharma capital structure: where the secured debt sits relative to the royalty carve-out, and whether covenants and lien grants in the debt constrain the company's ability to monetise royalties later.

The contrast with Beren is instructive. In Viridian, the debt and the royalty are written by different parties who must negotiate priority; in Beren, Hercules holds both sides and sets the waterfall itself.

Royalty buyer view. Hercules is the senior secured lender you underwrite around.

Channel 3: marketed-product specialty pharma exposure

Through borrowers like Corium Therapeutics, which markets and distributes AZSTARYS (a CNS stimulant for ADHD), Hercules holds debt against commercial product cash flows. AZSTARYS itself carries upstream royalty and milestone obligations to its originators, a stacked economic structure of exactly the kind this publication tracks. Hercules' exposure is to the borrower's enterprise, not to the product royalty, but its $185 million commitment was repaid or crystallised through the $650 million Collegium acquisition announced in March 2026.

Royalty buyer view. Indicator of where marketed-product credit is being written; not a royalty target.

Channel 4: warrants and equity (upside, not royalty)

Hercules converts part of its credit risk into warrants across 113 companies and equity across 73 companies. These produce capital appreciation on IPOs and M&A (Alamar Biosciences' 2026 IPO, the Collegium and SAP acquisitions of portfolio names), but they are equity-linked upside, not contractual royalty cash flow.

Royalty buyer view. Not a royalty stack. Equity optionality on the same names a royalty fund might also be tracking.

Summary: Hercules royalty stack relevance

Four channels of relevance, ranked by directness to a royalty buyer. Since June 2026, one channel is genuinely new.

| Channel | Royalty-stack relevance | Buyer interest |

|---|---|---|

| Hercules-originated hybrid (Beren) | Direct: Hercules writes the royalty tranche itself | Competitor on launch-stage royalty origination |

| Senior secured debt beside royalties | Structural: sits senior to / beside third-party royalty | Capital-structure counterparty |

| Marketed-product specialty pharma | Indirect: lends against products that carry royalties | Commercial-credit indicator |

| Warrants and equity | None directly | Equity upside on shared names |

| All other portfolio (tech, etc.) | None | Not therapeutics-related |

The net read: Hercules remains, first and foremost, a senior secured venture lender and a frequent neighbour in the capital structure. But the Beren financing is the first clear sign that it will write royalty paper directly when bundling it with debt wins the deal. That makes it both a map of where commercial-stage biopharma credit is being written and, increasingly, a competitor at the launch-stage end of the royalty market.

Leadership

| Person | Role | Background |

|---|---|---|

| Scott Bluestein | CEO, President, and CIO | Joined 2010 as Chief Credit Officer, CIO from 2014, CEO since 2019; previously founder/partner at Century Tree Capital and managing director at Laurus-Valens; Emory University |

| Seth Meyer | Chief Financial Officer | Oversees ratings, capital markets, and balance-sheet strategy |

| Robert P. Badavas | Chairman of the Board | Long-tenured independent director; interim chairman in 2019; chairman since the role was separated from CEO |

| Manuel Henriquez | Founder (former Chairman/CEO) | Founded the firm in 2003; resigned March 2019 amid Operation Varsity Blues; no longer involved |

| R. Bryan Jadot | Head of Venture Lending, Life Sciences | Joined 2005; previously VP of the Life Sciences Group at Silicon Valley Bank |

| Michael McMahon | Managing Director, Healthcare and Life Sciences | Joined 2023; 18 years at Silicon Valley Bank across senior secured, mezzanine, and recurring-revenue structures; Boston-based |

The life sciences team is notably ex-Silicon Valley Bank, which is consistent with where venture-debt underwriting talent migrated after SVB's 2023 failure.

Blue team, red team. Both readings are defensible from the same public record.

Blue Team: the case for Hercules Capital

Two decades as the dominant venture lender. Hercules has committed more than $27 billion to over 700 companies since 2003 and describes itself as the largest non-bank venture lender in the US. The franchise has operated through the global financial crisis, the 2022 rate shock, and the 2023 banking stress, with a cumulative realised loss rate of roughly 0.49% of commitments, or about 2.3 basis points annualised.

Record originations and investment income. Q1 2026 produced record total new commitments of $1.81 billion and record total investment income of $141.5 million, with NII covering the base distribution at 120%.

First-lien, floating-rate, low non-accrual. The debt book is 88.6% first-lien senior secured and 98.0% floating-rate, with a single loan on non-accrual at 0.1% of fair value. Asset sensitivity works in the firm's favour while base rates stay elevated.

Investment-grade across three agencies. Hercules carries KBRA BBB+, a Moody's upgrade to Baa2, and Fitch BBB-, all stable, with roughly 86% of debt unsecured.

Internally managed structure. Unlike most BDCs, Hercules is internally managed, which aligns the manager with shareholders and avoids the external-manager fee drag that weighs on peers.

A growing private credit platform. The fourth Hercules Adviser private credit fund adds fee income and institutional capital alongside the permanent BDC balance sheet, and the firm was named 2025 Americas BDC Manager of the Year.

Red Team: the case against Hercules Capital

An active securities class action. A securities fraud class action was filed against Hercules and certain officers in the Northern District of California (case 26-cv-02465), covering a class period of May 1, 2025 to February 27, 2026. The complaint alleges the firm overstated the rigour of its deal-sourcing and valuation processes, misclassified portfolio investments, and overstated portfolio valuations.

It treats the February 27, 2026 Hunterbrook report as the corrective disclosure; HTGC fell 7.9% that day to $14.21. The lead-plaintiff deadline was May 19, 2026. The case is unproven and Hercules disputes the underlying claims, but litigation of this kind is an overhang on the stock and on management's disclosure record.

Heavy software concentration. The February 2026 Hunterbrook Media short thesis argued that Hercules carries roughly $1.5 billion of software debt, about 35% of its loan portfolio, making it (per the report's reading of JPMorgan analysis) the most software-exposed lender of meaningful size in the US.

The report questioned the firm's "portfolio turns every 18 to 24 months" framing and alleged that some software loans were marked at or above par despite sector distress. Hercules disputed the figures, stating that since 2022, 63% of new fundings went to new portfolio companies. The dispute is contested, but it is now also the spine of the class action.

The stock has de-rated. After the report and Q1 2026 volatility, several brokers cut targets (Citizens to $22, Keefe Bruyette to $18, Piper Sandler to $16.50), and the shares trade around $15 against a 52-week range of roughly $13.70 to $19.67, with a market capitalisation near $2.9 billion. The premium to the $11.90 NAV has compressed materially from its highs.

NAV is grinding lower. NAV per share fell 1.9% in Q1 2026 to $11.90, driven by net unrealised depreciation on the debt and equity book, including market-yield marks. The equity and warrant marks add volatility that a pure-credit BDC would not carry.

Royalty origination is unproven for Hercules. The Beren hybrid is a first, not a track record. Writing a $55 million royalty tranche on a drug whose approval is still pending (a PDUFA date extended three months after an FDA major amendment) is a different risk than senior secured lending, and Hercules has no public history underwriting royalty duration or sales curves the way a dedicated royalty fund does.

Founder-scandal legacy. The 2019 departure of founder Manuel Henriquez under criminal charges was an idiosyncratic governance shock. The post-2019 record under Bluestein has been strong, but the episode remains part of the firm's history and reputation.

Private fund LP opacity. The institutional LP base in the Hercules Adviser funds is undisclosed, and the private credit funds are still young relative to the BDC. The cross-allocation of originations between the BDC and the Adviser Funds is a structure that requires watching for conflicts, even where none has surfaced.

Implications for the pharmaceutical royalty and biotech capital markets

For a royalty fund, Hercules is now two things at once: a frequent counterparty and, as of June 2026, an occasional competitor. When a late-stage biopharma name does a synthetic or traditional royalty deal, there is often a Hercules first-lien facility already in the structure (the Viridian and DRI Healthcare pairing), so understanding where Hercules' lien and covenants sit determines how much royalty a company can actually sell.

But the Beren financing shows Hercules will also write the royalty itself when it can bundle it with debt and win the whole package. A royalty underwriter who ignores the senior secured layer underwrites half the capital structure; one who assumes Hercules will always stay in that layer may find it bidding on the same royalty.

For a BD executive, Hercules is a window into which commercial-stage and late-clinical companies are funding through debt rather than out-licensing or equity, and into the milestone structures lenders are willing to write.

For a technology transfer office, Hercules is largely out of scope. It does not absorb academic IP or take licensing positions; it lends to companies that already have a clinical or commercial asset.

The broader signal is that the non-dilutive financing stack for biopharma is layering. Senior secured venture debt (Hercules), revenue-interest and royalty monetisation (the royalty funds), and development financing now coexist in the same companies. The competitive map is less about who displaces whom and more about who sits where in the waterfall.

Conclusion

Hercules Capital is the largest non-bank venture lender in the United States: a 20-year-old, internally managed, publicly traded BDC with roughly $6.1 billion of platform AUM, a first-lien floating-rate book, investment-grade ratings from three agencies, and a growing institutional private credit franchise alongside the public vehicle.

A blue team sees a disciplined, scaled, cycle-tested franchise compounding record originations with a near-zero historical loss rate and a 120%-covered double-digit distribution. A red team sees heavy software concentration, a contested turnover narrative, an active securities class action, a de-rated stock, a NAV grinding lower on equity and credit marks, and a founder-scandal legacy. Both readings are defensible from the public record.

For the royalty market specifically, the story changed in June 2026. Hercules has long mattered as the senior secured layer sitting above and beside the royalty in commercial-stage biopharma capital structures, with the Viridian and DRI Healthcare pairing as the template.

The Beren Therapeutics financing adds a second template: Hercules writing the royalty tranche itself, bundled with senior secured debt, in a single facility at the launch inflection point. Whether that becomes a repeatable product or stays a one-off will determine whether Hercules is a counterparty the royalty funds underwrite around or a competitor they bid against. Either way, whoever underwrites one side of these structures had better understand the other.

All information in this article was accurate as of June 2026 and is derived from publicly available sources including Hercules Capital's own filings and press releases, SEC filings, rating agency publications, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.