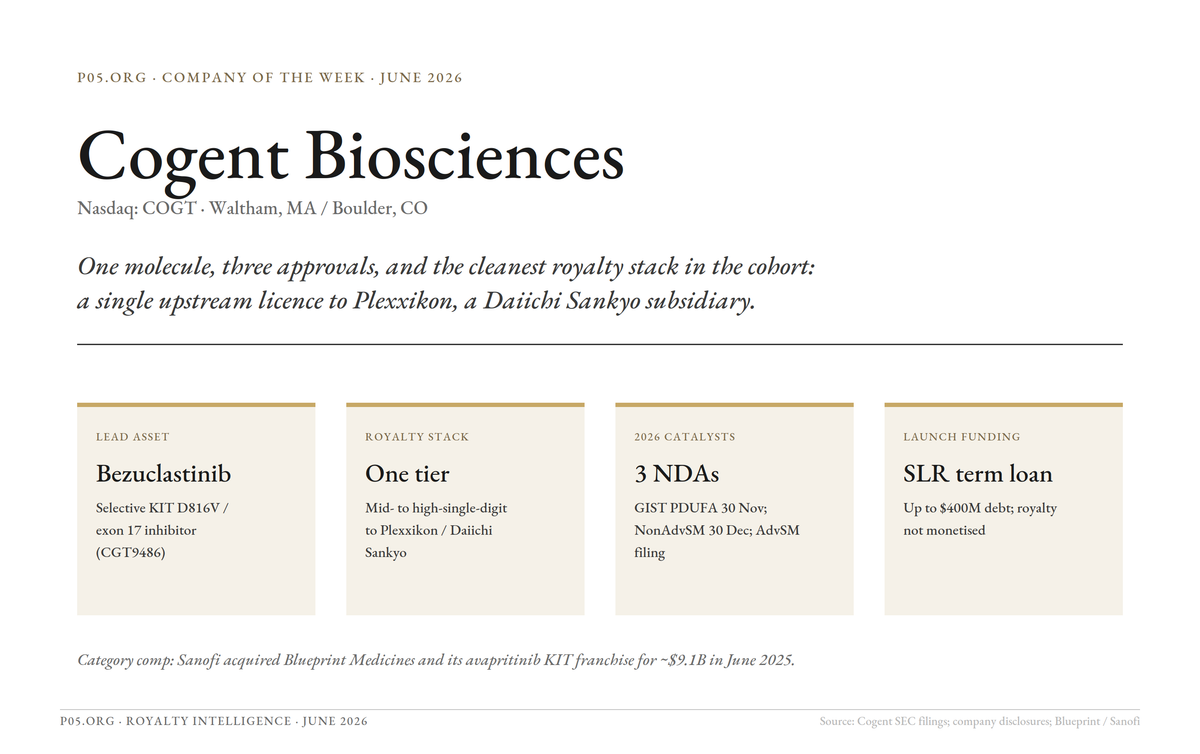

Company of the week: Cogent Biosciences

Cogent Biosciences, Inc. (Nasdaq: COGT) is a Waltham and Boulder based biotechnology company developing precision therapies for genetically defined diseases. Its single clinical-stage product, bezuclastinib, is a selective tyrosine kinase inhibitor of the KIT D816V mutation and other KIT exon 17 mutations, and is the engine behind three near-simultaneous U.S. regulatory filings in 2026.

The company was formerly Unum Therapeutics, a cell-therapy company that recapitalised, in-licensed bezuclastinib and renamed itself Cogent in October 2020. It is led by President and CEO Andrew Robbins, a former Array BioPharma commercial executive, and runs its discovery effort out of the Cogent Research Team in Boulder, Colorado.

For a royalty market reader, Cogent is interesting for reasons that have little to do with the AI-platform or novel-modality framings that dominate most biotech coverage.

Bezuclastinib was licensed worldwide from Plexxikon Inc., a subsidiary of Daiichi Sankyo, and carries one clean upstream royalty layer rather than a stacked patent thicket. The molecule is approaching three separate U.S. approvals (non-advanced systemic mastocytosis, advanced systemic mastocytosis and second-line gastrointestinal stromal tumours) inside roughly twelve months. And the company sits squarely in the category that Sanofi validated in June 2025 when it paid approximately USD 9.1 billion for Blueprint Medicines and its KIT franchise.

Cogent also did something that royalty-market participants should notice: faced with a textbook synthetic-royalty monetisation profile, it chose a structured term loan instead.

This article examines Cogent's origins and the bezuclastinib in-licence, the royalty stack on the asset, the three pivotal datasets (SUMMIT, PEAK, APEX) and the 2026 regulatory cascade, the competitive position against Sanofi's avapritinib, the financing structure and why the royalty was not monetised, the early-stage pipeline, and an asset-by-asset royalty potential read.

Origins: a recapitalised shell and one in-licensed molecule

Cogent's corporate history is unusual. The listed entity began as Unum Therapeutics, a CAR-T and antibody-coupled T-cell receptor company that ran into clinical and financing difficulty. Rather than wind down, the company in-licensed a clinical-stage small molecule, brought in a new management team, and relaunched as Cogent Biosciences in October 2020.

The molecule was bezuclastinib, then known by the development codes CGT9486 and PLX-9486.

Cogent licensed the exclusive worldwide rights to develop and commercialise bezuclastinib from Plexxikon. Under the agreement, Plexxikon received an upfront payment and is eligible for additional development and regulatory milestone payments along with mid- to high-single-digit royalty payments on sales.

The asset itself is a selective KIT inhibitor. KIT D816V, the activating mutation that holds the receptor in a constitutive on state, drives the great majority of systemic mastocytosis cases through unchecked mast-cell proliferation. The same exon 17 mutations appear in advanced gastrointestinal stromal tumours, a cancer with strong dependence on oncogenic KIT signalling, where they are a frequent mechanism of resistance to earlier therapy.

Bezuclastinib was therefore a single molecule with two biologically distinct disease franchises attached to the same target. That breadth is what allowed a recapitalised single-asset company to build a three-indication late-stage programme.

The team profile matters. Robbins came from a commercial rather than a discovery background, and Cogent built an internal commercial organisation well ahead of approval rather than positioning itself purely as a partnering vehicle. The strategic intent from the relaunch was to commercialise bezuclastinib directly in the United States, not to out-license it.

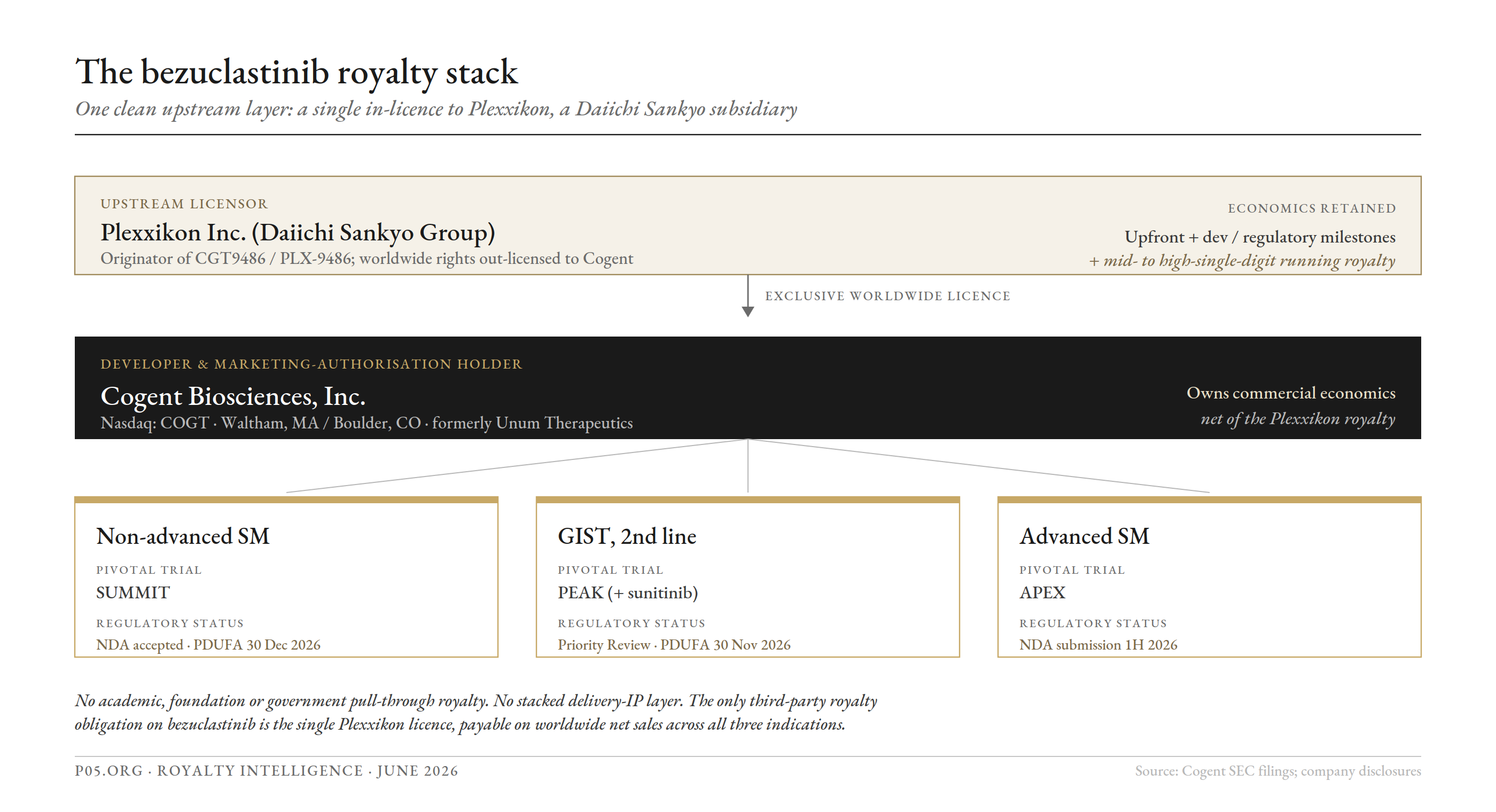

The royalty stack: one clean upstream layer

The royalty structure on bezuclastinib is the cleanest of any company we have profiled in this series.

There is exactly one third-party royalty obligation: the Plexxikon licence. It runs on worldwide net sales, at a disclosed mid- to high-single-digit rate, across all three indications. There is no academic or foundation licensor in the published filings, no government grant pull-through, and, because bezuclastinib is a conventional oral small molecule, no separate delivery-technology or manufacturing-IP layer of the kind that complicates the LNP and antibody-drug-conjugate franchises.

Three observations on the stack as a structural matter.

Cogent is a royalty payer on a single tier, not a royalty stacker.

The economics flow from Cogent (the marketing-authorisation holder) up to Plexxikon, and from Plexxikon up to Daiichi Sankyo as its parent. For a royalty-financing counterparty, this is a simple waterfall to diligence: there is one senior contractual royalty ahead of any synthetic layer a financier might create, and that royalty is held by a creditworthy global pharma group rather than a fragile academic spin-out.

The composition-of-matter base is in-house to the originator.

Bezuclastinib (CAS 1616385-51-3) is a new molecular entity discovered at Plexxikon, not a reformulation of an existing generic. Unlike a Category 2.2 improved-drug play, the patent estate protecting the active is the originator's own composition-of-matter position. That makes the royalty-bearing exclusivity period a function of the underlying NCE patents and any regulatory exclusivity, rather than of a formulation-patent fence around a known molecule.

The same royalty applies across three independent revenue streams.

Because the Plexxikon royalty is struck on net sales of bezuclastinib rather than on a single indication, the three approvals (non-advanced SM, advanced SM, GIST) feed one consolidated royalty base. For a financier, this is diversification within a single contract: three launch curves, three reimbursement dynamics, and three competitive contexts, all underneath one royalty definition.

The structural conclusion is that bezuclastinib is a rare example of a near-commercial asset whose royalty stack is genuinely simple. The diligence question is not who else holds a claim, but whether the single product can convert three approvals into durable sales against an entrenched incumbent.

The three pivotal datasets

Bezuclastinib reported positive results from all three of its registration-directed trials across 2025, an unusually clean run for a single-asset company.

SUMMIT (non-advanced systemic mastocytosis)

SUMMIT is the registration-directed, randomised, double-blind, placebo-controlled Part 2 trial in non-advanced SM, the larger and more chronic of the two mastocytosis populations.

In the July 2025 top-line readout, the bezuclastinib arm achieved a mean reduction of 24.3 points in total symptom score at 24 weeks versus 15.4 points for placebo, an 8.91-point placebo-adjusted improvement (p=0.0002), measured on the Mastocytosis Symptom Severity Daily Diary. The trial met its primary endpoint and all key secondary endpoints, including objective measures of mast-cell burden.

Open-label extension data presented at AAAAI 2026 showed the benefit deepening over time, with a mean total symptom score reduction of 32.0 points at 48 weeks (a 56% relative improvement), 99% of patients achieving at least a 50% reduction in serum tryptase, and 83% normalising tryptase levels by week 48. Bezuclastinib received Breakthrough Therapy Designation in non-advanced SM in October 2025.

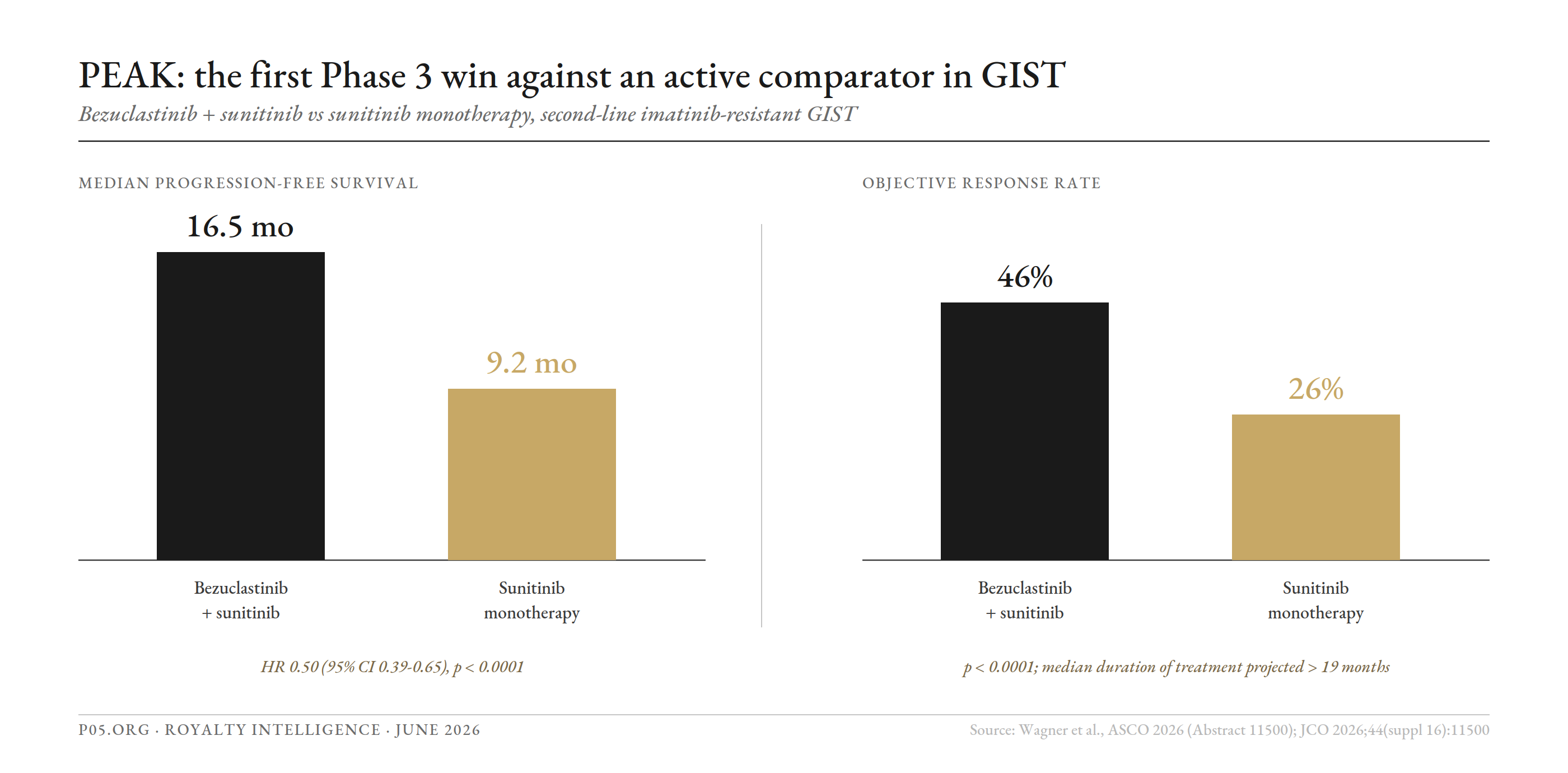

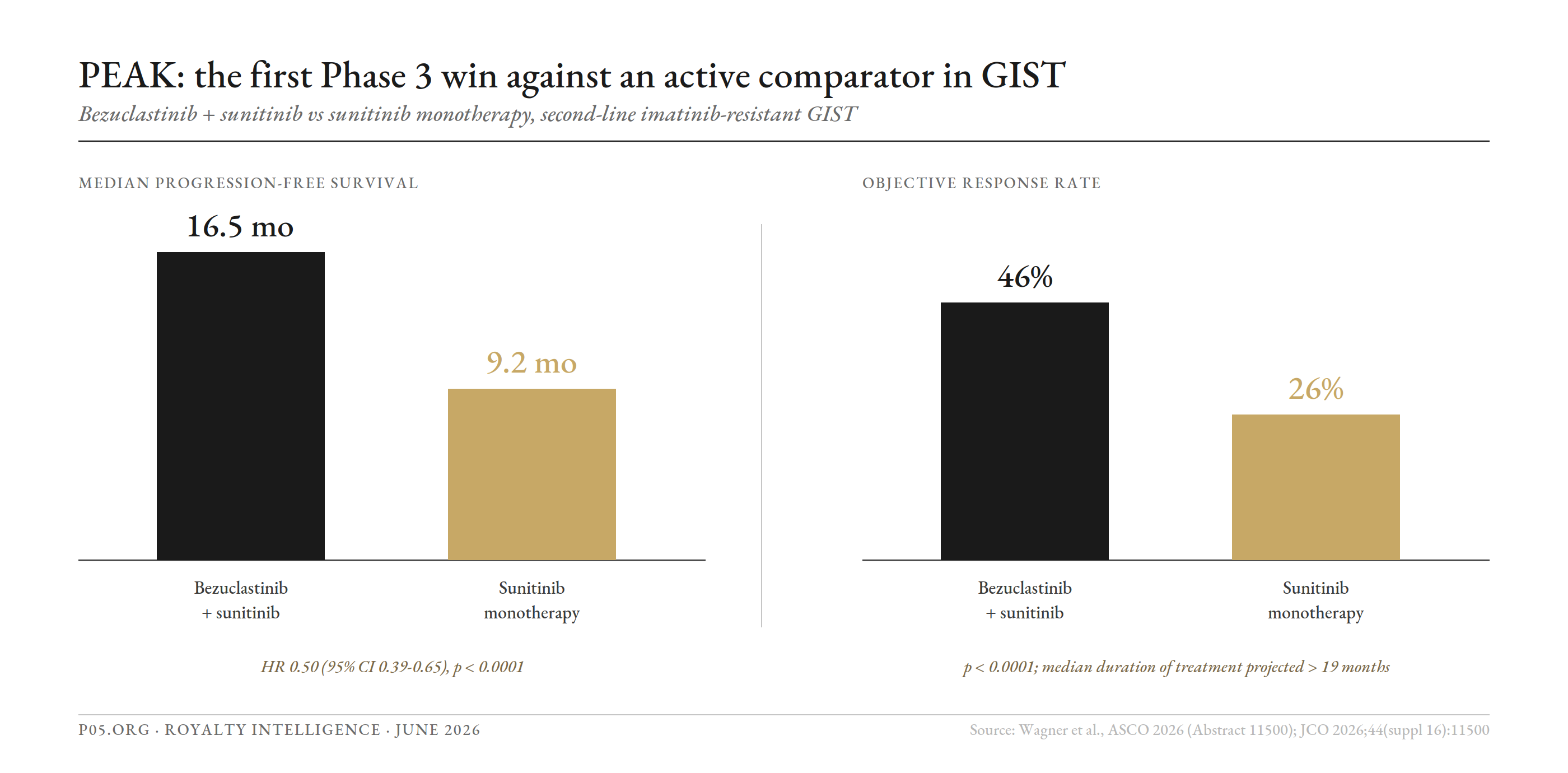

PEAK (second-line GIST)

PEAK is the global, randomised Phase 3 trial of bezuclastinib in combination with sunitinib versus sunitinib monotherapy in patients with imatinib-resistant or intolerant GIST. It is the most consequential dataset in the portfolio.

At the September 30, 2025 cutoff, the combination delivered a median progression-free survival of 16.5 months versus 9.2 months for sunitinib alone, a 50% reduction in the risk of progression or death (HR 0.50, 95% CI 0.39-0.65, p<0.0001). The objective response rate was 46% for the combination versus 26% for monotherapy (p<0.0001), and the estimated median duration of treatment on the combination arm is projected to exceed 19 months. Full results were presented in an oral session at ASCO 2026 on May 30, 2026 (Abstract 11500) by Andrew Wagner of Dana-Farber Cancer Institute.

This is, by the company's framing and by independent oncology coverage, the first Phase 3 trial in over twenty years to demonstrate a statistically significant advantage over an active comparator in GIST. On safety, hepatic adverse events were predominantly transient and manageable laboratory abnormalities; ALT/AST elevations led to bezuclastinib dose reductions in 12.7% of patients, with only 1.5% discontinuing for that reason.

APEX (advanced systemic mastocytosis)

APEX is the registration-directed Part 2 trial in advanced SM, the rarer and more aggressive mastocytosis population. Positive top-line results were announced in December 2025, demonstrating clinically meaningful benefit on the consensus response criteria used to assess the disease. This was the third positive pivotal readout for bezuclastinib in a single year.

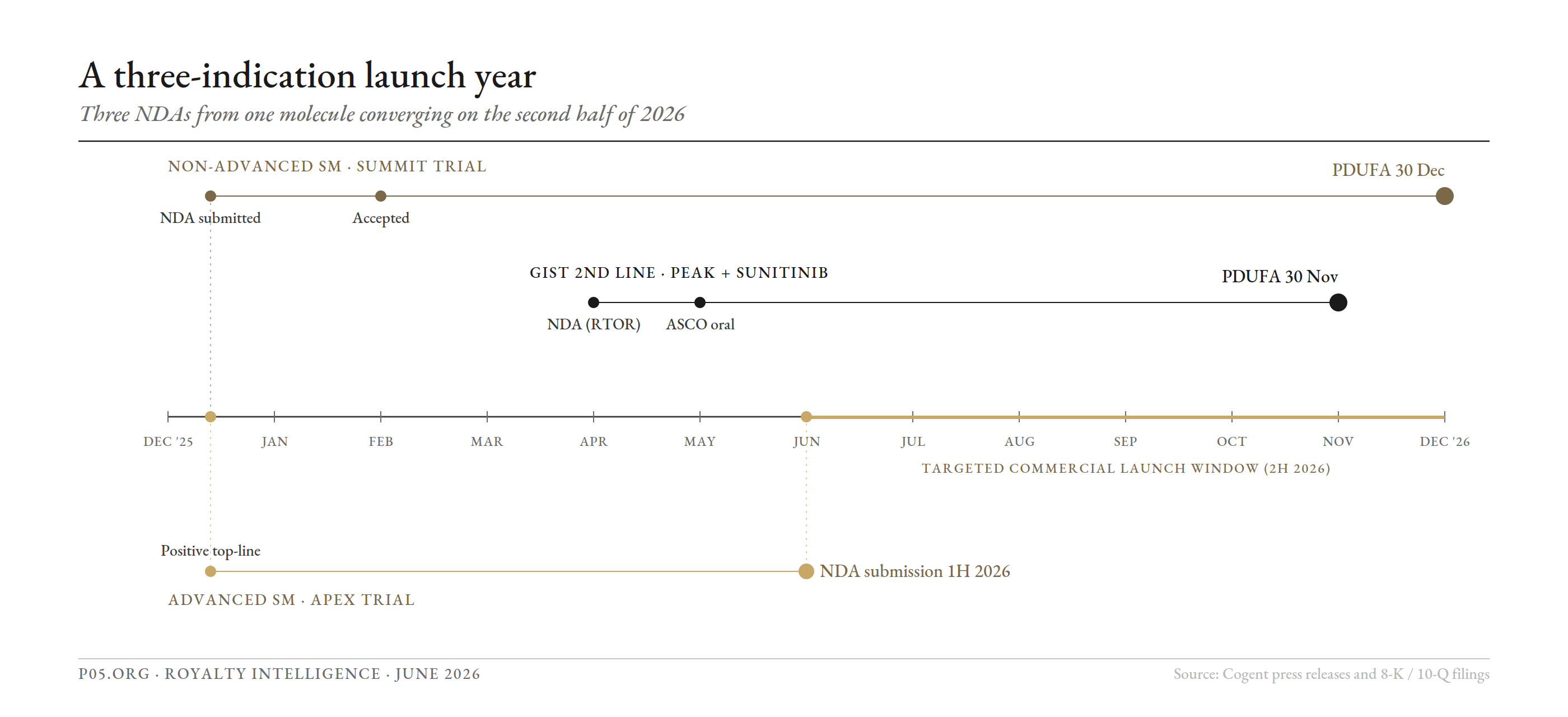

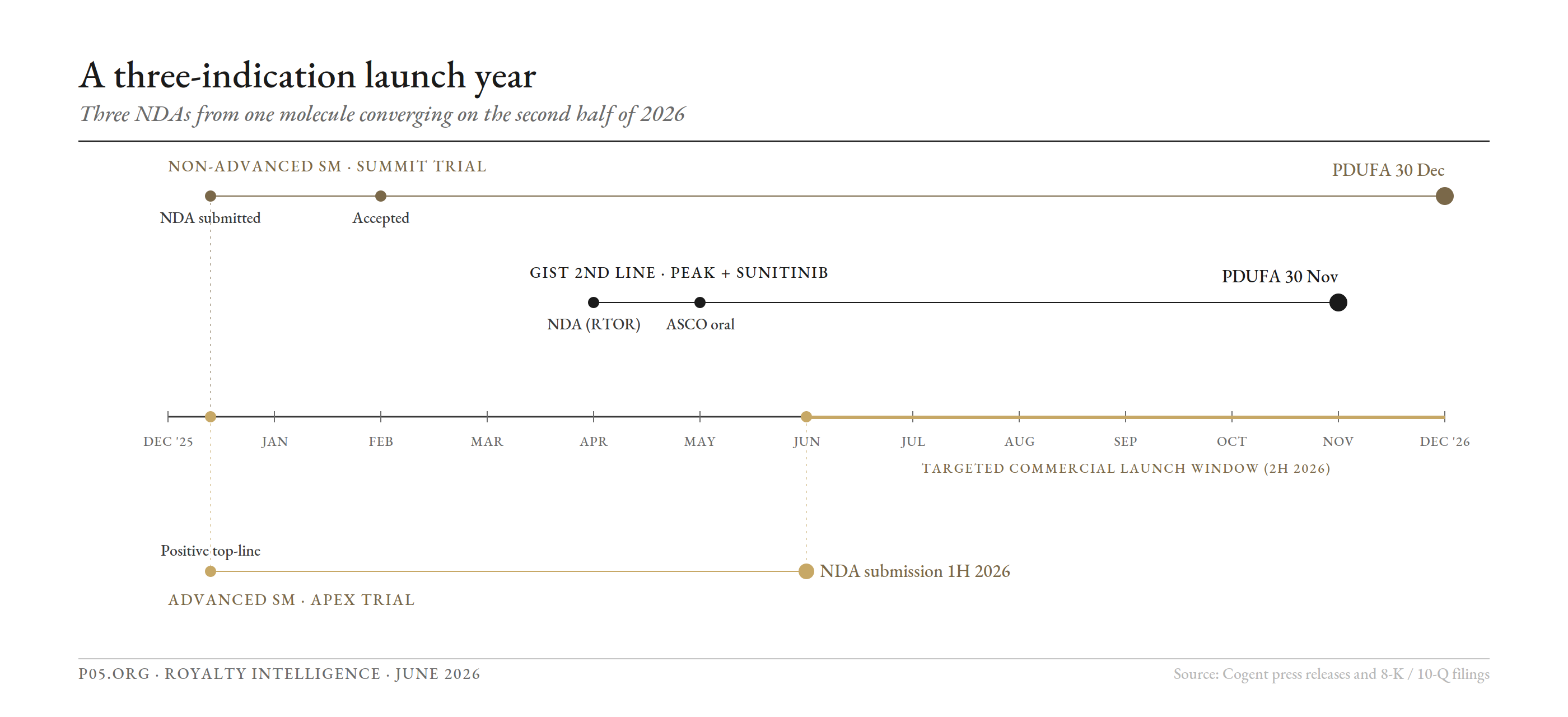

The 2026 regulatory cascade

The three datasets translate into three NDAs and a regulatory calendar that converges on the second half of 2026.

| Indication | Trial | Regulatory pathway | Status as of June 2026 |

|---|---|---|---|

| Non-advanced SM | SUMMIT | Breakthrough Therapy | NDA submitted Dec 2025; accepted, PDUFA 30 Dec 2026 |

| GIST, 2nd line | PEAK (+ sunitinib) | RTOR + Breakthrough Therapy | NDA submitted Apr 2026; accepted with Priority Review, PDUFA 30 Nov 2026 |

| Advanced SM | APEX | Standard | NDA submission expected 1H 2026 |

The FDA has communicated that it has no current plan to hold an advisory committee for either accepted application and has not identified review issues. Pending approval, Cogent intends to launch bezuclastinib in the United States in the second half of 2026, supported by the internal commercial organisation it has been building since the relaunch.

For the royalty market the structurally relevant point is that the first commercial royalty base is imminent and concentrated. Two PDUFA dates (November 30 and December 30, 2026) sit roughly one month apart, with a third filing in train. A single approval cycle converts bezuclastinib from a development-stage asset to a multi-indication commercial product, which is precisely the inflection at which royalty-financeable cash flows begin.

The competitive position: Sanofi's avapritinib sets the comp

Bezuclastinib does not enter an empty field. In systemic mastocytosis it faces avapritinib, marketed as Ayvakit in the United States and Ayvakyt in Europe, the first and only approved disease-modifying medicine for both advanced and indolent SM.

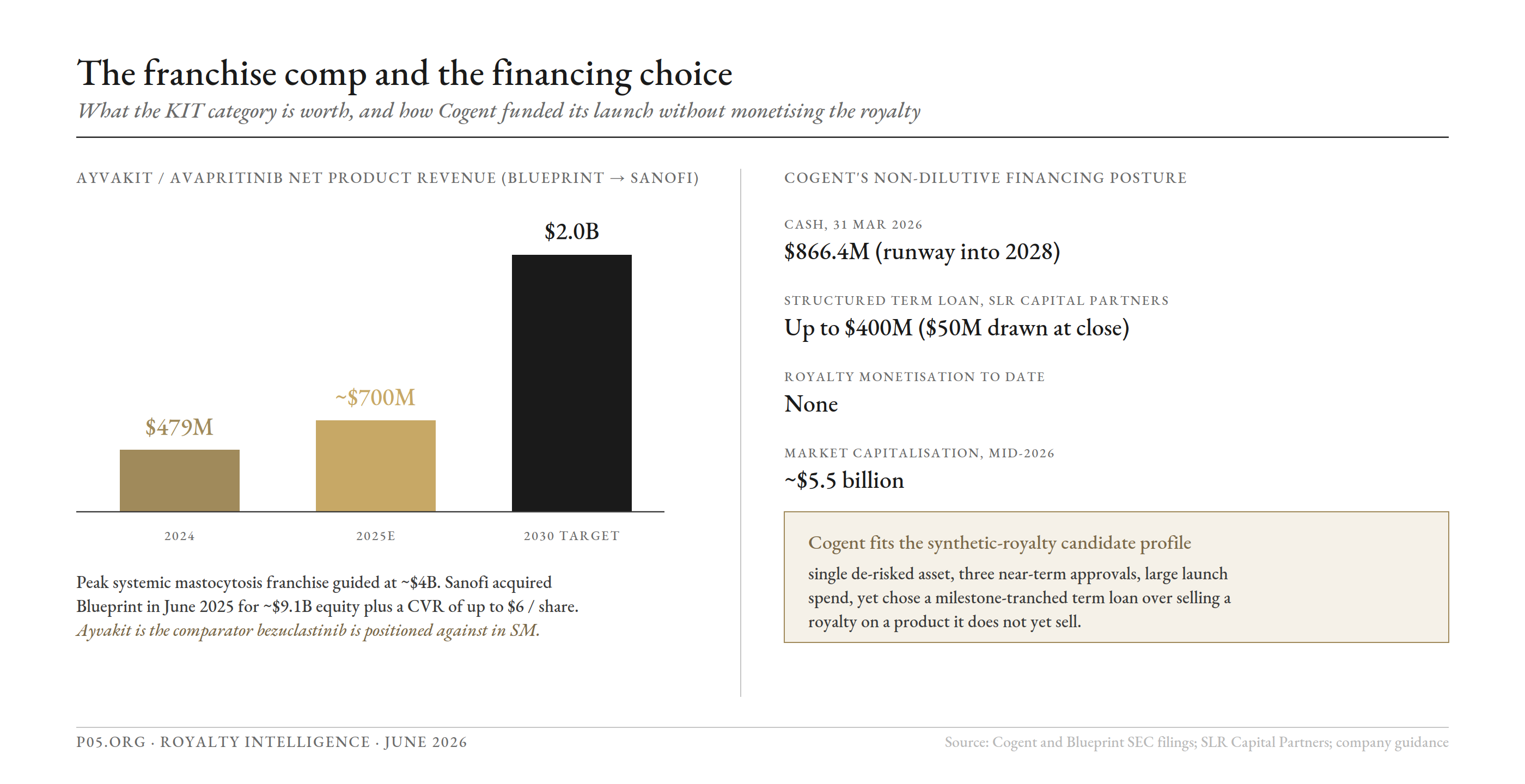

Avapritinib is the asset at the centre of one of the most important rare-disease franchise transactions of 2025. On June 2, 2025, Sanofi agreed to acquire Blueprint Medicines for USD 129.00 per share, an equity value of approximately USD 9.1 billion, plus a contingent value right of up to USD 6.00 per share tied to milestones on the next-generation KIT inhibitor BLU-808. The acquisition also brought elenestinib, Blueprint's next-generation SM candidate.

The franchise economics behind that price are the comparison set bezuclastinib will be measured against. Ayvakit generated USD 479 million in net product revenue in 2024, with 2025 guidance subsequently raised to roughly USD 700 to 720 million, a path toward USD 2 billion by 2030, and a peak SM franchise opportunity guided at approximately USD 4 billion against an estimated 25,000 diagnosed SM patients in the United States alone.

Two implications follow for the royalty market.

The category is large, growing and now strategically owned.

A USD 4 billion peak-franchise estimate and a USD 9.1 billion acquisition establish that KIT-driven mast-cell disease is a real commercial category, not an orphan curiosity. Bezuclastinib does not need to displace avapritinib to be financeable; it needs a defensible share of an expanding, under-diagnosed market, and in GIST it addresses a population where avapritinib is not the standard of care.

Bezuclastinib's GIST position is differentiated from the SM contest.

In second-line GIST the comparator is sunitinib, with regorafenib and ripretinib in later lines. The PEAK combination is positioned to be the first regimen to beat an active comparator head-to-head, a cleaner differentiation claim than the SM franchise fight with an entrenched Sanofi product. The royalty value of the GIST indication is therefore less contingent on share-of-voice against avapritinib and more on the strength of the head-to-head PFS and ORR data.

The other implication is corporate. Sanofi's willingness to pay USD 9.1 billion for the adjacent franchise makes Cogent a plausible strategic target in its own right. That matters for royalty structuring, where change-of-control provisions and acquirer creditworthiness are first-order diligence items.

The financing choice: structured debt, not a monetised royalty

This is the point at which Cogent becomes genuinely instructive for the royalty market.

On the conventional checklist, Cogent is a near-perfect synthetic-royalty monetisation candidate. It is a single-product company with a de-risked, multi-indication asset, three near-term approvals, a large pre-launch commercial build, and a clean one-tier royalty stack. This is the profile that royalty aggregators and structured-credit funds compete to finance.

Cogent chose differently. In June 2025 it secured a non-dilutive debt facility of up to USD 400 million with credit funds managed by SLR Capital Partners, drawing an initial USD 50 million at closing, with subsequent tranches released against clinical and commercial milestones. An additional USD 100 million was tied to the SUMMIT and PEAK readouts and a further USD 50 million to early commercial success. Leerink Partners advised on the term loan.

Combined with approximately USD 866.4 million in cash at the end of the first quarter of 2026 and a stated runway into 2028, the SLR facility means Cogent funded its launch without selling a royalty on a product it does not yet sell.

The structural read for a royalty market participant is threefold.

A milestone-tranched term loan preserved the royalty optionality.

By taking structured debt rather than monetising the royalty, Cogent kept the full economics of the asset and retained the ability to monetise later, post-approval, when a royalty on actual net sales would command a materially tighter advance rate and a lower cost of capital than a pre-launch synthetic on forecast sales. The financing was sequenced to defer the royalty decision until the asset is de-risked further.

The advance was sized to milestones, not to a forecast royalty curve.

The tranche structure (initial draw, data-contingent tranches, commercial-success tranche) mirrors the de-risking schedule rather than discounting a single projected sales forecast. For the company this lowers the dilutive and economic cost of capital in the pre-revenue window; for a future royalty financier it leaves the most attractive collateral, the running royalty on launched product, unencumbered by a prior monetisation.

The candidate did not become a transaction.

For deal-flow trackers, Cogent is a reminder that the synthetic-royalty candidate set is wider than the executed-deal set. A company can fit every screen a royalty fund runs and still route its launch capital through structured credit. The next financing datapoint to watch is whether Cogent monetises the bezuclastinib royalty after a first approval, which would be the cleaner, post-launch royalty-financeable cash flow, or whether it continues to draw on the SLR facility and preserve the royalty intact.

The pipeline: the Cogent Research Team

Behind bezuclastinib, the Boulder-based Cogent Research Team is building a portfolio of selective small-molecule inhibitors against genetically defined targets.

| Programme | Target / mechanism | Indication focus | Stage as of June 2026 |

|---|---|---|---|

| CGT4859 | FGFR2/3 inhibitor | FGFR2/3-altered tumours, cholangiocarcinoma | Phase 1/2 |

| CGT4255 | CNS-penetrant mutant ErbB2 inhibitor | HER2-mutant / CNS-involved tumours | Phase 1 |

| CGT6297 | Wild-type-sparing PI3Ka inhibitor | PI3Ka-driven tumours | Phase 1 |

| CGT1815 | pan-KRAS(ON) inhibitor | KRAS-driven tumours | IND in 2026 |

| CGT1145 | JAK2 V617F inhibitor | Myeloproliferative neoplasms | IND in 2026 |

The pipeline is consistent in approach: selective, often wild-type-sparing or CNS-penetrant inhibitors of well-validated oncogenic drivers, several of which (pan-KRAS, JAK2 V617F) are among the most contested targets in oncology and haematology. All of these programmes are wholly owned and internally discovered, so unlike bezuclastinib they carry no upstream royalty obligation. For the royalty market they are early, but they establish that any future royalty-bearing assets from the research engine would have an even cleaner stack than the in-licensed lead.

Asset-by-asset royalty potential

| Asset | Royalty stack | Out-licensing status | Royalty-financeable horizon |

|---|---|---|---|

| Bezuclastinib, non-advanced SM | One-tier; Plexxikon mid- to high-single-digit | Wholly owned; U.S. commercialisation planned | First cash flow on approval (PDUFA 30 Dec 2026) and 2H 2026 launch |

| Bezuclastinib, GIST 2nd line | Same one-tier stack | Wholly owned | First cash flow on approval (PDUFA 30 Nov 2026); strongest differentiation claim |

| Bezuclastinib, advanced SM | Same one-tier stack | Wholly owned | NDA 1H 2026; cash flow on subsequent approval |

| Bezuclastinib, ex-US | Same one-tier stack | Worldwide rights retained; no ex-US partner disclosed | Optionality on ex-US partnering or self-commercialisation |

| CGT4859 / CGT4255 / CGT6297 | Clean; in-house, no upstream | Wholly owned | 2028+ pending early clinical data |

| CGT1815 / CGT1145 | Clean; in-house, no upstream | Wholly owned | Pre-clinical to IND; 2028+ |

The portfolio-level observation is that the entire royalty-financeable value today sits in one molecule with one upstream royalty, payable to a creditworthy global pharma group, across three converging approvals. There is no patent-thicket caveat of the kind that attaches to LNP or ADC franchises, and no fragile academic licensor in the chain. The binary risk is commercial execution against an entrenched incumbent, not IP cleanliness.

Red team vs blue team analysis

Risk analysis (red team)

Single-asset concentration. Effectively all near-term value depends on one molecule. A regulatory delay, a label restriction, or a commercial stumble at launch would hit every revenue line at once, because the three indications share one active ingredient and one franchise organisation.

An entrenched, well-capitalised incumbent in SM. Avapritinib is the only approved disease-modifying SM therapy, is now owned by Sanofi, and carries a commercial infrastructure and prescriber base built since launch. Bezuclastinib must win share in SM against a product with first-mover advantage and a deep-pocketed owner, and Sanofi also holds the next-generation candidate elenestinib.

The GIST benefit is a combination, with a hepatic-safety signal to manage. The PEAK result is for bezuclastinib added to sunitinib, not as monotherapy, and the safety narrative centres on transient ALT/AST elevations. While discontinuations for hepatic events were low (1.5%), the label and real-world tolerability of the combination will shape uptake.

Overall survival remains immature. The PEAK primary endpoint is PFS; overall survival data are not yet mature. Payers and some prescribers weight OS heavily in oncology, and the durability of the commercial case depends partly on how OS reads out over time.

A royalty has not been monetised, so the structure is untested. Cogent's clean one-tier stack is attractive in theory, but the company has not executed a royalty transaction. Until one is done, the advance rate, the running-royalty disclosure and the change-of-control terms that a financier would actually obtain remain hypothetical.

Pre-profitability and a debt layer. The business is pre-revenue, carries a structured term loan with milestone covenants, and is funding a full U.S. commercial build. Runway is stated into 2028, but a slower-than-modelled launch would compress that horizon and elevate the role of the SLR facility's later tranches.

Opportunities and mitigants (blue team)

Three positive pivotal datasets in a single year. SUMMIT, PEAK and APEX all read out positively across 2025, an unusually clean late-stage run that materially de-risks the molecule across two diseases and three patient populations.

A genuine first in GIST. PEAK is the first Phase 3 trial in over twenty years to beat an active comparator in GIST, with a 50% reduction in the risk of progression and a doubling-plus of response rate. This is a differentiation claim that does not depend on out-competing avapritinib.

The cleanest royalty stack in the cohort. One upstream royalty, held by Daiichi Sankyo's Plexxikon, with no academic, foundation, government or delivery-IP layer. For a royalty financier this is close to an ideal diligence profile once the product is launched.

A validated, strategically owned category. Sanofi's USD 9.1 billion acquisition of Blueprint and a USD 4 billion peak-franchise estimate confirm the commercial scale of KIT-driven disease and, by extension, make Cogent a plausible strategic target.

Preserved royalty optionality and a multi-year runway. By financing with structured debt rather than a pre-launch royalty sale, Cogent retained the full economics of the asset and the ability to monetise the royalty later on better terms, while approximately USD 866 million in cash funds the launch into 2028.

A wholly owned discovery engine with no upstream encumbrance. The Cogent Research Team's pipeline (FGFR, ErbB2, PI3Ka, pan-KRAS, JAK2) is internally discovered, so any future royalty-bearing assets would carry an even simpler stack than the in-licensed lead.

Scenario analysis

Base case. Bezuclastinib is approved in GIST (PDUFA 30 Nov 2026) and non-advanced SM (PDUFA 30 Dec 2026), with the advanced SM NDA accepted on its 1H 2026 submission. Cogent launches in the United States in the second half of 2026 with its internal commercial team, drawing later SLR tranches as commercial milestones are met. The Plexxikon royalty base begins to build across three indications, and the running royalty remains unencumbered as Cogent defers any monetisation decision.

Better than expected. All three indications are approved on schedule with broad labels. GIST uptake is rapid on the strength of the head-to-head PEAK data, and bezuclastinib takes meaningful SM share despite avapritinib's incumbency. Cogent either monetises the now-launched royalty on favourable post-approval terms or becomes a strategic-acquisition target in the wake of the Sanofi-Blueprint precedent, crystallising the franchise value.

Worse than expected. A review delay or a narrower-than-hoped label slows the launch. SM share gains prove hard against a Sanofi-backed avapritinib and the next-generation elenestinib, GIST uptake is tempered by the combination's hepatic-safety management, and immature overall-survival data weigh on payer positioning. Runway tightens toward the SLR facility's later tranches and their covenants, and the single-asset concentration amplifies any single setback.

Conclusion

Cogent Biosciences is, in the narrow sense, a single-product biotechnology company whose one molecule, bezuclastinib, is approaching three U.S. approvals across systemic mastocytosis and GIST inside roughly twelve months.

For a royalty market readership the more interesting facts are four.

First, the royalty stack is unusually clean. There is one upstream royalty, payable to Plexxikon (a Daiichi Sankyo subsidiary) at a mid- to high-single-digit rate on worldwide net sales, with no academic, foundation, government or delivery-IP layer behind it. This is close to an ideal diligence profile, and the binary risk is commercial execution rather than IP cleanliness.

Second, three approvals from one molecule create a concentrated but diversified-within-contract royalty base. The November 30 and December 30, 2026 PDUFA dates, with a third filing in train, convert bezuclastinib from a development asset to a multi-indication commercial product inside a single approval cycle, which is exactly the inflection at which royalty-financeable cash flows begin.

Third, the Sanofi-Blueprint transaction sets the comp. A USD 9.1 billion acquisition and a USD 4 billion peak-franchise estimate validate the KIT category, frame the avapritinib competitive contest in SM, and make Cogent itself a plausible strategic target, which bears directly on change-of-control terms in any royalty structure.

Fourth, and most instructive, Cogent fits the synthetic-royalty monetisation profile almost perfectly and chose not to use it. Faced with a textbook candidate setup, it took a milestone-tranched SLR term loan instead, preserving the full royalty economics and the option to monetise later, post-launch, on tighter terms. For deal-flow trackers, this is a reminder that the royalty-candidate set is wider than the executed-deal set.

The next datapoint to watch is the first approval, and then whether Cogent monetises a now-launched bezuclastinib royalty or continues to preserve it intact. Either outcome will be a clean precedent for how a single-asset, one-tier-stack commercial-stage biotech finances a multi-indication launch.

All information in this article is derived from publicly available sources including company press releases, exchange disclosures, SEC filings, regulatory communications, peer-reviewed and conference publications, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.