No-Royalty Thresholds in Pharma Royalty Financing: When the Cash Doesn't Flow

A no-royalty threshold is a contractually defined level of net sales, time, or performance below which the buyer of a royalty receives nothing. The mechanism is uncontroversial in concept and notoriously consequential in practice. It moves cash flow timing, reshapes IRR distributions, alters accounting recognition, complicates true-sale opinions, and creates pre-petition flashpoints when the seller approaches insolvency.

Across the $32.7 billion in royalty-linked transactions documented by Gibson Dunn for 2020 through 2025, some form of threshold appears in the substantial majority of synthetic deals and in nearly every academic out-licence. Understanding which form is present, and how it interacts with the rest of the deal architecture, is the difference between modelling the cash flows correctly and being surprised in year three.

This article maps the four threshold mechanics that recur in pharmaceutical royalty agreements, explains the economic compression each produces, and traces how the threshold structure propagates through accounting, tax, security, and insolvency layers. The treatment assumes familiarity with the underlying synthetic royalty toolkit and the insolvency architecture that sits on top of it.

What a No-Royalty Threshold Is, and What It Is Not

A no-royalty threshold is a structural floor on payment obligations. The seller pays nothing on the first dollar of net sales, the first month after launch, or the first dollar of an underperforming year, depending on how the threshold is drafted.

It is not the same as a cap multiple, which terminates payments at the upper end. It is not the same as a minimum annual royalty (MAR), which is the inverse: a guaranteed floor for the buyer rather than the seller. And it is not the same as a milestone payment, which is event-triggered and paid in a lump sum rather than computed against a running net-sales base.

The economic question that a threshold answers is which party bears the risk of the launch ramp, the demand curve, and the patent cliff. A threshold shifts that risk toward the buyer in the early period and toward the seller in the late period. The negotiation almost always pairs the threshold with a compensating term: a higher rate above the threshold, an extended royalty term, a step-up tier in later years, or a buyer-protective cap multiple.

The Four Threshold Mechanics

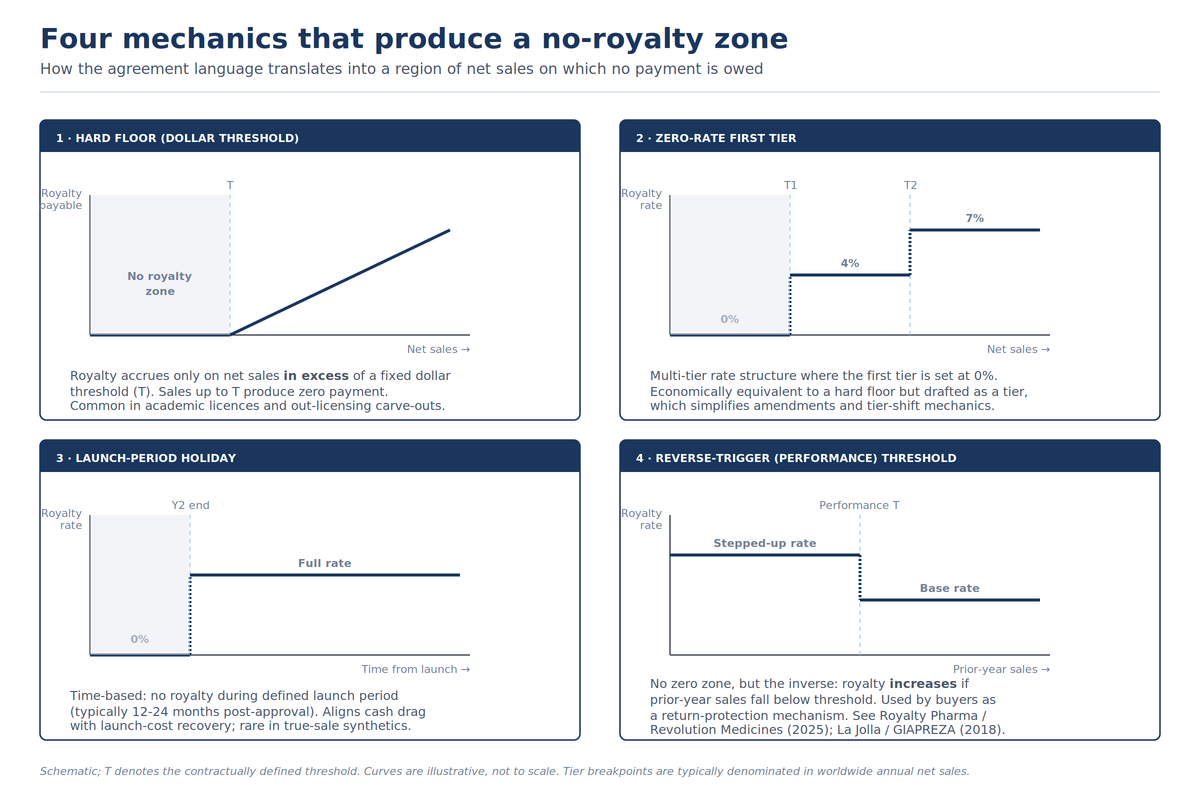

1. Hard Floor (Dollar Threshold)

The cleanest construction. The agreement specifies a fixed annual or cumulative net sales figure, and royalty accrues only on net sales in excess of that figure. The drafting is straightforward: "Royalty shall be payable at X% of Net Sales in excess of USD T per Calendar Year."

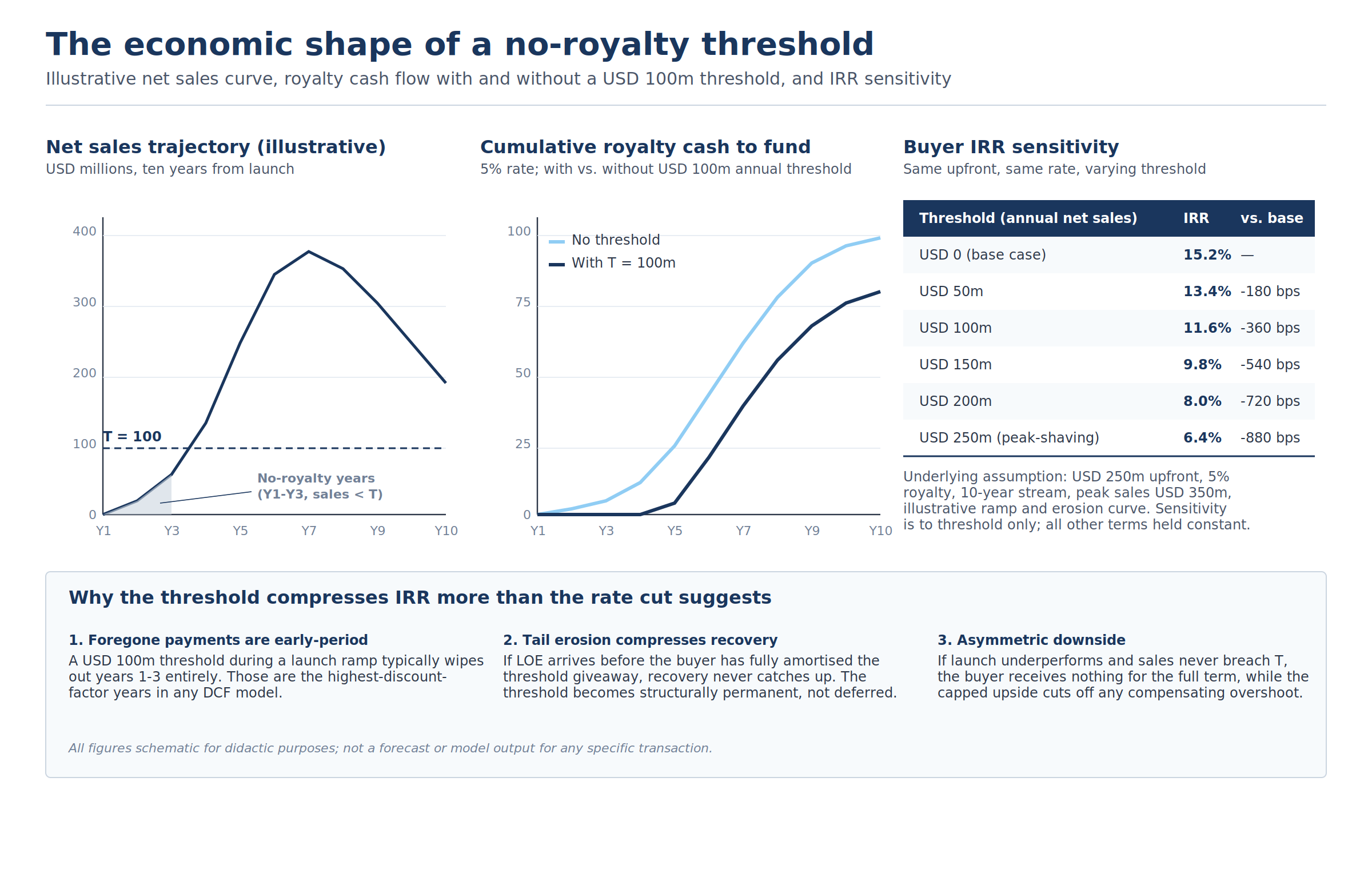

Hard floors are the dominant form in academic out-licensing. They serve a practical function: the licensor needs the licensee to commit resources to commercialisation but accepts that early-stage marketing costs and prescriber adoption curves make the first dollars uneconomic. The licensor takes nothing until the asset has cleared a commercial-viability bar. The Biovest / Accentia royalty agreement is a public example: the next royalty payment becomes due only once aggregate net sales exceed a defined dollar figure following an advance payment.

In synthetic royalty financings the hard floor is rarer but appears in launch-stage deals where the buyer is willing to forgo near-term cash for a higher post-threshold rate.

2. Zero-Rate First Tier

Functionally identical to the hard floor, but drafted as the first band of a tiered rate schedule. A tier table that reads "0% on Net Sales of USD 0 to 100m; 4% on Net Sales of USD 100m to 250m; 7% on Net Sales above USD 250m" produces the same cash flow as a hard floor at USD 100m paired with a 4% / 7% step-up.

The drafting choice between a hard floor and a zero-rate first tier is mostly aesthetic, but it has three operational consequences. First, amendments are easier within a tier table because the parties can shift breakpoints without reopening the floor concept. Second, accounting disclosure under ASC 606 / IFRS 15 is cleaner because a tier is presented as a single variable consideration schedule rather than a separate floor covenant.

Third, regulatory filings and licence summaries (10-K, 20-F, prospectus) treat tier tables as a familiar disclosure format, while standalone floor language tends to attract investor questions.

Gibson Dunn's 2026 Royalty Finance Market Update finds that tiered rate structures appear in 73% of synthetic royalty financings between 2020 and 2024. The lowest tier is usually a positive but small percentage rather than zero, but the zero-tier variant is contractually identical to a hard floor and shows up wherever the seller has the leverage to push for one.

3. Launch-Period Holiday

A time-based threshold rather than a sales-based one. The agreement specifies that no royalty is payable for a defined number of months or quarters after first commercial sale, regardless of sales performance.

Launch holidays are most common where the buyer is funding launch costs directly (a development financing or hybrid structure) and accepts a deferred payment schedule that aligns with the seller's expected cash recovery curve.

They are less common in pure true-sale synthetics because they are difficult to reconcile with a fully-transferred property interest: if the buyer "owns" a royalty stream, but is contractually denied any payment for two years, the substance of the transaction starts to look like deferred consideration on a loan rather than a sale of an asset.

Where launch holidays do appear in synthetic deals, they are typically capped at 12 to 24 months and paired with a cap multiple that compensates the buyer for the lost cash flow at the end of the deal life.

4. Reverse-Trigger (Performance) Threshold

Not a no-royalty zone, but the inverse: a sales-based threshold below which the royalty rate increases rather than decreases. The buyer is protected against underperformance by an automatic escalation in the rate if prior-year net sales fall short of an agreed figure.

The cleanest contemporary example is the June 2025 Royalty Pharma / Revolution Medicines synthetic royalty on daraxonrasib. The deal includes tiered royalty rates of 2.55% / 1.50% / 0.60% on annual sales bands of USD 0-2bn / USD 2-4bn / USD 4-8bn. Crucially, the agreement specifies that the royalty rate on annual sales of USD 0 to 2 billion may increase from 2030 to 2041 if sales in the immediate prior year fall below an agreed-upon threshold.

The mechanism functions as a backstop on Royalty Pharma's IRR: if commercial uptake disappoints, the rate ratchets up to compensate.

The 2018 La Jolla / GIAPREZA financing with HealthCare Royalty used a calendar-based version of the same concept: each royalty tier increases by 4% if HCR has not received aggregate royalties equal to at least 50% of the investment amount by January 1, 2022, and by another 4% if not 100% by January 1, 2024. The structure converts a sales-performance shortfall into a rate adjustment that preserves the buyer's modelled return.

Reverse-trigger thresholds are the most legally complex of the four mechanics because the conditional rate change creates a contingent payment obligation. The accounting and tax characterisation analyses are correspondingly more involved, and pre-petition amendments waiving or modifying the trigger have become a contested issue in biotech bankruptcies (see below).

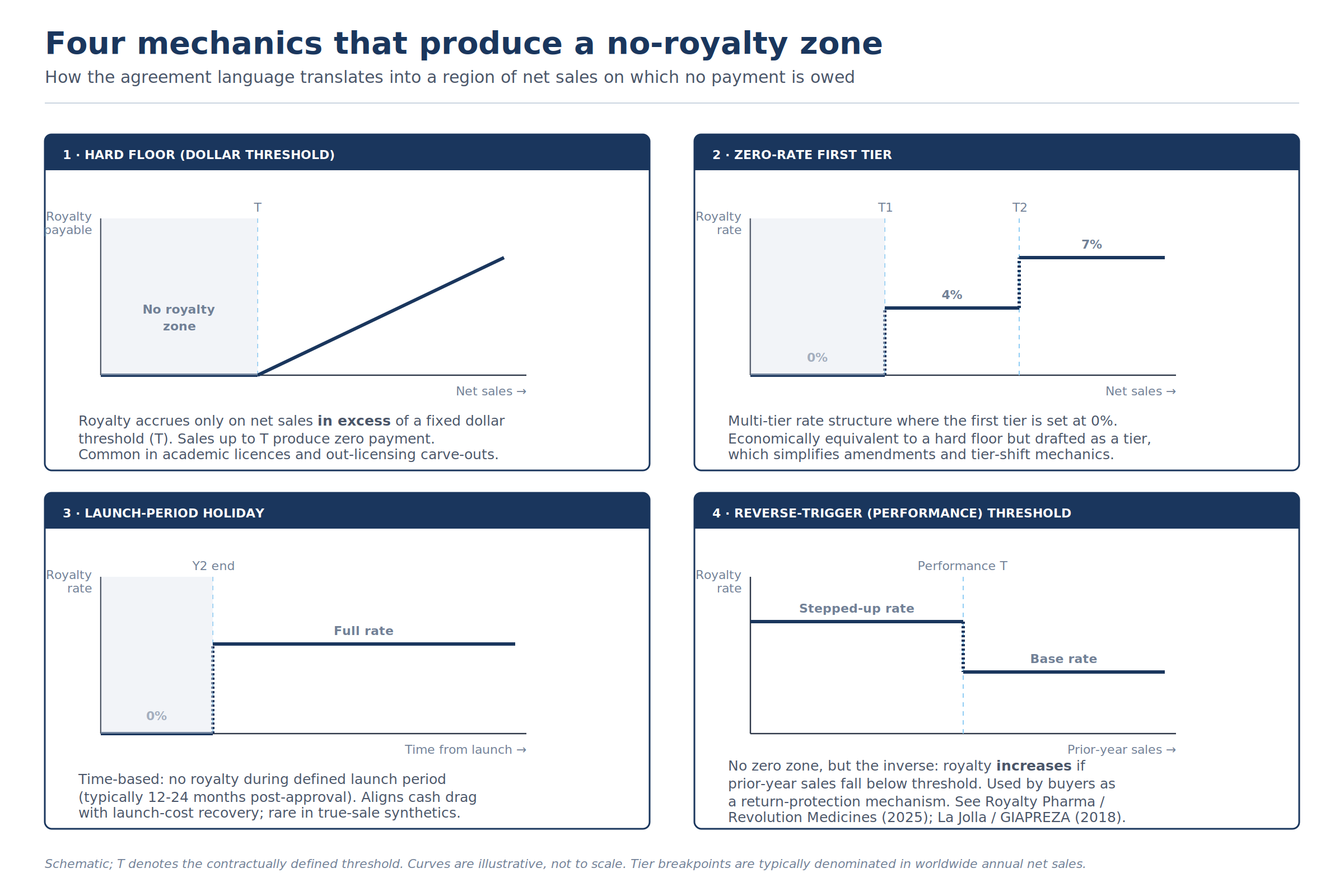

The Economics: Why a Modest-Looking Threshold Compresses Returns Sharply

The mechanical effect of a threshold is straightforward to state and easy to underestimate. The illustrative numbers above hold the upfront investment, royalty rate, term, and underlying sales curve constant, and vary only the threshold. A USD 100m annual threshold compresses buyer IRR by roughly 360 basis points relative to an otherwise identical unfloored deal. A USD 200m threshold compresses it by 720 basis points.

Three structural features explain why the IRR compression is larger than the rate-equivalent intuition would suggest.

The first is that foregone payments are concentrated in the early years of the deal. A launch-stage product hitting USD 100m in net sales typically does so in years one through three. Those years carry the highest discount factors in any DCF. A threshold that wipes out years one through three is not equivalent to a 30% rate cut applied across the term; it is equivalent to a much steeper cut applied to the most valuable years.

The second is that tail erosion compresses the recovery period. If loss of exclusivity (LOE) arrives before the buyer has fully amortised the threshold giveaway, the recovery never catches up. The threshold becomes structurally permanent rather than economically deferred. For products with defined patent expiries 7 to 10 years out from launch, this is a genuine concern: the period after threshold breach but before LOE may be shorter than the threshold-period itself.

The third is asymmetric downside. If the launch underperforms and net sales never breach the threshold, the buyer receives nothing for the full term while the cap multiple, if present, cuts off any compensating overshoot in the rare scenario where the product later catches fire. The expected-value distribution is left-skewed in ways that the headline royalty rate does not communicate.

For the seller, the economic logic runs in reverse. The threshold preserves operating cash during the period when burn rate is highest and product contribution margin is lowest. A USD 100m threshold during launch typically buys 24 to 36 months of unencumbered cash flow that the seller can deploy against launch infrastructure, salesforce build-out, and second-indication development. The effective cost of capital during the threshold period is zero. The trade-off is post-threshold: the seller pays a higher rate, a longer term, or a higher cap to fund the early-period relief.

Drafting Considerations: Where the Threshold Language Goes Wrong

Threshold language fails in production for predictable reasons. Five drafting traps recur in disputes and in licence amendment workouts:

Net sales definition drift. A threshold expressed in "Net Sales" inherits all of the deductions, allowances, and adjustments built into that defined term. Aggressive deductions for distribution costs, freight, government rebates, and 340B chargebacks can push reported net sales below the threshold even when gross sales materially exceed it. The buyer typically negotiates a list of capped or excluded deductions; the seller pushes for a broad inclusion.

The Court of Appeal's 2024 ruling in the Tesaro / Janssen niraparib licence dispute is a recent reminder that ambiguity over what net sales include is a litigation magnet.

Annual versus cumulative calculation. A threshold drafted as an annual figure resets each calendar year. A threshold drafted as cumulative is breached once and stays breached. The economic and accounting consequences differ materially. A USD 500m cumulative threshold breached in year three produces full-rate royalty for the rest of the term. A USD 100m annual threshold can produce alternating zero-and-full years if sales hover near the threshold or decline post-LOE.

Combination products and bundled discounts. Where the licensed product is sold as part of a combination or kit, the threshold calculation must specify whether the entire bundle counts toward the threshold or only the portion attributable to the licensed component. The default approach is to allocate net sales pro-rata by reference to standalone selling price, but disputes over whether such a price exists, or whether the allocation methodology is faithful to the parties' intent, are a frequent source of audit findings.

Currency conversion and hedging. A threshold denominated in USD applied to net sales in EUR, JPY, or CHF requires a conversion methodology. Spot rate at end of quarter, average rate over the quarter, and rate at the date of invoice all produce materially different threshold breach dates in volatile currency periods. The agreement should specify, and the calculation should be auditable.

Successor liability on M&A. A threshold that resets on change of control, or that survives but is recalculated at the time of acquisition, can dramatically alter the economics of a buy-side transaction involving the seller. Buyers in pharma M&A regularly underwrite threshold-bearing royalty obligations as if they were full-rate from day one to be conservative. Sellers seeking acquisition value want the threshold to survive intact.

Accounting and Tax Implications

The accounting treatment of threshold-bearing royalty agreements is governed by ASC 606-10-55-65 (and the parallel IFRS 15 guidance) for licensors, and by general variable consideration principles for buyers and licensees.

The sales-based royalty exception defers revenue recognition until the underlying sales occur, which means a licensor with a threshold-burdened royalty does not estimate or recognise revenue in advance of threshold breach.

The wrinkle is that any "minimum guarantee" component, a payment owed regardless of whether sales reach the threshold, falls outside the exception and must be accounted for separately. PwC's guidance on minimum royalties (RR 9.8.3) treats minimum guarantees as fixed consideration that is recognised over the licence period rather than as variable consideration tied to sales.

For reverse-trigger structures, the analysis is more involved. The contingent rate increase is variable consideration that depends on a future sales performance condition. The licensor must estimate the expected rate using either the expected value or most likely amount method under ASC 606-10-32-8, subject to the variable consideration constraint that requires highly probable revenue not to be recognised until reasonably assured.

The tax characterisation question runs in parallel. A threshold strengthens the true-sale narrative for synthetic royalty financings because it demonstrates that payment is genuinely contingent on commercial performance, not a fixed obligation in disguise. But the same feature, if too extensive, can push the analysis toward equity-like treatment.

The 2022 PhaseBio / SFJ Pharmaceuticals recharacterisation challenge illustrated the failure mode: a five-times-return structure with payment fully contingent on FDA approval and commercial sales was argued by the debtor to be equity, not debt or sale. The dispute settled through mediation, but the underlying tension between threshold-driven contingency and sale characterisation remains unresolved in case law.

For cross-border transactions, the substance-over-form analysis differs by jurisdiction. Swiss, French, and German tax authorities typically place greater weight on economic substance than US authorities, and a threshold structure that materially defers payment to the back end of the deal life can attract scrutiny on whether the upfront has been correctly characterised.

The Insolvency Layer: Where Thresholds Become Litigation Risk

Threshold mechanics interact with insolvency law in three operational ways that have become contested in recent biotech bankruptcies.

Pre-petition amendments to thresholds. When a seller anticipates insolvency, it may seek to renegotiate threshold terms, often to access cash relief in exchange for buyer-favourable amendments elsewhere in the agreement. The November 2025 Clearside Biomedical Chapter 11 brought this dynamic to the surface. An ad hoc group of equity holders alleged that a September 2025 amendment to Clearside's royalty agreement with HealthCare Royalty Partners had waived a contingent USD 12.5 million payment, nearly five times the stalking horse bid for the company's entire asset base.

The dispute centres on whether the amendment was a fraudulent transfer or a legitimate workout. The structural lesson is that amendments to threshold mechanics, made when the seller is in the zone of insolvency, become flashpoints for fiduciary duty and avoidance challenges.

Avoidance and preference exposure. Threshold-period payments are zero by construction, which means there is no payment within the typical 90-day or one-year preference look-back window for the bankruptcy trustee to claw back. This is a structural advantage of threshold-bearing deals: the buyer's collateral is a contingent receivable rather than a stream of recently-received payments, and the avoidance attack surface is correspondingly narrower.

The trade-off is that the buyer's UCC-1 is attached to a receivable that has zero realisable value until the threshold is breached, which complicates collateral valuation in a stress scenario.

Section 365(n) and the executory contract analysis. Where the underlying transaction is structured as an IP licence, Section 365(n) of the Bankruptcy Code allows the licensee to retain its rights even if the debtor-licensor rejects the contract. The threshold structure does not directly affect the 365(n) analysis: the licensee continues to owe royalties (above the threshold) under the rejected contract if it elects to retain the licence.

But the threshold can affect the economic decision to elect, because the value of retention depends in part on whether the licensee expects to clear the threshold at all in the post-rejection period.

Reverse-trigger litigation risk. Reverse-trigger thresholds introduce a contingent claim that may crystallise post-petition. If the trigger condition (a sales shortfall) materialises after the petition date, the question is whether the resulting rate step-up creates a pre-petition or post-petition claim.

The analysis turns on when the underlying obligation arose and whether the trigger event was predictable at petition. Courts have not settled this question for the specific case of a sales-performance trigger, and parties drafting reverse triggers should specify the treatment of the trigger event in insolvency to avoid post-hoc disputes.

For an asset-class view of how these dynamics interact with the broader insolvency architecture, see Insolvency Liens in Pharma Royalty Transactions. The threshold layer sits on top of the lien, true-sale, and Section 365(n) protections discussed there, and it inherits all of their strengths and limitations.

What This Means for Funds and Companies

For royalty funds and dedicated buyers, threshold structures are increasingly difficult to avoid. Goodwin's October 2025 market update reports that 90% of biotech executives surveyed are considering a royalty financing within the next three years, and the seller-side bargaining posture has strengthened materially. Tiered structures, capped multiples, and threshold mechanics are now standard rather than exceptional.

The buyer's protection against the resulting IRR compression is to negotiate a higher post-threshold rate, a longer royalty term, a more favourable cap multiple, or a reverse-trigger backstop. The 2025 Royalty Pharma / Revolution Medicines structure shows what an institutional buyer looks like after fully internalising this trade-off: 2.55% on the first USD 2bn tier, with a contingent step-up if performance falls short of plan.

For biotech sellers and their advisors, the threshold is one of the most leveraged terms in the negotiation. A USD 100m annual threshold during a 24-month launch ramp is worth 200 to 400 basis points of effective cost of capital relative to the unfloored alternative.

Sellers who frame the threshold negotiation in those terms, rather than as a defensive concession, recover meaningful value. The threshold also has accounting and tax benefits that can be material for public companies managing earnings volatility around launch.

For lawyers drafting the agreement, the threshold language should be specified with the same precision as the cap multiple and the rate. Net sales definition, annual versus cumulative calculation, currency conversion, combination product allocation, and successor liability on M&A all need to be unambiguous on the face of the contract.

Threshold disputes are not common in litigation, but when they occur they tend to be sized to the full life of the deal, and the cost of ambiguity is large. The Tesaro / Janssen precedent in patent royalty drafting is a useful reminder of what the cost looks like when the language is ambiguous and the stakes are high.

Two Provisions to Watch

Two threshold-adjacent provisions are worth tracking through 2026 and 2027.

The first is the interaction between threshold mechanics and US drug pricing reform. The Inflation Reduction Act's price negotiation provisions, combined with potential most-favoured-nation pricing rules, will compress net realised prices in a meaningful subset of products. A threshold denominated in dollar net sales becomes harder to breach when the underlying price is administratively reduced. Royalty agreements drafted before pricing reform may produce no-royalty zones that were never intended at the negotiation stage.

Sellers and buyers signing today should consider whether the threshold should adjust for material price reform events, and whether the calculation should reference gross-to-net deductions in a way that reflects the pre-reform commercial environment.

The second is the European harmonisation of insolvency rules. The November 2025 EU directive on harmonised pre-pack and avoidance provisions will reach implementation in member states over the coming years.

For threshold-bearing royalty agreements with EU-domiciled counterparties, the harmonised avoidance regime will affect how pre-petition threshold amendments are reviewed, and the pre-pack provisions may allow threshold-burdened products to be sold quickly in distress with the threshold structure intact (or, depending on the buyer's preference, restructured at sale). Royalty investors with EU exposure should be modelling the directive's effect on their existing portfolios.

All information in this article was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, court decisions, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.