Fund of the week: High-Tech Gründerfonds

What is High-Tech Gründerfonds?

High-Tech Gründerfonds (HTGF) is Germany's largest and most active seed-stage venture investor. It is a public-private partnership, founded in 2005 in Bonn to close the early-stage funding gap that once left many German university and research spin-outs without a first institutional cheque.

Two decades later it has financed roughly 800 start-ups, manages over €2 billion across all of its funds, and sits upstream of almost every German deep-tech and life-science success story of the period.

Its relevance to royalty and structured-finance professionals is therefore indirect. It originates and seed-finances the German biotech companies that, years later, sign the licence agreements and reach the commercial inflection points that royalty buyers and specialty lenders actually transact around.

Three of those companies have produced billion-euro exits: MYR to Gilead, Cardior to Novo Nordisk, and Tubulis to Gilead again. The licence agreements embedded inside the Tubulis story are a textbook example of how a royalty stack accrues to everyone except the seed investor that made the company possible.

This piece focuses on HTGF specifically: its mandate and capital structure, its position in the German ecosystem, its typical ticket sizes, its life-science portfolio, the equity-mediated royalty economics that sit beneath it, its leadership, a blue-team and red-team assessment, and what it all means for the commercial royalty markets.

Overview and position

HTGF was created through a German federal government mandate, initiated by what is today the Federal Ministry for Economic Affairs and Climate Action. The aim was to revive seed financing for technology start-ups after the early-2000s downturn had largely emptied the German early-stage market.

The structure chosen was a public-private partnership. The federal government and KfW Capital, the state-owned promotional bank's investment arm, provide the anchor capital, and a rotating group of around 45 German corporates contribute the rest as limited partners.

BASF has invested in every fund generation and participates in the investment committees. Other corporate backers across the generations include SAP, QIAGEN, RWE, STIHL, Phoenix Contact, Vector Informatik, Wacker Chemie, and the Schwarz Gruppe.

That structure gives HTGF a distinctive position. It is simultaneously a policy instrument of German innovation strategy and a commercially run venture investor, operating at a scale and consistency that no purely private German seed fund matches.

Across its history it has supported around 800 companies and recorded somewhere between 170 and 200 realisations. External investors have poured well over €5 billion into its portfolio through more than 2,400 follow-on rounds.

Its mandate spans three sectors, restructured in 2025 into clearly delineated pillars: Life Sciences and Chemistry, Industrial and Deep Tech (including climate tech), and Digital Tech. For the purposes of this publication, the Life Sciences and Chemistry pillar is the relevant one, and it has been, by capital outcome, the most consequential of the three.

Capital structure and the funds

HTGF has raised four seed-fund generations and, in 2024, added a later-stage growth vehicle. The seed funds are the heart of the franchise; the Opportunity Fund is the recent and strategically significant addition.

| Fund | Vintage | Approx. volume | Notes |

|---|---|---|---|

| HTGF I | 2005 | ~€272M | First public-private seed fund; rebuilt the German seed market |

| HTGF II | 2011 | ~€304M | Expanded corporate LP base |

| HTGF III | 2018 | ~€320M | Broader sector mandate |

| HTGF IV | Final close Feb 2023 | €493.8M | Largest generation to date; BMWK, KfW Capital, and 45 corporates as LPs |

| Opportunity Fund | June 2024 | €660M | Later-stage follow-on into existing portfolio; from the Future Fund and ERP Special Fund |

| Matching Fund | Nov 2025 | ~€25M | Lets corporate seed-fund LPs co-invest in later-stage rounds |

The four seed funds together account for roughly €1.4 billion under management.

The 2024 launch of the €660 million Opportunity Fund was a deliberate response to a structural weakness in the German market. Growth-stage rounds in Germany are disproportionately filled by American and other foreign capital, and a seed investor that could not follow its winners into Series B and C was leaving both returns and influence on the table.

Drawn from Germany's Future Fund and the ERP Special Fund, and run by chief investment officers Ulrich Schmitt and Anke Caßing, the Opportunity Fund lets HTGF write growth cheques of up to €30 million, and in exceptional cases up to €50 million, always alongside private co-investors.

The November 2025 Matching Fund extended that later-stage access to the corporate LPs of the seed funds. This later-stage capability matters directly to the life-science thesis, as the Tubulis case below demonstrates.

Typical ticket size and investment parameters

HTGF's first cheque is small by design. The stated sweet spot for an initial pre-seed or seed investment is €800,000 and upward, with around €1 million a common round number.

The fund frequently leads or co-leads at that stage while assembling a syndicate of national and international co-investors. Over its history the average seed round it participates in has run in the low single-digit millions of dollars, with follow-on Series A participations averaging in the high single digits.

Eligibility is narrow in two respects worth flagging. A company must generally be no more than three years old at the time of the first investment, and it must have a clear connection to the German market.

Both constraints follow from the fund's origin as a German innovation-policy instrument, and both shape, and limit, the portfolio in ways the red-team section returns to.

The Opportunity Fund changes the upper bound. Where HTGF once topped out at modest follow-on participations, it can now deploy up to €30 million, or €50 million in exceptional cases, into a portfolio company's growth rounds. Its largest single growth investment to date was made through this vehicle into the 2025 Tubulis Series C.

Royalty and strategic income positions

HTGF invests through equity. It holds no pharmaceutical royalty interests, issues no royalty-backed debt, and earns no ongoing royalty income on the products its companies develop.

This is the same structural distinction that separates a venture investor from a dedicated royalty buyer such as Royalty Pharma, HealthCare Royalty, or DRI Healthcare. Those firms purchase royalty streams directly, whereas HTGF's exposure to any royalty economics is entirely mediated by its shareholding in companies whose own licence agreements happen to carry royalty terms.

That equity-mediated exposure is nonetheless real, and one HTGF portfolio company illustrates the mechanics with unusual clarity.

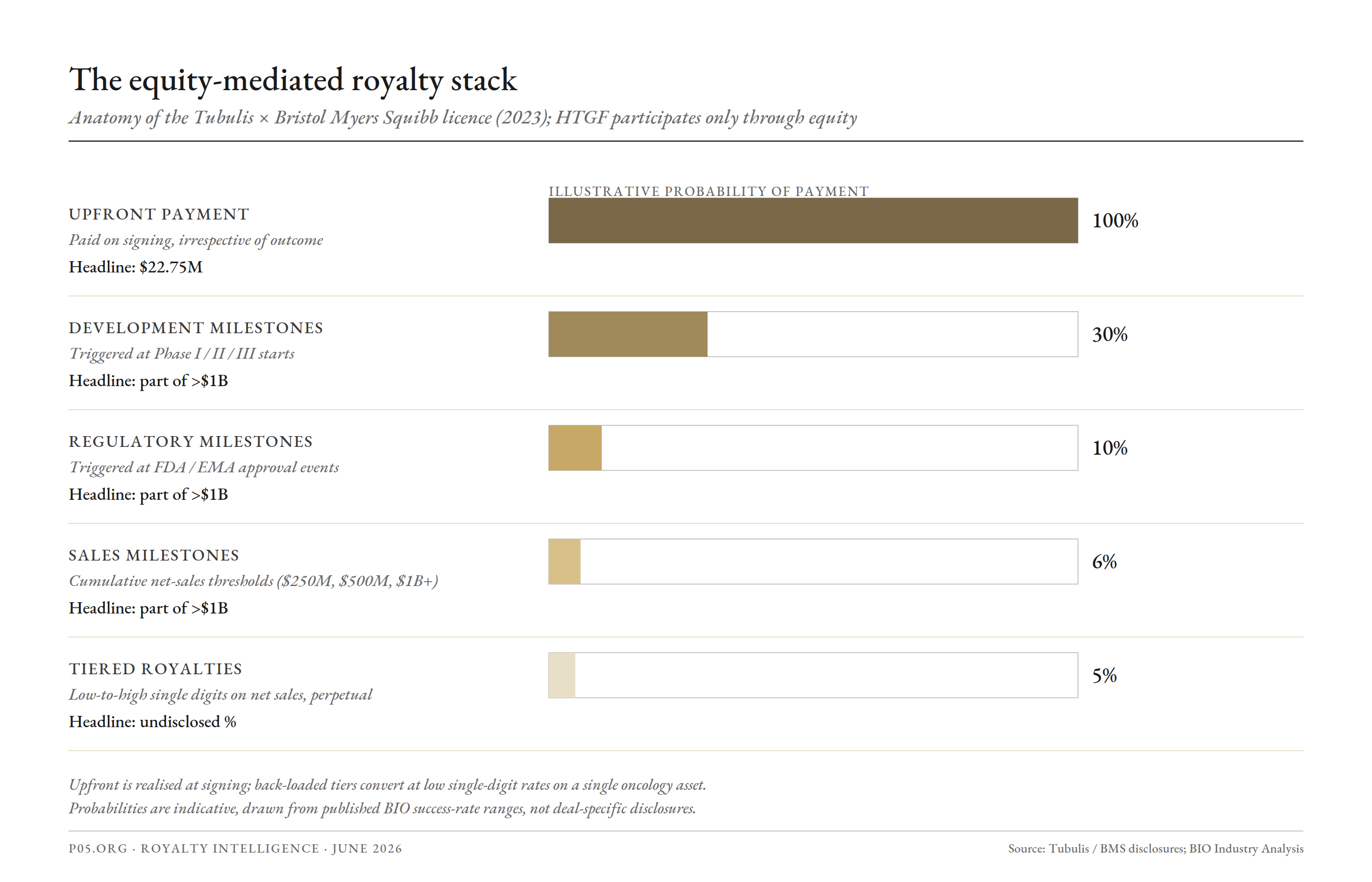

The Tubulis royalty stack: anatomy of an equity-mediated agreement

In April 2023, Tubulis, the Munich antibody-drug conjugate company that HTGF had co-led at Series A in 2020, signed a strategic licence agreement with Bristol Myers Squibb.

The published terms are a clean example of the standard pharmaceutical royalty stack: an upfront payment of $22.75 million, development, regulatory, and commercial milestones potentially totalling more than $1 billion, and tiered royalties on net sales of any resulting product.

BMS took rights to apply Tubulis's P5 conjugation and Tubutecan payload platforms to its own antibody targets, and assumed sole responsibility for development, manufacturing, and commercialisation. The first program from the collaboration entered clinical development in May 2025, triggering a milestone.

The architecture has five economic tiers, and they convert to cash at radically different rates. The upfront is realised on signing, with certainty.

Development milestones depend on the partner choosing to advance the asset through successive trial phases. Regulatory milestones depend on approval. Sales milestones depend on commercial penetration crossing contractual thresholds. And the royalty itself, though perpetual once it begins, depends on the product reaching market at all.

Applying the kind of probability-of-success ranges that BIO Industry Analysis publishes for oncology assets, the back-loaded tiers of a single-asset deal like this convert at low single-digit rates against their headline. The headline "over $1 billion" is a measure of theoretical maximum value, not of expected cash.

A second Tubulis agreement, a 2024 collaboration with Gilead, followed the same shape: roughly $20 million upfront against up to $415 million in milestones.

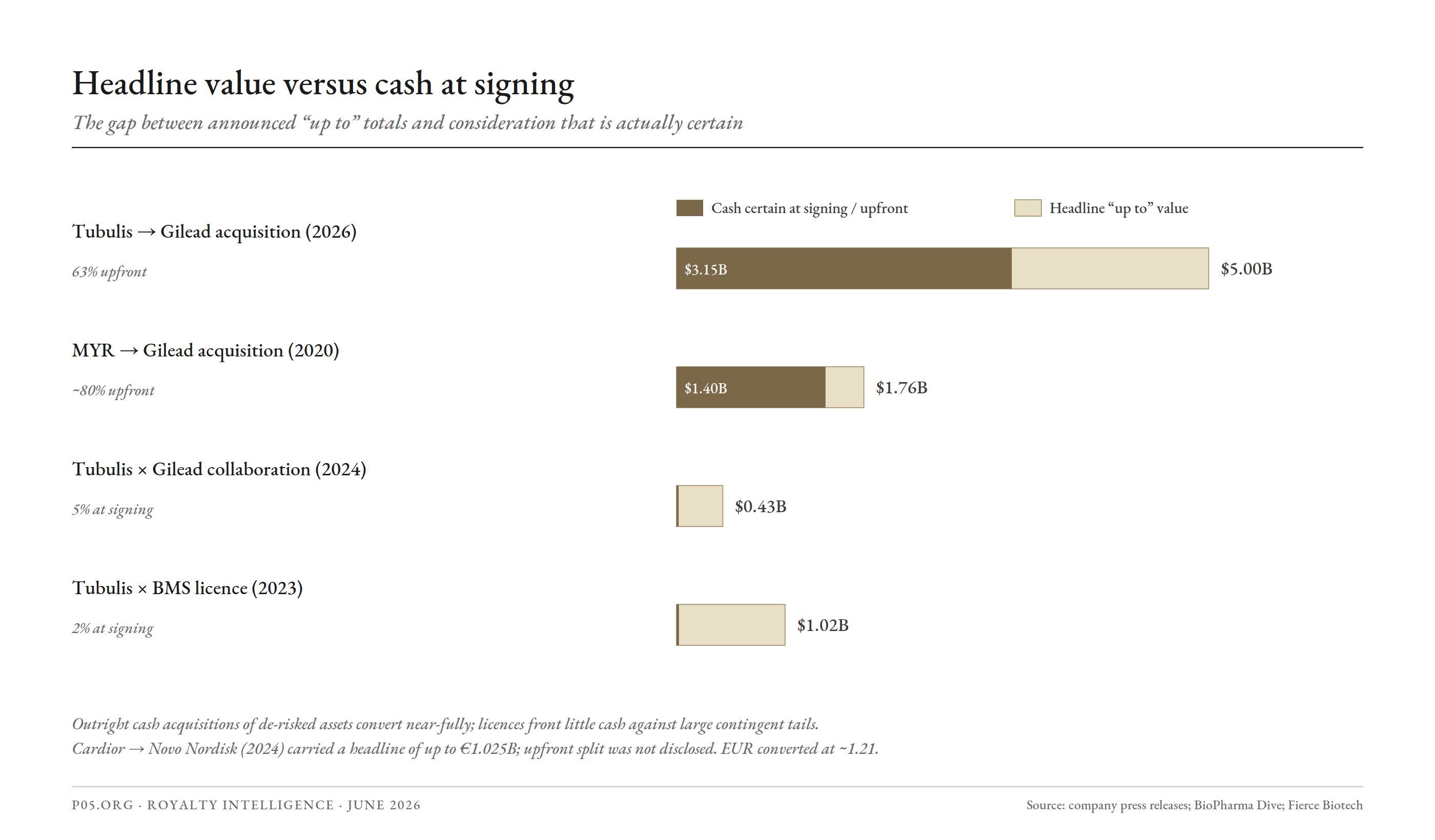

Headline value versus cash at signing

The gap between announced "up to" totals and consideration that is actually certain is the single most important number to internalise when reading any of HTGF's life-science outcomes.

The pattern is consistent. Outright cash acquisitions of de-risked assets convert near-fully: Gilead's 2020 purchase of MYR was structured as cash, and even the 2026 Tubulis acquisition front-loads 63 percent of its $5 billion as upfront cash.

Licence and collaboration agreements behave in the opposite way, fronting a small fraction of headline value against a large contingent tail. The Tubulis–BMS licence put roughly 2 percent of its headline in hand at signing; the Gilead collaboration roughly 5 percent.

This is precisely why dedicated royalty buyers prefer streams on already-approved products, where commercial uncertainty has largely resolved, over milestone streams on assets still in the clinic.

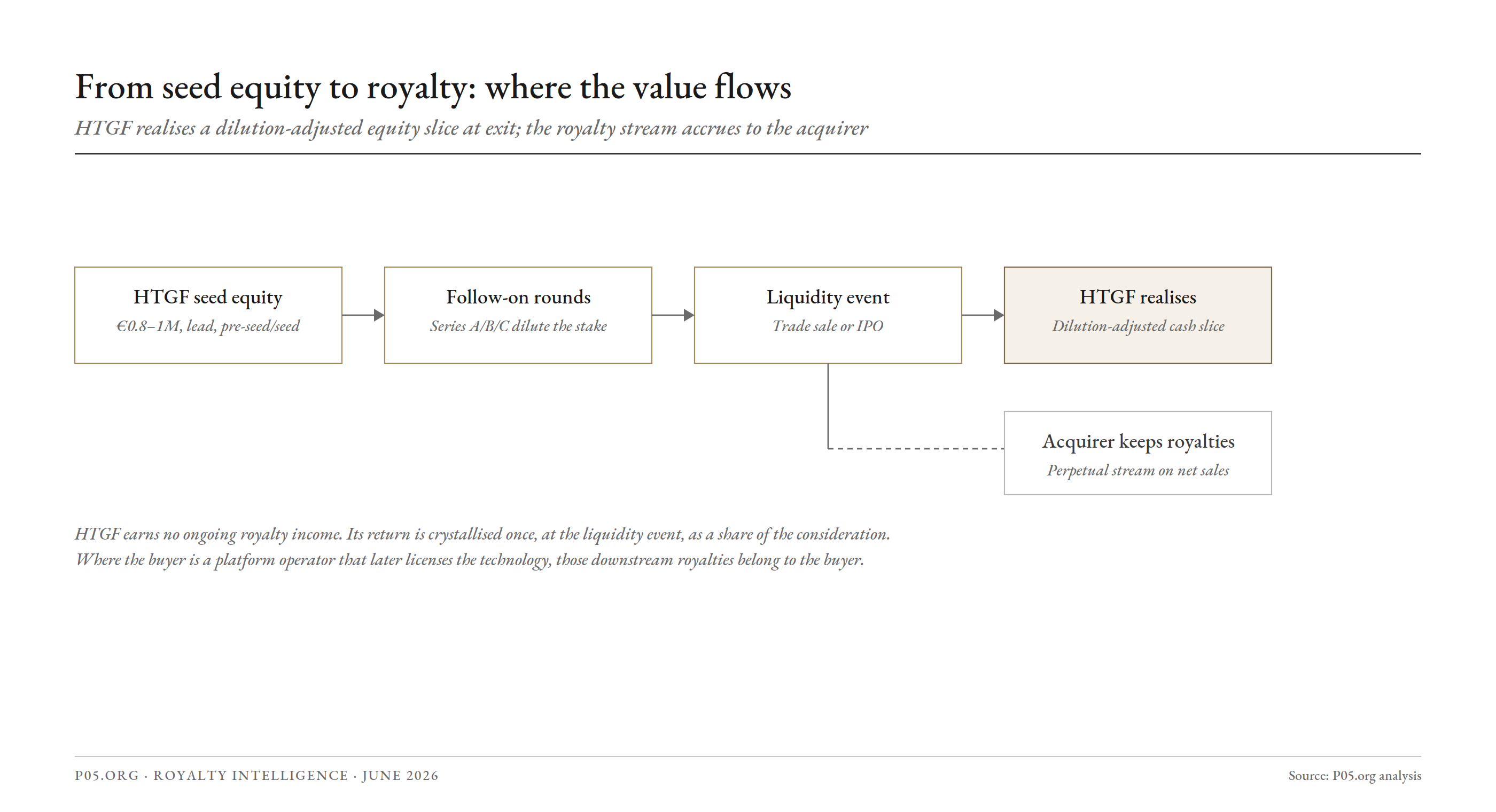

Where the value flows

The final point is the one most often missed. HTGF captures value from these royalty-bearing agreements only through its equity, and only once, at a liquidity event.

HTGF's seed stake dilutes through every subsequent financing round, so by the time a company is acquired its ownership is a fraction of what it held at Series A. It then realises a dilution-adjusted slice of the acquisition consideration in cash. It does not retain any claim on the royalty stream.

Worse, where the acquirer is a platform operator that goes on to license the underlying technology, as Gilead now can with the Tubulis ADC platforms, those downstream royalty rights belong to the buyer.

The royalty stack that the seed investor helped bring into existence ends up enriching the acquirer, not the originator. HTGF's economics are equity economics, crystallised at exit, and nothing more.

Life-science and biotech portfolio

HTGF's Life Sciences and Chemistry pillar covers therapeutics, platform biotech, research tools, diagnostics, medtech, and digital health. Its therapeutic outcomes have been concentrated in a small number of high-conviction names, three of which reached billion-euro headline valuations.

MYR GmbH

MYR was HTGF's first biotech unicorn. HTGF was the first institutional investor in 2011, backing a preclinical hepatitis delta virus program when few others would.

The lead asset, bulevirtide, marketed as Hepcludex, became the first and only conditionally EMA-approved therapy for chronic HDV. In December 2020 Gilead agreed to acquire MYR for approximately €1.15 billion in cash plus up to €300 million in milestones, an aggregate of up to €1.45 billion.

It remains one of the largest trade sales of a venture-backed German biotech in the past two decades. Notably, it was an acquisition of an approved, revenue-generating product, the category a royalty buyer would find most legible.

Cardior Pharmaceuticals

Cardior, a Hannover RNA-therapeutics company built on research from Hannover Medical School and the Max Planck Institute, took HTGF capital in its first financing round in 2017.

Its lead compound CDR132L, a non-coding RNA inhibitor targeting microRNA-132 for heart failure, reached Phase II. In March 2024 Novo Nordisk agreed to acquire Cardior for up to €1.025 billion in upfront and milestone payments, giving Novo a cardiovascular foothold to complement its cardiometabolic franchise.

Tubulis

Tubulis is the most instructive recent case, because it ties together the portfolio, the Opportunity Fund, and the royalty mechanics. HTGF engaged with the founding team before incorporation and co-led the 2020 Series A.

It followed through the company's growth, and in October 2025 made its largest-ever growth investment, via the Opportunity Growth Fund, in Tubulis's €344 million Series C, at the time the largest financing of a private ADC developer globally.

Six months later, in April 2026, Gilead agreed to acquire Tubulis for up to $5 billion, $3.15 billion upfront plus $1.85 billion in milestones, for the NaPi2b-targeting ADC TUB-040 and the 5T4-targeting TUB-030 along with the underlying conjugation platform.

The deal validated both HTGF's early conviction and its decision to build later-stage capacity that could let it hold a meaningful position into a landmark exit.

The rest of the book

Beyond the three headline outcomes, the active life-science portfolio includes Algiax Pharmaceuticals (chronic neuropathic pain, lead candidate AP-325), FundaMental Pharma (first-in-class small-molecule inhibitors for ALS and Huntington's disease, spun out of Heidelberg University), SciRhom (immunology, which closed a €63 million round), Argá Medtech, Biograil (oral drug delivery), Avelios Medical (clinical software), and Verovaccines (animal-health vaccines).

Historical life-science realisations beyond MYR and Cardior include the oncology ADC company Emergence Therapeutics, the viral-vector tools company SIRION Biotech, and the industrial-biotech firm c-LEcta.

The through-line for royalty professionals is that HTGF's therapeutic portfolio skews toward modalities, ADCs, RNA therapeutics, and platform biology, that sit at the centre of current licensing and acquisition activity.

Leadership

HTGF reorganised its management in 2025 into a sector-aligned structure, with one managing director responsible for each of the three investment pillars. The transition, completed in October 2025, also marked the departure of two long-serving leaders.

| Person | Role | Background |

|---|---|---|

| Dr Achim Plum | Managing Director, Life Sciences and Chemistry | PhD geneticist; 20+ years in life sciences (Epigenomics, Siemens, Curetis, Ares Genetics, SphingoTech, InfanDx); two IPOs; joined HTGF management 1 January 2025 |

| Romy Schnelle | Managing Director, Industrial and Deep Tech | Long-serving HTGF partner; promoted to managing director in 2023; covers industry, deep tech, and climate tech |

| Sebastian Borek | Managing Director, Digital Tech | Serial founder; founder of the Founders Foundation and Hinterland of Things; joined HTGF management 13 October 2025 |

| Ulrich Schmitt | Partner; co-CIO, Opportunity Fund | Leads later-stage growth investing |

| Anke Caßing | Principal; co-CIO, Opportunity Fund | Leads later-stage growth investing |

The arrival of Dr Plum, a life-science specialist, at the management table was a deliberate signal that the firm intends to elevate the segment that has produced its largest outcomes. He succeeded Guido Schlitzer, who left at the end of 2024.

The other significant change was the October 2025 departure of Dr Alex von Frankenberg, who had led HTGF for 20 years. His exit was long-signalled and the succession orderly, but it removed an unusually durable institutional anchor.

HTGF's team numbers around 90 to 100 people, including roughly nine partners.

Blue team: the bull case

A quasi-evergreen public mandate and counter-cyclical capital. Because HTGF is a federal innovation instrument rather than a conventional ten-year private fund, it has invested steadily through downturns that emptied private German seed markets. It can take very early, very patient positions, exactly the profile that the MYR, Cardior, and Tubulis outcomes required.

Demonstrated ability to originate billion-euro outcomes. Three life-science exits at or above €1 billion headline, to three different global acquirers, is a track record few European seed investors can match. It spans virology, cardiology, and oncology rather than a single lucky modality.

Growth capital to follow its winners. The 2024 Opportunity Fund closed the historical weakness of a seed investor that could not maintain ownership through later rounds. The Tubulis Series C, HTGF's largest-ever growth investment six months before a $5 billion exit, is the clearest proof that the new structure works as intended.

Sector specialisation at the top. The 2025 reorganisation put a life-science specialist in charge of the life-science book, aligning decision rights with domain expertise in a way the previous generalist structure did not.

Deep, proprietary German deal flow. Two decades of relationships with German universities, research institutes such as the Max Planck and Leibniz networks, and 45 corporate LPs give HTGF a sourcing advantage in German academic spin-outs that foreign funds struggle to replicate.

Red team: the bear case

Policy and budget dependency. HTGF's capital ultimately rests on German federal commitments: the Future Fund, the ERP Special Fund, and the seed-fund anchor allocations. That base has been stable, but it is exposed to fiscal politics and shifting innovation priorities in a way that a private fund's committed LP capital is not.

Thin ownership by the time of exit. A seed cheque of around €1 million, diluted across Series A, B, and C, leaves HTGF with a modest percentage of a company at acquisition. A $5 billion headline is spectacular, but the seed investor's realised return is a small slice of it, and the Opportunity Fund only partially offsets this.

The royalty upside leaks away. As the value-chain analysis shows, HTGF captures equity, not royalties. The recurring, perpetual economics its companies create through licence agreements accrue to the acquirers. For a publication focused on royalty intelligence, HTGF is structurally on the wrong side of the most durable cash flows it helps bring into existence.

Geographic and stage constraints. The under-three-years and German-market eligibility rules concentrate the portfolio in a single national ecosystem and the earliest stage. That limits diversification and forces reliance on foreign capital to scale the winners, the very dependency the Opportunity Fund was created to reduce.

Headline-versus-realised risk runs through the whole book. Most of HTGF's disclosed life-science value is expressed in "up to" terms. Milestone-heavy structures convert at low rates, and a single clinical failure can extinguish an entire back-loaded tail.

Leadership turnover and a new growth arena. The orderly but real departures of von Frankenberg and Schlitzer removed long-tenured institutional memory. The push into later-stage growth investing also places a seed specialist into direct competition with crossover and US growth funds that dominate that segment.

Implications for the royalty and biotech capital markets

HTGF matters to commercial royalty markets as an originator and a signal node, not as a counterparty.

First, it is upstream of the assets royalty buyers eventually transact around. MYR's Hepcludex is an approved, revenue-generating product, now inside Gilead, of exactly the kind a royalty investor references. Cardior's CDR132L, if it advances under Novo Nordisk, is a candidate for the synthetic-royalty or milestone-monetisation structures that have grown rapidly in recent years.

Royalty teams tracking which German and European assets are approaching commercial inflection will find HTGF's life-science exits a useful leading indicator.

Second, HTGF's portfolio composition signals where future licensing activity is likely to cluster. Its concentration in ADCs (Tubulis, Emergence) and RNA therapeutics (Cardior) maps directly onto the modalities attracting the heaviest pharma licensing and acquisition interest, and therefore the heaviest royalty-stack creation.

Third, the Tubulis story is a compact lesson in royalty economics. A seed-stage equity investor can help create more than a billion dollars of headline royalty-bearing licence value and still capture none of the royalty itself, because the stream attaches to the company and then to its acquirer.

The distinction between owning equity in a company that earns royalties and owning the royalty directly is the entire reason dedicated royalty funds exist.

Recent developments (2025–2026)

| Date | Event |

|---|---|

| June 2024 | €660M Opportunity Fund launched for later-stage follow-on investing |

| 1 January 2025 | Dr Achim Plum joins management as life-science lead, succeeding Guido Schlitzer |

| Throughout 2025 | Roughly 52 investments completed across all sectors |

| October 2025 | Tubulis closes €344M Series C; HTGF makes its largest-ever growth investment via the Opportunity Growth Fund |

| 12 October 2025 | Dr Alex von Frankenberg departs after 20 years |

| 13 October 2025 | Sebastian Borek completes the new sector-aligned management team as Digital Tech lead |

| November 2025 | ~€25M Matching Fund launched for corporate LP co-investment in later-stage rounds |

| April 2026 | Gilead agrees to acquire portfolio company Tubulis for up to $5 billion |

| Q2 2026 | Tubulis acquisition expected to close; HTGF in active deployment, ~27 investments year-to-date by May |

As of June 2026, HTGF is in active deployment, has completed its leadership transition, and is realising the payoff from its earliest life-science convictions while building the growth-stage capacity to hold those positions longer.

Conclusion

High-Tech Gründerfonds is the most important seed investor in German technology, and one of the most consequential in European life sciences, despite being neither a private fund nor a royalty participant.

Its public-private structure has let it back German academic spin-outs with a patience and consistency that private seed capital could not sustain. That patience has produced three billion-euro therapeutic exits in virology, cardiology, and oncology.

The 2024 Opportunity Fund and the 2025 sector reorganisation have addressed its two longest-standing weaknesses, an inability to follow its winners and a generalist management structure. The Tubulis sequence shows both fixes working in concert.

For royalty and structured-finance professionals, the lesson is the one the value chain makes plain. HTGF originates assets that become royalty-bearing, but it captures equity, not royalties, and the durable streams it helps create flow to acquirers.

It is best read as a leading indicator of where German and European royalty-eligible assets are forming, and as a reminder that the gap between a headline licence value and realised cash is where most of the analytical work in this market actually lives.

All information in this article was accurate as of June 2026 and is derived from publicly available sources including HTGF press releases and portfolio disclosures, company announcements from Tubulis, Cardior, MYR, Gilead, Novo Nordisk, and Bristol Myers Squibb, German federal communications, Tracxn and PitchBook data, and financial news reporting. Probability and risk-adjustment figures are illustrative and drawn from published BIO Industry Analysis success-rate ranges, not from deal-specific disclosures. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.