The Pre-Funded Warrant: A Share That Does Not Count, Until It Does

A pre-funded warrant is a paid-up share that counts for EPS, disappears from beneficial ownership, and reappears as owned stock for tax. How the gap between the three lets a fund hold 15 percent while reporting 9.99, and where it meets royalty finance.

When Aadi Bioscience closed the equity leg of its December 2024 reinvention, it did not sell one instrument. It sold two.

Investors bought 21,592,000 shares of common stock at 2.40 dollars and, in the same subscription agreement, 20,076,500 pre-funded warrants at 2.3999 dollars, each carrying an exercise price of one hundredth of a cent. Nearly half of a 100-million-dollar raise went into an instrument that is economically a paid-up share sitting one costless keystroke from issuance, and legally is not a share at all.

The split was not a quirk of one deal. It is the standard architecture of life-science equity finance, and the reason is that the pre-funded warrant is counted three different ways by three different rulebooks.

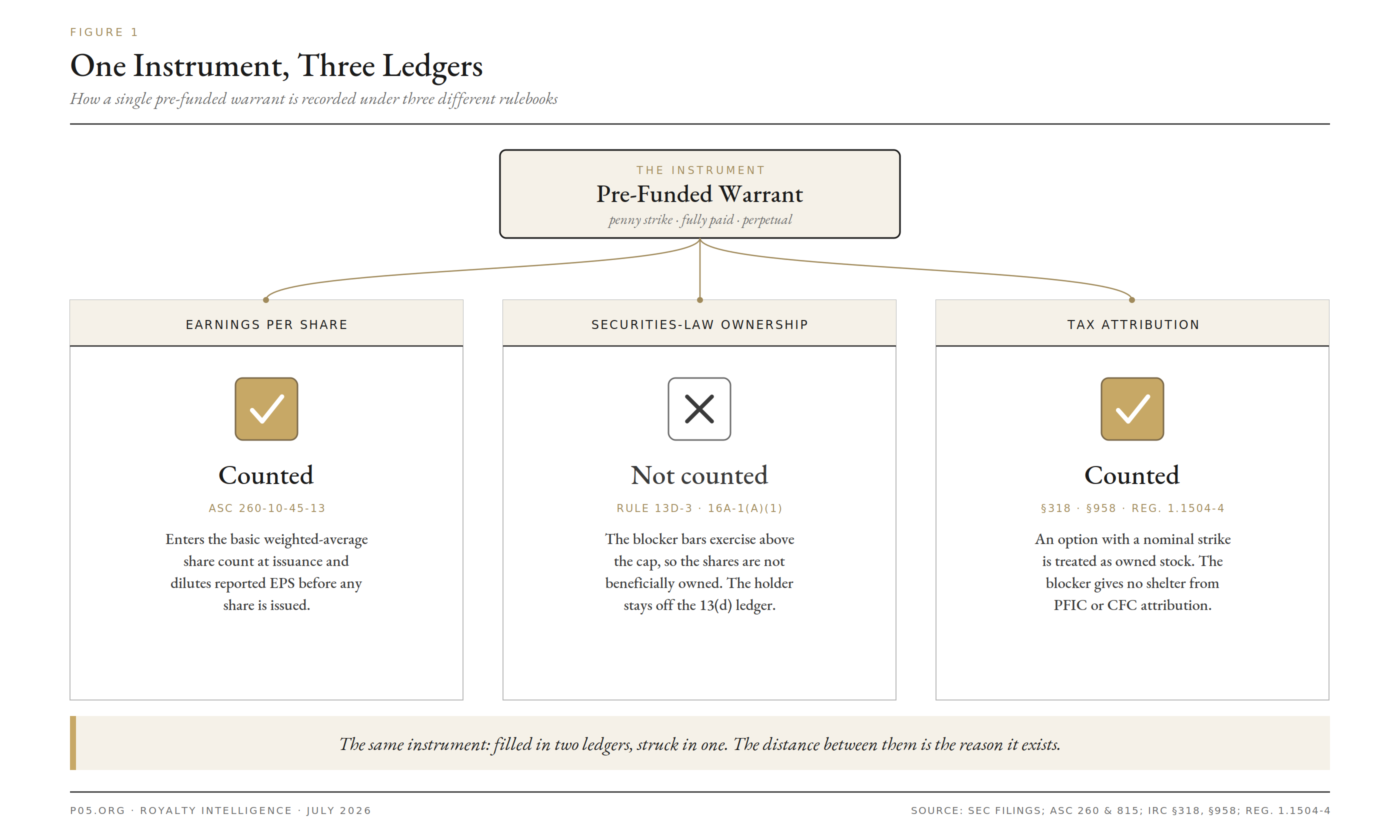

- For the earnings-per-share denominator, the underlying shares are treated as outstanding and dilute reported figures from the day the warrant is issued.

- For beneficial-ownership reporting under Section 13(d) and Section 16, the same shares are not owned at all, because a contractual blocker prevents exercise, so a holder can carry the economics of nineteen percent while disclosing four point nine nine.

- For US federal income tax, the issuer will tell you the warrant is the underlying stock, while the constructive-ownership rules treat an unexercised warrant as owned stock for attribution regardless of the securities-law blocker.

One contract, three regimes, three characterisations. The distance between them is not a technicality. It is the product.

Figure 1. The same pre-funded warrant is counted as an outstanding share for EPS, excluded from beneficial ownership by the blocker, and treated as owned stock for tax attribution.

That distance matters in life sciences more than anywhere else. The sector's equity is supplied by a concentrated set of crossover funds that repeatedly bump against ownership caps, PIPEs ran at roughly 87 percent of biotech follow-on volume in 2025, and the pre-funded warrant has become the standard equity-side companion to the royalty and structured-credit tools covered elsewhere on this site.

What follows is the equity-side companion to the analysis of how a financing's balance-sheet treatment so often diverges from its legal form.

What the Instrument Actually Is

The economics are almost pure common stock. The legal form is a warrant, and the operative terms are worth reading rather than summarising, because the whole structure lives in them. The provisions below are drawn from filed warrant forms, which across issuers track a common template.

The strike is nominal and the purchase price is pre-paid. A pre-funded warrant recites that the aggregate exercise price, except for a nominal residual, was pre-funded to the company at or before issuance, so no further consideration beyond the residual is required to exercise. The residual is set as low as the drafting will bear: one hundredth of a cent at Aadi and TScan Therapeutics, one tenth of a cent at Tango Therapeutics, and five millionths of a dollar at Precision BioSciences. The residual exists only to keep the instrument a warrant in form.

It is non-refundable and, in the modern form, perpetual. The pre-paid amount is not returnable under any circumstance, including expiry unexercised. Older pre-funded warrants sometimes carried a short life, the 2015 Gevo form ran one year, but the current convention is no expiry. TScan's December 2024 warrants are immediately exercisable and do not expire; 4D Molecular Therapeutics discloses its as exercisable from issuance until exercised in full. The holder has bought the shares and faces no deadline to take title.

It is cashless-exercisable on a defined formula. By election, and where a resale registration is unavailable, the holder can net-exercise for a Net Number of shares equal to (A x B - A x C) / B, where A is the shares being exercised, B is the relevant VWAP, and C is the exercise price. With C at a hundredth of a cent, the reduction is trivial, so the holder can move from warrant to share without paying anything and without a fresh cash outlay hitting the issuer.

It confers no shareholder rights until exercise. The holder has no vote, receives no dividends, and is not a stockholder for any purpose until the warrant shares are issued. The single exception is a distribution-participation clause: on a dividend or asset distribution the holder participates as if it had exercised, but only up to the ownership cap, with the balance held in abeyance.

Anti-dilution is structural, not economic. Because the strike is already nominal, the full-ratchet and weighted-average mechanics of ordinary warrants do not fit. Protection is delivered instead by proportionally adjusting the number of shares underlying the warrant on stock splits, combinations, and asset distributions. 4D Molecular's disclosure is representative: the share number adjusts for stock dividends, splits, combinations, reclassifications and distributions of assets, and nothing else.

On a change of control the holder can demand cash. A fundamental-transaction clause requires any successor entity to assume the warrant, or, at the holder's election within a defined window, requires the company or successor to buy the unexercised warrant for its Black-Scholes value, calculated on the Bloomberg option-valuation function with volatility capped at the lesser of 100 percent and the 90-day historical figure. The instrument therefore carries a cash exit on a takeover that ordinary common stock does not.

The Blocker, Read Closely

The single provision that makes the pre-funded warrant useful is the beneficial-ownership limitation, and its drafting is more aggressive than the shorthand "4.99 percent cap" suggests.

The company may not effect, and the holder may not exercise, any portion of the warrant to the extent that after giving effect to the exercise the holder together with its Attribution Parties would beneficially own more than the Maximum Percentage of the outstanding common stock. Attribution Parties is drawn broadly, capturing affiliated funds, feeder funds, managed accounts, and any person whose ownership aggregates with the holder's under Section 13(d), so the cap binds the manager's whole complex rather than one legal entity.

The count itself is narrow by design. Beneficial ownership is computed under Section 13(d), and it excludes both the unexercised remainder of this warrant and the unexercised portion of any other capped instrument the holder owns. The blocker measures against the shares the holder could actually take, not its full paper position.

Two features give the clause teeth.

- Overage is void ab initio. Any shares issued in breach of the cap are cancelled from inception: the holder cannot vote or transfer them, and the company holds the exercise price paid on them for future exercises.

- The exclusion is expressed for all purposes. The warrant states that shares issuable above the Maximum Percentage are not deemed beneficially owned by the holder for any purpose, including Section 13(d) and Rule 16a-1(a)(1). That is the sentence that keeps the holder off the ownership ledger.

The cap is a floor the holder controls. The holder may raise or lower the Maximum Percentage by written notice, commonly up to 9.99 or 19.99 percent, but an increase does not take effect until the sixty-first day after notice. The reported figure is therefore a lagging floor, not a ceiling: a holder shown at 4.99 percent can be a near-20 percent holder two months after it decides to be, and nothing on the current register signals the latent position.

The First Reason to Use It: Ownership Thresholds

The blocker exists because a fund can want a position's economics while being unable or unwilling to hold the corresponding legal ownership. The constraints it is written against are concrete and cumulative.

| Constraint | Threshold that bites | What crossing it triggers |

|---|---|---|

| Schedule 13D / 13G reporting | 5% | Public ownership disclosure and amendments on material change |

| Section 16 insider status | 10% | Short-swing profit disgorgement, Forms 3/4/5, no netting of round trips |

| Fund and adviser internal limits | Often 4.99% or 9.99% | Breach of investment mandate or concentration policy |

| Regulatory ownership rules | Various | Bank holding company control presumptions, insurance limits, 1940 Act diversification |

| HSR pre-merger notification | Size-of-transaction tests | Filing, waiting period, deal delay |

| Change-of-control and pill triggers | Contractual, often 10% to 20% | Poison-pill dilution, covenant defaults, change-of-control puts |

The 2025 and 2026 record shows each of these managed through the instrument.

Aadi's placement was led by Ally Bridge Group with OrbiMed, Invus, Kalehua, Avoro, KVP and Acuta, a roster of concentrated healthcare funds, and the pre-funded tranche let them take the capital without any one of them crossing a reporting or mandate line. OrbiMed's position in ImageneBio's 2026 PIPE, priced at 5.199 dollars per pre-funded warrant, sits behind a 19.99 percent blocker. TScan's December 2024 registered direct placed 7,500,000 pre-funded warrants with a single existing investor precisely because a direct share issuance of that size would have pushed the holder through a threshold.

The through-line is that the fund is fully committed economically and formally under the line.

The Second Reason: Nasdaq Rule 5635(d)

A separate constraint drives the same structure from the issuer's side. Nasdaq Rule 5635(d) requires shareholder approval before a "20% Issuance" at a price below the applicable Minimum Price, which captures most sub-market PIPEs. A large private placement runs straight into that limit.

Pre-funded warrants give issuers two ways to manage it.

The blocker itself caps how many underlying shares any single holder can bring into issuance at once, holding issued share count below the trigger. Alternatively, the warrants can be made exercisable only after shareholder approval, converting the excess into a contingent instrument.

Cue Biopharma's 2026 PIPE took the second route: 2,727,272 pre-funded warrants and 1,363,636 common warrants at an effective 11.00 dollars, with the pre-funded warrants exercisable only following stockholder approval at a special meeting, and no expiration. Wrap Technologies shows the same pattern in a related instrument, disclosing warrants that became exercisable on the date stockholder approval was obtained and are classified within permanent equity.

That approval contingency has an accounting consequence, because a warrant whose exercise depends on a vote is a different instrument for EPS than one that depends only on the holder's election. That is the subject of the next section.

The Accounting: Equity, With an EPS Sting

A pre-funded warrant issued in a life-science financing is, in the ordinary case, equity on the issuer's balance sheet. The route to that conclusion is worth stating precisely, because the classification is not automatic.

Why it lands in equity

The analysis runs first through ASC 480-10, which forces liability treatment for instruments that are mandatorily redeemable, that oblige the company to repurchase shares by transferring assets, or that oblige settlement in a variable number of shares. A plain pre-funded warrant is none of these.

It then runs through ASC 815-40, which permits equity classification only where the instrument is indexed to the entity's own stock and meets the settlement conditions. Indexation turns on the fixed-for-fixed test in ASC 815-40-15-7E: a settlement equal to the difference between a fixed number of shares and a fixed strike. A pre-funded warrant on the issuer's own shares, with a fixed share count and a fixed nominal strike, clears it.

The blocker does not disturb that conclusion, and the reason is specific. Equity classification fails where settlement terms vary with the identity of the holder. The blocker limits when the holder may exercise, and voids overage, but it does not change the number of shares delivered or the consideration paid, so it is not a holder-dependent settlement feature. This is the same distinction the SEC drew in its SPAC-warrant guidance, where warrants whose settlement varied with who held them were pushed to liability treatment.

The basic-EPS inclusion

The consequence that surprises finance functions is on earnings per share.

Under ASC 260-10-45-13, shares issuable for little or no cash consideration that are not contingently issuable are treated as outstanding and included in the computation of basic EPS. A penny-strike pre-funded warrant is the textbook case: the underlying shares enter the basic weighted-average denominator even though the warrant is unexercised and no shares have been issued.

Deloitte's guidance is explicit that this holds whether the warrant is immediately exercisable or becomes exercisable merely with the passage of time. The instrument therefore dilutes reported per-share earnings immediately, which is the opposite of how an ordinary out-of-the-money warrant behaves.

The contingent exception

The exception is the contingent case, and this is where the Cue structure diverges.

Where exercise depends on a condition beyond the passage of time, such as a shareholder vote, the shares are contingently issuable and are excluded from basic EPS until the condition is met. The same instrument thus dilutes basic EPS from day one in the plain structure and not at all in the vote-contingent structure. The dividing line is whether anything other than the holder's own choice stands between the warrant and the shares.

Valuation

Because the only difference between a pre-funded warrant and the underlying share is a de minimis strike, its fair value is generally taken to approximate the value of the share itself. That drives the purchase-price allocation when the warrant is sold in a unit alongside common stock and ordinary warrants: the pre-funded piece absorbs very nearly a whole share's value, and the accompanying warrant takes the remainder by relative fair value.

The Tax: The Mirror Image of the Blocker

Tax is where the decoupling that makes the instrument work for securities-law purposes turns against a careless holder, because the tax system does not honour the blocker.

The issuer's position

The issuer's stated position, recited in offering documents such as C4 Therapeutics', is that a pre-funded warrant should be treated as the underlying common stock for US federal income tax. On that view, no gain or loss is recognised on exercise, the holding period carries over to the share, and the tax basis carries over increased by any exercise price paid.

The treatment is favourable and consistent with the economics. It is also, as the same disclosure concedes, not binding on the IRS, which could recharacterise the instrument as an ordinary warrant with different timing and character. Where the warrant is sold as a unit with an accompanying common warrant, the holder must allocate the unit price between the two by relative fair value, and anti-dilution adjustments that increase a holder's proportionate interest can be a constructive distribution under Section 305, taxable even though no cash moves.

The attribution mirror-image

The sharper point is attribution. For beneficial-ownership reporting the blocker keeps the underlying shares off the holder's ledger; for the tax constructive-ownership rules it does nothing.

Under the Section 318 and Section 958 regimes, an option to acquire stock is treated as owned stock, and chains of options are counted through, so a small warrant can push a holder over a 10 or 50 percent line. The affiliation regulation at Treasury Regulation 1.1504-4 treats warrants as exercised where exercise is reasonably certain, weighing exactly the features a pre-funded warrant maximises: a nominal exercise price and the absence of any contingency beyond the mere passage of time.

A penny-strike, no-expiry, immediately exercisable pre-funded warrant is close to the paradigm of an instrument reasonably certain to be exercised. A holder can therefore be under 5 percent for Schedule 13D and simultaneously over a threshold for controlled-foreign-corporation or passive-foreign-investment-company purposes, with the unexercised warrant counted as owned throughout.

The cross-border overlay

For a cross-border holder this is not academic. A Swiss or EU fund taking pre-funded warrants in a US-listed biotech has to test its position under the attribution rules that determine PFIC and CFC status and the associated Form 8621 and 5471 filings, none of which respect the blocker. And FATCA withholding at 30 percent can reach deemed dividends on the warrants as much as on the shares.

The instrument that renders a holder invisible to one regulator renders it fully visible to another.

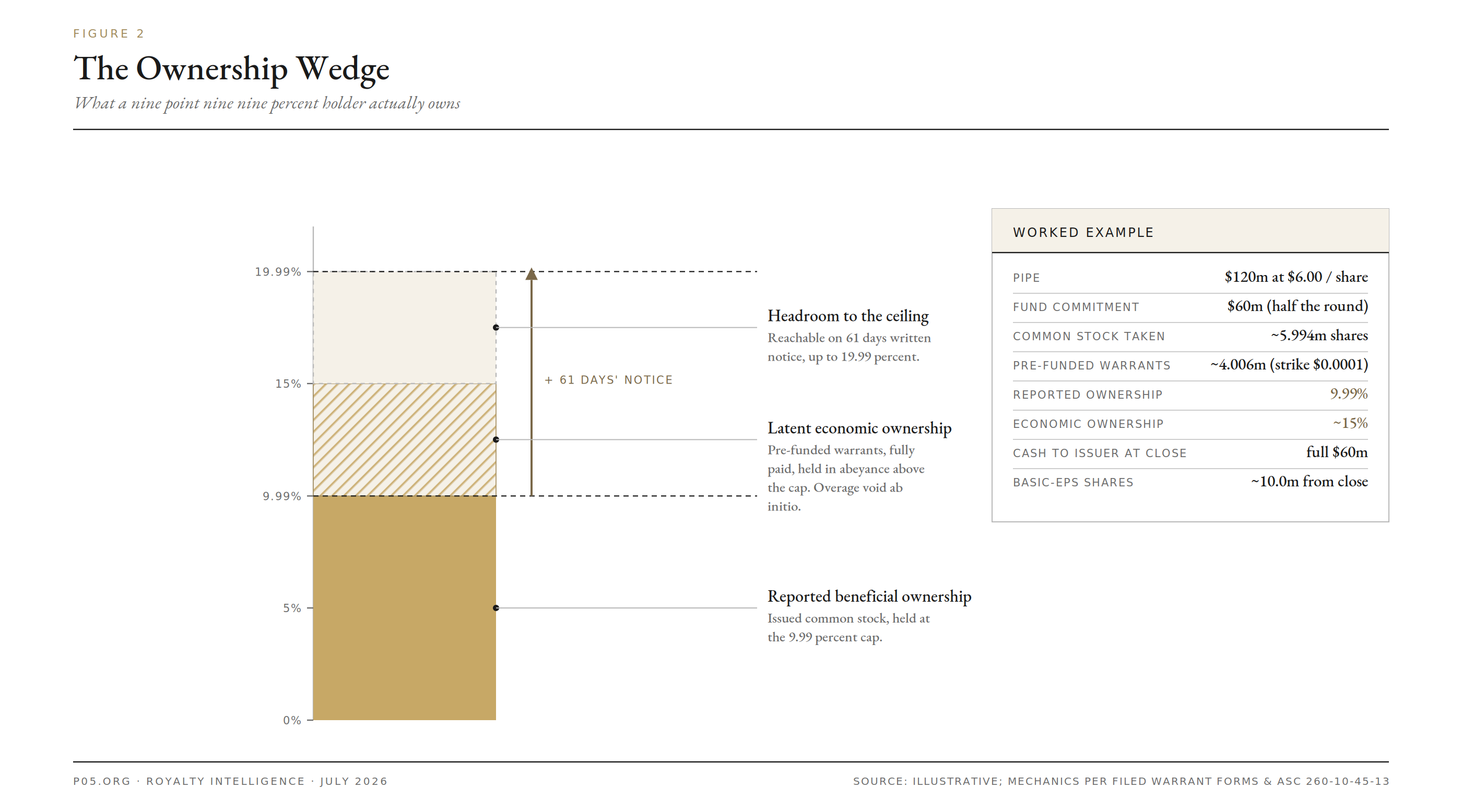

A Worked Example: Building 15 Percent While Reporting 9.99

The mechanics are clearest with numbers.

Take a clinical-stage issuer with 40,000,000 shares outstanding, raising 120 million dollars in a PIPE at 6.00 dollars per share, with a single crossover fund wanting to deploy 60 million dollars, half the round. A straight share purchase of 10,000,000 shares would give the fund 10,000,000 of a post-deal 60,000,000 shares, or 16.7 percent, through a 13D filing and into Section 16 territory.

Figure 2. Reported ownership stops at the 9.99 percent cap, while the fully paid pre-funded warrants carry economic ownership up to roughly 15 percent, with headroom to the elective ceiling reachable on 61 days' notice.

Structured with a 9.99 percent blocker, the fund takes the largest block of common stock that keeps it under the cap and takes the rest as pre-funded warrants. To stay at 9.99 percent on a post-deal base of 60,000,000 shares, it holds roughly 5,994,000 shares and takes the remaining roughly 4,006,000 units as pre-funded warrants at 5.9999 dollars.

| Line | Amount |

|---|---|

| Fund total commitment | 60,000,000 dollars |

| Common shares taken | ~5,994,000 at 6.00 dollars |

| Pre-funded warrants taken | ~4,006,000 at 5.9999 dollars, strike 0.0001 |

| Reported beneficial ownership at close | 9.99% |

| Economic ownership of the post-deal company | ~15% |

| Cash received by the issuer at close | full 60,000,000 dollars |

| Shares in issuer's basic EPS denominator from close | full ~10,000,000 |

The issuer receives the entire 60 million dollars at closing, not on some later exercise. Its basic EPS denominator picks up all ten million underlying shares immediately. And the fund reports 9.99 percent while holding roughly 15 percent of the economics, with the option to convert the gap into voting shares on sixty-one days' notice.

Every party gets what it wants, and the ownership register tells only part of the story. This is the calculation that recurs, deal after deal, behind the pre-funded tranches in the transaction table below.

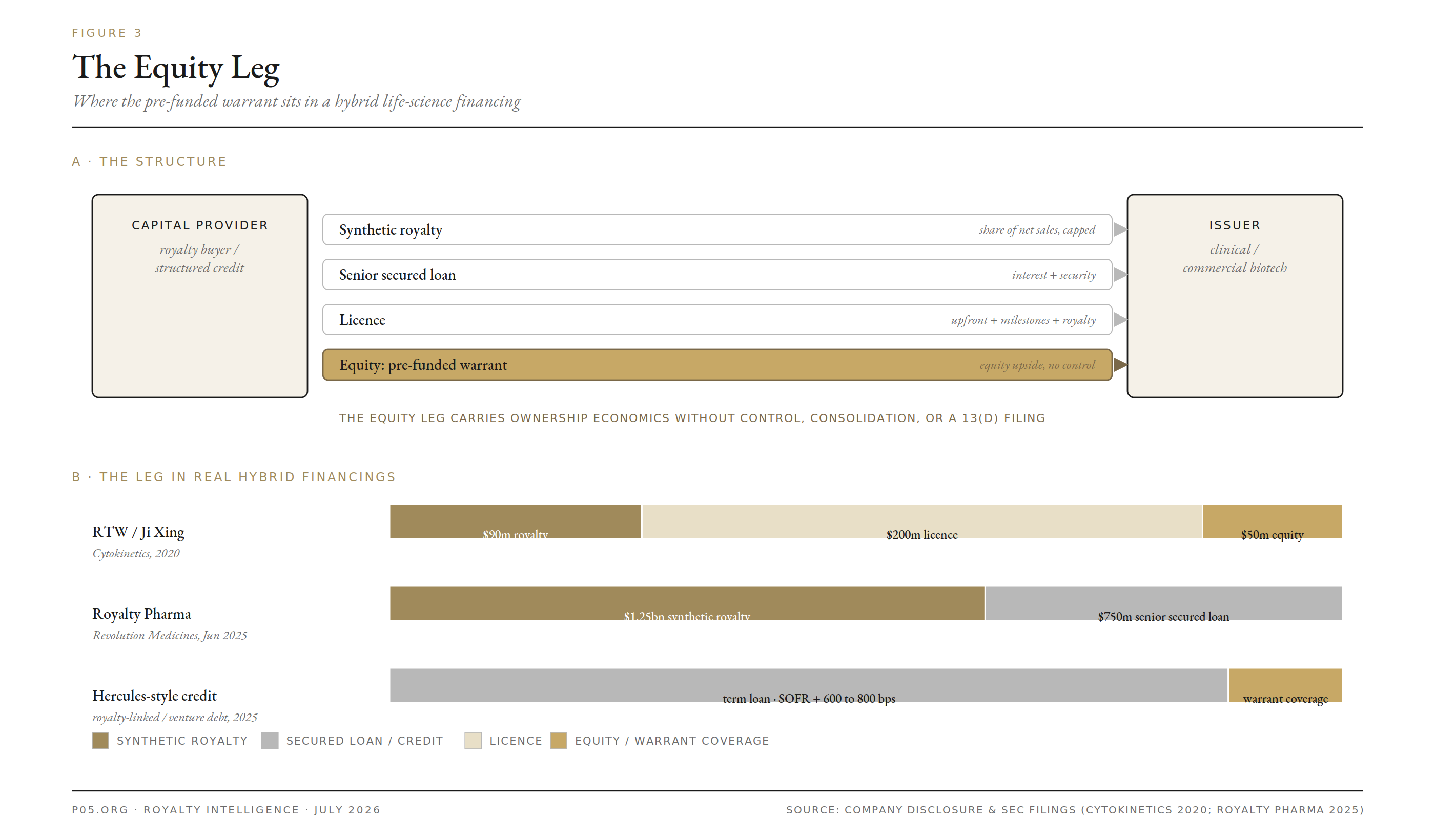

Where They Meet Royalty and Structured Finance

Pre-funded warrants are an equity-markets instrument, not a royalty instrument, but they have become the standard equity-side complement to royalty and structured credit. They appear at three distinct points in the life-science capital stack.

Figure 3. In a hybrid financing the pre-funded warrant sits as the equity leg alongside non-dilutive royalty and credit, carrying ownership economics without control, consolidation, or a 13(d) filing.

The companion equity raise. A company monetising a royalty for non-dilutive cash frequently runs a concurrent equity round, and when concentrated crossover investors anchor that round the equity is delivered through pre-funded warrants for the threshold reasons above. The royalty supplies balance-sheet cash without dilution; the pre-funded warrant supplies the equity a lead investor wants without crossing its cap.

The 2025 royalty market, which Gibson Dunn tracks at more than 32 billion dollars across 133 deals since 2020 with a median synthetic cap of 2.0x, ran in parallel with a PIPE market in which pre-funded warrants were routine.

The equity kicker inside a hybrid structure. The more interesting intersection is within a single financing. Structured deals increasingly bundle a synthetic royalty, a licence, and an equity investment, and the equity leg is a natural home for a pre-funded warrant when the provider wants upside without control.

The equity kicker inside a hybrid structure. The more interesting intersection is within a single financing. Structured deals increasingly bundle a synthetic royalty, a licence, and an equity investment, and the equity leg is a natural home for a pre-funded warrant when the provider wants upside without control.

The 2020 RTW and Ji Xing financing of Cytokinetics captures the shape: a synthetic royalty of up to 90 million dollars, a 200-million-dollar Ji Xing licence, and a 50-million-dollar equity investment in one package. That equity leg was direct common stock, but it is exactly the slot a pre-funded warrant fills when the provider wants the upside without the ownership footprint, for the same reasons a crossover fund does: to avoid affiliate status, to sidestep change-of-control provisions in its own fund documents, or to avoid consolidating the issuer.

Royalty Pharma's funding agreement with Revolution Medicines of June 2025, up to 1.25 billion dollars of synthetic royalty alongside a 750-million-dollar senior secured loan, shows how far the blended structures now stretch.

Warrant coverage on royalty-linked and venture credit. At the credit end, lenders extending royalty-linked or venture debt to development-stage companies routinely take warrant coverage as part of their return. Hercules Capital's 2025 book carried effective yields near 13 to 14 percent, structured as SOFR plus 600 to 800 basis points with warrant coverage, and it crossed 25 billion dollars in cumulative commitments by late 2025. Where such a provider wants the equity kicker without the ownership footprint, the pre-funded warrant is the vehicle.

The through-line is structural. For a firm bundling fragmented royalty streams or arranging capital into structured paper, the pre-funded warrant captures equity upside on a financed asset without the control, the consolidation, or the reporting that legal ownership would bring. It sits beside the royalty as the instrument that carries the economics the royalty does not, and its interaction with a target's change-of-control machinery is a further reason a strategic holder prefers it to common stock.

The Risks the Structure Carries

The features that make pre-funded warrants attractive also create exposures that the "just like stock" framing obscures.

The dilution is real and often large. A pre-funded warrant is dilutive for EPS from issuance and fully dilutive on the register the moment it is exercised. 4D Molecular carried 9,947,145 pre-funded warrants outstanding at the end of 2024; TScan's June 2023 offering alone created 47,010,526 of them. When these sit atop ordinary warrant series and option pools, the potential share count can run well beyond the issued base. And exercise, when it comes, can be sudden: Virax Biolabs reported in April 2026 that all 12,500,000 of its pre-funded warrants had been exercised, lifting shares outstanding to 19,923,432.

The capital is committed and non-refundable. The holder cannot walk away to recover its money if the thesis breaks; the pre-paid amount is gone regardless, and the only remaining decision is whether and when to exercise. That is correct given the economics, but it removes the optionality an ordinary out-of-the-money warrant preserves.

Liquidity is thin and the ownership picture is not static. The warrants themselves generally do not trade, so a holder's liquidity runs only through exercise and sale of the underlying. And a register showing a holder at 4.99 or 9.99 percent understates both the economic and the latent voting position, because the sixty-one-day notice can convert the reported figure into something approaching 20 percent. Read the reported percentage as a lagging floor.

The change-of-control cash-out is a real liability. The Black-Scholes put in the fundamental-transaction clause means an acquirer may face a cash claim from warrant holders that scales with volatility, not a simple share conversion. In a stressed sale it is a payable to model, not a footnote.

What Each Side Should Ask

For the issuer and its advisers:

- Does the pre-funded piece clear equity classification, and have we confirmed no holder-dependent settlement or net-cash feature slipped into the form? The default is equity, but the form has to earn it under ASC 480 and ASC 815-40.

- Are the underlying shares in our basic EPS denominator? If the strike is nominal and exercise turns only on the holder's choice, they are under ASC 260-10-45-13.

- Did we make any tranche contingent on a shareholder vote, and have we tracked which shares are therefore excluded from EPS until approval?

- Have we modelled the fully diluted overhang and the change-of-control cash-out? The pre-funded layer is permanent equity and the fundamental-transaction put is a contingent cash liability.

For the investor:

- What is our real position across every regime? Below the 13(d) line, potentially above a tax-attribution line, and dilutive to the issuer's basic EPS from day one. These do not move together.

- What does exercise cost us in tax terms if the IRS declines the issuer's stock characterisation? The favourable treatment is a position, not a ruling.

- For a cross-border fund, does the warrant create PFIC, CFC, or FATCA exposure the blocker does not shield? Under Section 318, Section 958, and Treasury Regulation 1.1504-4 it very likely does.

- In a hybrid royalty-plus-equity deal, does the pre-funded leg actually keep us clear of affiliate status, consolidation, and change-of-control triggers? That is usually the reason to use it rather than common stock, and it should be confirmed rather than assumed.

In almost every case the pre-funded warrant is the device that lets a concentrated holder take paid-up equity while its reported ownership stays under a line, or that lets an issuer place a large block without tripping the 20 percent rule.

The instrument is a share for the cash the company receives and the dilution it bears, and not a share for the ownership the holder reports. Read the warrant form rather than the press release, and the reason the two statements can both be true is in the blocker.

All information in this article was accurate as of the research date and is derived from publicly available sources including SEC filings, accounting standards guidance, tax regulations, law-firm practice notes, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, accounting, tax, or financial advice. The author is not a lawyer, accountant, tax adviser, or financial adviser.