Fund of the week: KCap Biotechnology Fund

What is KCap Biotechnology Fund?

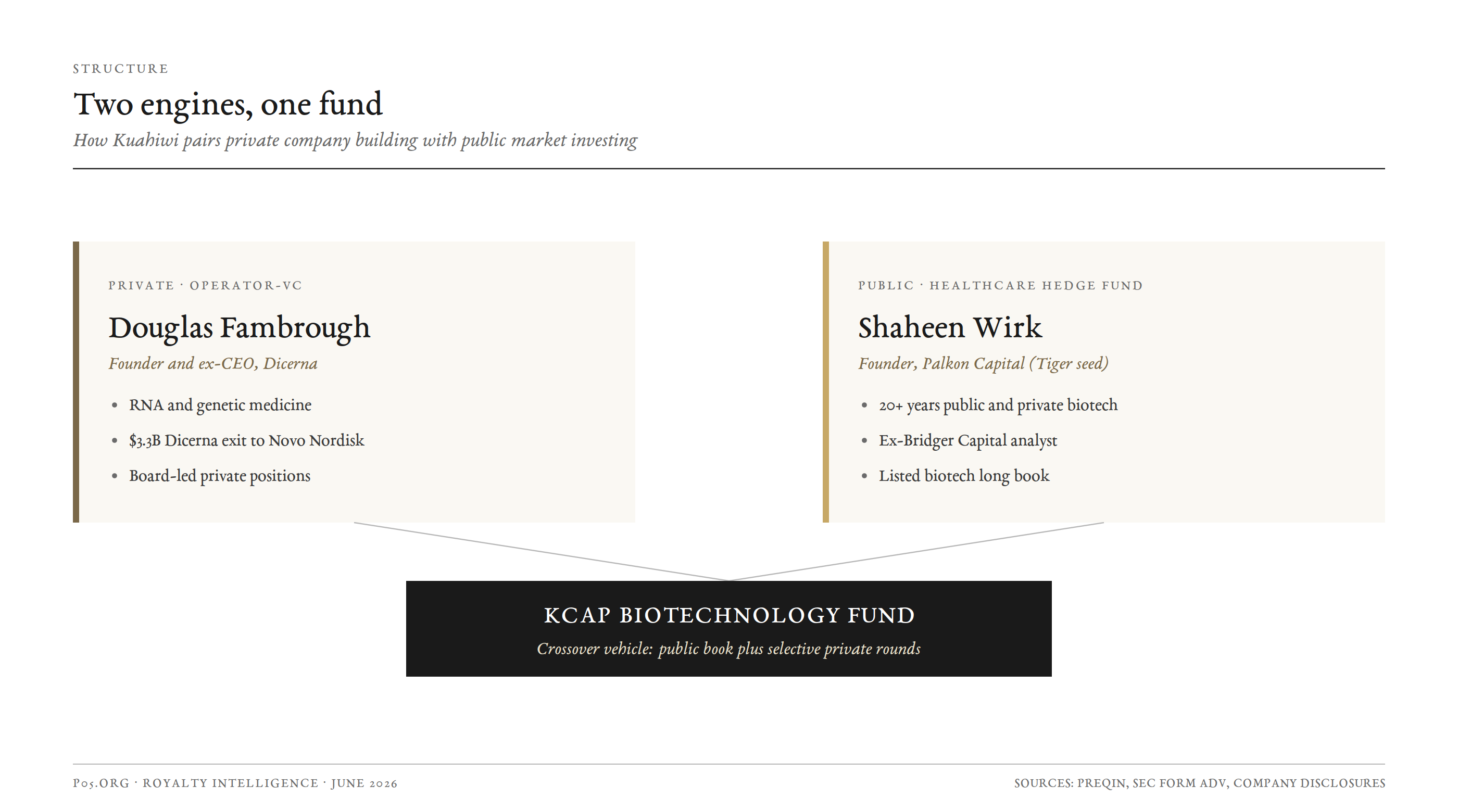

KCap Biotechnology Fund LP is a small, Boston based investment fund focused on RNA and genetic medicine companies. It is run through two related entities, Kuahiwi Capital LLC as general partner and Kuahiwi Management LLC as the management company, and it was co founded in 2023 by Douglas M. Fambrough III, the founder and former chief executive of Dicerna Pharmaceuticals, and Shaheen Wirk, a healthcare hedge fund manager who runs Palkon Capital.

The fund occupies a very different position in the life sciences capital stack from the large corporate venture units this series usually profiles. It is not an institutional platform with a hundred plus portfolio companies, a multi office footprint, and an investor relations team. It is a focused, founder led vehicle that appears to operate as a crossover fund, combining listed biotech positions with selective participation in private financings.

For royalty investors, structured credit funds, and licensing executives, the interest in KCap is less about its size and more about its lineage. Fambrough spent more than a decade building Dicerna into a public company and then selling it to Novo Nordisk for 3.3 billion dollars, negotiating one of the more instructive RNAi licensing books in the sector along the way.

Wirk brings two decades of public and private healthcare investing through a Tiger Management seeded hedge fund. The fund itself does not own royalties. The people running it have spent their careers creating, structuring, and trading the kind of assets that royalty markets ultimately buy.

This piece focuses on KCap specifically: its structure, its capital base, its limited partner picture, the track record of its principals, the single confirmed private position disclosed to date, and its relevance to the commercial life sciences capital markets. It also flags clearly where the public record is thin, because for a fund of this size and disclosure profile, honesty about what is and is not knowable matters more than the appearance of completeness.

Overview and Investment Focus

KCap is organised as a Delaware limited partnership, with Kuahiwi Capital LLC as general partner and Kuahiwi Management LLC as the management entity and registered adviser. It is based at 23 Holyoke Street in Boston. The fund custodies assets with JP Morgan Securities LLC and uses Grant Thornton LLP as auditor, signals of an institutional grade back office rather than an informal angel vehicle, notwithstanding the fund's modest size.

The fund maintains no public website and discloses almost nothing about its strategy in materials available to the public. What can be established with confidence comes from three sources: the fund's SEC filings (Form D for the offering, Form ADV for the adviser), the public financing announcements of companies it has backed, and third party data providers.

Public and private in one vehicle. Industry data describes Kuahiwi Management as long oriented and focused on publicly traded biotech, consistent with Wirk's hedge fund background. Yet the one financing the fund has been named in, the Oak Hill Bio Series A, is a private round.

The most reasonable reading is that KCap functions as a crossover vehicle: a public biotech book alongside a small number of private positions sourced through Fambrough's company building network. Readers should treat the precise public versus private split as undisclosed.

Inferred therapeutic thesis. No published thesis exists, so any characterisation is an inference. On the evidence, KCap concentrates on RNA based and genetic medicines: RNA interference, antisense oligonucleotides, conditionally activated RNA, and non viral gene therapy. This is the field Fambrough has worked in for more than two decades, and it maps cleanly onto the company boards he sits on. The fund trades breadth for depth in a modality its principals know better than almost anyone.

Capital Formation

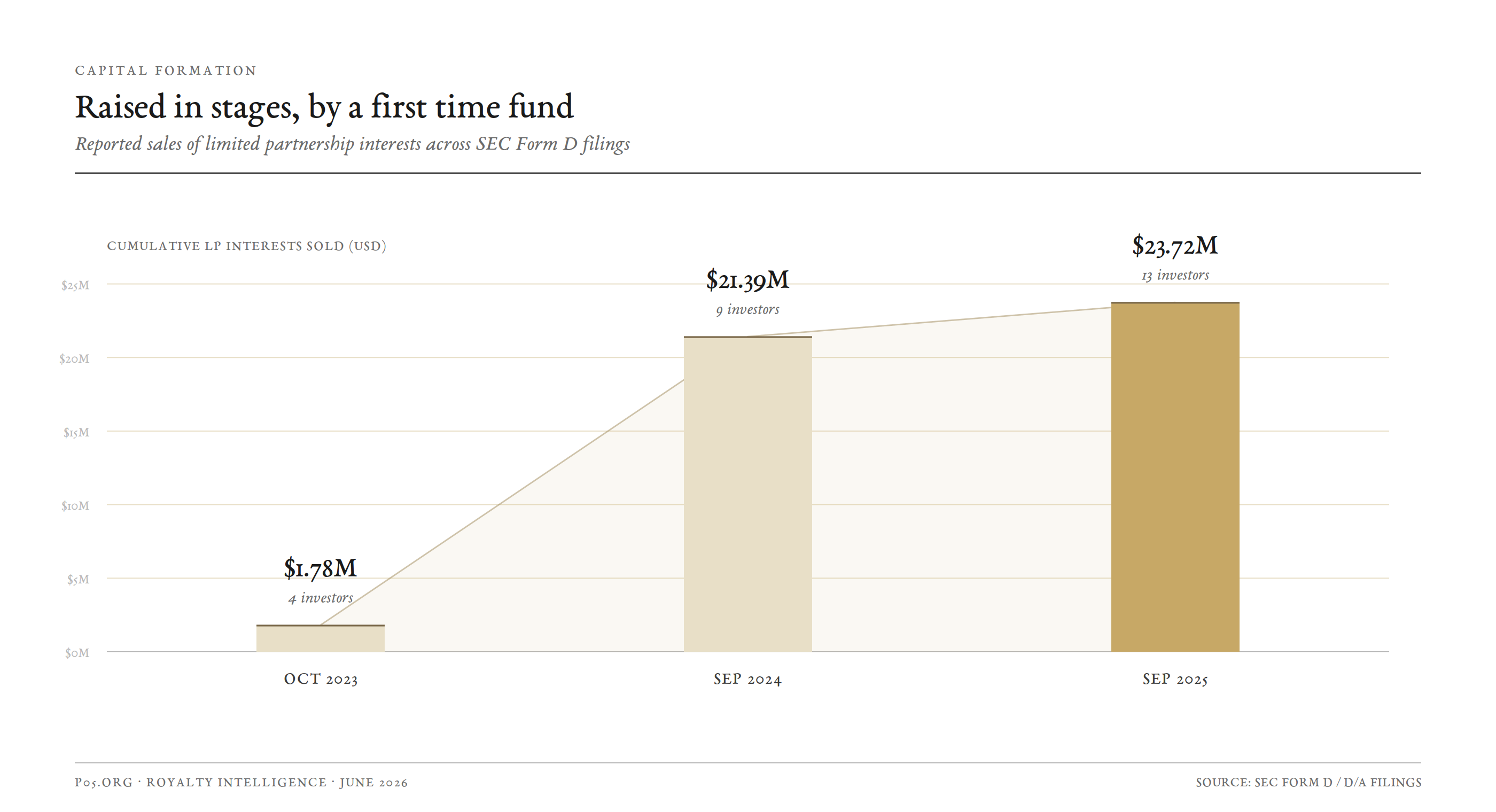

KCap raised capital in stages, reflected in a sequence of amended Form D filings. The fund grew from a small first close in 2023 to a little under 24 million dollars of reported sales by late 2025.

| Date | Filing | Amount sold | Investors | Notes |

|---|---|---|---|---|

| 10 October 2023 | Form D (initial) | ~1.78 million USD | 4 | First close |

| 27 September 2024 | Form D/A | ~21.39 million USD | 9 | Principal raise |

| 17 September 2025 | Form D/A | ~23.72 million USD | 13 | Latest reported figure |

A few structural points follow. The fund charges both a management fee based on asset value and a performance based fee on profits, the conventional management fee plus carried interest model. The reported figures are cumulative sales of limited partnership interests, not committed capital or a net asset value, so they should be read as a floor on capital raised rather than a precise statement of fund size.

At a little under 24 million dollars, KCap is a niche vehicle. Its cheque sizes are correspondingly modest, and its role in the private financings it joins is participation alongside larger funds rather than lead investor setting terms.

Management Company and Limited Partners

The adviser behind the fund, Kuahiwi Management LLC, is a Massachusetts registered investment adviser (CRD 334146, SEC file 801-131958). Its most recent Form ADV reports regulatory assets under management of approximately 21.4 million dollars across a single advisory client, that client being the pooled fund itself.

The adviser describes its business as portfolio management for pooled investment vehicles. The figures line up with the 2024 Form D close, which is consistent with a small adviser whose only client is its own fund.

On the limited partners themselves, the public record is, as expected for a private fund of this size, effectively silent. No specific limited partner names are disclosed in any public filing. What can be said is structural rather than nominal:

- The investor count grew from 4 at the 2023 first close to 9 in 2024 and 13 by 2025, a small and slowly widening base.

- A base of this size and profile is typically composed of high net worth individuals and industry insiders qualifying as accredited investors or qualified purchasers, rather than large institutional limited partners such as pensions, endowments, or funds of funds.

- The fund has no disclosed cornerstone institutional anchor, which is normal for a first time, founder led vehicle.

In short, the limited partner picture is best understood as a small circle of private investors backing two well known principals, not as an institutionally syndicated fund. Anyone seeking specific names will not find them in the public record, and this article does not speculate about individual investors.

The Principals

KCap is, to a first approximation, its two founders. Understanding the fund means understanding their records, which are unusually deep for a manager of a fund this size.

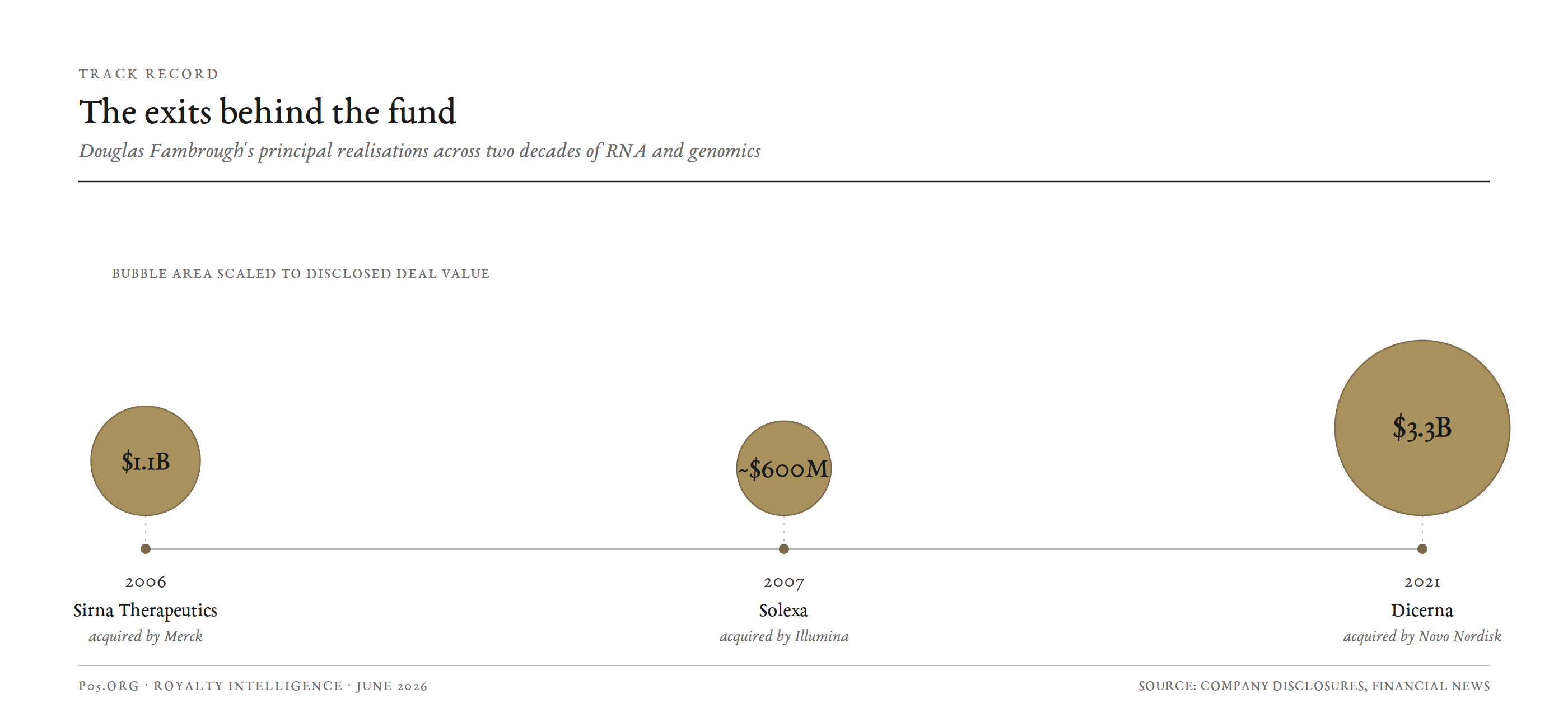

Douglas Fambrough (private, operator and venture). Fambrough co founded Dicerna in 2007 and served as president and chief executive from 2010 until its acquisition. Under his leadership the company developed the GalXC and GalXC-Plus RNAi platforms, completed a NASDAQ initial public offering in 2014, advanced nearly twenty discovery, preclinical, and clinical programs, and signed six major corporate collaborations.

In November 2021, Novo Nordisk agreed to acquire Dicerna for 38.25 dollars per share in cash, a total equity value of approximately 3.3 billion dollars and an 80 percent premium to the prior close.

Before Dicerna, Fambrough spent over a decade as a general partner at Oxford Bioscience Partners, where his investments included the first generation RNA interference pioneer Sirna Therapeutics, acquired by Merck for 1.1 billion dollars in 2006, and the DNA sequencing pioneer Solexa, acquired by Illumina for roughly 600 million dollars, alongside Xencor, Rib-X Pharmaceuticals, and Solstice Neurosciences.

He holds a PhD in genetics from the University of California, Berkeley, and an undergraduate degree in biology from Cornell University, and worked as a genomic scientist at the Whitehead/MIT Center for Genome Research, now the Broad Institute, before entering venture capital.

Shaheen Wirk (public, healthcare hedge fund). Wirk is the founder and chief investment officer of Palkon Capital Management, a healthcare dedicated investment firm he launched in 2013 in partnership with Julian Robertson and Tiger Management, placing it in the Tiger lineage of seeded managers.

Before Palkon he spent more than a decade as a senior analyst at Roberto Mignone's Bridger Capital. He trained as a research scientist in oncology and trauma surgery and holds MD, MBA, and undergraduate degrees from Duke University. He has served on the boards of Tvardi Therapeutics and Movano Health, and brings public market discipline and more than 20 years of life sciences investing to the partnership.

The combination is the point: a company builder who has created and sold platform companies, paired with a public market healthcare investor. One sources and shapes private assets, the other underwrites listed equities. The precise division of day to day responsibilities at Kuahiwi is not publicly detailed, and Wirk continues to run Palkon separately, but the two records together explain the fund's apparent crossover design.

How the fund is built

The two engine structure is what differentiates KCap from both a conventional seed fund and a conventional biotech hedge fund. A private operator and venture engine supplies sourcing, scientific diligence, and board level company building in RNA and genetic medicine. A public market engine supplies the discipline of underwriting listed biotech equities. Folded into a single small partnership, the result is a crossover vehicle that can hold a public book and step into selective private rounds where the principals have an edge.

Royalty and Strategic Income Positions

KCap invests through equity. It does not own a pharmaceutical royalty portfolio, does not issue royalty backed debt, and does not earn ongoing royalty income on the products its portfolio companies develop. Its royalty exposure is entirely indirect, mediated by equity stakes in companies whose own licensing agreements may carry royalty terms. A royalty buyer such as Royalty Pharma, HealthCare Royalty, DRI Healthcare, or Sagard Healthcare buys cash flows directly. KCap buys equity and accepts the binary risk of clinical development in exchange for exit upside.

What makes KCap worth a royalty reader's attention is not the fund's balance sheet but the licensing playbook its lead principal ran at Dicerna, which is a compact lesson in how RNAi royalty stacks are built, and which includes one structure that functioned very much like a royalty.

The Dicerna licensing book

By the time of its acquisition, Dicerna had assembled collaborations with Novo Nordisk, Roche, Eli Lilly, Alexion, Boehringer Ingelheim, and Alnylam, alongside earlier deals with Kyowa Hakko Kirin and Ipsen. The standard architecture of these agreements is the milestone and royalty stack that recurs across the sector: an upfront payment realised on signing, research funding during the collaboration, development and regulatory milestones tied to clinical and approval events, sales milestones tied to cumulative net sales thresholds, and tiered royalties on net sales of any commercialised product.

The headline value is almost always dominated by the back loaded milestone and royalty tiers, which carry low probabilities of payment, while the certain cash sits in the upfront and near term components.

For a royalty investor, the Dicerna book illustrates a structural point: a platform company monetises its technology through a series of partner specific royalty bearing agreements long before any single product reaches the market, and the equity holders capture that value only at a liquidity event. Dicerna's liquidity event was the Novo Nordisk acquisition, which crystallised the equity value of the entire collaboration book into a single cash purchase price and transferred the future royalty and milestone economics to the acquirer.

The Alnylam settlement: a royalty style override

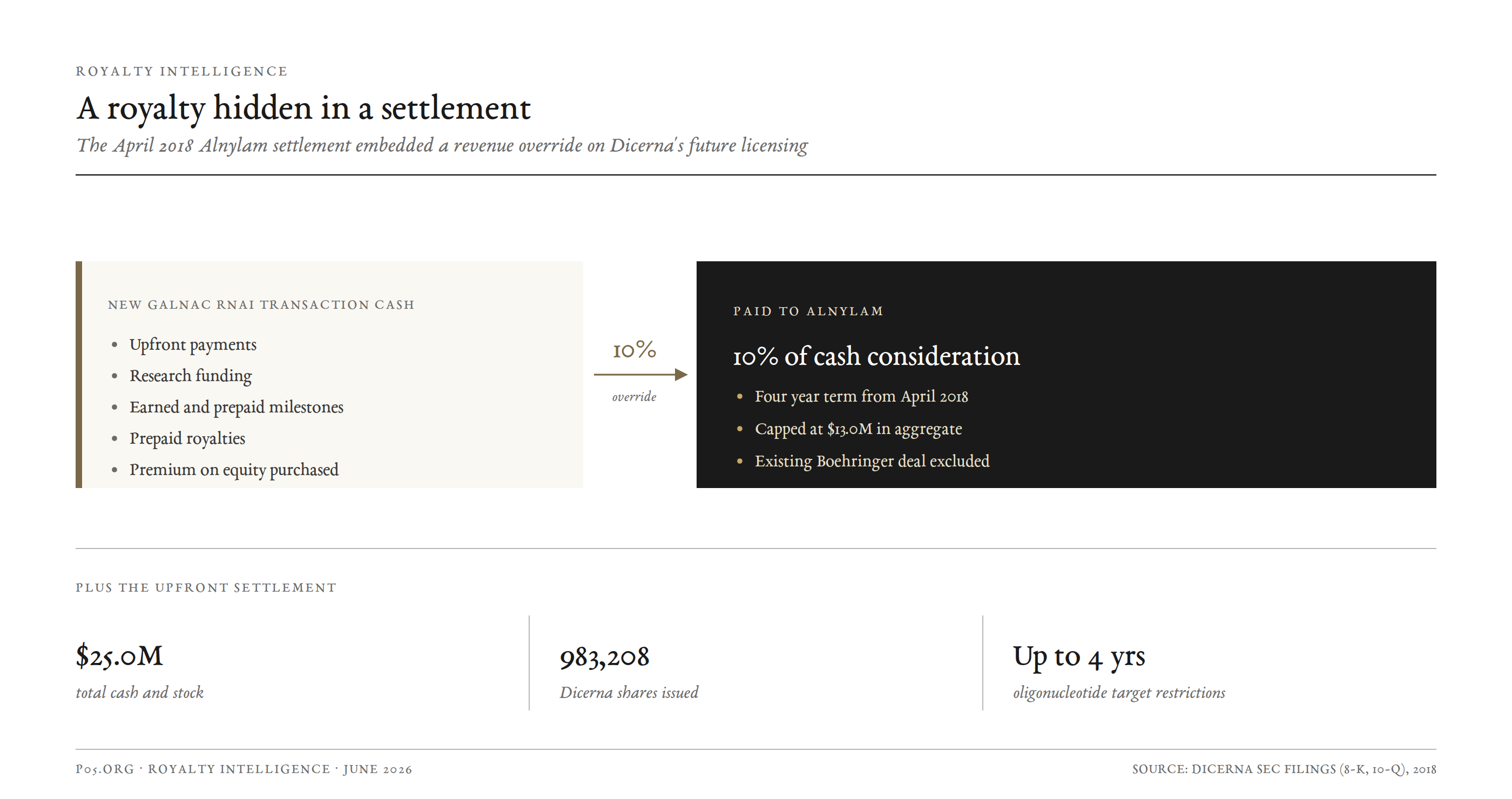

The most directly royalty relevant episode in Fambrough's record is the April 2018 settlement of the long running trade secret litigation between Alnylam and Dicerna over GalNAc conjugate delivery technology. The dispute originated in Alnylam's 2014 acquisition of Sirna's assets from Merck and its subsequent claim that Dicerna had improperly obtained related know how.

The settlement is interesting precisely because of how it was structured. Dicerna agreed to pay Alnylam 25 million dollars in cash and stock, including the issuance of 983,208 Dicerna shares, and accepted development restrictions on a defined set of Alnylam targets for up to four years. Critically, Dicerna also agreed to pay Alnylam 10 percent of any cash consideration it received, including upfronts, research funding, milestones, prepaid royalties, and equity premiums, on any new GalNAc conjugated RNAi transaction signed within four years, capped at 13 million dollars and excluding the existing Boehringer Ingelheim collaboration.

That is, in substance, a royalty style override on Dicerna's own future licensing revenue, negotiated to settle litigation rather than to finance a product. It is a useful reminder for royalty professionals that synthetic royalty and revenue share structures arise in many contexts beyond a financing, including in intellectual property disputes.

Oak Hill Bio and the Roche origin of rugonersen

KCap's one confirmed private position, Oak Hill Bio, also carries an embedded royalty dimension. Oak Hill's lead asset, rugonersen, is an antisense oligonucleotide originally developed by Roche to restore UBE3A production in neurons as a treatment for Angelman syndrome. An asset originated inside a large pharmaceutical company and then advanced by a venture backed company typically carries contractual royalty and milestone obligations back to the originator.

While the specific terms of any Roche arrangement are not public, the structure is familiar: a smaller company takes on the development risk of a deprioritised large pharma asset in exchange for rights, subject to royalty and milestone payments back to the originator on success. For royalty markets, assets of this kind become candidates for synthetic royalty and development financing as they approach the market.

Equity to royalty exposure

The mechanism by which KCap captures any value from its portfolio companies' royalty agreements is the same equity mediated chain that applies to any venture or crossover investor. The fund's stake erodes with each subsequent financing round, it captures value only at a liquidity event, and where a portfolio company is acquired, any earnout or milestone consideration is typically held in escrow and released against the same low probabilities of payment that govern milestone economics generally.

Royalty rights that arise after an acquisition flow to the acquirer, not to the original investors. KCap, in short, is an upstream actor whose portfolio may eventually generate royalty eligible assets, not a counterparty in the royalty market itself.

Portfolio of Investments

KCap's portfolio is largely undisclosed. The fund does not publish its holdings, and individual positions become visible only when a company announces a financing and names its investors, or when one of the principals takes a board seat. The picture below distinguishes between the one confirmed KCap private investment and the broader set of company boards the principals sit on, which signal the thesis but are not all confirmed as fund positions.

Confirmed KCap private investment

Oak Hill Bio is a clinical stage rare disease therapeutics company. On 1 June 2026 it closed a 32.5 million dollar Series A co led by Balyasny Asset Management, venBio, and Janus Henderson Investors, with participation from KCap Biotechnology Fund. Proceeds are funding the advance of rugonersen, an antisense oligonucleotide for Angelman syndrome, into a pivotal Phase 3 study. Angelman syndrome affects roughly 30,000 diagnosed patients across the US and EU5 with no approved treatments. Fambrough joined the Oak Hill board alongside venBio's Rich Gaster and Sandeep Kulkarni.

Principal board portfolio (thesis indicators, not all confirmed as KCap positions)

The companies on whose boards the principals sit map cleanly onto the RNA and genetic medicine thesis. Some board seats predate the 2023 launch of KCap and reflect personal involvement rather than a confirmed fund investment, so they are best read as evidence of focus rather than as a portfolio roster.

| Company | Focus | Principal and role | Notes |

|---|---|---|---|

| Oak Hill Bio | ASO, rare disease (Angelman) | Fambrough, director, June 2026 | Confirmed KCap fund position |

| Switch Therapeutics | Conditionally activated siRNA (CASi) | Fambrough, director, July 2023 | Board seat concurrent with fund launch |

| Anjarium Biosciences | Non viral gene therapy (Zurich) | Fambrough, non executive director, October 2022 | Predates fund launch |

| TScan Therapeutics | TCR cell therapy | Fambrough, director, 2020 | Predates fund; company now public (NASDAQ: TCRX) |

The pattern is consistent: RNA interference, antisense, conditionally activated RNA, and non viral gene therapy, with a tilt toward rare and genetically defined diseases. This is the GalXC playbook extended into a fund.

A note on disclosure: a fund of KCap's size is under no obligation to publish its holdings, and the absence of a public portfolio is normal for an emerging manager. Readers should treat the confirmed position as a floor, not a complete picture.

Strengths and Competitive Advantages

Operator credibility paired with public market discipline. Few small funds combine a founder operator who built and sold a 3.3 billion dollar company in their target field with a public market healthcare investor of two decades' standing. In diligence on oligonucleotide chemistry, delivery, and licensing structure, KCap's principals operate at the level of a strategic acquirer.

Reputation driven deal access. The companies KCap has backed are not obscure. Oak Hill's Series A was co led by Balyasny, venBio, and Janus Henderson. Access to syndicates of that quality, for a fund of this size, is a function of the principals' standing rather than the fund's cheque.

Focus over breadth. Where a corporate venture unit runs more than a hundred positions across biotech and deep technology, KCap appears to do the opposite: a concentrated set of positions in a field its principals understand at a granular level.

Independence. As a financial investor with no strategic parent, KCap can back the strongest companies in its field without the mandate constraints that shape corporate venture activity.

Risks, Challenges, and Vulnerabilities

Acute key person concentration. KCap's deal access, diligence capability, and board representation run through two individuals, one of whom also runs a separate hedge fund. Any interruption to the principals' involvement, or a material claim on their attention from outside vehicles, would weigh on the fund in a way that does not apply to a deep bench team.

Divided attention. Wirk continues to operate Palkon Capital, and the principals hold multiple external board seats. The fund benefits from their networks but competes with their other commitments for time.

Small fund size. At a little under 24 million dollars of reported sales, KCap writes small cheques, participates rather than leads in private rounds, and can hold only a limited number of positions. A single clinical failure in a concentrated portfolio has an outsized effect on returns.

Single modality exposure. The apparent concentration in RNA and genetic medicine is a strength when sentiment for the modality is strong and a vulnerability when it is not. RNAi and oligonucleotide sentiment has been cyclical, and a focused fund has no diversification away from a modality wide drawdown.

Disclosure opacity. The near absence of public information about strategy, terms, and holdings is normal for an emerging manager but limits external assessment. Conclusions about the thesis are inferences, and the portfolio picture is necessarily incomplete.

Emerging manager track record risk. As a first time fund launched in 2023, KCap has not yet demonstrated a realised return as an investing entity, as distinct from its principals' prior records. The vintage is young and exits are years away.

Implications for the Pharmaceutical Royalty and Biotech Capital Markets

For commercial capital markets, KCap matters less as a counterparty and more as a signal and as a case study.

First, the fund's principals are reliable early indicators of where credible RNA and genetic medicine assets are forming. When a manager with Fambrough's record takes a board seat and writes a cheque, the implied scientific and commercial validation of the underlying asset is meaningfully higher than that of a generalist syndicate. Royalty and structured credit teams that track specialist investor participation can use KCap's involvement as a partial proxy for asset quality in the oligonucleotide and gene therapy space.

Second, KCap's private positions are exactly the kind of late preclinical and clinical stage assets that become royalty eligible over time. Oak Hill's rugonersen, a Roche originated antisense oligonucleotide heading into Phase 3, is the type of asset that royalty buyers and development financiers evaluate for synthetic royalty and milestone backed structures as it approaches the market. Assets carrying embedded royalty obligations back to a large pharma originator are a recurring feature of this part of the market.

Third, Fambrough's Dicerna history is a useful reference for anyone modelling RNAi licensing economics. The Dicerna collaboration book, and in particular the Alnylam settlement override on future GalNAc transaction cash, are concrete examples of how royalty and revenue share structures are negotiated in the RNA field, including outside the financing context. The gap between headline deal value and realised cash, and the transfer of future royalty economics to an acquirer at the point of sale, are both visible in the Dicerna outcome.

Recent Developments

| Date | Event |

|---|---|

| 2023 | KCap Biotechnology Fund launched; Kuahiwi Management co founded by Fambrough and Wirk; first Form D filed 10 October (~1.78M USD, 4 investors) |

| July 2023 | Fambrough joins board of Switch Therapeutics (conditionally activated siRNA) |

| September 2024 | Form D/A reports ~21.39M USD raised across 9 investors |

| 2024 and 2025 | KCap serves as a presenting sponsor of the Timmerman Traverse for Life Science Cares |

| September 2025 | Form D/A reports ~23.72M USD raised across 13 investors |

| June 2026 | Oak Hill Bio closes 32.5M USD Series A with KCap participation; Fambrough joins board; rugonersen advances toward Phase 3 in Angelman syndrome |

Conclusion

KCap Biotechnology Fund is a focused, founder led crossover fund whose significance is out of proportion to its size. It is not a competitor for royalty buyers, structured credit funds, or specialty lenders, and at a little under 24 million dollars it is not a large force in venture or public markets either. Its importance lies in its lineage. The fund pairs a company builder who took an RNAi platform from founding to a 3.3 billion dollar exit with a public market healthcare investor of two decades' standing, and it concentrates that experience in the modality its principals helped shape.

For royalty and licensing professionals, the practical reading is twofold. KCap is a high quality signal node in RNA and genetic medicine, and its lead principal's track record is a compact field guide to how royalty and milestone structures are built, monetised, and ultimately transferred in this part of the sector.

The open questions are the ordinary ones for an emerging manager: whether a concentrated, two principal fund can convert distinguished individual records into realised fund returns, whether the public and private halves of the strategy reinforce rather than dilute one another, and whether the vehicle can institutionalise beyond its founders. Those answers are years away. For now, KCap is best understood as one of the most credible small funds in RNA medicine, worth watching precisely because of who is making the decisions.

All information in this article was accurate as of June 2026 and is derived from publicly available sources including SEC Form D and Form ADV filings, company press releases and financing announcements, Novo Nordisk and Dicerna disclosures, court and settlement filings, third party data providers, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.