Digital Health Royalties

A mechanics-and-gap analysis of royalties in digital health and prescription digital therapeutics as of 2026.

When pharma companies started licensing prescription digital therapeutics, they reached for the only royalty template they knew: the drug deal. An upfront, development and regulatory milestones, commercial milestones, then tiered royalties on net sales.

On paper the deals looked like biotech licensing. Otsuka's 2019 deal with Click Therapeutics was worth up to $302 million with tiered double-digit royalties. Boehringer Ingelheim's schizophrenia deal with the same company ran to more than $500 million plus royalties.

Those are real pharma-scale numbers. And yet the digital therapeutics sector, as a financing story, has been closer to a graveyard than a gold rush.

This piece does two things, in the style of our veterinary mechanics analysis. First, the mechanics: how a digital health royalty is actually built, and how the pharma template fits, or fails to fit, the underlying asset. Second, the gap: whether a financeable royalty even exists here, and why the answer, as of 2026, is mostly not yet.

The short version is a structural mismatch. Digital health borrowed an instrument designed for patent-protected molecules and applied it to subscription software. Almost every feature that makes a drug royalty financeable is weaker, or absent, in software. The result was predictable, and it happened.

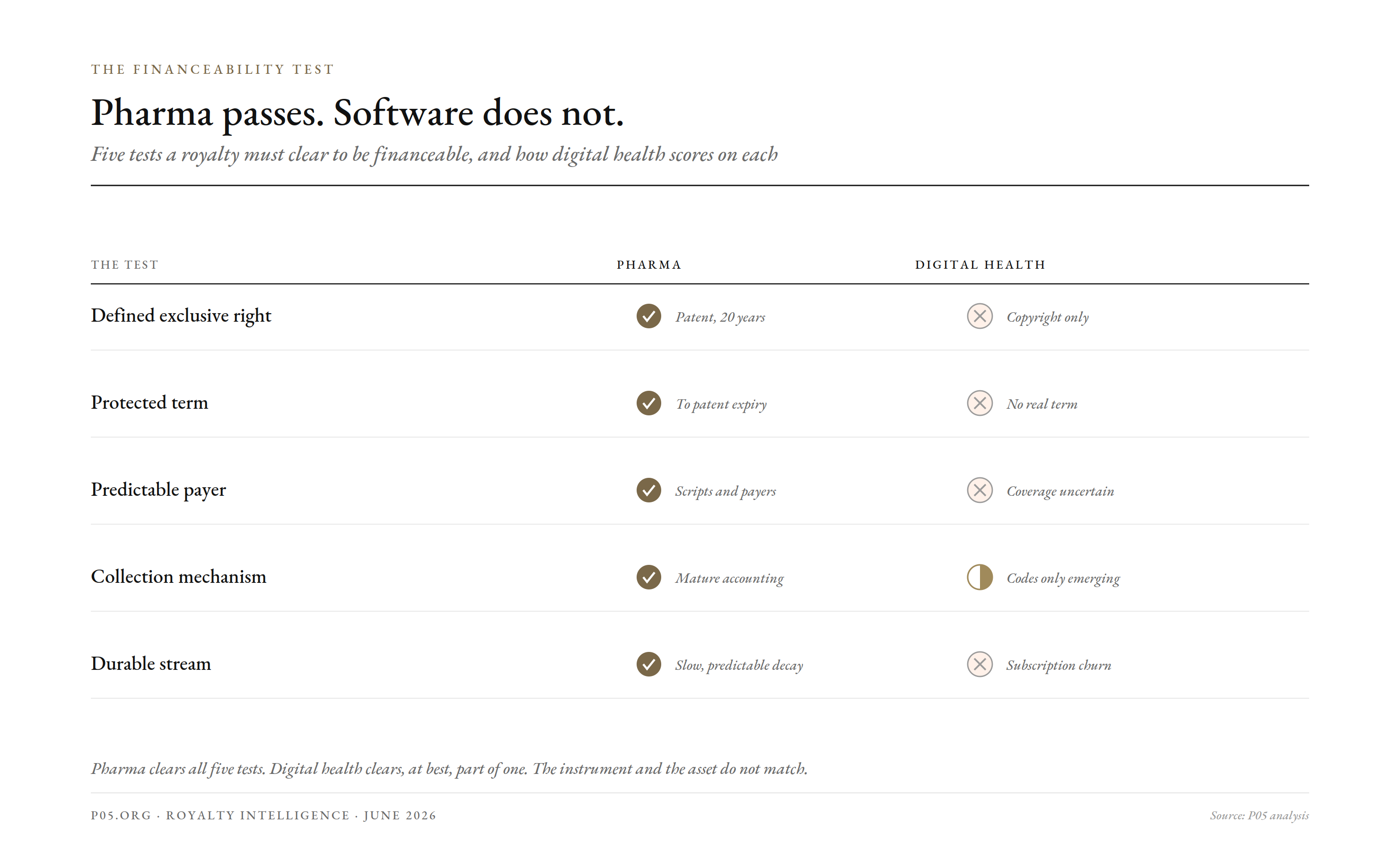

The financeability test ] Five tests a financeable royalty must pass. Pharma clears all five; digital health clears almost none.

The financeability test, applied to software

A royalty becomes financeable when four or five things hold at once: a defined and enforceable right, a long and predictable term, a diversified or creditworthy payer, a working collection mechanism, and a stream durable enough to discount. Pharma clears all of them.

Run digital health through the same test and it fails most of them.

| Test | Pharma | Digital health / DTx |

|---|---|---|

| Defined exclusive right | Patent, 20-year term | Software copyright and trade secret; weak moat |

| Protected term | To patent expiry, years out | None comparable; competitors re-build features |

| Predictable payer | Rated pharma or broad scripts | Payer coverage uncertain, often absent |

| Collection mechanism | Mature licence accounting | Immature; billing codes only emerging |

| Durable stream | Slow decay after expiry | Subscription churn; can vanish in a year |

The first row is the deepest problem. A drug's value rests on a composition-of-matter patent that blocks copies for two decades. A digital therapeutic rests mostly on copyright and trade secret, which protect the specific code but not the clinical idea.

A competitor can build a different cognitive-behavioral-therapy app for the same indication without infringing. There is no twenty-year wall, so there is no protected stream to sell.

The second problem is the term. A drug royalty has a clock: it runs to patent expiry and you discount against it. A software subscription has no natural term. It runs as long as customers renew, which is a churn assumption, not a property right.

That single difference changes everything downstream. A royalty buyer prices duration. Pharma offers a contractually bounded duration; software offers a behavioral guess.

The pharma template, and where it strains

Despite the mismatch, the deals were built on the drug-licensing chassis. It is worth seeing the structure, because the structure is exactly what strained.

The Click deals are the clearest specimens, because their terms were disclosed in pharma-style detail.

| Deal element | Otsuka / Click (2019, MDD) | BI / Click (2020-22, schizophrenia) |

|---|---|---|

| Upfront and regulatory milestones | up to $10m | undisclosed upfront |

| Development funding | ~$20m | R&D funding included |

| Commercial milestones | $272m | part of >$460-500m total |

| Royalty | tiered, double-digit on net sales | tiered, on worldwide net sales |

| Headline total | ~$302m | >$500m |

Look at the shape. It is a biotech deal: the pharma partner funds development, pays milestones at regulatory and commercial gates, and pays a tiered double-digit royalty on sales. The digital therapeutics company plays the role of the biotech licensor.

The milestone ladder even rhymes with the drug one. The asset is regulated by the FDA as Software as a Medical Device, so it passes through clearance gates that look like regulatory milestones, and the Otsuka product, Rejoyn, did reach FDA clearance in 2024.

So the front of the deal worked. Development got funded, milestones got paid, products got cleared. The structure did its job up to launch.

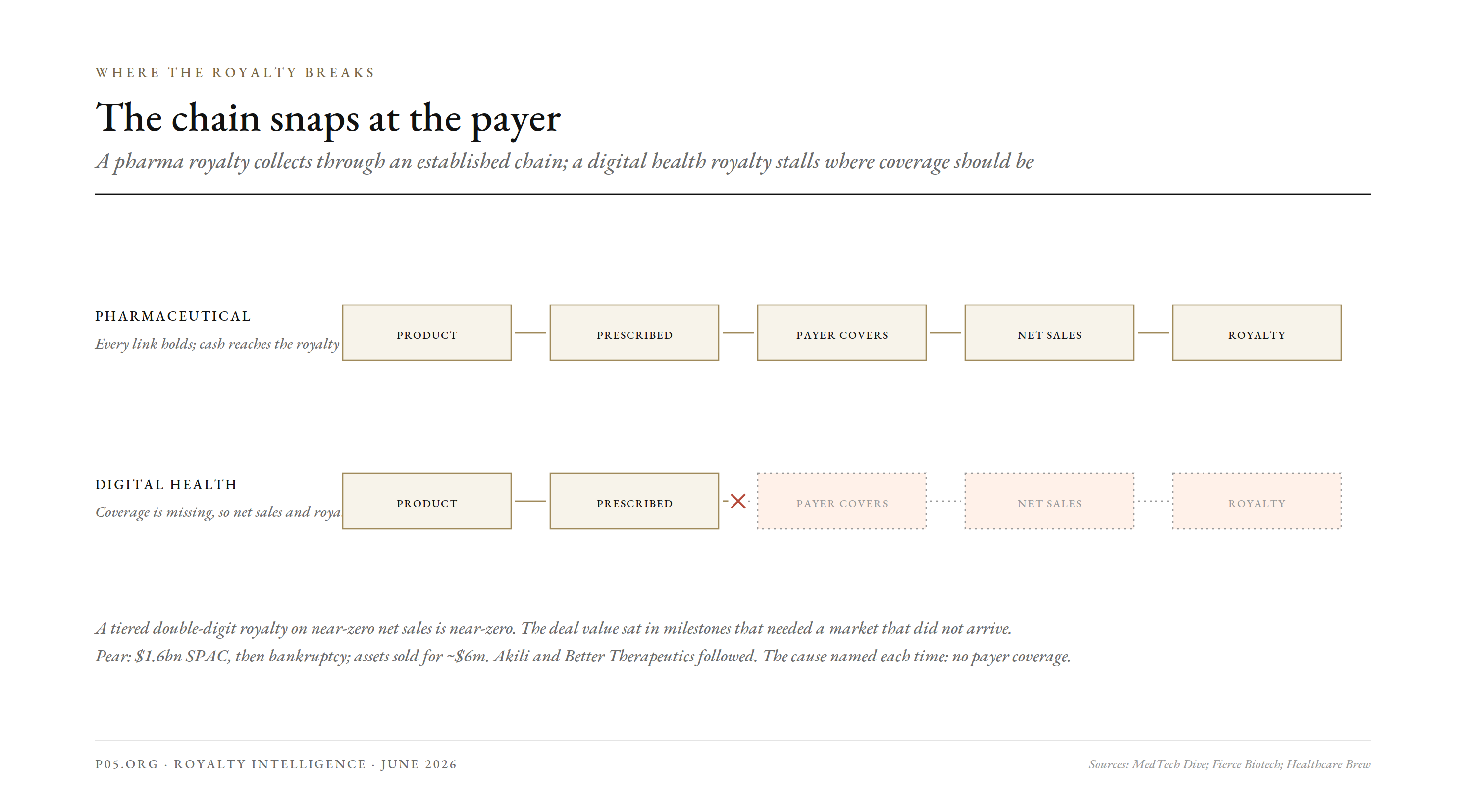

The break came at the royalty. A royalty on net sales is only worth something if there are net sales, and net sales require someone to pay for the product. That is where the template met the asset, and lost.

By April 2026, even the surviving flagship had been restructured: Boehringer Ingelheim took over commercialization of CT-155 and reworked the original marketing arrangement, a reminder that the commercial half of these deals has been the fragile half.

The reimbursement break ] Where the royalty breaks. A pharma royalty collects through scripts and payers; a DTx royalty depends on coverage that often does not exist.

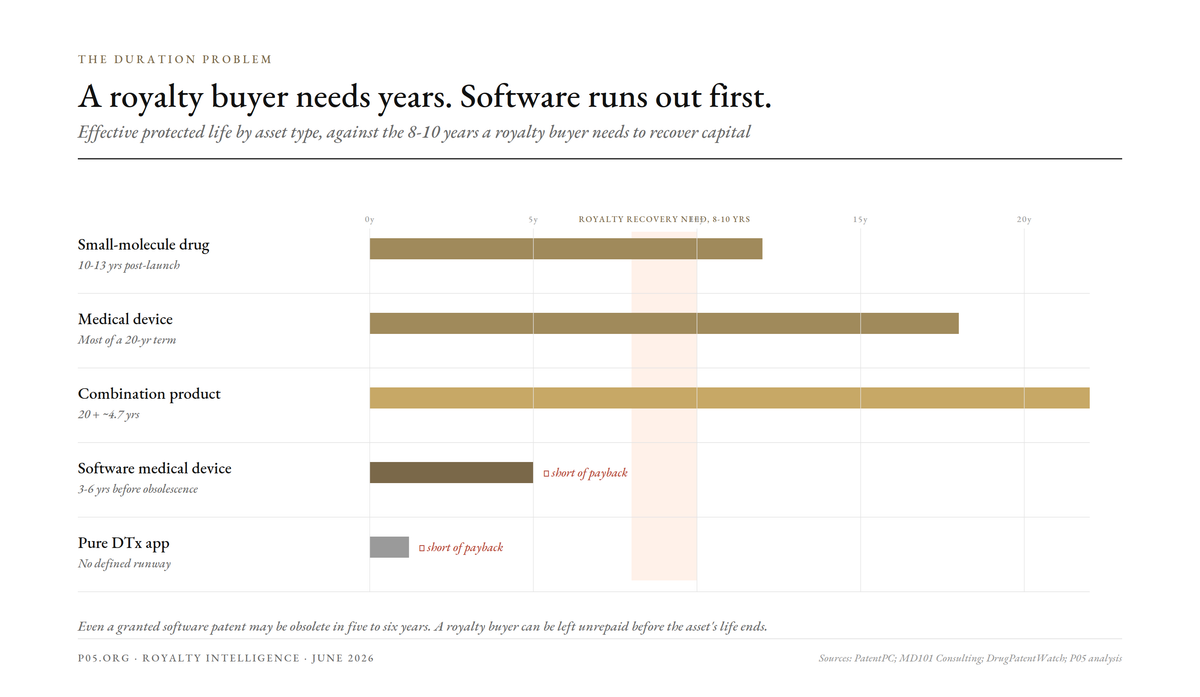

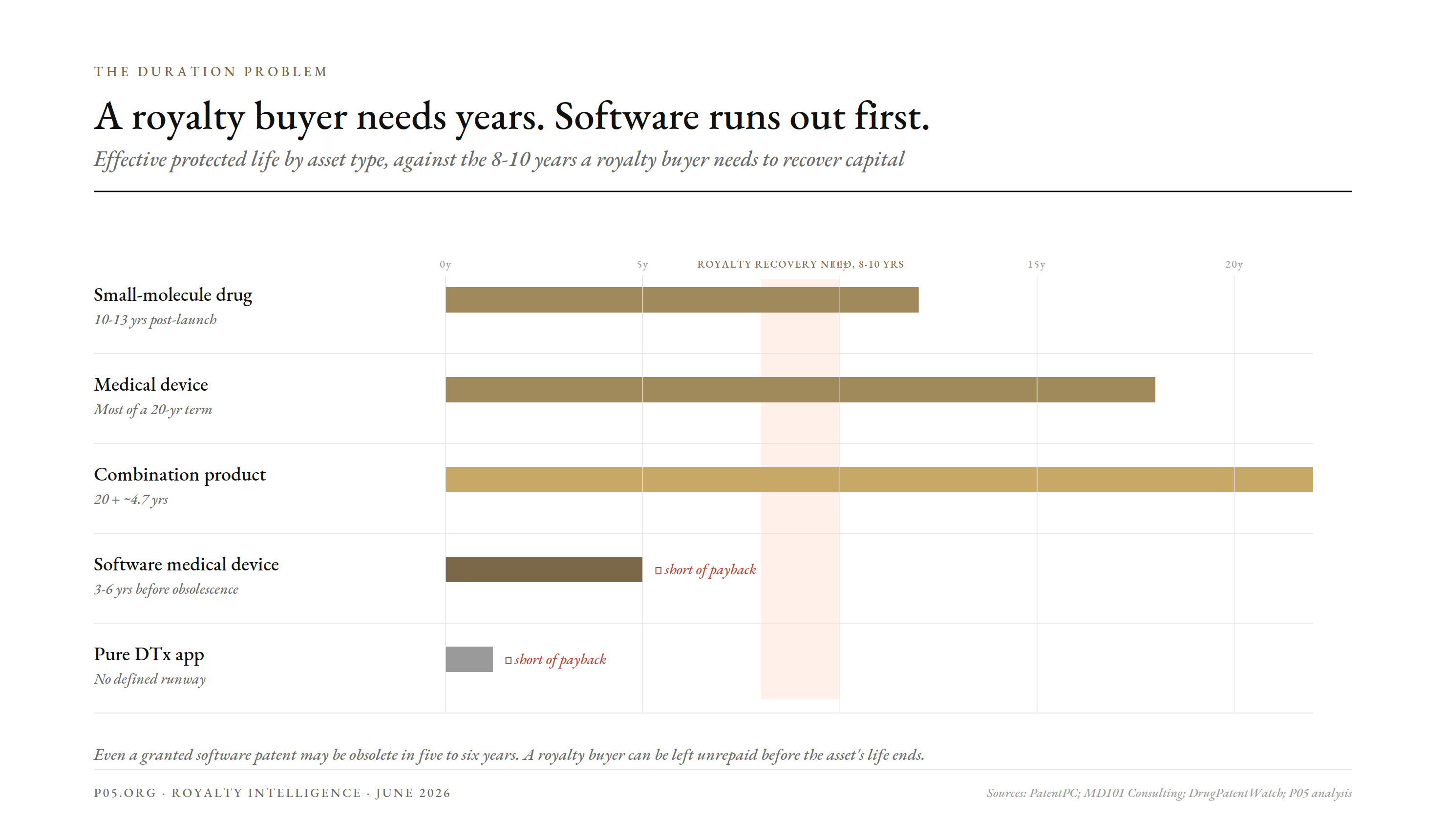

The term problem, in detail: a patent that expires before it matters

The single deepest reason a software royalty is hard to finance is duration, and it is worth going past the slogan. A royalty buyer is buying years. The instrument is a claim on cash flows out to a horizon, and the horizon is set by exclusivity.

A drug gives roughly twenty years from filing, often with the most valuable decade arriving after launch. Medical-device patents run the same twenty-year course, and combination products can stretch exclusivity by a further 4.7 years on average through device and formulation patents. That is a long, discountable runway.

Software does not get that runway, even when it is patented. The problem is twofold: getting a patent at all, and the patent outliving the product.

Pure algorithms are not patentable. Courts have held that an algorithm itself cannot be patented, only a device or process that uses it, which is why most digital therapeutics fall back on trade secret and copyright to protect the code rather than the clinical method. Trade secret protects nothing once a competitor independently builds the same function.

Even where a software patent issues, its effective life is short. One US appeals judge has argued the realistic useful life of a software patent is five to six years, not twenty, because the product cycle ends before the twenty-year clock does. The patent is granted on technology that is already being replaced.

The product itself ages even faster. Industry guidance puts the working lifetime of software as a medical device at three to five years for a typical build, and shorter still for machine-learning models, which need retraining and revalidation as clinical practice and data shift. Cloud products require constant major-version revalidation just to stay live.

Put those together and the contrast with pharma is stark.

| Asset | Nominal patent term | Effective protected life | Royalty runway |

|---|---|---|---|

| Small-molecule drug | 20 years from filing | 10-13 years post-launch | Long, discountable |

| Medical device | 20 years | Often most of the term | Long |

| Combination product | 20 years + ~4.7 | Extended | Long |

| Software medical device | 20 years (if granted) | 3-6 years before obsolescence | Short, uncertain |

| Pure DTx app | Often unpatentable | Trade secret only | No defined runway |

A royalty buyer typically needs to recover capital over eight to ten years. A drug royalty offers that comfortably. A software royalty, even a patented one, may be obsolete before the buyer is repaid. That is not a discount-rate problem; it is a duration problem, and it is close to disqualifying on its own.

The duration problem ] A royalty buyer needs years; software runs out first. Effective protected life by asset type against the 8-10 years needed to recover capital.

The payer problem is the whole problem

In pharma, the payer question is largely solved. A prescription is filled, an insurer or a pharmacy benefit manager pays, and the royalty flows off net sales through mature accounting. The plumbing exists.

In digital therapeutics, the plumbing barely existed at all. A doctor could prescribe an FDA-cleared app, and then no one would pay for it.

This is the opposite of the veterinary case. Vet products are cash-pay, which removes reimbursement risk entirely. Digital therapeutics tried to be reimbursed like drugs, but without the coding and coverage infrastructure drugs spent decades building.

The consequence was a direct hit to the royalty base. A tiered double-digit royalty on near-zero net sales is near-zero. The headline deal value sat almost entirely in milestones that required a commercial market that never arrived.

The failures make the point in sequence, and they are recent enough to matter. Pear Therapeutics built the first FDA-cleared prescription digital therapeutics, went public in a $1.6 billion SPAC, priced its apps above $1,000, and could not get them reimbursed.

It filed for bankruptcy in 2023. Its assets sold at auction for about $6.05 million, against 2022 revenue of $12.7 million and expenses over $136 million.

Akili, maker of the video-game ADHD therapeutic EndeavorRx, abandoned the prescription model for over-the-counter, then sold off its assets. Better Therapeutics shut down. The common cause, named repeatedly by the founders and the trade press, was a lack of payer coverage, not a lack of clinical evidence.

For a royalty investor the lesson is blunt. The asset can be FDA-cleared, clinically validated, and still produce no royalty, because the stream depends on a reimbursement decision the developer does not control.

The supply problem and the funding mismatch

Even setting reimbursement aside, the asset does not fund like a royalty for two further reasons.

The first is the moat problem, again, viewed from the buyer's side. A royalty buyer underwrites patent survivability and generic-entry timing. With software there is no patent wall to survive and no generic-entry date to model. There is only the risk that a better-funded competitor, or the customer's own IT department, rebuilds the function.

The second is churn. A pharmaceutical royalty erodes slowly and predictably. A subscription royalty can collapse in a single contract cycle if a health plan drops the product or an employer switches vendors. Duration is the asset in royalty finance, and software duration is short and behavioral.

This is why digital health raised venture capital, not royalty capital. The sector took billions in equity, $3.2 billion of DTx startup investment in 2021 alone, precisely because equity prices optionality and growth, while a royalty prices a defined, durable, contractible stream. The asset matched the former and not the latter.

| Why a DTx royalty is hard to finance | Mechanism |

|---|---|

| No patent wall | Copyright and trade secret protect code, not the clinical idea |

| No defined term | Subscription renews or churns; no expiry to discount to |

| Reimbursement dependence | Stream needs payer coverage the developer does not control |

| Churn risk | A stream can vanish in one contract cycle |

| Re-buildable function | Competitors or in-house teams can replicate the feature |

| Equity-shaped returns | Value is in growth optionality, which equity prices better |

What deals actually exist, and what shape they take

If you ask what financing happens in digital health today, the answer is clear, and it is not royalties. It is equity, M&A, and a small amount of recurring-revenue lending.

2025 was the sector's strongest financing year in some time: $14.2 billion of digital health funding, 195 M&A deals, up 61% on 2024, and a roughly 600% jump in private-equity healthtech spend. None of that capital arrived as a royalty.

The marquee events were equity exits. Five digital health companies went public: Hinge Health, Omada Health, Heartflow, Carlsmed, and Profusa. The two flagships show the profile investors actually fund.

| 2025 digital health exit | Profile | What it tells a financier |

|---|---|---|

| Hinge Health IPO | ~$432m revenue, 80%+ gross margin, 117% net dollar retention, FCF-positive, ~$3bn cap | Funded as premium SaaS equity, not a royalty |

| Omada Health IPO | $170m revenue (+38%), first positive adjusted EBITDA in Q3 2025, raised $150m | Equity on growth and a path to profit |

| Sword Health, private | Raised $40m at a $4bn valuation in June 2025, explicitly to delay its IPO | Equity optionality, not stream monetization |

| Sword / Kaia Health | $285m acquisition (2026) | Consolidation for scale, not a royalty purchase |

The pattern is unambiguous. Strong digital health businesses are valued at 3.8x to 10x ARR and monetized through IPO or acquisition. The cash flow is treated as equity, because it is inseparable from the operating company.

Where the underlying asset is weakest, the deals turn into distress. The 2026 M&A wave, Sword buying Kaia, Spring Health buying Alma, is partly about scale and partly about companies merging to extend runway after failing to reach breakeven alone. That is the opposite of a maturing royalty market; it is consolidation of operating businesses.

So the honest answer to which royalty deals exist is: almost none, outside the pharma-funded prescription therapeutics already discussed. The financeable event in digital health is an equity exit, not a royalty sale.

How the money actually flows in digital health

If the drug-style net-sales royalty mostly does not work, what does the real revenue look like? It is software revenue, and it is priced like software.

The dominant model is recurring subscription, usually per member per month or per employee per month, billed to a health plan, an employer, or a provider group. It is the SaaS playbook, applied to health.

Increasingly it is value-based: a portion of the fee is tied to outcomes, such as reduced readmissions or closed quality gaps, with bonuses or penalties attached. That aligns incentives, but it makes the cash flow even harder to predict, and therefore harder to finance as a fixed stream.

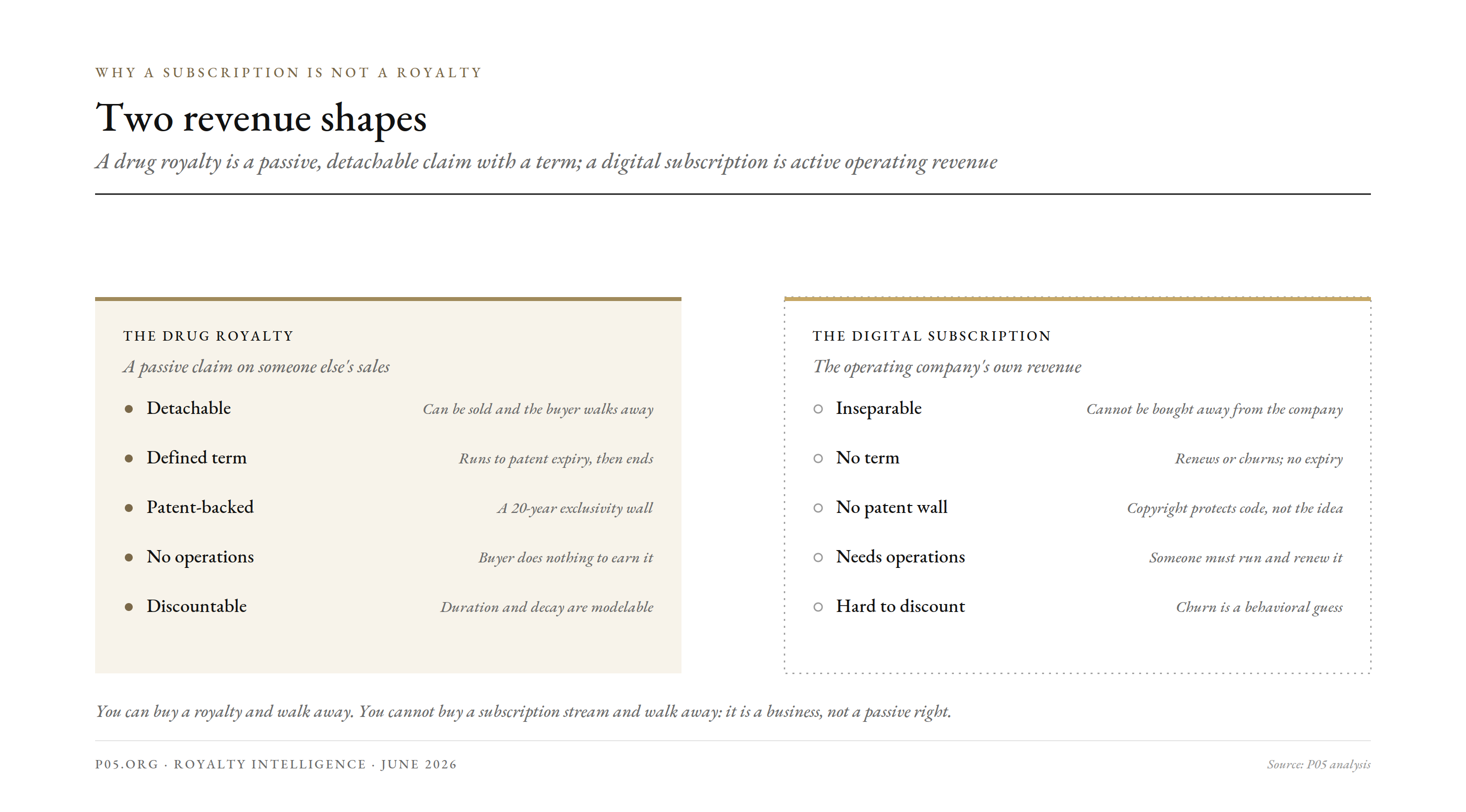

These models can be excellent businesses. Recurring PMPM revenue is the foundation of many durable digital health companies. But it is not a royalty in the financeable sense, because it is not detached from the operating company.

That is the crux. A drug royalty can be sold away from the company that discovered the drug, because it is a contractual claim on a third party's sales. A PMPM subscription is the operating company's own revenue, inseparable from its ongoing effort to deliver and renew the service.

You cannot buy the PMPM stream and walk away. Someone has to keep running the platform, supporting the customers, and winning the renewals. The cash flow is a business, not a passive right.

What the cash flow actually looks like

It helps to look at real numbers, because the shape, not just the size, is the point.

A successful digital health company today looks like Hinge Health, a musculoskeletal-care platform. For 2025 it guided to revenue of about $572-574 million, up 47%, with $118 million of free cash flow in the first three quarters and roughly $500 million of cash on the balance sheet. That is a strong, scaling SaaS business.

But look at how that revenue behaves. Hinge tells the SEC that for most contracts, the potential revenue per member is known within the first quarter of a member's first billable activity, with quarterly true-ups. The revenue is real and recurring, but it is contingent on enrolment, engagement, and renewal, the operating metrics of a live business.

That is the opposite of a royalty. A royalty is fixed by contract against a third party's sales and needs no further effort. Hinge's revenue needs continuous selling, onboarding, and retention. You cannot carve it off and sell it as a passive stream, because without the company running behind it, the stream stops.

The cash flow is also front-loaded with cost. Customer acquisition, integration with health plans, and clinical staffing all precede the revenue, and the revenue itself arrives monthly and can churn. This is a venture-and-growth-equity cash-flow profile, lumpy, operationally dependent, and optionality-rich, which is exactly why the sector raised equity, not royalty capital.

Two revenue shapes ] A royalty versus a subscription. The drug royalty is a passive claim with a defined term; the digital health subscription is active, operating revenue with no term.

Where a real royalty does exist

There is a narrow band where digital health does throw off a financeable, royalty-like stream. It is worth isolating, because it is where any financing market would start.

The cleanest case is the platform or component licensor. A company that licenses an underlying engine, an algorithm, a sensor-processing method, a validated digital biomarker, into many other companies' products earns a per-use or per-sale royalty across a diversified base. That is structurally close to the bioprocessing-platform royalties we have described elsewhere.

The second case is the pharma-funded prescription therapeutic that does reach reimbursement. If the coverage problem is solved, the Click-style tiered royalty on net sales behaves like a small pharma royalty, and could in principle be monetized like one. The structure is already pharma-shaped; it only ever needed the sales.

The third is intellectual-property licensing proper: a patented method or device-software combination licensed for a defined royalty and term. Where a genuine patent exists, for example around a novel sensor or a hardware-software medical device, the analysis reverts to the medical-device royalty case, which is firmer ground than pure software.

What these three share is the thing pure DTx lacks: a defined claim on someone else's sales, detachable from the licensor's own operations, ideally with real IP behind it. That is the financeable shape. Most of digital health does not have it.

Is there a playbook? Germany already runs one

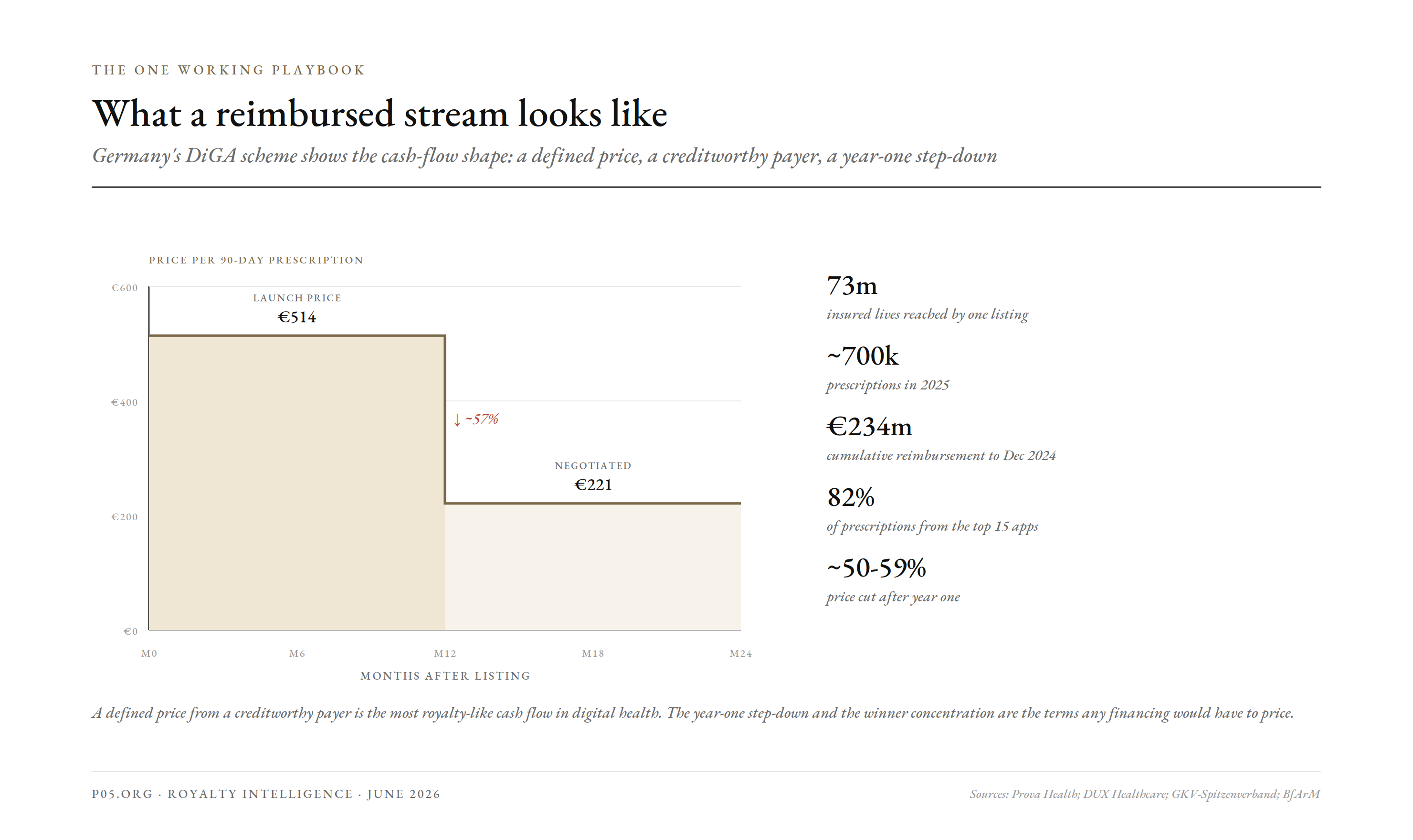

The recurring objection to a digital health royalty is the missing payer. Germany has spent five years proving what it looks like when that payer exists, and its DiGA scheme is the closest thing to a working playbook the sector has.

Under DiGA, a single decision by the federal regulator BfArM makes an approved app reimbursable across roughly 73 million statutory-insured lives, about 87% of the population. One listing, one price, one reimbursement decision, and the product is payable nationwide. That is the payer infrastructure US digital therapeutics never had.

The pricing mechanism is the interesting part for a royalty lens, because it is essentially a regulated net-sales schedule. A manufacturer sets a launch price, then after one year it is replaced by a negotiated price.

| DiGA pricing and volume | Figure |

|---|---|

| Insured lives reachable by one listing | ~73 million |

| Launch price, per 90-day prescription | median ~€514 (range €200-700) |

| Negotiated price after year one | median ~€221-227 |

| Typical year-one price cut | ~50-59% |

| Prescriptions, 2020/21 to 2022/23 | ~41,000 to ~209,000 |

| Prescriptions, 2025 | ~700,000 |

| Cumulative reimbursement to Dec 2024 | ~€234 million |

| Listed DiGAs (late 2025) | ~56-61 |

| Share of prescriptions from top 15 apps | ~82% |

Three features of that table matter for whether a royalty could ever sit on top of it.

First, the cash flow is real and contractually defined. A reimbursed DiGA earns a known price per prescription from a creditworthy payer, the statutory insurance system. That is a far more royalty-like stream than an uncertain US coverage decision.

Second, the year-one price cut is a built-in step-down, like a royalty tier in reverse. Any financing structured on DiGA revenue has to price that ~50% haircut after twelve months. It is modelable, which is what matters, but it is severe.

Third, the concentration. With the top 15 apps driving 82% of prescriptions, the financeable universe is a handful of winners, not the whole directory. Most listed DiGAs are provisionally listed and unproven, which is the same diligence problem royalty buyers face everywhere.

The working playbook ] What a reimbursed stream looks like. Germany's DiGA scheme: a defined price, a creditworthy payer, a year-one step-down.

So could there be a playbook? The components now exist, in pieces, across geographies. Germany supplies the payer and a defined price. The US, with its new Medicare DMHT codes and the FDA TEMPO pilot, is assembling the same infrastructure a decade later. The pharma-style licence, from the Click deals, supplies the royalty contract.

The missing piece is an aggregator. No single reimbursed app throws off enough to interest an institutional royalty buyer, the same scale problem as veterinary royalties. A workable playbook would bundle royalties or revenue interests across many reimbursed products and geographies, price the year-one step-downs and the churn, and lean on the handful of proven winners rather than the long tail.

That is a structuring problem, not an impossibility. But it requires two things the sector still mostly lacks: durable reimbursement in more than one major market, and a real exclusivity moat on the underlying products. Until both arrive together, the playbook stays theoretical.

Are there precedents? Yes, but for the stream, not the royalty

The instinct to finance recurring digital revenue is not new, and there are real precedents. They just point to a different instrument than a royalty.

The closest precedent is recurring-revenue securitization. Starting around 2020, Pipe built a marketplace that treats SaaS subscriptions as an asset class, letting software companies sell future subscription payments for upfront cash. ARR-based lending, advancing capital against annual recurring revenue, is now a mainstream financing route for subscription businesses.

This matters because most digital health revenue is exactly that: recurring subscription income. The precedent for financing it already exists. But note what it is. It is lending or advancing against a company's own forward revenue, with recourse to that company. It is not the purchase of a detached, passive royalty.

The second precedent is the one this whole series keeps returning to: the diversified royalty trust. Pharmaceutical royalty securitization and music-catalog ABS both took many individual streams, none financeable alone, and pooled them into rated, tradable paper. The lesson is that aggregation, not any single asset, is what creates a financeable instrument.

The third precedent is the pharma-style prescription therapeutic royalty itself, the Click model. Where a digital therapeutic is licensed to a pharma company and earns a tiered royalty on net sales, the instrument is already a royalty. It simply needs the sales, which means it needs reimbursement.

| Precedent | What it finances | Relevance to digital health |

|---|---|---|

| Pipe / ARR lending | A company's own recurring revenue | Direct: most digital health revenue is recurring; but it is lending, not a royalty |

| Pharma royalty securitization | Pooled drug royalties as rated paper | Aggregation model for many small streams |

| Music-catalog ABS | Pooled song royalties | Proof that non-traditional royalties can be securitized if diversified |

| Pharma-funded DTx licence | Tiered royalty on net sales | Already a royalty; needs reimbursement to produce sales |

The precedents converge on a single conclusion. The way to finance digital health is not to invent a software royalty from nothing. It is to either advance against recurring revenue, as Pipe does, or to aggregate the genuinely royalty-shaped streams, the reimbursed prescription therapeutics and the platform licences, into a pool, as pharma and music did.

What 2026 changes

The reimbursement wall is the binding constraint, and 2026 is the first year it has visibly cracked.

In 2025, the US Centers for Medicare and Medicaid Services introduced Digital Mental Health Treatment codes, a Medicare pathway to pay for qualifying digital therapeutics. Seven digital mental health devices became eligible.

The early verdict is mixed. CMS did not set a single national rate, leaving it to regional contractors, and observers say uptake has not yet met its potential. A coding pathway is necessary, but not sufficient; the rate and the adoption still have to follow.

Two further developments point the same way. The FDA launched the TEMPO pilot in December 2025, aimed at encouraging uptake of technology-enabled care. And Germany's DiGA fast-track reimbursement scheme has, for several years, shown that a national coverage pathway can produce real prescription volume.

If, and it remains an if, reimbursement becomes routine, the central objection to a digital therapeutic royalty weakens. A reliably reimbursed, FDA-cleared therapeutic with a tiered royalty on net sales starts to look like a small, financeable pharma-style stream.

That still leaves the moat and the term problems. Reimbursement fixes the payer, but not the missing patent wall or the absence of a defined exclusivity period. So even a post-2026 digital therapeutic royalty would be a weaker instrument than a drug royalty: financeable, perhaps, but shorter, softer, and more exposed to competition.

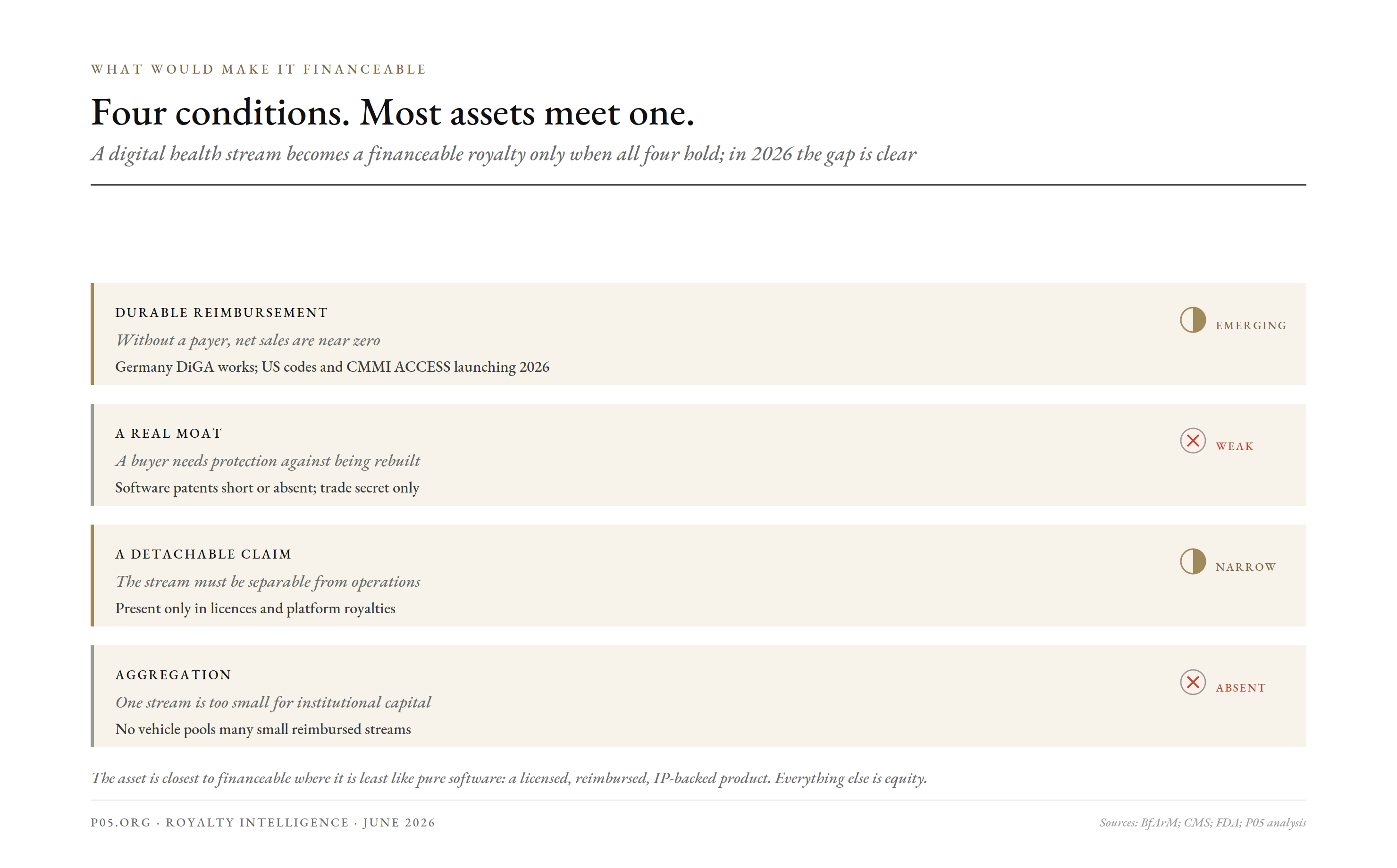

What would actually make it financeable

Pulling the mechanics and the precedents together, a digital health stream becomes financeable as a royalty when four conditions hold. Today, most assets meet one or two. The gap is the checklist.

| Condition | Why it is required | Status in 2026 |

|---|---|---|

| Durable reimbursement | Without a payer, net sales are near zero | Emerging: Germany DiGA works; US codes and CMMI ACCESS launching |

| A real moat | A buyer needs protection against being rebuilt | Weak: patents short or absent; trade secret only |

| A detachable claim | The stream must be separable from operations | Present only in licences and platform royalties |

| Aggregation | One stream is too small for institutional capital | Absent: no aggregator exists |

The financeability checklist ] Four conditions, and most assets meet one. A digital health stream becomes a financeable royalty only when all four hold.

The first condition is the one in motion. Germany's DiGA shows durable reimbursement is achievable. The US is assembling it: the new Medicare DMHT codes, the FDA TEMPO pilot, and the CMMI ACCESS Model launching in July 2026, a ten-year Medicare value-based pathway for digital health interventions. Reimbursement is the condition most likely to be solved this decade.

The second, the moat, is the hardest and may never fully resolve for pure software. It is why the financeable band is narrow: the platform licence, the genuine device-software patent, and the pharma-funded therapeutic, all of which carry more protection than a standalone app.

The third is a structuring choice. A licence to a third party is detachable; a company's own subscription is not. An arranger would have to work with the licence-shaped streams, or convert recurring revenue into a contractual interest a buyer can hold, which is closer to the Pipe model than to a pharma royalty.

The fourth, aggregation, is the missing institution, and it is the same gap we found in veterinary royalties. No one has built the vehicle that pools many small, reimbursed digital health streams across products and geographies into something an institutional buyer can underwrite once. The precedents, pharma and music ABS, show it can be done. It simply has not been done here.

Put plainly: the asset is closest to financeable where it is least like pure software and most like a licensed, reimbursed, IP-backed product. The further a digital health stream sits from that description, the more it is an operating business to be funded with equity, and the less it is a royalty to be bought.

The verdict

Digital health adopted the pharmaceutical royalty template before it had a pharmaceutical-grade asset to put inside it. The headline deals, Otsuka and Boehringer with Click, were structured like biotech licences and carried biotech-scale numbers. The chassis was sound; the cargo was not.

The asset fails most of the financeability tests. There is no patent wall, so no protected stream. There is no defined term, only subscription churn. And the payer, for most of the sector's history, simply was not there, which is what turned a clinically validated field into a sequence of bankruptcies.

Where a real royalty exists in digital health, it is in the narrow band that does not look like pure software: platform and component licensing, genuine IP, and the pharma-funded therapeutic that actually gets reimbursed. Everything else is operating SaaS revenue, which is a fine business but not a detachable, financeable royalty.

As of 2026, the one variable genuinely in motion is reimbursement. The new Medicare codes and the FDA pilot could, over time, supply the missing payer and turn the best prescription digital therapeutics into small, financeable streams. Whether that is enough to overcome the absent patent wall and the absent term is the open question.

For now, the honest conclusion is the mirror image of our veterinary one. In vet, the asset is sound and the financing market is merely thin. In digital health, the financing instinct was there from the start, the deals were even pharma-shaped, but the underlying asset was not yet one a royalty could safely be built on.

All information in this report was accurate as of the research date and is derived from publicly available sources including regulatory guidance, company disclosures, SEC filings, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.