How Veterinary Royalty Deals Are Built

Why animal-health royalties are structured the way they are: FDA-CVM regulatory triggers, species fragmentation, the cash-pay market, the option-to-acquire lifecycle that keeps eliminating royalties, and the deleveraging monetizations, with the numbers and the deal anatomy.

Our 2023-2025 deal census mapped what happened in veterinary royalties, deal by deal. This piece asks a different question: how are these deals actually built, and why do they look the way they do?

The veterinary royalty market is small, an estimated $650 million to $975 million a year, against a human-pharma royalty market north of $20 billion. But it is not just a scaled-down copy of human pharma. The structures differ in specific, mechanical ways, and those differences are the point.

This is a mechanics piece, not a market survey. It works through six structural features that define how a vet royalty is assembled, then asks why, given all of them, the market has stayed so thin, and what would change that. The six: the regulatory triggers that set the milestones, the species fragmentation that splits the stream, the cash-pay market that changes the risk, the acquisition reflex that keeps killing royalties, the monetization trade that turns them into cash, and the shallow patent cliff that lengthens the tail.

The deals named here appear as illustrations of structure, with their disclosed terms, not as a catalogue. For the full catalogue, see the census.

To frame the whole piece, here is how a veterinary royalty differs from its human equivalent, feature by feature.

| Mechanic | Human pharma | Veterinary | Consequence for the royalty |

|---|---|---|---|

| Regulator | FDA-CDER | FDA-CVM or USDA-CVB | Different, shorter milestone ladder |

| Clinical ladder | Phase I/II/III | Target-animal safety, pivotal field study | Fewer, smaller, earlier milestones |

| Approval scope | One species (human) | Per species, separately | Stream fragments into parallel programs |

| Who pays | Insurers, PBMs | Cash, owner or producer | No reimbursement risk; capped ceiling |

| Blockbuster ceiling | $5-10bn+ | $500m-1.5bn | Lower absolute royalty, similar rate |

| Preferred deal shape | License, often standalone | Option to acquire | Royalty retired by buyout |

| Patent cliff | Steep, 80-90% year-one erosion | Shallow, 20-40% over years | Longer, more valuable royalty tail |

| Typical exit | Royalty persists | Acquisition or monetization | Few mature streams accumulate |

The veterinary milestone ladder versus the human one. Vet deals compress the human Phase I/II/III ladder into a shorter set of regulatory triggers.

1. The milestones follow a different regulator

A royalty deal is mostly a schedule of payments tied to events. In human pharma, those events track the clinical ladder: an IND, then Phase I, II, and III, then an NDA, then approval, then sales thresholds. The milestones map onto that ladder.

Veterinary deals map onto a different one. The regulator is the FDA's Center for Veterinary Medicine (CVM), not CDER, and for biologics it can instead be the USDA's Center for Veterinary Biologics. The names rhyme with the human system, an INAD instead of an IND, a NADA instead of an NDA, but the path is shorter.

There is no three-phase human-trial paradigm. Efficacy can often be confirmed early, in a controlled study using an established animal model of the disease, in the target species itself. A field study of a few hundred animals then confirms it. The probability of late failure is lower than in human development.

So the milestone triggers are different. Instead of Phase I/II/III readouts, a vet deal pays on target animal safety, pivotal efficacy, manufacturing scale-up, regulatory submission, and approval. Those are the rungs.

This compression shows up directly in the numbers. The table below sets the typical veterinary milestone and royalty structure against the human one, drawn from disclosed terms in our census and standard human-pharma benchmarks.

| Deal component | Veterinary range | Human pharma range | Ratio |

|---|---|---|---|

| Upfront, early-stage candidate | $500k-2m | $5-50m | ~10x |

| Upfront, approved product | $10-45m | $50-500m | ~5-10x |

| Development milestones (cumulative) | $5-20m | $50-200m | ~10x |

| Regulatory milestones (cumulative) | $10-30m | $50-150m | ~5x |

| Commercial milestones (cumulative) | $20-95m | $100-500m | ~5x |

| Total milestone potential | $80-130m | $500m-2bn | ~10x |

| Royalty rate, novel biologics | 10-18% | 12-20% | comparable |

| Royalty rate, approved pharma | 5-15% | 5-15% | comparable |

Notice the pattern. The absolute figures are roughly an order of magnitude smaller, but the royalty rates as a percentage of net sales are comparable. The difference is the base, not the rate.

It also changes the discounting. A shorter, less failure-prone path means the expected value of a milestone arrives with less time-and-probability decay. The royalty buyer is underwriting a different risk shape, not just a smaller number.

Two disclosed deals anchor the ranges. The Kindred Biosciences KIND-030 license to Elanco, a canine biologic, carried a $500,000 upfront, a low-to-high-teens royalty (10-18%), and roughly $110 million in total milestone potential. The Aratana Galliprant deal with Elanco carried a $45 million upfront against $83-85 million in sales milestones, at the high end of veterinary upfronts because the product was already approved.

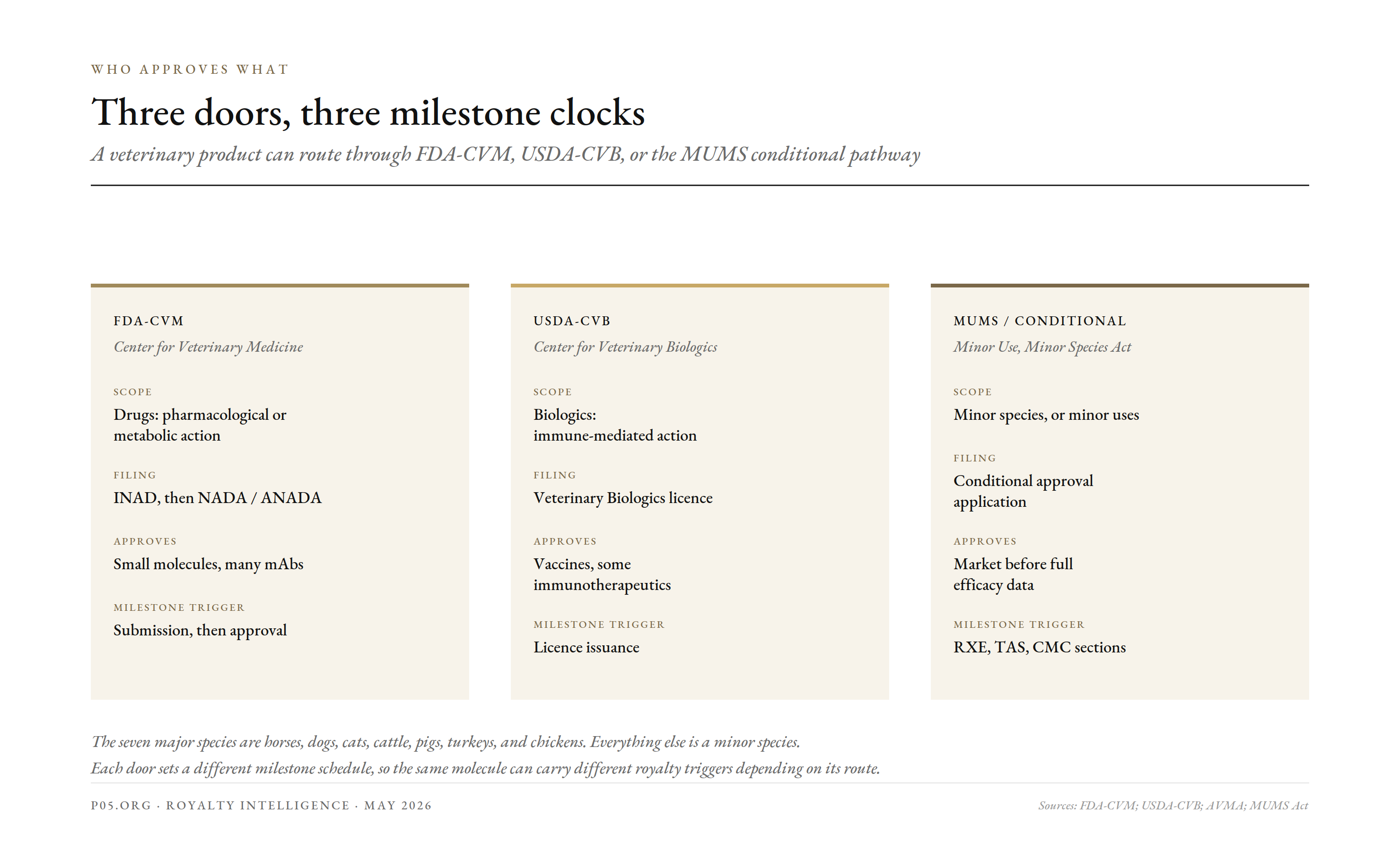

Who approves what. The veterinary product splits across FDA-CVM, USDA-CVB, and the MUMS conditional pathway, each setting different milestone triggers.

The conditional-approval wrinkle

Veterinary regulation has a feature human pharma mostly lacks, and it matters for milestone timing. Under the MUMS Act, drugs for minor species, or for minor uses in a major species, can reach the market on conditional approval, before full effectiveness data is complete.

The seven major species are horses, dogs, cats, cattle, pigs, turkeys, and chickens. Everything else is a minor species. A sheep or goat drug qualifies for the faster path on that basis alone.

The clearest 2026 example is Loyal's canine longevity program. As of January 2026, LOY-002 had cleared two of the three technical sections the CVM requires for a conditional launch: Reasonable Expectation of Effectiveness, and Target Animal Safety, with manufacturing the last to clear.

That three-section structure, RXE, TAS, and CMC, is itself a milestone schedule. A deal on a conditional-approval asset can pay on each section's acceptance, a sequencing no human deal has. It lets a royalty start flowing on a conditional launch years before full approval, which front-loads the cash flows a buyer is discounting.

| Conditional-approval section | What it certifies | Milestone analog |

|---|---|---|

| RXE, Reasonable Expectation of Effectiveness | Plausible efficacy on partial data | Proof-of-concept payment |

| TAS, Target Animal Safety | Safety in the target species | Safety milestone |

| CMC, manufacturing | Consistent, scalable production | Scale-up milestone |

| Conditional approval granted | Market entry before full data | Launch milestone, royalty begins |

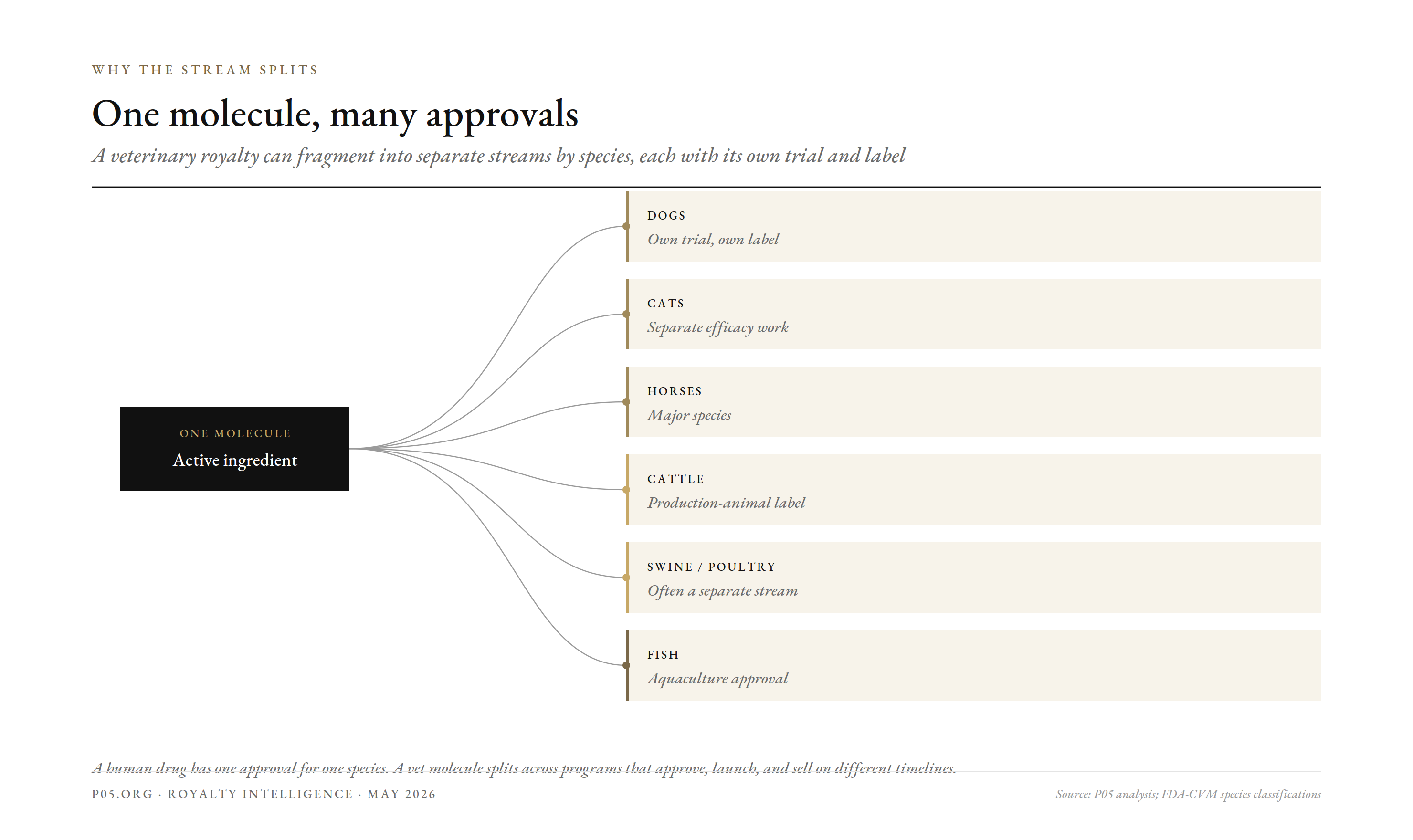

One molecule, many approvals. A veterinary royalty can split into separate streams by species, each with its own trial, label, and milestone.

2. The royalty fragments by species

A human drug is approved for one species. A veterinary molecule is not.

The same active ingredient often needs separate approvals for dogs, cats, horses, cattle, swine, poultry, and fish. Each species can require its own safety and efficacy work, its own label, and its own regulatory submission. Each is potentially a separate milestone trigger, and sometimes a separate royalty stream.

This fragments the asset in a way human royalties are never fragmented. A single human approval covers the whole human market. A vet molecule's value is split across species programs that approve, launch, and sell on different timelines.

For a royalty buyer this cuts both ways.

| Effect of species fragmentation | For the licensor | For the royalty buyer |

|---|---|---|

| Multiple approvals | More milestone triggers to earn | More events to diligence |

| Staggered launches | Revenue arrives in waves | Cash flows harder to model |

| Per-species risk | A feline setback spares the canine program | Built-in diversification |

| Smaller per-species markets | No single approval unlocks full value | Lower peak per stream |

| Contractible separately | Can license by species or territory | Must specify exactly what is bought |

The contract has to reflect this. A worldwide, all-species license is one structure; a species-limited or territory-limited license is another, and territory carve-outs, often for Asia, are common. The right being sold has to specify which species and which geographies, because those are separable assets.

The reverse case is the cross-species jump, where a compound developed in animals is licensed for humans, or the other way. Elanco's monepantel, a sheep dewormer, was licensed to Neurizon for human ALS for $9.75 million in development milestones and $65 million in sales milestones. That deal lives on a human milestone ladder again, with its larger payments, even though the molecule started on the veterinary side.

3. Cash-pay changes the credit

The single biggest difference from human pharma is who pays at the counter. There is no pharmacy benefit manager, no insurer negotiation, no formulary. The pet owner or the producer pays cash.

That removes a whole risk that dominates human royalty underwriting. A human drug royalty lives or dies on reimbursement: coverage decisions, rebates, net-to-gross erosion, payer step-edits. None of that applies to a companion-animal product bought over the counter at a clinic.

The upside is cleaner, more predictable demand, and almost no pricing-power risk from payers. Pet spending is also relatively recession-resilient. For a royalty on an approved companion-animal product, the cash flow is unusually direct.

The offset is the ceiling. Cash-pay means the manufacturer cannot lean on an insurer to absorb a high price, so unit economics are bounded by what owners will pay. The biggest veterinary products top out far below human blockbusters.

| Risk or feature | Human pharma royalty | Veterinary royalty |

|---|---|---|

| Reimbursement risk | High, dominates underwriting | Effectively none |

| Pricing power | Negotiated with payers | Bounded by owner willingness to pay |

| Demand cyclicality | Moderate | Low, pet spend resilient |

| Peak product sales | $5-10bn+ | $500m-1.5bn |

| Exclusivity erosion | Off-label restricted | AMDUCA permits extra-label use |

| Generic pathway | ANDA | ANADA, similar, smaller markets |

So the royalty rate can match human deals, biologics and monoclonal antibodies still command 10-18%, but the base it applies to is capped lower. A 15% royalty on a $100 million vet product is $15 million a year. The same rate on a $1 billion human drug is $150 million. The percentage is similar; the absolute is not.

The ceiling is visible in the actual leaders. Zoetis's osteoarthritis-pain antibodies, Librela for dogs and Solensia for cats, and franchises like Apoquel and Simparica are the category's biggest sellers, in the hundreds of millions to perhaps $1.5 billion. A royalty on even a best-in-class vet product is sized accordingly.

There is one more exclusivity quirk. Under AMDUCA, veterinarians can legally prescribe approved drugs extra-label in many circumstances. That can erode the practical exclusivity a royalty implicitly relies on, in a way the more restrictive human off-label rules do not.

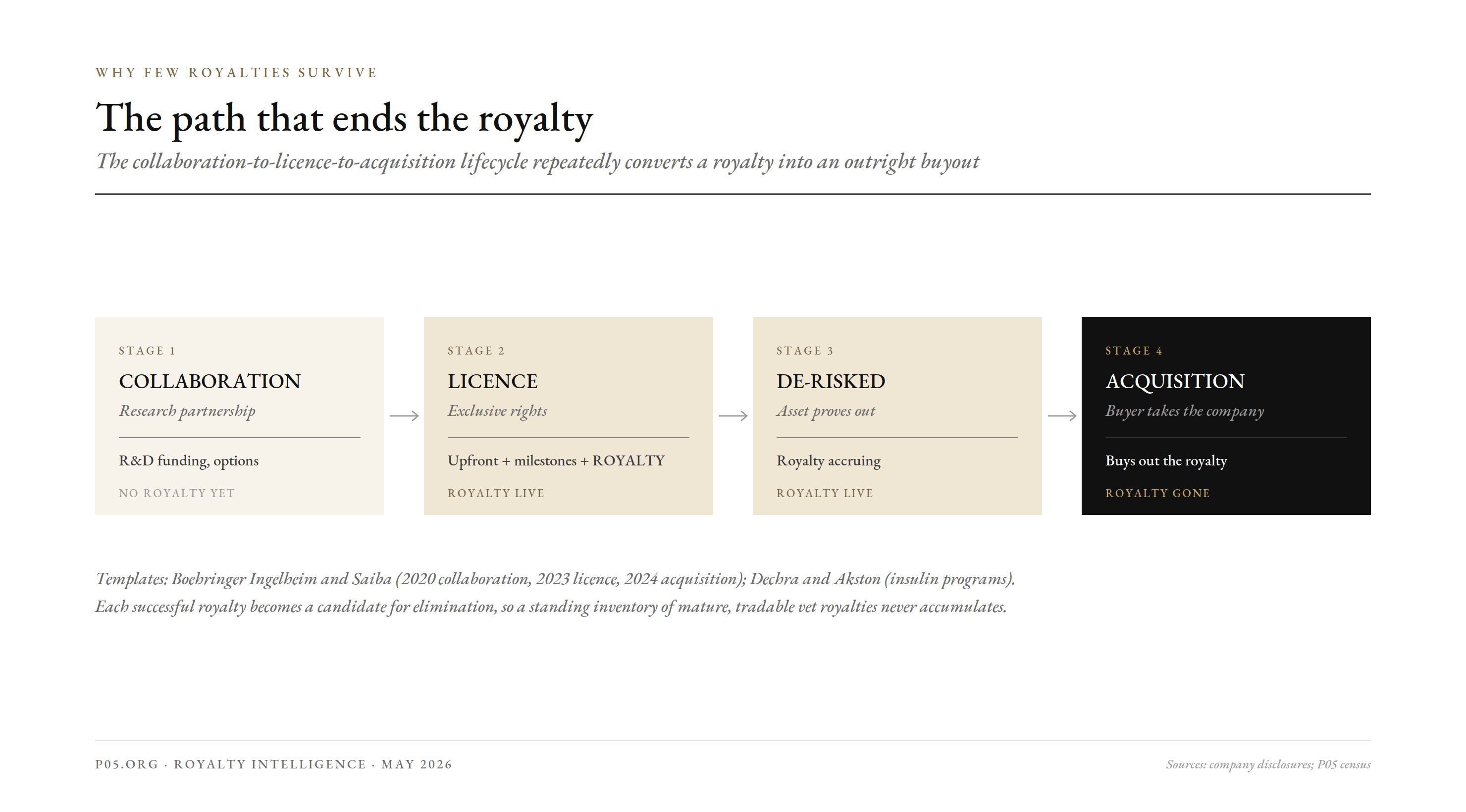

Why so few royalties survive. The collaboration-to-licence-to-acquisition path repeatedly converts a royalty into an outright purchase.

4. The structure that keeps killing the royalty

Here is the central mechanical fact of veterinary royalties: the industry's preferred deal shape is designed to end them.

A royalty is an ongoing obligation. It shares future margin with an outside party for the life of the patent. A large animal-health company with the balance sheet to do so would usually rather own the asset outright and keep the whole margin. So it buys.

This is why our census found acquisitions so dominant. When Elanco bought Kindred Biosciences for $444 million in 2021 and Aratana Therapeutics for $234 million in 2019, part of the explicit logic was to eliminate the royalties it would otherwise owe on KIND-030 and Galliprant. The purchase retires the royalty.

The more revealing structure is the staged one: collaboration, then license, then acquisition. It lets an acquirer de-risk in steps, and end with no royalty at all. The two clearest templates run as follows.

| Stage | Boehringer Ingelheim and Saiba | Dechra and Akston |

|---|---|---|

| Collaboration | 2020 research partnership with options | 2019 canine, 2021 feline co-development |

| License | June 2023 exclusive license on a VLP vaccine, upfront plus milestones plus royalties | Licensing on long-acting pet insulins |

| Acquisition | September 2024 full buyout | 2024 outright acquisition of the programs |

| Royalty outcome | Bought out in the acquisition | Bought out in the acquisition |

Boehringer Ingelheim's path with Saiba Animal Health is the template: a research collaboration, then an exclusive license with royalties, then a full acquisition that bought out those very royalty obligations. Dechra's path with Akston Biosciences ran the same way. The royalty was a bridge, not a destination.

For the licensor, this is often the goal, not a loss. The royalty is the placeholder value that an eventual buyout crystallizes. The option-to-acquire is the mechanism that turns a small, uncertain royalty into a larger, certain lump sum.

But the consequence for the market is structural. Every successful royalty is a candidate for elimination by acquisition, which is one reason a standing inventory of mature, tradable veterinary royalty streams never accumulates the way it does in human pharma.

There is a subtler version still. Even in acquisitions, an academic licensor can retain a royalty. When Ceva acquired the UPenn spin-out Scout Bio, UPenn kept a royalty interest on the licensed IP. The university's stream survives the corporate buyout, because it sits one layer below the company.

5. When a royalty does get monetized

The one place a veterinary royalty behaves like a human one is monetization, and even there the motive is distinctive.

The reference deal is Elanco and Blackstone. In 2025, Elanco sold the US royalty and milestone rights on lotilaner, its Credelio molecule licensed to Tarsus for the human eye drug XDEMVY, for $295 million.

Look at how that deal was carved. This is the anatomy of a single monetization.

| Element | Terms |

|---|---|

| Asset | US royalty on lotilaner, via XDEMVY (Tarsus) |

| Upfront to Elanco | $295 million cash |

| Royalty rate sold | Tiered mid-single-digit, estimated 4-6% |

| Royalty term | April 2025 through 2033 |

| Geography sold | United States only |

| Retained by Elanco | All ex-US royalties; all new human indications; all veterinary rights |

| Buyer's motive | Long-dated, predictable cash flow |

| Seller's motive | Immediate cash for debt reduction |

That carve is the mechanics in miniature. A royalty can be split by geography, by indication, and by species, and each slice can be sold separately. Elanco sold the most predictable slice, the US human ophthalmic stream, and kept the optionality.

The numbers behind it have since validated the buyer's thesis. XDEMVY generated $451.4 million in net sales in 2025, up more than 150% year over year, with Tarsus guiding to peak sales above $2 billion. At an estimated 5% rate, the US stream alone implies roughly $20-25 million a year and rising, against Blackstone's $295 million outlay.

The motive on the sell side was deleveraging. Elanco converted a passive, long-dated stream into immediate cash to pay down debt, targeting lower net leverage. The royalty was worth more to it as a lump sum today than as a trickle to 2033. That debt-reduction driver, rather than a thesis about the asset, is what powers most veterinary monetizations.

It is also why these deals are rare. They tend to require an unusual setup: a veterinary company that happens to hold a human-drug royalty, with a balance-sheet reason to sell it. That is a narrow intersection, and it is why veterinary-origin monetizations remain occasional rather than routine.

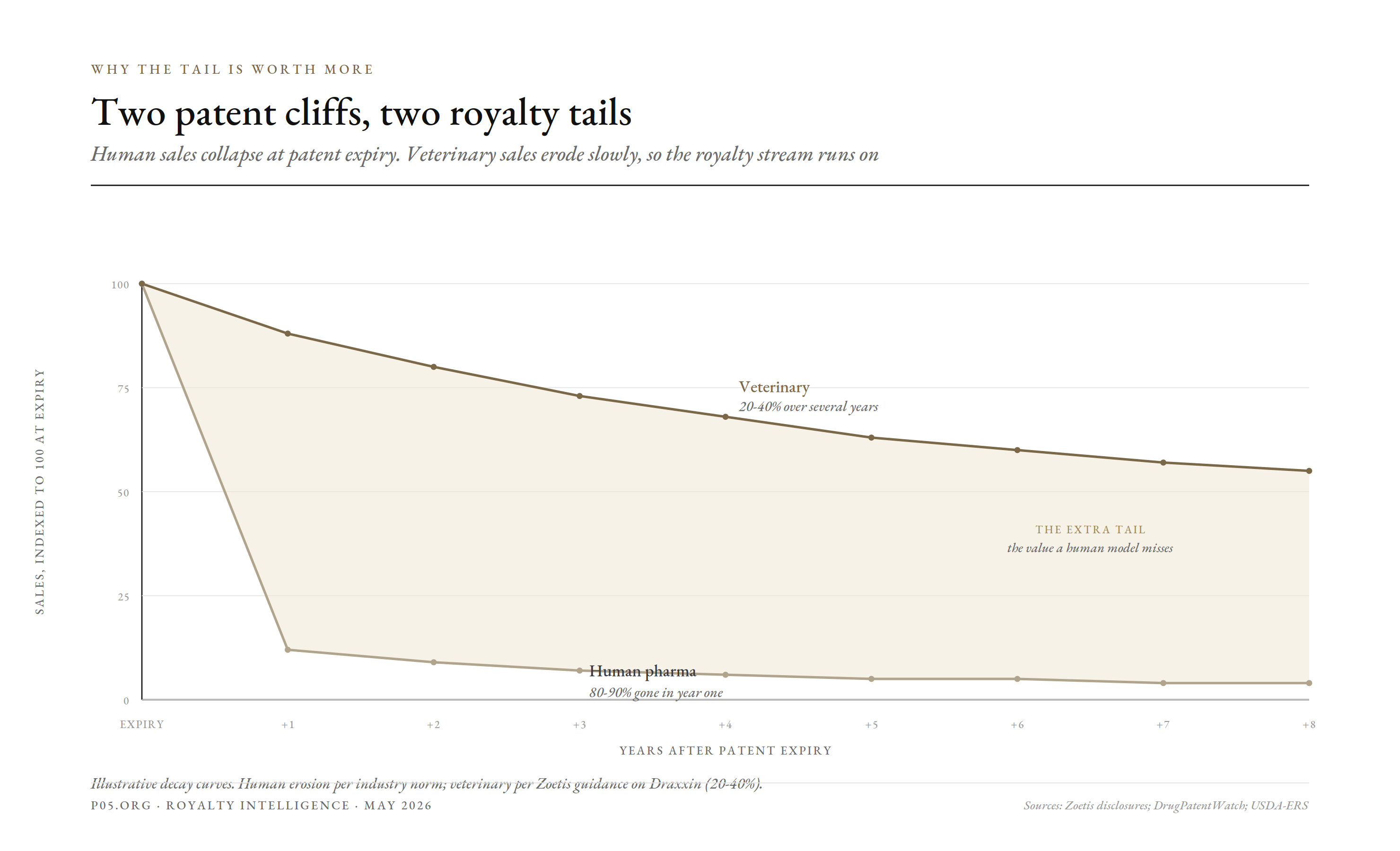

6. The patent cliff is shallower, so the tail is worth more

A royalty's value is not just its peak. It is the whole discounted stream, including the years after patent expiry. This is where veterinary royalties diverge most from the human intuition, and it is easy to get wrong.

In human pharma, the patent cliff is brutal. A small-molecule blockbuster typically loses 80 to 90% of revenue in the first year of multi-source generic competition. The royalty tail past expiry is, for modeling purposes, close to worthless.

Veterinary products do not fall like that. The erosion is far slower, and sometimes barely happens at all.

Two patent cliffs, two royalty tails. Human sales collapse at expiry; veterinary sales erode slowly, so the stream runs on.

The clearest disclosed example is Zoetis's Draxxin, a cattle and swine antibiotic and once its largest livestock product. When it went off-patent, Zoetis guided to a decline of only 20 to 40%, spread over several years, not a one-year collapse. At the extreme, Terramycin is still sold roughly six decades after its patent expired.

The right mental model is the branded generic. In human pharma, a brand near patent loss can sometimes hold a price premium on loyalty alone, the strategy behind Rx-to-OTC switches, where brand equity survives the cliff. In veterinary medicine that is not a clever strategy; it is the default state of the whole market.

Draxxin makes the point in a hard case. After its patent lapsed, an unusually aggressive 17 generics won marketing authorization, far more than the handful most antibiotics attract. Even into that crowded field, the Zoetis brand kept meaningful share and pricing, which is exactly why the company guided to a 20-40% decline rather than a collapse.

So a post-patent veterinary product behaves like a branded generic that never fully de-brands. Sales stay broadly similar, at a modest discount, because the vet still reaches for the trusted name and the owner still pays cash for it. The originator keeps a durable, premium-priced tail instead of watching the franchise evaporate.

Several structural features, most of them already in this piece, combine to flatten the cliff.

| Why the vet cliff is shallow | Mechanism |

|---|---|

| No PBM or insurer | Nothing forces substitution to a generic at the counter |

| Direct dispensing | Vets often prescribe and dispense, so the brand stays in the clinic routine |

| Brand loyalty | Owners and producers prize quality and safety; loyalty outlives the patent |

| Thin generic supply | Generics are only ~10% of dispensed animal-health products |

| No global generic major | Small per-product markets do not attract a well-capitalized generic giant |

| Rational pricing | The few generic entrants tend not to push prices to the floor |

| Chronic and preventive use | Parasiticides, dermatology, and pain franchises generate recurring routine demand |

| Branded-generic persistence | Even with generics present, the brand holds share and a price premium |

Zoetis says this directly in its own risk disclosures: there is no large global animal-health generics company, because of small per-product markets, direct distribution to veterinarians, and the self-pay nature of the business, and as a result significant brand loyalty often continues after the loss of patent and regulatory exclusivity.

For a royalty buyer, this is the most underappreciated feature of the asset class, and it runs in the buyer's favor.

The conventional human-royalty model writes the stream down to near zero at patent expiry. Applied to a veterinary royalty, that model understates the asset, because the post-expiry years still carry meaningful, slowly-eroding sales. The duration of a vet royalty is effectively longer than its patent term implies.

It does not fully offset the lower peak. A vet product's ceiling is still a fraction of a human blockbuster's. But it changes the shape of the cash flows: lower and flatter, with a long, durable tail rather than a sharp peak and a cliff. That is a different discounting problem, and arguably a more forgiving one.

There is an asymmetry worth naming. The same direct-dispensing and self-pay dynamics that flatten the cliff also work through AMDUCA extra-label use, which can blur exclusivity while a product is still on patent. So exclusivity is softer at both ends: less absolute during the patent term, but more durable after it. For a long-dated royalty, the durable tail is usually the more valuable half of that trade.

7. Why the market stays this thin

The mechanics so far explain how individual deals are built. They do not, on their own, explain why so little capital has organized around the asset class. That has its own set of reasons, and they compound.

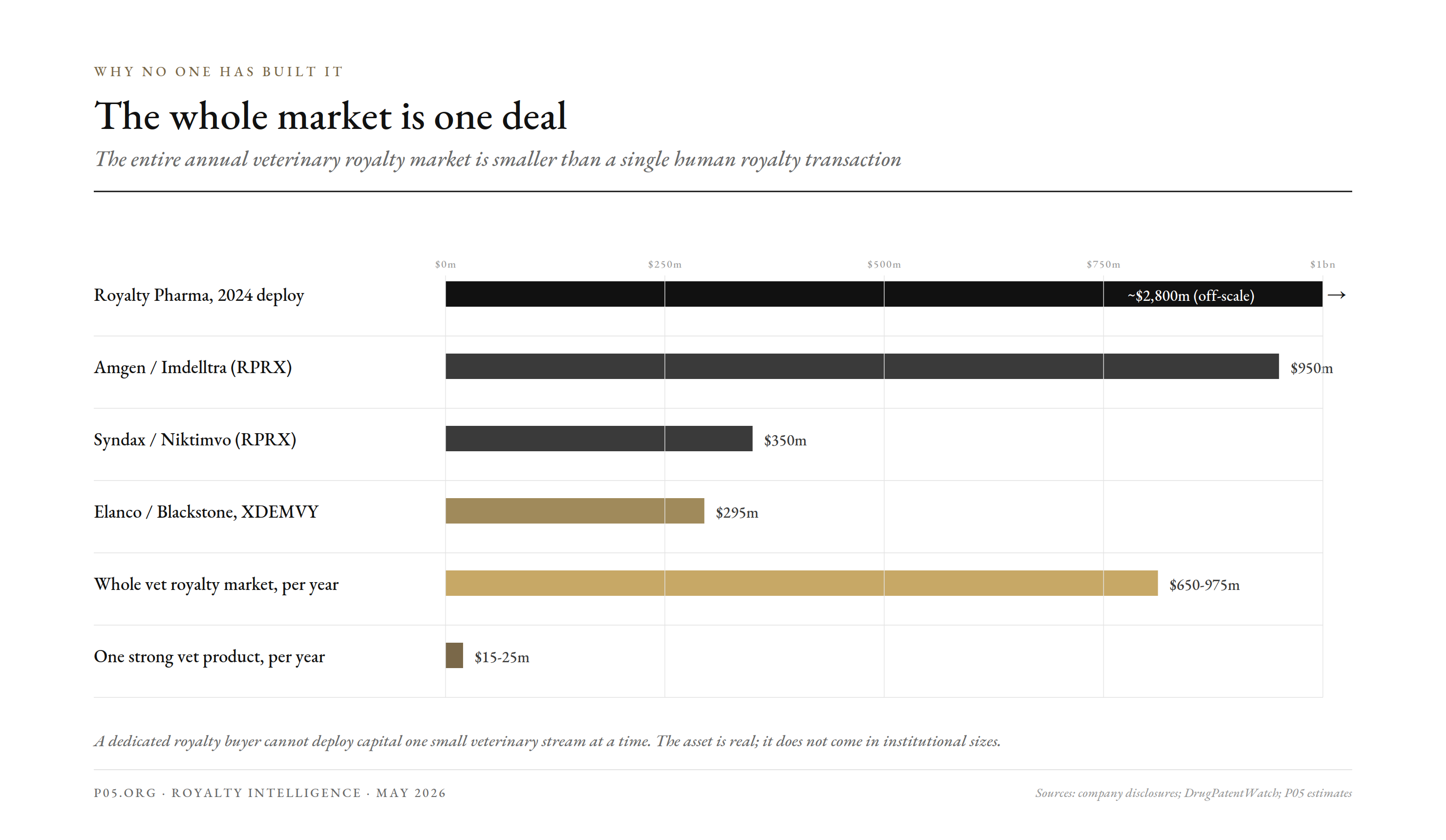

Start with the size mismatch, which is the dominant one. A dedicated royalty buyer writes large cheques. Royalty Pharma deployed roughly $2.8 billion in 2024 alone, in deals like $950 million on Amgen's Imdelltra and $350 million on Syndax's Niktimvo.

A best-in-class veterinary product might throw off $15-25 million of royalty a year. The entire veterinary royalty market, $650-975 million a year, is smaller than a single one of those human transactions.

The whole market is one deal. The entire annual veterinary royalty market is smaller than a single human royalty transaction.

That is the heart of it. A specialist royalty fund cannot deploy meaningful capital one $20 million vet stream at a time. The asset is real, but it does not come in institutional sizes.

Then there is the diligence problem, which makes the size problem worse. Underwriting a royalty means assessing patent survivability, generic-entry timing, and commercial forecasts. That work has a largely fixed cost, and it does not shrink just because the cheque is smaller.

The same legal and analytical spend that is trivial against a $950 million deal is prohibitive against a $20 million one. Per dollar deployed, a vet royalty is far more expensive to diligence than a human one.

The supply side is just as constrained, and it is the throughline of this whole piece. The option-to-acquire reflex means successful royalties are bought out before they mature. Species fragmentation thins each stream. So even a willing buyer faces a shortage of large, seasoned, unencumbered royalties to purchase.

There is also a data problem. Most veterinary deal terms are never disclosed; royalties are described as undisclosed or estimated, as our census repeatedly had to note. With only around 280 animal-health partnering deals since 2017, against thousands in human pharma, there is barely a comparables set to underwrite against.

Finally, capital that does want animal-health exposure has a more scalable target. Private equity has poured into veterinary clinics and hospitals, a cash-pay, recession-resilient, roll-up-friendly business, with more than 20 PE-backed platforms in the US and multi-billion-dollar deals like JAB's. Services scale; royalties do not. The capital follows the scalable target.

| Barrier | Why it blocks a royalty market | Effect |

|---|---|---|

| Deal size | Whole vet royalty market < one human royalty deal | Below institutional minimums |

| Fixed diligence cost | Same underwriting spend on a $20m or $950m deal | Uneconomic per dollar |

| Supply | Buyouts and species splits thin the streams | Few seasoned royalties to buy |

| Data | Terms mostly undisclosed; ~280 deals since 2017 | No comparables base |

| Better alternative | Vet clinics scale; royalties do not | Capital goes to services |

None of these is fatal on its own. Together they explain why the market has stayed a cottage industry: real, recurring, well-structured royalties that no institution has found a way to aggregate at scale.

This is also where the opportunity sits, if there is one. Every barrier above is a structuring problem, not a fundamental flaw in the asset. The streams are durable, the rates are healthy, the credit is clean, and, as the previous section showed, the tails are long.

What is missing is an aggregator: someone willing to bundle many small veterinary royalties into a pool large enough to interest institutional capital, and to build the comparables and diligence machinery once, across many deals, rather than deal by deal. That is precisely the gap that music royalties, and then diversified drug-royalty trusts, were built to fill in their own markets. No one has yet built it here.

8. What would make a vet company choose royalty financing

If the default is to acquire and to self-fund, the fair question is what would ever push a veterinary company to the royalty side instead. There are real answers, and 2026 already shows one of them working.

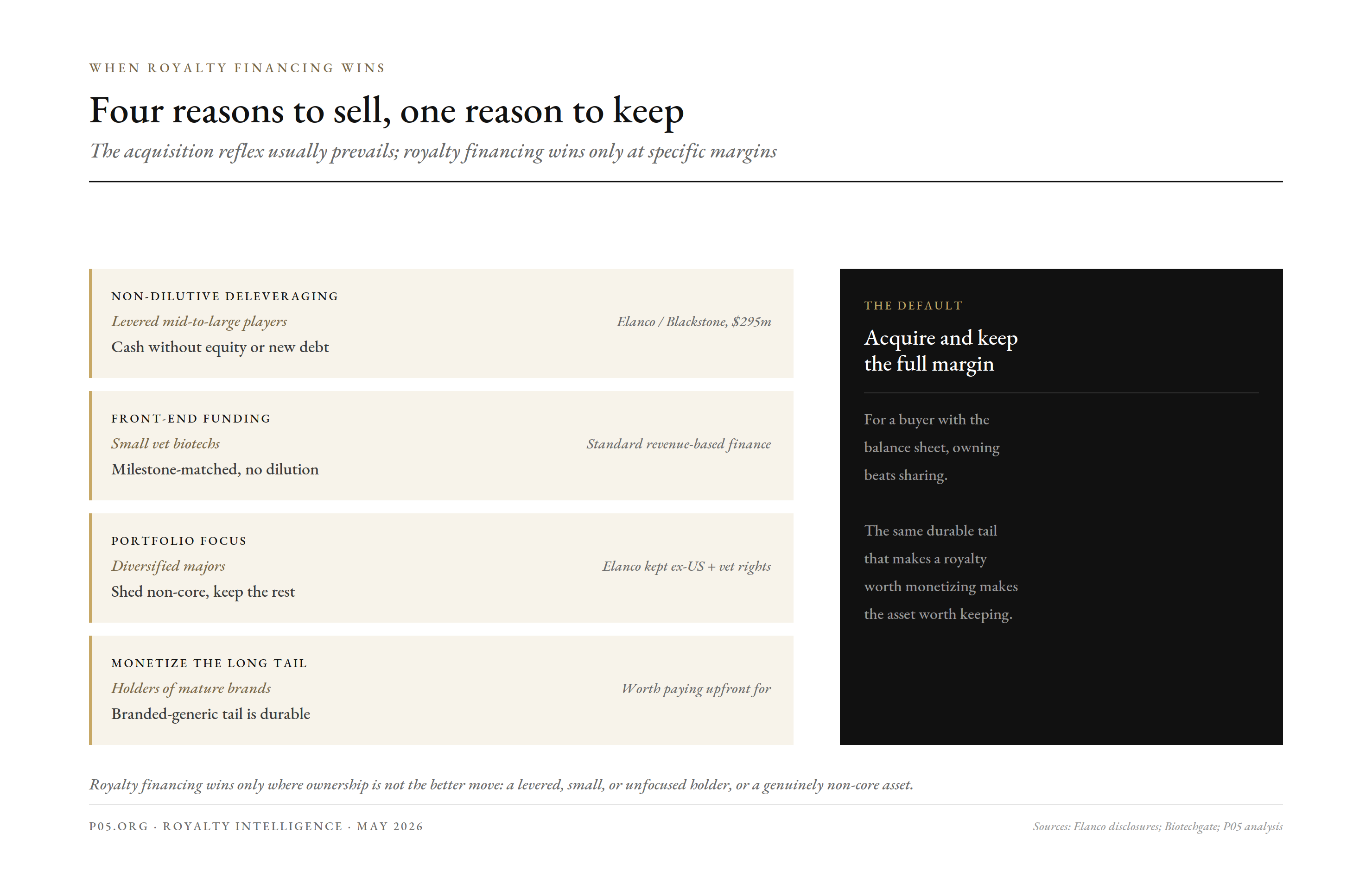

Four reasons to sell, one reason to keep. The acquisition reflex usually prevails; royalty financing wins only at specific margins.

The cleanest incentive is non-dilutive deleveraging. A levered animal-health company can raise cash against a future royalty without issuing equity or adding debt. Elanco did exactly this. It sold the US lotilaner royalty to Blackstone for $295 million, and used it to pull net leverage toward 3.8-4.1x and cut roughly $10 million of annual interest.

That is the template. For a company carrying real leverage, monetizing a non-core stream is cheaper than equity and cleaner than more debt, and the buyer takes the performance risk.

The second incentive is funding the front end without giving away the company. A small vet biotech with a promising asset faces the same choice every biotech does: dilute, borrow, or sell future revenue. Royalty and revenue-based financing is explicitly non-dilutive and milestone-matched, repaying more when sales grow and less when they do not. For a founder who does not want to sell equity at a low valuation, that is attractive.

The third is portfolio focus. Large players routinely divest non-core lines. A royalty sale lets a company shed the economics of a non-core asset for cash while keeping the rest, the optionality Elanco preserved by selling only the US human slice of lotilaner and retaining everything else.

The branded-generic tail, from the previous section, quietly strengthens all three. Because the post-patent stream is durable rather than cliff-like, there is more total value to monetize, and the seller can credibly argue the tail is worth paying for. A buyer who believes the stream runs for years past expiry will pay more upfront.

| Incentive | Who it suits | Why royalty financing fits | 2026 proof point |

|---|---|---|---|

| Non-dilutive deleveraging | Levered mid-to-large players | Cash without equity or new debt | Elanco / Blackstone, $295m |

| Front-end funding | Small vet biotechs | Milestone-matched, no dilution | Standard RBF structures |

| Portfolio focus | Diversified majors | Shed non-core economics, keep the rest | Elanco retained ex-US and vet rights |

| Monetizing the long tail | Holders of mature brands | Durable post-patent stream is worth selling | Branded-generic persistence |

There is also a latent incentive that has not yet activated: price discovery. As long as almost no veterinary royalties trade, no one knows what they are truly worth, and that uncertainty itself deters both buyers and sellers. The first cluster of clean, well-priced transactions would tell the market what a vet royalty is worth, which would lower the diligence burden on the next ones. Someone has to go first.

The honest counterweight is that the acquisition reflex still usually wins. For a buyer with the balance sheet to own an asset outright, capturing the full margin beats sharing it, and the branded-generic tail that makes a royalty attractive to monetize makes the asset just as attractive to keep.

Royalty financing wins only at the margins where ownership is not the better move: when the holder is levered, small, or focused elsewhere, or when the asset is genuinely non-core, as the human-drug crossovers tend to be.

What the mechanics add up to

Put the five features together and the shape of the market follows from them.

The milestones are smaller and arrive sooner, because the regulatory ladder is shorter. The asset fragments by species, so no single event unlocks the whole value. The cash-pay market strips out reimbursement risk but caps the upside.

The acquisition reflex keeps retiring successful royalties before they can mature into tradable assets. And monetization, when it happens, is usually a balance-sheet move on a human-drug royalty that a vet company happens to hold. The one feature that runs in a royalty buyer's favor is the shallow patent cliff, which gives the stream a longer, more durable tail than a human-pharma model would assume.

None of this makes veterinary royalties unviable. The rates are comparable to human deals, the credit can be cleaner, and the development risk is lower. The instruments are real and well understood.

What it does explain is why a deep, liquid veterinary royalty market has not formed. The structures that dominate the sector are, one after another, structures that prevent a standing inventory of streams from building up: buyouts that retire royalties, species splits that thin them, and monetizations that depend on a rare human-royalty crossover.

As of 2026, the clearest near-term change is on the regulatory side. Conditional-approval pathways like the one Loyal is using let novel modalities reach the market sooner, which front-loads the milestone schedule and could let royalties start flowing earlier on a wider set of assets.

But the deeper gap is structural, not regulatory. The asset is sound; what is missing is an aggregator willing to bundle many small, durable veterinary royalties into something institutional capital can underwrite at scale. Until someone builds that layer, the veterinary royalty market will stay what it is today: real, recurring, and almost entirely unbought. That is the same conclusion our census left standing, now with the reasons attached.

All information in this report was accurate as of the research date and is derived from publicly available sources including regulatory guidance, company disclosures, SEC filings, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.