What Actually Gets Wired: How a Pharmaceutical Royalty Is Calculated and Paid

A mechanics walk-through of the royalty payment, from the shelf price to the wire and into the buyer's account, as of June 2026.

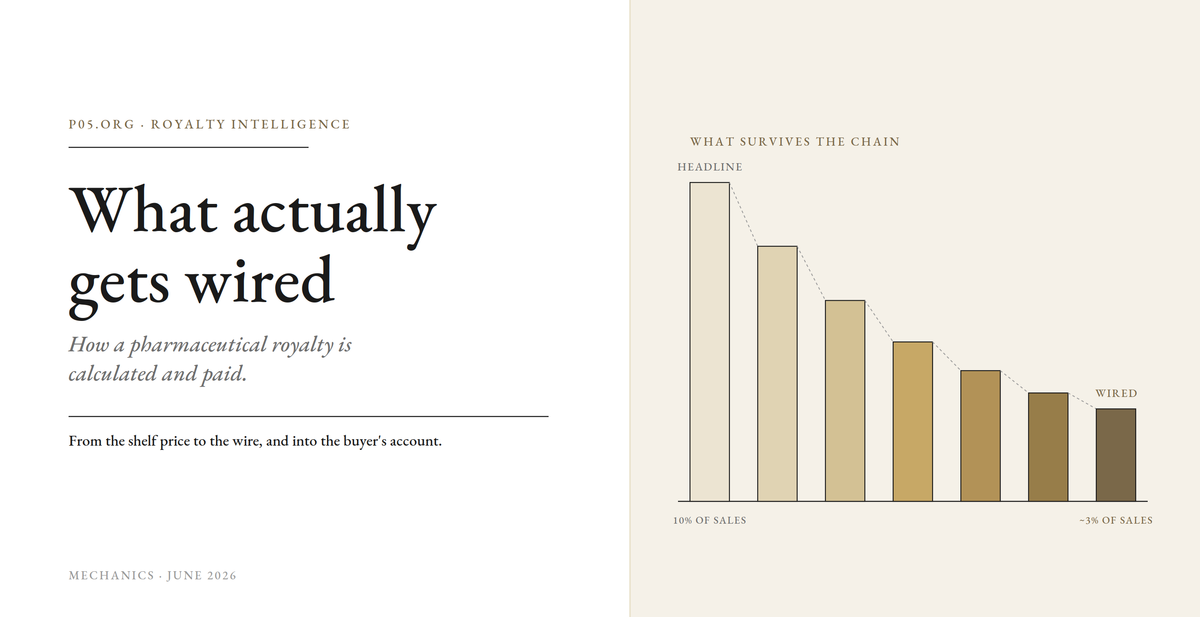

A royalty deal is usually summarised in a single number. "Tiered double-digit on net sales." "Eight percent." "A 2.5% synthetic royalty." That number is the headline, and it is almost never the amount that lands in the account.

Our earlier piece on gross-to-net modeling followed a drug's price from list down to net, the macro waterfall of rebates, discounts and government programs that separates the WAC sticker from the money a manufacturer keeps. This piece picks up where that one stopped. Once there is a net sales number, what does the contract do with it: how a percentage becomes a payment, who computes it, how it is verified, and what moves when the royalty has been sold to a financier.

A royalty is not a fee on revenue. It is a contractual claim on a precisely engineered subset of revenue, run through a rate structure that is rarely flat, bounded by a clock, adjusted by modifiers that can quietly halve it, reported on a lag, certified, audited, taxed at the border, and, increasingly, redirected to a third party who bought the stream. Each step changes the number that gets wired. This is the same mechanics-first approach used for veterinary and digital health royalties, turned on the payment itself.

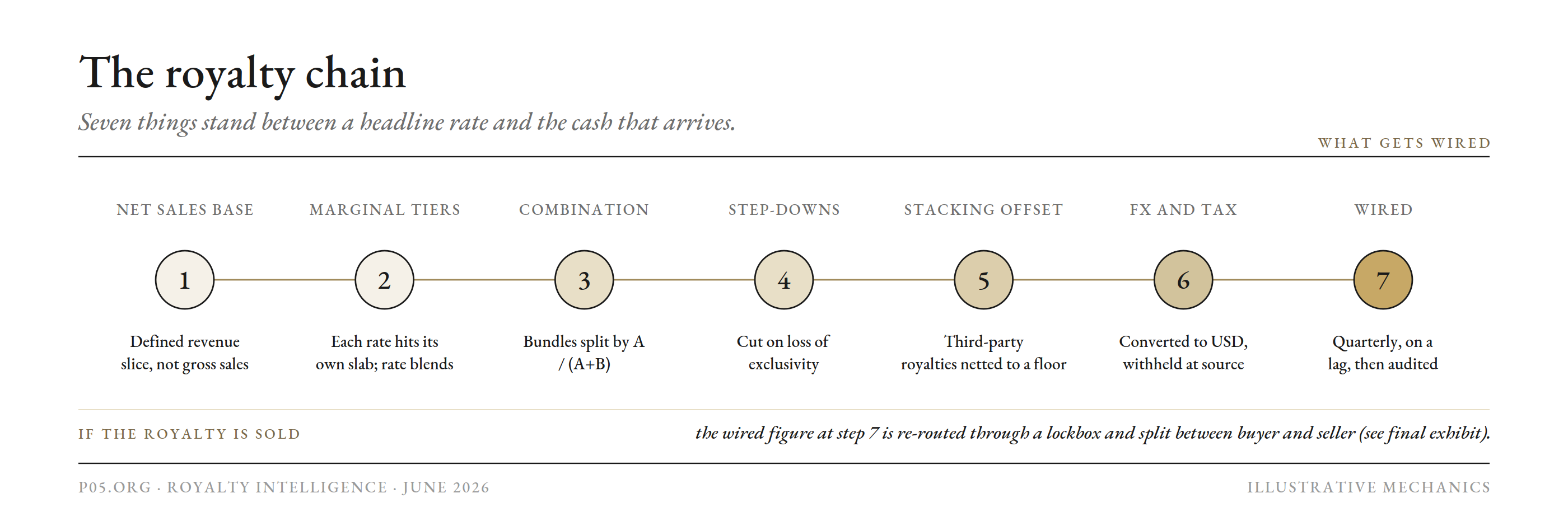

The royalty chain ] Seven things stand between a headline rate and the cash that arrives.

1. The base is "Net Sales," a defined term

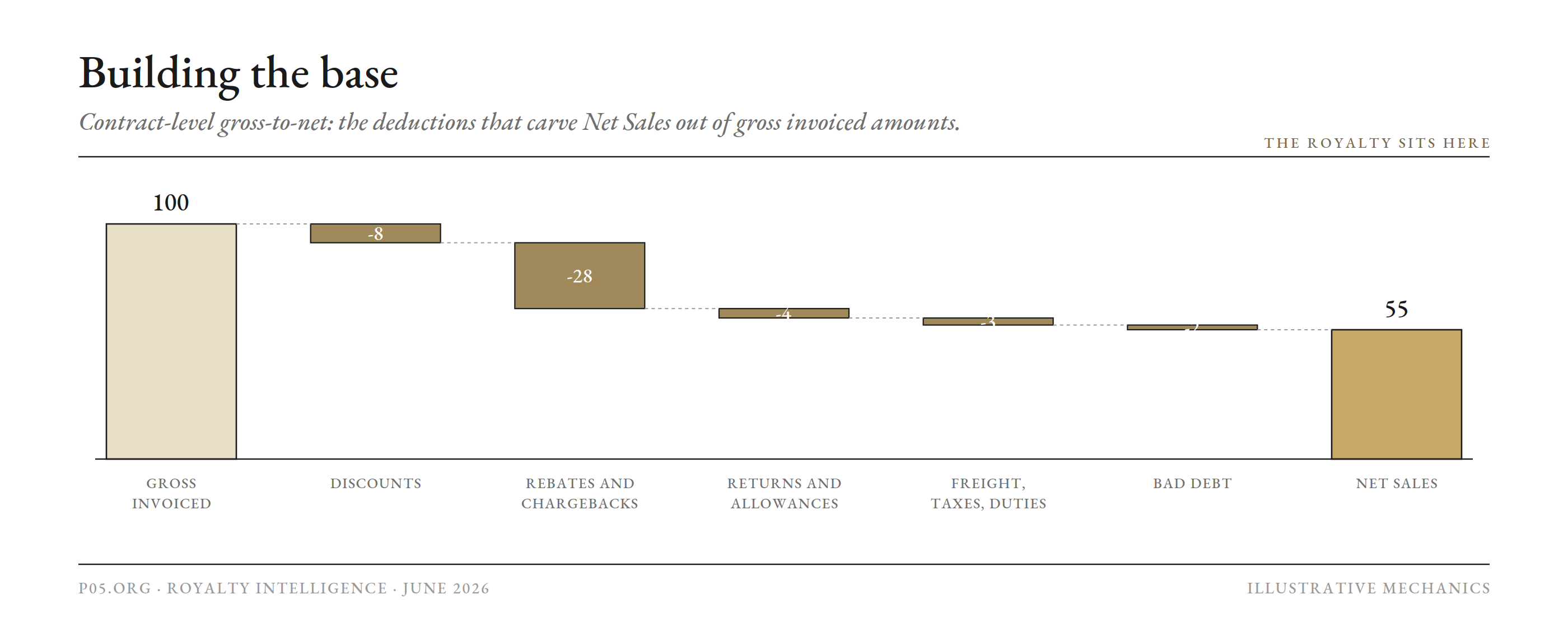

The royalty almost never sits on gross revenue, and never on income-statement revenue. It sits on a defined contractual term, usually "Net Sales": the gross amount invoiced for the licensed product, sold by the licensee, its affiliates and its sublicensees to unaffiliated third parties, minus a closed list of permitted deductions. The deduction list is the whole negotiation.

| Permitted deduction | Captures | Typical condition | Input controlled by |

|---|---|---|---|

| Trade, cash, quantity discounts | Concessions to wholesalers and distributors | Given at or near time of sale | Licensee |

| Rebates and chargebacks | Managed-care, Medicaid, Part D, 340B | Accrued, trued-up later | Licensee |

| Returns and allowances | Credits for rejected or expired product | Actually credited | Licensee |

| Freight, insurance, handling | Outbound transport, in-transit cover | Usually only if separately invoiced | Licensee |

| Sales/excise tax, VAT, duties | Transaction taxes on the sale | Separately stated, not reimbursed | Licensee |

| Bad debt | Uncollectible amounts | Per the agreed accounting standard | Licensee |

The mirror image matters as much as the list. Costs that sit upstream of the sale are generally not deductible, which is where licensees most often overreach.

| Often disallowed | Why |

|---|---|

| Cost of goods sold | Incurred before sale; sits in COGS, not in the sale price |

| Import tariffs on API or finished product | Upstream cost unless the contract explicitly allows it |

| Income and franchise taxes | Taxes on the seller, not on the transaction |

| Internal commissions, marketing, rebate-admin overhead | Cost of doing business, not a price concession |

Three structural rules decide how generous the base is.

| Rule | Market practice | Effect on the base |

|---|---|---|

| Recognition | Accrual: at shipment or invoice, whichever first | Blocks cash-basis and bad-debt timing games |

| Intercompany / affiliate sales | Royalty bites at first sale to an unaffiliated buyer | Stops base-shrinking via cheap intra-group transfer |

| Deduction cap | Often capped at 5 to 10% of gross, or a fixed lump-sum in lieu of line items | Caps struck against gross, never net, to avoid circularity |

A filed definition reads, in composite: gross invoice price to end-users, less trade allowances, discounts and returns customarily given, less separately stated taxes and transport, less amounts credited for rejection, and less compulsory rebates to third parties including managed-care and government programs. That last clause imports the entire gross-to-net problem into the royalty base. The same rate produces very different cash depending on the base:

| Gross sales | Net sales (after GTN) | 5% royalty | |

|---|---|---|---|

| Commercial-heavy drug | $1,000m | $650m | $32.5m |

| IRA-negotiated channel | $1,000m | $350m | $17.5m |

The rate did not change. The base did.

Building the base ] Contract-level gross-to-net: the deductions that carve Net Sales out of gross invoiced amounts. Illustrative.

Affiliates and sublicensees

Net Sales counts sales by the licensee, its affiliates and its sublicensees. A sublicensee, though, generates two different payments, and they are not the same instrument.

| Payment | Base | Typical level | Paid when |

|---|---|---|---|

| Running royalty on sublicensee sales | The sublicensee's Net Sales | The same tiered rate, passed up the chain | Quarterly, with everything else |

| Sublicense income share | Non-royalty consideration the licensee receives (upfronts, milestones, option and licence fees) | Stage-based, commonly 15 to 40%, higher the earlier the asset was sublicensed | Often within 30 to 45 days of receipt |

The sublicense-income share deliberately excludes the running royalties (captured separately), and usually excludes equity bought at fair value, R&D funding and cost reimbursements, so the licensee cannot disguise a licence fee as something else.

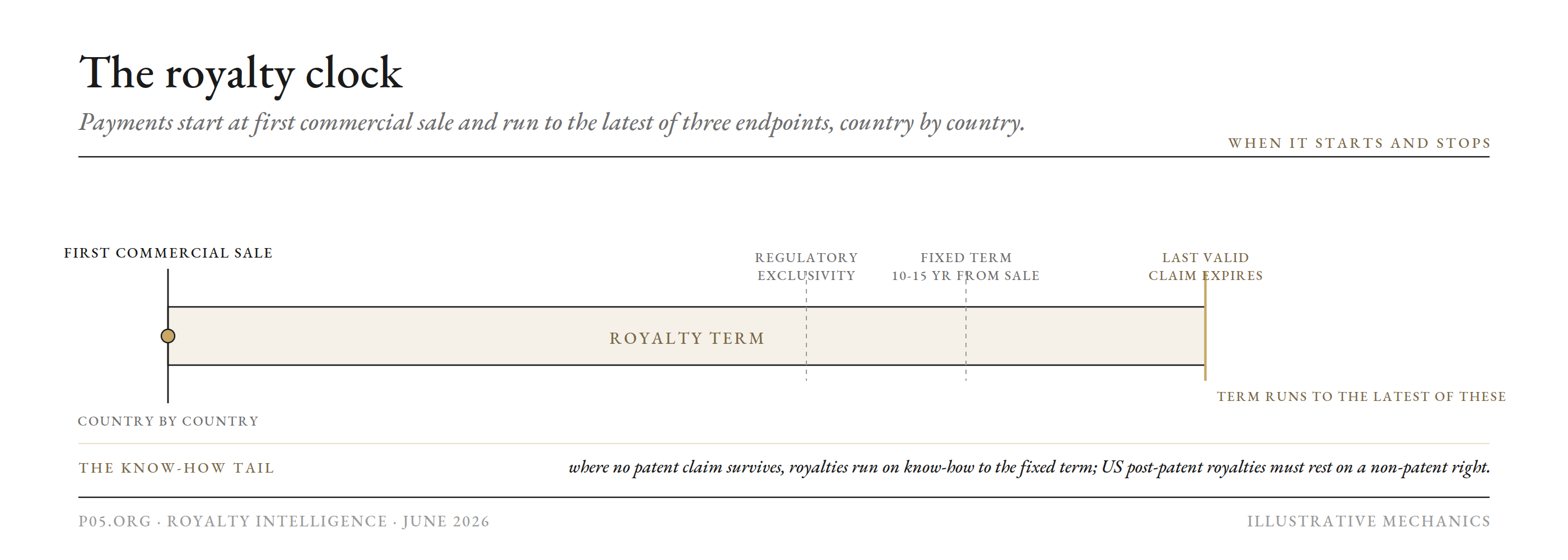

2. The clock: when the royalty starts and stops

A royalty has a beginning and an end, both defined per country and per product. This is the duration a buyer actually prices.

| Element | Standard term |

|---|---|

| Starts | First commercial sale of the product in that country |

| Basis | Country-by-country, product-by-product |

| Ends | The latest of: (a) last valid patent claim expires; (b) regulatory exclusivity expires; (c) a fixed term, commonly 10 to 15 years from first commercial sale |

The royalty clock ] Payments start at first commercial sale and run to the latest of three endpoints, country by country.

The third limb is the know-how tail, and it carries the royalty where no patent survives. It exists partly for legal reasons: in the US, a licensor cannot collect patent royalties after the patent expires (Kimble v. Marvel, reaffirming Brulotte).

Agreements that want a tail therefore tie the post-expiry payments to know-how or another non-patent right, or amortise pre-expiry sales over a longer period. The practical link to the next sections: once a country drops onto the know-how tail, it is also where the step-down rate (below) applies.

3. The rate is a marginal tier schedule, not a flat percentage

Outside early-stage deals, settlements and simple synthetic royalties, most biopharma alliances tier the royalty: not one rate but two to six, each attached to a band of annual net sales. A disclosed schedule filed with the SEC shows the shape.

| Calendar-year net sales | Tier rate |

|---|---|

| up to $500m | 10% |

| $500m to $750m | 12% |

| $750m to $1,000m | 14% |

| $1,000m to $2,500m | 17% |

| $2,500m and above | 20% |

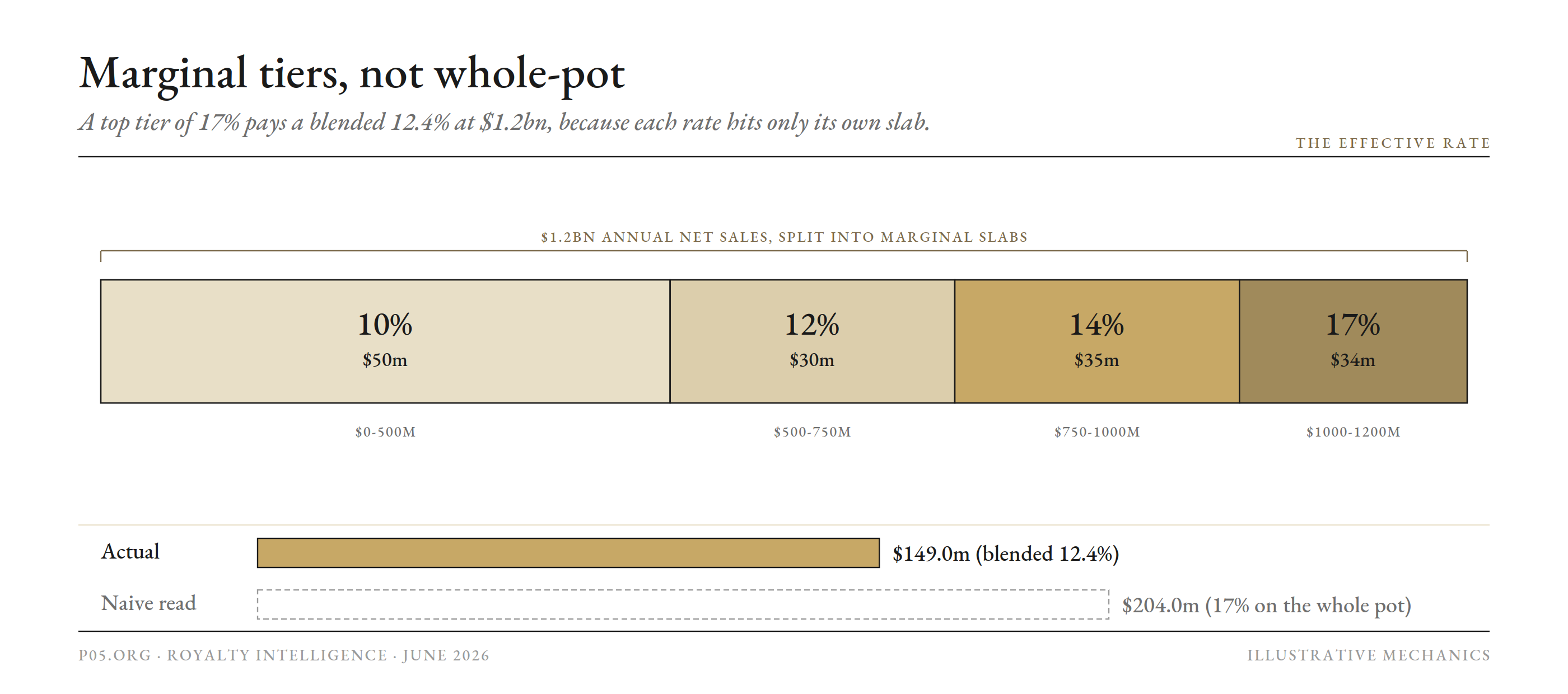

The mechanic that moves the wired number most: tiers are marginal, not whole-pot. When cumulative net sales cross a breakpoint, the higher rate applies only to the slice above it, not retroactively to every dollar. The counter resets each January. At $1.2bn of annual net sales:

| Slice | Rate | Royalty |

|---|---|---|

| First $500m | 10% | $50.0m |

| Next $250m | 12% | $30.0m |

| Next $250m | 14% | $35.0m |

| Final $200m | 17% | $34.0m |

| Total | blended 12.4% | $149.0m |

The product never "pays 17%." It pays a blend that climbs through the year and resets each January. Reading the stream off the top tier overstates it by tens of millions: $204m versus $149m here.

Marginal tiers, not whole-pot ] A top tier of 17% pays a blended 12.4% at $1.2bn, because each rate hits only its own slab.

Deals are only comparable once collapsed into an effective royalty rate, the schedule applied at assumed sales levels.

| Annual net sales | Royalty on the schedule above | Effective rate |

|---|---|---|

| $200m | $20.0m | 10.0% |

| $500m | $50.0m | 10.0% |

| $1,000m | $115.0m | 11.5% |

| $2,500m | $370.0m | 14.8% |

Two layers often sit alongside the running royalty, and both are commonly confused with it.

| Layer | What it is | How it pays |

|---|---|---|

| Commercial sales milestone | One-time payment when annual or cumulative sales first cross a threshold | Lump sum, on top of the royalty, once |

| Minimum annual royalty / floor | Guaranteed baseline regardless of volume | Tops the running royalty up to the floor |

4. The modifiers that move the number

If the base and the schedule set the starting figure, four modifiers pull it down. This is where the wired number diverges most from the headline.

Combination products

When the licensed product is sold bundled (a fixed-dose combination, or a drug packaged with a device), the base is allocated so the licensor is paid only on the licensed share.

| Method | Formula | When used |

|---|---|---|

| Price-based (standard) | A / (A+B), A = standalone price of licensed component, B = the rest | Both sold separately |

| Cost-based fallback | C / (C+D) on fully allocated cost | No standalone price exists |

| Good-faith allocation | Negotiated on relative value | Neither price nor clean cost available |

The contested point, as one practitioner frames it, is whether the licensed product drives the bundle's sales; licensors resist allocations that give away value on a component merely along for the ride, and often cap the cut at 50%. The licensee supplies the prices and costs that feed the fraction.

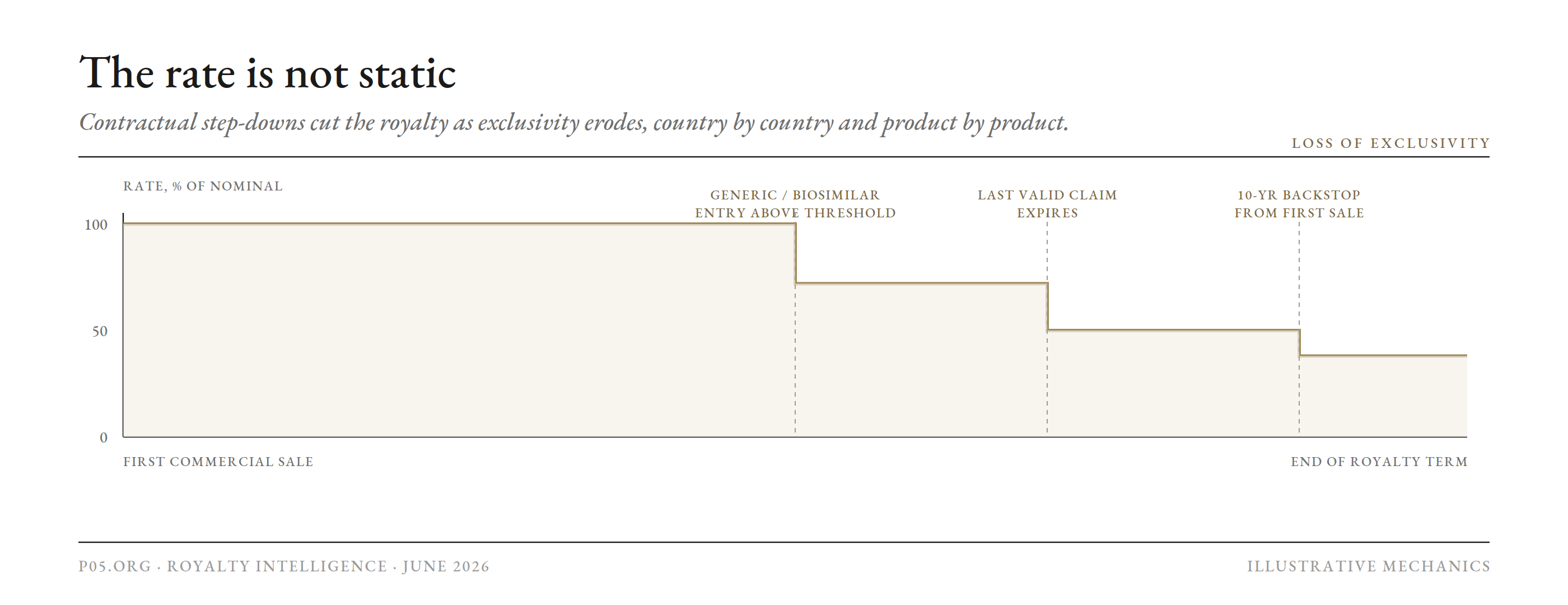

Step-downs on loss of exclusivity

The rate is not constant across the term. It steps down, country by country and product by product, on defined triggers.

| Trigger | Typical effect | Scope |

|---|---|---|

| Last valid patent claim expires | Rate cut to a fraction, often 50% of weighted-average | That country |

| Generic / biosimilar entry above a share threshold | Further reduction | That country |

| Time backstop (commonly 10 years from first sale) | Reduction even if a claim survives | That country |

This is the contractual cousin of the patent cliff, written into the payment formula, and the main reason a long-dated royalty is worth far less than a flat extrapolation.

The rate is not static ] Contractual step-downs cut the royalty as exclusivity erodes, country by country and product by product.

Royalty stacking offsets

If the licensee must take a third-party licence to sell without infringing, it can claw some of that cost back from the licensor.

| Element | Common term |

|---|---|

| Deductible share of third-party royalties | Often 50% |

| Floor on the licensor's rate | Never below an agreed level (for example 50% of nominal) |

| Carry-forward | Unused offset can roll to later quarters |

| Limitation | Only IP genuinely necessary to practise the licence, not bolt-ons |

The aggregate floor

Combination allocation, step-downs and stacking can all bite in the same quarter. Well-drafted agreements add a single cumulative backstop: in no event shall all reductions together cut the royalty below a set fraction of what would otherwise be due. The floor is commonly 50% of the amount that would have been payable but for the reductions.

| Reduction | Its own limit | In the aggregate floor? |

|---|---|---|

| Combination allocation | Often capped at a 50% cut | Yes |

| Stacking offset | 50% of third-party, with a rate floor | Yes |

| Step-down | To a fraction of the rate | Sometimes carved out separately |

| Aggregate floor | Royalty never below, for example, 50% of otherwise-due | Binds the others together |

Stack the modifiers on a notional 10% headline and the gap becomes vivid. None of it is hidden. It is simply not in the headline.

| Step | Running royalty | Effective on gross |

|---|---|---|

| 10% headline on $1,000m gross | n/a | n/a |

| On Net Sales of $550m (after 45% GTN) at blended 11% | $60.5m | 6.1% |

| After combination allocation (70% licensed share) | $42.4m | 4.2% |

| After blended step-down (part of territory post-exclusivity) | $37.1m | 3.7% |

| After stacking offset | $31.5m | 3.2% |

| After 15% withholding on the cross-border share | $29.2m | 2.9% |

A "10% royalty" wires at under 3% of gross. The construction, not the headline, is the asset.

5. The plumbing: reported, certified, paid, checked

Knowing the right number is one thing. Getting it on time, and proving it, is another.

| Step | Market-standard term |

|---|---|

| Accrual | Royalty accrues when product is invoiced or sold |

| Cadence | Paid quarterly |

| Payment window | 30 to 60 days after quarter-end; 45 days is modal, longer for sublicensee pass-through |

| Report | Statement of net sales by product and country, deductions, tier math, FX, CFO-certified |

| Mechanism | Wire of immediately available funds, stated currency, no set-off except as permitted; payer bears its own bank charges |

| Late payment | Interest at 1.5% per month or prime plus a spread, capped at the maximum legal rate |

| Blocked currency | If a country bars conversion or remittance, amounts may be held in a local account until released |

Because the payor controls every input, the payee's protection is the audit clause.

| Audit term | Common setting |

|---|---|

| Frequency | Once per calendar year |

| Notice | Ten business days or more |

| Auditor | Independent accountant, bound by confidentiality, not on a contingency fee |

| Lookback | Three years |

| Cost-shift threshold | Payor pays the audit cost if underpayment exceeds, commonly, 5% |

| Remedy | Shortfall plus interest; overpayments credited forward |

Cross-border royalties carry a tax layer that the wire has to clear.

| Tax item | Mechanic |

|---|---|

| Character | Royalties are FDAP income, subject to source withholding, statutory rates commonly 15 to 30% |

| Treaty relief | Recipient files Form W-8BEN-E to claim a reduced or zero treaty rate; valid roughly three years |

| Gross-up | Negotiated: whether the payer tops up so the recipient nets the full amount |

| Cooperation | Parties supply documentation so the recipient can claim a foreign tax credit |

Two realities sit underneath all of this. Audits are not a formality: underpayments surface routinely, usually not through fraud but through aggressive deduction reads and combination allocation. And because gross-to-net uses accrual estimates, reported net sales get trued-up in later quarters as real rebate and return data land.

The royalty rides those true-ups, so a stream is real but lumpy quarter to quarter, which is why a buyer underwrites a smoothed multi-quarter figure rather than any single print.

6. What changes when the royalty is sold

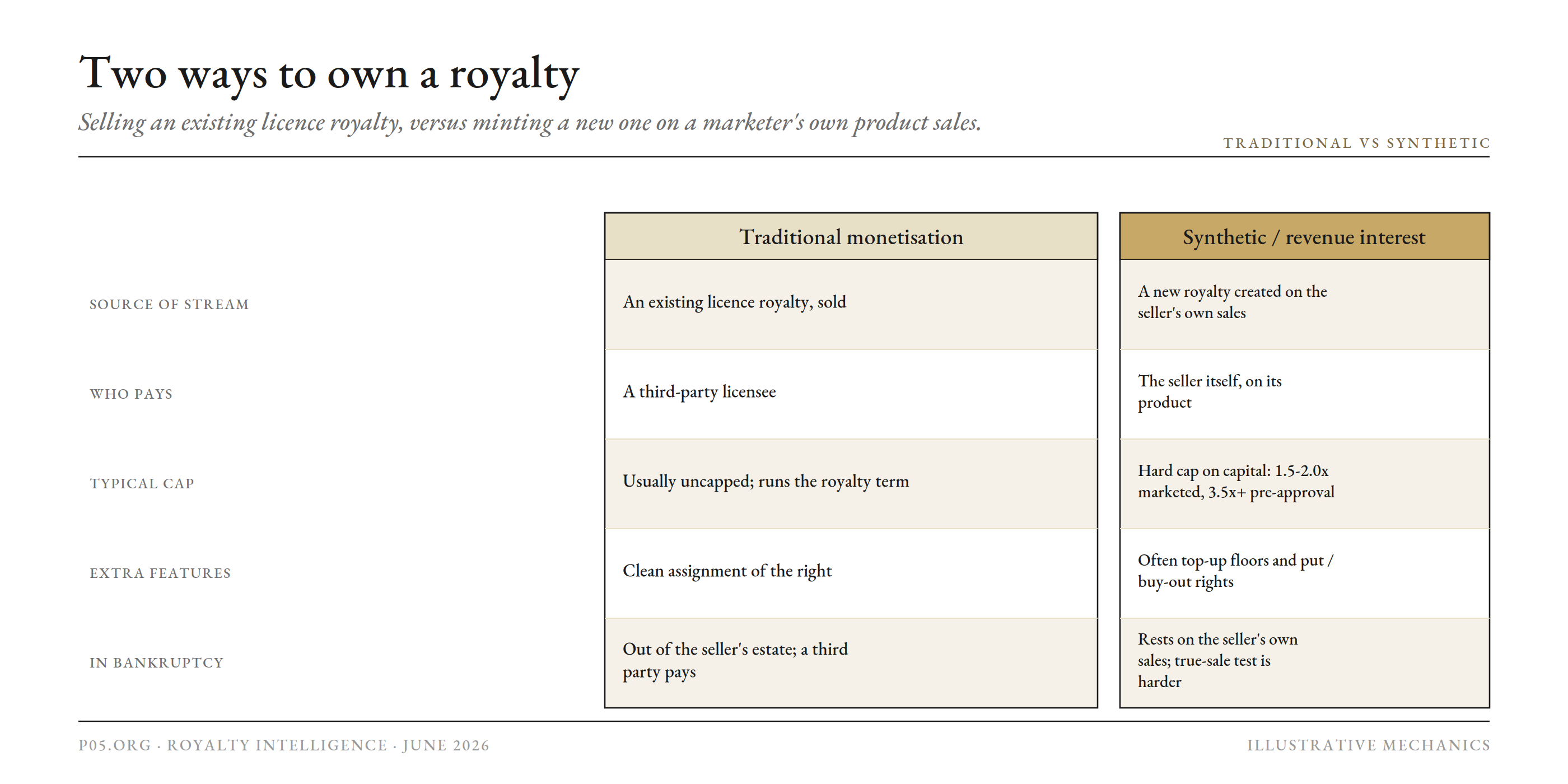

For a buyer or an arranger, "what gets wired" becomes literal: the cash has to move from the original payer to a new owner. First, two different things can be sold.

Two ways to own a royalty ] Selling an existing licence royalty, versus minting a new one on a marketer's own product sales.

A traditional monetisation sells an existing licence royalty: a third-party licensee keeps paying, and the buyer steps into the seller's shoes. A synthetic royalty, or revenue interest financing, mints a brand-new royalty on the marketer's own top-line product sales in exchange for upfront capital.

The economics differ most in the cap: a synthetic is usually capped at a multiple of invested capital, and terminates once the buyer has been paid that multiple.

| Deal | Upfront | Royalty on | Cap or feature |

|---|---|---|---|

| Phathom (vonoprazan) | up to $260m | net sales | 2.0x invested capital, then terminates |

| Albireo / Sagard (Bylvay) | $115m | global net revenues | Hard MOIC cap plus a buy-out option |

| OMERS / BioCryst (ORLADEYO) | $150m | net sales | Capped, tiered, declining royalty |

| PTC / Royalty Pharma (Evrysdi) | up to $1.5bn | risdiplam royalties | Royalty purchase of an existing stream |

Typical caps run 1.5 to 2.0x for marketed products and 3.5x or higher pre-approval. Features like top-up floors, put rights and other recourse push a deal toward "financing" rather than a clean sale, which matters in the seller's bankruptcy.

Either way, the deal is structured as a true sale, not a loan: the buyer pays a lump sum, the seller assigns the stream, and the buyer assumes none of the seller's other obligations.

| Deal | Seller | What was sold | Structure |

|---|---|---|---|

| RPI / Cytokinetics ($90m) | Cytokinetics | Slice of a CK-452 royalty | True sale of a portion |

| Arena / Longboard | Arena (356 Royalty) | Eisai-derived royalty and milestones | True sale, buyer takes only purchased rights |

| Deerfield / Titan | Titan | Sublicense royalty stream | Paid via paying-agent account at US Bank |

| Agenus / XOMA receivables | Agenus | XOMA-related receivables | Escrow amended to pay the buyer directly |

The "true sale" characterisation is load-bearing: it keeps the asset off the seller's balance sheet and out of its bankruptcy estate. The nuance is that a traditional royalty is paid by a third-party licensee, so it sits outside the seller's estate cleanly; a synthetic royalty depends on the seller's own continued sales, so the true-sale analysis is harder and structurers lean on the cap, true-sale opinions and precautionary security interests.

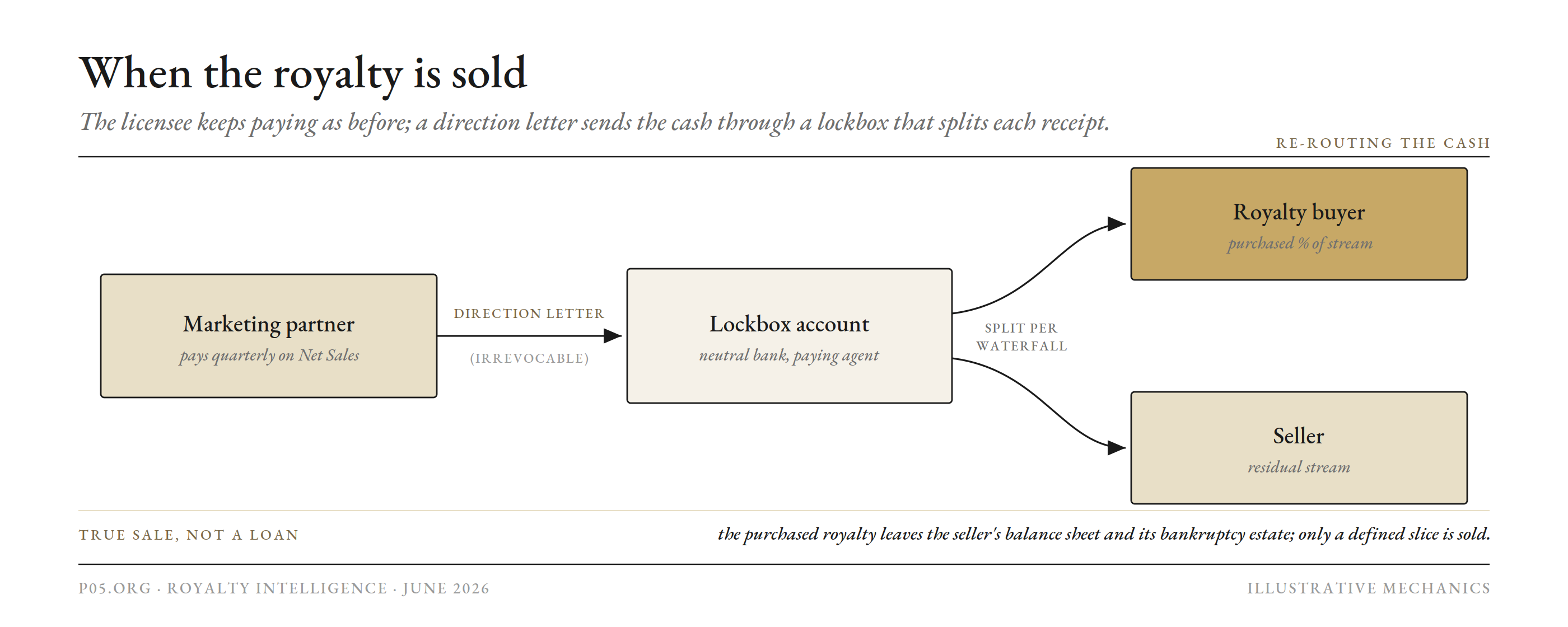

Whichever it is, the marketing partner keeps paying the same way, quarterly on net sales, so the deal re-routes the cash through three mechanics.

| Mechanic | What it does |

|---|---|

| Payment-direction letter | Seller irrevocably instructs the payer to send the purchased royalty to a named account |

| Lockbox + paying agent | Neutral bank holds the account; agent disburses the purchased portion to the buyer and the rest to the seller |

| Escrow amendment | Where an escrow exists, it is amended to pay the buyer directly, with a lockbox fallback |

When the royalty is sold ] The licensee keeps paying as before; a direction letter sends the cash through a lockbox that splits each receipt.

The buyer rarely takes the whole stream. It buys a defined slice, a portion of the royalty, or a tiered, capped or declining interest, and the lockbox waterfall divides each receipt per the agreed percentages and caps.

The reason everything above matters to a buyer is now obvious: it is purchasing the number that survives the entire chain, the headline rate on the defined base, run through the marginal schedule, bounded by the clock, after combination allocation, step-downs and stacking, under the aggregate floor, converted for FX, net of withholding and audit true-ups, paid on a 45-day lag.

Diligence is, almost entirely, re-deriving that number from the licence and the payor's historical reports and pricing each modifier. The contract mechanics are the asset.

The verdict

"What gets wired" is not a percentage of sales. It is a percentage applied to a contractually constructed base called Net Sales, bounded by a clock that starts at first commercial sale and runs to the latest of patent, exclusivity and a fixed term, computed on a marginal tier schedule that resets each January, after the base is allocated for combination products and the rate is cut by step-downs and stacking offsets under a single aggregate floor, then converted across currencies, reduced by withholding, reported quarterly on a lag, certified, audited and trued-up.

If the royalty has been sold, or minted synthetically, that surviving number is redirected by an irrevocable direction letter into a lockbox and split by a paying agent, often against a hard multiple-of-capital cap.

A royalty is a claim on a manufactured figure, and the manufacturing is where both the value and the risk live. The headline rate tells you almost nothing. The Net Sales definition tells you how much of the market reaches the formula; the clock tells you for how long; the tier mechanics tell you the real effective rate; the step-down triggers, the stacking floor and the aggregate floor tell you what the stream is worth as the product ages; the payment plumbing tells you when, and whether, the cash arrives; and the monetisation mechanics tell you who it arrives to, and how much before the cap shuts it off.

For an originator or a buyer, that stack is the entire diligence, and it is exactly where streams get mispriced.

All information in this report was accurate as of the research date and is derived from publicly available sources including court opinions, regulatory guidance, academic literature, SEC filings, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.