Non-Recourse Litigation Sales in Pharmaceutical Royalty Finance: How They Work, How They Reshape the Stack

Non-recourse litigation sales are the fastest-growing and least-understood asset class in modern pharmaceutical royalty finance.

They sit at the intersection of three distinct markets: the established institutional litigation finance industry (Burford Capital, Omni Bridgeway, Parabellum, Therium), the pharmaceutical royalty fund universe (Royalty Pharma, HealthCare Royalty, OMERS, XOMA), and the specialized distressed-credit market that prices contingent claims. The product they transact is the same in each case: a pending or accrued legal claim whose value depends on a future judicial, arbitral, or settlement outcome, sold or monetized for non-recourse capital today.

The pharmaceutical context is distinctive. Many of the largest pharma claims today are claims for royalty underpayment (PDL v. MedImmune, PDL v. Genentech/Roche), claims for breach of contingent value rights agreements (UMB Bank v. Bristol Myers Squibb, CVR Trustee v. Sanofi), or claims for breach of post-closing efforts covenants (SRS v. Alexion). These are economically the same kind of asset that a royalty fund underwrites in its core business: contractual receivables denominated in dollars, with their amount, timing, and probability of receipt determined by a third-party obligor's behavior.

This piece builds on our prior coverage of CVR tradability (which treated these cases as legal precedents on enforceability) and the LaaS analysis (which examined them as drafting templates). Here the same cases are reframed as financial assets, valued and underwritten by litigation funders and royalty buyers as a distinct asset class.

This piece works through the mechanics of non-recourse litigation sales as they appear in modern pharmaceutical royalty finance, the resulting impact on the royalty stack at the claimant level and at the buyer level, the recent litigation cohort that illustrates the variation in pricing and structure, the legal architecture (champerty, assignability, attorney-client privilege, work product, and bankruptcy treatment), and the practical drafting and diligence considerations for claimants, royalty funds, and counsel.

What a non-recourse litigation sale actually is

A non-recourse litigation sale is the transfer of all or part of the economic interest in a pending or accrued legal claim, in exchange for upfront capital, with the funder's return contingent on a successful resolution of the claim. The defining feature is the non-recourse character: if the claim fails (the plaintiff loses, the defendant proves insolvent, or the case settles for less than the funder's invested capital plus return), the funder receives nothing and the claimant retains the upfront cash.

The standard formulation, repeated almost verbatim across hundreds of commercial litigation finance agreements since 2009, runs along the following lines: "Capital typically is non-recourse, not debt, meaning the investment and return are paid only on a successful resolution." Read in isolation, the language looks like a description of a venture investment. In practice, it describes an asset class with very specific risk and pricing properties.

The structural distinction matters because of a peculiar feature of common-law jurisdictions: contingent claims have historically been treated as personal to the holder and not freely transferable. The doctrines of champerty and maintenance, which originated in medieval English law to prevent powerful third parties from stirring up litigation for their own profit, restrict the assignment of bare litigation claims in many U.S. states. The modern litigation finance industry has navigated these doctrines by structuring transactions as financing of the claimant rather than as outright purchases of the claim, but the underlying tension remains a structuring constraint.

For pharmaceutical royalty finance, this distinction is not academic. It determines whether a biotech with a pending royalty audit claim against its commercial licensee can monetize that claim alongside its underlying royalty stream. It determines whether a CVR trustee like UMB Bank can finance the multi-year litigation against an acquirer without exhausting the trust's reserves. And it determines whether the holders of breach-of-efforts-covenant claims can extract any value before final judgment, or must wait through years of motion practice and appeals.

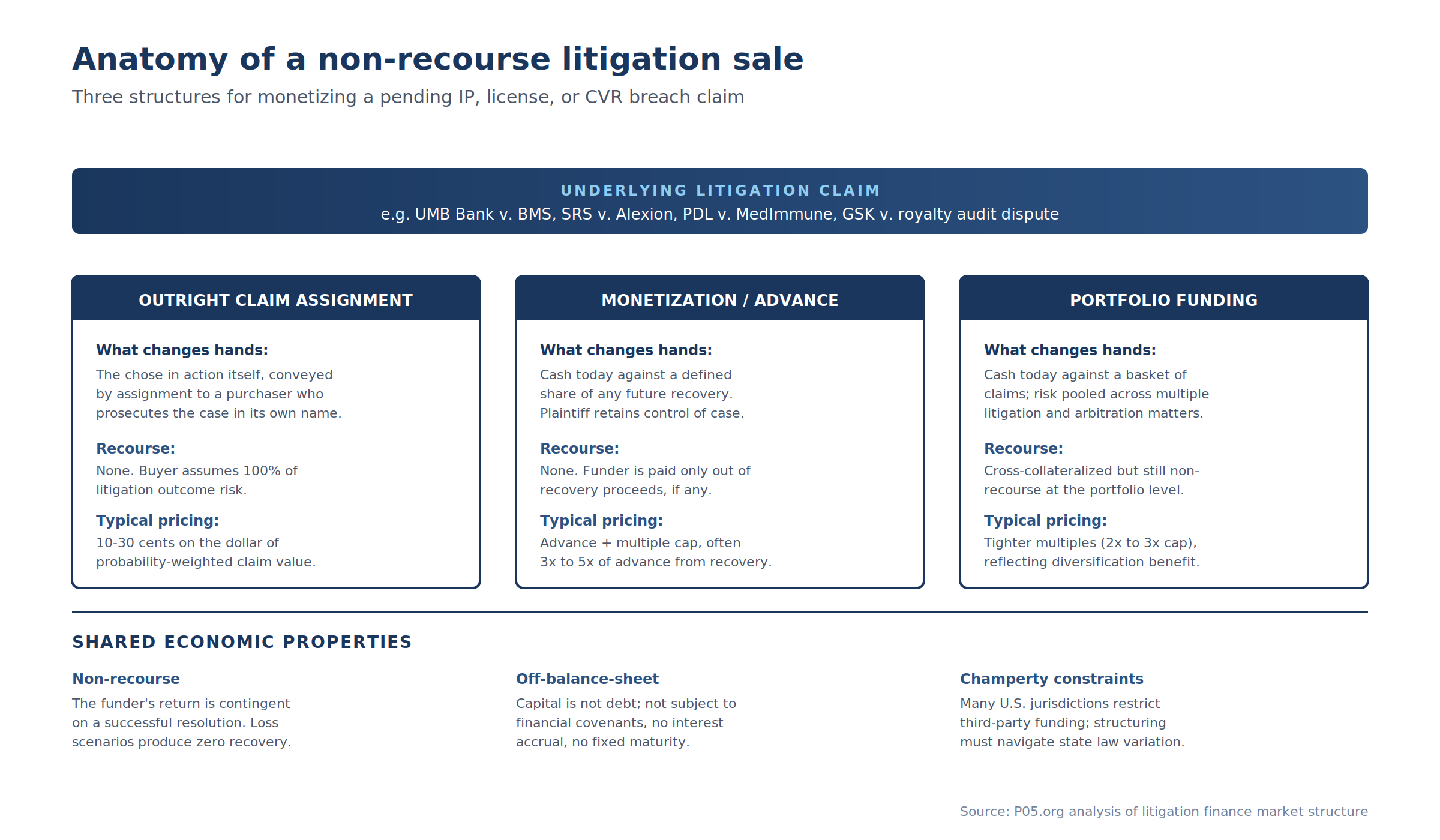

Three structural archetypes dominate the modern non-recourse litigation sale market. The summary is captured below, and each is discussed in turn after the table.

| Archetype | What changes hands | Recourse | Pricing | Claimant retains control? |

|---|---|---|---|---|

| Outright claim assignment | Chose in action itself, conveyed to a purchaser who then prosecutes | None; buyer takes 100% outcome risk | 10-30 cents on expected-value dollar | No, buyer is now named plaintiff |

| Monetization advance | Cash today against defined share of any future recovery | None; funder paid only out of recovery | Advance + 3-5x multiple cap on recovery | Yes, plaintiff controls litigation |

| Portfolio funding | Cash today against basket of claims | None at portfolio level | Tighter multiples (2-3x cap) reflecting diversification | Yes, plaintiff or law firm retains control |

Outright claim assignment. The chose in action itself is conveyed by assignment to a purchaser who then prosecutes the case in its own name. The buyer takes 100% of the outcome risk and 100% of the recovery. The claimant exits entirely.

This structure is rare for pharmaceutical claims because most state laws restrict outright assignment of legal claims, and even where assignment is permitted, attorney-client privilege and work product protections do not automatically transfer to the assignee. Typical pricing on the rare outright assignments is 10% to 30% of probability-weighted expected value, reflecting both the litigation risk and the structural friction.

Monetization or advance against recovery. Cash today against a defined share of any future recovery, with the plaintiff retaining control of the case. This is the modal modern structure, pioneered by Burford Capital and now standard across the institutional litigation finance industry.

The economic structure is typically (i) the funder advances a defined cash sum to the claimant at signing, (ii) the claimant retains all litigation control, attorney selection, and settlement authority, (iii) on a successful resolution, the funder receives the greater of a multiple of advance (typically 2x to 5x) or a defined percentage of recovery (typically 15% to 35%), capped at a defined ceiling, and (iv) on a failed resolution, the funder receives nothing and the claimant keeps the advance.

The Burford Fortune 100 case study is the standard public example: $75 million advanced to a Fortune 100 plaintiff in an antitrust opt-out claim, later increased to $140 million as additional cases were added as collateral.

Portfolio funding. Cash today against a basket of claims, with risk pooled across multiple litigation and arbitration matters. The structure is non-recourse at the portfolio level rather than at the individual claim level.

This structure is most common in law firm financings (where the firm pools its contingency cases as collateral) but appears with increasing frequency in corporate contexts where a single claimant has multiple monetizable claims. Pricing is tighter than single-case structures (typically 2x to 3x advance multiple) reflecting the diversification benefit.

Shared economic properties

Three properties define the asset class across all three archetypes.

| Property | Mechanism | Implication |

|---|---|---|

| Non-recourse | Funder's return contingent on successful resolution | Loss scenarios produce zero recovery; advance is kept regardless |

| Off-balance-sheet | Capital is not debt; no interest accrual, no fixed maturity | Not subject to existing financial covenants |

| Champerty constraints | Many U.S. states still restrict third-party funding | Structuring (financing vs. purchase) and governing law matter |

Omni Bridgeway summarizes the position on non-recourse: "Omni Bridgeway's capital is non-recourse, meaning that a return on investment is collected only if the case is successful. If the claimant does not recover any proceeds from their case by way of settlement, judgment, award or otherwise, it is not obligated to repay the funder."

The off-balance-sheet treatment is structurally important. The capital is not debt. It is not subject to financial covenants, does not accrue interest, has no fixed maturity, and (in most accounting frameworks) is not recognized as a financial liability on the claimant's balance sheet. For pharmaceutical companies operating under tight debt covenants from senior lenders or royalty financiers, this off-balance-sheet treatment is structurally important.

The Institute for Legal Reform's recent summary captures the regulatory status: "Traditionally, the common law doctrines of maintenance and champerty prohibited non-parties from financing litigation, but recently some jurisdictions have relaxed these outright prohibitions."

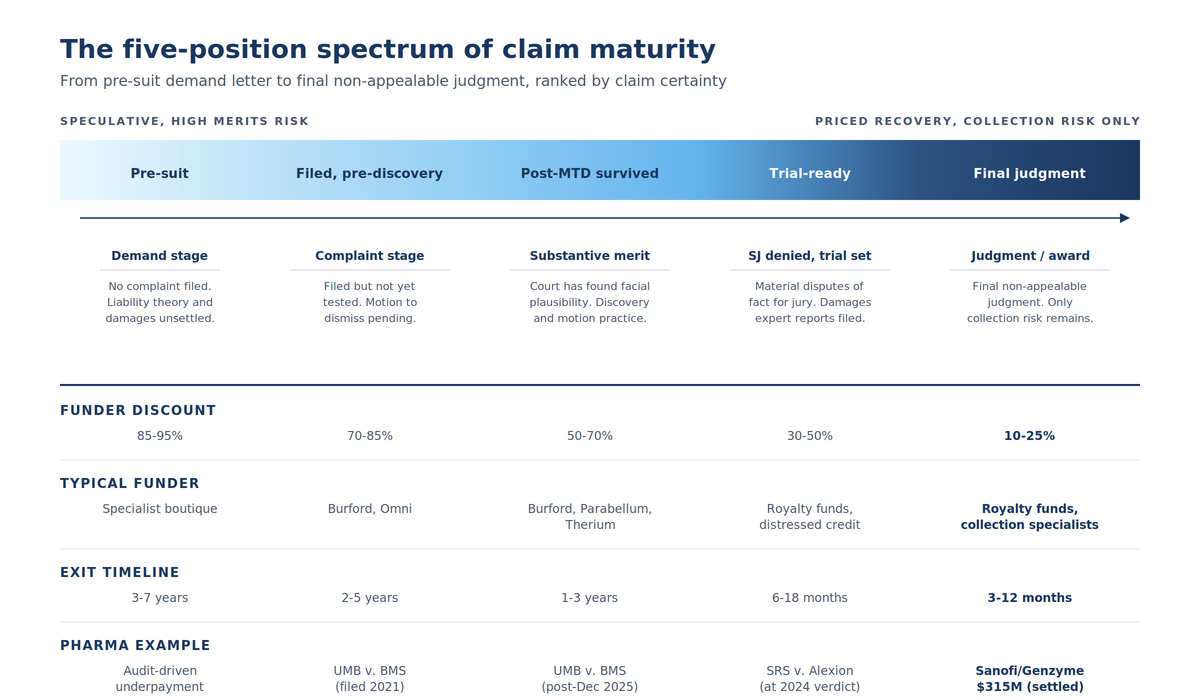

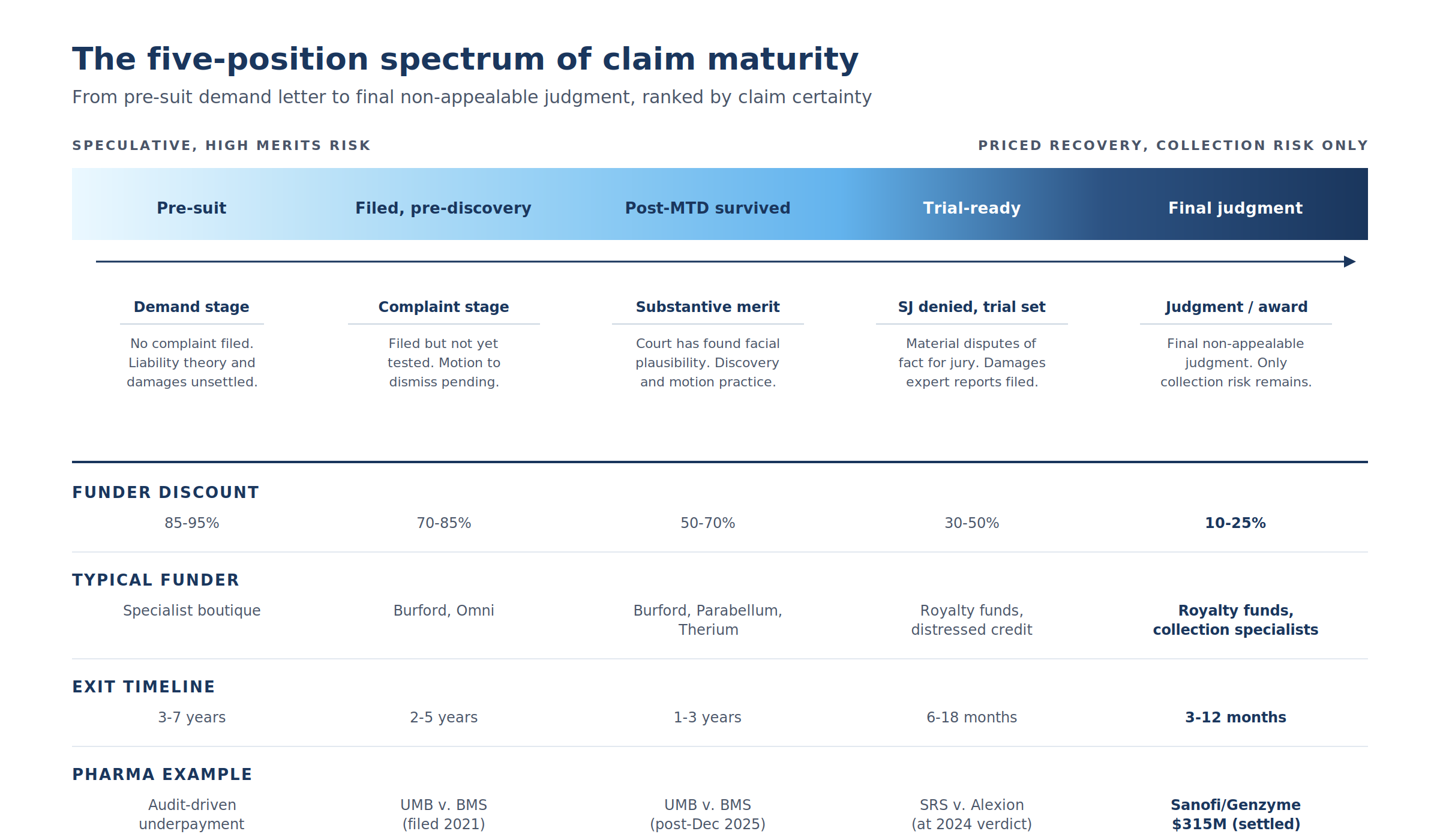

The five-position spectrum of claim maturity

Litigation claims exist on a continuum from pre-suit demand letter (no complaint yet filed, liability theory and damages unsettled) to final non-appealable judgment (only collection risk remains). Each position implies a different funder discount, a different typical exit timeline, and a different fit for the underlying transaction.

The spectrum collapses into five identifiable positions, summarized below before the detailed discussion of each.

| Position | Procedural posture | Funder discount | Exit timeline | Typical funder | Pharma example |

|---|---|---|---|---|---|

| Pre-suit demand | No complaint filed; liability theory unsettled | 85-95% | 3-7 years | Specialist boutiques | Audit-driven underpayment |

| Filed, pre-discovery | Complaint filed; MTD pending | 70-85% | 2-5 years | Burford, Omni Bridgeway | UMB v. BMS (filed June 2021) |

| Post-MTD survived | Court found facial plausibility; discovery starts | 50-70% | 1-3 years | Burford, Parabellum, Therium | UMB v. BMS (post-Dec 2025 ruling) |

| Trial-ready | SJ denied; material disputes for jury | 30-50% | 6-18 months | Royalty funds, distressed credit | SRS v. Alexion (Sept 2024 liability) |

| Final judgment | Non-appealable judgment; collection risk only | 10-25% | 3-12 months | Royalty funds, collection specialists | Sanofi/Genzyme (settled 2019) |

Pre-suit demand stage. No complaint has been filed. The claimant has identified a potential cause of action, possibly issued a demand letter, but has not yet committed to the cost and visibility of litigation. The merits, damages theory, and liability quantum are all unsettled.

Funder discount at this position is the deepest, typically 85% to 95% of expected recovery, reflecting the combined merits, discovery, and trial risk. Typical funders are specialist boutiques willing to underwrite the risk in exchange for the largest possible multiple. The typical exit timeline is three to seven years.

For pharmaceutical royalty finance, the most common pre-suit position is an audit-driven royalty underpayment claim. A licensor has conducted a routine royalty audit, found a material discrepancy, and is preparing a demand letter. Big Four audit firm reports indicate that royalty audits routinely disclose under-reporting in excess of 10% across industries, with regulated pharmaceuticals at the lower end but still material.

Filed, pre-discovery. The complaint has been filed but not yet tested on the merits. A motion to dismiss is typically pending, and the defendant's responsive pleading frames the contested issues.

Funder discount is 70% to 85% of expected recovery. Burford, Omni Bridgeway, and the other major institutional funders are active at this position. The typical exit timeline is two to five years.

The UMB Bank v. BMS filing in June 2021 sits at this position when first filed. UMB, acting as trustee for former Celgene shareholders, alleged that BMS breached the CVR agreement by failing to apply "diligent efforts" to secure FDA approval of Liso-cel (Breyanzi) by the December 31, 2020 deadline. The 36-day miss converted what would have been a $6.4 billion CVR payment into a complete forfeiture, and the litigation was structured to recover those amounts plus interest.

Post-MTD survived. The court has denied the motion to dismiss or granted only in part, signaling that the claims pled state a facially plausible cause of action under Bell Atlantic Corp. v. Twombly. Discovery and motion practice begin in earnest.

Funder discount is 50% to 70%. Burford, Parabellum, and Therium are the typical funders at this position. The exit timeline is one to three years.

The UMB Bank v. BMS case post-December 2025 ruling sits at this position. Judge Furman's December 1, 2025 decision rejected BMS's bid to dismiss the $6.7 billion lawsuit and allowed UMB to pursue claims for breach of contract and breach of implied covenant of good faith. The judge "rejected Bristol Myers' claim that its alleged lack of diligence did not trigger an 'event of default,' and said a jury should decide whether Bristol Myers breached an implied agreement to act in good faith by delisting the CVRs."

The procedural posture means the claim is no longer speculative at the threshold; it has survived the principal substantive challenge and is now in a contested discovery and pre-trial phase.

Summary judgment denied, trial set. Material disputes of fact remain for a jury. Damages expert reports have been filed. The case has matured into a litigation asset with defined contours.

Funder discount is 30% to 50%. Royalty funds and distressed credit specialists begin to be plausible buyers at this position, alongside the traditional litigation finance funders. The exit timeline is six to eighteen months.

The SRS v. Alexion Pharmaceuticals case sits at this position from the September 2024 liability ruling through the June 2025 damages award. Vice Chancellor Zurn found Alexion liable for breach of its commercially reasonable efforts obligation to develop ALXN1830 after the Syntimmune acquisition. The merger agreement had defined CRE by reference to "a hypothetical, similarly situated biotechnology company would take under the circumstances," an outward-facing standard that "did not leave room for Alexion to deprioritize and then terminate the development program at issue based on idiosyncratic, company-specific priorities."

Final judgment or arbitral award. A final non-appealable judgment or award has been entered. Only collection risk remains: the defendant's solvency, willingness to pay, and (if cross-border) the enforceability of the judgment in the defendant's home jurisdiction.

Funder discount narrows to 10% to 25%, reflecting the dramatically reduced uncertainty. Royalty funds, collection specialists, and increasingly traditional fixed-income investors are buyers at this position. The exit timeline is three to twelve months.

The Sanofi/Genzyme Lemtrada $315 million settlement in 2019 is the canonical pharmaceutical example of the post-judgment position. The case had been pending since 2015 and had survived multiple motions to dismiss; by the time of settlement, the question was no longer whether Sanofi had breached but how the damages should be calculated. The settlement value represented approximately 8% of the maximum potential $3.8 billion CVR exposure, with the discount reflecting the residual litigation and collection risk on the post-judgment outcome.

The spectrum collapses to a single economic principle: each step rightward narrows the funder discount, compresses the exit timeline, and broadens the universe of potential buyers from specialist litigation funders to mainstream credit and royalty investors. The rightward positions are gated by procedural progress and judicial decisions, which is why claim maturity rather than economic merit is often the primary determinant of monetization terms.

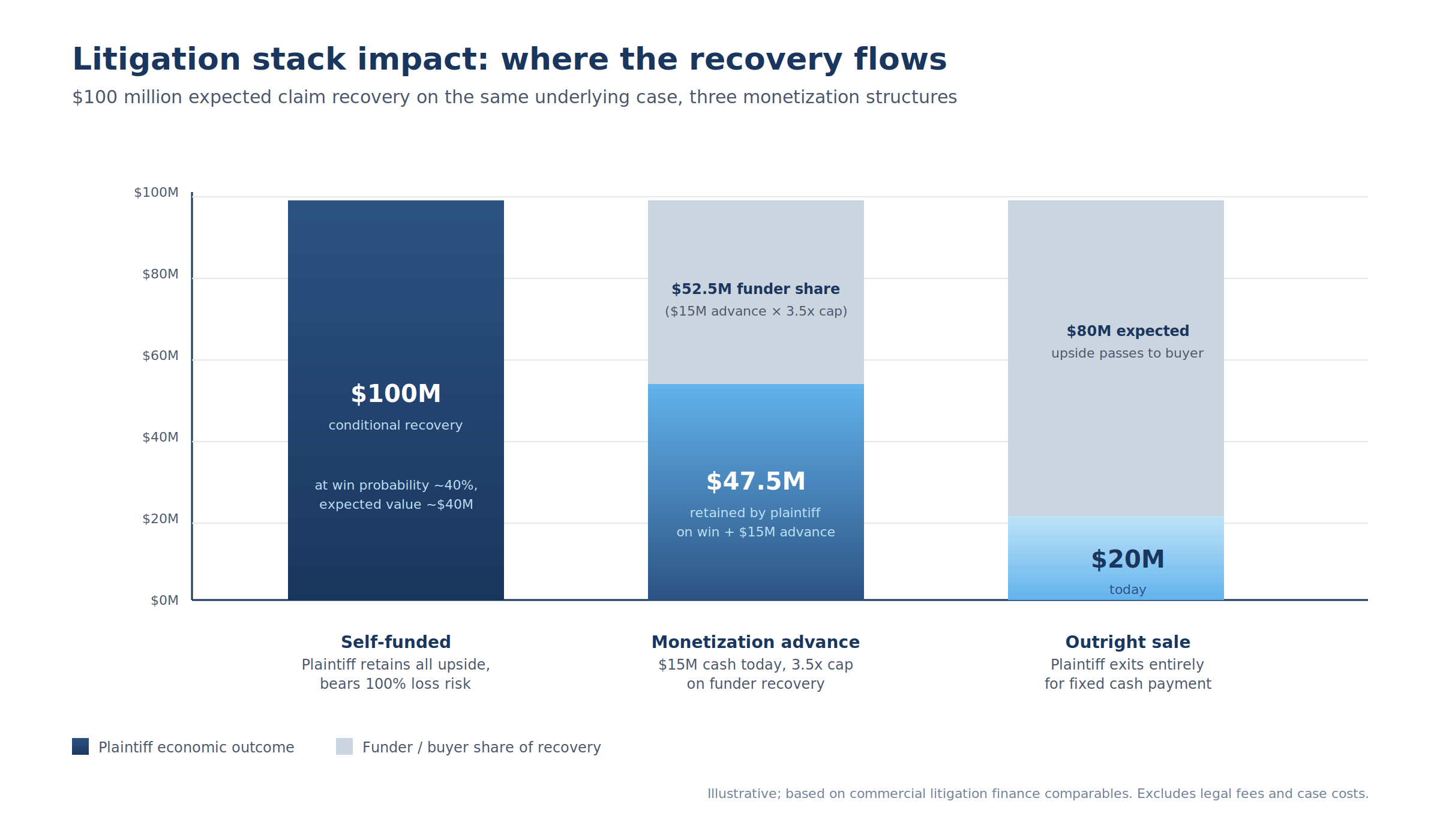

Litigation stack impact: where the recovery flows

The economic distinction between these positions becomes vivid when traced through a representative $100 million expected claim recovery. Assume a single claimant holding a pharmaceutical breach-of-efforts CVR claim with $100 million in damages at stake, a probability of plaintiff success estimated at 40%, and an expected exit timeline of three to four years from current procedural posture.

The three scenarios summarized:

| Scenario | Plaintiff outcome on win | Plaintiff outcome on loss | Funder outcome on win | Funder outcome on loss | Plaintiff expected value (40% win) |

|---|---|---|---|---|---|

| Self-funded | $100M | $0M | n/a | n/a | $40M |

| Monetization advance ($15M, 3.5x cap) | $47.5M + $15M advance = $62.5M | $15M advance kept | $52.5M | $0 | $34M (plus $15M cash certainty) |

| Outright sale | $20M | $20M | $100M | $0 | $20M |

In the self-funded case, the claimant prosecutes the case using its own balance sheet (or under a partial contingency arrangement with outside counsel), receives the full $100 million if it wins, and receives nothing if it loses. The probability-weighted expected value is $40 million, but the realized outcome is binary.

The claimant bears 100% of the litigation risk, must reserve cash for legal fees and case costs estimated at $5 million to $15 million for a multi-year complex commercial dispute, and cannot recognize any revenue from the claim until final resolution. For pharmaceutical companies operating with constrained working capital, the opportunity cost of holding a single illiquid binary asset can be substantial.

In the monetization advance case, the claimant accepts $15 million in upfront cash from a litigation funder in exchange for a defined share of any future recovery. The typical structure caps the funder's recovery at 3.5x of advance, with a fallback percentage in case the recovery exceeds the multiplied advance.

On a winning outcome of $100 million, the funder receives $52.5 million (15 × 3.5) and the claimant receives the remaining $47.5 million plus the $15 million advance, for a total of $62.5 million. On a losing outcome, the claimant keeps the $15 million advance and the funder receives nothing.

The expected-value math is straightforward: at 40% win probability, the claimant's expected outcome is $15 million × 1.0 (advance, kept regardless) + $47.5 million × 0.4 = $34 million. The self-funded case had a $40 million expected value, so the monetization costs the claimant $6 million of expected value in exchange for $15 million of certain cash and full transfer of downside risk.

For most pharmaceutical claimants, the trade is structurally attractive. The $15 million of immediate cash funds working capital, R&D, or distributions to shareholders without diluting equity, taking on debt, or pledging the underlying royalty stream. The risk transfer means the claim outcome no longer affects the claimant's financial covenants or going-concern assessment.

In the outright sale case, the claimant sells the entire claim to a buyer for $20 million in cash today. The claimant exits the litigation entirely, the buyer becomes the named plaintiff, and the buyer assumes all upside and downside.

The buyer's expected return is the $100 million × 40% probability = $40 million expected value, less the $20 million purchase price, less the buyer's own legal and case costs of $10 million to $20 million through resolution. The net expected return for the buyer is therefore in the $0 million to $10 million range, with a wide variance reflecting the binary outcome.

Outright sales are rare in pharmaceutical claims because of the privilege and work-product issues described below, but they appear occasionally for very large claims where the original claimant prefers the certainty of immediate exit to the continued operational distraction of litigation.

Second-order effects on the royalty stack

Three specific effects warrant attention.

| Effect | Mechanism | Why it matters |

|---|---|---|

| Capital structure independence | Non-recourse capital not classified as debt | Avoids existing royalty/credit facility covenant issues |

| Recovery timing alignment | Litigation recovery lags royalty stream by years | Creates two cash streams to manage |

| Settlement coordination | Funder may want fastest cash; claimant may value licensee relationship | Settlement authority terms become sensitive |

Capital structure independence. Non-recourse litigation capital does not appear as debt on the claimant's balance sheet. For pharmaceutical companies with existing senior debt or royalty financing, the litigation finance proceeds are not subject to the financial covenants, anti-layering restrictions, or affirmative covenants of those existing facilities. The structural independence is meaningful for biotechs operating under tight covenants from royalty buyers, who would otherwise need to obtain consent for any new financing.

Recovery timing alignment. The litigation finance recovery typically lags the principal royalty stream recovery by years. A claimant that has monetized both its forward royalty entitlement (to a royalty fund) and its pending royalty audit claim (to a litigation funder) ends up with two distinct cash flow streams, one running through the licensee's normal payment process and one running through the litigation finance funder's distribution waterfall. The two structures can interact in unexpected ways. For example, a royalty purchase agreement may include a representation that the seller has no pending or threatened material disputes with the licensee, which the audit claim could potentially breach. Pre-signing diligence and explicit disclosure of any pending claims is essential.

Settlement coordination. When a pharmaceutical claim is litigated against a counterparty that is also a commercial licensee, the litigation funder's incentives may not be perfectly aligned with the claimant's. The funder typically wants the largest possible cash recovery in the shortest possible time, while the claimant may value the continued commercial relationship with the licensee. Most modern litigation finance agreements address this by giving the claimant final settlement authority, subject to certain economic minimums or "waterfall" provisions that protect the funder's return. The negotiation of these provisions is one of the more sensitive aspects of pharmaceutical litigation finance structuring.

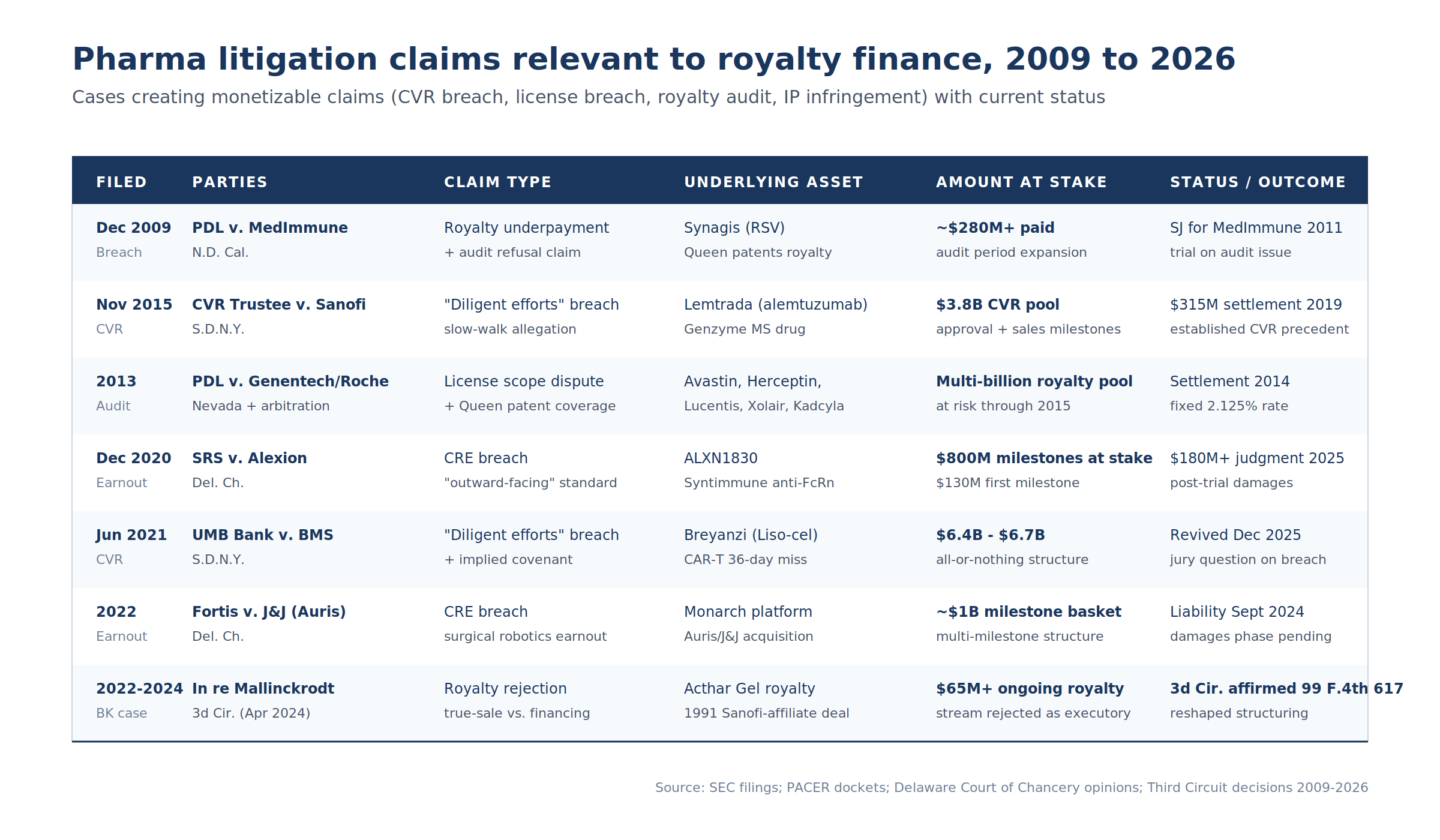

Recent deal evidence: pharma litigation cohort, 2009 to 2026

The 2009 to 2026 cohort of pharmaceutical litigation claims relevant to royalty finance illustrates the range of monetizable disputes and the variation in resolution outcomes. Seven representative cases span the principal claim types: royalty underpayment, CVR breach, license scope dispute, earnout breach, and royalty rejection in bankruptcy.

The summary table before the case-by-case discussion:

| Case | Filed | Court | Claim type | Stake | Status |

|---|---|---|---|---|---|

| PDL v. MedImmune | Dec 2009 | N.D. Cal. | Royalty underpayment + audit | ~$280M+ paid through 2009 | SJ for MedImmune Jan 2011; later settled |

| CVR Trustee v. Sanofi | Nov 2015 | S.D.N.Y. | "Diligent efforts" breach | $3.8B CVR pool | $315M settlement Oct 2019 |

| PDL v. Genentech/Roche | 2013 | Nevada + arbitration | License scope + audit | Multi-billion royalty pool | Settlement 2014: 2.125% rate |

| SRS v. Alexion | Dec 2020 | Del. Ch. | CRE breach (outward-facing) | $800M milestones | $180M+ damages June 2025 |

| UMB Bank v. BMS | Jun 2021 | S.D.N.Y. | "Diligent efforts" + implied covenant | $6.4B-$6.7B | Revived Dec 1, 2025 |

| Fortis v. J&J (Auris) | 2022 | Del. Ch. | CRE breach (surgical robotics) | ~$1B milestone basket | Liability Sept 2024 |

| In re Mallinckrodt | 2022-2024 | 3d Cir. | Royalty rejection (executory) | $65M+ ongoing | 99 F.4th 617 affirmed Apr 2024 |

The PDL v. MedImmune Synagis litigation, filed in December 2009 in the Northern District of California, is the canonical pharmaceutical royalty audit dispute. PDL alleged that MedImmune had breached its license agreement by failing to pay royalties on sales of Synagis through Abbott Laboratories (MedImmune's exclusive ex-U.S. distributor) and by refusing to allow PDL to conduct a contractually-permitted audit of sales and revenue.

PDL had received more than $280 million in royalties from MedImmune through the fourth quarter of 2009, and the dispute centered on additional royalties allegedly owed under the broader scope of the Queen patents. The court ruled in a January 2011 summary judgment decision that the patent claim asserted as the basis for infringement was invalid as anticipated by prior art, and that MedImmune had not breached its license agreement obligations.

The audit-cooperation portion of the dispute survived for jury trial. The case ultimately resolved through settlement, but its trajectory through three years of summary judgment motion practice illustrates the timeline and pricing dynamics of pre-trial commercial royalty disputes.

The Sanofi/Genzyme CVR Lemtrada litigation, filed November 2015 in the Southern District of New York, is the foundational modern CVR breach precedent. Genzyme shareholders, represented by the CVR trustee, alleged that Sanofi had breached the "diligent efforts" provision of the 2011 acquisition CVR agreement by deliberately slowing development of Lemtrada (the multiple sclerosis therapeutic) to avoid milestone payments.

The complaint specifically alleged that Sanofi "embarked on a slow path to FDA approval and departed from its own drug commercialization patterns and those of others in the industry," contrasting Sanofi's treatment of Lemtrada with its parallel development of Aubagio, a competing MS drug that was not subject to CVR payments. The court found that the complaint adequately stated a claim, with the Lexology analysis noting that the court "found that the Trustee on behalf of the CVR holders pled sufficient facts to raise a reasonable inference that Sanofi breached its agreement to use diligent efforts."

The case settled for $315 million in 2019, representing approximately 8% of the maximum potential $3.8 billion CVR exposure. The settlement established the CVR-breach legal precedent that the BMS, Alexion, and J&J cases would later build on.

The PDL v. Genentech and Roche audit dispute, prosecuted in Nevada state court and parallel arbitration proceedings from approximately 2013, illustrates the multi-billion-dollar scale that pharmaceutical license disputes can reach. PDL's Queen patents covered the production of Avastin, Herceptin, Lucentis, Xolair, Kadcyla, and Perjeta, generating a royalty stream estimated at hundreds of millions of dollars annually.

The dispute concerned the license scope, the patent coverage, and the proper audit procedures. The 2014 settlement established (i) a fixed royalty rate of 2.125% on worldwide sales (replacing the previous tiered rate), (ii) the parties' agreement that all six products were licensed products, (iii) preclusion from challenging the validity of the Queen patents, and (iv) defined audit inspection procedures. The settlement extracted multi-billion-dollar value from the dispute and illustrates that license audit and patent coverage disputes can be the largest royalty-related litigation claims in the industry.

The SRS v. Alexion Pharmaceuticals litigation, filed December 2020 in the Delaware Court of Chancery, is the textbook modern CRE breach case. SRS, as shareholder representative for former Syntimmune stockholders, alleged that Alexion breached its commercially reasonable efforts obligation under the 2018 Syntimmune acquisition agreement by deprioritizing and ultimately terminating the ALXN1830 development program.

Vice Chancellor Zurn's September 2024 liability ruling found that the merger agreement's outward-facing CRE definition, benchmarked against "what a comparable biopharmaceutical company would do when developing a similar product under similar circumstances," did not permit Alexion to deprioritize the program based on company-specific portfolio decisions. The June 2025 damages ruling awarded former stockholders more than $180 million, with the October 2025 supplemental ruling addressing interest calculations.

The Alexion case has become the de facto template for modern CVR and earnout drafting, with both buyers and sellers carefully considering whether efforts standards should be inward-facing (referenced to the buyer's own conduct) or outward-facing (referenced to a hypothetical comparable company).

The UMB Bank v. Bristol Myers Squibb litigation is the largest pending pharmaceutical CVR breach case. UMB, as successor trustee under the 2019 BMS-Celgene merger CVR agreement, alleges that BMS breached the diligent efforts obligation by failing to secure FDA approval for Breyanzi (Liso-cel), Abecma (Ide-cel), and Ozanimod by the contractual milestone deadlines.

The procedural history is consequential. The case was originally filed in June 2021. Judge Furman dismissed UMB's standing in 2024, ruling that UMB had not been properly appointed as successor trustee. UMB refiled in November 2024 after correcting the procedural defect, and Judge Furman's December 1, 2025 ruling denied BMS's renewed motion to dismiss. The judge held that "a jury should decide whether Bristol Myers breached an implied agreement to act in good faith by delisting the CVRs" and that "the company's alleged lack of diligence" could trigger an event of default.

The damages claim is $6.7 billion. At post-MTD-survived position, the case represents one of the largest single litigation finance opportunities in the U.S. corporate litigation market, with the timing and outcome of the litigation having multi-billion-dollar implications for both BMS and the CVR holders.

The Fortis v. Johnson & Johnson (Auris) litigation, decided alongside Alexion in the Delaware Court of Chancery, addressed the surgical robotics earnout from J&J's $3.4 billion acquisition of Auris Health in 2019. Vice Chancellor Glasscock's September 4, 2024 ruling found that J&J had breached its commercially reasonable efforts obligation in the development of the Monarch platform.

The damages phase is pending as of early 2026. The combined Alexion and Auris rulings establish a clear Delaware Chancery position that outward-facing CRE definitions impose meaningful enforceable obligations on acquirers, distinct from the inward-facing standard the courts have applied where the contractual language is less specific.

The In re Mallinckrodt litigation, affirmed by the Third Circuit at 99 F.4th 617 in April 2024, reshaped the structural treatment of pharmaceutical royalty agreements in bankruptcy. The court held that Mallinckrodt's obligation to pay ongoing royalties on Acthar Gel under a 1991 deal with a Sanofi affiliate was an "executory contract" that could be rejected in Chapter 11.

The decision is not itself a non-recourse litigation sale but it dramatically affects the underwriting of pharmaceutical claims generally. Royalty sellers, CVR holders, and earnout claimants must now diligence the bankruptcy treatment of their claims with particular care, structuring transactions to qualify as true sales rather than secured financings wherever possible to avoid the Mallinckrodt outcome.

Case-specific monetization positions today

| Case | Position today | Estimated funder discount | Notes |

|---|---|---|---|

| UMB Bank v. BMS | Post-MTD survived (Dec 2025) | 50-70% | Largest pending pharma claim |

| SRS v. Alexion | Final judgment + interest | 10-15% | Only collection risk; appeal possible |

| Fortis v. J&J | Trial-ready (damages phase) | 30-50% | Liability decided; damages to be determined |

| Sanofi/Genzyme | Resolved (settled 2019) | n/a | Reference precedent |

| PDL v. MedImmune | Resolved (settled) | n/a | Reference precedent |

| PDL v. Genentech/Roche | Resolved (settled 2014) | n/a | Reference precedent |

| Mallinckrodt | Resolved (3d Cir. affirmed) | n/a | Reshaped post-bankruptcy structuring |

The pattern across this cohort is clear. Pharmaceutical litigation claims of significant size (typically $50 million and above) are now routinely structured as monetizable assets. The institutional litigation finance industry has developed the underwriting capacity, the legal infrastructure, and the standardized documentation to price and transact these claims at every position on the maturity spectrum.

The legal architecture: champerty, assignability, privilege, and bankruptcy

The interaction between contractual provisions for non-recourse capital, statutory and common-law restrictions on litigation funding, attorney-client privilege, work product protection, and bankruptcy treatment is the central legal puzzle of non-recourse litigation sales.

Champerty and maintenance

The common-law doctrines of champerty (financing litigation in exchange for a share of recovery) and maintenance (financing litigation as an intermeddler) historically prohibited third-party litigation funding in most U.S. jurisdictions. The doctrines have been substantially relaxed since 2010, but the relaxation varies meaningfully by state.

| Jurisdiction | Treatment of litigation finance | Notes |

|---|---|---|

| New York | Permissive | NY Judiciary Law § 489 narrowly construed |

| Delaware | Permissive | Express acceptance of commercial litigation finance |

| California | Permissive | Champerty challenges rejected in modern cases |

| Illinois, Texas | Permissive | Federal courts apply permissive approach |

| Arkansas, Indiana, Mississippi | Restrictive | Traditional champerty doctrine retained |

| Ohio | Mixed | Specific disclosure and registration requirements |

New York's champerty statute (NY Judiciary Law § 489) prohibits the assignment of claims for the purpose of bringing suit, but courts have generally interpreted the statute narrowly to exclude commercial litigation finance arrangements where the primary purpose is financing rather than litigation in the funder's own name. Delaware has explicitly accepted commercial litigation finance under Delaware law. California has rejected champerty challenges in modern litigation finance cases. Illinois, Texas, and the federal courts generally apply a permissive approach.

But other states (Arkansas, Indiana, Mississippi, Ohio at certain times) have retained more restrictive doctrines or imposed specific disclosure and registration requirements on litigation funders. Pharmaceutical claimants with potential venue choices should consider the governing-law and venue implications carefully.

Assignability of claims

Even where champerty does not apply, the assignability of a particular claim depends on the nature of the claim and the contractual provisions in the underlying agreement.

| Claim type | Assignable by default? | Override mechanism |

|---|---|---|

| Personal-injury / tort | No | Limited exceptions only |

| Contract claims | Generally yes | Contract may prohibit |

| Royalty receivables | Yes (payment intangible) | UCC § 9-406 override applies |

| Breach-of-warranty | Generally yes | Subject to contract terms |

| Intellectual property licenses | Personal-services treatment | License consent typically required |

For pharmaceutical claims, the most common assignability issue is the anti-assignment clause in the underlying license, CVR agreement, or merger agreement. A claim arising under an agreement that prohibits assignment may itself be inalienable absent the obligor's consent. The interaction with UCC § 9-406 and § 9-408 overrides for security interest purposes is complex; the override applies for security-interest perfection but not necessarily for outright assignment.

Attorney-client privilege and work product

Communications between the claimant and its outside counsel about a pending or anticipated litigation are protected by attorney-client privilege. The privilege is generally not waived by sharing communications with a litigation funder under a properly-drafted confidentiality and common-interest agreement.

| Protection | Source | Survives sharing with funder? |

|---|---|---|

| Attorney-client privilege | Common law + state codes | Yes, under common-interest agreement |

| Work product (fact) | FRCP 26(b)(3) | Yes, "anticipation of litigation" survives |

| Work product (opinion) | FRCP 26(b)(3) higher standard | Yes, with stronger protection |

| Funder's own analysis | Work product (funder's) | Generally protected |

| Funder's communications | Common-interest doctrine | Protected if properly documented |

The Federal Rule of Evidence 502 and the work product doctrine codified in Federal Rule of Civil Procedure 26(b)(3) provide additional protection. Most federal courts have held that materials shared with a litigation funder for purposes of evaluating the funding decision are protected under the common-interest doctrine, though some courts have applied a stricter standard.

The funder's own analytical work (probability assessments, damages models, settlement valuations) is typically protected as the funder's work product, but the question of whether sharing the funder's analysis with the claimant breaks the privilege has been litigated repeatedly. The current consensus is that information shared between funder and claimant for purposes of evaluating the case is protected, but the line is not perfectly clear.

Pharmaceutical claimants should document the diligence-sharing relationship with the funder carefully, requiring a confidentiality and common-interest agreement to be in place before sharing any privileged or work-product materials.

Disclosure of funding

Federal courts and certain state courts have begun to require disclosure of litigation funding arrangements, particularly in class action and multi-district litigation contexts.

| Court / forum | Disclosure required? | Scope |

|---|---|---|

| D.N.J. | Yes (local rule) | Funder identity + no-control representation |

| N.D. Cal. | Yes (local rule) | Similar to D.N.J. |

| Federal courts (general) | Case-by-case | Increasing trend in MDL contexts |

| Delaware Chancery | Generally no | Standard practice does not require |

| S.D.N.Y. | Generally no | Standard practice does not require |

| State trial courts | Variable | Some require for class actions |

The U.S. District Court for the District of New Jersey has a standing local rule requiring disclosure of funding arrangements. The Northern District of California has similar local provisions. The disclosure requirement does not typically reveal the economic terms of the funding (which remain protected as commercial-in-confidence) but does require identification of the funder and confirmation that the funder has no control over the litigation.

Bankruptcy treatment

The bankruptcy treatment of non-recourse litigation finance proceeds depends on the structure of the transaction.

| Transaction structure | Treatment in claimant bankruptcy | Treatment in defendant bankruptcy |

|---|---|---|

| Pure non-recourse advance (true sale) | Not part of estate (sale of recovery share) | Defendant's bankruptcy stays litigation |

| Recourse financing | Part of estate as financial liability | Same as above |

| Outright claim assignment | Asset already transferred; not in estate | Same as above |

| Portfolio funding | Mixed; document-dependent | Same as above |

A pure non-recourse advance characterized as a sale of a portion of recovery is typically not a debt obligation and is not part of the claimant's bankruptcy estate. A monetization characterized as a secured loan against the claim, however, would create a financial liability on the claimant's balance sheet that would be part of the estate in any subsequent bankruptcy. The Mallinckrodt decision reinforces the structural importance of true-sale characterization in any context where bankruptcy risk is meaningful.

For pharmaceutical claimants with going-concern uncertainties (typically late-stage biotechs running on negative working capital), the bankruptcy treatment of any litigation finance facility is a non-trivial diligence item.

Cross-border enforceability

Where the litigation claim is being prosecuted in U.S. courts but the funder, the claimant, or the defendant is located outside the United States, the choice-of-law and enforcement analysis becomes layered. UK litigation finance is permitted under the Damages-Based Agreements Regulations 2013, but the regime is different from the U.S. model in several important respects.

EU member states vary widely in their treatment of litigation funding, with the European Parliament's 2022 resolution on third-party litigation funding pushing for greater regulation. Cross-border pharmaceutical claims that involve U.S., UK, and EU dimensions should be structured with careful attention to the applicable regulatory regimes.

Accounting and financing consequences

The accounting and financing treatment of non-recourse litigation sales has several non-obvious implications for both claimants and funders.

Accounting recognition

Cash received from a non-recourse litigation funder is not debt and is not equity. The accounting characterization under U.S. GAAP depends on the substantive economics of the transaction.

| Transaction characterization | Cash treatment | Balance sheet | Income recognition |

|---|---|---|---|

| Sale of recovery share | Gain on sale | Reduce claim asset; recognize gain | At closing |

| Deferred revenue | Liability | Deferred revenue | On claim resolution |

| Financing (loan) | Liability | Financial liability | Interest over time |

Where the funding is properly characterized as a sale of a portion of future litigation recovery (true sale), the cash is recognized as either (i) a sale of a financial asset (the litigation claim, valued at its expected recovery) with corresponding gain on sale, or (ii) deferred revenue, recognized only on claim resolution.

Where the funding is characterized as a financing (essentially a loan repayable only out of recovery proceeds), the cash is recognized as a financial liability with interest expense recognized over time and the liability extinguished only on claim resolution.

The choice between sale and financing characterization is one of the more contested areas of litigation finance accounting. The trend in recent years has been toward sale characterization for pure non-recourse advances, with financing characterization reserved for arrangements that include meaningful recourse to other assets.

Tax treatment

The federal income tax treatment of non-recourse litigation finance proceeds depends on the substantive characterization.

| Structure | Federal income tax | Capital gain eligibility |

|---|---|---|

| Sale of portion of recovery | Capital gain (LTCG if held >1 year) | Yes |

| Financing arrangement | No immediate tax; borrowed funds | n/a |

| Outright claim sale | Capital or ordinary depending on basis | Depends on character |

A sale of a portion of recovery generates capital gain (long-term if held for more than one year) on the difference between the sale price and the claimant's basis in the claim. A financing arrangement generates no immediate taxable income at the advance stage; the proceeds are treated as borrowed funds. The eventual recovery is then offset against the financing repayment, with interest expense potentially deductible.

For pharmaceutical claimants, the tax characterization can matter substantially because of the typical net operating loss positions of clinical-stage biotechs and the timing of recovery relative to existing tax attributes.

Disclosure obligations

Public-company claimants must consider whether the litigation funding arrangement is required to be disclosed under SEC rules. The disclosure analysis typically focuses on materiality and the impact on the claimant's reported financial position.

| Claimant type | Disclosure trigger | Form |

|---|---|---|

| Public pharma company | Material funding + characterization | 8-K + 10-K/10-Q exhibit |

| CVR / trustee plaintiff | Trustee reporting only | Trustee notice to holders |

| Private claimant | Generally none | Confidentiality clauses |

| Class action plaintiff | Court-ordered in some venues | Local rule disclosure |

Where the funding is material and characterized as a sale, disclosure on Form 8-K may be required. Where the funding is material and characterized as a financing, the same disclosure plus inclusion of the funding agreement in the next 10-K or 10-Q exhibit list may be required.

Capital structure and covenants

For pharmaceutical claimants with existing senior debt or royalty financing, the question is whether the litigation finance arrangement constitutes "indebtedness" under the existing facility documents.

| Existing financing | Litigation finance implication | Action required |

|---|---|---|

| Senior secured debt | Confirm carveout for non-recourse | Pre-signing check |

| Royalty purchase agreement | Confirm no breach of representations | Pre-signing check |

| Synthetic royalty | Confirm covenants permit | Pre-signing check |

| Convertible notes | Generally permissive | Standard review |

Most modern indebtedness definitions in royalty purchase agreements and credit facilities explicitly carve out non-recourse arrangements that do not encumber the claimant's general assets. But the carveout is not universal, and pre-signing diligence is essential to confirm that the proposed litigation funding does not breach an existing covenant.

The Verona Pharma OMERS strategic financing of $650 million in 2025 is illustrative of the kind of senior financing facility whose covenants would need to be diligenced before any subsequent litigation funding could be put in place.

Information rights and reporting

Non-recourse litigation finance agreements typically grant the funder defined information rights with respect to the underlying case: periodic case status reports, copies of significant pleadings, settlement offer disclosures, and consultation on major strategic decisions. The information rights are typically structured to preserve attorney-client privilege through the use of common-interest doctrine, and the funder is bound by confidentiality with respect to all received information.

For pharmaceutical claimants, the practical operational burden of complying with the funder's information rights is typically modest, but the integration with existing reporting obligations (to royalty funds, senior lenders, and public shareholders) should be coordinated carefully.

What this means for new deals

Four implications follow for the negotiation, structuring, and execution of non-recourse litigation sales in 2026 and beyond, particularly for pharmaceutical claimants and royalty funds.

For pharmaceutical claimants with pending or threatened claims

The non-recourse litigation finance market has matured to the point where most material commercial claims (typically $25 million and above in disputed amounts) are economically monetizable. The recommended sequence:

| Stage | Action |

|---|---|

| Dispute identification | Preliminary valuation across range of probability and damages outcomes |

| Demand letter / filing | Solicit indications from established funders (Burford, Omni Bridgeway, Parabellum, Therium) |

| Pre-signing | Confidentiality + common-interest agreement before sharing privileged material |

| Structuring | True-sale characterization for bankruptcy / accounting |

| Closing | Confirm no breach of existing royalty / credit facility covenants |

The Burford intro to monetization materials and the Sidley royalty financing practice description provide useful starting points for understanding the market landscape.

For royalty funds evaluating litigation-augmented opportunities

Royalty funds are increasingly encountering opportunities where the underlying claim is partly or wholly a litigation claim rather than a pure commercial royalty entitlement. The diligence and underwriting approach for these opportunities differs meaningfully from the standard royalty diligence.

| Diligence item | Key question |

|---|---|

| Procedural posture | What is the position on the claim-maturity spectrum? |

| Defendant credit | Litigation track record? Solvency? |

| Plaintiff's counsel | Track record? Economic alignment? |

| Assignability | Contractual + statutory + state-law analysis |

| Bankruptcy treatment | What happens if defendant insolvent? |

| Disclosure obligations | Required filings, audit trail |

The trend in 2025 to 2026 is for royalty funds to develop in-house litigation finance expertise rather than relying on third-party funders, recognizing that the underlying skill set (probability-weighted valuation of contractual receivables) is closely related to traditional royalty underwriting.

For litigation funders entering the pharmaceutical space

Traditional commercial litigation funders have historically focused on antitrust, patent, and contract disputes outside the pharmaceutical industry. The growing volume of pharmaceutical CVR and earnout disputes has created a meaningful opportunity for these funders to develop pharma-specific expertise.

| Challenge | Required capacity |

|---|---|

| Scientific complexity | FDA approval timing, manufacturing inspections, clinical trial design |

| CVR / earnout drafting | Efforts standards, milestone definitions, sales targets |

| Multi-year timelines | Operational discipline through litigation lifecycle |

| Collection risk | Post-judgment recovery from financially-stressed pharma |

Funders that develop pharma-specific underwriting capacity should be positioned to capture the growing volume of monetizable claims emerging from the post-2020 wave of pharmaceutical M&A.

For counsel structuring efforts covenants

The Delaware Chancery jurisprudence on commercially reasonable efforts (Alexion, Auris, Cephalon) has crystallized into a clear set of drafting choices for new CVR and earnout agreements.

| Drafting choice | Recommendation |

|---|---|

| Standard direction | Outward-facing more enforceable than inward-facing |

| Permitted considerations | Cost, safety, regulatory likelihood, competitive position |

| Excluded considerations | The existence of the CVR / milestone payment itself |

| Milestones | Binary vs. graduated structure |

| Information rights | Specific audit and reporting cadence |

| Forum and choice of law | Delaware Chancery for pharmaceutical CVR disputes |

The drafting choices made today will determine the litigation outcomes (and therefore the monetizable claim values) ten years from now.

The verdict

Non-recourse litigation sales are no longer a niche or experimental asset class in pharmaceutical royalty finance.

The institutional litigation finance industry has matured, the pharmaceutical CVR and earnout litigation docket has expanded, and the convergence of these two markets has produced a structurally important new financing tool for biotech and pharmaceutical claimants. The 2009 to 2026 cohort of pharmaceutical litigation claims shows that the most material disputes (Sanofi/Genzyme at $315 million, Alexion at $180 million+, UMB v. BMS at $6.7 billion, PDL v. Genentech at multi-billion-dollar settlement value, In re Mallinckrodt reshaping structural treatment) are now routinely monetizable through one of the three structural archetypes.

The 2025 to 2026 procedural developments are consequential, summarized below.

| Development | Implication |

|---|---|

| UMB v. BMS revived Dec 1, 2025 | $6.7B claim active; largest pharma litigation finance opportunity |

| SRS v. Alexion $180M+ damages June 2025 | CRE breach awards confirmed; outward-facing standard enforceable |

| Alexion interest ruling Oct 2025 | Pre-judgment interest at substantial rates compounds awards |

| Goodwin royalty report Oct 2025 | $29.4B in pharma royalty deals 2020-2024 |

| Funder expansion into pharma | Burford, Omni Bridgeway developing pharma capacity |

Each step rightward on the claim maturity spectrum, from pre-suit demand letter through final non-appealable judgment, narrows the funder discount, compresses the exit timeline, and broadens the universe of potential buyers from specialist litigation funders to mainstream credit and royalty investors.

For pharmaceutical claimants, the practical response is to evaluate every material litigation or pre-litigation claim as a potentially monetizable asset, to engage litigation funders early in the dispute lifecycle while preserving privilege and work product protection, and to structure financing to maintain true-sale characterization for accounting and bankruptcy purposes.

For royalty funds, the practical response is to develop in-house expertise in pharmaceutical litigation underwriting, recognizing that the skill set is closely related to traditional royalty diligence and that the litigation claim asset class is structurally consistent with royalty fund investment mandates.

For litigation funders, the practical response is to develop pharma-specific capacity to evaluate CVR, earnout, and royalty audit disputes, recognizing that the post-2020 wave of pharmaceutical M&A has created a multi-year pipeline of monetizable claims emerging from contractual disputes over efforts covenants, milestone definitions, and royalty calculations.

For counsel, the practical response is to draft efforts covenants, anti-assignment provisions, and audit rights with the eventual monetization of any resulting claim in mind, and to advise claimants and funders on the privilege, work product, champerty, and bankruptcy issues that arise in modern litigation finance transactions.

The next two to three years of pharmaceutical capital formation will reveal whether the convergence of royalty finance and litigation finance becomes a structurally enduring feature of the market or recedes back into specialized adjacent practices. The volume of pharmaceutical CVR and earnout disputes filed in 2024 to 2025 suggests it will become enduring; the Goodwin October 2025 royalty deals report noted that "tiered royalties, milestone-based arrangements, capped or hybrid instruments, territory or indication splits, multiproduct deals, and tranched funding" are increasingly common, each of which can generate downstream litigation if the contractual provisions are not met.

The structural advantages of getting the litigation finance architecture right are substantial enough that, in the modern pharmaceutical royalty finance market, the non-recourse litigation sale has moved from a curiosity to a regular item on the deal team's structuring checklist.

This article reflects publicly available information as of May 2026. It does not constitute investment, legal, or tax advice. Mechanics and structural details described are derived from court opinions, SEC filings, royalty purchase agreements, and published legal analysis. Claimants, royalty financiers, litigation funders, and counsel evaluating specific transactions should rely on the underlying documents and counsel. This content is for informational purposes only. The author is not a lawyer or financial adviser.