Capitalising the Royalty Stream: Basel, the Warehouse, and the Output Floor in 2026

Two things in pharmaceutical finance carry the name of the same Swiss city, and they are starting to collide.

The first Basel is the one this newsletter follows. It is the city on the Rhine where Roche and Novartis turn chemistry into product, where the monoclonal antibody was first made, the headquarters of the industry whose royalties are the asset.

The second Basel sits a short tram ride away, by the main station: the Bank for International Settlements, home since 1930 to the committee whose capital rules have carried the city's name since the 1980s.

The reason the second Basel reaches the first is that a royalty financing is, underneath the percentage sign, a loan. A financing royalty is debt service in royalty clothing, capped and reverting, not a licensing price. It is structured credit. And structured credit, wherever a regulated bank holds it, is priced by Basel before it is priced by the drug.

The companion piece argued that what matters most to royalty finance is not the insurance market but the capital rules governing the insurers who now fund royalty paper. The same holds for the banks, with one word changed. For a bank lending against royalties, what matters is not the asset, the patent, or the licensee. It is the capital charge on the loan, because the bank passes that charge straight back to the royalty fund.

This piece is for counsel and royalty principals reading a warehouse facility, a forward-flow purchase, or a draft securitisation, who need to know which box the bank's risk team will use, what that box costs, and how the cost lands in their advance rate. The answer turns on one classification and one floor.

Royalty financing is funded by balance sheets Basel governs

The market this reaches is large and crowded. The pharmaceutical royalty market entered 2026 at record volume, with new capital arriving, a wave of assets out of China, and a consolidating set of aggregators. All of that capital has to sit somewhere, and where it sits decides whom Basel touches.

A royalty financier funds itself in one of a few ways, and a bank stands behind most of them:

- A revolving warehouse credit facility, where a bank advances against a pool of acquired royalties and the originator holds the residual. The bank is the senior lender.

- A securitisation, where the pool's cash flow is tranched into rated notes sold to investors, with a bank often arranging, warehousing, or retaining a piece.

- A direct balance-sheet purchase by an insurer or private-credit platform, increasingly the dominant channel as the sector consolidates.

The first two run through a bank balance sheet. The third runs through an insurer's, governed by its own capital regime, which was the subject of the companion piece. In every case the royalty financing is priced by a capital rule before it is priced by the asset. This piece follows the bank channel, because that is where Basel sits.

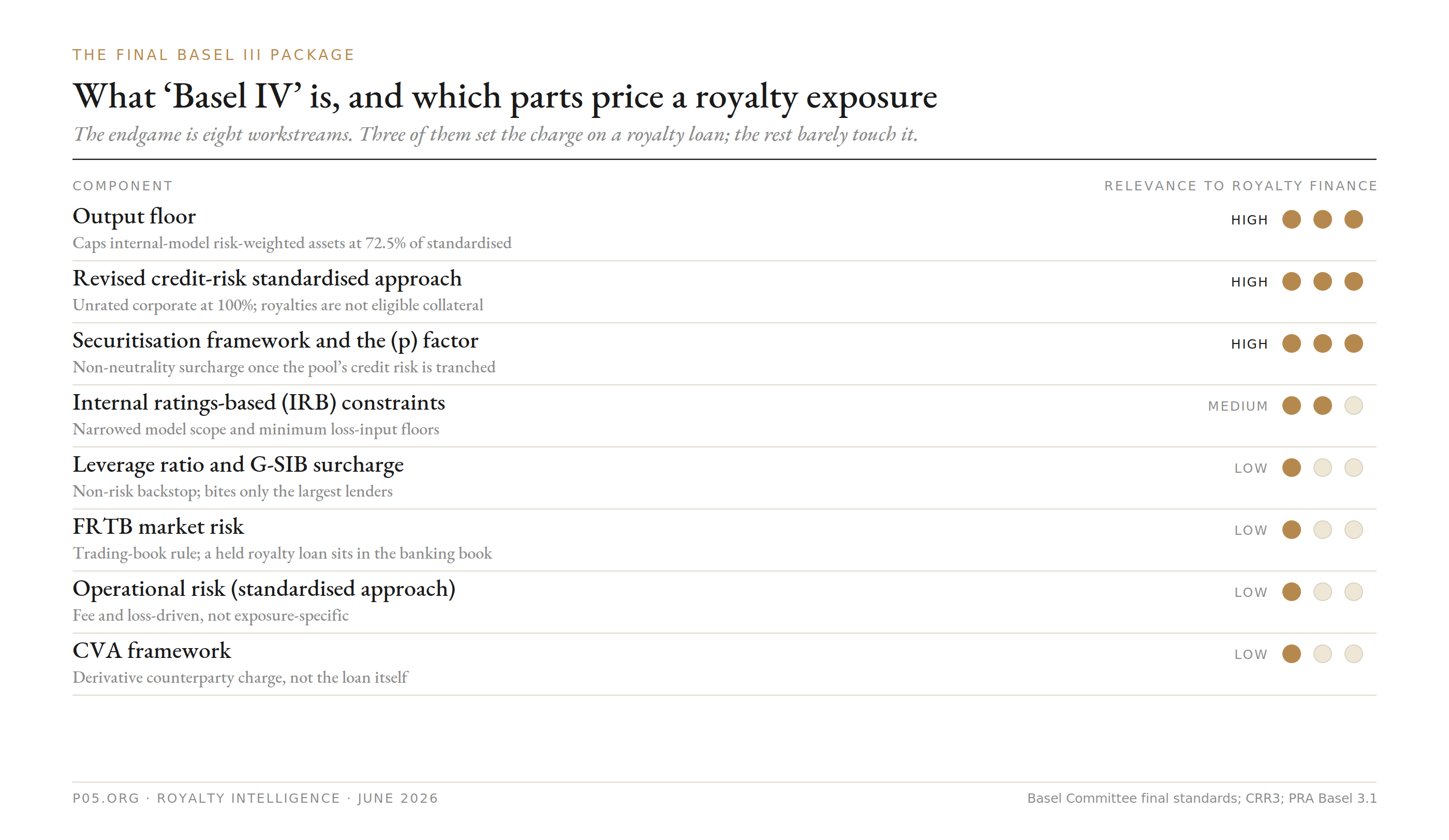

Which Basel levers touch a royalty financing

The rule in question is the 2017 finalisation of Basel III: the package the US calls the endgame, the EU implements as the Capital Requirements Regulation III and Directive VI (CRR3 and CRD6), and the UK implements as Basel 3.1. Market shorthand is "Basel IV." It is eight workstreams, and most of them never reach a royalty loan.

Three levers do the work. The output floor caps the relief a bank can earn from its own models of royalty risk. The revised credit-risk standardised approach governs how the loan is risk-weighted when the bank cannot model it. The securitisation framework governs what happens the moment the deal is tranched.

The rest (the Fundamental Review of the Trading Book, or FRTB; operational risk; the credit valuation adjustment, or CVA; and the leverage ratio and global systemically important bank, or G-SIB, add-ons) are trading-book, fee-based, or derivative rules that a royalty term loan rarely touches. The whole of what follows is about the three.

How the charge reaches the royalty fund

A royalty fund never sees Basel. It sees Basel in the advance rate it is quoted and the margin it pays. The transmission is mechanical, and it is the heart of why a banking rule belongs in this newsletter.

A bank holds equity against its assets in proportion to their risk weight. Take a royalty warehouse line of 100. If Basel assigns the exposure a 100% risk weight, the bank carries 100 of risk-weighted assets (RWA) against it, and must fund roughly a tenth of that, say 10 to 13, as equity-like capital. That capital is the bank's own money, and it has to earn the bank's hurdle return, typically in the low-to-mid teens.

So the capital alone costs the bank something like 130 to 170 basis points a year on a 100 loan, before any funding cost or overhead. The bank recovers it through three levers, and a royalty originator meets all three at the term sheet:

- the spread on the drawn facility,

- the advance rate, meaning how much the bank will lend against a given pool,

- and the coverage and covenant package.

Where the charge is high enough, there is a fourth outcome: no facility at all. (Figures illustrative.)

This is the entire link between a banking rule and a royalty deal. Halve the risk weight through a better model and the capital cost roughly halves, which the fund feels as a tighter spread or a higher advance rate. Double it by tranching the deal into the securitisation framework, and the fund feels that too. Everything below is which of those two worlds a given royalty financing lands in.

Where the rules are live

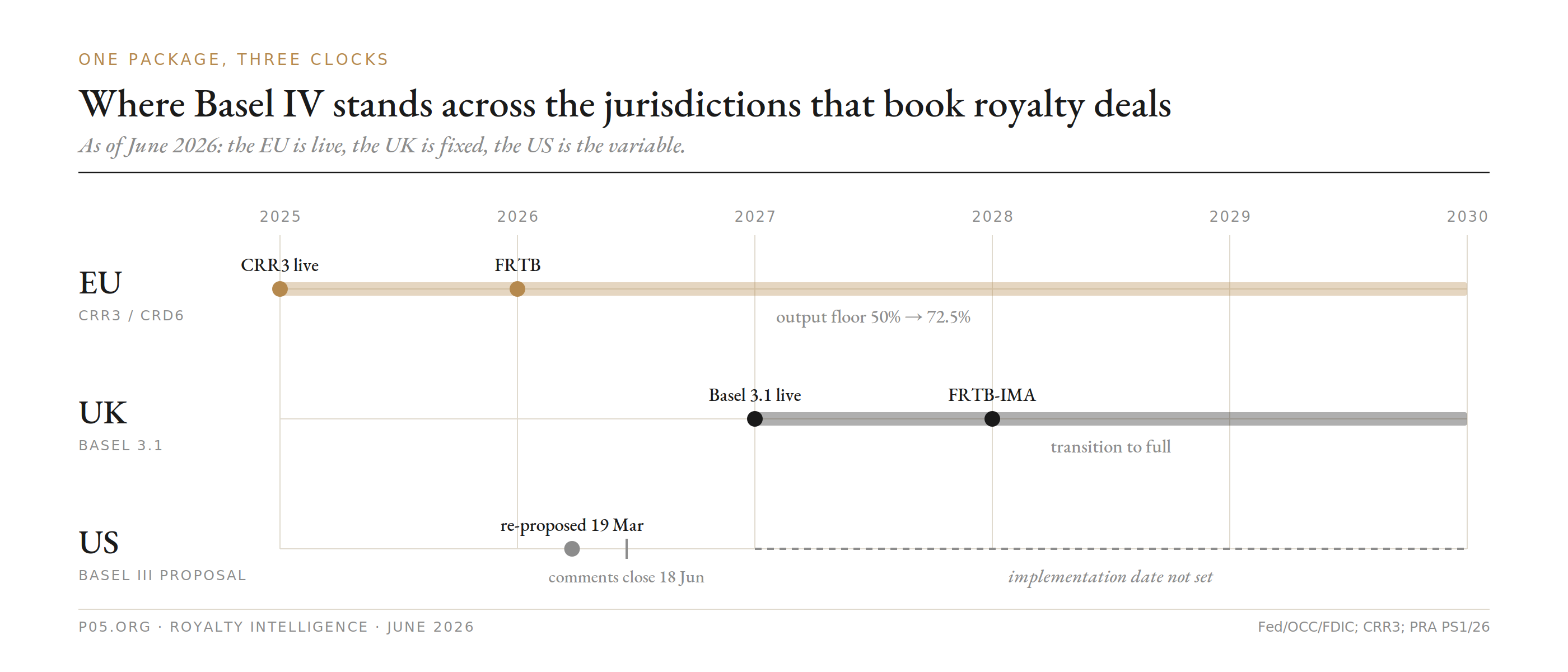

For a fund choosing where to book a facility, timing matters, because the three jurisdictions sit at three different points as of June 2026.

The EU is live: CRR3 has applied since 1 January 2025, so a European bank lending against a royalty pool already runs the new charge, with the output floor phasing toward 72.5% by 2030. The UK is fixed but not yet effective: the Prudential Regulation Authority (PRA) confirmed a 1 January 2027 start. The US is the variable: the agencies (the Federal Reserve, the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation) re-proposed the package on 19 March 2026, with comments closing on 18 June, in a version that pulls capital down rather than up and replaces the advanced internal model approach (IMA) with a standardised expanded risk-based approach.

For a royalty financing the direction is the same everywhere: less internal modelling, more prescribed risk weights. Wherever the loan is booked, the bank's freedom to model its way to a kind price on an esoteric royalty is narrowing.

The classification that sets the charge

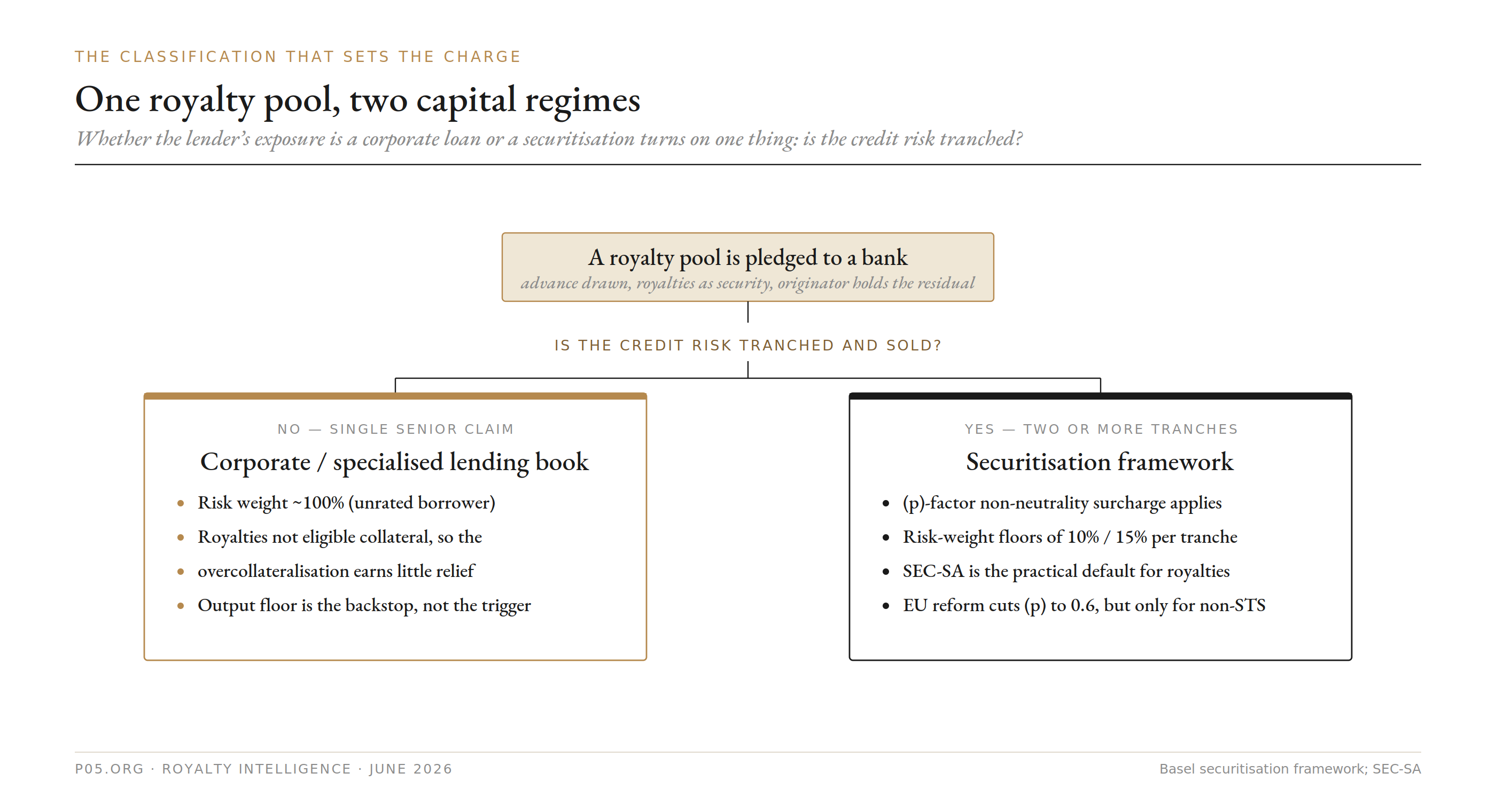

A royalty financing reaches a bank in one of two postures, and the gap between them is large.

A securitisation, under Basel, requires two things together: the credit risk of a pool is tranched into at least two positions of different seniority, and payment depends on the pool's performance. Tranching is the trigger.

A single senior facility, where the lender holds one undivided claim and only the originator's equity sits beneath it, is not a securitisation. One position above one equity layer is not two stratified credit-risk positions, and the value break sits below the bank rather than inside its claim. The exposure stays in the corporate book.

Add a placed mezzanine, or split the bank's commitment into senior and junior loss-attaching pieces, and the same royalty deal becomes a securitisation. The risk is now tranched and sold, and the exposure moves into the securitisation framework, where the arithmetic is worse.

The lesson is structural, and it is a structuring instruction for the fund. The cheapest bank treatment for a royalty pool is usually the least structured one. The instinct to tranche for distribution is the instinct that converts a corporate-book problem into a securitisation problem.

Why the pledge helps less than the documents suggest

Inside the corporate posture, the overcollateralisation does more economically than it does for the bank's ratio.

Basel recognises collateral relief only from a closed list: cash, gold, eligible debt securities and equities, eligible fund units, and eligible real estate. A portfolio of royalty contracts is none of these. It is contractual receivables and the intangible rights behind them, and it does not appear on the list. Anti-pledge language in the underlying licences can weaken the security further, but even a clean, perfected pledge buys little capital relief, because the collateral itself is ineligible.

So a 2:1 overcollateralised royalty warehouse, which any credit committee treats as conservatively secured, is risk-weighted much like an unsecured corporate exposure to the borrower: 100% under the standardised approach for an unrated corporate, with a transitional EU softening while the output floor phases in.

Part of the warehouse spread, in other words, is compensation for a capital charge the collateral is not allowed to relieve. The fund pays for security the regulation refuses to count.

The securitisation penalty

When a royalty deal does cross into the securitisation framework, whether as a rated asset-backed security (ABS) sold to investors or as a tranched warehouse, it meets a hierarchy of approaches and a deliberate surcharge that the royalty fund pays for in its cost of capital.

| Approach | Driver | Available for a royalty ABS? |

|---|---|---|

| SEC-IRBA | Bank's modelled capital of the pool | Rare; needs model approval and pool data |

| SEC-ERBA | External tranche rating | EU and UK only, not the US |

| SEC-SA | Standardised pool capital plus the (p) factor | Yes, the practical default |

The prefixes decode simply: SEC marks them as the securitisation versions, then internal ratings-based (IRBA), external ratings-based (ERBA), or standardised (SA).

The cost lives in the (p) factor, the parameter that produces what the framework openly calls non-neutrality: the capital against all the tranches exceeds the capital against the same pool held whole. Under SEC-SA the (p) value is 1.0, a 100% surcharge over the underlying. On top sit risk-weight floors of 10% senior and 15% non-senior, with the US applying 15% across the board.

This bites harder on royalties than on a granular consumer pool. The data scarcity that pushes a royalty deal to SEC-SA is the same scarcity that keeps its pool-capital input high. Conservative input, multiplied by the surcharge, caught by the floor. It is why the one royalty securitisation programme to issue through the post-2008 era clears its ratings with heavy overcollateralisation rather than a thin tranche stack.

It connects to the companion piece. The classic 2003 move, wrap a pool to print a AAA (top-grade) senior note and sell the tranches, now fails twice: the monoline that made the rating is extinct, and even a bought rating leaves the holder paying the non-neutrality penalty that the plain corporate loan against the same royalty pool avoids.

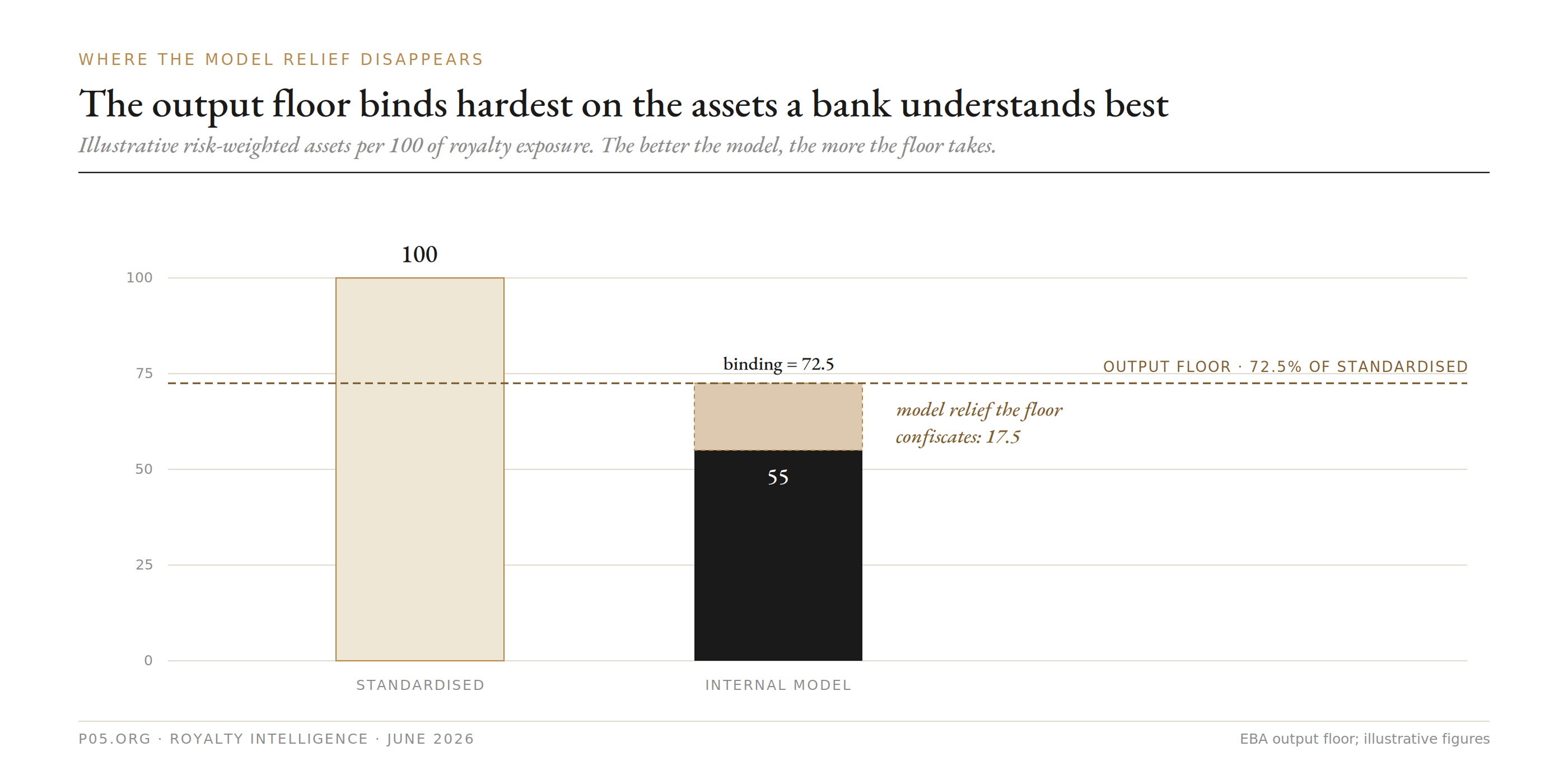

The output floor, where the model relief disappears

The output floor is the provision that decides whether a large bank can make royalty lending pay.

It sets a minimum: internal-model risk-weighted assets cannot fall below 72.5% of the standardised figure, phased in to 2030. The European Banking Authority (EBA) calls it the single largest driver of the EU capital increase, about a third of the total.

For a generic corporate loan the floor is often slack. For a royalty exposure it binds, and the reason is specific. A good model of a seasoned, diversified royalty pool produces a genuinely low loss estimate, because realised royalty credit experience is benign. The standardised approach treats the same exposure as an unrated 100% corporate. The gap is wide, and the floor exists to close it.

The result: the relief a bank earns for understanding royalty risk evaporates at 72.5% of the standardised charge. The better the model, the more the floor confiscates.

This is the quiet reason royalty warehouse lending is leaving large internal-model banks (those on the internal ratings-based, or IRB, approaches). The institution best equipped to underwrite the asset is the one the floor most penalises for doing so, and the royalty fund borrowing from it inherits the penalty in its spread.

The EU securitisation review: help for the senior, not the mezzanine

The EU has noticed its securitisation capital is too high and is fixing it. The fix helps some royalty structures and pointedly not others.

On 17 June 2025 the Commission published a review amending the Securitisation Regulation and the CRR. It replaces the flat senior risk-weight floors with a risk-sensitive floor and cuts the (p) factor, from 1.0 to 0.6 for positions that are not simple, transparent and standardised, or non-STS, with deeper cuts reserved for senior and STS positions.

The process has moved. The Council fixed its position at the end of 2025, and the European Parliament adopted its negotiating position in early May 2026. Trilogue between the three institutions is expected in the second half of 2026, and the reforms are not expected to take effect before around mid-2027. The relief is real, but it is not yet law, and it will not arrive in time to reprice a 2026 deal.

The catch is the STS line. The label that attracts the deepest relief is built for homogeneous, granular, self-amortising pools. A royalty securitisation, with a few heterogeneous streams across pharma, vaccines, medtech and animal health, actively managed or revolving, is non-STS by construction. It sits in the collateralised loan obligation (CLO) bucket, and for that bucket the negotiated texts read as neutral to negative.

So the review improves the senior arithmetic and does little for the mezzanine. It narrows the penalty for the structure the asset class actually produces; it does not erase it.

Significant risk transfer keeps the bank in the deal

The capital rules push royalty risk off bank balance sheets. Significant risk transfer (SRT) lets a bank originate the royalty exposure and move the risk without moving the relationship with the royalty fund.

An SRT transfers the credit risk of a loan pool to an outside investor through a guarantee, credit default swap, or credit-linked note, while the loans stay on the books. The bank releases the risk-weighted assets and keeps the client and the servicing.

The market is now structural. The Basel Committee's February 2026 report put protected assets at roughly EUR 750 billion, about 1.1% of total bank assets, and the BIS found issuance up fivefold since 2016. The risk-takers are the non-banks: hedge funds, asset managers, and increasingly insurers, the same balance sheets that fund royalty deals directly.

This is the exact complement to the output-floor problem. A bank that wants royalty exposure but cannot hold it efficiently originates the loan and lays the risk off through an SRT. The floor itself drives more SRT issuance, because the floor raises the charge the SRT is built to relieve.

For an originator, the practical point is that the warehouse bank and the ultimate risk-holder are increasingly different parties. Knowing who bears the loss on a royalty facility now means reading the risk-transfer documentation behind the credit agreement, not just the agreement.

The wrap, from the capital side

The companion piece showed the monoline wrap is dead as a rating tool. From the bank-capital side it gives nothing either, and counsel still meet guarantees and credit-insurance policies offered as relief on royalty facilities.

A guarantee or credit-insurance policy is unfunded credit protection. If the provider is an eligible guarantor with a lower risk weight, the bank may substitute it for the borrower; otherwise the policy is regulatory-inert. In the EU and UK credit insurance can qualify; in the US most credit insurers do not. A specialty insurer wrapping a single esoteric royalty stream usually fails the test, especially in the US, so the protection has to come from the structure, not a third party, on the capital side exactly as on the ratings side.

The net effect: the same destination, a different road

The companion piece traced how National Association of Insurance Commissioners (NAIC) reform steers insurers away from bespoke royalty tranches. Basel steers banks to the mirror conclusion from the other bank of the same river.

| Posture | Book | Practical charge | What triggers it |

|---|---|---|---|

| Single senior warehouse line | Corporate / specialised lending | ~100% risk weight, collateral unrecognised, floored at 72.5% of standardised | Default |

| Tranched and distributed | Securitisation | (p)-factor surcharge plus risk-weight floors | Selling or carving credit risk |

Basel makes the esoteric royalty exposure expensive to hold on a regulated bank balance sheet. The collateral does not relieve the standardised charge. Tranching triggers the non-neutrality penalty. The output floor confiscates the model relief. The EU review softens the senior arithmetic but leaves the royalty-shaped deal in the neutral-to-negative bucket. The credit-insurance wrap is, for most carriers, ineligible.

One caveat runs the other way. The US re-proposal is calibrated in part to improve the economics of traditional bank lending and could pull some activity back toward banks. But that pull is general, aimed at mainstream corporate and mortgage credit. It does little for the esoteric royalty exposure, where the output floor and the collateral-eligibility problem bite regardless of the headline calibration.

The capital does not disappear. It relocates, to the private-credit and insurance-backed lenders outside the Basel perimeter, reaching them directly or through the SRT a bank uses to pass the risk along. The banking system stays in the asset as originator and senior-retention holder, not as the ultimate risk-bearer.

For a fund raising a warehouse line in 2026, the operative conclusions are concrete:

- Keep the senior facility a single undivided claim, and resist tranching it, because tranching moves the lender's capital into the punitive securitisation book.

- Do not lean on overcollateralisation as a capital argument to the bank; the pledge the credit committee values is not collateral the regulation recognises.

- Expect the cheapest senior capital to come from lenders outside the Basel perimeter, and expect the bank that does lend to be laying the risk off behind the scenes.

- Treat any offered wrap as economic comfort, not capital relief, unless the carrier is a demonstrable eligible guarantor.

The asset is sound, and the cash flows are real and increasingly monetised across four verticals. What the capital rules govern is not whether the royalty is good, but who is allowed to finance it cheaply. As the sector consolidates into investment-grade and insurance-backed platforms, that answer is, less and less, a bank.

The molecules still come from Basel. Increasingly, the financing does not come from the banks the other Basel regulates.

All information in this report was accurate as of the research date and is derived from publicly available sources including court opinions, regulatory guidance, academic literature, SEC filings, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.