Sidecars in royalty financing: capacity, allocation, and co-investment economics

A companion note to our piece on sleeves takes the opposite cut. The sleeves note was about the boundary: how capital is segregated, and what a creditor can reach. This note is about the vehicle that sits beside the fund, why it exists, and the governance and economics that surround it.

In the sleeves note the co-investment sidecar appeared briefly, as one of the capital sleeves. Here it is the subject.

This note does not re-cover segregation, true sale, or insurer capital treatment. Those are in the sleeves note. It is current to June 2026, with the status flagged where a rule is in motion. The legal framing is United States adviser law, where most of the conflict and allocation doctrine sits; the deal context is pharmaceutical and life sciences royalties.

Summary

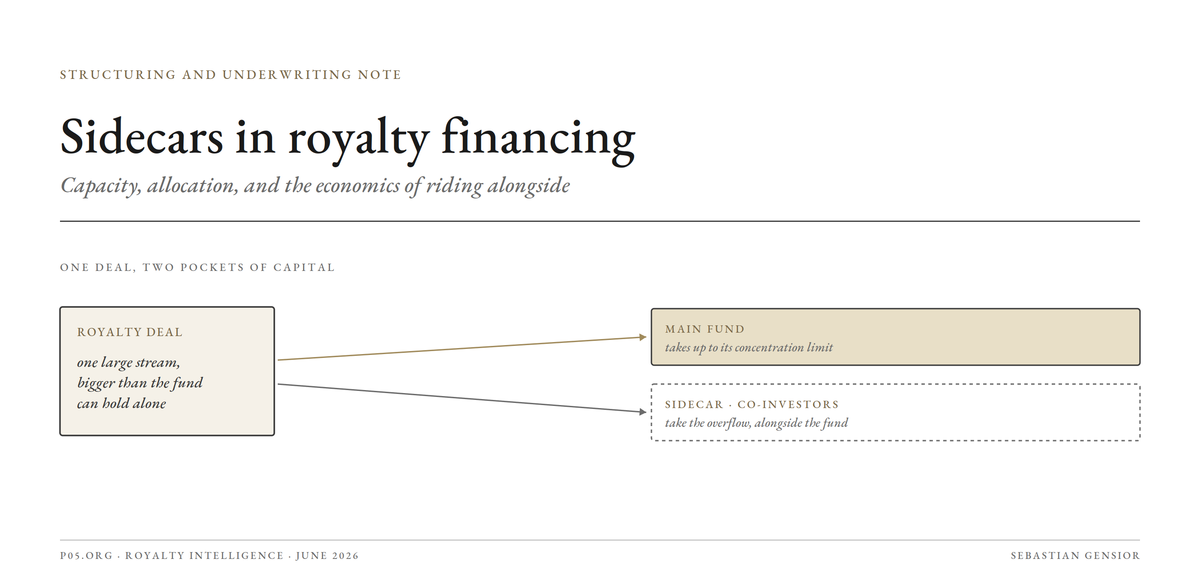

A sidecar is a vehicle beside the fund. It exists to put additional capital into a deal the main fund either cannot hold alone or chooses not to, usually because a single royalty is large relative to the fund and its concentration limits.

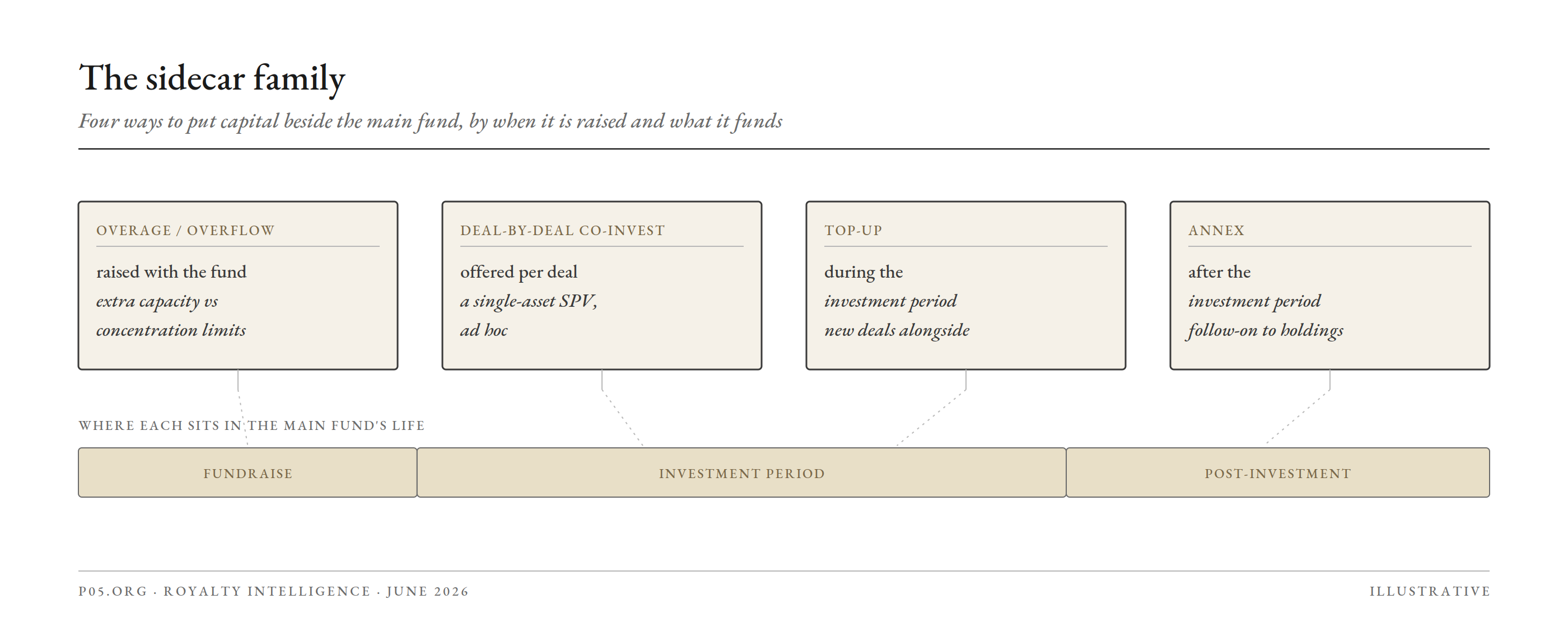

It is not one thing. The family runs from the deal-by-deal co-investment vehicle to blind-pool sidecars: overage or overflow funds, top-up funds, and annex funds. Which one fits depends on when it is raised and what it funds.

The hard part is allocation, not formation. How a deal is divided between the fund and the sidecar, and how costs are shared, is where the conflicts live. After the 2023 SEC private fund rules were vacated in June 2024, that governance runs on Advisers Act fiduciary duty, disclosure, and a long line of enforcement, not a bright-line rulebook.

The economics are about fees, not gross returns. Co-investment usually carries reduced or no fee and carry, which lifts net returns. The large-sample evidence finds no systematic adverse selection, but single-deal returns are skewed, so the saving shows up reliably only across a portfolio.

In royalties the use case is acute. Royalty tickets are lumpy and often large, and sellers want certainty and speed, so an arranger that can commit the whole ticket and place the overflow through a sidecar wins mandates a single fund could not.

1. What a sidecar is

A sidecar is a co-investment vehicle organised by the sponsor of a main fund to participate in one or more co-investment opportunities alongside that fund. It is typically a special purpose vehicle managed by the same general partner, and the fund's own interest in the asset is what drives it, which distinguishes a sidecar from an ordinary syndication between a sponsor and outside investors.

The idea is old. The economist Richard Zeckhauser is usually credited with popularising the sidecar as a way for investors to benefit from another party's skill at sourcing opportunities, the way early Berkshire Hathaway shareholders rode alongside its investments.

The sidecar sits between two more familiar structures and is often confused with them.

| Vehicle | What it is | Relationship to the main fund | Typical use |

|---|---|---|---|

| Sidecar / co-investment vehicle | An SPV the GP forms to invest in specific deals | Invests because the fund is investing; fund's interest drives it | Take capacity beyond the fund in chosen deals |

| Standalone SPV | A single-purpose entity any group can use | None required | A syndicate with no pre-existing fund |

| Parallel fund | A second fund running in tandem | Invests pro rata on the same terms | Segment investors for tax or regulatory reasons |

| SMA / fund-of-one | A managed account for one investor | Separate mandate, may overlap the fund | A single large LP wanting bespoke terms |

| Continuation fund | A GP-led secondary vehicle | Buys assets out of the fund | Provide liquidity and extend hold on existing assets |

The practical markers of a sidecar are that it is sponsor-organised, deal-linked to the flagship fund, usually offered to a subset of the fund's existing limited partners or to chosen third parties, and structured on lighter economics than the fund.

2. Why royalty deals need sidecars

The structural reason sidecars exist is that a limited partnership agreement almost always prohibits concentrated single-asset exposure through concentration limits. When a single opportunity is large relative to the fund, the fund cannot take all of it, and the excess has to go somewhere or the deal is lost.

Royalty financing makes this binding rather than occasional, for four reasons.

- Tickets are lumpy and large. A single royalty monetisation can run from tens of millions to well over a billion. Royalty Pharma alone announced funding agreements of up to 500 million dollars each with Johnson and Johnson and with Teva in recent quarters. A ticket of that size will breach the concentration limit of most funds below the very largest.

- Origination outruns the balance sheet. An arranger that sources more deal flow than its fund or balance sheet can hold needs a place to put the surplus. The sidecar is that place.

- Sellers want certainty and speed. Biotechs, universities, and foundations selling a royalty value a committed, single-counterparty close. An arranger that can commit the whole ticket and place the overflow through a sidecar offers certainty a syndicate assembled deal-by-deal cannot.

- The market already runs this way. Large royalty deals are increasingly executed as a syndicated process rather than a single bilateral trade, with a lead and co-investors, which is the sidecar pattern by another name.

The result is that in royalty financing the sidecar is not an occasional convenience. It is part of the standard operating model for any deal larger than the lead vehicle can hold.

3. The sidecar family

"Sidecar" covers a family of vehicles that differ by when they are raised and what they fund. Industry usage is not fully consistent, but the working distinctions are clear enough.

Four ways to put capital beside the main fund, placed by when each is typically raised in the fund's life.

| Type | When raised | What it funds | Form |

|---|---|---|---|

| Deal-by-deal co-investment | Ad hoc, per opportunity | A single named asset alongside the fund | Single-asset SPV, disclosed |

| Overage / overflow fund | With the fund, or early | Capacity beyond the fund's concentration limits | Blind pool |

| Top-up fund | During the investment period | New opportunities alongside the fund | Blind pool |

| Annex fund | After the investment period | Follow-on into existing holdings | Blind pool |

The deal-by-deal vehicle is the classic sidecar: the GP identifies a deal too large for the fund, then forms an SPV to gather the rest of the capital for that single asset, offered to chosen LPs. It can be blind or disclosed, commingled or a fund-of-one, and is usually a closed-end vehicle with back-ended carry, paid only after all invested capital is returned.

The blind-pool variants differ mainly in timing. An overage fund is raised pre-emptively to invest the part of a deal that is "over" the fund's limit. A top-up fund is raised during the investment period to chase new opportunities. An annex fund is raised after the investment period to provide follow-on capital to existing positions, and is normally offered to existing LPs first, pro rata, before third parties.

A fifth case worth naming is the seed or warehouse sidecar, used to hold a first deal before a fund has closed, which lets an arranger commit to a seller on day one and term the position out once the fund is raised.

4. How a deal is split

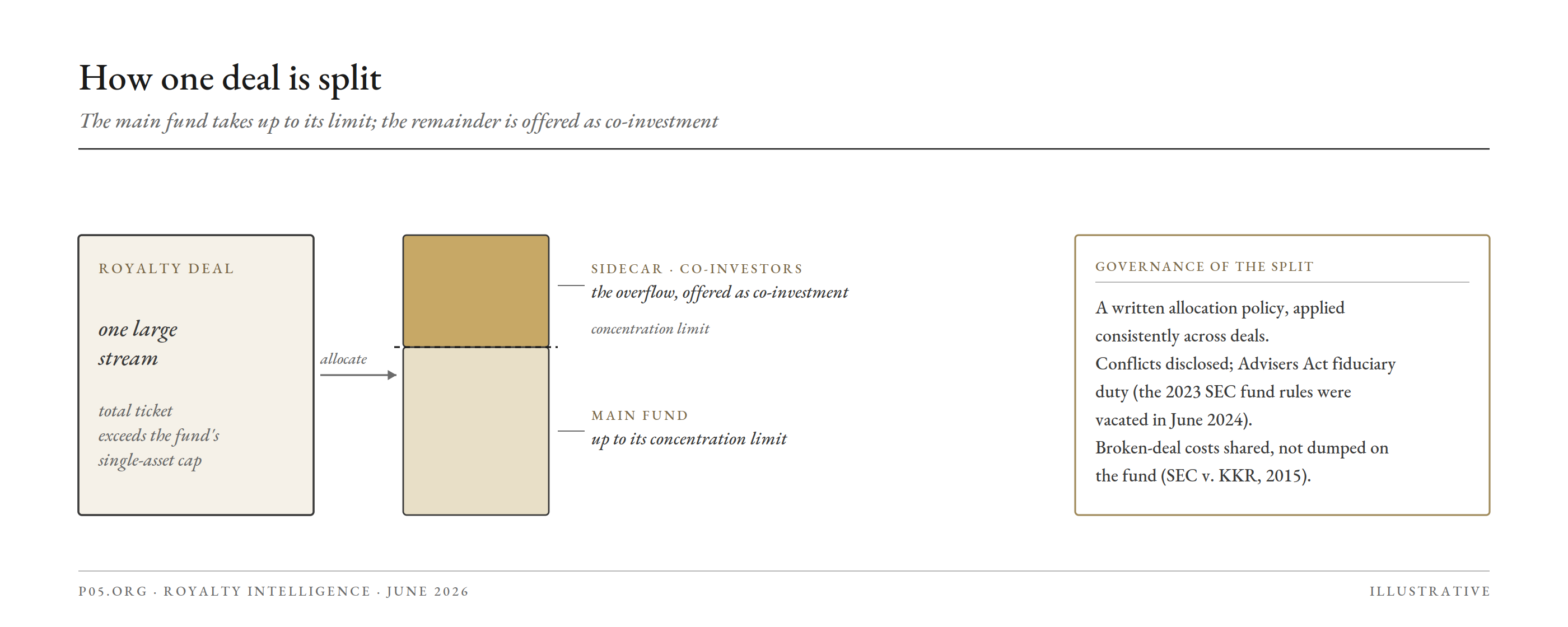

Forming a sidecar is straightforward. The governance problem is allocation: how a deal is divided between the fund and the sidecar, who is offered the co-investment, and how shared costs are borne. This is where the conflicts sit, because every dollar routed to a sidecar is a dollar of fee-bearing exposure removed from, or added beside, the flagship fund.

The fund takes up to its concentration limit; the remainder is offered as co-investment, under an allocation policy and disclosure.

The common allocation convention is that the main fund has the first opportunity and is filled to its limit, with the remainder apportioned to the sidecar, often pro rata to commitments or by a stated policy. Real estate and other co-investment programmes commonly allocate the sidecar portion first-come-first-served or pro rata so the offer is demonstrably fair.

The legal frame for that governance shifted in 2024. The SEC's 2023 Private Fund Adviser Rules, which would have imposed bright-line requirements on preferential treatment, expense allocation, and disclosure, were vacated in full by the Fifth Circuit on 5 June 2024, on the ground that the SEC had exceeded its statutory authority.

What did not change is the adviser's fiduciary duty under the Advisers Act: the duty to act in the funds' best interest, not to favour its own interest, and to disclose conflicts, particularly around fees and expenses. Co-investment allocation remains an examination and enforcement focus, now governed by that duty and by anti-fraud principles rather than a rulebook.

The canonical cost-allocation case predates the vacated rules and still frames the issue. In 2015 the SEC charged KKR with misallocating broken-deal expenses: over a six-year period it incurred about 338 million dollars of broken-deal and diligence costs and charged effectively all of it to its flagship funds, while allocating none to the co-investors who benefited from the same sourcing, and without disclosing that practice. KKR settled for nearly 30 million dollars, and the SEC also faulted the absence of a written allocation policy until late in the period.

The governance items a counterparty or LP confirms reduce to a short list.

| Item | The question | The standard |

|---|---|---|

| Allocation policy | Is there a written policy, applied consistently | Required in substance to evidence the fiduciary duty |

| Offer order | Fund first to its limit, then sidecar by a stated rule | Disclosed, consistent, not deal-by-deal favouritism |

| Broken-deal expenses | Are dead-deal costs shared with co-investors | Shared, not dumped on the fund (the KKR line) |

| Expense allocation | Are shared costs split on a disclosed basis | Disclosed in the LPA and offering materials |

| Information and MNPI | Do co-investors get selective material information | Controlled and disclosed; even-handed within the offer |

| Preferential terms | Do some co-investors get better terms | Permissible if disclosed; track side letters |

5. The economics of riding alongside

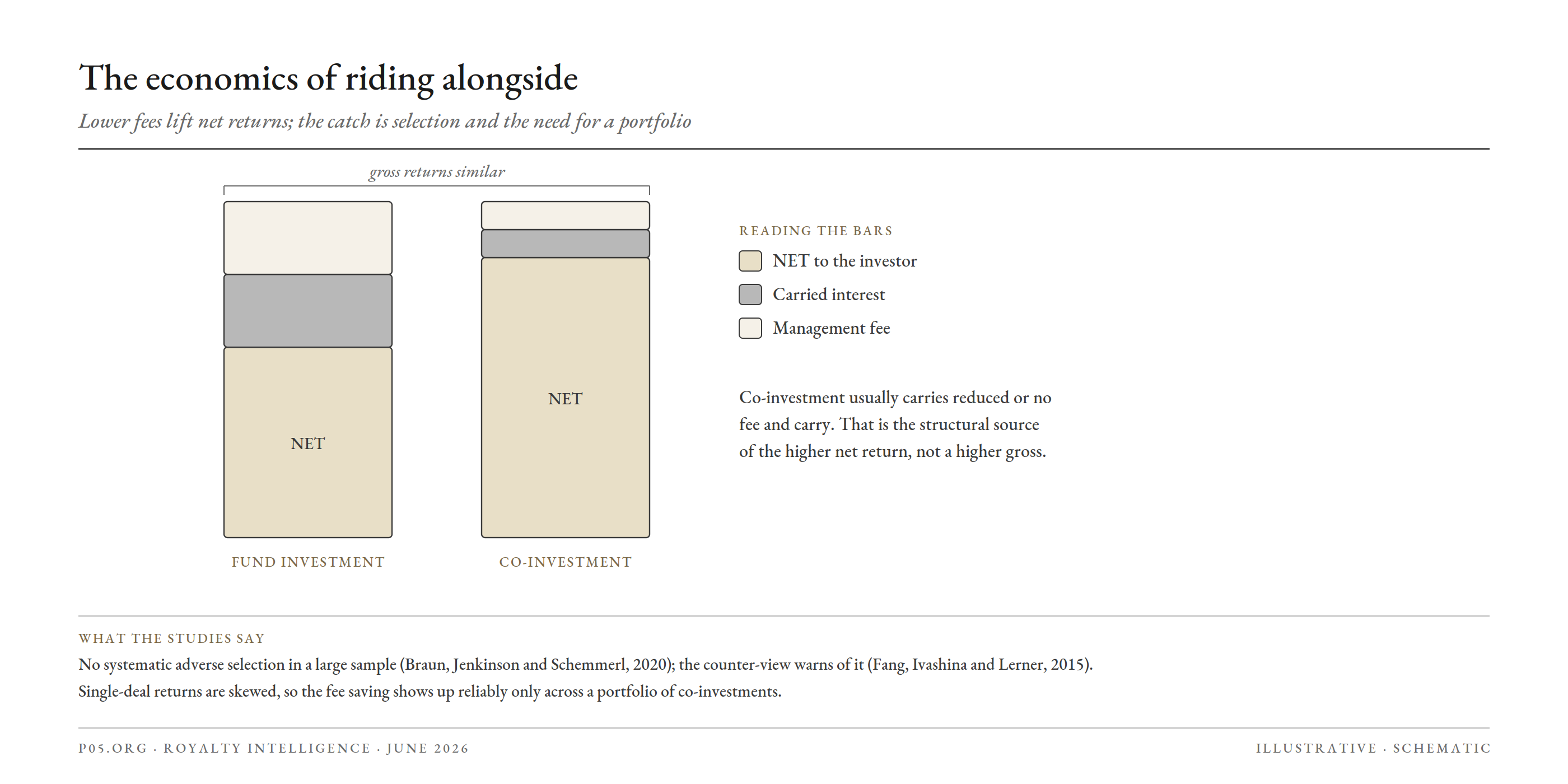

For the investor, the case for co-investment is almost entirely about cost, not about getting better assets.

Co-investment usually carries reduced or no fee and carry. The net pickup comes from the fee line, not from a higher gross return.

Co-investment opportunities typically carry lower management fees and carried interest, and often none, which is the structural source of the net pickup. The deal-by-deal sidecar is usually a closed-end vehicle with back-ended carry, so the GP earns only after all invested capital is returned.

The natural objection is adverse selection: that a GP keeps its best deals for the fund, where it earns full carry, and offers the marginal ones for co-investment. The evidence is mixed but, in the largest study, reassuring.

- The cautionary view comes from Fang, Ivashina and Lerner (2015), who found selection and timing problems in direct and co-investments.

- The larger, later sample in Braun, Jenkinson and Schemmerl (2020) found no evidence of adverse selection: gross return distributions of co-investments and other deals were similar, co-investments carried lower costs, and net of fees they outperformed fund deals. The authors attribute this to GPs weighting long-term reputation over short-term opportunism.

Two qualifications matter for how an analyst should use that finding.

First, the benefit is a portfolio property. Single-deal returns are highly skewed, so an investor benefits in expectation only by building a portfolio of co-investments, not from one or two concentrated bets. A royalty co-investor that takes a single large position is exposed to the dispersion of that one asset, not to the average.

Second, healthcare is over-represented in co-investment deal flow in the data, which means the royalty and life sciences investor sees more of these opportunities than a generalist, and needs a deliberate selection and portfolio-construction discipline rather than a reactive one.

| Dimension | Main fund | Co-investment sidecar |

|---|---|---|

| Management fee | Full | Reduced or none |

| Carried interest | Full | Reduced or none, usually back-ended |

| Diversification | Portfolio by construction | One asset per deal; build the portfolio yourself |

| Gross return | Baseline | Similar, on the large-sample evidence |

| Net return | Baseline | Higher, from the fee saving, across a portfolio |

| Underwriting time | Full process | Compressed; often take-it-or-leave-it on the lead's terms |

The last row is the underrated risk. Co-investment runs on the lead's timetable, so the co-investor underwrites faster and with less independent diligence than it would as a sole buyer. In royalties, where value turns on patent and exclusivity tails, that compression is where mistakes are made.

6. Structuring and tax

A few structuring points sit on top, kept brief because the vehicle's segregation and security mechanics are covered in the sleeves note.

The sidecar is usually a closed-end SPV, a fund-of-one for a single anchor or commingled for several co-investors. Its jurisdiction follows the investor base and the lead's platform, commonly Luxembourg, Cayman, or Delaware.

Tax drives much of the structuring, because co-investors frequently have special tax needs: US tax-exempt investors managing unrelated business taxable income, foreign investors managing effectively connected income and withholding, and pension or sovereign investors with treaty considerations. The usual answer is a blocker corporation in the sidecar stack for those investors, which is a structuring decision taken at formation, not a documentation afterthought.

Where the sidecar holds a royalty directly, the segregation, true sale, and perfection analysis is the same as for any royalty-holding vehicle, and is treated in the sleeves note rather than repeated here.

7. A worked example

The following is hypothetical and simplified.

An arranger is mandated by a biotech to monetise a single marketed royalty for 300 million dollars, with a seller that wants one counterparty and a fast close. The arranger's fund has a single-asset concentration limit that caps its participation at 120 million dollars.

- The fund takes its 120 million, to the limit.

- The arranger commits to the seller for the full 300 million on the strength of a pre-arranged sidecar, and closes bilaterally, giving the seller certainty.

- The remaining 180 million is placed into a deal-by-deal co-investment sidecar, a fund-of-one for an anchor pension that wants concentrated exposure to this asset, on reduced fee and back-ended carry.

- Allocation follows the written policy: fund first to its limit, remainder to the sidecar. The broken-deal expenses of the arranger's wider pipeline are shared between the fund and co-investors, not charged solely to the fund.

- A blocker corporation sits in the sidecar stack for the pension's tax position.

The points that decide whether this holds up are governance, not formation. The allocation has to follow a consistent, disclosed policy; the conflicts of giving one anchor a concentrated, fee-light position have to be disclosed and even-handed within the offered group; and the cost sharing has to survive the standard the KKR settlement set. On the economics, the anchor's single 180 million position carries the dispersion of one royalty, so its fee saving is real but its risk is undiversified, which is the central tension of co-investment in this asset class.

8. Examples in the market

Public filings rarely use the word "sidecar," because the commingled blind-pool versions are private and surface only indirectly. What is visible in SEC filings is the same economic pattern: capital riding alongside a lead in a single royalty, or several investors taking one stream together. A few documented cases show the range.

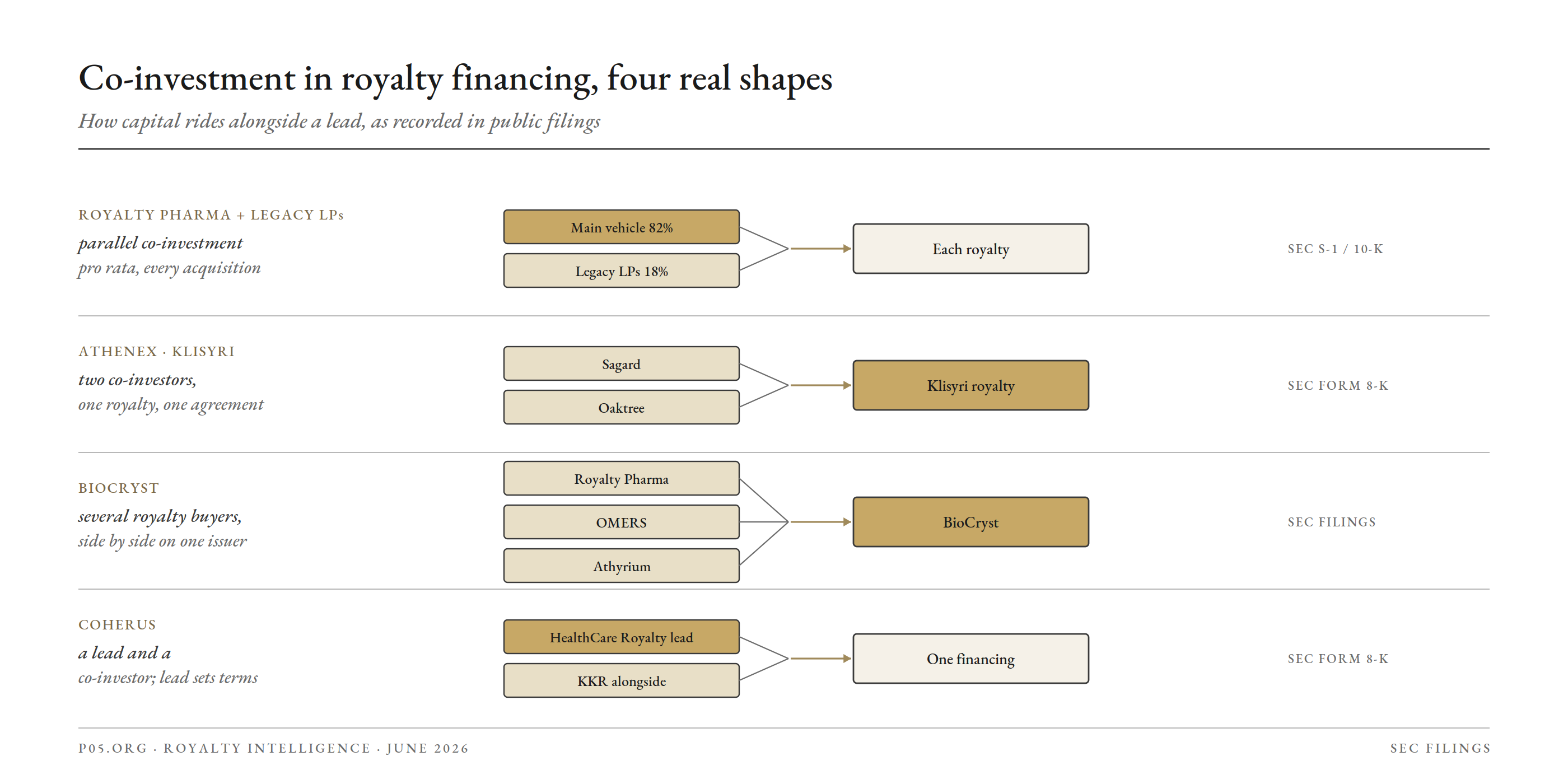

Royalty Pharma and its legacy partnerships, parallel co-investment. Royalty Pharma's pre-IPO structure is itself a standing co-investment arrangement.

Its filings explain that, until their investment period expired on 30 June 2020, the Legacy Investors Partnerships (RPI US Partners, LP; RPI US Partners II, LP; RPI International Partners, LP; and RPI International Partners II, LP) participated proportionately with Royalty Pharma Investments in each acquisition, with the public company holding an 82 percent economic interest and the legacy partnerships the balance.

After that date the legacy partnerships stopped making new investments and became legacy entities. This is the parallel-fund end of the family: a continuing pool investing pro rata beside the main vehicle, not a deal-by-deal SPV.

Athenex and Klisyri, two co-investors in one royalty. In June 2022 Athenex sold the United States and European royalty and milestone interests in Klisyri (tirbanibulin) for 85 million dollars under a single Revenue Interest Purchase Agreement dated 21 June 2022, with two investors taking the stream together: Sagard Healthcare Royalty Partners and funds managed by Oaktree. This is the clean deal-by-deal case: one royalty, one agreement, two co-investors riding alongside each other.

BioCryst, several royalty buyers on one issuer. In November 2021 BioCryst raised 350 million dollars by selling royalties to more than one investor at once: Royalty Pharma bought royalties on two Factor D inhibitors, and OMERS separately bought a capped, tiered royalty on Orladeyo, each for 150 million dollars upfront, on top of an earlier Royalty Pharma purchase and an Athyrium facility. T

here is no single co-investment vehicle here; instead an issuer assembling royalty capital from several investors side by side, which is the syndicated pattern on the sell side that makes sidecars useful on the buy side.

Coherus, a specialist leading with a co-investor. In February 2016 Coherus raised 100 million dollars of senior convertible notes led by HealthCare Royalty Partners with 75 million dollars, joined by KKR with 20 million dollars and by founding investors.

The instrument was convertible notes rather than a royalty purchase, but the shape is the lead-and-co-investor pattern a sidecar formalises: a specialist leads and others ride alongside on its diligence.

| Example | Period | Pattern | Primary source |

|---|---|---|---|

| Royalty Pharma / Legacy Investors Partnerships | to 2020 | Parallel co-investment, pro rata beside the main vehicle | SEC Form S-1 and Form 10-K |

| Athenex / Klisyri | 2022 | Two co-investors take one royalty under one agreement | SEC Form 8-K |

| BioCryst | 2021 | Several royalty buyers fund one issuer side by side | SEC filings and company release |

| Coherus | 2016 | A specialist leads, a co-investor rides alongside | SEC Form 8-K |

A caution on reading these. None is labelled a sidecar, and the deal-level economics, the allocation between the parties, the fee and carry, and who bore broken-deal cost, are not generally disclosed. They show that co-investment alongside a lead is routine in royalty financing. They do not reveal the governance terms, which is the part this note argues a co-investor has to confirm directly.

9. Diligence and underwriting map

| Dimension | What the GP confirms | What the co-investor confirms |

|---|---|---|

| Authority | LPA and side letters permit the sidecar and the offer order | The lead is acting within its fund documents |

| Allocation | Written policy, applied consistently, fund-first then sidecar | The split is policy-driven, not ad hoc favouritism |

| Conflicts | Disclosure of the co-invest conflict; even-handed offer | The conflict is disclosed and the terms are not adverse |

| Costs | Broken-deal and shared expenses split, not dumped on the fund | Its share of dead-deal cost is defined, not open-ended |

| Economics | Fee and carry terms; back-ended waterfall | The fee saving is real; carry alignment is acceptable |

| Diligence | Deal materials and timetable | Independent underwriting despite the compressed window |

| Tax | Blocker and jurisdiction fit the investor base | UBTI, ECI, withholding, and treaty position are handled |

| Concentration | Portfolio impact for the fund | This is one asset; the portfolio must be built across deals |

Implications

For sellers and originators. The sidecar is what lets an arranger commit a full ticket and close bilaterally while syndicating the overflow, which is the source of the certainty and speed sellers pay for. An originator whose model depends on placing deals larger than its fund should treat sidecar capacity, and pre-arranged anchor relationships, as core infrastructure rather than a deal-time scramble.

For managers and counsel. The exposure is allocation and cost-sharing, governed since June 2024 by Advisers Act fiduciary duty and disclosure rather than the vacated rules. A written, consistently applied allocation policy, disclosed conflicts, and shared broken-deal expenses are the controls that matter; the KKR settlement remains the reference point for what happens without them.

For co-investors and LPs. The fee saving is the prize and it is real on the evidence, but it accrues across a portfolio, not on a single concentrated position. Underwrite independently despite the compressed timetable, size the position against the dispersion of one royalty rather than the average, and confirm the allocation and cost-sharing governance before relying on the lead's diligence.

Reflects publicly available information as of 2026, derived from US adviser law and SEC enforcement materials, fund-formation and co-investment legal commentary, academic studies of co-investment performance, and public company disclosure. The regulatory position described, including the consequences of the June 2024 vacatur of the SEC private fund adviser rules, may change. The worked example and any figures are hypothetical and illustrative. For informational purposes only; not investment, legal, or financial advice. The author is not a lawyer or financial adviser.