Sleeves in royalty financing: structure, segregation, and capital treatment

The term "sleeve" appears in royalty financing documents in at least three distinct senses. They are not interchangeable.

Each carries a different answer to the two questions that decide what a sleeve is worth:

- Can a creditor of one sleeve reach the assets of another.

- Has the cash flow in the sleeve been transferred in a way that survives the seller's insolvency and qualifies for the capital treatment the buyer is paying for.

This note sets out the taxonomy, then works through the legal tests a transaction lawyer would run and the capital and rating mechanics a fund analyst would model.

It is written for pharmaceutical and life sciences royalty streams, with the principal vehicles in Luxembourg and the principal capital rules in the United States. It is current to June 2026, and where a rule is in motion the status is stated rather than smoothed over.

Summary

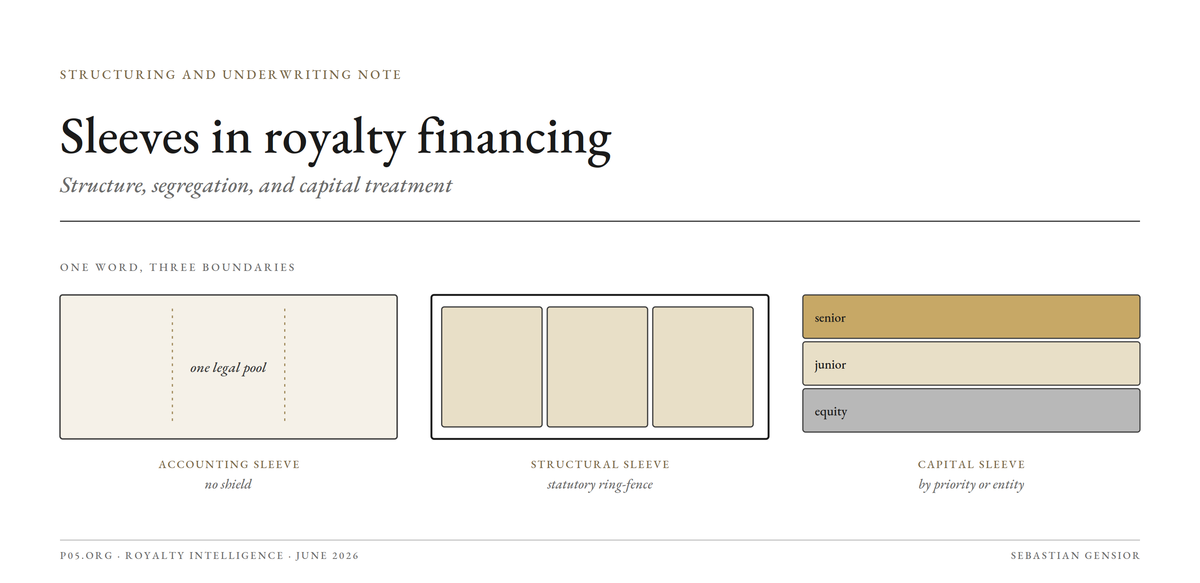

The boundary is the whole question. A sleeve is a sub-allocation inside a larger structure, and the only thing that matters is what its boundary is made of: an accounting partition inside one legal pool, a statutory ring-fence inside one legal person, or a separate legal person. Only the second and third bind a creditor.

Accounting sleeve. A sub-account with no separate legal personality and no statutory segregation. A reporting and mandate device, not a liability shield.

Structural sleeve. A compartment, cell, or series. In Luxembourg the segregation is statutory and is the default. The compartment has no legal personality of its own, which has consequences for contracting, enforcement, and insolvency.

Capital sleeve. A tranche of an issuer's stack, or a parallel vehicle beside the main fund. It segregates by payment priority or by separate incorporation, not by ring-fence.

Whether the royalty is in the sleeve, or only pledged to it, turns on a fact-intensive true sale analysis under US law. Recharacterisation as a secured loan keeps the royalty in the seller's estate and undermines the asset-backed analysis the rated sleeve depends on.

The rated-note sleeve is where insurer capital enters. Its capital efficiency now depends on two moving NAIC workstreams: the principles-based bond definition effective 1 January 2025, and the rating-discretion regime effective 1 January 2026.

1. Three senses of the word

The three uses separate cleanly by their legal boundary.

The same word, three different boundaries. Only the structural sleeve stops a creditor by statute.

The accounting sleeve is a partition within one portfolio: a virtual sub-account with its own tracked positions, cash, and tax lots, but no custodial registration and no separate legal personality. The assets remain a single legal pool.

The structural sleeve is a compartment, cell, or series whose assets and liabilities are segregated by statute. The vehicle is one legal person, but the law treats each compartment as a distinct pool for creditor recourse.

The capital sleeve is either a tranche of a single issuer's liabilities, a senior note ranking above a junior or equity interest, or a separate vehicle that invests alongside a main fund. It segregates by priority or by incorporation.

For each, a lawyer asks: can a creditor of A reach B, does A's failure trigger B's, and what perfection and characterisation analysis applies to assets moving in. An analyst asks the parallel set: how correlated are the sleeves on the downside, what is the capital charge on the instrument the sleeve issues, and how stable is that charge.

The answers differ by boundary type, which is why conflating the three produces mispricing in both directions.

2. The accounting sleeve

The accounting sleeve comes from managed-account practice, where one custodial account is partitioned so that several managers or strategies can be run and reported separately within it.

In royalty work it appears in two places:

- As a strategy or risk-budget carve-out inside a diversified credit or multi-strategy fund. A manager that runs royalties alongside direct lending, as H.I.G. does within its healthcare royalty and credit platform, is operating a royalty sleeve in this sense.

- As a liquidity sleeve of cash and short-dated paper held against undrawn warehouse capacity or pending deployment.

The defining legal feature is the absence of segregation. The assets booked to an accounting sleeve are not ring-fenced from the rest of the legal pool. A creditor of the fund reaches them regardless of which sleeve they sit in, and the failure of one strategy is not contained by the partition. Sleeve-level accounting supports attribution and reporting, and nothing more.

For the analyst it supports clean performance attribution. For the lawyer it provides no insulation. The recurring error is a limited-partnership document that uses "sleeve" for a strategy carve-out in a way that invites an investor to assume a ring-fence the legal form does not supply.

3. The structural sleeve: compartments, cells, and series

This is the sleeve that makes royalty bundling possible, because it lets a single vehicle hold many separate deals without each deal's risk reaching the others.

The Luxembourg compartment

The four product laws, the Part II regime under the Law of 17 December 2010, the SIF Law of 13 February 2007, the SICAR Law of 15 June 2004, and the RAIF Law of 23 July 2016, each permit an umbrella with multiple compartments, where each compartment is a segregated part of the assets and liabilities of the vehicle, and the constitutive documents must expressly allow their creation.

Under the RAIF Law, Article 49 establishes the umbrella and the segregation. The operative recourse rule is that the rights of investors and creditors relating to a compartment are limited to the assets of that compartment unless the constitutive documents provide otherwise.

Segregation is therefore the default. It must be effective vis-a-vis third parties to do its work, which is why the ring-fence has to be carried through the contractual documentation and not merely asserted in the prospectus.

Four features of the compartment matter to a transaction lawyer and are routinely underweighted.

| Feature of the Luxembourg compartment | Consequence | What to confirm |

|---|---|---|

| No legal personality | The compartment cannot contract or be sued alone; the umbrella acts "in respect of" it | Limited-recourse and non-petition language in every compartment-level contract |

| Two-level insolvency | A compartment can be wound up alone, but the umbrella is one legal person | Whether the regime is insolvency-remote enough; securitisation vehicle versus fund |

| Cross-investment permitted | Inter-compartment exposure reintroduces the correlation the ring-fence removes | That cross-investment is switched off where not needed |

| Risk-spreading per compartment | 30% single-issuer cap (SIF, RAIF), 20% (Part II), applied inside each compartment | Cohorting, or the risk-capital, unregulated, or securitisation route for concentrated holdings |

On the detail of those four:

A compartment has no legal personality, so no agreement may be signed by, nor any action brought against, a compartment in isolation. Recourse limitation against a counterparty therefore depends on the contract incorporating limited-recourse and non-petition terms on top of the statutory ring-fence.

Insolvency operates at two levels. A single compartment can be wound up without liquidating the vehicle: the SIF Law provides for the liquidation of one or several compartments, and the RAIF Law is to the same effect. But the umbrella is one legal person, so entity-level insolvency remains a tail exposure the compartment wall does not by itself remove. The structure is insolvency-remote, not insolvency-proof.

This is why the Securitisation Act of 22 March 2004, as amended in February 2022, is frequently the better chassis for rated paper than a fund vehicle. It provides statutory compartment ring-fencing, separate compartment liquidation, and statutory recognition of limited recourse, non-petition, and non-seizure, so that proceedings brought in breach of those provisions should in principle be declared inadmissible. The 2022 reform also widened the permitted financing and active-management scope, which is what lets a securitisation undertaking hold and manage a revolving pool rather than a static one.

Cross-investment is a deliberate gap in the wall. The RAIF Law permits a compartment to hold interests issued by other compartments of the same fund. Used without discipline, this reintroduces precisely the correlation the segregation was built to remove.

Risk-spreading binds inside each compartment. A regulated SIF or RAIF may not, in principle, place more than 30 percent of its assets in a single issuer, applied per compartment, with 20 percent for a Part II fund and ramp-up and wind-down exceptions where documented. A literal one-royalty-per-compartment design therefore fails diversification unless it runs the risk-capital regime, is structured outside the product laws as an unregulated SCS or SCSp, or uses a securitisation undertaking, which is not a risk-diversification vehicle. Cohorting royalties by compartment, rather than isolating each one, is the usual reconciliation.

Cross-jurisdiction equivalents

The compartment has counterparts that perform the same segregation under their own statutes: the Irish ICAV sub-fund under the ICAV Act 2015, the Delaware series and registered series LLC under section 18-215 of the Delaware LLC Act, the Cayman segregated portfolio company, and the protected cell and incorporated cell companies of Jersey and Guernsey.

The mechanism is consistent. The diligence point is recognition. Statutory ring-fencing is reliably honoured in the jurisdiction that created it, but a foreign court asked to enforce against the vehicle, or a foreign insolvency forum, may not give full effect to a cell wall it does not recognise. Where a key counterparty, a licensee, or the governing law of the underlying royalty sits outside the cell's home jurisdiction, recognition is a confirmed legal opinion, not an assumption.

4. The capital sleeve: tranches and parallel vehicles

The capital sleeve segregates by something other than statutory ring-fencing.

A tranche sleeve divides one issuer's liabilities by priority: a senior rated note ranking ahead of a junior note and an equity or first-loss interest. Segregation here is the waterfall, not the corporate boundary.

A co-investment or sidecar sleeve is a separate vehicle formed to invest alongside a main fund in a specific asset or in overflow, structured as a fund-of-one or commingled, blind or disclosed. New Jersey's pension committed 300 million dollars to a TCW separately managed account together with a co-investment sleeve in one allocation. Because it is a separate legal person, it segregates by incorporation.

A warehouse sleeve is the revolving facility, usually a bank line to a ramp vehicle, that holds royalties before they are termed out. Its boundary is the facility and its borrowing base.

The rated-note sleeve is the tranche an insurer buys. It is treated in section 7, because its mechanics are driven by insurance capital rules rather than by royalty structuring.

5. Has the royalty entered the sleeve, or only been pledged to it

This is the question that decides whether the structural sleeve actually contains the asset.

Under US law a royalty transfer is governed by UCC Article 9 whether it is a sale or a secured loan, because Article 9 applies to sales of accounts, chattel paper, payment intangibles, and promissory notes as well as to security interests. The sale-versus-loan distinction does not change whether Article 9 applies. It changes whether the royalty is in the seller's bankruptcy estate, whether it is caught by the automatic stay, and how it is treated for usury and tax.

Characterising the royalty

A pharmaceutical license royalty is generally a payment intangible or a general intangible, not an "account," because an account is a right to payment for goods sold or services rendered, which a license royalty is not.

The classification has a perfection consequence. A sale of a payment intangible is automatically perfected on attachment under section 9-309, with no filing required, whereas a royalty characterised as an account requires a UCC-1 to perfect a sale. In practice a protective UCC-1 is filed regardless, because the characterisation is not always clean and a filing is cheap against being wrong.

The true sale test

Whether the transfer is a sale or a disguised financing is decided on a fact-intensive, multi-factor test applied as federal common law, with no single factor dispositive. Recourse to the seller and the seller's right to excess collections carry the most weight. In Shoot the Moon the transaction was recharacterised as a disguised financing; in R&J Pizza the comparable factors supported a true sale.

| Factor | Points toward true sale | Points toward secured loan |

|---|---|---|

| Recourse to seller | Limited to closing reps and warranties | Ongoing recourse for collection shortfalls |

| Right to surplus collections | Buyer keeps the upside | Seller retains the excess over a fixed return |

| Repurchase rights | None or narrow | Broad or mandatory |

| Risk and reward of ownership | Transferred to the buyer | Retained by the seller |

| Pricing | Arm's-length purchase price | Advance against a discounted balance |

| Language and conduct | "Seller" and "buyer"; sale terms | "Lender" and "borrower"; debt terms |

Why this is the sleeve question. A true sale into a compartment is what makes that compartment's assets bankruptcy-remote from the seller. If the transfer is recharacterised, the royalty stays in the seller's estate and the compartment holds only a security interest, subject to the stay and to the seller's other creditors.

For a rated-note sleeve the damage compounds. The asset-backed analysis assumes the ABS issuer owns the collateral, so recharacterisation that leaves ownership with the seller is not just a bankruptcy-remoteness problem but a threat to the bond characterisation the sleeve was built to obtain.

6. Security and perfection at the sleeve level

Perfection is done per sleeve and against the right debtor, not at the umbrella.

In the US that means a UCC-1 naming the correct transferring entity, with the collateral described to match the characterisation, plus a backstop filing for the protective security interest. In Luxembourg, security follows the applicable pledge and assignment formalities: a pledge over SCS or SCSp interests is perfected by notification and registration in the partners' register and requires the general partner's consent, and a pledge over receivables is perfected on notice to the debtor.

Two frictions sit on top:

- Anti-assignment terms in the underlying license. Sections 9-406 and 9-408 of the UCC render many restrictions on assignment of payment rights and general intangibles ineffective against the secured party, but they do not cure the commercial reality of a change-of-control or consent provision that can disrupt the cash flow upstream. That has to be traced through to the sleeve.

- Collection mechanics. Notice to the licensee as account debtor and control over the collection account determine whether the buyer actually receives the cash it has bought, independent of perfection in the abstract.

7. The rated-note sleeve and insurer capital

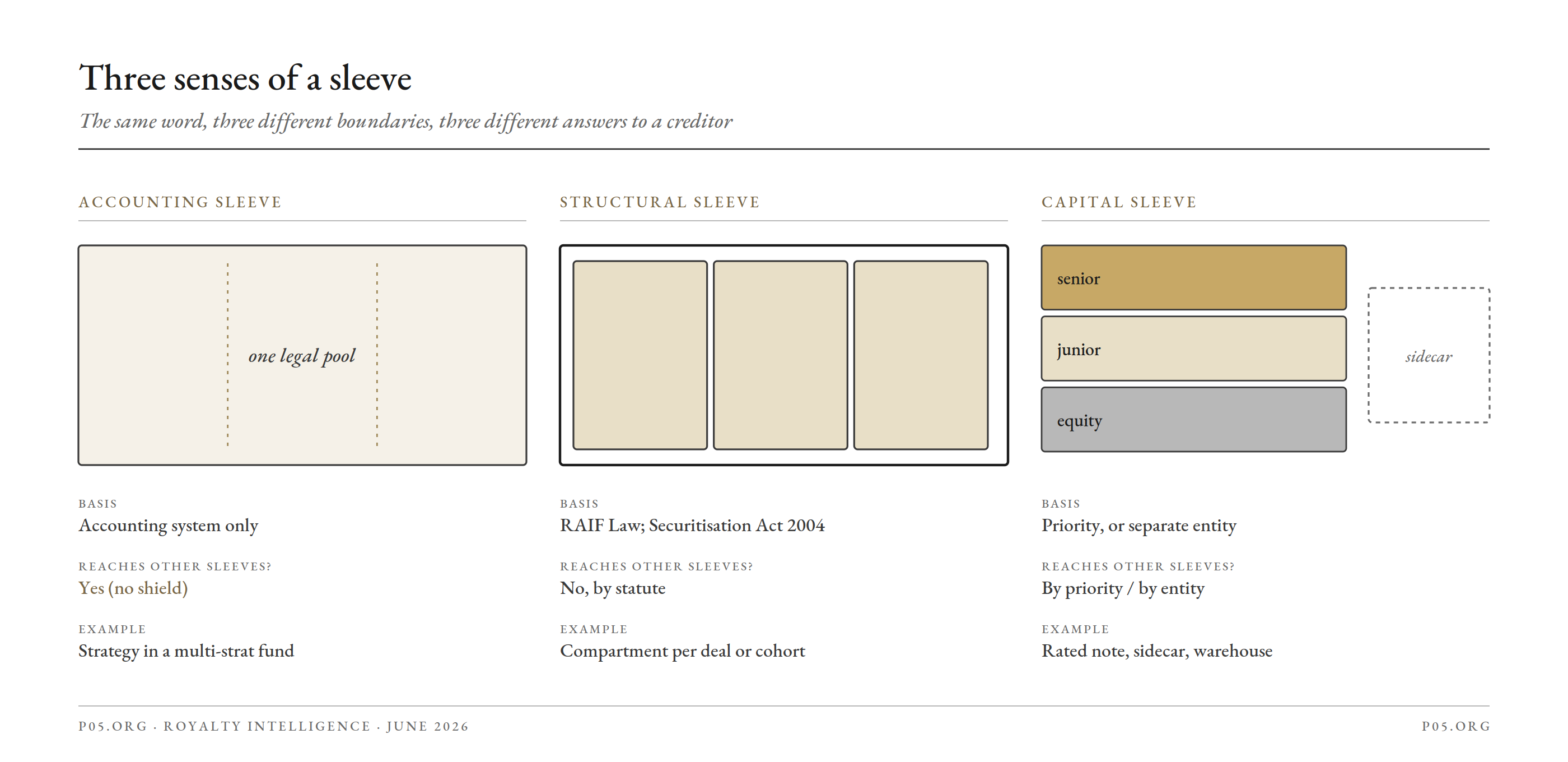

The rated-note sleeve exists to convert an exposure an insurer would otherwise hold as equity into one it can hold as a bond, because the capital charge on the two is very different.

An insurer holding a limited-partner interest in a royalty fund reports it on Schedule BA and takes an equity-like risk-based capital charge. An insurer holding a qualifying bond reports it on Schedule D-1 and takes a charge set by its NAIC designation, which for investment-grade paper is materially lower. The dual-issuance feeder issues both ordinary equity interests and rated notes so the insurer can buy the notes.

Two NAIC workstreams now govern whether that conversion holds.

The rated-note sleeve has to pass both gates to keep its Schedule D-1 charge. Failing either drops it to Schedule BA.

| Workstream | What it tests | Effective | Status, June 2026 | Effect on the sleeve |

|---|---|---|---|---|

| Principles-based bond definition (SSAP 26R / 43R) | Whether the note is a genuine ABS, not equity in a debt wrapper | 1 Jan 2025, no grandfathering | In force | Failure moves it off Schedule D-1 to Schedule BA, raising the charge |

| CRP rating discretion (P&P Manual) | Whether the agency rating is a reasonable assessment of risk | 1 Jan 2026 | In force; operational systems still being built; expected rare use | A three-notch challenge can strip filing-exempt status and raise the designation |

Gate one: the bond definition

The NAIC adopted the principles-based bond project (REF 2019-21) on 16 March 2024, effective 1 January 2025 with no grandfathering, revising SSAP No. 26R and SSAP No. 43R.

It splits qualifying bonds into issuer credit obligations, repaid from the general creditworthiness of an operating entity, and asset-backed securities, where the issuer is an ABS Issuer and the primary source of repayment is the cash flow of the defined collateral. A royalty feeder is an asset-backed security, so it must satisfy the ABS test.

The analysis is demanding for feeders. Where repayment relies on equity interests there is a rebuttable presumption that the note is not a creditor relationship. To qualify, the note needs predetermined principal and interest that do not vary with collateral performance, sufficient predictable cash flows, and substantive credit enhancement, with an agency rating expressly not treated as automatic validation.

A note that fails drops from Schedule D-1 to Schedule BA. The design implication is concrete: the collateral has to read as a genuine, diversified, cash-generating pool with real subordination, not a thin wrapper over a single concentrated, equity-shaped interest.

Gate two: rating discretion

As of 1 January 2026 the NAIC's investment analysis office may challenge the agency rating used to grant a security filing-exempt status where the rating differs from its own assessment by three or more notches and does not, in its view, provide a reasonable assessment of investment risk.

Removal from filing-exempt status forces the security to be filed, which can raise its NAIC designation and therefore its capital charge. Under the standard mapping, an agency rating in the A range corresponds to NAIC 1 and the BBB range to NAIC 2, so a downward revision moves the charge up a band.

The authority took effect on 1 January 2026, though the operational systems were still being built out through the first half of the year, and it is expected to be used in well under five percent of cases. The institutional context is also shifting: the Valuation of Securities Task Force was replaced on 1 January 2026 by the Invested Assets Task Force, a separate credit-rating-provider due diligence framework is in development, and the CLO modelling project that informs structured-security capital has been extended to year-end 2026.

For an analyst the takeaway is that the rated sleeve's capital charge is now a function of two things that can move after closing, the bond characterisation and the designation, rather than a fixed input set at issuance.

Europe

A sleeve sold into European balance sheets meets the EU and UK Securitisation Regulations, which impose risk retention, transparency, and investor due-diligence obligations that have to be cleared at structuring, and which apply to the feeder and collateralised-fund-obligation analysis as much as to a conventional securitisation.

8. Tax and structural overlays

Two points affect the choice of wrapper rather than only the documentation.

Subscription tax. A Luxembourg fund vehicle is generally subject to the annual subscription tax (taxe d'abonnement) at 0.01 percent of net assets per quarter, with exemptions including investments in other Luxembourg funds already subject to the tax, money-market, microfinance, and pension-pooling vehicles. A securitisation undertaking is taxed on a different and broadly neutral basis, with payments to investors generally deductible, which is part of why rated paper tends to be issued from a securitisation vehicle rather than a fund.

Reverse hybrids. Where the equity sleeve is built through an SCSp with non-EU investors, the ATAD 2 reverse-hybrid rule can apply, so a partnership that is otherwise tax-transparent in Luxembourg becomes taxable on certain income if a majority of its interests are held by associated enterprises in jurisdictions that treat it as opaque. This is a structuring item for the equity sleeve's investor base, not a documentation afterthought.

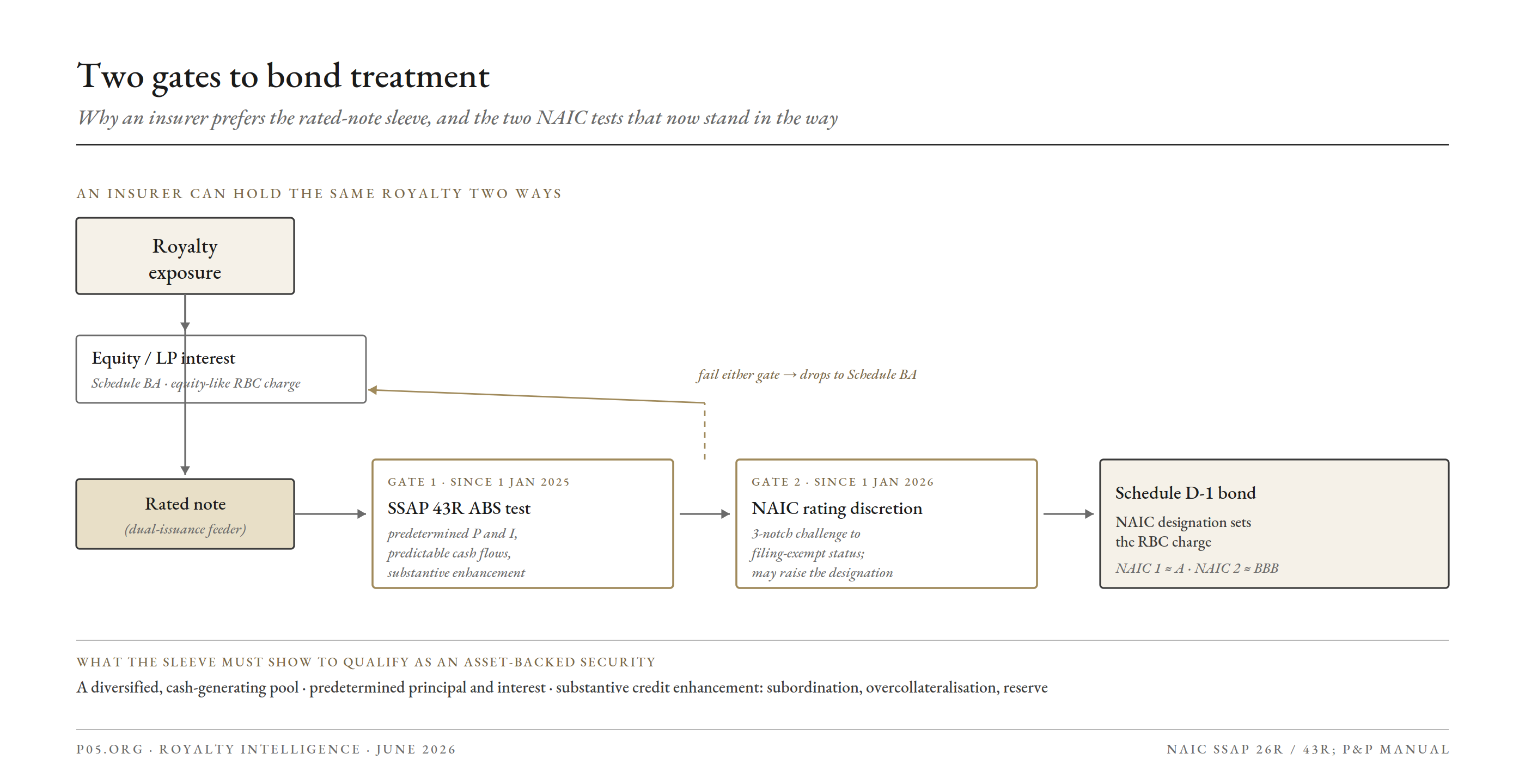

9. A worked structure

The following is hypothetical and simplified, used to show how the sleeves interlock and where the diligence sits.

Origination, a revolving warehouse, ring-fenced compartments by cohort, and the holders of each sleeve.

The chassis is a Luxembourg securitisation undertaking with compartments, chosen over a fund for the statutory limited-recourse and non-petition protection and for the absence of a risk-spreading constraint.

- Royalties are grouped by cohort, so each compartment holds a diversified basket rather than a single asset.

- Each acquisition is a true sale into the compartment, documented to the true-sale factors and supported by an opinion.

- Each compartment issues a senior rated-note sleeve to insurers, targeted at an investment-grade designation, and a junior or first-loss sleeve to the sponsor and family offices.

- An anchor investor takes a co-investment sleeve in one named orphan-drug royalty through a parallel SCSp.

- A warehouse sleeve, a bank facility to a ramp vehicle, revolves new royalties before allocation to a compartment.

The points that decide whether the structure performs as drawn are the ones the diagram hides:

- A default in one royalty is contained to its compartment by the statutory ring-fence and the limited-recourse and non-petition provisions, leaving note holders in other compartments unaffected, provided cross-investment is switched off.

- Each acquisition needs a true-sale opinion at the compartment level. Broad recourse, a retained right to surplus, or wide repurchase rights threaten recharacterisation, and with it both bankruptcy remoteness and the asset-backed characterisation of the senior sleeve.

- Perfection is per seller and per asset: protective UCC-1 filings, Luxembourg pledge and assignment formalities, account control, and notice to licensees as account debtors.

- The rated-note sleeve has to clear the ABS test under SSAP 43R, carry substantive enhancement through subordination, overcollateralisation, and a reserve, and is exposed to the 2026 rating-discretion regime. A European placement adds the Securitisation Regulation retention and disclosure obligations.

On the analyst side the structure resolves to a familiar set of inputs: an advance rate on the warehouse set by eligibility and the borrowing base; credit enhancement on the term sleeve sized to the attachment point for the target designation; a weighted-average life driven by royalty run-off and any step-downs in the underlying licenses; and a capital charge on the senior sleeve that is now contingent on the bond and designation analysis rather than fixed.

Illustrative economics

The figures below are hypothetical and rounded, used to show how the structure resolves into numbers rather than to quote a market.

Take one compartment holding a cohort of marketed royalties with a blended weighted-average life of around six years and broad diversification across products and payors.

- The warehouse advances against eligible royalties at, say, 70 to 80 percent of an agreed valuation, with the gap funded by first-loss equity, so the ramp is mostly debt-funded before term-out.

- On term-out, the senior rated-note sleeve is sized to a target designation. The lower the targeted category, the more enhancement sits beneath it: subordinated notes, overcollateralisation, and a cash reserve together set the attachment point.

- Weighted-average life and the dispersion of the cohort's cash flows drive the rating. A longer tail or a more concentrated pool widens the loss distribution the agency models, which raises the enhancement required for any given designation.

- The same pool can therefore be cut into a thicker, cheaper senior plus a thinner mezzanine, rather than one blended tranche, to optimise the overall cost of capital across the holders.

| Target senior designation | Enhancement beneath the senior | Senior coupon | Insurer capital charge |

|---|---|---|---|

| NAIC 1 (A range and above) | Higher | Lower | Lower |

| NAIC 2 (BBB range) | Lower | Higher | Higher |

Directional only. The relationships hold; the magnitudes are deal-specific.

The capital charge an insurer ultimately carries against the senior note follows from that designation. As set out in section 7, the designation is now contestable under the 2026 rating-discretion regime, so the enhancement that comfortably supported it at closing is also what defends it against a later challenge.

Precedent transactions sit in the public record for calibration, including the Cystic Fibrosis Foundation's sale of its residual Vertex royalty to Royalty Pharma for 575 million dollars upfront plus milestones, the Sagard and Oaktree acquisition of the Klisyri royalty from Athenex, and an OMERS-managed fund's purchase of ImmunoGen's residual Kadcyla royalties, and the older practice of issuing pharmaceutical royalty bonds collateralised by a licensed royalty stream.

10. Diligence and modelling map

| Sleeve type | Segregation mechanism | Insolvency and recharacterisation exposure | Perfection and documentation | Capital and rating sensitivity |

|---|---|---|---|---|

| Accounting / portfolio | None. Partition within one legal pool | Full exposure to the fund's creditors and other strategies | Not applicable; assets held at fund level | None at the sleeve level; relevant only for attribution |

| Lux compartment (RAIF, SIF, Part II) | Statutory, default segregation; opposable to third parties if documented | Single-compartment wind-up possible; entity-level insolvency is a tail; no legal personality; cross-investment must be off | Constitutive docs must allow compartments; pledge and assignment per asset; risk-spreading per compartment | Indirect; affects the rated sleeve's collateral isolation |

| Lux securitisation compartment (Act of 2004, amended 2022) | Statutory; limited recourse, non-petition, non-seizure recognised by statute | Strongest insolvency-remoteness available; separate compartment liquidation; still one legal person | True sale into compartment; protective filings; collection-account control | Preferred chassis for rated paper; supports the ABS analysis |

| Cell / series (Cayman SPC, Delaware series, Irish ICAV, Channel Islands PCC) | Statutory, jurisdiction-specific | Recognition of the cell wall by a foreign court or insolvency forum is the open question | Local formalities; cross-border recognition by opinion | As above, subject to recognition |

| Co-investment / sidecar | Separate legal person | Segregated by incorporation; ordinary entity insolvency analysis | Vehicle-level security; allocation and conflicts policy | Charge depends on the instrument issued |

| Warehouse | Facility and SPV | Ramp-vehicle insolvency; limited recourse to the facility | Borrowing base, eligibility, perfection on revolving collateral | Advance rate and eligibility drive available leverage |

| Rated-note (feeder) | Tranche priority within an issuer | Recharacterisation of the transfers undermines the ABS analysis | True sale at collateral level; substantive enhancement | SSAP 43R ABS test; NAIC designation; 2026 rating discretion; EU/UK Securitisation Regulation |

Implications

For originators and sellers. The sleeve a buyer uses identifies who is funding the bid and on what capital math. A bid routed through a rated-note sleeve is an insurance bid that depends on the post-2025 bond characterisation and the post-2026 designation holding, so price and certainty follow from those rather than from the headline. Presenting cohorts that read as genuine asset-backed collateral, rather than single concentrated interests, widens the set of balance sheets that can bid.

For structurers and counsel. Confirm which boundary each sleeve actually has. Only the structural sleeve segregates liability by statute, and only as far as its governing law is recognised and its cross-investment provisions are disabled. The true-sale analysis is the load-bearing legal work, because recharacterisation defeats both bankruptcy remoteness and the bond characterisation at once. Perfect at the right level, against the right entity, with the underlying license's assignment and change-of-control terms traced through to the cash flow.

For investors and insurers. Treat the rated sleeve's capital charge as a variable rather than a constant. Confirm the pool meets the ABS definition on substance, that enhancement is real and not nominal, and that the agency rating is defensible against a three-notch divergence under the rating-discretion regime now in force. For European holders, confirm the retention and disclosure position under the Securitisation Regulation.

Reflects publicly available information as of June 2026, derived from Luxembourg fund and securitisation legislation, the Uniform Commercial Code and US insolvency practice, NAIC statutory accounting and valuation guidance, and specialist legal commentary. Several of the regimes described, in particular the NAIC rating-discretion process and related workstreams, are in active development and their application may change. The worked structure and any figures are hypothetical and illustrative. For informational purposes only; not investment, legal, or financial advice. The author is not a lawyer or financial adviser.