Royalty Financing on the Balance Sheet: Liability, Disposal, or Something the Rating Agencies See Through

A royalty fund's pitch to a pharmaceutical finance function compresses three claims into a single sentence: monetisation is non-dilutive, it is off-credit, and it is good for the accounts. The first is almost always true. The second and third are true for one version of the transaction and misleading for the other, and the distinction is not a drafting detail. It determines whether the upfront cash leaves the balance sheet, sits on it as a deemed borrowing for the next decade, or produces a one-time gain that flatters the year of sale.

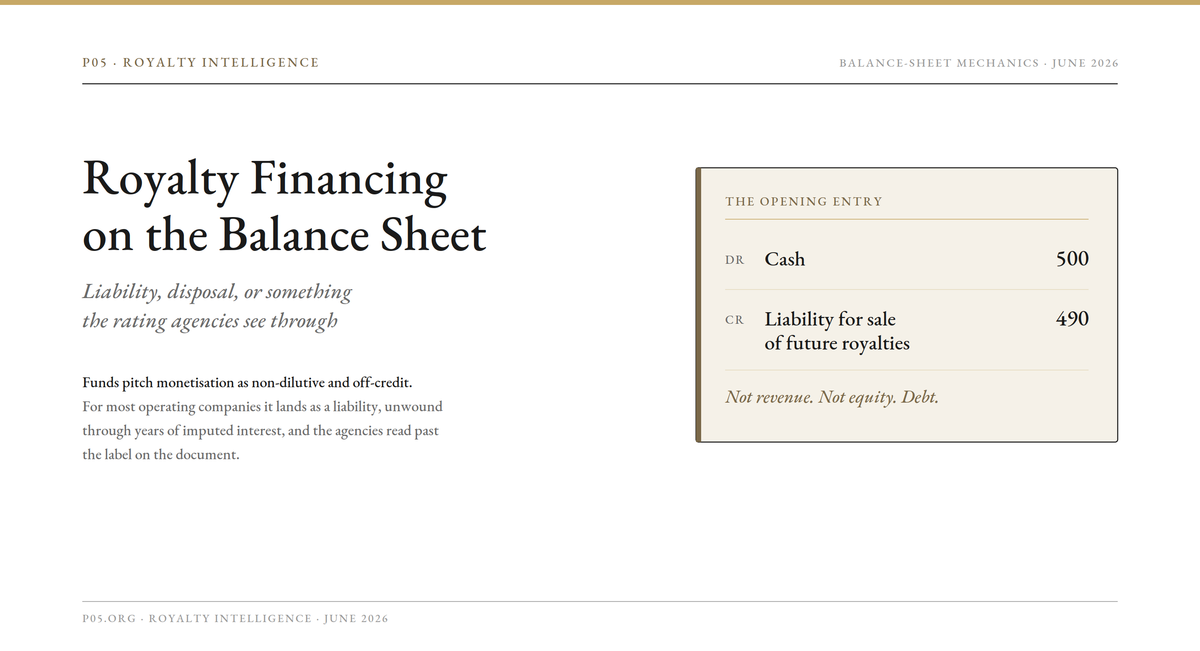

The empirical reality is the place to start, because it cuts against the intuition the pitch relies on. When Ionis monetised part of its SPINRAZA royalty to Royalty Pharma for USD 500 million in January 2023, it did not record a sale. It recorded a liability. W

When PTC Therapeutics monetised its EVRYSDI royalty to the same buyer, first for USD 650 million in 2020 and then for a further USD 1.0 billion in 2023, it did not record a sale either. It recorded a "liability for sale of future royalties" and explicitly classified the proceeds as debt. Both companies were selling royalties they received from a third party, the cleanest version of the transaction, the version a controller would expect to come off the books. Both ended up with a liability and a stream of non-cash interest expense.

That outcome is not an accident of those two deals. It follows from how the accounting standards are built, and from a single structural feature, the cap with reversion, that almost every operating-company monetisation contains.

The decision to take royalty capital, and whether it is priced fairly against the alternatives, is a separate question, worked through stage by stage in the CFO's complete guide to royalty financing. That guide notes in passing the fact this article is built around: most monetisations are documented as legal sales yet land on the balance sheet as debt.

This piece is the financial-statements companion to it. It takes that one observation and works it all the way through, from first principles under both US GAAP and IFRS, into the liability roll-forward and the income-statement mechanics with real disclosed numbers, through the cash flow statement, and out to how rating agencies and existing lenders look past the presentation. It assumes familiarity with the insolvency architecture and the threshold and cap mechanics that determine the risk transfer the accounting then tests.

Four Transactions Wearing One Name

"Monetisation" is an umbrella over at least four structures that diverge in their accounting from the first journal entry. The label a fund uses describes the legal form. It does not decide the accounting, which turns on substance.

| Structure | What is sold | Underlying cash flow | Who keeps operating the product |

|---|---|---|---|

| Traditional royalty sale | An existing contractual royalty the company receives from a licensee | Third-party net sales | The licensee (a third party) |

| Synthetic royalty | A newly created revenue interest in the company's own product | The company's own net sales | The company |

| Development / R&D funding | A return contingent on success, funding a trial or launch | Future milestones and royalties on an unapproved asset | The company |

| Royalty-backed note | A non-recourse note serviced by a defined royalty stream | Royalty or sales stream pledged to service the note | The company or licensee |

The traditional sale looks like a disposal of an asset the company already owns. The synthetic looks like a forward sale of revenue the company has not yet earned and still controls. Development funding sits at the intersection of financing and risk-sharing on an asset that may never reach the market. The royalty-backed note, the structure in Royalty Pharma's March 2026 USD 250 million non-recourse note against Ziihera royalties, is debt in form as well as substance.

The legal documents across these can look almost identical. The accounting does not, because the question the standards ask is not "what is this called" but "has the company genuinely parted with the risk and reward, or has it borrowed against a cash flow it still owns." The same four types can be cut by availability and use case rather than by accounting substance, which is the angle the CFO's guide takes; the table above is cut by the question that drives the balance-sheet outcome.

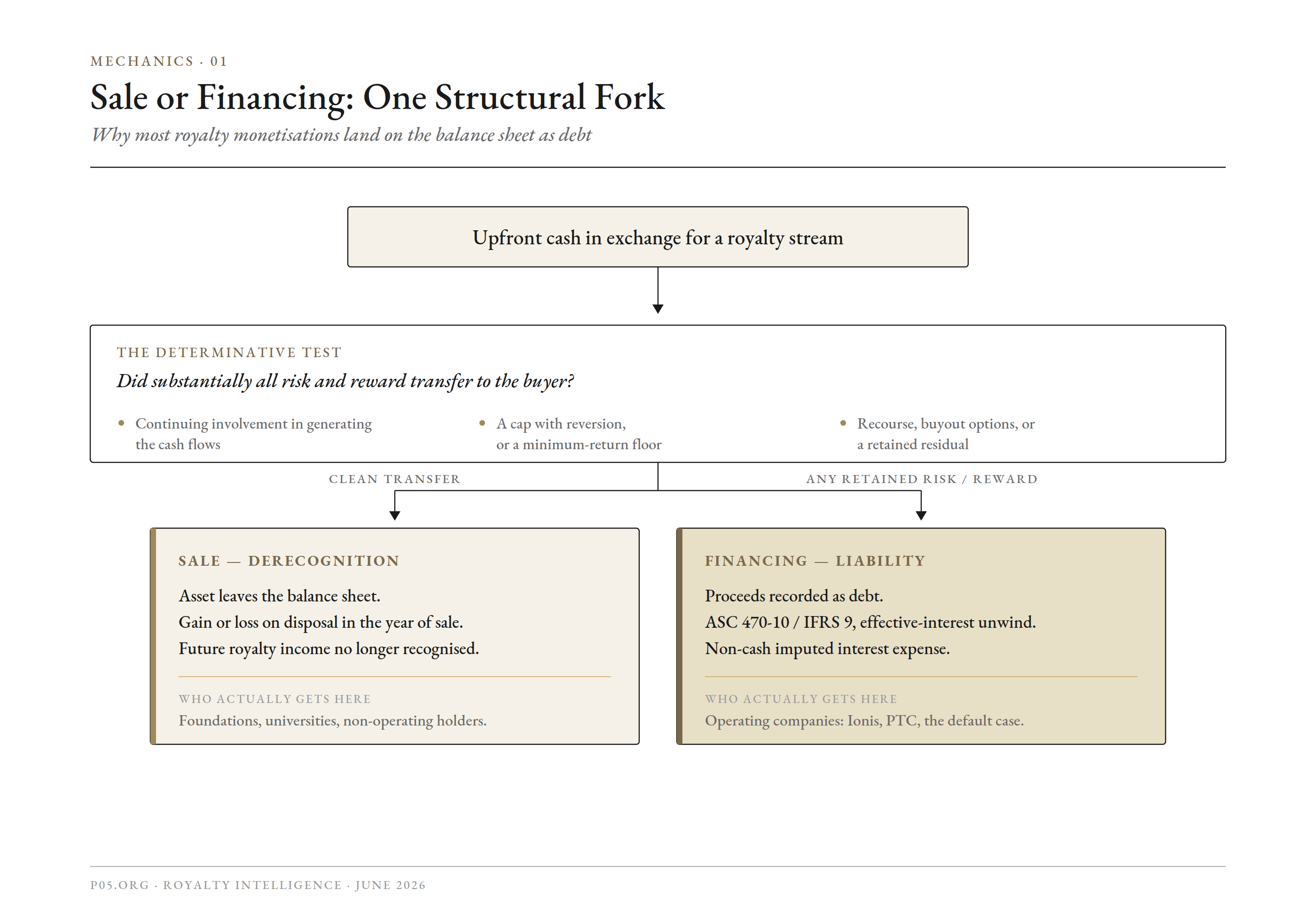

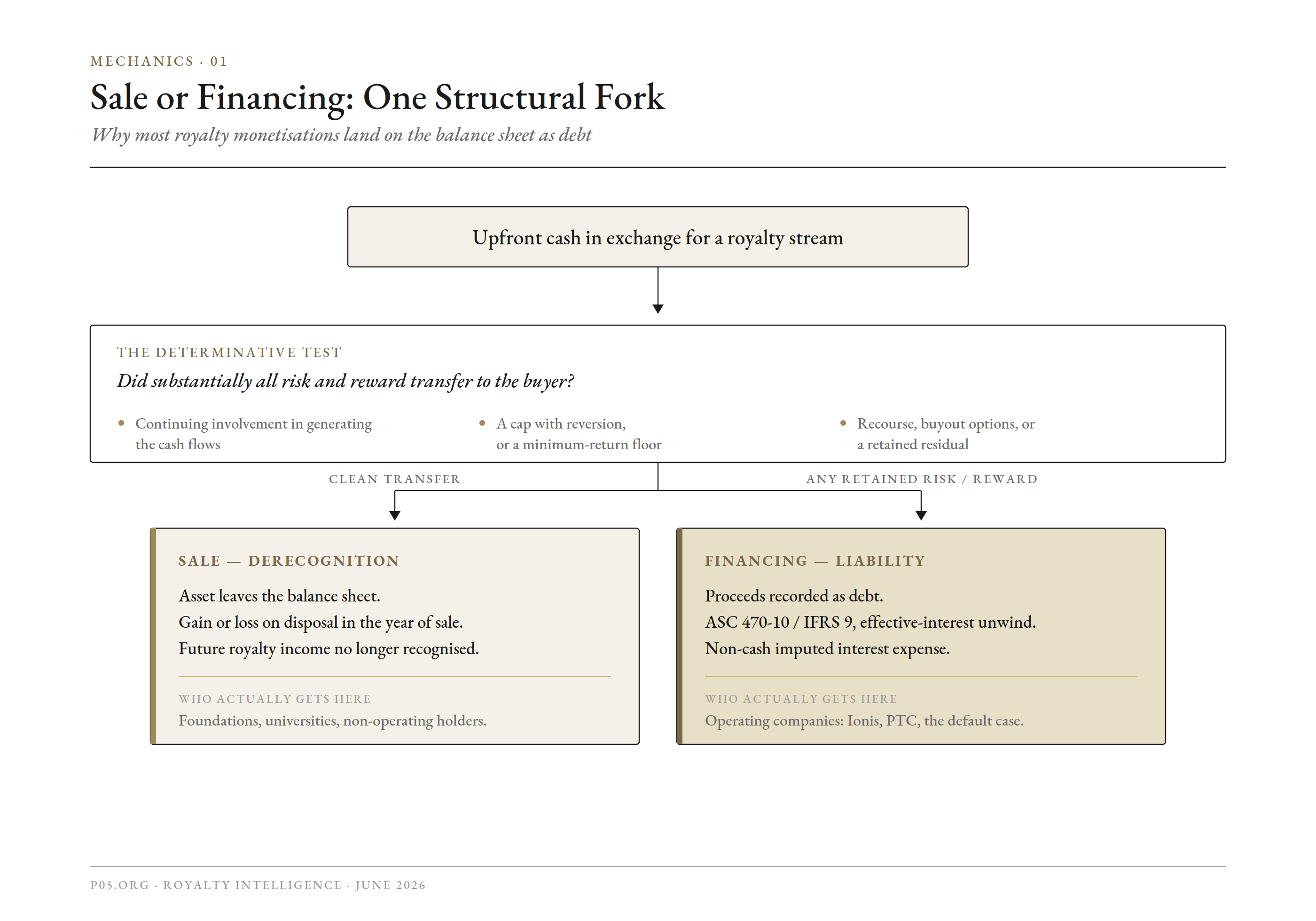

The Threshold Question: Sale or Financing

Every monetisation by an operating company runs into the same fork. Either the proceeds are consideration for an asset the company has disposed of, in which case it derecognises the asset and books a gain or loss, or the proceeds are a financing the company must unwind, in which case it records a liability and recognises interest. US GAAP and IFRS reach this fork by different routes and, in the typical pharma case, arrive at the same answer.

The US GAAP Route: ASC 470-10

An arrangement in which an investor pays cash for a percentage of a company's future revenue is, as the revenue standard's own scope guidance confirms, generally not a contract with a customer and therefore not in the scope of ASC 606. It falls instead under ASC 470-10, "Sales of Future Revenue."

That subtopic describes the fact pattern precisely: an entity receives an upfront sum and agrees to pass a specified percentage of future revenue, originating either from its own operations or from third-party royalties it receives, to the investor for a defined period, sometimes with a guaranteed minimum, often with a maximum total.

The seller must then decide whether the proceeds are debt or deferred income. ASC 470-10-25-2 lists six factors, any one of which independently creates a rebuttable presumption of debt classification.

| ASC 470-10-25-2 factor | Typical pharma synthetic or capped monetisation | Points toward |

|---|---|---|

| (a) Transaction does not purport to be a sale | Most are drafted as sales, so this one often does not bite | Sale |

| (b) Significant continuing involvement in generating the cash flows | The company still makes, markets, and books the product | Debt |

| (c) Cancellable by either party via lump sum or asset transfer | Buyout and call options are common | Debt |

| (d) Investor's return is implicitly or explicitly limited | A cap multiple limits the buyer's return | Debt |

| (e) Revenue variation has only a trifling impact on investor return | Rare in true synthetics; return usually tracks sales | Sale |

| (f) Investor has any recourse to the entity | Non-recourse is common, but guarantees and indemnities recur | Debt |

Factor (b) is the one that catches almost every monetisation by a company that still operates the product. If the seller manufactures, promotes, prices, and recognises the sales that generate the very cash flows the fund is buying, it has significant continuing involvement, and the presumption is debt. Factor (d) catches the rest: a cap multiple, present in the substantial majority of synthetic deals, limits the buyer's upside and points to debt regardless of continuing involvement.

This is why the traditional sale of a third-party royalty does not reliably escape debt treatment. Ionis sold a royalty it receives from Biogen and Novartis, not a slice of its own product sales, yet the deal reverts to Ionis once Royalty Pharma collects USD 475 million to USD 550 million.

That reversion leaves Ionis with the residual interest and the tail upside, which is retained reward, which is debt. PTC's EVRYSDI agreement terminates once the buyer has received USD 1.3 billion, and PTC retained a slice of the royalty and the milestones, the same retained-interest pattern, the same debt conclusion.

Where debt classification applies, ASC 470-10-35-3 requires the company to determine an effective interest rate from the proceeds and the projected timing and amount of future cash outflows, then amortise the liability using the interest method.

Where the facts instead support deferred income, the liability is amortised as the related revenue is recognised, the units-of-revenue method, which produces a different expense pattern but the same balance-sheet presence. For operating-company monetisations, debt classification is the dominant outcome.

This is the mechanism behind a statistic that otherwise looks paradoxical. A Covington study of 39 royalty monetisations from 2019 to 2023 found that roughly 95 percent were documented as legal true sales, with no fixed repayment obligation. The accounting outcome runs the other way: the same continuing-involvement and capped-return features that the legal true-sale opinion tolerates are precisely the features that ASC 470-10-25-2 reads as debt.

A transaction can be a sale for the lawyers and a borrowing for the accountants in the same closing binder, and for operating companies it usually is.

The IFRS Route: IFRS 9 Derecognition

A company reporting under IFRS finds no ASC 470. The analysis runs through IFRS 9 and turns on the same substance question.

If the company is selling a royalty receivable it already recognises as a financial asset, it applies the IFRS 9 derecognition test. The asset comes off the balance sheet only if the company has transferred substantially all the risks and rewards of ownership, or, failing that clean test, has transferred control. IFRS 9's derecognition model is deliberately resistant to off-balance-sheet structuring, designed to stop entities parking assets elsewhere while retaining the economics.

A cap with reversion, a minimum-return guarantee, recourse, or a retained residual all mean the company keeps substantially all the risks and rewards, fails derecognition, keeps the asset on its books, and recognises the proceeds as a financial liability. Where risk and reward are split rather than cleanly transferred, continuing-involvement accounting can require the company to keep recognising the asset to the extent of its continuing involvement and book an associated liability, a partial version of the same result.

If the company is doing a synthetic royalty on its own future product sales, there is no pre-existing financial asset to derecognise. Future self-generated revenue is not an asset under IFRS until the underlying sales occur. The proceeds are a financial liability under IFRS 9, measured at amortised cost and unwound using the effective interest method, unless the contract contains or constitutes a derivative, which the sales-volume settlement exclusion generally prevents.

| Dimension | US GAAP | IFRS |

|---|---|---|

| Governing model, sell own future revenue | ASC 470-10, sale of future revenue | IFRS 9 financial liability at amortised cost |

| Governing model, sell owned royalty receivable | ASC 860 transfer analysis, then ASC 470 if not a sale | IFRS 9 derecognition (risks and rewards, then control) |

| Default outcome for operating company | Liability (debt), effective interest method | Financial liability, effective interest method |

| Path to off-balance-sheet | True sale, no continuing involvement, clears 25-2 factors | Derecognition, transfer of substantially all risks and rewards |

| Subsequent expense | Imputed interest (output rate) | Imputed interest (output rate) |

| Re-estimation | Prospective, catch-up, or retrospective | Recalculate at original EIR, adjust carrying amount |

The practical conclusion is identical across both regimes. The synthetic is a liability. The traditional sale can be a disposal, but only where the risk transfer is real and complete, which a cap or reversion defeats.

The Default Outcome: A Liability That Behaves Unlike a Bond

When the analysis lands on debt, the balance sheet does not shrink. Cash comes in, a liability of roughly equal size goes up, and both sides of the balance sheet grow until the royalty stream retires the liability. The line item is consistent across filers: a "liability related to the sale of future royalties," recorded initially at proceeds net of issuance costs.

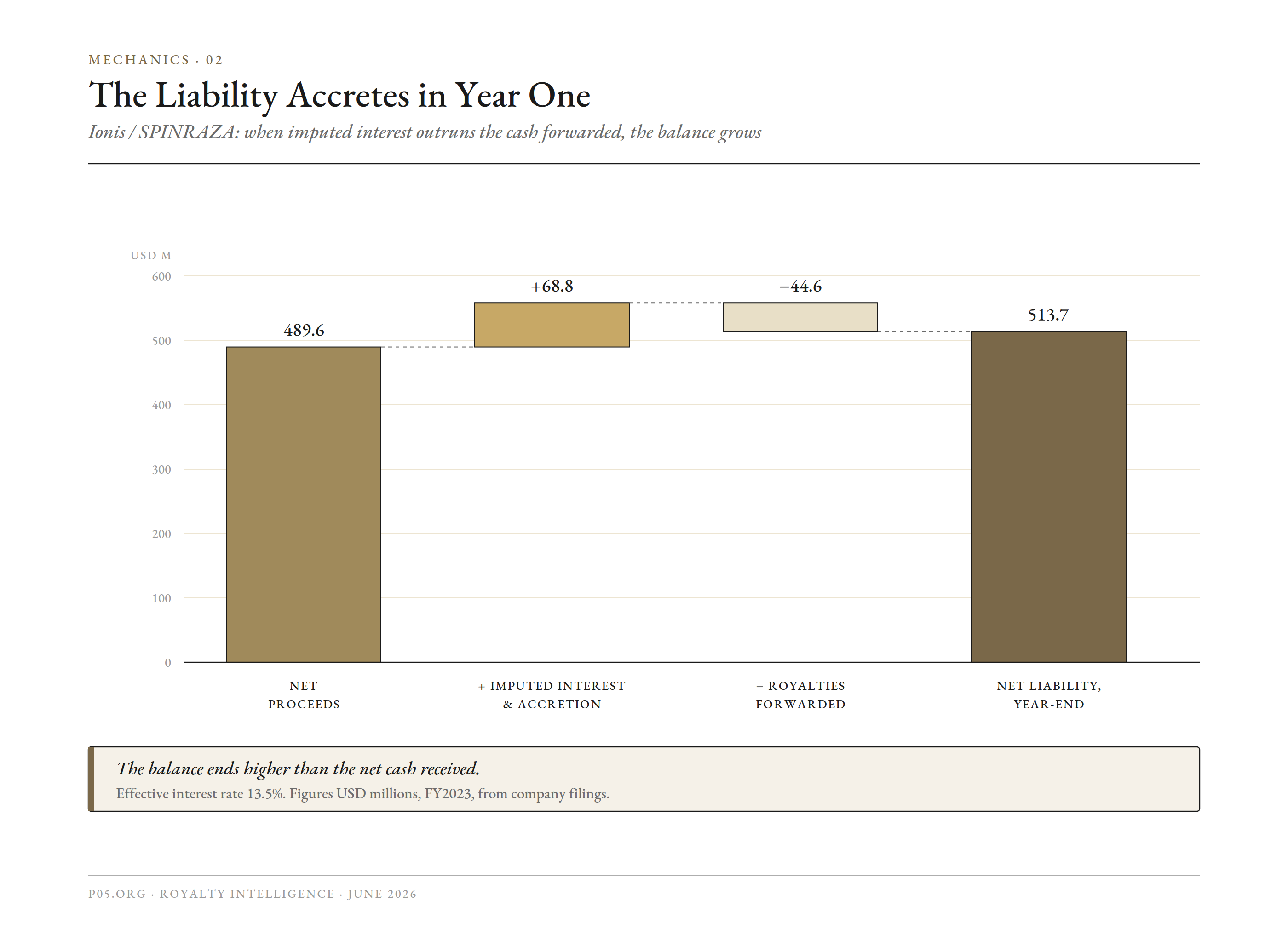

The Ionis SPINRAZA arrangement is the cleanest worked example in the public record. The figures below are drawn from its filings.

| Liability related to sale of future royalties (Ionis / SPINRAZA, USD thousands) | Amount |

|---|---|

| Proceeds from sale of future royalties, January 2023 | 500,000 |

| Issuance costs | (10,434) |

| FY2023 royalty payments forwarded to Royalty Pharma | (44,628) |

| FY2023 imputed interest expense | 68,238 |

| FY2023 amortisation of issuance costs | 560 |

| Net liability at 31 December 2023 | 513,736 |

| Estimated effective interest rate, 2023 to 2024 | 13.5% |

| Estimated effective interest rate, Q3 2025 | 12.4% |

| Reversion to Ionis after Royalty Pharma collects | 475,000 to 550,000 |

Three features of that table reward attention.

First, the liability rose in its first year. Ionis took in USD 500 million, forwarded USD 44.6 million to the buyer, and still owed more at year-end (USD 513.7 million) than the net proceeds it started with, because imputed interest of USD 68.2 million exceeded the cash forwarded. A monetisation whose early royalty payments do not cover the imputed interest accretes, exactly as a zero- or low-cash-pay instrument would.

Second, the company keeps recognising the royalty as its own revenue. Ionis recognises SPINRAZA royalty revenue in the period the counterparty sells the product, and records the cash forwarded to Royalty Pharma as a reduction of the liability, not as a reduction of revenue. The income statement therefore grosses up: full royalty revenue at the top, a new imputed interest charge below.

Third, and the part that belongs to the accounting rather than the deal model, the effective interest rate is an output, not a contractual coupon. It is whatever rate equates the proceeds to the projected future cash flows, and the company is required to disclose it.

That makes it the one place where the true cost of the "non-dilutive" capital appears on the face of the financial statements, after the fact, in a number management cannot frame away. Ionis's 13.5 percent is the implied cost of its money, sitting in the notes for any analyst to read. The pre-deal question of whether that cost is worth paying against debt, converts, or equity is the subject of the CFO's guide; the point here is narrower and harder to argue with, which is that the accounting will eventually publish the answer.

The pattern repeats across the market. PTC classified its EVRYSDI proceeds as debt and carried a current "liability for sale of future royalties" of USD 194.3 million at the end of 2023, up from USD 72.1 million a year earlier, sitting in current liabilities alongside its convertible notes.

The KYNMOBI sale of future revenue was treated as debt financing under ASC 470 and amortised under the effective interest method over the estimated life of the royalty stream. The structure is the rule for operating-company monetisations, not the exception.

The Income Statement: The Gross-Up and the EBITDA Wedge

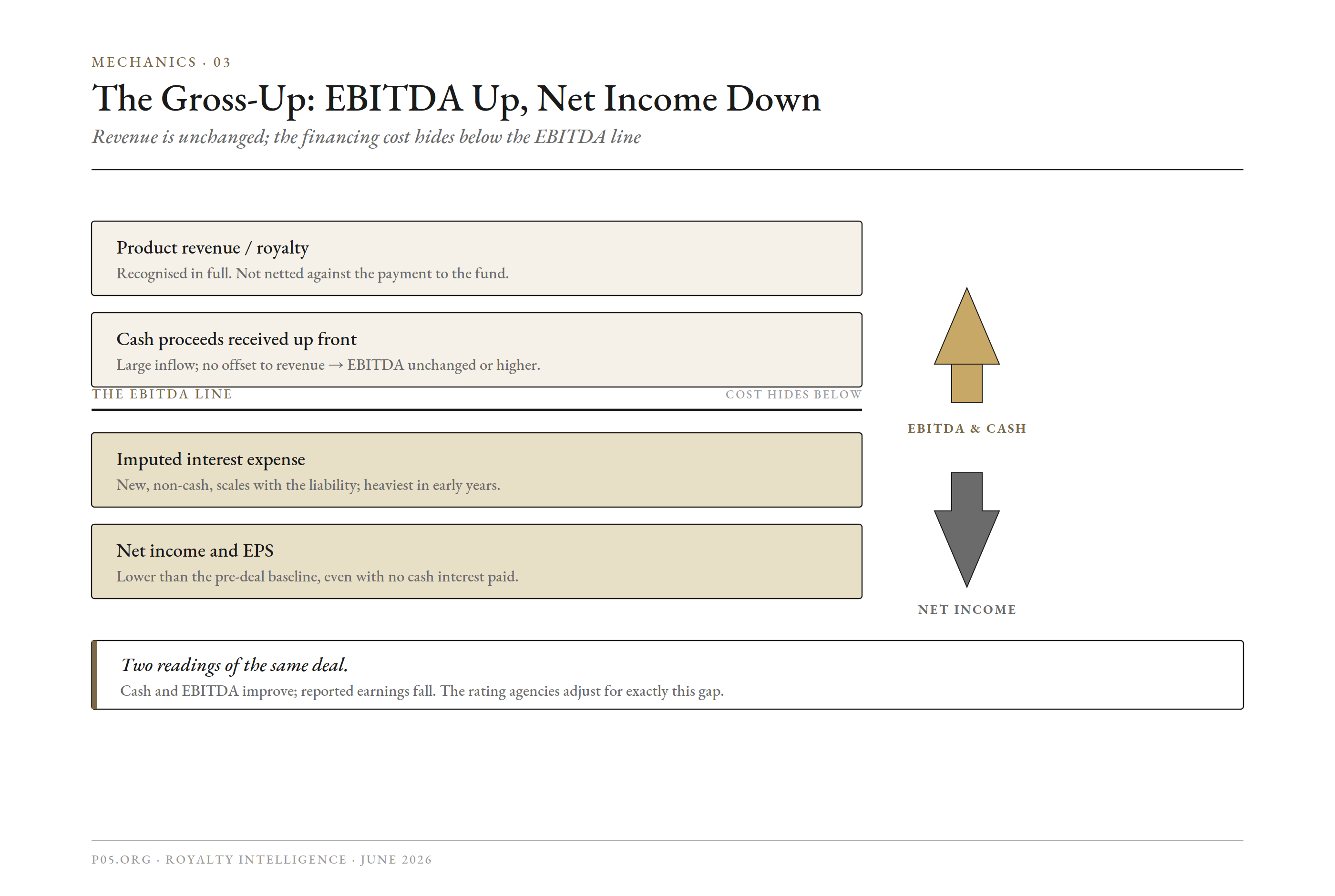

The income-statement consequence is the part that most often surprises a finance function that has heard "good for the accounts."

Under debt classification, the company continues to recognise its full product net sales, or its full third-party royalty, as revenue. It does not net the amount paid to the fund against revenue. Instead, each payment to the fund is split: the imputed-interest portion is interest expense, and the remainder reduces the carrying amount of the liability. Two effects then pull in opposite directions, and a board needs both in front of it.

Reported net income falls relative to the pre-deal baseline, because of the imputed interest charge, even though the company is not writing an interest cheque in the conventional sense. The charge is real for earnings per share, for any earnings-based covenant, and for management incentive metrics tied to net income.

EBITDA, by contrast, is usually flattered. Imputed interest sits below the EBITDA line. The company took in a large slug of cash, kept booking full revenue, and parked the financing cost in interest expense that EBITDA excludes. The wedge between the two readings is the whole problem.

Consider a stylised synthetic on a product generating USD 200 million of annual net sales, where the fund takes a 10 percent royalty and the deal carries an implied 12 percent effective rate on USD 300 million of proceeds.

| Line | Pre-deal | Post-deal (illustrative) | Effect |

|---|---|---|---|

| Product net sales | 200 | 200 | Unchanged: still the company's revenue |

| Royalty forwarded to fund (10% of sales) | 0 | (20) cash out | Split below into interest and principal |

| Of which imputed interest (≈12% of liability) | 0 | ≈(36) | Interest expense, below EBITDA |

| Of which liability reduction | 0 | the remainder | Financing, not P&L |

| EBITDA | unchanged | unchanged or higher | Cash in, cost excluded |

| Net income | baseline | lower | Imputed interest drags |

| Reported gross debt | baseline | unchanged on the face | But see leverage adjustments below |

The numbers are illustrative, but the direction is structural: cash and EBITDA up, net income down, and a liability the company now has to explain. In early years, when imputed interest exceeds the cash royalty forwarded, the liability accretes and the interest drag is at its heaviest.

The re-estimation regime makes the drag volatile. ASC 470-10 requires the company to revisit its forecast of future cash outflows each period and, when the amount or timing changes, to apply a prospective, catch-up, or retrospective approach.

A product that ramps faster or slower than modelled moves interest expense, sometimes through a single catch-up charge in the period of revision. The cash obligation scales gently with sales, which is the genuine attraction. The accounting charge does not.

The traditional sale that does achieve derecognition produces a different income statement. The asset leaves the books, future royalty income is no longer recognised, and the company books a gain or loss equal to proceeds less carrying amount.

Where the receivable was internally generated and carried at little or nothing, that gain can be large and immediate. This is the version that genuinely improves the reported result. It is also the version operating companies rarely achieve, for the reasons set out above.

The Cash Flow Statement

Classification follows the balance sheet. When the proceeds are debt, the upfront inflow is a financing activity. Subsequent payments to the fund split the same way they split in the P&L: the interest portion is an operating outflow, the principal portion a financing outflow. Non-cash imputed interest in excess of cash paid is added back in the operating-section reconciliation.

| Cash flow event | Classification under debt treatment |

|---|---|

| Upfront proceeds received | Financing inflow |

| Issuance costs paid | Financing outflow (netted against proceeds) |

| Interest portion of royalty forwarded | Operating outflow |

| Principal portion of royalty forwarded | Financing outflow |

| Non-cash imputed interest accretion | Added back in operating reconciliation |

The consequence is that operating cash flow is largely insulated from the financing itself, which is correct, while the headline "we raised USD X non-dilutively" lands in the financing section next to the term loans and notes, in exactly the company a credit analyst expects borrowings to keep.

The Rare Clean Sale, and Who Actually Achieves It

There is a version of monetisation that does come off the balance sheet and can book a gain. It requires selling a royalty the company already owns and transferring substantially all the risk and reward, no continuing involvement, no recourse, no cap with reversion, no minimum-return floor, no retained residual.

In practice the parties best positioned to deliver that clean transfer are not operating companies. They are non-operating royalty holders: foundations, universities, research hospitals, and individual inventors who hold a royalty but play no role in generating the underlying sales. The Cystic Fibrosis Foundation's USD 3.3 billion sale of its royalty interest in the Vertex CF franchise to Royalty Pharma in 2014 is the archetype.

A foundation has no continuing involvement in Vertex's commercialisation, no operations to entangle, and nothing to hand back, so the transfer is clean and the proceeds are sale consideration rather than a borrowing.

An operating company can occasionally reach the same place by selling 100 percent of a non-core legacy royalty tail outright, with no cap and no reversion, on an asset it out-licensed long ago and no longer touches. That is the configuration where derecognition and an immediate gain are most achievable, precisely because the company genuinely has nothing to do with generating the cash and can cleanly part with it.

The further a deal moves from that profile, toward retained upside, caps, options, and continuing operational involvement, the more certainly it becomes a liability.

The same downside-protection features that sellers negotiate hardest for, the cap that returns the upside, the minimum return, the reversion, are the features that defeat sale treatment. A controller cannot have both maximum downside protection and clean off-balance-sheet treatment. That trade-off, not a drafting nuance, is the real content of the structuring conversation.

What the Rating Agencies and Lenders See

Even where the accounting permits a liability that is not styled "debt," whether the financing constrains the company is decided outside the financial statements.

Rating agencies look through the presentation. Moody's standard analytical adjustments explicitly reclassify to debt those securitisations that a sponsor reports as sales but that do not fully transfer risk, and a royalty monetisation serviced out of the company's own cash flows is analytically the same animal. The adjustment is designed to strip out exactly the EBITDA flattery described above: the agency adds the monetisation liability back to adjusted debt and treats the imputed-interest-like cost as a financing charge, so adjusted leverage rises whether or not the face of the balance sheet calls the proceeds debt.

A controller who presents the board with an "off-credit" characterisation and is then surprised by the agency's adjusted-leverage treatment has skipped the diligence the pitch invited.

The existing lenders look through it too, but through the defined terms of the existing facilities. Whether a monetisation counts against a debt-incurrence covenant, a lien covenant, or a permitted-disposition basket is a question of how "Indebtedness," "Permitted Liens," and the relevant baskets are drafted in the company's credit agreement and indentures, not of how the transaction is booked.

This is why non-incurrence covenants, which stop the seller from layering additional secured debt onto product-related assets, appear in roughly 96 percent of synthetic royalty financings: the fund is protecting its revenue interest against precisely the leverage the company may not have realised it was taking on.

The honest summary is that "it does not count as debt" is true only as a statement about a particular line on a particular financial statement, and false as a statement about how the company's raters and creditors will treat it. The non-recourse, sales-scaling nature of the liability is a genuine difference from a term loan in a downside scenario. It is not a difference the leverage screens recognise on the upside.

The Large-Pharma Calculus Is Different

Most public examples of monetisation are emerging and mid-cap companies buying runway, because they are the ones for whom equity is expensive and traditional debt is unavailable or covenant-heavy.

A large pharmaceutical company with investment-grade access to the bond market is rarely monetising because it needs the cash, and its motivation changes the accounting that matters.

| Large-pharma motivation | Typical structure | Likely accounting outcome |

|---|---|---|

| P&L play: offset R&D spend with outside funding | Development / R&D funding, milestone-and-royalty contingent return | ASC 730-20 offset to R&D expense if risk is transferred; ASC 470 interest cost on any excess repayment obligation |

| Monetise a non-core legacy royalty tail | Outright sale of a third-party royalty, no cap, no reversion | Potential derecognition and gain on disposal |

| De-risk a single asset without divesting | Synthetic royalty on the company's own product | Liability, effective interest, EBITDA flatter and net-income drag |

The first row is where the "better accounting" claim can be literally true. As Goodwin has documented, big pharma is increasingly undertaking earlier-stage royalty and development-funding deals not for capital but as a profit-and-loss mechanism that uses third-party economics to offset its own R&D, with Teva and Biogen among recent participants. The relevant guidance sits at the intersection of ASC 730-20, "Research and Development Arrangements," and ASC 470-10. Where repayment is genuinely contingent on the success of the funded programme and risk has passed to the funder, the funding can offset R&D expense.

Where the company is expected to repay more than it received regardless of outcome, the excess is interest cost, and the arrangement is a financing in substance. The accounting benefit is real only in the configuration where real risk has actually moved.

The pattern across the three rows is that the transaction large pharma can most credibly present as "good accounting" is the legacy-tail disposal, while the deal most often pitched as a growth or de-risking tool is the synthetic, which is a liability with an interest drag. Same word, opposite balance-sheet outcome.

The strategic side of that de-risking choice, including how a synthetic royalty can deter or complicate an acquisition, is treated separately in royalty financing as defensive capital.

The Tax and Cross-Border Overlay

Book and tax classification need not agree, and the divergence is its own line of diligence. A monetisation treated as debt for book purposes may be a sale for tax, triggering a current tax charge on a gain the income statement never shows, or it may be a financing for tax as well, deferring the charge.

The mismatch generates deferred tax assets or liabilities that the controller has to track separately from the book liability, and the cash-tax timing can diverge sharply from the accounting.

Cross-border, the substance-over-form analysis is weighted differently by jurisdiction. Swiss, German, and French tax authorities place greater weight on economic substance than US authorities, and a structure that defers most of the payment to the back end of the deal life can attract scrutiny over whether the upfront was correctly characterised in the first place.

For a Swiss-domiciled group monetising a royalty on a product sold through US and EU subsidiaries, the characterisation can differ by jurisdiction within the same transaction, which is a coordination problem the insolvency and security analysis compounds rather than resolves.

What the Controller Should Actually Ask

The diligence reduces to a short set of questions, each of which moves the accounting before the lawyers begin drafting.

- Are we selling something we already own, or a slice of our own future sales? This decides whether derecognition is even available.

- What is our continuing involvement? If we keep making and selling the product, the ASC 470-10-25-2 presumption is debt and IFRS 9 points the same way.

- Is there a cap with reversion, a minimum-return guarantee, recourse, or a retained residual? Each of these keeps risk or reward with us and forces a liability. Ionis and PTC both landed on debt for exactly this reason.

- What is the implied effective interest rate? It is the true cost of this capital. Compare it to what senior debt would cost before calling it cheap.

- Will it produce a gain, no income, or an interest drag? Only a clean disposal of an owned receivable produces a gain. A synthetic lowers net income while flattering EBITDA.

- How will the rating agencies treat it? Assume the liability is added to adjusted debt and pre-clear it, rather than discover it at the next review.

- Does it trip a covenant? Check the defined "Indebtedness," the lien covenant, and the disposition baskets in every facility and indenture before signing.

- Do book and tax agree, and across which jurisdictions? Model the deferred tax and the cash-tax timing, and confirm the characterisation holds in each relevant country.

Selected Transactions and Their Accounting Outcomes

| Transaction | Year | What was sold | Structure feature | Accounting outcome |

|---|---|---|---|---|

| Ionis / SPINRAZA to Royalty Pharma | 2023 | Third-party royalty (from Biogen, Novartis) | Reversion after USD 475 to 550m collected | Liability, ASC 470, EIR ≈13.5% |

| PTC / EVRYSDI to Royalty Pharma | 2020, 2023 | Third-party royalty (from Roche) | Cap at USD 1.3bn, retained interest and options | Liability, classified as debt |

| KYNMOBI sale of future revenue | recent | Future product revenue | Sale of future revenue | Liability, ASC 470, effective interest |

| PhaseBio / SFJ development funding | 2020 | Contingent return on a Phase III asset | Five-times return, secured | Financing; recharacterisation litigated in bankruptcy |

| Cystic Fibrosis Foundation / Vertex CF franchise | 2014 | Owned royalty held by a non-operating foundation | Outright sale, no continuing involvement | Clean sale, off balance sheet |

| Royalty Pharma / Zymeworks Ziihera note | 2026 | Non-recourse note serviced by royalties | Royalty-backed note | Debt in form and substance |

The table makes the central point at a glance. The clean off-balance-sheet outcome belongs to the non-operating holder. The operating companies, including the two marquee sellers of clean third-party royalties, ended up with liabilities, because the features that protect a seller's economics are the features that keep the risk and reward, and the standards follow the risk and reward, not the name on the document.

The funds knocking on the door are not wrong that royalty financing is non-dilutive and can be a sensible source of capital. They are selling a real product. But "non-dilutive" is a statement about the equity, not about the balance sheet, and "good for the accounts" is true for one of these transactions and misleading for the others.

The controller's task is to determine which one is actually on the table, and the answer is visible in the first structural question, long before the term sheet reaches the audit committee.

All information in this article was accurate as of the research date and is derived from publicly available sources including accounting standards guidance, company SEC filings, rating agency methodology documents, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, accounting, tax, or financial advice. The author is not a lawyer, accountant, tax adviser, or financial adviser.