The Fulcrum Security in Pharmaceutical Royalty Financing: Locating the Value Break

The fulcrum security is the most senior class in a debtor's capital structure that does not recover in full under a plan of reorganization. Classes above it are paid in cash, reinstated, or cashed out at par.

The fulcrum security is the most senior class in a debtor's capital structure that does not recover in full under a plan of reorganization. Classes above it are paid in cash, reinstated, or cashed out at par. Classes below it receive minimal recovery (often a consensual gift to facilitate plan voting) or are wiped out.

The fulcrum class typically receives the bulk of the reorganized equity, and its holders therefore end up controlling the post-emergence company. Identification of this class is the central analytical task in any distressed pharmaceutical investment, and it is materially complicated when royalty financing instruments are part of the capital stack.

In pharmaceutical bankruptcies, the fulcrum question turns not only on enterprise value and debt seniority but also on which royalty interests are inside the bankruptcy estate, which are outside it, and how license agreements (the contractual basis for most royalty cash flows) are treated as executory contracts under Section 365 of the Bankruptcy Code. The treatment of these instruments determines both where the value breaks and what the resulting equity ownership looks like.

This article walks through the mechanics, applies them to a structured methodology for locating the fulcrum in royalty-financed pharma, and tests the framework against six recent Chapter 11 cases.

Mechanics: The Value-Break Analysis

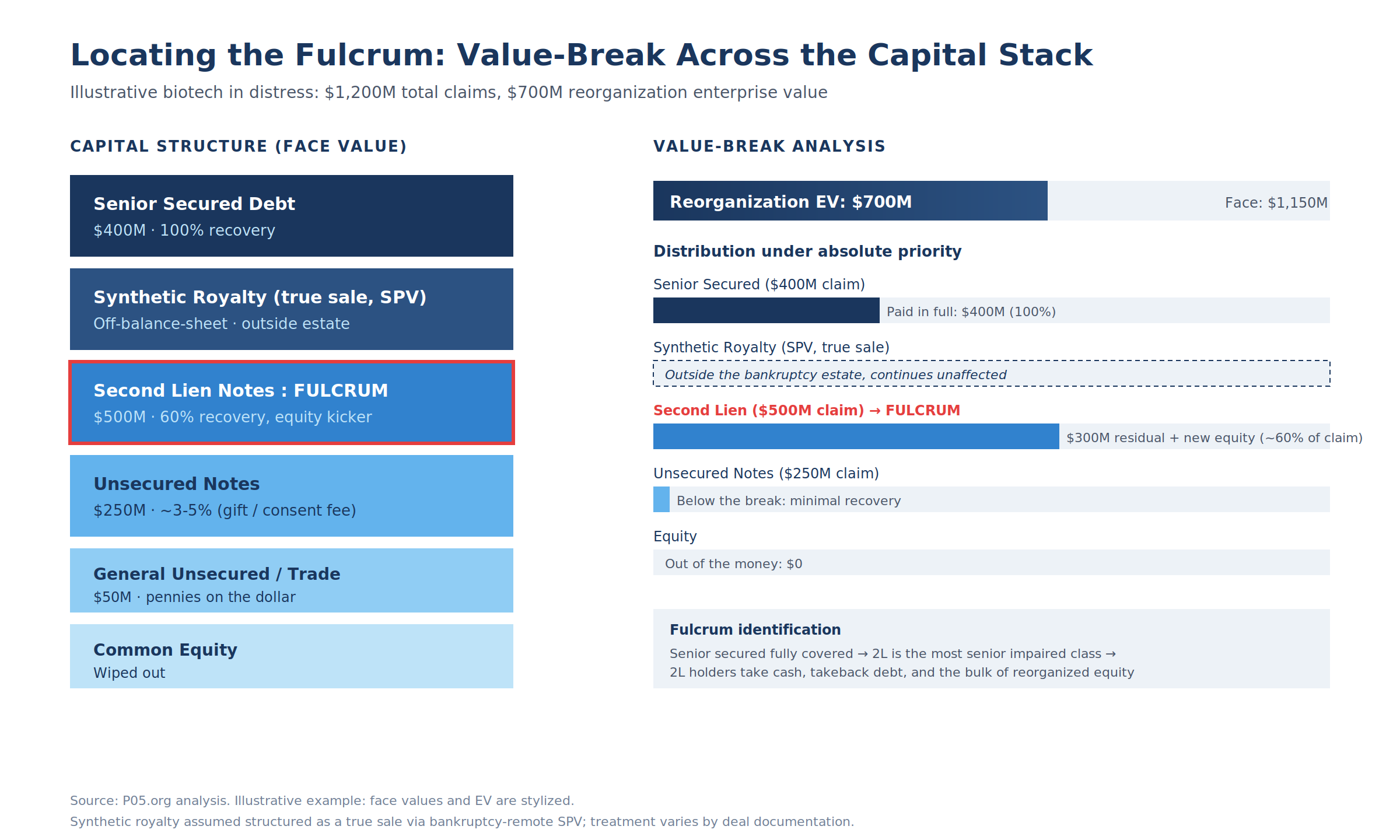

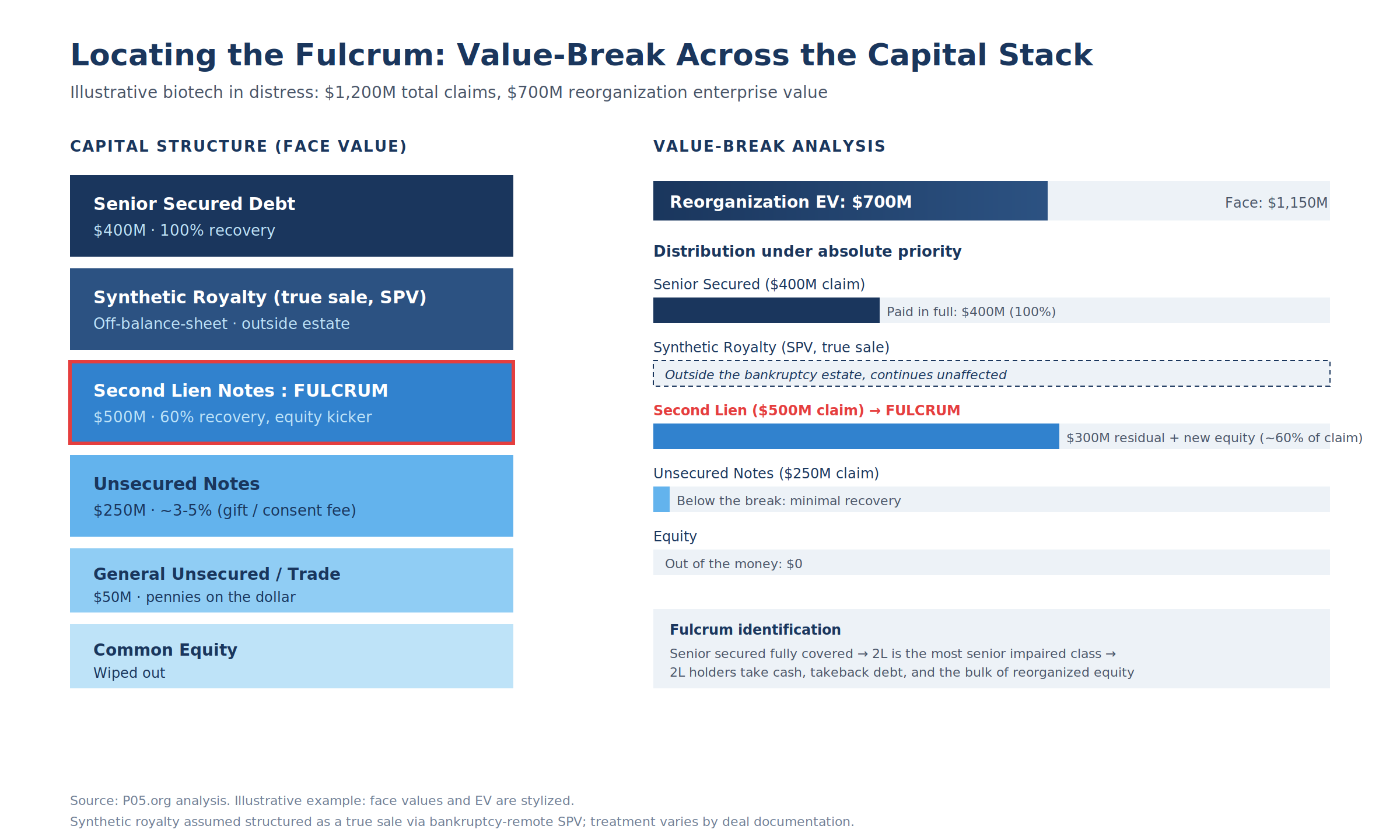

The fulcrum is identified by mapping reorganization enterprise value against the priority waterfall. Enterprise value is the total pool available to satisfy creditors. The waterfall allocates that pool in strict priority: administrative claims, secured claims, unsecured claims, and finally equity. The class where allocated value falls below the face amount of the claim is, by construction, the fulcrum.

Wall Street Prep frames this as the "value break": the point in the cap stack where remaining value reaches zero. Identifying it requires three things, as practitioners summarize: a defensible enterprise valuation, a complete capital structure map, and disciplined application of the waterfall.

In a classical industrial bankruptcy this analysis is straightforward. In pharmaceutical bankruptcies, two complications arise. First, the principal source of enterprise value is often a stream of contingent royalty payments that depend on commercial performance, patent integrity, and counterparty solvency. Second, royalty obligations and royalty receivables sit in different places relative to the estate depending on how the underlying transactions were structured.

The cramdown rules of Section 1129(b) and the absolute priority rule discipline this distribution. A plan can be confirmed over the objection of a dissenting impaired class only if no junior class receives any property under the plan. In practice, this is regularly relaxed via the gifting doctrine, where a senior class voluntarily allocates a portion of its recovery to a junior class to streamline voting, as analyzed by St. John's Center for Bankruptcy Studies.

Where Royalty Interests Sit Relative to the Fulcrum

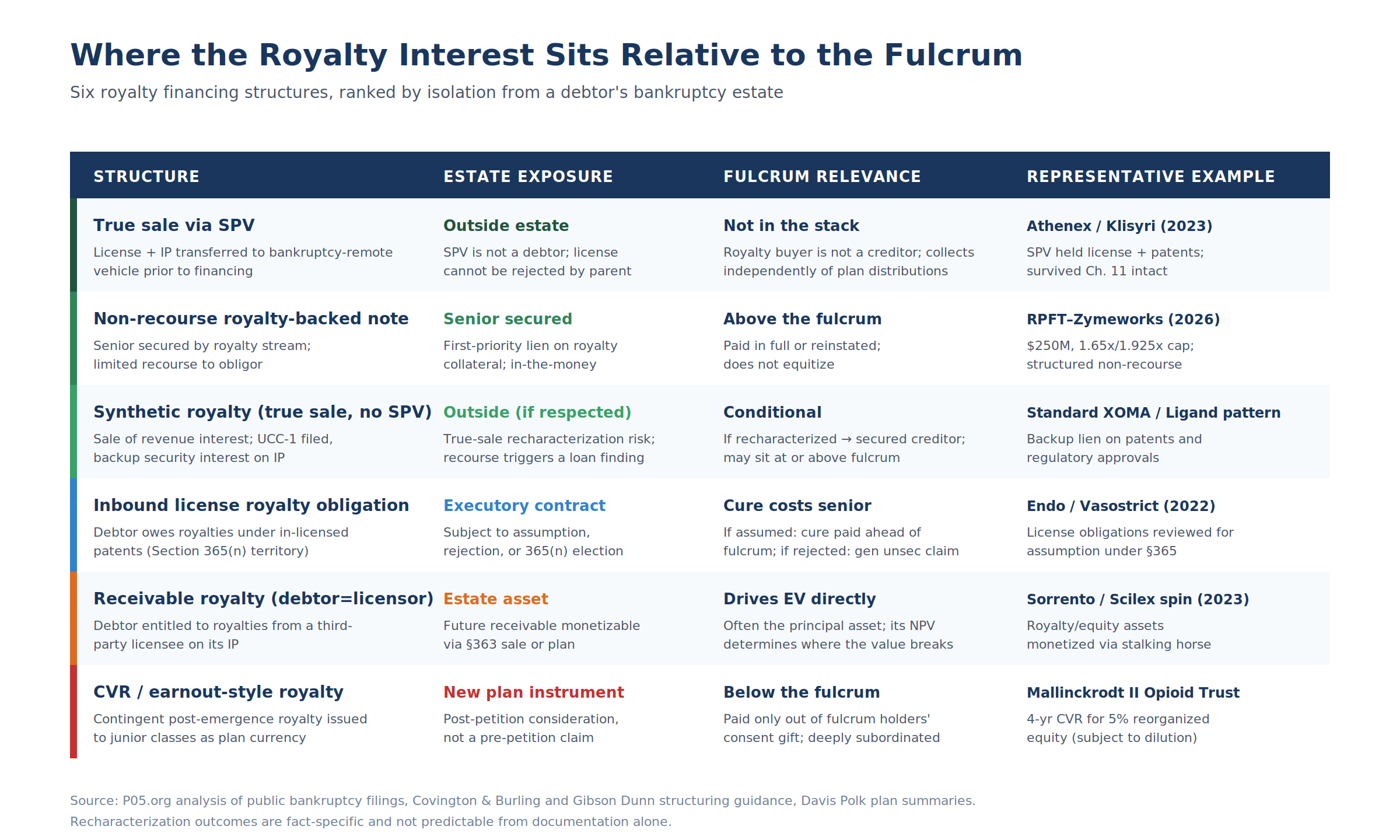

The position of a royalty interest in the priority waterfall is determined by the documentation, not by labels. Six structures recur across the pharmaceutical royalty market, each with a different relationship to the fulcrum.

True sale via bankruptcy-remote SPV

The cleanest structure isolates the royalty stream from the operating company entirely. The license agreement and underlying patents are transferred to a bankruptcy-remote SPV before the financing closes. The royalty buyer purchases its interest from the SPV, not from the operating company. If the operating company files for bankruptcy, the SPV is not a debtor, the license is not part of the estate, and rejection under Section 365 is unavailable to the parent.

The Athenex Klisyri financing (2022, $85 million from the Klisyri Purchasers) is the leading recent example. Athenex placed the license agreement and underlying patents into an SPV jointly owned with the buyers. When Athenex filed for Chapter 11 in May 2023 (Case No. 23-90295, S.D. Tex.), the Covington & Burling analysis confirmed that the SPV structure was validated: the license remained in effect and was not subject to rejection by the parent debtor. From a fulcrum perspective, the royalty buyer was simply not in the stack.

Non-recourse royalty-backed note

A royalty-backed note pledges the future royalty stream as collateral for senior secured debt. The lender holds a first-priority lien on the royalty stream and limited (or no) recourse to the broader estate. The Royalty Pharma–Zymeworks $250 million transaction (March 2026), structured with a 1.65x cap if achieved by end-2033 and 1.925x thereafter, is the recent reference structure. In a hypothetical Zymeworks insolvency, the noteholder sits at the top of the secured stack, above any fulcrum candidate.

Synthetic royalty (true sale, no SPV)

The most common structure in the synthetic royalty market is a true sale of a revenue interest without an SPV. The buyer files a UCC-1 to perfect the sale and typically takes a backup security interest in the underlying intellectual property and regulatory approvals, per Gibson Dunn's structuring guidance. The risk is recharacterization: if a bankruptcy court applies the eight-factor true-sale test and concludes the transaction was in substance a secured loan, the royalty asset comes back into the estate and the buyer holds a secured (or unsecured, if the backup lien is unperfected) claim. That recharacterization can shift the fulcrum.

Inbound license royalty obligation

Where the debtor is the licensee paying royalties to a third party, the license is an executory contract that the debtor may assume or reject. Assumption requires cure of all monetary defaults; rejection is treated as a pre-petition breach giving rise to an unsecured damages claim. If the licensee elects to continue using the licensed intellectual property after rejection under Section 365(n), it must continue to make royalty payments. Cure costs are administrative and rank ahead of the fulcrum; rejection damages rank below it.

Receivable royalty (debtor as licensor)

When the debtor is itself entitled to receive royalties from a third party, the receivable is an estate asset. Its present value is a major component of enterprise value, often the dominant component for late-stage clinical-stage biotechs whose only marketable assets are out-licensed programs. The location of the fulcrum is therefore highly sensitive to the assumptions used to value these receivables. The Sorrento Therapeutics bankruptcy (Case No. 23-90085, S.D. Tex.) is illustrative: the principal estate asset was Sorrento's equity in Scilex Holding Company, monetized through an Oramed-led $105 million stalking horse bid for Scilex stock and warrants.

CVR or earnout-style royalty

Plan currency itself can take the form of a contingent value right or earnout-style royalty, issued to junior or wiped-out classes as part of a plan of reorganization. These instruments are post-petition consideration, not pre-petition claims, and they sit below the fulcrum by construction. The Mallinckrodt II Opioid Trust CVR (a four-year contingent value right for 5% of reorganized equity, subject to dilution) is the canonical example.

Methodology: Locating the Fulcrum in Royalty-Financed Pharma

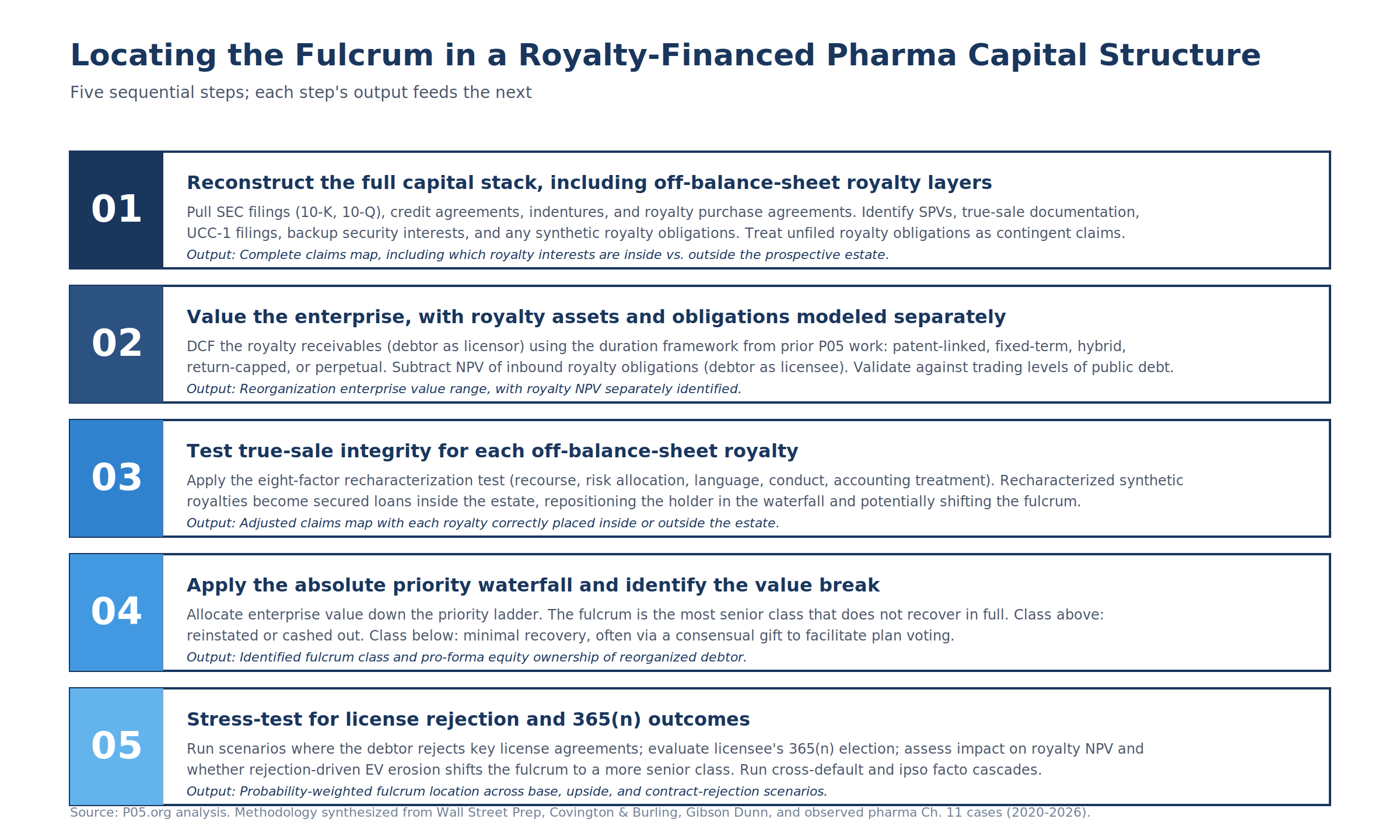

A defensible fulcrum analysis in this context proceeds in five steps.

Step 1: Reconstruct the full capital stack. Pull the latest 10-K and 10-Q, the credit agreement and indentures, and every royalty purchase agreement disclosed via Form 8-K or otherwise traceable through the SEC EDGAR system.

Identify SPVs (typically disclosed as wholly-owned or joint-venture financing subsidiaries), UCC-1 filings (searchable through Delaware, New York, and California secretary of state databases), backup security interests, and any obligations under in-licensing arrangements. Treat unfiled royalty obligations as contingent claims pending verification.

Step 2: Value the enterprise with royalties modeled separately. DCF the royalty receivables (debtor as licensor) using the duration framework laid out in the P05.org analysis on royalty stream expiry: patent-linked, fixed-term, hybrid "later of," return-capped, or perpetual. Subtract the NPV of inbound royalty obligations (debtor as licensee).

Validate the resulting enterprise value range against trading levels of the public debt: as practitioners note, bonds trading below 80 are pricing in recovery values, and the implied EV from the most junior in-the-money class is a useful triangulation point.

Step 3: Test true-sale integrity. For each off-balance-sheet royalty, apply the eight-factor recharacterization test: language in the documents, conduct of the parties, allocation of risk, recourse provisions, accounting treatment, presence of UCC-1 filings, structural separation via SPV, and any retained ownership rights. Hunton Andrews Kurth's analysis summarizes the factor weighting.

A recharacterized synthetic royalty becomes a secured loan inside the estate, repositioning the holder in the waterfall and potentially shifting the fulcrum to a more senior class than the unadjusted analysis suggested.

Step 4: Apply the waterfall. Allocate enterprise value down the priority ladder using the absolute priority rule. The fulcrum is the most senior class that does not recover in full. Document the gifting and consent dynamics that may modify strict priority distributions. In recent pharma cases, gifting to second lien or unsecured classes has ranged from minimal (Endo: 3.7% of equity to second lien deficiency and unsecured notes, plus $23.3 million cash) to material (Mallinckrodt II: 7.7% of equity to second lien holders).

Step 5: Stress-test for license rejection and Section 365(n) outcomes. Run scenarios in which the debtor rejects key license agreements. Evaluate whether the licensee will elect Section 365(n) treatment to preserve its rights (typically yes, if the IP is generating revenue, but as Covington & Burling note, a licensee may instead bid to purchase the IP outright, leaving the royalty buyer with an unsecured damages claim). Assess whether rejection-driven enterprise value erosion shifts the fulcrum to a more senior class.

Recent Pharmaceutical Cases

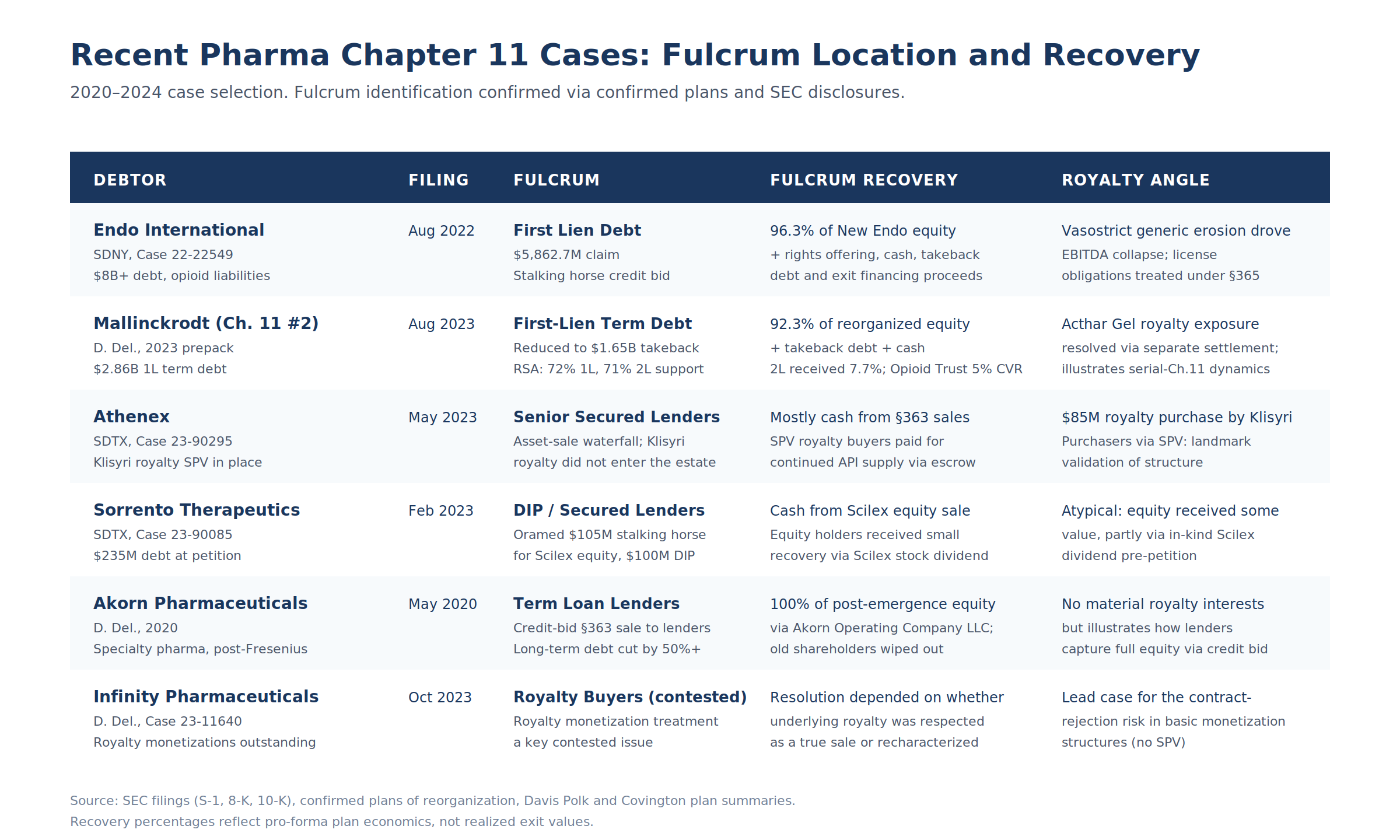

The methodology above predicts where the fulcrum will sit in any given pharma capital structure. The table below tests that prediction against six confirmed Chapter 11 cases from 2020 to 2024.

Endo International (Aug 2022)

Endo's prearranged Chapter 11 (Case No. 22-22549, S.D.N.Y.) was driven by approximately $8 billion of debt and thousands of opioid lawsuits. The plan, confirmed in March 2024, allocated 96.3% of the equity in Endo, Inc. (the new entity acquiring substantially all assets) to first lien creditors holding $5,862.7 million of claims.

Second lien deficiency claims and unsecured notes claims, totaling approximately $1,355.25 million, received the remaining 3.7% of equity, $23.3 million in cash, and certain litigation and insurance proceeds.

The fulcrum was unambiguously the first lien debt, executed via a credit-bid stalking horse structure. The case also illustrates the impact of generic erosion on the fulcrum location: the collapse of Vasostrict revenues following multiple generic launches in early 2022 reduced enterprise value sufficiently that the value break occurred at the senior secured layer rather than further down the stack.

Mallinckrodt (Aug 2023, second filing)

The Mallinckrodt II prepackaged Chapter 11 (D. Del., 2023) was supported by an RSA covering 72% of first lien debt and 71% of second lien debt. First lien term debt was reduced from $2.86 billion to $1.65 billion of takeback debt. Holders of first lien term debt received 92.3% of reorganized equity (subject to dilution), cash, and takeback debt. Second lien holders received 7.7% of reorganized equity.

The Opioid Master Disbursement Trust II received a $250 million prepetition lump-sum settlement and a four-year contingent value right for 5% of reorganized equity. The case is notable for two features relevant to royalty analysis: it was the second Chapter 11 filing by the same debtor (a pattern that creates serial-filing risk in royalty due diligence), and the Acthar Gel royalty exposure was resolved through a separate settlement structure rather than through the plan waterfall.

Athenex (May 2023)

Athenex's Chapter 11 (Case No. 23-90295, S.D. Tex.) is the most informative case for royalty financing structurers. The pre-petition Klisyri royalty financing had used the SPV structure described above, with the Klisyri Purchasers acquiring royalty rights through a bankruptcy-remote vehicle jointly owned with Athenex.

When Athenex filed, the license agreement and underlying patents were not part of the bankruptcy estate. The fulcrum analysis at the operating company level concerned the senior secured lenders, who recovered through Section 363 asset sales. The royalty financing operated independently.

The case validated the SPV structure but also exposed a residual risk: the supply agreement under which Athenex provided the active pharmaceutical ingredient to the licensee remained at the parent level and was a candidate for rejection. The parties resolved this through a negotiated settlement under which Athenex continued API supply for a transition period, funded in part by the Klisyri Purchasers.

Sorrento Therapeutics (Feb 2023)

Sorrento (Case No. 23-90085, S.D. Tex.) entered Chapter 11 with approximately $235 million of debt, exacerbated by adverse rulings in litigation against the Soon-Shiong entities. The fulcrum analysis was unusual because Sorrento's principal asset was its majority equity stake in publicly traded Scilex Holding Company. Oramed Pharmaceuticals provided $105 million of stalking horse stock-purchase commitment for Scilex equity and $100 million of debtor-in-possession financing. The DIP and secured lenders sat at the fulcrum.

Notably, equity holders received some recovery (atypically for biotech bankruptcy) via the Scilex stock dividend that had been distributed pre-petition, although Bloomberg Law reported that under the proposed asset sale plan, shareholders were expected to receive minimal additional value.

Akorn Pharmaceuticals (May 2020)

Akorn's Chapter 11 (D. Del., 2020) ended in a Section 363 credit-bid sale to its term loan lenders, who emerged owning 100% of the post-emergence equity through Akorn Operating Company LLC. Long-term debt was reduced by more than half.

The case has limited direct royalty financing implications (no material royalty interests were involved), but it cleanly illustrates the credit-bid mechanism that recurs in pharma bankruptcies: senior secured lenders convert their claims into equity through a sale process under Section 363(k), with junior creditors and shareholders wiped out.

Infinity Pharmaceuticals (Oct 2023)

Infinity Pharmaceuticals (Case No. 23-11640, D. Del.) is the lead case for the contract-rejection risk in basic royalty monetization structures (without an SPV). The treatment of the underlying royalty monetizations was a key contested issue, with resolution depending on whether the structures were respected as true sales or recharacterized as secured loans.

The case reinforces the structural lesson from Athenex: in the absence of bankruptcy-remote SPV isolation, royalty buyers face exposure to the licensor's bankruptcy estate, and their position in the waterfall depends on legal characterization rather than commercial intent.

Implications for Practitioners

Three points follow from the analysis.

First, the fulcrum analysis in royalty-financed pharma is not complete without a true-sale integrity review of every off-balance-sheet royalty in the structure. A royalty financing that the parties intended to be outside the estate may, on the facts, be inside it. The eight-factor test is fact-intensive, and the outcome can move the fulcrum by one or more classes.

Second, license agreements (whether the debtor is licensor or licensee) introduce executory-contract dynamics that have no analog in classical industrial bankruptcies. Section 365 assumption costs are administrative and rank ahead of the fulcrum. Section 365(n) elections preserve royalty cash flows but only at the licensee's option. Rejection damages rank below the fulcrum. These provisions create cash flow profiles that cannot be modeled by mechanical application of the priority waterfall.

Third, the structural choice between SPV and non-SPV royalty financings has direct fulcrum implications for both parties. For royalty buyers, the SPV adds documentation cost and complexity but provides the cleanest insulation from the licensor's insolvency, as confirmed by Athenex.

For licensors, the SPV restricts operational flexibility (the SPV cannot be repurposed as collateral for other financings) but lowers the financing cost by reducing the buyer's bankruptcy risk premium. The Endo, Mallinckrodt, and Akorn cases show that without an SPV, the royalty position in the waterfall is determined by the same priority rules that govern any other secured or unsecured claim.

The fulcrum security is the place where negotiating leverage concentrates in any restructuring. In pharmaceutical royalty financing, the question is not just where the value breaks, but which slice of that value sits inside the estate to be broken in the first place. Locating that slice precisely is the analytical work that defines the deal.

All information in this article was accurate as of the publication date and is derived from publicly available sources including SEC filings, confirmed plans of reorganization, court dockets, and law firm publications. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.