The Weekly Term Sheet (2026-W24)

The week in numbers

- $10.6B all-cash: GSK to acquire Nuvalent (Nasdaq: NUVL), a clinical-stage precision-oncology company, at $124.00 per share (about a 40% premium, roughly $9.4B net of Nuvalent's cash) via a tender offer for all Class A and Class B shares. The window's largest print by an order of magnitude and the second-largest deal in GSK's history; an equity acquisition of two near-commercial NSCLC inhibitors. GSK assumes Nuvalent's existing revenue-sharing arrangements: low-single-digit royalties payable to Royalty Pharma and Deerfield, a confirmed third-party royalty layer surviving the buyout.

- $1.25B upfront cash: Incyte to acquire Vega Therapeutics, the wholly owned Star Therapeutics subsidiary holding VGA039, a Phase 3 anti-Protein S antibody for von Willebrand disease. Ceiling up to $2.0B with sales milestones; an equity acquisition, no retained royalty.

- $1.0B cash: Johnson & Johnson to acquire Firefly Bio for the Firelink degrader-antibody-conjugate (DAC) platform in KRAS-driven solid tumours. All-cash, no disclosed milestones or retained royalty; closing targeted later in 2026.

- $700M upfront cash: Roche to Nurix Therapeutics for bexobrutideg (NX-5948), a BTK degrader, in a co-development and co-commercialisation collaboration across haematology, immunology, and neurology. Ceiling up to $2.3B with milestones, plus low- to high-teens tiered royalties to Nurix on ex-US net sales and a 50/50 US profit split. The window's lead royalty-bearing print.

- $670M IPO plus $75M Regeneron private placement (~$745M total): Parabilis Medicines priced an upsized, above-range Nasdaq IPO (PBLS), the largest ever for a venture-backed biotech, with a concurrent Regeneron private placement tied to a separate, undisclosed research collaboration. A primary equity print, no royalty origination; the Regeneron collaboration is a partnering watch item.

- ~$2.5B equity value, $900M+ combined cash: Treeline Biosciences to go public via an all-stock merger with Standard BioTools (Nasdaq: LAB), a reverse merger that lists the Bilenker / Engelman oncology company as Treeline Biosciences (ticker TRLN). Pre-merger Standard BioTools holders receive a CVR on legacy diagnostics monetisation plus an Illumina / SomaLogic earnout; Treeline's lead EZH2 inhibitor TLN-254 carries a 10 to 12.5% royalty to Hengrui.

- Up to CHF 250M committed, CHF 150M first tranche: Pharmakon Advisors (BioPharma Credit) to Idorsia, a senior secured term loan with a 5-year maturity at a fixed 7% rate, the window's only structured-finance print from a royalty- and credit-finance house on the watchlist. The first tranche refinances Idorsia's existing New Money Facility (CHF 105M drawn, due May 2027) and extends runway into 2028. Non-dilutive debt rather than a royalty monetisation.

- $135M equity plus up to $165M from Hercules Capital (including $55M royalty financing): Beren Therapeutics raised about $300M combined to fund commercial readiness for adrabetadex, a cyclodextrin therapy for infantile-onset Niemann-Pick disease type C (I-NPC), ahead of a November 17, 2026 PDUFA date. The Hercules tranche pairs senior secured debt with a $55M royalty-financing sleeve, the window's only explicit royalty layer and its second structured-finance print after Idorsia / Pharmakon.

- $175M Series E: Samsung Electronics invested $175M in Element Biosciences, a DNA-sequencing and life-science-tools company. A tools and instrumentation financing, not a therapeutic royalty event.

- $125M Series B: SonoThera closed an oversubscribed round to take its ultrasound-mediated nonviral genetic-medicine platform (RIPPLE / PORE) into the clinic in DMD and ADPKD. The window's largest venture round; a clean raise, no royalty layer.

- $99.5M committed: City Therapeutics Series B, to advance its next-generation extrahepatic RNAi platform (cityRNAs activating Argonaute-3), led by CITY-FXI in Phase 1. A clean equity raise; City is an inbound-royalty recipient on its Biogen and Bausch + Lomb out-licenses.

- $32M upfront, up to $64M total, no retained royalty: Adial Pharmaceuticals (Nasdaq: ADIL) acquired Azora Therapeutics in a stock-for-stock merger handing Azora's former equityholders majority ownership, alongside a concurrent private placement of up to $64M (about $32M upfront via pre-funded warrants at $2.7489, including conversion of assumed notes, plus up to $32M on Phase 1 initiation). Adds AT177, a colon-targeted AhR agonist for ulcerative colitis. A micro-cap reverse takeover plus PIPE, no royalty layer.

- $40M upfront, up to $1.4B ceiling, tiered royalties to Orionis: Orionis Biosciences to Novartis, a renewed and expanded multi-year molecular glue discovery collaboration using Orionis's Allo-Glue platform and AI discovery engine. Tiered royalties to Orionis on net sales of collaboration products. A privately held originator royalty in the making against a large-cap.

- $10M upfront, up to $527M total, tiered single- to double-digit royalties plus a high-teens equity option: Laekna to Vasque Bio for ex-Greater-China rights to LAE118, a PI3K-alpha pan-mutant-selective inhibitor. Up to $517M in development and sales milestones, tiered royalties, and Laekna's right to acquire up to a high-teens percentage of Vasque's stock at no extra cost (or cash in lieu). A China-outbound originator royalty with an equity kicker, extending the W23 Asia-outbound theme.

- $10M upfront, >$1B ceiling excluding royalties: AlzeCure Pharma to out-license global rights to ACD680, a gamma-secretase modulator for Alzheimer's disease, to Eli Lilly, with mid-single-digit royalties to AlzeCure on product sales. A sub-scale Swedish originator royalty; subject to Swedish foreign direct investment screening.

- EUR 7M for a 30.4% stake, no royalty: Shilpa Biocare (a Shilpa Medicare subsidiary, BSE/NSE: SHILPAMED) took a 30.4% equity stake in Barcelona-based Gate2Brain for EUR 7M (EUR 0.5M cash, EUR 5.5M in equity for services, EUR 1M project development) and became CMC, manufacturing, and regulatory partner for G2B-002, a MiniAp4 peptide shuttle delivering SN-38 across the blood-brain barrier in pediatric DIPG and pGBM (US FDA and EMA orphan drug). A strategic equity-and-services investment, no royalty layer.

- $2M upfront, quarterly royalties to ExCellThera plus milestones: Medexus to license exclusive Canadian commercialisation rights to UM171 Cell Therapy (Zemcelpro / dorocubicel) from ExCellThera and its subsidiary Cordex Biologics. A small regional commercial royalty accruing to the Canadian originator on a conditionally EU-approved cell therapy, with Cordex supplying on a cost-plus basis.

- Up to GBP 44.5M upfront and near-term, GBP 118M per target in milestones: Engitix to GSK, a research collaboration and option agreement on liver fibrosis regression targets, carrying tiered low-single-digit royalties to Engitix on future product sales. A UK originator platform royalty, earlier-stage and per-target.

- ~SEK 124M rights issue plus up to SEK 75M venture loan: Cantargia, a Lund-based IL1RAP oncology company, opened a rights issue (June 8 to 22) alongside a Fenja Capital loan facility, up to ~SEK 199M combined, to fund a nadunolimab plus daraxonrasib Phase Ib in pancreatic cancer and a hematology programme. A dilutive raise with a venture-debt sleeve, no royalty origination.

- ~NOK 300M (USD ~32M) gross: Circio Holding (OSE: CRNA) completed a warrant-exercise programme plus an underwritten private placement, taking H1 2026 proceeds to ~NOK 620M (USD ~65M) to fund the circVec circular-RNA platform to clinical proof of concept. A clean equity print, no royalty layer.

- US$36.5M (C$50M), royalty-retiring: PharmaEssentia (TWSE: 6446) closed its acquisition of 100% of FORUS Therapeutics, its Canadian BESREMi (ropeginterferon alfa-2b) licensee. Agreed April 9 and completed June 11; only the closing falls in-window. The buy-in collapses an existing downstream royalty: under the October 2024 Canada license FORUS owed PharmaEssentia double-digit percentage royalties on BESREMi net sales plus up to $107M in milestones. A third-party royalty converted into wholly owned commercial economics, the inverse of an origination.

- Undisclosed terms, Lonza platform royalty model: AmMax Bio to license Lonza's GlycoConnect, HydraSpace, and exatecan-based SYNtecan linker-payload technologies (non-exclusive) for AMB-104, an ADC in venetoclax / azacitidine-resistant AML. Terms not disclosed; Lonza's near-identical Stipple Bio license (June 4) carried upfront, milestone, and net-sales royalty terms to Lonza, marking a Basel CDMO platform-royalty model.

- Undisclosed terms, upfront and milestones to WestGene: Cartesian Therapeutics to license WestGene Biopharma's targeted LNP platform, pairing it with Cartesian's Descartes-08 mRNA payload for in-vivo mRNA CAR-T in autoimmune disease. No royalty disclosed.

- Undisclosed terms: GENESIS Pharma to expand its commercialisation of Alnylam's RNAi therapeutics into four Nordic markets. A regional distribution expansion, no disclosed royalty origination.

- Undisclosed terms, no royalty: Verge Labs (formerly Verge Genomics; San Francisco) and China-based, Bain Capital-backed Tenacia Biotechnology formed a strategic platform partnership applying Verge's multimodal human brain-tissue AI platform to prioritise targets across Tenacia's CNS pipeline. The first deal under Verge's May 2026 platform-first model. A data-and-AI collaboration, no royalty layer.

- Undisclosed terms, no royalty: Syntax Bio (Chicago) and Mayo Clinic formed an R&D collaboration to develop an allogeneic, iPSC-derived pancreatic beta-cell therapy for type 1 diabetes using Syntax's CRISPR-based Cellgorithm platform; Mayo provides pancreatic biology and preclinical functional testing and holds a financial interest. A research collaboration, no royalty layer.

- Undisclosed terms: Galmed Pharmaceuticals to acquire Colospan for the CG-100 intraluminal bypass device in colorectal anastomotic protection. A GI medtech pivot, terms not disclosed, no royalty layer.

- Undisclosed terms, royalties to BioNTech: BioNTech's planned separation from founders Ugur Sahin and Ozlem Tureci (Handelsblatt, June 8) would carve early-stage CAR-T and RiboMAB mRNA programmes into a new founder-led company, in exchange for a minority stake plus milestones and royalties to BioNTech and a RiboMAB license-back option. The Pfizer / Comirnaty profit split stays at BioNTech.

- Survodutide Phase 3 re-rate, no new capital: Boehringer Ingelheim and Zealand Pharma presented SYNCHRONIZE-1 (obesity) and SYNCHRONIZE-MASLD Phase 3 data at ADA 2026 (Sun June 7), published in NEJM and Nature Medicine. Up to a 16.6% average weight loss at 76 weeks; re-rates Zealand's high-single-digit to low-double-digit royalty plus up to EUR 315M in outstanding milestones.

- Elecoglipron Phase 2b re-rate, no new capital: AstraZeneca presented positive VISTA (obesity) and SOLSTICE (type 2 diabetes) Phase 2b data on elecoglipron (AZD5004 / ECC5004), supporting global Phase 3 initiation. Re-rates Eccogene's tiered royalty plus up to ~$1.825B in outstanding milestones on AstraZeneca's ex-China net sales.

- Anbenitamab Phase 3 breast cancer topline, no new capital: Alphamab Oncology's anbenitamab (KN026), co-developed with CSPC subsidiary JMT-Bio, read out positive Phase 3 breast cancer data with CSPC's albumin-bound docetaxel (HB1801). A China-domestic co-development with no disclosed tradable third-party royalty held by an independent originator.

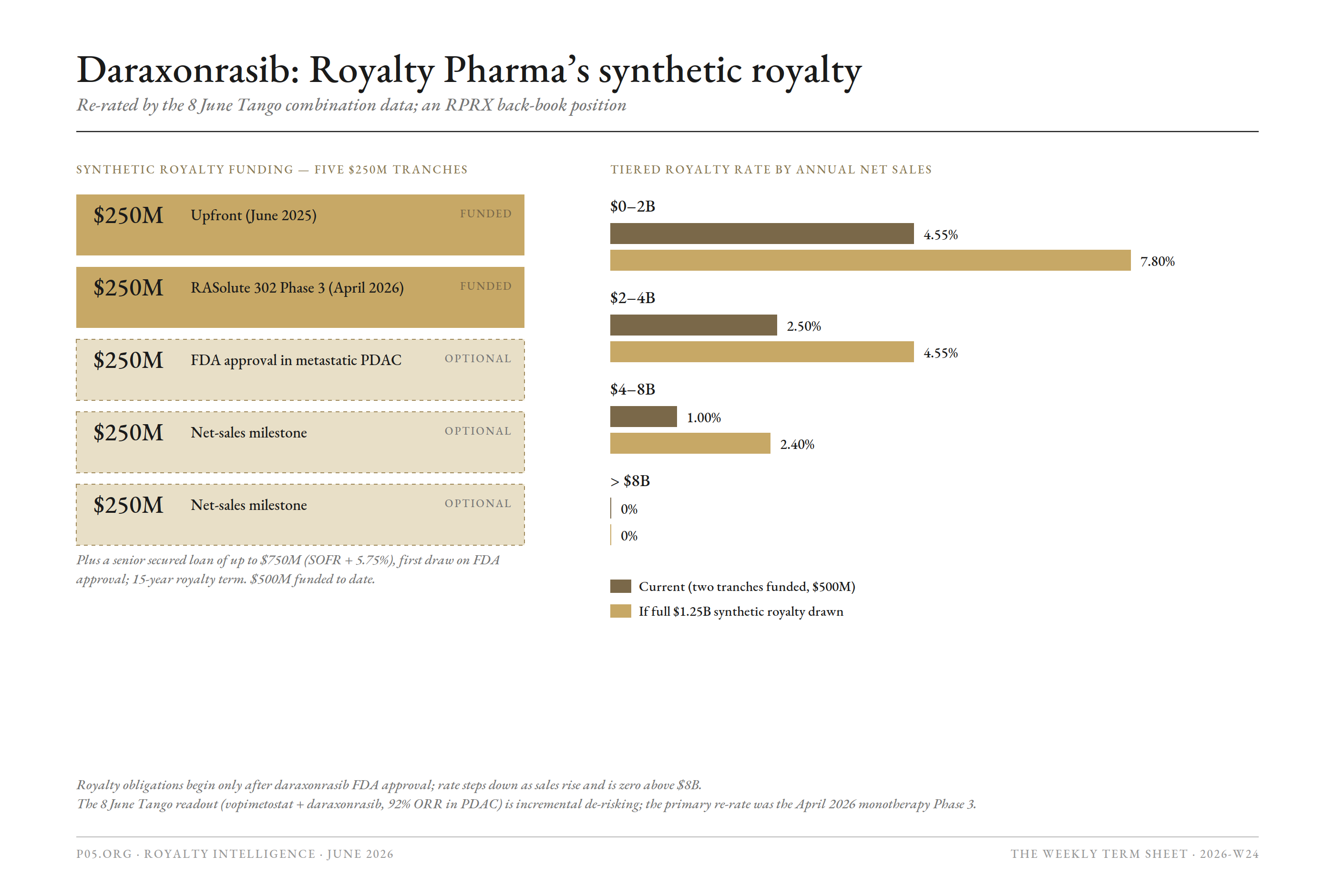

- Vopimetostat plus daraxonrasib PDAC re-rate, no new capital: Tango Therapeutics (Nasdaq: TNGX) reported initial Phase 1/2 data for its PRMT5 inhibitor vopimetostat combined with Revolution Medicines' RAS(ON) inhibitor daraxonrasib in MTAP-deleted, RAS-mutant metastatic PDAC: a 92% objective response rate (11 of 12 response-evaluable patients, 9 of 11 confirmed) and a 90% six-month PFS rate, supporting Phase 3 in first-line disease. Incremental de-risking of the commercial base behind Royalty Pharma's up to $1.25B synthetic royalty plus up to $750M senior secured loan on daraxonrasib (June 2025); the primary daraxonrasib re-rate was the April 2026 RASolute 302 monotherapy Phase 3, which triggered the second $250M royalty tranche. An RPRX back-book position, not a new origination.

- Zasocitinib Phase 3 head-to-head win, no new capital: Takeda (NYSE: TAK) reported LATITUDE Atlas topline data showing zasocitinib (TAK-279) statistically superior to deucravacitinib on PASI 100 at week 16 in moderate-to-severe plaque psoriasis (more than 35% complete skin clearance, more than 2.5 times the comparator). Advances the oral TYK2 inhibitor Takeda acquired from Nimbus Therapeutics in 2022; Nimbus holds up to $2B in contingent sales milestones (two $1B tranches at $4B and $5B in annual net sales), not a running royalty.

- Bondholder restructuring, no new external capital: Magle Chemoswed (Magle Group) reached agreement in principle on key restructuring terms with an ad hoc group holding ~70% of its SEK 350M senior secured bonds (June 11), a debt-for-control workout under which bondholders may take control. A distressed restructuring, no royalty content.

- Fund first close, size undisclosed: Star51 Capital held the first close of its inaugural medtech-and-AI "ecosystem" venture fund, anchored by Abbott and Mayo Clinic with a roster of medtech-operator LPs (June 11). A supply-side capital-formation event, not a deal; relevant as a read on dedicated medtech / device capital, in CFC's device scope but not a royalty origination.

- Clinical and regulatory prints, no royalty layer: Sanofi's anti-C1s antibody SAR445088 Phase 3 in CIDP discontinued for lack of efficacy (June 10); FDA RMAT for a CD22-targeting allogeneic CAR-T (lasme-cel) in r/r B-ALL (June 9); FDA orphan drug designation for Tris Pharma's once-nightly oxybate TRN-257 in idiopathic hypersomnia (June 10); FDA Complete Response Letter to Camurus for CAM2029 (Oclaiz) in acromegaly (June 10), tied to a third-party manufacturer's cGMP observations rather than efficacy or safety.

M&A and major licensing:

- GSK / Nuvalent acquisition (Tue June 9): $10.6B all-cash tender offer at $124.00 per share (about a 40% premium, ~$9.4B net of cash) for clinical-stage precision-oncology company Nuvalent and its two near-commercial NSCLC inhibitors, zidesamtinib (ROS1) and neladalkib (ALK); GSK's third 2026 buyout under CEO Luke Miels and the second-largest deal in its history. An equity acquisition; GSK assumes Nuvalent's existing low-single-digit royalties payable to Royalty Pharma and Deerfield (see M&A and Restructuring)

- Incyte / Vega Therapeutics (Star Therapeutics) acquisition (Mon June 8): $1.25B upfront, up to $2.0B with sales milestones; an equity acquisition of the Star subsidiary holding VGA039, no retained royalty; closing targeted Q3 2026 subject to HSR clearance (see M&A and Restructuring)

- Roche / Nurix Therapeutics bexobrutideg collaboration (Mon June 8): $700M upfront, up to $2.3B with milestones, plus low- to high-teens tiered royalties to Nurix on ex-US net sales; 60/40 Roche/Nurix development cost share and a 50/50 US profit split (see BD Origination and Licensing)

- Johnson & Johnson / Firefly Bio acquisition (Mon June 8): $1.0B all-cash acquisition of the Firelink degrader-antibody-conjugate (DAC) platform targeting KRAS-driven solid tumours; preclinical-stage, no disclosed milestones or retained royalty (see M&A and Restructuring)

- Galmed Pharmaceuticals / Colospan acquisition (Mon June 8): definitive agreement for the CG-100 intraluminal bypass device in colorectal anastomotic protection; terms undisclosed, a GI medtech pivot, no royalty layer (see M&A and Restructuring)

- Treeline Biosciences / Standard BioTools reverse merger (Mon June 8): all-stock merger taking private oncology company Treeline public via Standard BioTools (Nasdaq: LAB); ~$2.5B Treeline equity value, $900M+ combined cash; CVR to pre-merger holders plus an Illumina / SomaLogic earnout; lead EZH2 inhibitor TLN-254 in-licensed from Hengrui (10 to 12.5% royalty) (see M&A and Restructuring)

- BioNTech / founders mRNA carve-out and separation (Handelsblatt Mon June 8): planned transfer of BioNTech's early-stage CAR-T and RiboMAB programmes to a new founder-led company, in exchange for a minority stake plus milestones and royalties to BioNTech and a RiboMAB license-back option; binding agreement targeted end of H1 2026 (see M&A and Restructuring)

- Magle Group bondholder restructuring (Thu June 11): agreement in principle on key restructuring terms with an ad hoc group holding ~70% of Magle Chemoswed's SEK 350M senior secured bonds; a debt-for-control workout under which bondholders may take control. A distressed restructuring, no royalty content (see M&A and Restructuring)

- PharmaEssentia / FORUS Therapeutics acquisition (closed Thu June 11; agreed April 9): US$36.5M (C$50M) acquisition of 100% of FORUS, PharmaEssentia's Canadian BESREMi licensee since October 2024. Retires FORUS's downstream royalty: under the Oct 2024 Canada license FORUS owed PharmaEssentia double-digit percentage royalties on BESREMi net sales plus up to $107M in milestones, now folded into wholly owned economics. A royalty-eliminating in-licensee buy-in, not a new origination (see M&A and Restructuring)

- Adial Pharmaceuticals / Azora Therapeutics acquisition and financing (Thu June 11): all-stock acquisition of Azora Therapeutics (lead AT177, a colon-targeted AhR agonist for ulcerative colitis), with Azora's former equityholders taking majority ownership, alongside a concurrent private placement of up to $64M (about $32M upfront via pre-funded warrants at $2.7489 including conversion of assumed notes, and up to $32M on Phase 1 initiation). A micro-cap reverse takeover with a PIPE, no retained third-party royalty; Lucid Capital Markets acted as placement agent (see M&A and Restructuring)

Royalty-bearing license-outs and platform layers (upfront + milestones + tiered royalties):

- Roche / Nurix bexobrutideg (Mon June 8): Nurix (San Francisco) grants Roche co-development and ex-US commercialisation rights to the BTK degrader bexobrutideg, retaining low- to high-teens tiered royalties on Roche's ex-US net sales alongside a 50/50 US profit split and a 40% development cost share. The royalty is the tradable piece (see BD Origination and Licensing)

- Orionis Biosciences / Novartis molecular glue collaboration (Tue June 10): $40M upfront, up to $1.4B in milestones, plus tiered royalties to Orionis on net sales of collaboration products. A renewal and expansion of the 2020 pact, deploying Orionis's Allo-Glue platform; the royalty accrues to a privately held, clinical-stage originator (see BD Origination and Licensing)

- Laekna / Vasque Bio LAE118 ex-China out-licence (Tue June 9): $10M non-refundable upfront, up to $517M in milestones (up to $527M total), tiered single- to double-digit royalties, plus Laekna's right to acquire up to a high-teens percentage of Vasque Bio common stock at no extra cost. A China-outbound originator royalty plus equity kicker (see BD Origination and Licensing)

- AlzeCure Pharma / Eli Lilly ACD680 (Tue June 9): AlzeCure (Sweden) grants Lilly global rights to the gamma-secretase modulator ACD680 for $10M upfront, milestones exceeding $1B excluding royalties, and mid-single-digit royalties; subject to Swedish FDI screening. A clean small-originator stream (see BD Origination and Licensing)

- Medexus / ExCellThera + Cordex Zemcelpro Canada license and supply (Tue June 9): $2M upfront, quarterly royalties to ExCellThera on Canadian net sales, and one-time milestones, with Cordex managing the Phase 3 trial and supplying on a cost-plus basis. A royalty-bearing in-licence of a conditionally EU-approved cell therapy (see BD Origination and Licensing)

- Engitix / GSK liver fibrosis collaboration (Mon June 8): up to GBP 44.5M upfront and near-term, up to GBP 118M per target in milestones, and tiered low-single-digit royalties to Engitix; GSK holds the option to license. An earlier-stage, per-target platform royalty (see BD Origination and Licensing)

- AmMax Bio / Lonza ADC linker-payload license (Tue June 9): non-exclusive access to Lonza's GlycoConnect, HydraSpace, and SYNtecan linker-payload technologies for AMB-104. Terms undisclosed; Lonza's near-identical Stipple Bio license one week earlier carried net-sales royalties to Lonza, indicating a CDMO platform-royalty model from a Basel licensor (see BD Origination and Licensing)

Structured finance and non-dilutive debt:

- Pharmakon Advisors (BioPharma Credit) / Idorsia senior secured term loan (Tue June 9): up to CHF 250M, 5-year maturity, fixed 7% rate; first tranche CHF 150M at closing, refinancing the existing New Money Facility and extending runway into 2028. Senior secured debt rather than a royalty monetisation, the window's one structured-finance print from a watchlist house (see Structured Finance and Non-Dilutive Debt)

- Beren Therapeutics / Hercules Capital $300M equity and royalty-backed financing (Wed June 10): $135M equity (Wellington Partners, JIC VGI, Founders Fund, Narya Capital, Eisai, others) plus up to $165M from Hercules Capital, structured as senior secured debt and $55M of royalty financing, to fund commercial readiness for adrabetadex (I-NPC) ahead of a Nov 17, 2026 PDUFA date. The royalty-financing sleeve is the tradable piece and the window's only pre-commercial royalty layer (see Structured Finance and Non-Dilutive Debt)

Financings (no royalty origination today):

- Parabilis Medicines $670M IPO plus $75M Regeneron private placement (priced Tue June 9, trading Wed June 10): 33.5M shares at $20 (above range), $670M gross, plus a 5.025M-share overallotment (up to ~$770M); a concurrent Regeneron placement of ~4.17M shares at $18, ~$75M, tied to a separate research collaboration. The largest IPO in venture-backed biotech history; funds the Helicon peptide platform and lead Wnt / beta-catenin inhibitor zolucatide. The Regeneron collaboration is an undisclosed-terms watch item (see Financings)

- SonoThera $125M Series B (Wed June 10): oversubscribed round led by Vida Ventures with ARK Invest, CureDuchenne Ventures, Leaps by Bayer, Otsuka, SymBiosis, UCB Ventures, Vivo Capital, and existing backers, to take the RIPPLE / PORE platform into the clinic in DMD and ADPKD. The window's largest venture round (see Financings)

- City Therapeutics $99.5M Series B (Mon June 8): co-led by Viking Global and Sofinnova with Casdin, NYBC Ventures, and existing backers, to advance the extrahepatic RNAi platform (cityRNAs / Argonaute-3) led by CITY-FXI in Phase 1. City is an inbound-royalty recipient on its Biogen and Bausch + Lomb out-licenses (see Financings)

- Element Biosciences $175M Series E (Samsung Electronics) (Tue June 9): Samsung Electronics invested $175M in the DNA-sequencing and life-science-tools company. A tools and instrumentation financing, not a therapeutic royalty event (see Financings)

- Cantargia ~SEK 124M rights issue plus up to SEK 75M Fenja Capital loan (subscription June 8 to 22): up to ~SEK 199M combined, ~60% covered by commitments (DNB Bank guaranteeing SEK 72.6M), to fund a nadunolimab plus daraxonrasib Phase Ib in pancreatic cancer. A dilutive raise with a venture-debt sleeve (see Financings)

- Circio Holding ~NOK 300M warrant exercise and private placement (Tue June 9): NOK 300M gross (NOK 213M from warrant exercises, NOK 87M from an underwriting commitment), taking H1 2026 proceeds to ~NOK 620M (USD ~65M) to advance the circVec circular-RNA platform to clinical proof of concept. A clean equity print, no royalty layer (see Financings)

- VERAXA Biotech / Voyager Acquisition Corp Nasdaq debut (closing June 10, trading June 11): completion of the de-SPAC (business combination agreement dated April 22, 2025) for the Heidelberg and Zurich ADC and BiTAC T-cell-engager developer; trades as VRXA (warrants VRXAW). Supported by a $27.5M senior secured note (issued at 87.5% of par, ~$24.2M net) and a $50M Lincoln Park Capital equity line, both signed May 27. The in-window event is the listing; the capital was arranged pre-window, no royalty layer (see Financings)

- Edesa Biotech ~$3.5M private placement (Wed June 10, announced June 11): 729,241 common shares at $4.69 (outside investors) and $5.21 (CEO), placed without an underwriter or placement agent, to fund the paridiprubart vitiligo programme and working capital; close expected about June 15. A clean micro-cap equity print, no royalty layer (see Financings)

- Shilpa Biocare / Gate2Brain EUR 7M strategic equity stake (Mon June 8; regulatory filing June 3): Shilpa Biocare (a Shilpa Medicare subsidiary) acquires a 30.4% stake in Barcelona-based Gate2Brain for EUR 7M (EUR 0.5M cash, EUR 5.5M in equity for services, EUR 1M project development) and becomes CMC, manufacturing, and regulatory partner for G2B-002 (MiniAp4 peptide shuttle delivering SN-38; pediatric DIPG and pGBM; US FDA and EMA orphan drug). A strategic equity-and-services investment into a private originator, no royalty layer (see Financings)

Fund formation (capital raised by GPs, not companies):

- Star51 Capital inaugural medtech venture fund first close (Thu June 11): first close of an operator-led medtech-and-AI "ecosystem" fund anchored by Abbott and Mayo Clinic, with medtech-operator LPs; targets early and growth-stage interventional therapies, diagnostics, monitoring, and healthcare digitalization across the US, Europe, and the Middle East. Size undisclosed; a supply-side capital-formation event in CFC's device scope, not a royalty origination (see Funds and Capital Formation)

Royalty re-ratings (no new capital):

- Boehringer Ingelheim / Zealand Pharma survodutide SYNCHRONIZE-1 and SYNCHRONIZE-MASLD Phase 3 (Sun June 7): up to a 16.6% average weight loss at 76 weeks in obesity (SYNCHRONIZE-1) and met MASLD endpoints (SYNCHRONIZE-MASLD), at ADA 2026, published in NEJM and Nature Medicine; re-rates Zealand's high-single-digit to low-double-digit royalty plus up to EUR 315M in outstanding milestones (see Survodutide and Elecoglipron Royalty Re-Rates)

- AstraZeneca / Eccogene elecoglipron VISTA and SOLSTICE Phase 2b (ADA 2026): positive Phase 2b obesity (VISTA) and type 2 diabetes (SOLSTICE) data on the oral GLP-1 receptor agonist elecoglipron, supporting global Phase 3 initiation; re-rates Eccogene's tiered royalty plus up to ~$1.825B in outstanding milestones on AstraZeneca's ex-China net sales (see Survodutide and Elecoglipron Royalty Re-Rates)

- Alphamab Oncology anbenitamab (KN026) Phase 3 breast cancer topline (Thu June 11): positive Phase 3 data for the anti-HER2 bispecific with CSPC's albumin-bound docetaxel (HB1801) in breast cancer; co-developed with CSPC subsidiary JMT-Bio. A China-domestic co-development with no disclosed tradable third-party royalty held by an independent originator

- Tango Therapeutics / Revolution Medicines vopimetostat plus daraxonrasib Phase 1/2 (PDAC) (Mon June 8): 92% objective response rate (11 of 12 response-evaluable patients, 9 of 11 confirmed) and a 90% six-month PFS rate in MTAP-deleted, RAS-mutant metastatic PDAC, supporting Phase 3 in first-line disease; incrementally de-risks the commercial base behind Royalty Pharma's up to $1.25B synthetic royalty plus up to $750M senior secured loan on Revolution Medicines' daraxonrasib (June 2025). The primary daraxonrasib re-rate was the April 2026 RASolute 302 monotherapy Phase 3, which triggered the second $250M tranche; an RPRX back-book position (see Daraxonrasib and Zasocitinib Re-Rates)

- Takeda zasocitinib (TAK-279) LATITUDE Atlas Phase 3 head-to-head (Thu June 11): zasocitinib statistically superior to deucravacitinib on PASI 100 at week 16 in moderate-to-severe plaque psoriasis (more than 35% complete skin clearance, more than 2.5 times the comparator); advances the oral TYK2 inhibitor Takeda acquired from Nimbus Therapeutics in 2022. Nimbus holds up to $2B in contingent sales milestones (two $1B tranches at $4B and $5B in annual net sales), not a running royalty (see Daraxonrasib and Zasocitinib Re-Rates)

Clinical and regulatory:

- Cartesian Therapeutics / WestGene Biopharma in-vivo CAR-T license (Tue June 9): Cartesian (Nasdaq: RNAC) pairs its Descartes-08 mRNA payload with WestGene's targeted LNP platform for in-vivo mRNA CAR-T in autoimmune disease (Phase 1 in myasthenia gravis targeted 2H 2026). WestGene receives an upfront and milestones; no royalty disclosed

- GENESIS Pharma / Alnylam Nordic commercialisation expansion (Wed June 10): GENESIS (Athens) adds Denmark, Finland, Norway, and Sweden to commercialise Alnylam's RNAi therapeutics; undisclosed terms, no disclosed royalty origination

- Verge Labs / Tenacia Biotechnology CNS platform partnership (Tue June 9): Verge Labs (San Francisco; formerly Verge Genomics) applies its multimodal human brain-tissue AI platform to prioritise targets across the CNS pipeline of China-based, Bain Capital-backed Tenacia Biotechnology; the first deal under Verge's May 2026 platform-first model. Terms undisclosed, no royalty layer

- Syntax Bio / Mayo Clinic type 1 diabetes cell therapy collaboration (Tue June 9): R&D collaboration to develop an allogeneic, iPSC-derived pancreatic beta-cell therapy for type 1 diabetes using Syntax's CRISPR-based Cellgorithm platform; Mayo provides pancreatic biology and preclinical functional testing and holds a financial interest. Terms undisclosed, no royalty layer

- Sanofi SAR445088 Phase 3 in CIDP discontinued (June 9 to 10): the anti-C1s monoclonal antibody was stopped for lack of efficacy at interim analysis; a negative readout, no royalty content

- FDA RMAT designation for a CD22-targeting allogeneic CAR-T (lasme-cel) (Tue June 9): in r/r B-ALL; a regulatory designation, no financing or royalty layer

- FDA orphan drug designation for Tris Pharma's once-nightly oxybate (TRN-257) (Wed June 10): in idiopathic hypersomnia; a regulatory designation, no financing or royalty layer

- FDA Complete Response Letter to Camurus for CAM2029 (Oclaiz) in acromegaly (Wed June 10): the CRL relates to observations from a September 2024 cGMP inspection at a third-party manufacturer, not to clinical efficacy or safety; resubmission targeted near term, with the EU and UK already approved (Oczyesa). A regulatory setback, no royalty layer

Window totals

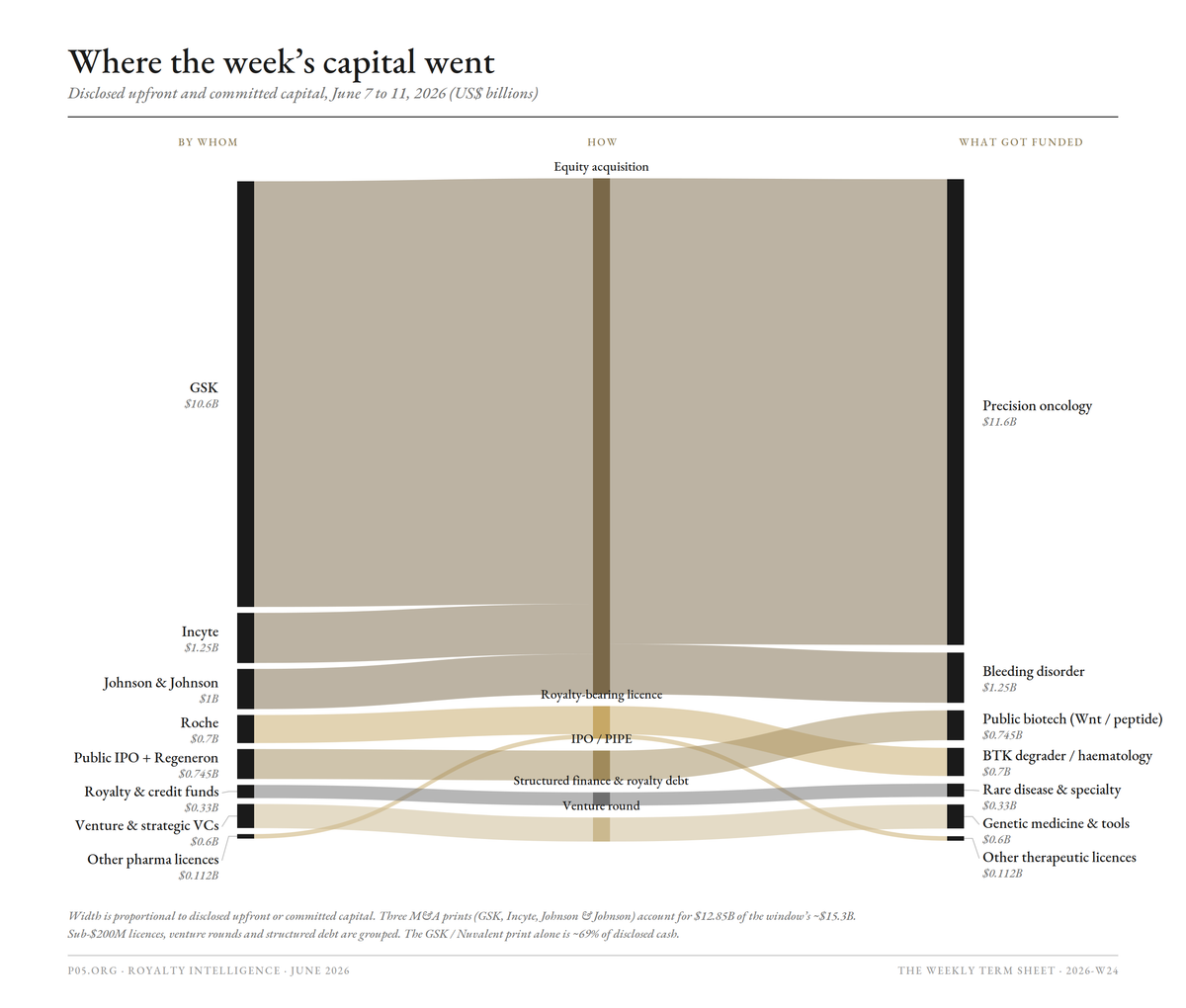

The window's cash is overwhelmingly M&A, concentrated in the GSK / Nuvalent print.

- M&A cash: ~$12.85B upfront (~$13.6B at ceilings) across three disclosed acquisitions: GSK / Nuvalent $10.6B all-cash, Incyte / Vega $1.25B upfront (up to $2.0B), J&J / Firefly $1.0B all-cash. Plus the Treeline / Standard BioTools all-stock reverse merger (~$2.5B equity value, $900M+ combined cash) and two undisclosed-terms events (Galmed / Colospan, BioNTech founder carve-out). Separately, PharmaEssentia / FORUS closed in-window (US$36.5M, agreed April 9), a royalty-retiring in-licensee buy-in not summed into the headline because the agreement predates the window. The Adial / Azora acquisition (Thu June 11) is all-stock with a concurrent private placement of up to $64M ($32M upfront), a micro-cap reverse takeover not summed into M&A cash.

- Royalty-bearing originations: 7 license-outs and platform layers carrying future third-party royalties, ~$822M in disclosed upfronts (Roche / Nurix $700M, Orionis / Novartis $40M, Laekna / Vasque $10M, AlzeCure / Lilly $10M, Engitix / GSK up to GBP 44.5M near-term, Medexus / ExCellThera $2M), headline value up to ~$5.2B+ excluding per-target and undisclosed terms (AmMax / Lonza). None is a present aggregator purchase; all are forward streams.

- Structured finance and non-dilutive debt: 2 prints, ~$300M of capacity at Beren (incl. a $55M Hercules royalty-financing sleeve, the window's only explicit royalty layer) plus up to CHF 250M at Idorsia (CHF 150M funded). Debt and pre-commercial royalty financing, not royalty paper traded.

- Equity financings: ~$1.2B gross across eight raises with no royalty origination: Parabilis ~$745M (incl. $75M Regeneron), Element $175M, SonoThera $125M, City $99.5M, Circio ~NOK 300M (USD ~32M), Cantargia ~SEK 199M (USD ~21M), Edesa ~$3.5M, and Shilpa Biocare's EUR 7M (USD ~7.5M) strategic stake in Gate2Brain. VERAXA's de-SPAC Nasdaq listing also completed in-window (VRXA), backed by a $27.5M senior secured note and a $50M equity line arranged May 27, not counted as in-window origination.

- Royalty re-rates (no new capital): 5 readouts: survodutide (Zealand), elecoglipron (Eccogene), anbenitamab (China-domestic co-development), the Tango / Revolution vopimetostat plus daraxonrasib PDAC combination (incrementally de-risking Royalty Pharma's daraxonrasib synthetic royalty, an RPRX back-book position), and Takeda's zasocitinib head-to-head Phase 3 (advancing Nimbus's contingent sales milestones, not a running royalty).

- Fund formation: 1 first close, Star51 Capital's inaugural medtech-and-AI fund (Abbott and Mayo Clinic anchors), size undisclosed. A GP-level capital-formation event, not summed into deal value.

- Royalty paper purchased by an aggregator this window: none. Net originated-and-traded royalty total = $0; the week's royalty content is forward originations and one pre-commercial royalty-financing sleeve.

Excluded from deal-value totals

| Transaction | Treatment |

|---|---|

| GSK / Nuvalent | Equity acquisition of internally discovered precision-oncology assets; GSK assumes Nuvalent's existing low-single-digit royalties payable to Royalty Pharma and Deerfield. Logged as M&A, the window's largest cash print; the assumed RPRX and Deerfield streams are a live back-book royalty layer, not newly originated paper |

| Incyte / Vega; J&J / Firefly Bio | Equity acquisitions with no retained third-party royalty; logged as M&A, not royalty paper. The VGA039 rare pediatric disease designation is a potential PRV source, a tradable asset but not a royalty |

| Galmed / Colospan | Medtech combination, no royalty layer, undisclosed terms |

| Treeline / Standard BioTools | Corporate combination and going-public transaction, not a royalty origination, though it carries an upstream Hengrui royalty on TLN-254 and a CVR to pre-merger holders |

| PharmaEssentia / FORUS | Royalty-retiring acquisition of an in-licensee, closing of an April 9 agreement; removes a downstream Canadian BESREMi royalty rather than originating one. Logged as M&A, not summed (announced pre-window) |

| Adial / Azora | All-stock acquisition with a concurrent up-to-$64M private placement ($32M upfront); micro-cap reverse takeover, no retained third-party royalty |

| Shilpa Biocare / Gate2Brain | Strategic 30.4% equity stake (EUR 7M) plus CMC, manufacturing, and regulatory partnership; investment into a private originator, no royalty layer |

| Parabilis IPO; SonoThera, City, Element / Samsung rounds | Primary equity raises, not royalty paper purchased by an aggregator |

| Roche / Nurix, AlzeCure / Lilly, Engitix / GSK, Orionis / Novartis, Laekna / Vasque, Medexus / ExCellThera, AmMax / Lonza royalties; BioNTech inbound stream | Future originations rather than present aggregator purchases |

| Cartesian / WestGene; GENESIS / Alnylam; Verge / Tenacia; Syntax / Mayo | No disclosed royalty |

| Idorsia / Pharmakon facility | Senior secured debt, not royalty paper |

| Beren / Hercules Capital financing | Equity plus senior secured debt and a $55M royalty-financing sleeve; the royalty layer is a forward stream, not an aggregator purchase today |

| Cantargia rights issue; Circio warrant exercise | Dilutive equity (Cantargia with a venture-debt sleeve), no royalty origination |

| VERAXA / Voyager de-SPAC | Nasdaq listing completion; business combination agreed April 2025, financing arranged May 27. In-window listing only, no royalty origination |

| Edesa private placement | Small primary equity raise (~$3.5M), no royalty layer |

| Magle Group bondholder restructuring | Distressed debt-for-control workout, no royalty content |

| Star51 Capital fund first close | GP-level capital formation, not a company transaction or royalty origination; tracked for LP-landscape intelligence only |

| Survodutide, elecoglipron, anbenitamab, vopimetostat plus daraxonrasib, zasocitinib readouts | No new capital; survodutide and elecoglipron re-rate existing Zealand and Eccogene royalties, the Tango / Revolution combination incrementally de-risks Royalty Pharma's daraxonrasib synthetic royalty (an RPRX back-book position), Takeda's zasocitinib advances Nimbus's contingent sales milestones rather than a running royalty, and anbenitamab re-rates a China-domestic co-development rather than a tradable third-party royalty |

M&A and Restructuring

Eight corporate events anchor this section. The GSK acquisition of Nuvalent, $10.6B all-cash, is the window's largest print and the second-largest deal in GSK's history, an equity acquisition of internally discovered precision-oncology assets with no disclosed third-party royalty. The Incyte acquisition of Vega Therapeutics, up to $2.0B, is an equity acquisition, so Star retains no running royalty on VGA039. The Johnson & Johnson acquisition of Firefly Bio, $1.0B all-cash, is a preclinical platform purchase with no disclosed retained royalty.

The smaller Galmed / Colospan combination is a GI medtech acquisition with undisclosed terms. Two further events carry royalty content: the Treeline Biosciences / Standard BioTools reverse merger carries an upstream Hengrui royalty plus a CVR, and BioNTech's planned founder separation would route a milestone-and-royalty stream back to BioNTech.

A seventh, the Magle Group bondholder restructuring, is a distressed debt-for-control workout with no royalty content. An eighth, the Adial / Azora acquisition, is an all-stock takeover paired with an up-to-$64M private placement, a micro-cap reverse takeover with no retained third-party royalty.

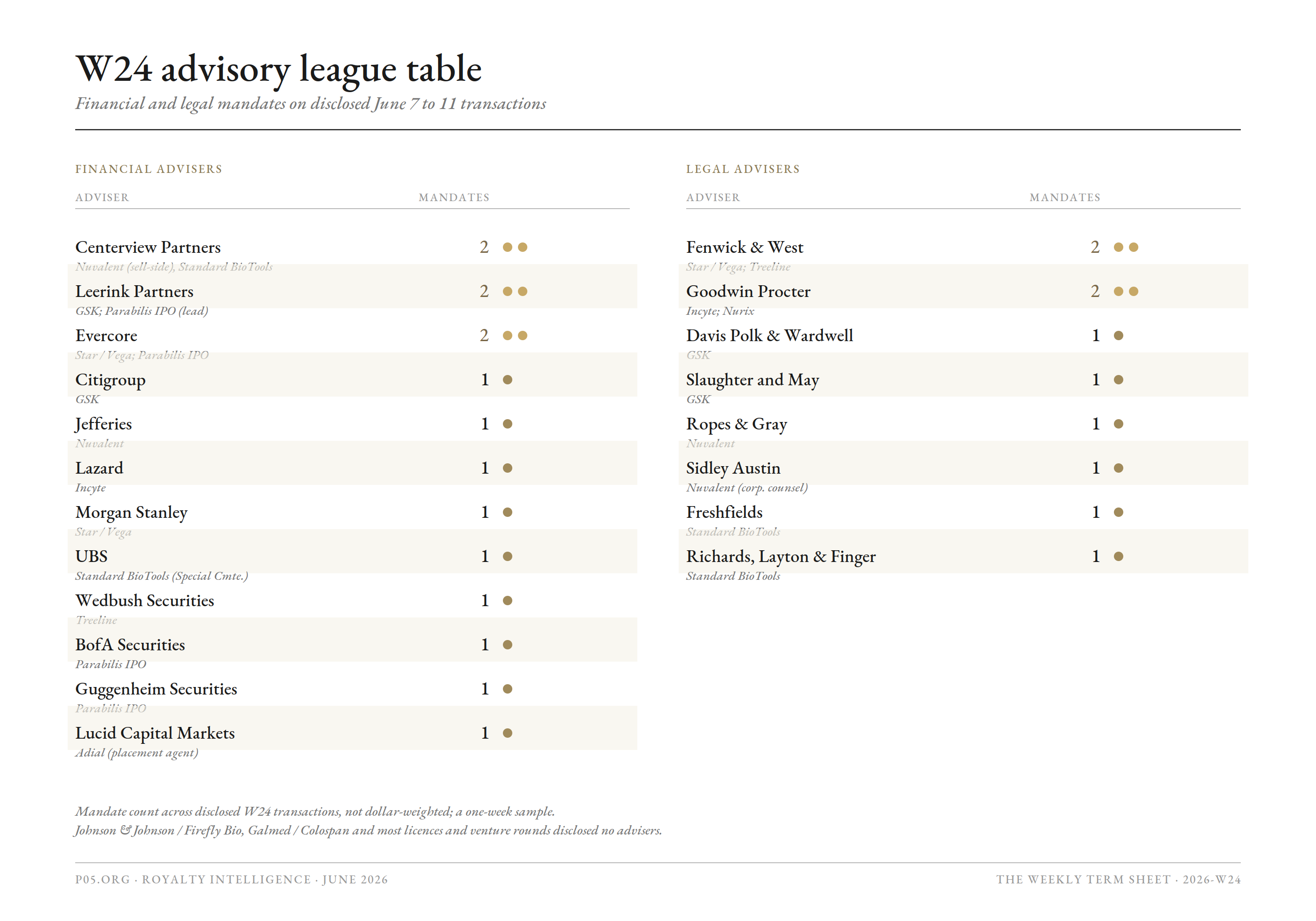

GSK / Nuvalent: NSCLC Precision-Oncology Acquisition, $10.6B All-Cash (Tue June 9)

GSK plc (LSE / NYSE: GSK) entered a definitive agreement to acquire Nuvalent, Inc. (Nasdaq: NUVL; Cambridge, MA; founded 2017), a clinical-stage precision-oncology company, for $124.00 per share in cash, an aggregate equity value of about $10.6B (£8.0B), roughly $9.4B net of Nuvalent's ~$1.3B cash. GSK will commence a tender offer for all outstanding Class A and Class B common stock within 10 business days, with closing targeted for Q3 2026 (GSK release; GSK 6-K, SEC).

The $124.00 price is about a 40% premium to Nuvalent's prior close (shares rose ~39% to $123.25 on the news). The deal centres on two late-stage, potential best-in-class NSCLC inhibitors discovered on Nuvalent's own structure-based chemistry platform: zidesamtinib (NVL-520), a ROS1-selective inhibitor with an FDA target action date of September 18, 2026, and neladalkib (NVL-655), an ALK-selective inhibitor with a target date of November 27, 2026. Both hold FDA Breakthrough Therapy and Orphan Drug designations, with pivotal data at IASLC WCLC 2025 and ASCO 2026; the pipeline also includes the earlier-stage NVL-330 (HER2). Analyst peak-sales estimates for the pair range widely, from ~$823M (CGS International, FY2029) to up to ~$4B combined (BofA). GSK frames the deal as accretive to sales and core operating profit in 2027 and core EPS in 2029, a platform for expansion with its B7-H3 ADC Ris-Rez, and an offset to the 2028 loss of exclusivity on dolutegravir, with no change to 2026 guidance. It is GSK's third 2026 acquisition under CEO Luke Miels, after Rapt Therapeutics ($2.2B, January) and 35Pharma ($950M, February), and the second-largest in GSK's history.

| Term | Detail |

|---|---|

| Acquirer | GSK plc (LSE / NYSE: GSK; CEO Luke Miels) |

| Target | Nuvalent, Inc. (Nasdaq: NUVL; Cambridge, MA; founded 2017; CEO James Porter; structure-based precision oncology) |

| Structure | All-cash tender offer for all Class A and Class B common stock at $124.00 per share, commencing within 10 business days |

| Economics | ~$10.6B equity value (£8.0B); ~$9.4B net of cash; about a 40% premium; $350.475M termination fee |

| Funding | New and existing debt facilities plus cash |

| Lead assets | Zidesamtinib (NVL-520; ROS1; PDUFA Sept 18, 2026) and neladalkib (NVL-655; ALK; PDUFA Nov 27, 2026), both Breakthrough Therapy and Orphan Drug; plus early-stage NVL-330 (HER2) |

| Peak-sales range | ~$823M (CGS International, FY2029) to up to ~$4B combined (BofA) |

| Strategic rationale | Entry into targeted lung cancer; platform for GSK's Ris-Rez B7-H3 ADC; offsets 2028 dolutegravir HIV loss of exclusivity; supports the £40B-by-2031 sales goal |

| Condition / timing | Subject to tender conditions, HSR and other regulatory clearances; Nuvalent board recommends acceptance; closing targeted Q3 2026 |

| Advisers | Leerink Partners and Citigroup (financial) and Davis Polk & Wardwell and Slaughter and May (legal) to GSK; Centerview Partners and Jefferies (financial), Ropes & Gray (legal) and Sidley Austin (corporate) to Nuvalent |

| Date | Tue June 9, 2026 |

| Royalty read | |

|---|---|

| Structure | Equity acquisition; GSK buys the assets outright via tender offer |

| Tradable element | Zidesamtinib and neladalkib are internally discovered from Nuvalent's chemistry platform, but the assets are not royalty-free: GSK assumes Nuvalent's existing revenue-sharing arrangements, low-single-digit royalties payable to Royalty Pharma and Deerfield, which survive the acquisition and accrue on GSK's net sales. Deerfield's stream traces to its 2017 founding-investor seeding of Nuvalent (sole Series A funder); Royalty Pharma holds a separate low-single-digit stream. A Guardant Health companion-diagnostics collaboration (April 2026) also travels with the assets but is a commercial pact, not a royalty |

| Read | The window's largest cash print, removing two near-commercial precision-oncology assets from the out-licensing universe into a wholly owned franchise; logged as M&A, but it carries a live Royalty Pharma (and Deerfield) low-single-digit royalty on two NSCLC inhibitors entering commercial review, an RPRX back-book position rather than new origination |

Incyte / Vega Therapeutics: VGA039 Bleeding-Disorder Acquisition, Up to $2.0B (Mon June 8)

Incyte (Nasdaq: INCY; Wilmington, DE) entered a definitive agreement to acquire Vega Therapeutics, Inc., a wholly owned subsidiary of Star Therapeutics, LLC (South San Francisco, CA), for $1.25B upfront, with up to $750M in additional payments on sales milestones, up to $2.0B total (Incyte 8-K exhibit, SEC).

The acquisition adds VGA039, an investigational anti-Protein S monoclonal antibody in Phase 3 pivotal development for von Willebrand disease (VWD), the most common inherited bleeding disorder (~135,000 diagnosed US patients). It is positioned as a potential first subcutaneous, once-monthly prophylactic therapy for VWD, against current factor-replacement regimens requiring two to three IV infusions a week.

| Term | Detail |

|---|---|

| Acquirer | Incyte Corporation (Nasdaq: INCY; Wilmington, DE; CEO Bill Meury) |

| Seller | Star Therapeutics, LLC (South San Francisco, CA; Founder and CEO Adam Rosenthal), selling its wholly owned subsidiary Vega Therapeutics, Inc. |

| Asset | VGA039: investigational anti-Protein S monoclonal antibody; subcutaneous, once-monthly |

| Lead indication / stage | Von Willebrand disease (all types); Phase 3 VIVID-6 (NCT07115004) |

| Regulatory designations | FDA Breakthrough Therapy, Fast Track, orphan drug, and rare pediatric disease designations |

| Structure | Equity acquisition; expected ~$1.25B R&D charge in Q3 and FY2026 |

| Economics | $1.25B upfront plus up to $750M sales milestones (up to $2.0B); no retained Star royalty |

| Condition | Subject to HSR clearance; closing targeted Q3 2026 |

| Advisers | Lazard and Goodwin Procter to Incyte; Evercore, Morgan Stanley, and Fenwick & West to Star |

| Date | Mon June 8, 2026 |

| Royalty read | |

|---|---|

| Structure | Equity acquisition; Incyte buys the asset outright, Star retains no running royalty on VGA039 |

| Tradable element | VGA039 rare pediatric disease designation, a potential priority review voucher on approval; a sellable asset, not a royalty stream |

| Read | Removes a private clinical-stage asset from the out-licensing universe into a wholly owned franchise; the largest disclosed cash print of the window |

Johnson & Johnson / Firefly Bio: Firelink Degrader-Antibody-Conjugate Platform, $1.0B Cash (Mon June 8)

Johnson & Johnson (NYSE: JNJ) entered a definitive agreement to acquire Firefly Bio, Inc. (South San Francisco, CA; privately held) for $1.0B in cash, adding the proprietary Firelink degrader-antibody-conjugate (DAC) platform and preclinical candidates targeting KRAS-driven solid tumours (J&J release).

The Firelink platform conjugates targeted protein degraders to antibodies, a next-generation variant of the ADC format. The deal is all-cash with no disclosed milestone tail; closing targeted later in 2026.

| Term | Detail |

|---|---|

| Acquirer | Johnson & Johnson (NYSE: JNJ) |

| Seller | Firefly Bio, Inc. (South San Francisco, CA; privately held; venture-backed) |

| Asset / platform | Firelink degrader-antibody-conjugate (DAC) platform; preclinical candidates in KRAS-driven solid tumours |

| Stage | Preclinical |

| Economics | $1.0B all-cash; no disclosed milestones or retained royalty |

| Condition | Subject to regulatory clearance; closing targeted later in 2026 |

| Date | Mon June 8, 2026 |

| Royalty read | |

|---|---|

| Structure | All-cash platform acquisition; no disclosed milestone or royalty tail |

| IP note | Firefly's degrader and conjugation IP may rest on in-licensed academic or platform components, but none was disclosed; no tradable third-party royalty to log today |

| Read | A platform consolidated into J&J rather than a stream created; a second degrader-modality print alongside the Roche / Nurix BTK degrader |

Galmed Pharmaceuticals / Colospan: CG-100 Anastomotic-Protection Device, Terms Undisclosed (Mon June 8)

Galmed Pharmaceuticals Ltd. (Nasdaq: GLMD; Tel Aviv) entered a definitive agreement to acquire Colospan Ltd. (Israel; privately held), maker of the CG-100 intraluminal bypass device, which protects colorectal anastomoses and can reduce the need for a diverting stoma (PharmExec roundup).

Financial terms were not disclosed. Colospan becomes a wholly owned Galmed subsidiary, a medtech pivot. CG-100 carries FDA Breakthrough Device Designation and a CE mark under EU MDR, with a US pivotal IDE trial ongoing.

| Term | Detail |

|---|---|

| Acquirer | Galmed Pharmaceuticals Ltd. (Nasdaq: GLMD; Tel Aviv) |

| Seller | Colospan Ltd. (Israel; privately held) |

| Asset | CG-100: intraluminal bypass device for protecting colorectal anastomoses and reducing diverting stomas |

| Regulatory status | FDA Breakthrough Device Designation; CE mark under EU MDR; US pivotal IDE trial ongoing |

| Economics | Terms undisclosed at announcement; no royalty layer |

| Date | Mon June 8, 2026 |

| Royalty read | |

|---|---|

| Structure | Medtech equity acquisition, undisclosed terms, no royalty mechanics |

| Read | The window's third corporate combination and a strategic pivot, not a royalty-relevant transaction |

Treeline Biosciences / Standard BioTools: All-Stock Reverse Merger, ~$2.5B Treeline Equity Value (Mon June 8)

Treeline Biosciences (Stamford, CT; privately held oncology company) agreed to combine with Standard BioTools (Nasdaq: LAB) in an all-stock merger that takes Treeline public, with the combined company keeping the Treeline name and trading as TRLN (release).

The exchange ratio is set against an assumed Treeline equity value of ~$2.5B versus Standard BioTools at ~$460M, leaving pro forma ownership of roughly 84% Treeline and 16% Standard BioTools. The combined company expects over $900M in cash at closing, funding a runway into 2029. Pre-merger Standard BioTools holders receive a five-year contingent value right (capped at 76 million combined-company shares) paying net proceeds from the legacy Mass Cytometry and Microfluidics businesses plus up to $50M in earnout tied to Illumina's earlier SomaLogic acquisition. Closing targeted 2H 2026.

| Term | Detail |

|---|---|

| Acquirer / public vehicle | Standard BioTools Inc. (Nasdaq: LAB), to be renamed Treeline Biosciences Holdings, Inc. (ticker TRLN) |

| Target / surviving identity | Treeline Biosciences (Stamford, CT; founded 2021 by CEO Josh Bilenker, ex-Loxo, and CSO Jeff Engelman, ex-Novartis NIBR; backers ARCH, OrbiMed, GV, KKR, Casdin, Access Industries) |

| Structure | All-stock reverse merger; tax-free; ~84% Treeline / ~16% Standard BioTools fully diluted; $16.1M termination fee; 180-day insider lock-ups |

| Valuation | ~$2.5B Treeline equity value; ~$460M Standard BioTools; $900M+ combined cash; runway into 2029 |

| CVR | Five-year term, capped at 76M shares; net proceeds from legacy Mass Cytometry and Microfluidics plus up to $50M Illumina / SomaLogic earnout |

| Pipeline | Phase 1 oncology: BCL6 degrader TLN-121, EZH2 inhibitor TLN-254, pan-KRAS inhibitor TLN-372; BCL-XL degrader TLN-499 clinic-bound later in 2026 |

| Upstream royalty | TLN-254 (EZH2; SHR-2554) in-licensed from Jiangsu Hengrui (2023, ex-Greater China): $11M upfront, up to $45M development and up to $650M sales milestones, plus 10 to 12.5% royalties to Hengrui |

| Advisers | Centerview Partners (financial), Freshfields and Richards, Layton & Finger (legal), and UBS (financial, to the Special Committee) to Standard BioTools; Wedbush Securities (financial) and Fenwick & West (legal) to Treeline |

| Date | Mon June 8, 2026 |

| Royalty read | |

|---|---|

| Upstream licensor royalty | TLN-254 carries a 10 to 12.5% royalty to Hengrui on net sales, a live third-party obligation that travels with the asset and a stream Hengrui could monetise once sales begin |

| CVR | A royalty-adjacent contingent-payment instrument, here tied to legacy diagnostics asset sales and the Illumina / SomaLogic earnout rather than a drug royalty |

| Structure | A corporate combination and going-public transaction, not a royalty origination; the $900M+ cash is balance-sheet cash, not a new third-party raise |

| Caveat | Fundraising figures differ (~$1.1B per Fierce Biotech late 2025 vs ~$1.2B in the June 8 release); the Hengrui royalty band is from 2023 reporting and should be confirmed against the merger proxy |

BioNTech / Founders: mRNA Carve-Out and Separation, Undisclosed Terms (Handelsblatt Mon June 8)

BioNTech (Nasdaq: BNTX; Mainz, Germany) and its founders Ugur Sahin and Ozlem Tureci have largely finalised the terms of their separation, first announced March 10, 2026, under which the pair will leave operational and board roles by end-2026 to start a new independent next-generation mRNA company (Handelsblatt).

Per Handelsblatt, BioNTech would transfer its early-stage CAR-T cell therapy portfolio and RiboMAB programme (mRNA-encoded antibodies) to the founders' new company, with roughly 300 mostly research staff expected to move. BioNTech retains the patents on its drug candidates, with the founders receiving a license to develop RiboMAB further and an option to return the technology later. The separation sits against a broader BioNTech restructuring (up to ~1,860 job cuts by end-2027).

| Term | Detail |

|---|---|

| Parties | BioNTech SE (Nasdaq: BNTX; Mainz) and founders Ugur Sahin and Ozlem Tureci |

| Structure | Corporate carve-out plus governance transition; founders exit by end-2026; binding agreement targeted end of H1 2026 |

| Transferred assets | Early-stage CAR-T portfolio and RiboMAB; ~300 mostly research employees |

| Retained by BioNTech | Patents on drug candidates; commercial and late-stage business, including the Pfizer / Comirnaty profit split and other commercial royalty streams; iNEST |

| Consideration to BioNTech | Minority stake plus milestones and royalties (arm's length per March 10 release); RiboMAB license-back option |

| Status | Asset valuation under negotiation; specifics from company circles, not yet confirmed by BioNTech |

| Date | Handelsblatt report Mon June 8, 2026; split announced March 10, 2026 |

| Royalty read | |

|---|---|

| In-scope stream | The inbound line back to BioNTech: a minority stake plus milestones and royalties from the new company, contributed on an arm's length basis |

| Structure | A rare case of a large-cap originating a fresh inbound royalty-and-milestone line through a corporate split, plus a RiboMAB license-back option preserving optionality |

| Status | Economics (rate, milestone schedule, stake size, patent valuation) not yet public; await the binding agreement targeted end of H1 2026 |

| Out of scope | The marquee royalty and profit-share franchises (Pfizer / Comirnaty chief among them) stay in the commercial business retained by BioNTech |

Magle Group: Bondholder Restructuring, Debt-for-Control Workout (Thu June 11)

Magle Chemoswed Holding AB (Nasdaq First North; Sweden; API, degradable starch microspheres, wound care and diagnostics, via subsidiaries Magle Chemoswed AB and Adroit Science AB) announced agreement in principle on the key principles of a restructuring with an ad hoc group of holders representing about 70% of its outstanding SEK 350M senior secured floating-rate bonds 2025/2028 (ISIN SE0025197403) (MarketScreener).

The terms point to a debt-for-control outcome, with bondholders set to convert into equity and potentially take control of the group. The update follows a stretched workout: an April written-procedure waiver of the maintenance tests conditional on raising at least SEK 100M of net proceeds by June 30, a ~SEK 40M rights issue, a 3% consent-fee set-off issue (~SEK 9.3M), and a bridge loan of up to SEK 60M from existing bondholders, all against the June 30 maturity of a Danske Bank facility. The associated written procedure runs to a June 22 voting deadline.

| Term | Detail |

|---|---|

| Company | Magle Chemoswed Holding AB (Nasdaq First North; Sweden; subsidiaries Magle Chemoswed AB and Adroit Science AB) |

| Instrument | SEK 350M senior secured floating-rate bonds 2025/2028 (ISIN SE0025197403) |

| Counterparty | Ad hoc group holding ~70% of the bonds (~73.8% under the May bridge-loan agreement) |

| Structure | Agreement in principle on key restructuring terms; debt-for-equity conversion, bondholders may take control |

| Context | April maintenance-test waiver conditional on SEK 100M net proceeds by June 30; ~SEK 40M rights issue; ~SEK 9.3M consent-fee set-off; up to SEK 60M bondholder bridge loan; Danske Bank facility maturing June 30 |

| Process | Written procedure with a June 22 voting deadline |

| Date | Thu June 11, 2026 |

| Royalty read | |

|---|---|

| Royalty layer | None; a distressed balance-sheet restructuring, not a royalty origination or monetisation |

| Read | A small-cap distressed debt-for-control workout. Of structural interest only as a worked example of senior secured bondholders converting to equity in a sub-scale pharma-chemistry issuer, not a tradable royalty stream |

PharmaEssentia / FORUS Therapeutics: Canadian BESREMi Licensee Buy-In, US$36.5M (Closed Thu June 11; Agreed April 9)

PharmaEssentia Corporation (TWSE: 6446; Taipei and Burlington, MA) closed the acquisition of 100% of FORUS Therapeutics Inc. (Oakville, Ontario), its Canadian commercialisation licensee for BESREMi (ropeginterferon alfa-2b-njft) in polycythemia vera, in a transaction valued at US$36.5M (C$50M) (PharmaEssentia release). The acquisition was agreed April 9, 2026 and completed June 11, 2026; only the closing falls inside this window.

Under the October 31, 2024 exclusive Canada license, FORUS registered and commercialised BESREMi for PV (New Drug Submission to Health Canada July 2025, approval expected Q3 2026) and owed PharmaEssentia up to $107M in milestones plus double-digit percentage royalties on Canadian net sales. By buying FORUS outright, PharmaEssentia retires that downstream royalty and milestone obligation and brings Canadian regulatory, medical, and commercial capability in-house. FORUS's existing Karyopharm relationship (XPOVIO) travels with the team.

| Term | Detail |

|---|---|

| Acquirer | PharmaEssentia Corporation (TWSE: 6446; Founder and CEO Ko-Chung Lin) |

| Target | FORUS Therapeutics Inc. (Oakville, Ontario; CEO Kevin Leshuk), PharmaEssentia's Canadian BESREMi licensee since October 2024 |

| Asset | BESREMi (ropeginterferon alfa-2b-njft) in polycythemia vera; essential thrombocythemia submission in preparation |

| Structure | Acquisition of 100% of FORUS; US$36.5M (C$50M) |

| Retired economics | The October 2024 Canada license carried up to $107M in milestones plus double-digit percentage royalties payable by FORUS to PharmaEssentia on Canadian net sales |

| Timing | Agreed April 9, 2026; closed June 11, 2026 |

| Royalty read | |

|---|---|

| Structure | Royalty-retiring acquisition: PharmaEssentia buys in its own licensee, collapsing a downstream royalty into wholly owned commercial economics |

| Tradable element | None created. The transaction removes a third-party royalty rather than originating one, the inverse of an aggregator purchase |

| Read | A small but instructive in-window print for royalty tracking: an originator electing to retire a royalty by acquiring the payer, the opposite of monetisation. Logged as M&A, royalty-eliminating, not royalty paper |

BD Origination and Licensing

Seven royalty-bearing items anchor this section. Roche / Nurix bexobrutideg ($700M upfront, up to $2.3B) is the window's lead royalty-bearing event. Orionis / Novartis ($40M upfront, up to $1.4B) is a platform-discovery collaboration carrying tiered royalties to a privately held originator. Laekna / Vasque Bio pairs a tiered royalty with a high-teens equity option.

AlzeCure / Lilly and Engitix / GSK are European originator out-licences. Medexus / ExCellThera originates a small regional Canadian commercial royalty, and AmMax / Lonza marks a Basel CDMO platform-royalty model.

Roche / Nurix Therapeutics: Bexobrutideg (NX-5948), Up to $2.3B (Mon June 8)

Nurix Therapeutics (Nasdaq: NRIX; San Francisco; originator and licensor) entered an exclusive licensing and collaboration agreement with Roche (SIX: RO, ROP; OTCQX: RHHBY) to co-develop and co-commercialise bexobrutideg (NX-5948), an oral, brain-penetrant BTK degrader, across B-cell malignancies, immunology, and neurology (Roche release).

Nurix receives a $700M upfront and is eligible for milestones to a total of up to $2.3B. Development costs split 40% Nurix / 60% Roche. In the US the two co-commercialise and split profits and losses equally; outside the US Roche commercialises and Nurix receives low- to high-teens tiered royalties. Phase 3 initiation is planned for summer 2026 in second-line CLL.

| Term | Detail |

|---|---|

| Licensor / originator | Nurix Therapeutics, Inc. (Nasdaq: NRIX; San Francisco; CEO Arthur T. Sands) |

| Licensee / partner | Roche (SIX: RO, ROP; OTCQX: RHHBY; Levi Garraway, CMO and Head of Global Product Development) |

| Asset | Bexobrutideg (NX-5948): oral, brain-penetrant BTK degrader; eliminates both the kinase and scaffolding functions of BTK rather than inhibiting the active site |

| Lead indication / stage | r/r B-cell malignancies; Phase 3 planned summer 2026 in 2L CLL; expansion into immunology (CSU) and neurology (MS) |

| Geography | Global; US co-commercialisation by both parties, ex-US by Roche |

| Economics | $700M upfront plus milestones (up to $2.3B); 60/40 Roche/Nurix development cost share; 50/50 US profit-and-loss split; low- to high-teens tiered royalties to Nurix on ex-US net sales |

| Condition | Subject to HSR clearance; closing targeted Q3 2026 |

| Advisers | Goodwin Procter (legal) to Nurix; Roche advisers not disclosed |

| Date | Mon June 8, 2026 |

| Royalty read | |

|---|---|

| Tradable instrument | Low- to high-teens tiered royalty to Nurix on Roche's ex-US net sales |

| Stacked on | $700M upfront and a milestone ladder within the $2.3B ceiling |

| Non-royalty economics | 50/50 US profit-and-loss split (co-promote economics, not a royalty); Nurix funds 40% of development |

| Read | A US-origin royalty line in the making, accruing to a clinical-stage developer that also retains a 50% US economic interest; the disclosed band is wider and more concrete than the single-digit and undisclosed W23 Asia-outbound rates |

| Caveat | Lead value gated on the summer 2026 2L CLL Phase 3; CSU and MS are earlier; the 40% cost share offsets near-term cash |

Orionis Biosciences / Novartis: Molecular Glue Discovery Collaboration, $40M Upfront, Up to $1.4B (Tue June 10)

Orionis Biosciences (Boston and Ghent, Belgium; HQ Waltham, MA; privately held, clinical-stage) entered a renewed and expanded multi-year collaboration with Novartis (NYSE: NVS; SIX: NOVN) to discover and design molecular glue drugs for challenging targets across multiple disease areas, deploying Orionis's Allo-Glue platform and AI discovery engine (Business Wire).

Orionis receives a $40M upfront and is eligible for research, development, and commercial milestones of up to $1.4B, plus tiered royalties on net sales of collaboration products. The deal renews and expands a 2020 four-year discovery pact.

| Term | Detail |

|---|---|

| Licensor / originator | Orionis Biosciences (Boston / Ghent; HQ Waltham, MA; privately held, clinical-stage; CEO Niko Kley) |

| Licensee / partner | Novartis (NYSE: NVS; SIX: NOVN; John Tallarico, Head of Discovery Sciences) |

| Structure | Multi-year discovery and development collaboration; renewal and expansion of the 2020 pact; Allo-Glue platform plus AI discovery engine |

| Modality / focus | Small-molecule molecular glues modulating targets via induced proximity; oncology, immunology, and more |

| Economics | $40M upfront; up to $1.4B in milestones; tiered royalties to Orionis on net sales of collaboration products |

| Date | Tue June 10, 2026 |

| Royalty read | |

|---|---|

| Tradable instrument | Tiered royalty to Orionis on Novartis's net sales of collaboration products |

| Stacked on | $40M upfront and a milestone ladder to $1.4B |

| Structure | Platform-discovery collaboration, so the royalty is portfolio-wide and contingent on programmes Novartis advances; a long-dated, multi-programme stream |

| Read | A privately held, clinical-stage originator retaining a royalty against a large-cap on a validated, repeat-partner platform; a forward monetisation candidate once programmes advance |

| Caveat | No collaboration product is yet in the clinic from this pact; the rate band is not specified; $1.4B is a ceiling, not committed value |

Laekna / Vasque Bio: LAE118 Ex-Greater-China Out-Licence, Up to $527M Plus Equity (Tue June 9)

Laekna, Inc. (HKEX: 02105; Shanghai) entered an exclusive licensing agreement granting Vasque Bio, Inc. (US; clinical-stage, rare-disease-focused; backed by The Column Group and F-Prime) worldwide rights excluding Greater China to develop, manufacture, and commercialise LAE118, an internally discovered PI3K-alpha pan-mutant-selective inhibitor (Laekna disclosure via Minichart).

Laekna receives a $10M non-refundable upfront, is eligible for up to $517M in combined milestones (up to $527M total), and retains tiered royalties ranging from single-digit to double-digit percentages on net sales. In addition, Laekna holds the right to acquire, at no extra cost, up to a high-teens percentage of Vasque's common stock, or cash in lieu. A structurally uncommon clause further entitles Laekna to up to 50% of the value of any qualifying strategic transaction (an acquisition or sublicence of LAE118) that Vasque enters, guarding the originator against an early, cheap exit before milestones are earned. LAE118 has cleared IND review with the US FDA and China's NMPA.

| Term | Detail |

|---|---|

| Licensor / originator | Laekna, Inc. (HKEX: 02105; Shanghai; retains Greater China rights and an oncology focus) |

| Licensee / partner | Vasque Bio, Inc. (US; clinical-stage, rare-disease focus; The Column Group and F-Prime backed; ex-Greater-China rights) |

| Asset | LAE118: allosteric PI3K-alpha pan-mutant-selective inhibitor; IND-cleared in the US and China; PIK3CA-mutant solid tumours and overgrowth-spectrum disorders |

| Geography | Worldwide excluding Mainland China, Hong Kong, Macau, and Taiwan |

| Economics | $10M upfront; up to $517M milestones (up to $527M total); tiered single- to double-digit royalties to Laekna |

| Equity | Laekna's right to acquire up to a high-teens percentage of Vasque common stock at no extra cost, or cash in lieu |

| Transaction upside | Up to 50% of the value of any qualifying strategic transaction (acquisition or sublicence of LAE118) that Vasque enters; an uncommon anti-flip clause |

| Date | Tue June 9, 2026 |

| Royalty read | |

|---|---|

| Tradable instrument 1 | Tiered single- to double-digit royalty to Laekna on Vasque's ex-Greater-China net sales |

| Stacked on | $10M upfront and an up-to-$517M milestone ladder |

| Tradable instrument 2 | An equity option: up to a high-teens stake in the licensee at no cost, converting part of the downstream economics into direct exposure to a Vasque exit |

| Tradable instrument 3 | A contingent claim on up to 50% of the value of any qualifying Vasque strategic transaction (acquisition or sublicence) on LAE118, an anti-flip provision that captures exit value before milestones are earned |

| Read | A royalty-plus-equity-plus-transaction-upside hybrid distinct from the royalty-only out-licences (AlzeCure, Engitix); China-outbound, sub-scale originator band; extends the W23 Asia-outbound theme; forward monetisation candidate |

| Caveat | Early clinical-stage and milestone-weighted; the field is well-capitalised (Novartis / Synnovation up to $3B, March 2026); terms from HKEX disclosure and secondary reporting |

AlzeCure Pharma / Eli Lilly: ACD680 Gamma-Secretase Modulator, >$1B Excluding Royalties (Tue June 9)

AlzeCure Pharma (Nasdaq First North Growth Market Stockholm: ACURE; Huddinge, Sweden) entered a collaboration and out-licensing agreement granting Eli Lilly (NYSE: LLY) global rights to ACD680, a gamma-secretase modulator from AlzeCure's Alzstatin platform for Alzheimer's disease (BioStock). AlzeCure receives a $10M upfront and is eligible for milestones to a total exceeding $1B excluding royalties, plus mid-single-digit royalties. AlzeCure shares rose more than 300% on the announcement.

ACD680 reduces production of the harmful Abeta42 peptide while increasing shorter, non-aggregating Abeta species. The transaction is subject to Swedish FDI screening clearance.

| Term | Detail |

|---|---|

| Licensor / originator | AlzeCure Pharma AB (Stockholm: ACURE; Huddinge, Sweden; CEO Martin Jonsson) |

| Licensee / partner | Eli Lilly and Company (NYSE: LLY) |

| Asset | ACD680: gamma-secretase modulator (Alzstatin platform); shifts amyloid processing from Abeta42 toward shorter non-aggregating species |

| Indication / stage | Alzheimer's disease; early-stage, with potential preventive positioning |

| Geography | Global |

| Economics | $10M upfront; milestones to a total exceeding $1B excluding royalties; mid-single-digit royalties to AlzeCure |

| Condition | Subject to Swedish foreign direct investment screening clearance |

| Date | Tue June 9, 2026 |

| Royalty read | |

|---|---|

| Tradable instrument | Mid-single-digit royalty to AlzeCure on Lilly's global net sales |

| Stacked on | A modest $10M upfront and a milestone ladder carrying the headline past $1B |

| Structure | A clean single-asset originator royalty: no cost share or co-promote, so the entire downstream interest sits in the royalty and milestones |

| Read | The cut's cleanest CFC-shaped origination: a sub-scale European originator to a US large-cap, retaining a running royalty; a forward monetisation candidate once de-risked |

| Caveat | Early-stage in one of the hardest CNS indications; value is milestone-dominated and the royalty is long-dated; the Swedish FDI gate is a genuine closing condition |

Medexus / ExCellThera and Cordex: UM171 Cell Therapy Canadian License and Supply, $2M Upfront Plus Royalties (Tue June 9)

Medexus Pharmaceuticals (TSX: MDP; OTCQX: MEDXF; Toronto and Chicago) secured exclusive Canadian commercialisation rights to UM171 Cell Therapy (Zemcelpro / dorocubicel) under license and supply agreements with ExCellThera Inc. (Montreal) and its wholly owned subsidiary Cordex Biologics (Medexus release).

Medexus pays a $2M upfront, will make quarterly royalty payments to ExCellThera on net sales, and owes one-time milestones. Cordex manages the planned pivotal Phase 3 trial and supplies product on a cost-plus basis. UM171 is conditionally approved in the EU as Zemcelpro; the brand has not yet been reviewed by Health Canada.

| Term | Detail |

|---|---|

| Licensee | Medexus Pharmaceuticals Inc. (TSX: MDP; OTCQX: MEDXF; Toronto / Chicago; exclusive Canadian rights) |

| Licensor / originator | ExCellThera Inc. (Montreal) and Cordex Biologics (wholly owned subsidiary; manages Phase 3 and supply) |

| Asset | UM171 Cell Therapy (Zemcelpro / dorocubicel): expanded allogeneic haematopoietic stem-cell therapy; conditionally EU-approved; allo-HSCT in haematological malignancies |

| Geography | Canada (subject to Health Canada review) |

| Economics | $2M upfront; quarterly royalties to ExCellThera on Canadian net sales; one-time milestones; Cordex supplies on a cost-plus basis |

| Date | Tue June 9, 2026 |

| Royalty read | |

|---|---|

| Tradable instrument | Quarterly royalty to ExCellThera on Medexus's Canadian net sales |

| Stacked on | A $2M upfront and one-time milestones |

| Structure | A small single-territory commercial royalty on a conditionally-EU-approved cell therapy, accruing to the Canadian originator; the cost-plus supply keeps manufacturing economics with Cordex |

| Read | Closer to a near-term cash-bearing stream than the discovery-stage out-licences, though the Canada-only scope and Health Canada gate cap its size |

| Caveat | Royalty rate and milestone amounts beyond the $2M upfront were not disclosed; launch contingent on Health Canada review and payer engagement |

Engitix / GSK: Liver Fibrosis Regression Target Collaboration and Option, Up to GBP 44.5M Upfront and Near-Term (Mon June 8)

Engitix Ltd. (London; privately held) entered a strategic research collaboration and option agreement with GSK (LSE / NYSE: GSK) to identify and validate first-in-class targets driving liver fibrosis regression, pairing Engitix's human extracellular-matrix (ECM) platform and multi-omics datasets with GSK's development capabilities (GlobeNewswire).

Engitix is eligible for up to GBP 44.5M in upfront and near-term payments, up to GBP 118M per target in downstream milestones, and tiered low-single-digit royalties on future product sales. GSK holds the option to license the validated targets and would lead development.

| Term | Detail |

|---|---|

| Licensor / originator | Engitix Ltd. (London; privately held; ECM-driven drug discovery) |

| Licensee / partner | GSK (LSE / NYSE: GSK; Kaivan Khavandi, SVP, R&D) |

| Structure | Research collaboration and option agreement; GSK option to license targets, datasets, and assays; GSK leads development |

| Platform / focus | Human ECM platform and multi-omics datasets; liver fibrosis regression (resolution) rather than progression |

| Economics | Up to GBP 44.5M upfront and near-term; up to GBP 118M per target in milestones; tiered low-single-digit royalties to Engitix |

| Date | Mon June 8, 2026 |

| Royalty read | |

|---|---|

| Tradable instrument | Tiered low-single-digit royalty to Engitix on net sales of any product GSK takes forward |

| Stacked on | Per-target milestone ladders (up to GBP 118M each) and the GBP 44.5M upfront and near-term band |

| Structure | The earliest-stage royalty in the cut: platform- and target-discovery driven, contingent on GSK exercising its option and carrying targets through development; a long-dated, multi-step option |

| Read | An origination watch item; the trigger to elevate is GSK exercising its option on a defined target |

| Caveat | Private originator, several validated-target and development steps from product sales; the GBP 118M figure is per target, not aggregate |

AmMax Bio / Lonza: ADC Linker-Payload Platform License, Terms Undisclosed (Tue June 9)

AmMax Bio, Inc. (Redwood City, CA; private, clinical-stage) entered a non-exclusive licensing agreement with Lonza (SIX: LONN; Basel) for access to Lonza's GlycoConnect conjugation, HydraSpace spacer, and exatecan-based SYNtecan linker-payload technologies, to develop AMB-104, an ADC for venetoclax / azacitidine-resistant AML (Contract Pharma).

Financial terms were not disclosed. AmMax plans an IND in early 2027. The structure mirrors Lonza's Stipple Bio ADC platform license one week earlier (June 4), which disclosed upfront, milestone, and net-sales royalty terms to Lonza.

| Term | Detail |

|---|---|

| Licensee | AmMax Bio, Inc. (Redwood City, CA; private, clinical-stage; Chairman and CEO Larry Hsu) |

| Licensor / originator | Lonza (SIX: LONN; Basel; CDMO; conjugation and linker-payload platform owner) |

| Asset | AMB-104: ADC combining AmMax's monoclonal antibody with Lonza's linker-payload technologies; venetoclax / azacitidine-resistant AML; IND targeted early 2027 |

| Structure | Non-exclusive platform license (GlycoConnect, HydraSpace, SYNtecan); Lonza manufactures proprietary-technology components |

| Economics | Terms undisclosed; Lonza's June 4 Stipple Bio license disclosed upfront, milestones, and net-sales royalties to Lonza |

| Date | Tue June 9, 2026 |

| Royalty read | |

|---|---|

| Tradable instrument | A net-sales royalty to Lonza, inferred from the Stipple Bio comparator (not disclosed for AMB-104) |

| Model | Lonza's ADC platform-licensing originates a CDMO platform royalty: a stream on the licensee's product sales in exchange for access to its conjugation and linker-payload IP |

| Read | A Basel-origin platform royalty held by a large listed CDMO; two licenses in one week (Stipple June 4, AmMax June 9) point to a repeatable, poolable royalty book |

| Caveat | AmMax terms undisclosed, the asset preclinical (IND 2027); the royalty is inferred from the comparator and Lonza's stated model, not from disclosed AMB-104 terms |

Structured Finance and Non-Dilutive Debt

Two structured-finance prints in the window. The Pharmakon Advisors / Idorsia senior secured term loan of up to CHF 250M is debt rather than a royalty monetisation, the one in-window deal from a house on the structured-finance watchlist and a Swiss commercial-stage borrower. The Beren Therapeutics / Hercules Capital financing of about $300M is the more royalty-relevant of the two: alongside $135M of equity, the Hercules tranche pairs senior secured debt with a $55M royalty-financing sleeve on a pre-commercial rare-disease asset, the window's only explicit royalty layer.

Pharmakon Advisors (BioPharma Credit) / Idorsia: Senior Secured Term Loan, Up to CHF 250M (Tue June 9)

Idorsia Ltd (SIX: IDIA; Allschwil, Switzerland; commercial-stage, lead product QUVIVIQ / daridorexant) entered a senior secured term loan of up to CHF 250M with funds managed by Pharmakon Advisors, LP, the manager of the BioPharma Credit funds (Idorsia release).

The first tranche of CHF 150M funds at closing to fully refinance the existing New Money Facility (CHF 105M drawn, due May 2027), extending runway into 2028. The loan carries a 5-year maturity at a fixed 7% rate.

| Term | Detail |

|---|---|

| Lender | Pharmakon Advisors, LP (manager of the BioPharma Credit funds; ~$13B committed across 77 investments since 2009) |

| Borrower | Idorsia Ltd (SIX: IDIA; Allschwil, Switzerland; Chairman and interim CEO Jean-Paul Clozel) |

| Instrument | Senior secured term loan, up to CHF 250M; first tranche CHF 150M at closing; further tranches subject to conditions |

| Pricing / tenor | Fixed 7% interest rate; 5-year maturity |

| Use of proceeds | Refinance the existing New Money Facility; eliminate near-term maturities; extend runway into 2028 |

| Date | Tue June 9, 2026 |

| Royalty read | |

|---|---|

| Instrument | Non-dilutive senior secured debt against Idorsia's commercial base; not a royalty purchase or synthetic royalty |

| Why logged | Pharmakon (BioPharma Credit) is on the structured-finance watchlist; this is the one such print in the window and a live pricing data point (fixed 7%, 5-year) for senior secured life-sciences debt against a single commercial franchise |

| Read | A Swiss commercial-stage borrower with both a debt and a royalty-monetisation path took the debt route |

| Caveat | This is the credit product, not royalty paper, and should not be counted as royalty originated or traded; only CHF 150M of the CHF 250M is funded at closing |

Beren Therapeutics / Hercules Capital: $300M Equity and Royalty-Backed Financing for Adrabetadex (Wed June 10)

Beren Therapeutics P.B.C. (Thousand Oaks, CA; founder-led, CEO Jason Camm; parent of Mandos LLC) secured about $300M in combined financing to fund commercial readiness for adrabetadex, its cyclodextrin therapy for infantile-onset Niemann-Pick disease type C (I-NPC), ahead of a November 17, 2026 PDUFA target action date (Business Wire).