Insuring the Royalty Stream: Wraps, Surety, Contingent Risk, and the CLO Question in 2026

Insurance once sat at the center of pharmaceutical royalty finance. The two foundational securitizations of the asset class both relied on a third-party guarantor standing behind the notes: BioPharma Royalty Trust I in 2000 and Royalty Pharma Finance Trust in 2003.

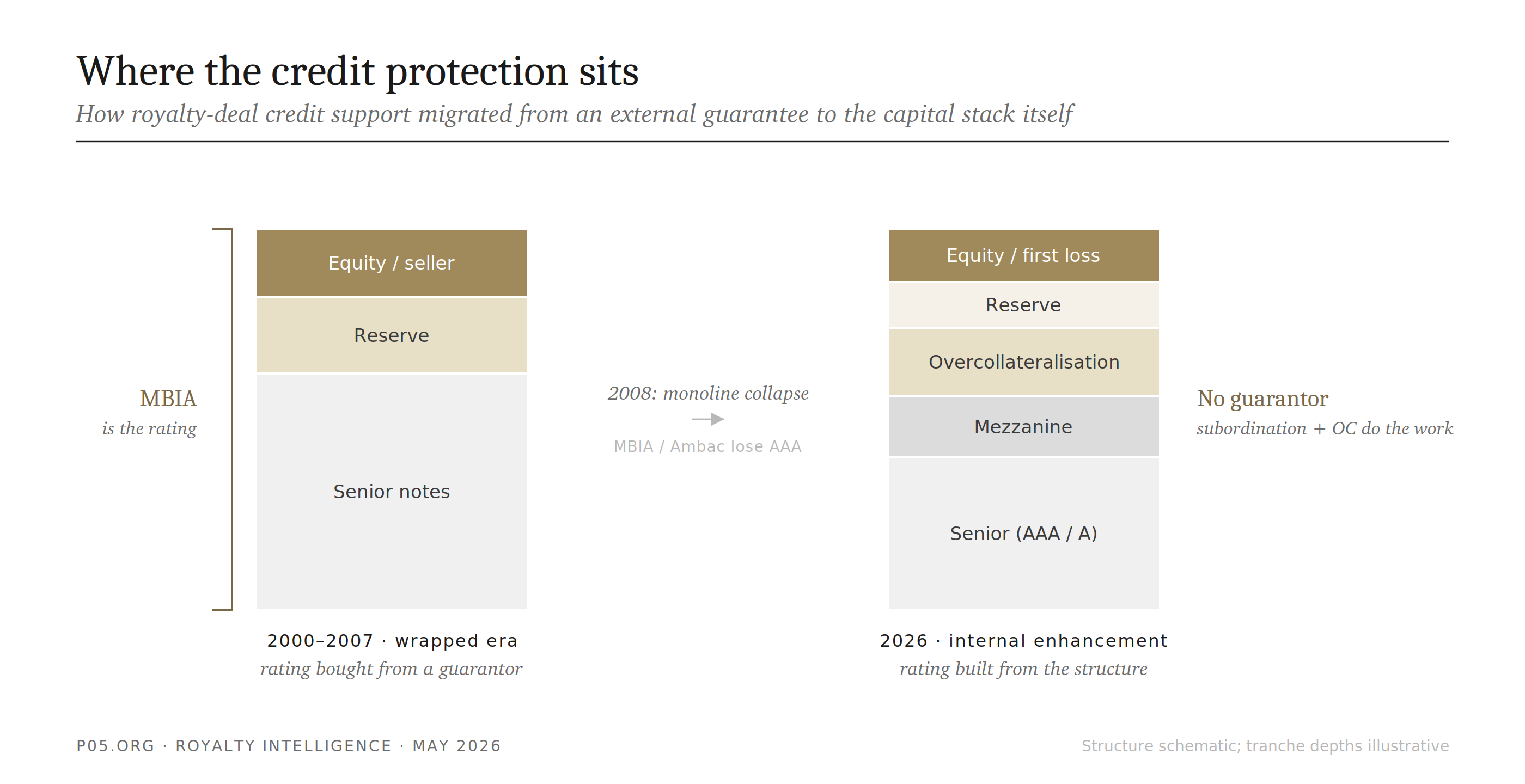

In the 2003 deal, the guarantor was the rating. A 13-asset revolving pool reached AAA/Aaa, not because the underlying drug royalties were AAA, but because MBIA wrapped the senior notes.

That model is gone. The monoline guarantors that wrote those wraps were destroyed in 2008. Nothing has replaced them at the same point in the structure.

The question for 2026 is narrower and more practical:

- With the monoline wrap extinct, what insurance, if any, still protects a royalty stream?

- How is a single stream insured differently from a pool of many? Does the answer change when the pool spans pharma, vaccines, medtech, and animal health rather than one therapeutic area?

- What does the protection cost?

- And the question that has displaced all of these for the largest holders: with the insurer now more often the funder of royalty deals than the guarantor of them, and with the NAIC rewriting the capital rules for CLOs and structured credit, does insurance-as-protection still matter to a royalty fund at all?

This piece is written for counsel and royalty fund principals who have seen the word "wrap" in a 2003-vintage offering circular and want to know what survives.

What the wrap actually did, and why it died

A monoline financial guaranty was an unconditional and irrevocable guarantee of timely payment of principal and interest. In a royalty securitization, it worked as a substitution of credit. The noteholder stopped analyzing the drug, the patent, and the licensee, and analyzed the guarantor instead.

If the assigned royalty cash flow fell short, the guarantor paid on schedule and took an assignment of the claim. The bonds carried the guarantor's rating, not the collateral's.

This is why the 2003 Royalty Pharma Finance Trust could print at AAA on a pool that, unwrapped, would have cleared several notches lower. The diversification across thirteen assets helped, but the rating uplift came from MBIA.

The migration that destroyed the product was the guarantors' move out of municipal finance and into structured credit. By 2007, combined non-public-finance insured exposures ran from 30% to over 80% of monoline portfolios. When the subprime losses hit, MBIA and Ambac had lost their triple-A ratings from all three agencies by June 2008.

A wrap is only as good as the wrapper's rating. Once the guarantor was downgraded, every insured bond faced downgrade pressure at once, and the product's reason for existing collapsed. Ambac entered a court-ordered restructuring; MBIA split its books. The AAA financial-guaranty wrap has not returned to structured finance.

What replaced it was not another external guarantee. It was the capital stack itself. Where the 2003 deal bought a wrap to convert a pool into AAA, the modern deal builds a junior tranche and an overcollateralization buffer, so that the senior class is protected by the assets.

The mezzanine cousin of the wrap had already shown its limits before 2008.

BioPharma Royalty Trust I, the 2000 securitization of Yale's Zerit royalty, was a single-asset, single-licensee, single-patent structure. A surety from ZC Specialty Insurance (a Centre Re subsidiary) covered the mezzanine.

Then Bristol-Myers Squibb discounted Zerit inventory in late 2001, as the drug lost ground to newer HIV therapies. Royalty receipts collapsed. The cash flow covenants broke within eighteen months, and the surety absorbed the shortfall.

The lesson the market drew was not that surety works. It was that a single-asset securitization is fragile enough that the surety gets called, which is exactly the outcome an insurer prices to avoid. The surety paid, but the product did not recur.

What insurance touches a royalty deal in 2026

The wrap is gone, but insurance has not left the asset class. It has moved to the edges of the transaction, covering discrete risks rather than guaranteeing the cash flow as a whole.

Four products are live in 2026. None is a substitute for the monoline wrap.

| Product | What it covers | What it does not cover | Live in 2026? |

|---|---|---|---|

| Reps & warranties (RWI) | Accuracy of the seller's representations in a royalty purchase | Commercial performance of the royalty | Yes, mature and competitive |

| Contingent / litigation risk | One identified, binary legal or tax outcome (e.g. a patent challenge) | General sales or LoE decline | Yes, but contracted post-2024 |

| IP infringement / patent monetization | Defense or enforcement of the patent; a monetization floor | The royalty cash flow itself | Yes, IP-campaign focused |

| Trade credit / political risk | Counterparty non-payment, FX inconvertibility, expropriation | Asset performance | Yes, scales with geography |

| Monoline wrap | The whole cash flow, as a guarantee | n/a | No, extinct since 2008 |

Representations and warranties insurance is the most mature of the four. When a royalty interest changes hands in an M&A-style transaction, the buyer can place an RWI policy over the seller's representations. Carriers have explicitly extended appetite into the asset class: WTW lists "pharmacological royalty streams" among the businesses RWI carriers will cover.

What it covers is the accuracy of what the seller said, not the performance of the asset. And the standard policy excludes known regulatory violations, which makes pre-closing diligence on FDA history and IP disputes both a coverage condition and a deal-risk question.

Contingent risk insurance is the closest the market comes to underwriting an outcome. Lockton frames it as cover for low-probability, high-severity events identified in diligence, where an insurer can underwrite the likelihood using legal analysis.

The market contracted sharply after a single large loss. Liberty Mutual took a hit on a policy covering part of a $1.6 billion judgment against IBM: insurers had covered between $500 million and $750 million of an award that was then overturned on appeal.

The response was swift. Some carriers stopped writing contingent risk altogether, others dropped judgment preservation insurance specifically, and the survivors curtailed limits and raised premiums. Carriers pivoted to portfolios, which offer many paths to a settlement rather than a single binary bet.

The same dynamic that killed the single-asset wrap, correlated exposure on one outcome, is what underwriters now avoid. The product that has emerged in its place is patent monetization insurance, which sets a floor value on a patent portfolio. CAC Specialty placed its first such structure in 2023. But the application is still to litigation-driven IP campaigns, not commercial product royalties.

Reinsurance is present, but not where the wrap was. Carriers writing the edge products cede portions to reinsurers in the ordinary course, so a reinsurer takes a share of a representation-breach or patent-litigation risk that sits over a royalty deal.

More consequentially, life reinsurers are buyers of the rated paper a royalty securitization produces. The Bermuda platforms with over $1.5 trillion in AUM access it through the rated-feeder structure.

But there the insurer is the investor in the royalty bond, not the guarantor of it. That distinction is the entire story of why the wrap has not returned.

Insuring one stream versus insuring many

The single most important structural fact about royalty insurance: a single stream and a pool of streams are insured by completely different mechanisms. The difference is the same one that killed the wrap.

A single royalty stream is a concentrated, binary risk. The drug either holds share or loses it. The patent either survives challenge or does not. The licensee either pays or disputes.

An insurer asked to stand behind that one cash flow is writing a position with no diversification and a fat tail. This is the BioPharma Trust I and Liberty/IBM profile.

So the only insurance that attaches cleanly to a single stream is the edge cover above: a representations policy on the acquisition, a contingent-risk policy ring-fencing one patent dispute, IP cover funding the litigation. None guarantees the stream. They carve off a named, underwritable slice and leave the commercial performance with the holder.

A pool of streams is different. It is insured, in practice, by its own internal structure rather than by an external policy.

The clearest example is the DRI Capital Drug Royalty III LP 1 master trust, the one royalty securitization that has continued issuing BBB-rated paper through the post-2008 vintage. It reaches its ratings through a tranched structure (4.94% on the AAA class down to 6.78% on the B1 notes in 2017-1), 36-52% overcollateralization, and a six-month interest reserve. The tools are subordination, overcollateralization, excess spread, and senior-subordinate tranching, used in place of a guarantee.

The cost of the wrap is replaced by the cost of the subordinate capital. Diversification does the work the guarantor's balance sheet used to do.

| Single stream | Pool of streams | |

|---|---|---|

| Risk shape | Concentrated, binary, fat tail | Diversified, averaged |

| How protected | Edge cover on named slices only | Internal subordination + OC |

| Who bears first loss | The holder | Equity / first-loss tranche |

| External party needed | An insurer, per named risk | None |

| Cost form | One-time premium per policy | Spread on subordinate capital |

For a single stream, insurance protects identified slices and nothing more. For a pool, it is not insurance that protects the senior holder. It is structural subordination, and the more diversified the pool, the less external support it needs.

The cross-vertical pool: pharma, vaccines, medtech, animal health

The diversification logic sharpens when the pool spans the healthcare continuum rather than sitting inside one therapeutic area. This is where the insurability question becomes genuinely different from the classic single-drug securitization.

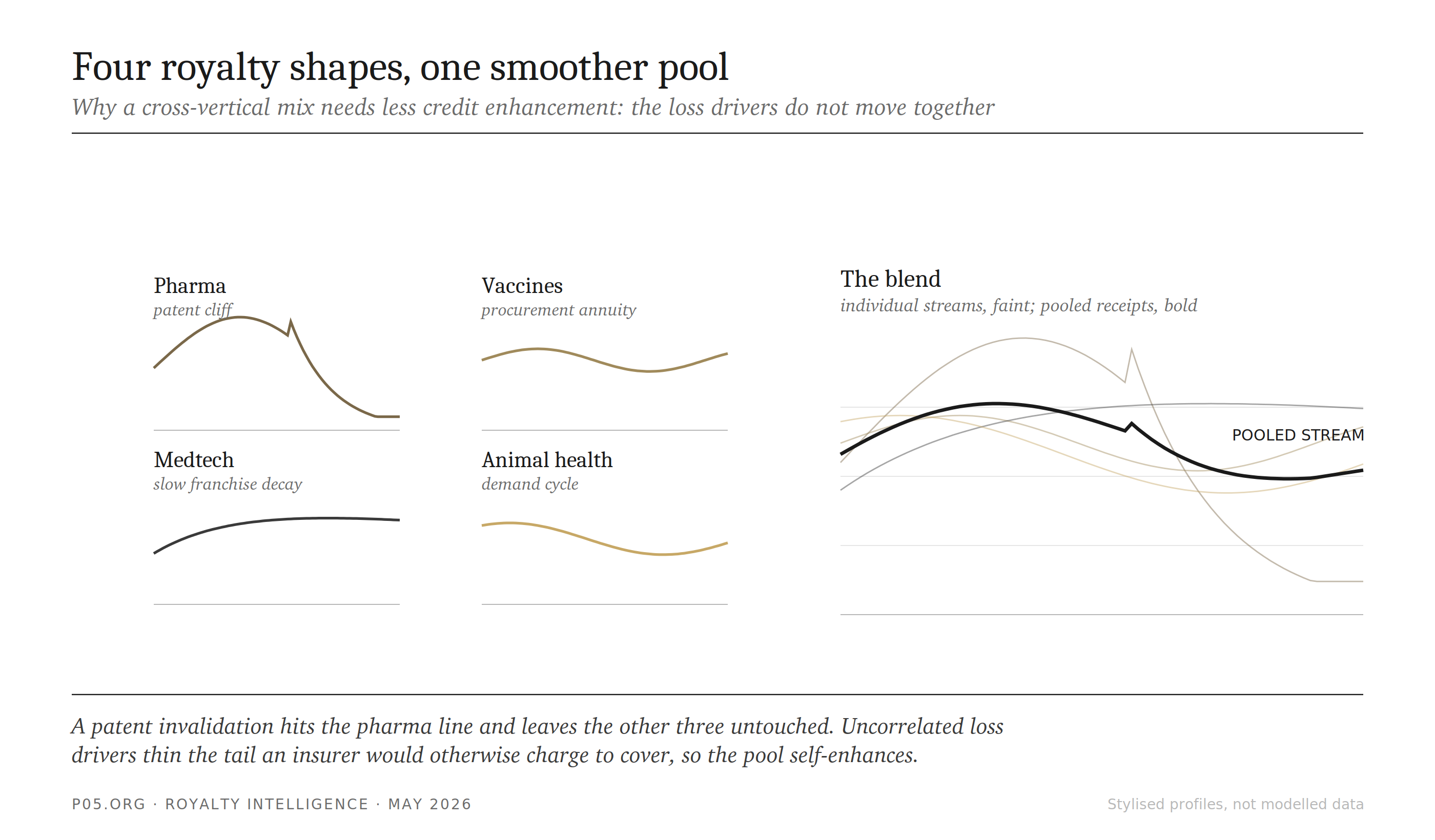

The four verticals carry structurally different risk shapes:

- Pharma. A small-molecule royalty is dominated by patent cliff and loss-of-exclusivity timing: strong, then a defined edge.

- Vaccines. Behaves like an annuity, with procurement and recommendation risk rather than a sharp cliff.

- Medtech. Rests on a device franchise. Iterative improvement and the regulatory moat around a 510(k) or PMA pathway extend the effective life past any single patent, so decay is gradual.

- Animal health. Depends on companion-animal and livestock demand cycles, largely uncorrelated with human-pharma reimbursement politics, IRA price negotiation, or human biosimilar entry.

These are real, monetizable streams, not hypotheticals. Elanco monetized certain US lotilaner royalties and milestones for $295 million in May 2025, running through 2033. It was required under GAAP to keep recognizing the royalty as revenue, because the structure was a financing rather than a true sale.

On the same product, HealthCare Royalty financed TheracosBio's future royalties and milestones on the veterinary version commercialized by Elanco. More broadly, PwC notes that pharmaceutical, biotech, medical-device and other life-sciences companies are all increasingly monetizing royalty and revenue streams.

The universe of originatable streams across the four verticals is wide. What is thin is the population of buyers that look outside human therapeutics.

From an insurance and rating standpoint, the cross-vertical pool is the strongest possible case for the internal-enhancement model, and the weakest for an external wrap. The whole point of mixing the four is that their loss drivers are uncorrelated.

A patent invalidation hits the pharma line and leaves the animal-health line untouched. An IRA price-negotiation selection hits a human drug and is irrelevant to a livestock vaccine. Correlation is the enemy of any pooled credit structure, and a cross-vertical pool is engineered to minimize it.

The consequence: a well-constructed cross-vertical pool needs less credit enhancement per dollar of senior notes than a single-vertical pool of the same size, because the diversification itself is the enhancement.

There is a real challenge that cuts the other way, and counsel should not gloss it. The rating agencies and any insurer pricing edge cover have decades of data on small-molecule pharma royalties, and comparatively little on bundled medtech, vaccine, and animal-health streams.

Thin data widens the confidence interval. A wider confidence interval raises both the subordination a rating agency demands and the premium an edge insurer charges. So part of the diversification benefit is offset, until a cross-vertical pool has a track record, by a data-scarcity premium. The structure is sound; the pricing of it in 2026 reflects that the market has not yet seen many of them.

What the protection costs

Pricing is where the abstract question of whether to insure becomes a concrete decision. The numbers explain why edge cover is used selectively rather than universally.

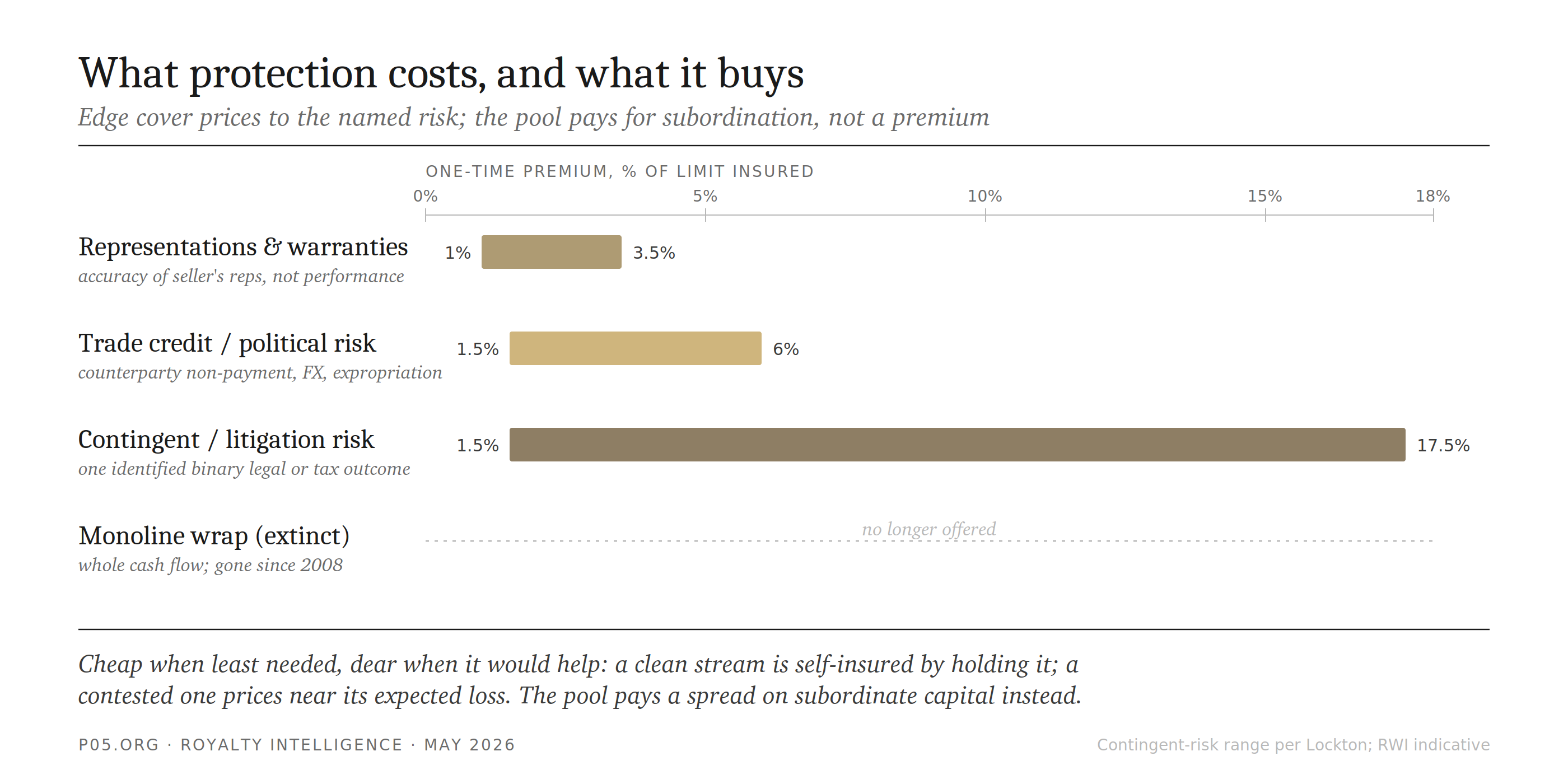

Contingent and litigation risk insurance is the product closest to insuring a specific royalty risk. It prices from roughly 1.5% to 17.5% of the limit insured, as a one-time premium rather than an annual rate.

Where a deal sits in that range turns almost entirely on the insurer's read of the probability. A strong favorable first-instance judgment on appeal prices near the bottom. A genuinely uncertain binary outcome prices toward the top, if a carrier will write it at all. After the Liberty/IBM loss, the market repriced upward and limits shrank.

Representations and warranties insurance is cheaper, because it covers the narrowest risk, typically in the low single digits of the limit.

For a royalty fund, the decision rule is a straightforward expected-value comparison. It usually comes out against buying performance cover.

A clean, approved, multi-year-runway royalty has an expected loss low enough that almost any premium is uneconomic. The fund self-insures by holding the position.

A short-runway asset facing a Paragraph IV challenge is the opposite. The expected loss is high enough that an insurer either declines, or prices the premium close to the expected payout. Either way, the fund ends up paying away exactly the spread it was being compensated to earn.

So edge cover gets bought when it unlocks something else: a representations policy that lets a deal close without an escrow, a contingent-risk policy that lets a fund return capital to LPs while a dispute resolves. It is rarely bought as standing protection on the cash flow.

For a pooled vehicle, the relevant cost is not a premium at all. It is the spread between the rated senior tranche and the un-rated equity, plus the opportunity cost of overcollateralization. That cost is paid to the markets and the equity holder, not to an insurer.

The CLO question: why capital rules now matter more than coverage

The development that has displaced insurance-as-protection from the center of royalty-fund economics is not in the insurance market at all. It is in the capital treatment of the insurers and reinsurers who are now the dominant buyers of, and increasingly the funders behind, royalty paper.

The CLO angle is the right lens. What the NAIC is doing to CLOs is the template for what it is doing to all structured credit, including any royalty ABS.

Start with where the capital comes from. The largest royalty and asset-based-finance platforms are now wired directly into insurance balance sheets: KKR acquired Global Atlantic; Apollo built Athene; Blackstone holds Everlake; Brookfield holds American National.

The scale is large and growing. Insurance-linked capital platforms deployed an estimated $180 billion into private credit in 2025, up from $120 billion in 2023. The structural advantage is duration: S&P observed that insurance-backed lenders' spread requirements run 75 to 150 basis points below PE-backed direct lenders for comparable credit quality.

In other words, the royalty fund's cheapest capital increasingly is insurance capital, deployed as an investor and lender, not pledged as a guarantor.

That makes the capital charge on the insurer's holding the binding variable. And the NAIC is tightening it.

| Reform | Status | Effect on royalty structures |

|---|---|---|

| 45% RBC charge on residual (equity) tranches | Adopted 2024, still in place | Penalizes the first-loss layer that protects a pool |

| CLOs moved out of filing-exempt to NAIC modeling | Loss model expected 2026 | Template for all structured securities, incl. royalty ABS |

| VOSTF restructured to Invested Assets (E) Task Force | Effective 1 Jan 2026 | Commissioner-level scrutiny of bespoke products |

| Separate CLO debt / collateral-loan charges | Advanced at Spring 2026 NAIC, San Diego | Comment periods extended, direction set |

Sources: Clifford Chance, InsuranceAUM, Dechert.

The implication runs in two directions.

First, it makes a revived wrap-and-securitize model even less likely. A single-asset or thinly diversified royalty ABS, even rated BBB, faces a higher post-2026 capital charge in an insurer's hands than a comparably rated investment-grade corporate. The regime now penalizes opacity and bespoke structure independent of the rating. For the marginal insurance buyer, that differential makes the plain corporate bond of a royalty fund a better risk-adjusted holding than the rated tranche of a royalty securitization.

Second, it raises the cost of the equity tranche that provides the internal credit protection in a pooled structure. If the natural holder of the first-loss piece is an insurer, and that piece carries a 45% capital charge, the insurer demands a higher return to hold it. That raises the all-in cost of the subordination that protects the senior notes.

One nuance runs the other way, and it explains why insurers keep buying royalty-adjacent private credit despite the tightening. The illiquidity and complexity of private credit does not, in itself, attract an additional NAIC capital charge the way it does under some rating-agency models. So an insurer holding rated royalty-backed debt can capture an illiquidity premium without a capital penalty.

But that advantage attaches to holding rated debt, not to guaranteeing the stream. And it does not survive the residual-tranche and modeling changes at the layers where credit protection sits.

Does any of this still matter to a royalty fund? Mostly not, and that is the point

For the large, consolidated royalty platforms that dominate the asset class in 2026, insurance-as-protection on the royalty stream is close to irrelevant. The reasons are structural, not cyclical.

Start with consolidation. The sector has narrowed into a small number of investment-grade or insurance-backed platforms. KKR controls HealthCare Royalty through its asset-based-finance franchise; the April 2026 Ligand-XOMA merger consolidated the public-equity aggregators. Royalty Pharma funds itself in the investment-grade corporate market at an all-in cost of debt in the 4-6% range.

A fund that can borrow that cheaply has no use for a wrap. It can issue unsecured corporate debt at 4-6% against a Baa2/BBB- rating, or sit on an insurer's balance sheet borrowing at a 75-150 bp discount to PE-backed lenders.

Its diversified portfolio is its credit enhancement. Its rating is its access. Its scale is what lets isolated losses be absorbed. XOMA's $30.9 million of 2024 credit losses on three positions hit earnings without threatening the platform. That is self-insurance through diversification, and it is cheaper than any premium, because the diversification is also the source of return.

Then there is the investor base. It has grown sophisticated enough to price royalty risk directly, rather than relying on a guarantor's rating as a substitute for analysis.

The whole function of the monoline wrap was to let a real-money buyer avoid underwriting the drug, the patent, and the licensee. But the buyers who matter today do exactly that underwriting as their core competence: the royalty funds, the ABF desks at KKR and Blackstone, the insurance-backed lenders. They do not want to pay a guarantor to substitute its judgment for theirs. The judgment is the edge.

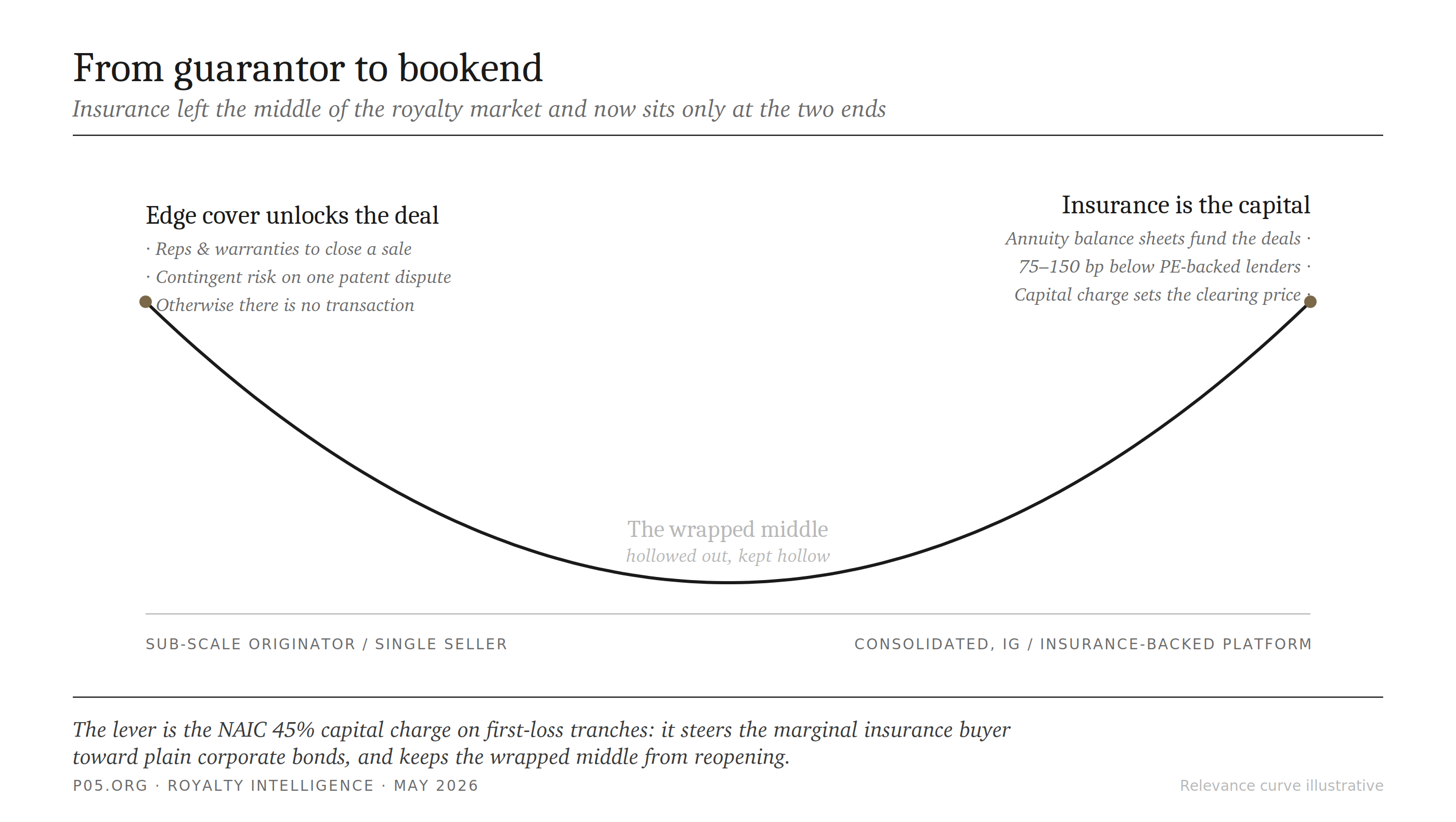

Where insurance does still matter is at the two ends of the size spectrum.

At the small end, a sub-scale originator or single seller who cannot reach an investment-grade rating, and cannot tap a corporate market, will still use edge cover. For that party, the alternative is no deal.

At the large end, insurance matters not as protection on the stream, but as the balance sheet funding the deals, and as the regulated buyer whose capital charges set the clearing price for the whole structure.

The middle, where the classic wrapped securitization used to live, has been hollowed out. The capital rules are keeping it hollow.

Conclusion: the protection moved, the guarantee did not return

Insurance was central to pharmaceutical royalty finance when the asset class began. It is peripheral now.

The AAA monoline wrap that made the 2003 Royalty Pharma Finance Trust possible was destroyed in 2008 and has not returned. The product depended on a thinly capitalized guarantor maintaining a rating it could not hold once its structured-finance book turned.

What survives is a set of edge products: representations and warranties insurance over royalty acquisitions, contingent-risk and patent-monetization cover on identified legal exposures, and trade credit and political risk on cross-border counterparties. None of them guarantees the cash flow as a whole.

A single stream can be insured only at these edges, slice by named slice. A pool is protected by its own internal subordination and overcollateralization. A cross-vertical pool spanning pharma, vaccines, medtech, and animal health is the strongest version of that logic, because uncorrelated loss drivers thin the tail that an insurer would otherwise charge to cover.

The development that matters most is not in the insurance market. It is in the capital rules governing the insurers who now fund and buy royalty paper. The NAIC's CLO and structured-credit reforms raise the cost of the first-loss capital that protects a royalty pool, and steer the marginal insurance buyer toward plain corporate bonds over rated royalty ABS.

For the consolidated, investment-grade, increasingly insurance-backed platforms that dominate the sector, insurance-as-protection on the stream is close to irrelevant. Diversification is the enhancement. The rating is the access. The balance sheet is the point.

Insurance still matters at the small end, where edge cover unlocks a deal that could not otherwise close, and at the large end, where insurance capital is the funding and the capital charge is the clearing price. The wrapped middle, where the story began, is gone. The economics that emptied it are more entrenched in 2026 than they were when the monolines failed.

All information in this report was accurate as of the research date and is derived from publicly available sources including court opinions, regulatory guidance, academic literature, SEC filings, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.